im matterley undervalued assets fund outlook for 2013 · pdf fileim matterley undervalued...

TRANSCRIPT

IM Matterley Undervalued Assets Fund

Outlook for 2013

Review of 2012

Retained Cash Flow

Asset Allocation

US

Europe

Banks

Portfolio Attribution

Outlook 2013

How Are We Positioned for the Year Ahead?

Conclusion

Valuation Matrix

Review of 2012

The Fund rose by 23.6% while the market rose by 12.3%. As we look back at our outlook

document for 2012 our standpoint at the time could be summarised as follows:

The value case was well supported on both earnings and asset metrics. Based on

retained earnings, it was our view that the equity market was displaying similar

valuation to the depths of March 2009 and we expand on this later in the document.

We also felt that equities, in a low interest rate environment, would continue to

prove themselves as a provider of an attractive and rising income stream. Asset

allocation would as a result have to be a little more measured having been so

heavily skewed to bonds.

We remained optimistic about improving economic data from the US, in no small

part assisted by ongoing house price rises. We were not optimistic about Europe

but we saw the Long Term Refinancing Operation as a valuable first step by the

European Central Bank in acting as a central bank should in times of crisis.

Ultimately, however, the extent of our hope was that a moderation of bad news

would prove to be powerful to sentiment.

At a sector level, a material change of view was articulated in the banking sector

owing to strong cash generation and our belief that, in many instances, equity

holders in the sector had become superior to bond holders owing to the advent of

contingent convertible bonds.

Finally, while we acknowledged there was little visibility, our confidence in the

ability of the portfolio to make good progress was based upon the fact that it was

the cheapest it had been at the outset of any year since its inception.

Taking each of the above in turn, the comment that has raised most suspicion is that we

have felt that at times this year the equity market was displaying similar value to the

trough of March 2009. Below we illustrate a simple cash flow bridge based upon rights

issue activity and retained earnings since the start of 2009. If the running tally of close to

1500 index points is added to the starting level of the FTSE in 2009 of 4434, then it would

appear we are on almost absolute parity as we start 2013.

FTSE 100 Retained Earnings and Rights Issues in Index Points (2009-2013e)

Rights Issue Activity in Index Points

Retained Earnings in Index Points

Source: Matterley

While this can only ever be a guide to the value of the FTSE 100, given constituent change,

the point we are keen to make is that the floor is rising rapidly. This was first and foremost

the result of significant rights issue activity. Subsequently, retained earnings have taken

up the baton given that dividend payout ratios remain low in the context of history.

