ils annual report 2021

TRANSCRIPT

ILS Annual Report 2021 Alternative Capital: Continuing Growth Momentum

Table of Contents

Foreword . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Aon Securities’ Annual Review of the Catastrophe Bond Market . . . . . . 4

Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4

Global Catastrophic Loss Activity in H2 2020 and H1 2021 . . . . . . . . . . . . . . . . . .7

Catastrophe Bond Transaction Review by Quarter . . . . . . . . . . . . . . . . . . . . . . . . . .8

Secondary Market Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .16

COVID-19 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .17

ILS Transaction Activity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Capital Providers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .18

Capital Sources . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .18

Aon ILS Indices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .19

ILS Related Markets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Collateralized Reinsurance Market Trends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .22

Sidecars . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .22

Industry Loss Warranties (ILW) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .23

Private Catastrophe Bond Placements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .25

Growth Areas within ILS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

Environmental, Social and Governance (ESG) & Socially Responsible Investment (SRI) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .28

Collateral Solutions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .30

Public Sector/Residual Markets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .32

Corporate Sponsors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .33

Market Analysis by Region . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

North America . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .34

Europe . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .40

Asia-Pacific . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .40

Model Updates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

North America . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .43

Europe . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .43

Asia-Pacific . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .44

ILS Annual Report 2021 3

Foreword

It is my pleasure to bring to you the fourteenth edition of Aon Securities’ annual Insurance-Linked Securities (ILS) report .

The report aims to offer an authoritative insightful review and analysis of the ILS asset class and related developments in the

market . This report is intended to be an important and useful reference document, both for ILS market participants and those

with an active interest in the sector . Unless otherwise stated, its analyses cover the 12-month period ending June 30, 2021 .

The ILS market was tested by a number of events during the period under review across Asia-Pacific, Europe, the US, and

Australia (e .g . China seasonal floods, Japan Kyushu floods, Cyclone Ampham, Windstorm Ciara (also referred to as Sabine), US

Midwest derecho, Hurricanes Laura, Zeta, Sally and Isaias, winter storm Uri, California wildfires, and Australian hailstorms) and

the after effects of the COVID-19 Global pandemic . ILS markets have shown resilience, with record issuances in Q4 2020, and in

the 6-month period ending June 30, 2021 .

Aon's Weather, Climate & Catastrophe Insight 2020 Annual Report1 summarises: Direct economic losses and damage from natural

disasters in 2020 were estimated at $268 billion . While much lower than peak loss years in 2011 ($557 billion) and 2017 ($485

billion), it was above the average ($244 billion) and median ($246 billion) of the 21st Century . The economic losses were 12%

lower than the average and 1% lower than the median of the past decade (2010-2019) .

In the period under review, $13 billion of catastrophe bond issuance was secured (including Life and Health), an increase of $4

billion year on year . During this significant time in the market, ILS capital has increased to $97 billion from $91 billion last year .

By June 30, 2021, catastrophe bonds outstanding were $33 billion,13 .8% greater than June 30, 2020 at $29 billion .

The period under review witnessed both new issuers and repeat issuers coming to market, along with new geographical

coverages and innovations in the cat bond market . At $8 .5 billion, H1 2021 surpassed H1 2017 as the largest six-month period

of primary issuance on record . The primary market in Q2 2021 was particularly busy, with the issuance pipeline momentum

continuing through the second half of the year . With approximately $3 .7 billion of cat bonds set to mature, we expect this

market’s momentum to power through the second half of 2021 to potentially set a record full-year issuance, surpassing the

record in 2020 .

The 2021 edition of this annual ILS report, "Continuing Growth Momentum", covers a wide range of topics in the

ILS market, including:

• Aon Securities’ Annual Review of the Catastrophe Bond Market;

• A review of ILS Transaction activity;

• An overview of ILS Related Markets, including trends in ILW, Sidecars, and Private Placements;

• Growth Areas within ILS;

• A review of North America, Europe, and Asia-Pacific activity; and

• A review of Model Updates .

We hope you will find this report useful and informative, and if you have any questions relating to the data herein, or any queries

regarding any aspect of the ILS sector, please contact me or my colleagues .

Paul Schultz,

Chief Executive Officer, Aon Securities LLC

1 Aon – Impact Forecasting – Weather, Climate & Catastrophe Insight – 2020 Annual Report

4

Aon Securities’ Annual Review of the Catastrophe Bond Market

OverviewThe July 1, 2020 to June 30, 2021 year in review saw

continued strong growth in the catastrophe bond market,

with consistent quarterly issuances, and a record issuance

year of approximately $13 billion placed in the period under

review including Life and Health, versus $9 billion in the prior

year . There was a record Q4 issuance of $3 .7 billion followed

by the second largest Q2 issuance of $5 .6 billion over the

past 8 years .2

The year in review brought new issuers along with repeat

issuers, and the expansion of perils and geographies .

A selection of new and diverse issuers and new transactions

during the period were:

• Blackstone’s entry via Gryphon Mutual Insurance into the ILS

market with the $50 million Wrigley Re Ltd . Series 2021-1

Class A Notes which provide Blackstone managed funds

three years of per occurrence, parametric earthquake

coverage for their entities in the state of California .

• In another testament to the cat bond market being an avenue

to secure additional capacity, the Los Angeles Department of

Water and Power (LADWP) secured $50 million of coverage

for California Wildfire using an innovative and tailored

parametric solution .

• The debut catastrophe bond for Vermont Mutual Insurance

Company and affiliates, with a single Series 2021-1 Class A

tranche of notes upsized to $150 million, covering indemnity

losses from catastrophe events in the US Northeast; named

storm, earthquake, severe weather and fire .

• The Cosaint Re Pte . $150 million catastrophe bond, the first

issuance sponsored by Universal Insurance Holdings, came

to market covering US named storm reinsurance on an

indemnity and per occurrence basis, across a three-year

term, with coverage focused on Florida .

A selection of repeat issuers during the period were:

• Fidelis Insurance Bermuda executed their second and third

cat bonds after successfully placing their inaugural issuance

under the Herbie Re Ltd . program only several months

earlier in June . Herbie Re 2020-2 leveraged the strength of

the market to secure $275 million annual aggregate

protection against US earthquake and US named storms,

while Herbie Re Ltd . 2021-1 secured $150 million of global

annual aggregate capacity, representing the broadest

range of covered regions and perils for an insured industry

loss index cat bond at the time of issuance .

• Florida Citizens Property Insurance Corporation (Florida

Citizens) returned to the catastrophe bond market with its

largest issuance since 2014 and largest transaction in the

market in the period under review . Split across two Series

and three Classes, the Everglades Re II Ltd . 2021-1 and

2021-2 notes secured $950 million of indemnity coverage

for Florida Citizens’ Coastal and Personal Lines Accounts,

providing a key pillar of Florida Citizen’s risk transfer

program going into the 2021 Atlantic hurricane season .

• The California Earthquake Authority (CEA) returned to

market in the first quarter of 2021 to execute their

fourteenth cat bond transaction since their initial

Embarcadero series was issued in 2011 . The veteran

cedent sought protection via a single Class of Notes

which was upsized to $215 million of capacity .

• Tokio Marine & Nichido Fire Insurance Co ., Ltd . returned to

market for the fifth time under the Kizuna Re cat bond program .

This Kizuna iteration marks the first time Tokio Marine has used

the relatively new Singapore domicile for the issuance . The

series of Notes for $150 million covers the sponsor for Japan

earthquake risk on an aggregate indemnity basis .

• Assicurazioni Generali S .p .A . (AG) returned to the bond

market for its third Lion reinsurance transaction . The first

catastrophe bond to have specific ‘green’ features

incorporated, to match the ethos and initiatives of the

company . Generali is committed to the green ILS

framework it has created3 . With an Irish-domiciled SPV, a

single tranche of notes issued for (Euro) €200 million . The

notes provide Generali four years of indemnity per

occurrence reinsurance protection against losses from

European windstorms and Italian earthquakes .

The ILS market has continued growth momentum, as the

average transaction size for H1 2021 was $282 .3 million over

thirty different issuances; nineteen of those issuances came in

Q2, five behind Q2 2017 for the most issuances in a quarter . As a

comparison, the average deal size for H1 2020 was $241 .8

million over twenty-seven transactions . To further highlight the

success from the quarter, approximately 70% of all classes issued

in Q2 2021 both upsized and saw their spreads tighten to the

low ends of their initial guidance or better .

2 Aon Securities ILS Database

3 Generali – Press Release dated 24 February 2020

ILS Annual Report 2021 5

We are now beginning to see innovation in our market

broadening geographic and peril coverage . One such

example being Fidelis’ above mentioned Herbie Re Ltd .

2021-1 transaction, offering an attractive alternative to

worldwide ILW or UNL covering US (including US

Caribbean) and Canada named storms and earthquakes, US

and Canada severe thunderstorms, US and Canada winter

storms, US wildfires, Japan typhoons and earthquakes,

Europe windstorms, Italy earthquakes, Turkey earthquakes,

Australian tropical cyclones and earthquakes, and New

Zealand earthquakes, all on an index basis .

We also see the emergence of ESG/SRI cat bond collateral

components in the Lion reinsurance transaction mentioned

above, a growth area for the future . Corporate activity is

increasing and under active consideration . Also, LADWP are the

first municipal utility to access the catastrophe bond market .

The low market volatility compared to other asset classes

has re-demonstrated the value in this market that was

proven in the 2008 Financial Crisis, the 2010-2012

European Debt Crisis, and the COVID-19 market pause in

March and April 2020 . The fundamentals of this asset class

have not changed, and the characteristics of the

diversification provided by this market were well received

by investors .

We see the catastrophe bond market in a strong position .

Capital inflows over the past year have assisted respective

market and transaction upsizing, approximatively $4 billion

market issuance increase year on year refers . With prolonged

low interest rates and in certain global regions a continuing

negative interest rate environment as well as the low correlation

and diversification benefits, the demonstrated value of the ILS

markets will continue to drive capital to this space .