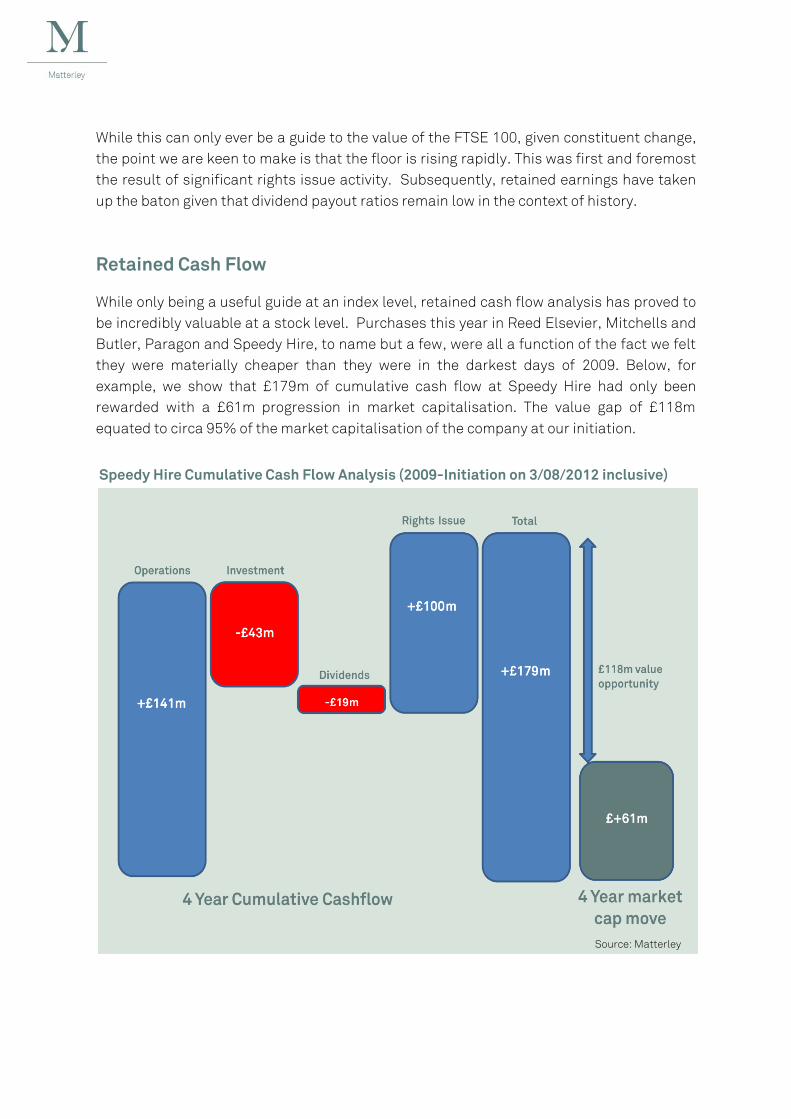

Retained Cash Flow

While only being a useful guide at an index level, retained cash flow analysis has proved to

be incredibly valuable at a stock level. Purchases this year in Reed Elsevier, Mitchells and

Butler, Paragon and Speedy Hire, to name but a few, were all a function of the fact we felt

they were materially cheaper than they were in the darkest days of 2009. Below, for

example, we show that £179m of cumulative cash flow at Speedy Hire had only been

rewarded with a £61m progression in market capitalisation. The value gap of £118m

equated to circa 95% of the market capitalisation of the company at our initiation.

Speedy Hire Cumulative Cash Flow Analysis (2009-Initiation on 3/08/2012 inclusive)

Source: Matterley

This cash generation, combined with low payout ratios, is allowing companies ample

opportunity in which to grow their dividends from a low base. Despite the fact that more

modest growth is forecast going forward, next year is still set to be a record dividend

distribution from the market.

Asset Allocation

It is therefore surprising to us that the retail buying patterns still favour bonds so heavily

and the source of cash, more often than not on a monthly basis, is UK equities.

Date Best Selling Net Retail Worst Selling Net Retail

Oct-12 Global Emerging Markets UK All Companies

Sep-12 Absolute Return – UK UK All Companies

Aug-12 £Strategic Bond UK All Companies

July -12 £ Corporate Bond Europe Excluding UK

June-12 £ Corporate Bond UK All Companies

May-12 £ Corporate Bond Europe Excluding UK

Apr-12 £ Corporate Bond Europe Excluding UK

Mar-12 £ Strategic Bond UK All Companies

Feb-12 £ Corporate Bond UK All Companies

Jan-12 £ Corporate Bond UK All Companies

Dec-11 £ Corporate Bond Europe Excluding UK

Nov-11 Mixed Investment 20-60% Shares Specialist

Oct-11 £ Strategic Bond UK All Companies

Source: Investment Management Association. Note: As of 01/01/2012 the Cautious Managed Sector has been re-named as

“Mixed Investment 20-60% Shares”.

The UK Equity market has also been falling out of favour with institutional investors in

recent years. Today, for example, UK pension funds allocate only 18% of their £1.5trn

worth to UK Equities.

Some of the reasons for this change are of course healthy, such as the development of

overseas equity markets. Others, however, are unhealthy in our view, namely the

extremely low bond yields we are experiencing as a result of Quantitative Easing, which is

causing material rises in the present value of pension liabilities. The response from

pension trustees to this move seems to be further investment in bonds to asset match

their liabilities to the best of their abilities in order to limit any further damage. From an

operating perspective, pension accounting rules also require companies to make

additional payments to plug the deficit which is diverting capital away from investment.

The government has already recognised the need to encourage corporates to spend their

accumulated cash reserves, but further to this a consultation process has been put

together to discuss whether current discount rates are appropriate. Any upward revision

of the allowable discount rate, be it using average gilt yields over a longer time frame for

example, would be good for investment and, as a result, economic growth. Ultimately, of

course it would be extremely good for equities, and it is difficult to envisage a scenario

whereby they remain as unpopular as they have been over the last year.

US

Source: Matterley

%

Percentage of UK pension funds allocated in UK Equities (1967-2011)

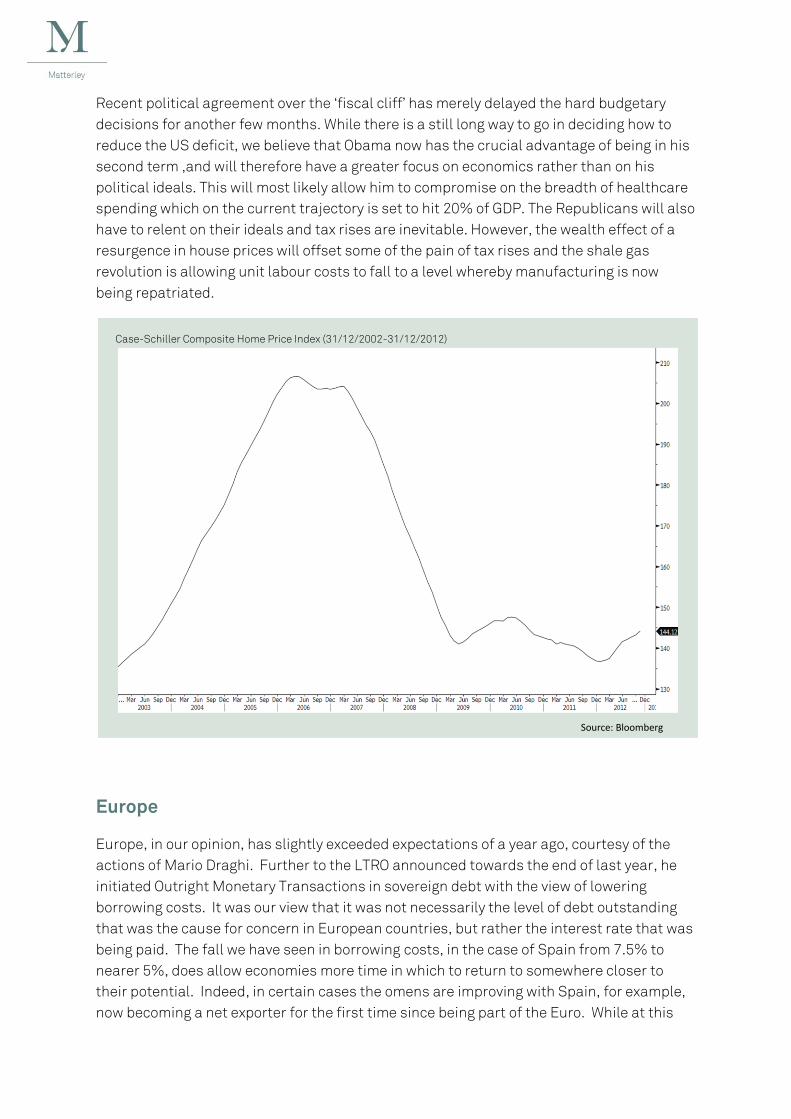

Recent political agreement over the ‘fiscal cliff’ has merely delayed the hard budgetary

decisions for another few months. While there is a still long way to go in deciding how to

reduce the US deficit, we believe that Obama now has the crucial advantage of being in his

second term ,and will therefore have a greater focus on economics rather than on his

political ideals. This will most likely allow him to compromise on the breadth of healthcare

spending which on the current trajectory is set to hit 20% of GDP. The Republicans will also

have to relent on their ideals and tax rises are inevitable. However, the wealth effect of a

resurgence in house prices will offset some of the pain of tax rises and the shale gas

revolution is allowing unit labour costs to fall to a level whereby manufacturing is now

being repatriated.