Exhibit 1: Catastrophe bond issuance by year, 2010 to 2021 (years ending June 30)

Source: Aon Securities LLC

Exhibit 2: Outstanding and cumulative catastrophe bond volume, 2010 to 2021 (years ending June 30)

Source: Aon Securities LLC

13,167 11,504 14,923 17,51322,422 23,387 22,562 25,821

30,109 30,538 29,860 33,74833,22337,605

44,03750,702

60,10267,083

72,273

83,59693,338

98,762107,774

121,058

- 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000 90,000

100,000 110,000 120,000 130,000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

USD

mill

ions

Property Outstanding L ife and Health

Outstanding Total Cumulative Property Issuances

Total Cumulative Bonds

USD

mill

ions

4,736 4,382

6,6656,431

9,400

6,981

5,190

11,323

9,742

5,424

9,012

13,284

0

2000

4000

6000

8000

10000

12000

14000

202120202019201820172016201520142013201220112010

Life and Health Issuance

Property Issuance

6

Issuer Domicile SummaryBermuda continued to be the largest issuer domicile for the

12-month period under review, as 38 issuances used the

jurisdiction, with Singapore accounting for 7, the Cayman

Islands 3, Ireland 2, and the UK 1 of the 51 total new issues .

Overall, as was the case in the 2020 review, Bermuda

continued to attract the majority of issuer domiciliation

under the period in review .

The Monetary Authority of Singapore (MAS) announced that

it is extending its ILS grant scheme until the end of 2022 .4

Exhibit 3: Number of transactions per issuer domicile

Domicile Period endingJune 30, 2020

Period endingJune 30, 2021

Bermuda 21 38

Singapore 5 7

Cayman 4 3

Ireland 3 2

USA 2 1

Grand Total 35 51

Source: Aon Securities LLC

New Issuer domicile developments – Hong KongOn July 17, 2020, the Hong Kong Legislative Council

passed the Insurance (Amendment) Bill 2020 . The bill

seeks to amend the Insurance Ordinance (Cap . 41) in order

to create new business opportunities for the insurance

sector . Key changes introduced by the bill include to

provide for a new regulatory regime for the ILS business

where the Hong Kong Insurance Authority (HKIA) have

been empowered to authorize a company to carry on

Special Purpose Business (SPB) .

The 2-year pilot ILS Grant Scheme of up to HKD $12 million

($1 .6 million) per issuance has been approved by the

Hong Kong Government to incentivize sponsors to the

domicile . The scheme grant in Singapore is equivalent to

approximately $1 .5 million and the HKIA scheme will have

similar qualifying requirements seen in Singapore such as

a minimum of 20% issuance costs to be billed locally and

a minimum investment size of $250,000 . However, the

licensing process of the HKIA at present may take anywhere

from 6 weeks to 2 months .

Further to the gazette of the Insurance (Amendment)

Ordinance 2020 and the Insurance (Special Purpose

Business) Rules on July 2020 which came into effect March

29, 2021, HKIA have since published a guideline (GL-33) for

authorization of Special Purpose Insurers (SPI) to carry on SPB

in or from Hong Kong . The GL-33 provides further guidelines

effective on June 30, 2021 . Additionally, the guideline also

highlights Rule 3(1) and Rule 3(4) of the SPB Rules, limiting

the scope of persons whom ILS may be offered or sold to .

The publication of the GL-33 represents another milestone of

the HKIA’s initiative in strengthening Hong Kong’s position as

a global risk management centre .

The addition of Hong Kong as a domicile will be pivotal

to the growth of the ILS market in the region, giving both

sponsors and investors to choose a location that may have

more suitability facets such as time zone and currency .

More importantly, Hong Kong provides a workable

connectivity to China, where recent increased competition

in traditional reinsurance motivates potential sponsors to

consider Capital Markets .

The Hong Kong and existing Singapore initiatives bode well

for the Asian market, and future growth developments .

4 Monetary Authority of Singapore

ILS Annual Report 2021 7

Global Catastrophic Loss Activity in H2 2020 and H1 2021

H2 2020Calendar year 2020 saw $97 billion in insured losses, which

represents a 37% increase from 2019 and a 40% increase over

the 20-year average . There remains material divergence of

economic loss ($268 billion) to insured loss ($97 billion) globally,

which demonstrates the persistent issue of protection gaps . The

US represented 76% of global insured losses over the annual

period . For comparison, the US share of global insured losses

has averaged at 57 percent during the 21st Century .

The year 2020 saw an active hurricane season with a record

frequency of named storms (30 events), 13 hurricanes, and 6

major hurricanes, the US mainland saw 12 of those named

storms (including six hurricanes) make landfall . The severe

convective storm (SCS) peril surpassed 2011, previously

considered the benchmark year for SCS, as the costliest severe

weather season on record with $63 billion in economic losses

(versus $53 billion in 2011) . It was led by the historic derecho

that swept across the Midwest on August 8-12 with economic

losses of $12 .6 billion . Wildfires in the Western US also

prompted a modern era record for acres burned and the third-

highest annual peril payouts for insurers on record (only

surpassed by 2017 and 2018) . Hurricane Laura, which impacted

the US and Caribbean, was the single largest event, with an

insured loss of $10 billion .

COVID-19 meant the insurance industry faced challenges in

attempting to accelerate the claims process, while balancing

multiple large-scale disasters, pending litigation from COVID-

19-related incidents, a disrupted supply chain, and other

complex scenarios . However, overall, the industry proved fairly

resilient through effective risk transfer, capital management and

capital deployment .

Source: Aon – Impact Forecasting – Weather, Climate & Catastrophe Insight - 2020 Annual Report

H1 2021The first half of 2021 has seen $93 billion in economic losses

from property catastrophe events, which is 16% below

the 20-year H1 average . Though well below the average

economic loss, total insured losses of $42 billion to date are

39% above the 21st century H1 average .

The US Polar Vortex event (Uri) in mid-February resulted in

$22 billion of economic loss, with high insurance penetration

translating to $15 billion insured loss . This was the costliest

event ever recorded for the peril of severe convective storm

and winter storm .

Western and Central Europe experienced $4 .5 billion of

insured loss from major storms and flooding during mid to

late June, with this number possibly set to rise . Ten separate

severe convective storm events (including hail, wind and

heavy rain) in the US caused approximately $500 million

of insured loss, which represents a reduced frequency

to H1 2020 . A number of countries experienced record

temperatures, such as Canada and parts of Africa, however

this resulted in no material industry loss events .

Source: Aon - Impact Forecasting - Global Catastrophe Recap First Half of 2021

8

Catastrophe Bond Transaction Review by Quarter

Q3 2020Historically, third quarter catastrophe bond issuance is the

low point in the quarterly issuance cycle compared to the

remainder of the year due to (re)insurance purchasing trends .

We observed four issuances in Q3 2020 totalling $742 million5,

up from zero in the year prior .

Hypatia Ltd .

Convex Re sponsored the Hypatia Ltd . Series 2021-1, their first

catastrophe bond transaction, with the Class A and B tranches

covering US named storms and earthquake perils totalling $300

million . Both note classes priced below the initial guidance at

6 .75% and 9 .75% respectively . Each class of notes utilizes an

industry loss index trigger on an annual aggregate basis for a

3-year term .

Matterhorn Re Ltd .

Matterhorn Re Ltd . Series 2020-4 came back to the market

with a dual tranche catastrophe bond issue covering US named

storms perils totalling $240 million . Class A priced at the tight

end of guidance at 10% and Class B priced at 86 .25% of par

lower than guidance . Each class of notes utilizes an industry

loss index trigger on a per occurrence basis for an approximate

18-month term .

SD Re Ltd .

Sempra Energy sponsored the SD Re Ltd Series 2020-1

catastrophe bond transaction, with a single note class covering

California wildfires totalling $90 million, utilizing an indemnity

trigger on an annual aggregate basis for an approximate 3-year

term . The notes priced at 9 .75% at the mid point of guidance .

Azzurro Re II DAC

UnipolSai Assicurazioni S .p .A sponsored the Azzurro Re II DAC

Series 2020-1 catastrophe bond transaction, with a single note

class covering Europe earthquake risk totalling (Euro) €100

million (equivalent to $112 million), utilizing an indemnity

trigger on a per occurrence basis for a 4-year term . The notes

priced at 4 .50% at the mid point of guidance .

We expect future Q3 issuance growth as new and opportunistic

issuers continue to evaluate the value of ILS capital in mitigating

climate risks .

Exhibit 4: Q3 2020 catastrophe bond issuance

Beneficiary Issuer Series ClassIssue Size (USD million)

Covered Perils Trigger Recovery Collateral

Swiss Reinsurance Company Ltd .

Matterhorn Re Ltd .

Series 2020-4 Class A $65 .00 US NS Industry

Index Occurrence MMF

Swiss Reinsurance Company Ltd .

Matterhorn Re Ltd .

Series 2020-4 Class B $175 .00 US NS Industry

Index Occurrence MMF

Sempra Energy SD Re Ltd . Series 2020-1 Class A $90 .00

CAL WF (originating from power/transformation system of insured)

Indemnity Annual Aggregate MMF

UnipolSai Assicurazioni S .p .A

Azzurro Re II DAC, an Irish special purpose

Series 2020-1 Class A $112 .44 EU EQ Indemnity Occurrence EBRD

Convex Re Limited . Hypatia Ltd . Series

2020-1 Class A $150 .00 US NS & EQ Industry Index

Annual Aggregate MMF

Convex Re Limited . Hypatia Ltd . Series

2020-1 Class B $150 .00 US NS & EQ Industry Index

Annual Aggregate MMF

Total $742.44

Source: Aon Securities LLC

5 Assumes 1 .12 EUR/USD conversion as of the issuance date

ILS Annual Report 2021 9

Q4 2020

Herbie Re Ltd .

Fidelis Insurance executed their second cat bond in October

after successfully placing their inaugural issuance only a few

months earlier in June . The strength of the market and the

support from investors on the Series 2020-1 transaction

allowed Fidelis to secure annual aggregate protection against

US earthquake and US named storms (including DC, Puerto

Rico and the US Virgin Islands) across different points in the risk

curve . Each class of notes utilizes an industry loss index trigger

on an annual aggregate basis and provides for either a 4-year

or a 2-year term . Classes A and B priced below the guidance at

6 .25% and 16 .00% respectively with Class B pricing at the tight

end of guidance at 9 .00% . The transaction was well received

by the market having upsized to $275 million across the three

tranches, after initially seeking $175 million .

Four Lakes Re Ltd .

The market was pleased by the return of American Family

Mutual Insurance to the cat bond market in November 2020,

10 years after their first transaction in 2010 . Given the evolution

of the market over the last decade AmFam was able to source

significantly broader peril coverage than their previous

deals, successfully upsizing their transaction that provides for

indemnity, per occurrence protection against US multi-peril

offering . Class A priced per guidance at 7 .00% and Class B at

9 .50% at the upper end of guidance . The two-tranche offering

initially targeted $150 million, however, due to positive investor

demand and market receptiveness, AmFam placed a $175

million deal .

Power Protective Re Ltd .

The Los Angeles Department of Water and Power secured $50

million of coverage for California Wildfires at a price of 10 .75%

using an innovative and tailored parametric solution . LADWP

are the first municipal utility to access the catastrophe bond

market and despite market stresses in the wildfire market,

LADWP were able to successfully complete their transaction .

The tailored recovery mechanism included a parametric

trigger based on reconstruction cost value in a pre-defined

area, and to reduce potential basis risk, leveraged a stepped

pay out function based on the severity of the event .

Exhibit 5: Q4 2020 catastrophe bond issuance

Beneficiary Issuer Series ClassIssue Size (USD million)

Covered Perils Trigger Recovery Collateral

California Earthquake Authority

Ursa Re Ltd . Series 2020-1

Class AA $425 .00 CAL EQ Indemnity Annual

Aggregate MMF

California Earthquake Authority

Ursa Re Ltd . Series 2020-1 Class D $350 .00 CAL EQ Indemnity Annual

Aggregate MMF

Fidelis Insurance Bermuda Limited Herbie Re Ltd . Series

2020-2 Class A $100 .00 US, PR, USVI: NS or EQ

Industry Index

Annual Aggregate MMF

Fidelis Insurance Bermuda Limited Herbie Re Ltd . Series

2020-2 Class B $150 .00 US, PR, USVI: NS or EQ

Industry Index

Annual Aggregate MMF

Fidelis Insurance Bermuda Limited Herbie Re Ltd . Series

2020-2 Class C $25 .00 US, PR, USVI: NS or EQ

Industry Index

Annual Aggregate MMF

United Services Automobile Association

Residential Reinsurance 2020 Limited

Series 2020-2 Class 1 $50 .00

US TC, EQ, WS, ST, WF, VE, MI, OP

Indemnity Occurrence MMF

United Services Automobile Association

Residential Reinsurance 2020 Limited

Series 2020-2 Class 3 $150 .00

US TC, EQ, WS, ST, WF, VE, MI, OP

Indemnity Occurrence MMF

10

Beneficiary Issuer Series ClassIssue Size (USD million)

Covered Perils Trigger Recovery Collateral

United Services Automobile Association

Residential Reinsurance 2020 Limited

Series 2020-2 Class 4 $200 .00

US TC, EQ, WS, ST, WF, VE, MI, OP

Indemnity Occurrence MMF

American Family mutual Insurance Company, S .I . (AFMICSI)

Four Lakes Re Ltd . Series 2020-1 Class A $100 .00

US NS, EQ, ST, WS, WD, VE, MI

Indemnity Occurrence MMF

American Family mutual Insurance Company, S .I . (AFMICSI)

Four Lakes Re Ltd . Series 2020-1 Class B $75 .00

US NS, EQ, ST, WS, WD, VE, MI

Indemnity Occurrence MMF

Alphabet, Inc . Phoenician Re Ltd .

Series 2020-1 Class A $237 .50 CAL EQ Indemnity Occurrence MMF

Swiss Reinsurance Company Ltd .

Matterhorn Re Ltd .

Series 2020-5 Class A $150 .00 US NS Industry

Index Occurrence EBRD

Swiss Reinsurance Company Ltd .

Matterhorn Re Ltd .

Series 2020-5 Class B $150 .00 US NS Industry

Index Occurrence EBRD

Los Angeles Department of Water and Power

Power Protective Re Ltd .

Series 2020-1 Class A $50 .00 CAL WF Parametric Occurrence MMF

AXIS Capital Northshore Re II Limited

Series 2021-1 Class A $150 .00

US, PR, USVI, CAN: NS, EQ, WS

Industry Index

Annual Aggregate MMF

Brit Syndicates Limited

Sussex Capital UK UCC Limited

Series 2020-1 - $300 .00 US, PR, USVI:

NS, EQIndustry index

Annual Aggregate MMF

Alphabet, Inc . Phoenician Re Ltd .

Series 2020-2 Class A $95 .00 CAL EQ Indemnity Occurrence MMF

American Strategic Insurance Group

Bonanza Re Ltd . Series 2020-2 Class A $200 .00 US HU Indemnity Occurrence MMF

American Strategic Insurance Group

Bonanza Re Ltd . Series 2020-2 Class B $95 .00 NS, WS, WF,

EQ, ST Indemnity Annual Aggregate MMF

Liberty Mutual Insurance Company

Mystic Re IV Ltd . Series 2021-1 Class A $300 .00 US, PR, USVI,

CAN: NS, EQIndustry Index Occurrence MMF

Hamilton Re Ltd . Easton Re Pte . Ltd .

Series 2020-1 Class A $150 .00 US NS, EQ Industry

index Occurrence MMF

Allied World Assurance Company

2001 CAT Re Ltd . Series 2020-1 Class A $210 .00

US, PR, USVI: NS, EQ, ST, EU Wind

Industry Index

Annual Aggregate MMF

Total $3,712.50

Source: Aon Securities LLC

Exhibit 5: Q4 2020 catastrophe bond issuance (continued)

ILS Annual Report 2021 11

Q1 2021

Ursa Re II Ltd .

The California Earthquake Authority (CEA) returned to market

in the first quarter of 2021 for their fourteenth cat bond

transaction since their initial Embarcadero series was issued

in 2011 . The transaction sought protection via a single class

of notes which was initially marketed for $150 million of

capacity at a target pricing range of 6 .75% to 7 .25% . Strong

investor support allowed the transaction to upsize to $215

million at a reduced risk interest spread of 6 .25% .

The CEA capitalized on strong market support in 2020 having

issued three transactions from May 2020 . Carrying on from

this 2020 momentum, with this Ursa Re II issuance in early

2021, the CEA was able to secure $1 .69 billion in support

across these four transactions within an approximately

10-month period .

Cosaint Re Pte .

The Cosaint Re Pte . $150 million catastrophe bond, the first

issuance sponsored by Universal Insurance Holdings, came

to market covering US named storm reinsurance on an

indemnity and per occurrence basis, across a three-year term,

with coverage focused on Florida . The notes priced below

the guidance at 9 .25% .

Kizuna Re III Pte . Ltd .

Tokio Marine & Nichido Fire Insurance Co ., Ltd . returned to

market for the fifth time under the Kizuna Re cat bond program .

This Kizuna iteration marks the first time Tokio Marine has used

the relatively new Singapore domicile for the issuance . The

series of notes covers the sponsor for Japan earthquake risk on

an aggregate indemnity basis . The structure of the program is

similar to previous Kizuna transactions which allows for a three-

year aggregate accumulation of losses within a 5-year overall

term of the notes . The transaction marketed for $150 million

of capacity at an initial price guidance of 2 .25% to 2 .50%;

however, due to strong investor support for the peril/region and

structure, it priced at a 2 .00% risk interest spread .

Sakura Re Ltd .

Sompo Japan and Sompo International came to market

with Sakura Re Series 2021-1 in Q1 . Sompo Japan has been

a consistent cat bond sponsor, with Sakura Re being their

fourth time accessing the cat bond market since 2014 . Sakura

Re represents the initial foray into the cat bond market for

the current Sompo International Group and the first joint

issuance by the newly combined entities of Sompo Japan and

Sompo International .

The transaction offered a progressive multi peril and multi

region structure with second event limit sharing features

between Sompo Japan and Sompo International subject

business . The unique structural feature incorporated into

the bond acts as a quasi-reinstatement feature that enables

additional limit of capacity to be accessed following an

initial large Japan typhoon or US earthquake from the

alternate class of notes . In addition, the business mix of the

US earthquake exposure was exclusively commercial and

industrial lines of business, which are underrepresented risks

in the cat bond market .

The transaction was issued across two classes of notes,

with Class A primarily covering Japan typhoons and Class B

primarily covering US earthquakes, both on an indemnity,

occurrence basis . The Class A notes priced below the

guidance at 2 .25% and the Class B notes priced just below

the mid point at 4 .00% . Each class was initially marketed at

$100 million but were upsized to $200 million due to strong

investor support .

12

Exhibit 6: Q1 2021 catastrophe bond issuance

Beneficiary Issuer Series ClassIssue Size (USD million)

Covered Perils Trigger Recovery Collateral

Bayview MSR Opportunity Master Fund, L .P .

Sierra Ltd . Series 2021-1 Class A $150 .00 US EQ Parametric

Index Occurrence MMF

Bayview MSR Opportunity Master Fund, L .P .

Sierra Ltd . Series 2021-1 Class B $50 .00 US EQ Parametric

Index Occurrence MMF

Federal Emergency Management Agency

FloodSmart Re Ltd .

Series 2021-1 Class A $450 .00 US, DC, PR,

VI: FL Indemnity Occurrence MMF

Federal Emergency Management Agency

FloodSmart Re Ltd .

Series 2021-1 Class B $125 .00 US, DC, PR,

VI: FL Indemnity Occurrence MMF

California Earthquake Authority

Ursa Re Ltd . Series 2021-1 Class F $215 .00 CAL EQ Indemnity Annual

Aggregate MMF

North Carolina Insurance Underwriting Association

Cape Lookout Re Ltd .

Series 2021-1 Class A $250 .00 NC NS, ST Indemnity Annual

Aggregate MMF

Security First Insurance Company

First Coast Re III Pte . Ltd .

Series 2021-1 Class A $225 .00 FL NS, ST Indemnity Occurrence

Cascading MMF

Universal Property and Casualty Insurance Company (UPCIC)

Cosaint Re Pte . Series 2021-2 Class A $150 .00

US NS: AL, DE, FL, GA, HI, IL, IN, IA, MD . MA, MI, MN, NH, NJ, NY, NC, PA, SC, TN, VA, WI

Indemnity Occurrence MMF

Tokio Marine & Nichido Fire Insurance Co ., Ltd .

Kizuna Re III Pte . Ltd .

Series 2021-1 Class A $150 .00 JP EQ Indemnity Aggregate MMF

Sompo Japan Insurance & affiliates

Sakura Re Ltd . Series 2021-1 Class A $200 .00

JP EQ, Typhoon and Flood, US EQ

Indemnity Occurrence MMF

Sompo Japan Insurance & affiliates

Sakura Re Ltd . Series 2021-1 Class B $200 .00

JP EQ, Typhoon and Flood, US EQ

Indemnity Occurrence MMF

Palomar Specialty Insurance Company

Torrey Pines Re Ltd .