Europe

Europe, in our opinion, has slightly exceeded expectations of a year ago, courtesy of the

actions of Mario Draghi. Further to the LTRO announced towards the end of last year, he

initiated Outright Monetary Transactions in sovereign debt with the view of lowering

borrowing costs. It was our view that it was not necessarily the level of debt outstanding

that was the cause for concern in European countries, but rather the interest rate that was

being paid. The fall we have seen in borrowing costs, in the case of Spain from 7.5% to

nearer 5%, does allow economies more time in which to return to somewhere closer to

their potential. Indeed, in certain cases the omens are improving with Spain, for example,

now becoming a net exporter for the first time since being part of the Euro. While at this

Case-Schiller Composite Home Price Index (31/12/2002-31/12/2012)

Source: Bloomberg

stage we only whisper it cautiously we could not rule out the Eurozone being a source of

positive surprise in the year ahead relative to depressed expectations.

Banks

The banking sector has enjoyed a good run this year as satisfactory asset quality has

resulted in strong cash flow. This has caused gearing levels to fall closer to those of their

US counterparts and has given investors more confidence in book values.

Also, as mentioned a year ago we felt that equity investors in certain names in the

domestic sector were assuming unique territory in that they had assumed the status of

ranking superior to bond holders. Lloyds for example have £9.2bn of capital with

professional investors which will convert to equity at 59 p (over 100% above the share price

at the start of the year) in the event their Tier 1 Ratio breaches 5%. Barclays however in

recent months seems to have gone one better by issuing $3bn Contingent capital bonds.

The contingency is that if their Tier 1 Capital Ratio breaches 7% then the bondholders of

this instrument lose the right to both the coupon payments as well as the principal, and

there is no conversion into the equity. This is an extraordinary state of affairs, and it is not

immediately clear to us why people would buy such a bond. The upshot for equity holders,

however, is that the cost of capital is falling materially. While returns on equity may

struggle to get meaningfully above 10% it is still a level in our view that can justify a price

Pe

rce

nta

ge

Net Exports of Spanish Goods and Services as a Percentage of GDP (1995-2012)

Source: Eurostat

target above book value. In the case of Barclays this would still suggest a price target 50%

above the current level.

Portfolio Attribution

At the outset of last year the portfolio was the cheapest it has been since its inception and

this gave us great deal of confidence in its ability to make good progress during the year.

Pleasingly, almost all sectors have positively contributed but the one slight frustration is

financials. While good money was made in absolute terms it has been a slight relative drag

owing to the size of the sector and its strong performance. Good returns were registered

by the Fund in the first quarter but many shares in the sector were approaching their price

targets which encouraged us to reduce positions. While another extremely good entry

point was provided to us by the LIBOR scandal in June our feeling was that the size of the

fine could severely impair cash flow and this held us back from investing in the domestic

banks sector. We did increase Paragon, the buy to let lender, to be our largest active

position and this features as one of our key contributors at a stock level. However, we are

ultimately extremely frustrated that more money was not made in the sector.

At a stock level, corporate activity played its part with Aegis falling to a Japanese

competitor and Aer Lingus once again attracting the attention of Ryanair. Galliford Try, the

housebuilder and construction company, was a key contributor for the second year running

and underlines why conglomerate discounts remain a fertile hunting ground for us.