Series 2021-1 Class A $200 .00 US EQ Indemnity Occurrence MMF

Palomar Specialty Insurance Company

Torrey Pines Re Ltd .

Series 2021-1 Class B $200 .00 US EQ Indemnity Occurrence MMF

State Farm Fire and Casualty Company

Merna Re II Ltd . Series 2021-1 Class A $350 .00

50 US States, DC, excl . CA, FL, TX

Indemnity Occurrence MMF

Total $2,915.00

Source: Aon Securities LLC

ILS Annual Report 2021 13

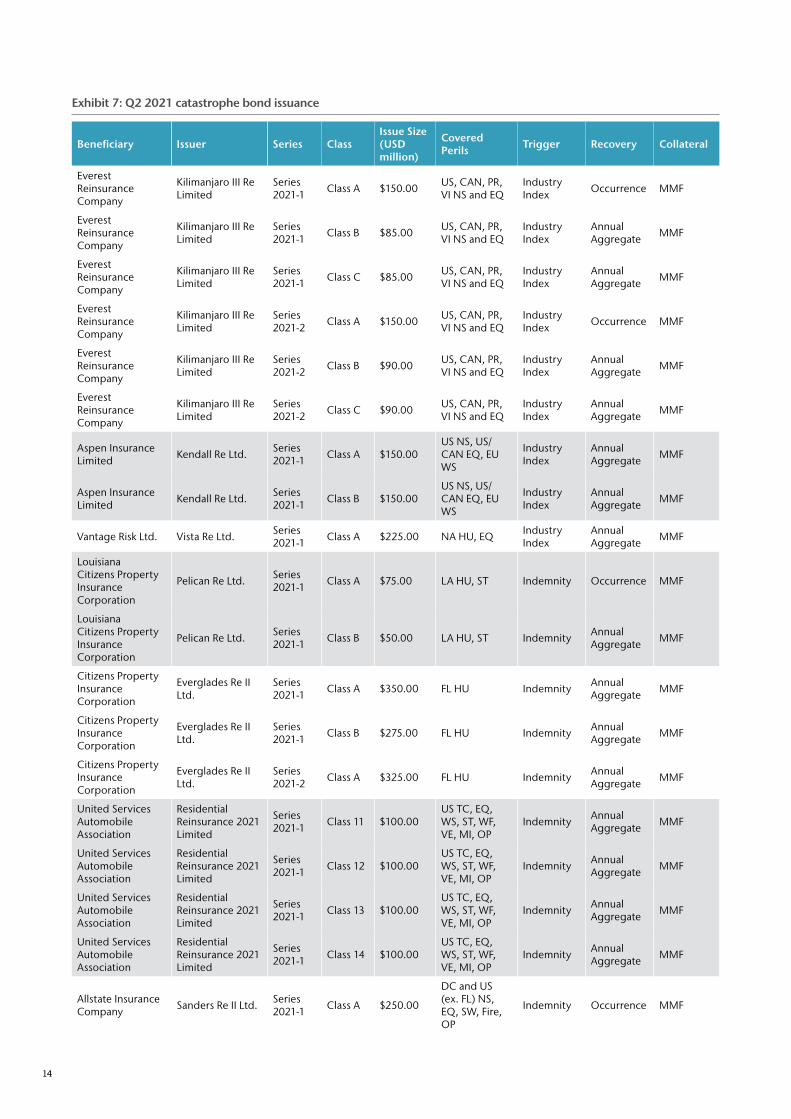

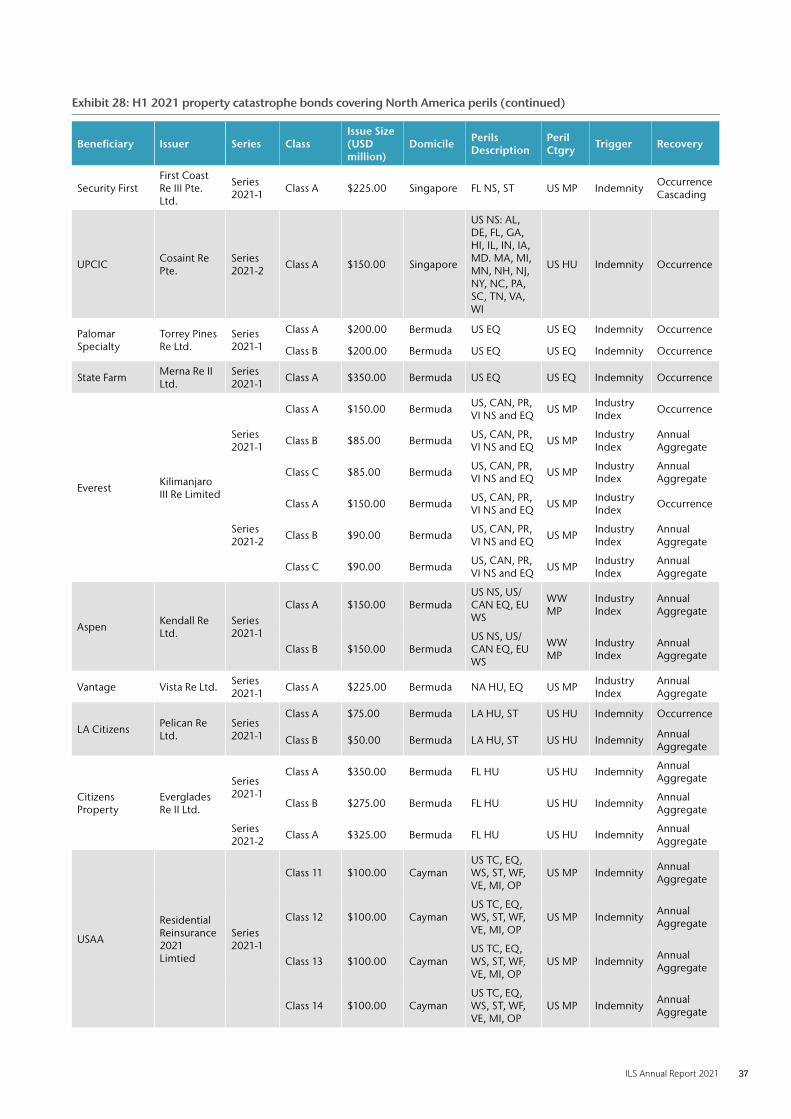

Q2 2021

Everglades Re II Ltd . 2021-1 and 2021-2

Florida Citizens returned to the catastrophe bond market

with its largest issuance since 2014 and largest transaction in

the market in the period under review .

Split across two Series and three Classes, the Everglades

Re II Ltd . 2021-1 and 2021-2 notes secured $950 million of

indemnity coverage on an annual aggregate basis for Florida

Citizens’ Coastal and Personal Lines Accounts to cover Florida

Hurricane risk, providing a key pillar of Florida Citizen’s risk

transfer program going into the 2021 Atlantic hurricane

season . All note classes priced at the tight end of guidance,

the Class A-1 and A-2 notes priced at 5 .75% and the Class B-1

notes priced at 6 .75% .

Kilimanjaro III Re Ltd . 2021-1 and 2021-2

Everest Re returned to the bond market with six tranches of

Kilimanjaro Re III Ltd . 2021-1 and 2021-2 notes, to maintain its

status as the largest sponsor of retrocessional bonds globally .

The bonds replace part of its maturing US and Canada multi-

peril retrocession cat bonds .

A total limit of $650 million was purchased, across a range

of risk levels and triggers (aggregate and occurrence) . Like

other recent issuances from Everest Re, Kilimanjaro III Re 2021

placement features two series, each with three tranches of

notes, with the only difference being tenure of coverage . This

allows Everest Re to stagger bond renewals and allows the

company to test investor appetite over time .

All note classes priced below the guidance, the Class A-1 and

A-2 notes priced at 11 .25%, the Class B-1 and B-2 notes priced

at 4 .50%, and the Class C-1 and C-2 notes priced at 4 .25% .

Sanders Re II Ltd . 2021-1

Allstate is a regular issuer of cat bonds, with this representing

the fourteenth Sanders Re Ltd . tranche ceded to the market .

Sanders Re II Ltd . issued a single tranche of notes, with a target

issuance size of $200 million, which upsized to $250 million .

The notes provide Allstate and subsidiaries with four years of

indemnity protection on a per occurrence basis . The notes

are exposed to US named storm, earthquake, severe weather,

wildfires and other perils, but will not cover Florida and

priced at tight end of guidance (3 .50% risk interest spread) .

Herbie Re Ltd . 2021-1

This third catastrophe bond transaction sponsored by Fidelis,

in fairly quick succession, secured annual aggregate

cover on a global basis, resulting in the broadest set of perils

and geographies covered in an industry loss index bond

at the time of issuance . Herbie Re Ltd ., Fidelis’ Bermuda-

domiciled special purpose insurer, issued a single tranche of

4-year annual aggregate Series 2021-1 Notes, with coverage

resembling a worldwide ILW .

The covered perils and regions included: North America

named storm and earthquake, US severe thunderstorm, US

wildfires, US winter storms, US Caribbean earthquake, Japan

typhoon, Japan earthquake, Canada severe storm, Canada

winter storm, European windstorm, Italy earthquake, Turkey

earthquake, Australia earthquake, Australia tropical cyclone,

and New Zealand earthquake .

The transaction tripled in size during marketing to $150

million and priced below initial guidance at 17 .25% .

Lion III Re DAC

Assicurazioni Generali S .p .A . returned to the bond market for

its third Lion reinsurance transaction . The first catastrophe

bond to have specific ‘green’ features incorporated, to

match the ethos and initiatives of the company . Generali is

committed to the green ILS framework it has created . With

an Irish-domiciled SPV, a single tranche of notes issued for

(Euro) €200 million . The notes provide Generali four years

of indemnity per occurrence reinsurance protection against

losses from European windstorms and Italian earthquakes .

Green and ESG credentials may have assisted the marketing of the

bond, which placed below the tight end of guidance at 3 .50% .

Baldwin Re Ltd . 2021

Debut catastrophe bond for Vermont Mutual Insurance

Company and affiliates, with a single Series 2021-1 Class A

tranche of notes upsized to $150 million, covering indemnity

losses from catastrophe events in the US Northeast; named

storms, earthquake, severe weather and fire .

The notes closed below the tight end of pricing, at 2 .25% .

Titania Re Ltd . 2021

The first catastrophe bond issued by Lloyd’s syndicate Ariel Re

1910 in a single $150 million tranche of notes, to cover US and

Canada named storms and earthquake . The notes contained an

industry loss index trigger providing annual aggregate protection

and priced below the tight end of guidance at 4 .50% .

14

Exhibit 7: Q2 2021 catastrophe bond issuance

Beneficiary Issuer Series ClassIssue Size (USD million)

Covered Perils Trigger Recovery Collateral

Everest Reinsurance Company

Kilimanjaro III Re Limited

Series 2021-1 Class A $150 .00 US, CAN, PR,

VI NS and EQIndustry Index Occurrence MMF

Everest Reinsurance Company

Kilimanjaro III Re Limited

Series 2021-1 Class B $85 .00 US, CAN, PR,

VI NS and EQIndustry Index

Annual Aggregate MMF

Everest Reinsurance Company

Kilimanjaro III Re Limited

Series 2021-1 Class C $85 .00 US, CAN, PR,

VI NS and EQIndustry Index

Annual Aggregate MMF

Everest Reinsurance Company

Kilimanjaro III Re Limited

Series 2021-2 Class A $150 .00 US, CAN, PR,

VI NS and EQIndustry Index Occurrence MMF

Everest Reinsurance Company

Kilimanjaro III Re Limited

Series 2021-2 Class B $90 .00 US, CAN, PR,

VI NS and EQIndustry Index

Annual Aggregate MMF

Everest Reinsurance Company

Kilimanjaro III Re Limited

Series 2021-2 Class C $90 .00 US, CAN, PR,

VI NS and EQIndustry Index

Annual Aggregate MMF

Aspen Insurance Limited Kendall Re Ltd . Series

2021-1 Class A $150 .00US NS, US/CAN EQ, EU WS

Industry Index

Annual Aggregate MMF

Aspen Insurance Limited Kendall Re Ltd . Series

2021-1 Class B $150 .00US NS, US/CAN EQ, EU WS

Industry Index

Annual Aggregate MMF

Vantage Risk Ltd . Vista Re Ltd . Series 2021-1 Class A $225 .00 NA HU, EQ Industry

IndexAnnual Aggregate MMF

Louisiana Citizens Property Insurance Corporation

Pelican Re Ltd . Series 2021-1 Class A $75 .00 LA HU, ST Indemnity Occurrence MMF

Louisiana Citizens Property Insurance Corporation

Pelican Re Ltd . Series 2021-1 Class B $50 .00 LA HU, ST Indemnity Annual

Aggregate MMF

Citizens Property Insurance Corporation

Everglades Re II Ltd .

Series 2021-1 Class A $350 .00 FL HU Indemnity Annual

Aggregate MMF

Citizens Property Insurance Corporation

Everglades Re II Ltd .

Series 2021-1 Class B $275 .00 FL HU Indemnity Annual

Aggregate MMF

Citizens Property Insurance Corporation

Everglades Re II Ltd .

Series 2021-2 Class A $325 .00 FL HU Indemnity Annual

Aggregate MMF

United Services Automobile Association

Residential Reinsurance 2021 Limited

Series 2021-1 Class 11 $100 .00

US TC, EQ, WS, ST, WF, VE, MI, OP

Indemnity Annual Aggregate MMF

United Services Automobile Association

Residential Reinsurance 2021 Limited

Series 2021-1 Class 12 $100 .00

US TC, EQ, WS, ST, WF, VE, MI, OP

Indemnity Annual Aggregate MMF

United Services Automobile Association

Residential Reinsurance 2021 Limited

Series 2021-1 Class 13 $100 .00

US TC, EQ, WS, ST, WF, VE, MI, OP

Indemnity Annual Aggregate MMF

United Services Automobile Association

Residential Reinsurance 2021 Limited

Series 2021-1 Class 14 $100 .00

US TC, EQ, WS, ST, WF, VE, MI, OP

Indemnity Annual Aggregate MMF

Allstate Insurance Company Sanders Re II Ltd . Series

2021-1 Class A $250 .00

DC and US (ex . FL) NS, EQ, SW, Fire, OP

Indemnity Occurrence MMF

ILS Annual Report 2021 15

Beneficiary Issuer Series ClassIssue Size (USD million)

Covered Perils Trigger Recovery Collateral

Great American Insurance Company

Riverfront Re Ltd . - Class A $235 .00US, DC, CAN NS, EQ, ST, WS, WF, VE, MI

Indemnity Occurrence MMF

Great American Insurance Company

Riverfront Re Ltd . - Class B $70 .00US, DC, CAN NS, EQ, ST, WS, WF, VE, MI

Indemnity Occurrence MMF

Fidelis Insurance Bermuda Limited Herbie Re Ltd . Series

2021-1 Class A $150 .00

US/CAN: NS EQ ST WS, US: WF, JP: TY EQ, EU: Wind, IT, TRK, AU, NZ: EQ, AU: TC

Industry Index

Annual Aggregate MMF

St . Johns Insurance Company

Putnam Re Pte . Ltd .

Series 2021-1 Class A $120 .00 FL and SC NS Indemnity Occurrence MMF

Texas Windstorm Insurance Association

Alamo Re Ltd . Series 2021-1 Class A $500 .00 TX NS, ST Indemnity Annual

Aggregate MMF

Syndicate 1910 (Ariel Re) Titania Re Ltd . Series

2021-1 Class A $150 .00US, DC, PR, VI, CAN: NS and EQ

Industry Index

Annual Aggregate MMF

Liberty Mutual Insurance Company

Mystic Re IV Ltd . Series 2021-2 Class A $225 .00

US, CAN, Caribbean NS, EQ

Indemnity Occurrence MMF

Liberty Mutual Insurance Company

Mystic Re IV Ltd . Series 2021-2 Class B $75 .00

US, CAN, Caribbean NS, EQ

Indemnity Occurrence MMF

Gryphon Mutual Insurance Company

Wrigley Re Ltd . Series 2021-1 Class A $50 .00 CA EQ Parametric Occurrence MMF

Tokio Marine & Nichido Fire Insurance Co ., Ltd .

Umigame Re Pte Ltd .

Series 2021-1

Class A-1 $100 .00 JP Typhoon

and Flood Indemnity Occurrence MMF

Tokio Marine & Nichido Fire Insurance Co ., Ltd .

Umigame Re Pte Ltd .

Series 2021-1

Class A-2 $50 .00 JP Typhoon

and Flood Indemnity Occurrence MMF

Tokio Marine & Nichido Fire Insurance Co ., Ltd .

Umigame Re Pte Ltd .

Series 2021-1 Class B $50 .00 JP Typhoon

and Flood Indemnity Occurrence MMF

State Farm Florida Insurance Company

Merna Re II Ltd . Series 2021-2 Class A $300 .00

US FL NS and Convective Storm

Indemnity Occurrence MMF

Assicurazioni Generali S .p .A Lion III Re DAC - - $239 .00 EU WS and

IT EQ Indemnity Occurrence EBRD

Vermont Mutual Insurance Com-pany

Baldwin Re Ltd . Series 2021-1 Class A $150 .00

CT, ME, MA, NH, NY, RI, and VT: NS, EQ, ST, WF, and other perils events

Indemnity Occurrence MMF

Renaissance Reinsurance Ltd . & DaVinci Reinsurance Ltd .

Mona Lisa Re Ltd . Series 2021-1 Class A $250 .00

NS: US, DC, PR USVI; EQ: US, DC, Canada, PR, USVI

Industry Index

Annual Aggregate MMF

Total $5,614.00

Source: Aon Securities LLC

Exhibit 7: Q2 2021 catastrophe bond issuance (continued)

16

Secondary Market Overview

Q3 2020 Historically, the third quarter of the year is the lightest by

traded volume compared to the rest of the year as primary

issuance halts and investors monitor the waters during

hurricane season . This was true once again as offers were

scarce, especially compared to the prior quarter when

COVID-19 escalated and some investors liquidated pieces

of their ILS portfolios . Because of the low volume of offers,

some investors were more permissive to increase their bids,

and, in some cases, we saw bonds trade at premiums . Over

the course of the quarter, secondary spreads tightened

moderately, a healthy response to the initial widening caused

by COVID-19 . This tightening of spreads was not the case for

every cat bond, as some widened as their aggregate towers

were eroded by the various events this summer including

California Wildfires, Hurricanes Isaias, Laura and Sally, as well

as the derecho in Iowa .

Q4 2020As the primary issuance pipeline picked up after a quiet Q3,

so did the volume of trading, which consistently increased

over the course of the quarter . Secondary spreads continued

to rebound moderately as they reflected the rates achieved

in the primary market . Index based transactions made

up approximately 75% of the new issuances and 45% of

secondary trades in December, despite only representing

approximately one third of the outstanding cat bond market

at the time .

Q1 2021Capital inflows and $2 .06 billion in maturities created a

wave of demand for cat bonds in the first quarter of 2021 .

$2 .57 billion of primary issuances, the third most for a first

quarter in 10 years, could not meet the increasing demand

and investors turned to the secondary market in search of

bonds . Investors were looking to put cash to work, but the

market was mostly one-sided . As the quarter progressed

and the primary market reopened, more offers came and

trading gradually increased, but remained quiet compared

to past quarters . Spreads tightened to levels last seen

in early 2019 and were down approximately 15-20% on

average from last year’s wides that were a result of the initial

COVID-19 outbreak . Some aggregate bonds that had already

seen losses building from past 2020 events traded at large

discounts following the winter storms in Texas, but overall,

the market tightened .

Q2 2021As the issuance pipeline brought twenty transactions, a

near record for the most cat bond issuances in a quarter, the

secondary market began seeing more offers with investors

rebalancing their portfolios . The market consistently saw 20+

trades on a weekly basis starting in mid-April and secondary

spreads followed the tightening seen in the primary market

as trades were often executed through the offer side of most

pricing sheets . Towards the end of June, spreads started to

consolidate around levels last seen in 2018, approximately

15-20% tighter than this time last year . Bonds facing potential

losses from 2020 events saw improved reporting through

the quarter . Some traded as a result of the positive news

while others saw their indicative prices increase to reflect the

positive reports .