Portfolio Sector Attribution (01/01/2012-31/12/2012)

Source: Matterley

The most significant disappointment was Higland Gold which suffered a significant

derating from a modest starting valuation and now trades on a mere 4x 2013 earnings. The

reasons for this, in our view, were a significant stock overhang and a confused dividend

policy. The latter can and should be easily addressed and stock overhangs tend not to

weigh on fundamentals indefinitely. Relative to expectations the loss in Cairn Energy was

also hugely disappointing. Starting the year at a discount to cash and investments the

share price has broadly fallen in line with any investment in further exploration assets. A

share buyback from the company, effectively buying their significant exploration portfolio

at less than zero , would be entirely sensible in our opinion and we are ever hopeful of such

an outcome in the coming months.

Portfolio Stock Attribution (01/01/2012-31/12/2012)

ANGLO AMERICAN PLC

CAIRN ENERGY

VODAFONE PLC

AVIVA PLC

HIGHLAND GOLD & MINING PLC

Source: Matterley

Outlook for 2013

The rise in the equity market of 10.5% pre dividends has happened at a time when earnings

forecast have fallen modestly. As a result the earnings multiple of the market for 2013 has

risen to 11x. While not extreme in the context of history it is a rating that most likely

requires some sort of earnings growth for attractive capital appreciation to be achieved in

the year ahead. As things stand very modest growth is forecast but relative to consensus

we see three areas of possible positive surprise.

The first is the UK employment picture which continues to improve. It is easy to say that

this is in spite of, rather than because of, the coalition government but perhaps they

should receive some credit for the strides they have taken in reducing corporation tax. That

close to 500,000 jobs have been created in the year compares favourably to the 2 million

added in the US given that the US economy is over 6x larger than ours.

This has yet to feed through into any meaningful economic growth as disposable income

has remained subdued. It is our view, however, that after four years of falling disposable

income this is about to change owing in no small part to a rise in the income tax free

allowance from £8105 to £9205. This will result in as much £200 more on average for each

of the 31m workers in this country. This equates to slightly over £6bn or c 0.6% of UK GDP.

UK Employment Workforce Jobs By Industry All Jobs Index (2003-2012)

Source: Bloomberg

Further good news could also come in the form of a falling oil price. The chart below shows

the spot oil price and the futures price in white. The futures market has tended to be less

emotional than the spot market, and just as it ignored much of the fall in 2009 we think it is

interesting that the future price remains c $15 below the spot price today. Should the spot

price fall by $15 then the sensitivity to western GDP is as much as 1.5%. Factors that

might precipitate such a fall would include, improving supply and demand in the US as well

as technological improvements.

The final area where we think there could be upside surprise is in capital investment.

Much of the good news in the Autumn Statement was leaked beforehand, be it the tax free

threshold and the freeze in fuel duty, but the one bit of legislation we felt was new and

material was the tenfold increase in the tax free capital investment allowance. The one

UK Percentage Change in Disposable Income (2000-2015e)

Brent Crude v Brent Crude Future (2007-2012)

Source: Bloomberg

Source: Oriel

section of our society that has the money to spend today is our corporate sector. However,

what every politician has failed to do in the West is put them in a frame of mind whereby

they are willing to spend it. When this is combined with cutbacks in government spending

we have a situation when capital investment is well below even that of the early 90s. It is

our view, given the state of corporate balance sheets, that private sector capital

investment will increase significantly.

How are we positioned for the year ahead?

The frequently cited argument by bearish commentators is that earnings based metrics

are currently being flattered by unsustainably high operating margins. The analysis we

have carried out to some extent corroborates this view but as stock pickers we are still able

to find close to a third of the market operating below their 10 year average margins.

As an overlay to our strict valuation criteria, it stands to reason that this analysis is

allowing us to expose ourselves to stocks with both a cheap starting valuation and also the

propensity for earnings surprise.