ILS Annual Report 2021 17

COVID-19

COVID-19’s coinciding impact to a natural disaster response

from a humanitarian perspective was enormous . World

organizations such as the United Nations (UN) pleaded for

financial support and volunteers to help people in need .

The insurance industry was faced with enormous challenges

in trying to accelerate the claims process while balancing

multiple large-scale disasters, pending litigation from

COVID-19 related incidents, increased replacement costs due

to a disrupted supply chain, and other complex scenarios .

However, the re/insurance industry managed to weather the storm successfully as continued strong capitalization allowed all disasters to be comfortably managed where cover was in place.

Perhaps the biggest takeaway from 2020 was the recognition

of how concurrent events can have major global implications .

These “compounded” or “connected extremes” will provide

critical learning opportunities for better planning as the

world becomes increasingly complex and faces growing

or emerging risks . 2020 also highlighted topics such as the

protection gap to address the underserved, increasingly

vulnerable populations, the need for additional investment

around risk mitigation strategies to navigate new forms of

volatility, and the growing influence from climate change on

daily life .

Source: Aon – Impact Forecasting – Weather, Climate & Catastrophe Insight – 2020 Annual Report

18

71%

4%

16%

10%

Capital Providers Over the past twelve months, many investors accumulated

a considerable amount of fresh capital from maturities and

continued success in capital raising . Particularly, ILS Funds

and Institutional Investors raised significant capital as their

investors continued to focus on the diversifying nature and

liquidity benefits of cat bonds . Together, the two provided

approximately 87% of the total capacity for new issuances

brought to market by Aon Securities during the period under

review and Institutional Investors recorded an increase in

market share from 11% to 16% . Despite reinsurers decreasing

their level of contribution over the past twelve months and

Multi-Strategy Funds’ contribution remaining constant, both

were meaningful supporters of the approximately $13 billion

of new issuances over the last four quarters .

Exhibit 8a and 8b: Investors by category (years ending June 30)

Capital SourcesSwitzerland and France saw their contribution to new

issuances brought to market by Aon Securities increase as

many European UCITS funds continued to be very successful

in their capital raising efforts over the past twelve months .

The US and UK’s contribution remained stable year-over-

year and the “Other” category, encompassing investors from

Canada, Germany, Japan and Sweden, marginally decreased

by a percentage point . Bermuda also saw its market

contribution decrease compared to other countries .

74%4%

11%

11%

ILS Transaction Activity

ILS Fund

Institution Multi-Strat Fund

Reinsurer

ILS Fund

Institution Multi-Strat Fund

Reinsurer

2021

2020

46%9%

23%

6% 8%8%

46%

12%

20%

7% 8%

7%

UK

US France

Bermuda Switzerland Other

UK

US France

Bermuda Switzerland Other

2021

2020

Source: Aon Securities LLC Source: Aon Securities LLC

Exhibit 9a and 9b: Investors by country/region (years ending June 30)

ILS Annual Report 2021 19

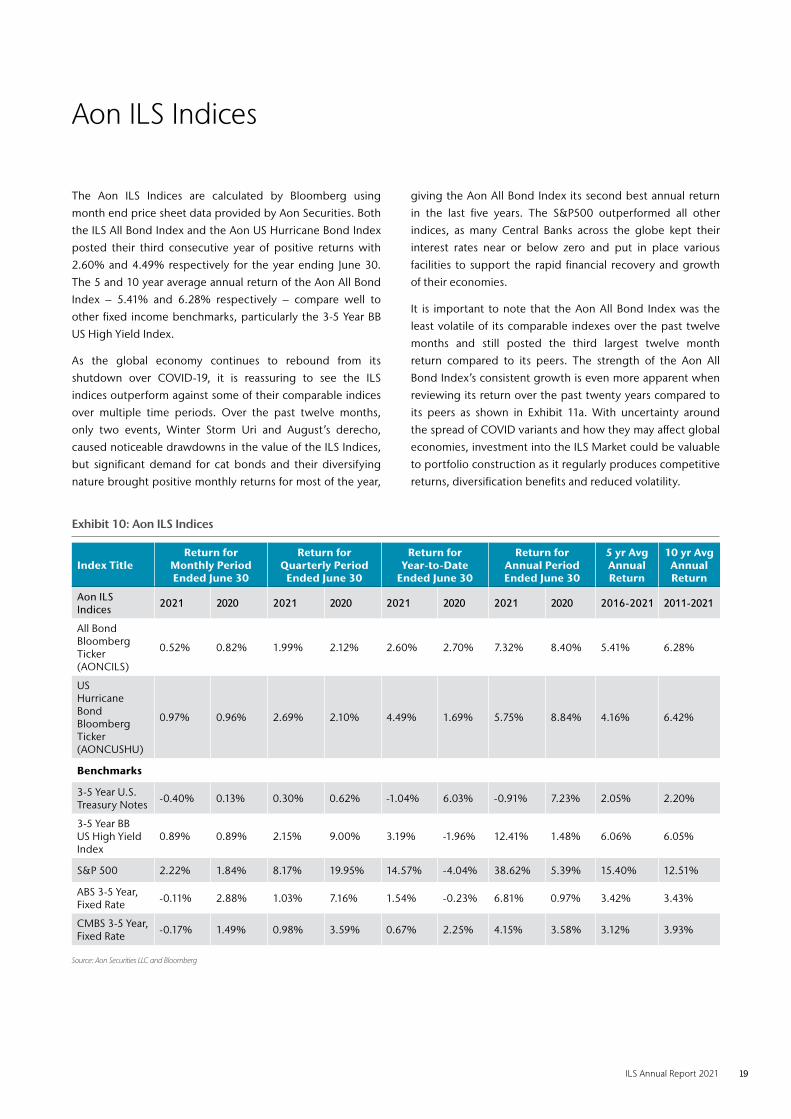

Aon ILS Indices

The Aon ILS Indices are calculated by Bloomberg using

month end price sheet data provided by Aon Securities . Both

the ILS All Bond Index and the Aon US Hurricane Bond Index

posted their third consecutive year of positive returns with

2 .60% and 4 .49% respectively for the year ending June 30 .

The 5 and 10 year average annual return of the Aon All Bond

Index – 5 .41% and 6 .28% respectively – compare well to

other fixed income benchmarks, particularly the 3-5 Year BB

US High Yield Index .

As the global economy continues to rebound from its

shutdown over COVID-19, it is reassuring to see the ILS

indices outperform against some of their comparable indices

over multiple time periods . Over the past twelve months,

only two events, Winter Storm Uri and August’s derecho,

caused noticeable drawdowns in the value of the ILS Indices,

but significant demand for cat bonds and their diversifying

nature brought positive monthly returns for most of the year,

giving the Aon All Bond Index its second best annual return

in the last five years . The S&P500 outperformed all other

indices, as many Central Banks across the globe kept their

interest rates near or below zero and put in place various

facilities to support the rapid financial recovery and growth

of their economies .

It is important to note that the Aon All Bond Index was the

least volatile of its comparable indexes over the past twelve

months and still posted the third largest twelve month

return compared to its peers . The strength of the Aon All

Bond Index’s consistent growth is even more apparent when

reviewing its return over the past twenty years compared to

its peers as shown in Exhibit 11a . With uncertainty around

the spread of COVID variants and how they may affect global

economies, investment into the ILS Market could be valuable

to portfolio construction as it regularly produces competitive

returns, diversification benefits and reduced volatility .

Exhibit 10: Aon ILS Indices

Index TitleReturn for

Monthly PeriodEnded June 30

Return for Quarterly Period

Ended June 30

Return for Year-to-Date

Ended June 30

Return for Annual PeriodEnded June 30

5 yr Avg Annual Return

10 yr Avg Annual Return

Aon ILS Indices 2021 2020 2021 2020 2021 2020 2021 2020 2016-2021 2011-2021

All Bond Bloomberg Ticker (AONCILS)

0 .52% 0 .82% 1 .99% 2 .12% 2 .60% 2 .70% 7 .32% 8 .40% 5 .41% 6 .28%

US Hurricane Bond Bloomberg Ticker (AONCUSHU)

0 .97% 0 .96% 2 .69% 2 .10% 4 .49% 1 .69% 5 .75% 8 .84% 4 .16% 6 .42%

Benchmarks

3-5 Year U .S . Treasury Notes -0 .40% 0 .13% 0 .30% 0 .62% -1 .04% 6 .03% -0 .91% 7 .23% 2 .05% 2 .20%

3-5 Year BB US High Yield Index

0 .89% 0 .89% 2 .15% 9 .00% 3 .19% -1 .96% 12 .41% 1 .48% 6 .06% 6 .05%

S&P 500 2 .22% 1 .84% 8 .17% 19 .95% 14 .57% -4 .04% 38 .62% 5 .39% 15 .40% 12 .51%

ABS 3-5 Year, Fixed Rate -0 .11% 2 .88% 1 .03% 7 .16% 1 .54% -0 .23% 6 .81% 0 .97% 3 .42% 3 .43%

CMBS 3-5 Year, Fixed Rate -0 .17% 1 .49% 0 .98% 3 .59% 0 .67% 2 .25% 4 .15% 3 .58% 3 .12% 3 .93%

Source: Aon Securities LLC and Bloomberg

20

Exhibit 11a: Aon All Bond Index versus financial benchmarks

-50%

50%

150%

250%

350%

450%

550%

650%

Jun-

02

Jun-

03

Jun-

04

Jun-

05

Jun-

06

Jun-

07

Jun-

08

Jun-

09

Jun-

10

Jun-

11

Jun-

12

Jun-

13

Jun-

14

Jun-

15

Jun-

16

Jun-

17

Jun-

18

Jun-

19

Jun-

20

Jun-

21

Source: Aon Securities LLC and Bloomberg

Exhibit 11b: Historical performance of Aon ILS Indices

Source: Aon Securities LLC and Bloomberg

-50%

0%

50%

100%

150%

200%

250%

300%

350%

400%

Dec

-00

Jun-

01D

ec-0

1Ju

n-02

Dec

-02

Jun-

03D

ec-0

3Ju

n-04

Dec

-04

Jun-

05D

ec-0

5Ju

n-06

Dec

-06

Jun-

07D

ec-0

7Ju

n-08

Dec

-08

Jun-

09D

ec-0

9Ju

n-10

Dec

-10

Jun-

11D

ec-1

1Ju

n-12

Dec

-12

Jun-

13D

ec-1

3Ju

n-14

Dec

-14

Jun-

15D

ec-1

5Ju

n-16

Dec

-16

Jun-

17D

ec-1

7Ju

n-18

Dec

-18

Jun-

19D

ec-1

9Ju

n-20

Dec

-20

Jun-

21

Aon ILS Index

AONCUS HU Index

Aon ILS Index

3-5 Yr BB US High Yield Index HFRX Global Hedge Fund Index

S&P 500 Total Return Index

3-5 Yr US Fix ABS ICE BofAML 3-5 Years US Fixed Rate

ILS Annual Report 2021 21

ILS Related Markets

As of H1 2021, Aon estimates the total ILS capital markets

capacity to be $97 billion which is comprised of Collateralized

Reinsurance, Catastrophe Bonds, ILW, and Sidecars . This total

value represents an increase of approximately $3 billion from

last year’s estimate at the time of writing .

Prior to the COVID-19 pandemic outbreak, a large portion of

the ILS investor universe were experiencing favorable capital

positions and positive fund flows; with the success of the

vaccination programs worldwide, investor confidence seems

to have continued where it left off .

The market has bounced back from the impact of recent

natural catastrophe losses and COVID-19 uncertainty, to

show healthy growth in supply . The bond market saw a

record annual issuance in 2020 of around $11 billion, over

double the $5 .4 billion issued in 2019 .

Exhibit 12: Alternative market development

5 7 8 1117

22 19 22 24 28

4450

6472

8089

97 95 94 97

0

10

20

30

40

50

60

70

80

90

100

Lim

it U

SD b

illio

ns

Source: Aon Securities LLC

Exhibit 13: Global reinsurer capital

Source: Individual Company Reports, Aon Reinsurance Solutions, Aon Securities LLC

4%5% 6% 6%

5%6%

9% 9%

11%13%

14%15%

17% 15%

14% 15%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0

100

200

300

400

500

600

700

USD

bill

ion

s

Collateralized Re and Other

Sidecars ILW

Catastrophe Bonds

Traditional Capital

Alternative Capital Share of Total Reinsurance Capital

Alternative Capital

22

Collateralized Reinsurance Market TrendsAon expects the Collateralized Reinsurance segment to

continue to expand, as capital continues to flow into the

sector targeting a variety of strategies . Although the segment

continues to form the largest part of the ILS market by

capacity volume, some investors have allocated additional

capital into more liquid, tradeable instruments .

Investor appetite for collateralized reinsurance can be more

sensitive to loss activity than catastrophe bonds, due to the

propensity for losses at lower return periods .

Funds looking to deploy reinsurance and retrocession

capacity continue to target fronters or establish their own

rated platform with market leading credit ratings, to leverage

the strength of these balance sheets .

Sidecars From H1 2020 to H1 2021, Aon Securities estimates that the

Sidecar market has increased from $6 .8 billion to $8 billion .

Generally, demand from cedents continues to outmatch capital

supply from investors, despite this increase in limit .

The Sidecar market had previously been trending downwards,

with recent catastrophe loss activity and the COVID-19 outbreak

causing further flight from the asset class . However, the impact

of COVID-19 has been diluted due to the stabilisation of loss

positions . The most material impact has been seen in Europe,

where business interruption contractual coverage tended to

be most expansive; thus, Sidecars with limited commercial

European business tended to outperform the market .

One notable development in January 2021 was Peak Re

successfully upsizing their Lion Rock Re Retrocessional Sidecar

from $77 million to $107 million . Still the only Sidecar in Asia,

Lion Rock Re allows Peak Re fluid access to the capital markets .

2021 winter storm Uri, in the southern states of the US, added

material unmodeled loss to a number of Sidecar portfolios,

providing for further discussions between fund managers and

investors . Veteran Sidecar sponsors continued to fortify their

relationships with the capital markets with repeat issuances,

however some were required to compromise on terms to

achieve scale .

Historically, the Sidecar market has been weighted towards

portfolios of reinsurance treaties concentrated in US peak

perils, namely Florida hurricane and California earthquake . As

alternative capital continues to migrate down the risk chain,

many investors are drawn to sharing the underwriting result

of quality writers of globally distributed portfolios, helping to

diversify away from peak peril exposures .

Sidecars continue to offer strategic value to (re)insurer sponsors

by providing a third party capital platform with increasing

benefits over the medium to long-term . Given the ongoing

potential pricing dislocation following the catastrophe events

of the last five years, leveraging all capital sources has become

increasingly important to sponsors . Demand for third party

capital therefore remains strong; however, this materially

outweighs capital supply at the moment .

ILS Annual Report 2021 23

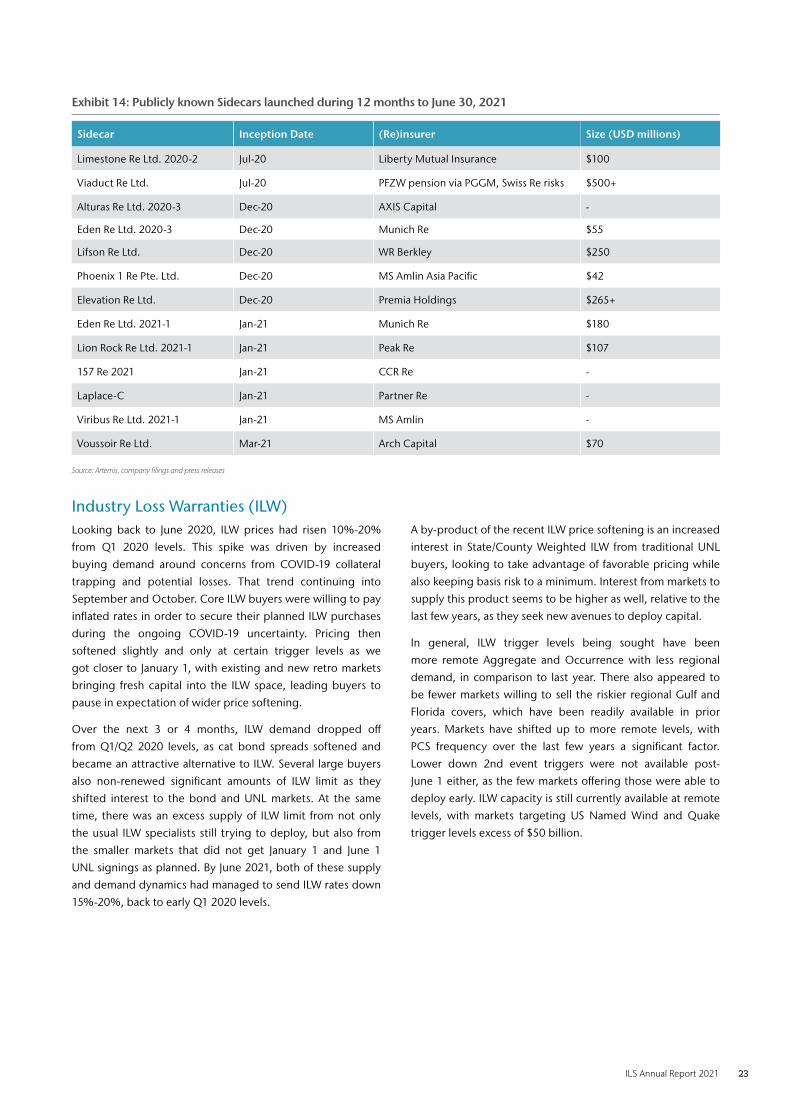

Exhibit 14: Publicly known Sidecars launched during 12 months to June 30, 2021

Sidecar Inception Date (Re)insurer Size (USD millions)

Limestone Re Ltd . 2020-2 Jul-20 Liberty Mutual Insurance $100

Viaduct Re Ltd . Jul-20 PFZW pension via PGGM, Swiss Re risks $500+

Alturas Re Ltd . 2020-3 Dec-20 AXIS Capital -

Eden Re Ltd . 2020-3 Dec-20 Munich Re $55

Lifson Re Ltd . Dec-20 WR Berkley $250

Phoenix 1 Re Pte . Ltd . Dec-20 MS Amlin Asia Pacific $42

Elevation Re Ltd . Dec-20 Premia Holdings $265+

Eden Re Ltd . 2021-1 Jan-21 Munich Re $180

Lion Rock Re Ltd . 2021-1 Jan-21 Peak Re $107

157 Re 2021 Jan-21 CCR Re -

Laplace-C Jan-21 Partner Re -

Viribus Re Ltd . 2021-1 Jan-21 MS Amlin -

Voussoir Re Ltd . Mar-21 Arch Capital $70

Source: Artemis, company filings and press releases

Industry Loss Warranties (ILW)Looking back to June 2020, ILW prices had risen 10%-20%

from Q1 2020 levels . This spike was driven by increased

buying demand around concerns from COVID-19 collateral

trapping and potential losses . That trend continuing into

September and October . Core ILW buyers were willing to pay

inflated rates in order to secure their planned ILW purchases

during the ongoing COVID-19 uncertainty . Pricing then

softened slightly and only at certain trigger levels as we

got closer to January 1, with existing and new retro markets

bringing fresh capital into the ILW space, leading buyers to

pause in expectation of wider price softening .

Over the next 3 or 4 months, ILW demand dropped off

from Q1/Q2 2020 levels, as cat bond spreads softened and

became an attractive alternative to ILW . Several large buyers

also non-renewed significant amounts of ILW limit as they

shifted interest to the bond and UNL markets . At the same

time, there was an excess supply of ILW limit from not only

the usual ILW specialists still trying to deploy, but also from

the smaller markets that did not get January 1 and June 1

UNL signings as planned . By June 2021, both of these supply

and demand dynamics had managed to send ILW rates down

15%-20%, back to early Q1 2020 levels .

A by-product of the recent ILW price softening is an increased

interest in State/County Weighted ILW from traditional UNL

buyers, looking to take advantage of favorable pricing while

also keeping basis risk to a minimum . Interest from markets to

supply this product seems to be higher as well, relative to the

last few years, as they seek new avenues to deploy capital .

In general, ILW trigger levels being sought have been

more remote Aggregate and Occurrence with less regional

demand, in comparison to last year . There also appeared to

be fewer markets willing to sell the riskier regional Gulf and

Florida covers, which have been readily available in prior

years . Markets have shifted up to more remote levels, with

PCS frequency over the last few years a significant factor .