UK Capital Investment as Percentage of GDP (1986-2012)

Source: Oriel

FTSE 350 Constituents: Percentage Above Or Below 10 Year Average Ebit Margin (31.12.2012)

Source: Matterley

Pe

rce

nta

ge

Percentage above or Below 10 Year Average Ebit Margin

Given our view of the trajectory of disposable income, we also think it is important to

challenge the largely consensus view that the end is nigh for consumer related areas. In

some instances, we believe we can expose ourselves to companies that are not only in a

position to beat conservative sales forecasts, but will also have the added benefit of falling

oil related costs.

The main message however, which we hope has been a consistent one, is that the portfolio

remains materially cheaper than the market as a whole. Below we show how the fund

compares to the market ex banks and life insurance, on four basic but extremely relevant

metrics. The significant sales uplift relative to the market is a function of the fact we seek

to expose ourselves to depressed company share prices where we believe there is a future.

A good starting point in establishing this is if sales and cash flow are being generated. The

earnings uplift is pleasing and when combined with the cash balance places the portfolio

on c 10x earnings. While not quite as cheap as a year ago it is still undemanding in both

absolute terms and relative to the market. It should also be extremely well rewarded if our

views on a possible growth surprise transpires during the year. When the cash balance is

taken in conjunction with the asset backing, we hope the portfolio will display defensive

qualities in the event of any pullback.

What do you get for every £1 invested? (Jan 2013)

Matterley Fund FTSE 100

Sales 156.1p 100.7p

Earnings 9.7p 8.0p

Tangible net assets 73.7p 34.0p

Net cash (Net debt) 4.5p -20.5p

Conclusion

We are perhaps surprisingly optimistic about the year ahead. However, the possibilities of

improving employment data, a rise in disposable income and capital investment as well as

a falling oil price, are not unreasonable. If this does unfold, the argument used by bearish

commentators that equities are only attractive relative to other expensive asset classes,

such as fixed interest, will quickly unravel. Indeed, with equities in mind, the saying goes

that a high price is paid for a happy consensus and it is our view that the consensus will be

happier by the end of the year than at any stage since the advent of the financial crisis in

2008. Within this, we hope that the portfolio will benefit disproportionately as it is

demonstrably cheaper than the market as a whole. While this is no guarantee of success,

it is a starting point that gives us a great deal of confidence in the year ahead.

Henry Dixon (7/01/2013)

Source: Matterley. Bloomberg consensus data for full year 2012e quoted on 31/12/12. Excludes

Banks and Life Insurance stocks and charges and expenses.

Valuation Matrix

Important Information

The information contained in this document does not constitute advice or a personal

recommendation, nor does it constitute an invitation to purchase units. Investment should be

made on the basis of the Prospectus and Simplified Prospectus, available on request. You are

recommended to seek advice concerning suitability from your investment adviser.

The information in this document is based upon sources we believe to be reliable, but its

accuracy cannot be guaranteed.

Please note past performance is not a reliable indicator of future returns. The value of

investments, and the income from them, can go down as well as up and may be affected by

exchange rate variations. The levels of taxation and their respective treatment depend on your

individual circumstances and the applicable law, which may be subject to change in the future.

The authorised corporate director of IM Matterley Investment Funds II is IFDS Managers Ltd

which is authorised and regulated by the Financial Services Authority, Registered Office: IFDS

House, St Nicholas Lane, Basildon, Essex, SS15 5FS.

The IM Matterley Undervalued Assets Fund is managed by Charles Stanley & Co. Limited, which is

authorised and regulated by the Financial Services Authority. This document has been issued

and approved for the purposes of section 21 of the Financial Services and Markets Act 2000 by

Charles Stanley & Co. Limited, which is authorised and regulated by the Financial Services

Authority. Unless a specific source is given, the source of all information within this document is

Charles Stanley & Co. Limited, with the exception of all share price data which is sourced from

Bloomberg. This document may also contain the fund managers' personal views and opinions

and does not necessarily reflect the views of Charles Stanley & Co Limited. Registered office 25

Luke Street, London EC2A 4AR. Registered in England no. 01903304.