Lower down 2nd event triggers were not available post-

June 1 either, as the few markets offering those were able to

deploy early . ILW capacity is still currently available at remote

levels, with markets targeting US Named Wind and Quake

trigger levels excess of $50 billion .

24

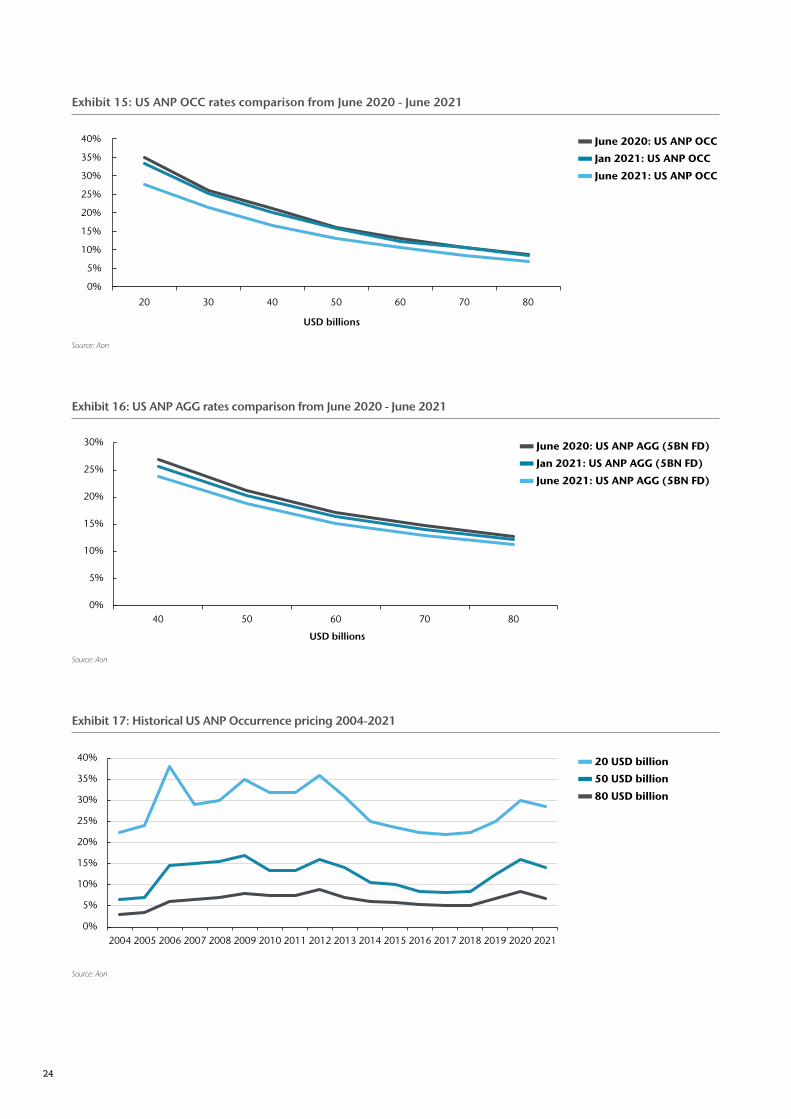

Exhibit 15: US ANP OCC rates comparison from June 2020 - June 2021

0%

5%

10%

15%

20%

25%

30%

35%

40%

20 30 40 50 60 70 80

USD billions

Source: Aon

Exhibit 16: US ANP AGG rates comparison from June 2020 - June 2021

Source: Aon

0%

5%

10%

15%

20%

25%

30%

40 50 60 70 80

USD billions

Exhibit 17: Historical US ANP Occurrence pricing 2004-2021

Source: Aon

0%

5%

10%

15%

20%

25%

30%

35%

40%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

June 2020: US ANP OCC

Jan 2021: US ANP OCC

June 2021: US ANP OCC

June 2020: US ANP AGG (5BN FD)

Jan 2021: US ANP AGG (5BN FD)

June 2021: US ANP AGG (5BN FD)

20 USD billion

50 USD billion

80 USD billion

ILS Annual Report 2021 25

Private Catastrophe Bond PlacementsDuring the first half of 2021, the private placement cat

bond market witnessed a healthy resurgence of utilization

compared to recent years with 16 known deals placed in

the market through the end of June 2021 as compared to 12

deals through a similar time period during 2020 .

There was a record number of privately placed catastrophe

bond transactions issued in the first quarter of 2021 . The

dollar-value of issuance from these deals came in above the

ten-year average for the period .

Hence the market experienced larger issuance sizes for several

deals with the recent $250 million issuance of Artex’s Aquarelle

bonds, and a couple of Hannover Re sponsored Seaside

Re bonds at $40 million and $50 million, respectively . This

incremental shift to larger issuance sizes continues to prove

that syndicated deals are supported in the private market . The

notional limit of these larger syndicated deals through June

of 2021 represented 72% of total volume over that period

compared to 51% of total volume throughout all of 2020 .

Certain sponsors like Hamilton Re migrated from utilizing

ILS private placements in late December 2019 into a more

traditional cat bond format during late 2020 / early 2021 . This

demonstrates that private placements remain a constructive

way for ILS sponsors to incrementally form growing

relationships with the ILS market .

These types of private notes have traded in the secondary

market via trading desks affiliated with the placement agent

as well as independent secondary desks . Typically, investors

who can trade these notes are represented by most if not all

of the dedicated and sophisticated ILS managers operating

within the ecosystem .

Smaller non-syndicated notes also experienced strong

issuance, where many of these bonds are sponsored /

established by either the fund investing in the notes or

through a rated fronting entity providing this service,

within its broader leveraged fronting relationship with the

respective ILS fund . Typically, these notes are smaller in size

below $30 million, but can be larger . The ability to issue

smaller size deals opens the door for additional creative

solutions . For example, the private placement market

embraced ESG issues through a very small $3 million private

issuance (Dunant Re IC) backed by the Danish Red Cross to

cover parametric volcano risk whose payout would benefit

affected communities .

The last half of 2020 and the first half of 2021 provided

continued evidence that collateral extensions related to loss

events continue to work . Like traditional bonds, collateral

can be held beyond the risk maturity if loss occurrences are

approaching the trigger . During 2020, we witnessed quite

a few private bonds within Hannover Re’s Seaside program

extend their maturity to allow for further loss development .

The scheduled maturity for the notes were for January 2021,

and the maturity was extended further into 2021 .

26

Exhibit 18: Private placement notional and deal count (not all known) (years ending June 30)

Source: Artemis

$537$455

$670$797

$498

$662 $711

19

12

19

22

24

28

23

0

5

10

15

20

25

30

0

100

200

300

400

500

600

700

800

900

2015 2016 2017 2018 2019 2020 2021

Dea

l Cou

nt

Not

ion

al U

SD m

illio

ns

Exhibit 19: Private placements (Syndicated vs. Non-syndicated)1 (years ending June 30)

USD

mill

ions

0

10

20

30

40

50

60

70

80

90

100

2021202020192018201720162015

38%

62%

22%

78%

18%

82%

20%

80%

72%

28%

49%

51%

28%

72%

1 Syndicated private placement defined as being a series of notes > $30 million notional Source: Artemis

Syndicated Non-Syndicated

Notional Deal Count (Not All Known)

ILS Annual Report 2021 27

Exhibit 20: Private placement catastrophe bond transactions1

Date Issuer Series Size (USD millions) Trigger Peril

Jul-20 Randolph Re 2020-1 $50 .25 Indemnity California Fire

Jul-20 Eclipse Re Ltd . 2020-03A $16 .59 unknown Unknown Property Cat Risk

Jul-20 Eclipse Re Ltd . 2020-04A $40 .00 unknown Property Cat Risk

Sep-20 ILN SAC Ltd 2020-1 $10 .00 Industry Loss Index US Property Cat Risk

Oct-20 Artex SAC Limited Tenby $30 .00 unknown Property Cat Risk

Oct-20 Eclipse Re Ltd . 2020-06A $20 .00 unknown US Property Cat Risk

Oct-20 Cerulean Re SAC Ltd . 2020-B $12 .60 unknown Property Cat Risk

Jan-21 Seaside Re (Kaith Re) 2021-1 $23 .90 unknown US Property Cat Risk

Jan-21 Seaside Re (Kaith Re) 2021-11 $3 .75 unknown US Property Cat Risk

Jan-21 Seaside Re (Kaith Re) 2021-12 $5 .75 unknown US Property Cat Risk

Jan-21 Seaside Re (Kaith Re) 2021-21 $4 .00 unknown US Property Cat Risk

Jan-21 Seaside Re (Kaith Re) 2021-22 $4 .00 unknown US Property Cat Risk

Jan-21 Seaside Re (Kaith Re) 2021-23 $5 .00 unknown US Property Cat Risk

Jan-21 Seaside Re (Kaith Re) 2021-31 $40 .00 unknown US Property Cat Risk

Jan-21 Seaside Re (Kaith Re) 2021-41 $3 .75 unknown US Property Cat Risk

Jan-21 Seaside Re (Kaith Re) 2021-42 $6 .25 unknown US Property Cat Risk

Jan-21 Seaside Re (Kaith Re) 2021-51 $50 .00 unknown US Property Cat Risk

Jan-21 Eclipse Re Ltd . 2021-01A $80 .00 unknown Property Cat Risk

Mar-21 Dunant Re IC 2021-1 $3 .00 Parametric Volcano

Mar-21 Asago Asago III $18 .30 unknown Japan Earthquake

Apr-21 Eclipse Re Ltd . 2021-02A $8 .70 unknown Property Cat Risk

Apr-21 Isosceles Insurance Ltd . 2021-B1 $25 .00 unknown Property Cat Risk

May-21 Artex SAC Limited Aquarelle $250 .00 unknown Property Cat Risk

1 Note that not all Private Placement transaction information is availableSource: Artemis

28

Environmental, Social and Governance (ESG) & Socially Responsible Investment (SRI)The events of the last 18 months have dramatically

accelerated the shift towards ESG . COVID-19 and the recent

focus on social factors, while extreme temperatures, historic

and catastrophic flooding and political changes have

galvanized action on environmental issues . Indeed, a host of

stakeholders, including investors, insurers, regulatory bodies,

asset managers, and corporate issuers, have all increasingly

embraced ESG factors as part of their risk management

framework .

Drivers of ESG

InvestorsSurveys consistently show that ESG is increasingly important

to institutional investors . For example:

• The Synpulse ESG Market Study6 states that investor demand,