ii - ikkm.edu.my · manakala skor bagi tahap keupayaan asas mengguna aplikasi komputer (skor(2))...

TRANSCRIPT

iiMalaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

iii

MALAYSIAN JOURNAL OF CO-OPERATIVE MANAGEMENT

EDITORIAL BOARD

Chief EditorDr. Sushila Devi Rajaratnam

EditorsRaja Maimon Raja Yusof Hayati Md. Salleh Dr. Jamilah DinNurizah NoordinRahimah Abd Samad

ReviewersProfessor Dr. Ismail Rejab Professor Dr. Mohd. Ghazali MohayidinAssociate Professor Dr. Rosmimah Mohd. RoslinAssociate Professor Dr. Rahmah Mohd. Rashid Associate Professor Syed Mohd. Ghazali Wafa Syed Adwam WafaDr. Ravichandran MoorthyDr. Tam Weng Wah

Editorial Advisory Board MembersIdris Ismail (Co-operative College of Malaysia)Professor Dr. Ismail Rejab (Universiti Teknologi Malaysia) Professor Dr. Mohd. Ghazali Mohayidin (Universiti Putra Malaysia)Ghazali Mohayidin (Universiti Putra Malaysia)Associate Professor Dr. Rosmimah Mohd. Roslin (Universiti Teknologi MARA)Associate Professor Dr. Rahmah Mohd. Rashid (Universiti Teknologi MARA)Associate Professor Syed Mohd. Ghazali Wafa Syed Adwam Wafa(Universiti Kebangsaan Malaysia)Dr. Ravichandran Moorthy (Universiti Kebangsaan Malaysia)Dr. Tam Weng Wah (Jabatan Perdana Menteri)

Managing EditorYusnita Othman

SecretariatHamidah Mohd. JosMohammad Zulkarnain Mohamad ZulkifliSharepah Nur Azirah Shareh Abd Rahman

iiMalaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

iii

CONTENTS

Vol. 5 July 2009 ISSN: 1823-5387

Literasi Komputer dalam Kalangan Anggota Lembaga dan Kakitangan Koperasi di MalaysiaSiti Fatimah Sajadi

1 - 24

Dana Koperasi: Sumber dan Kecenderungan PenggunaanHj Ramlan Kamsin 25 - 42

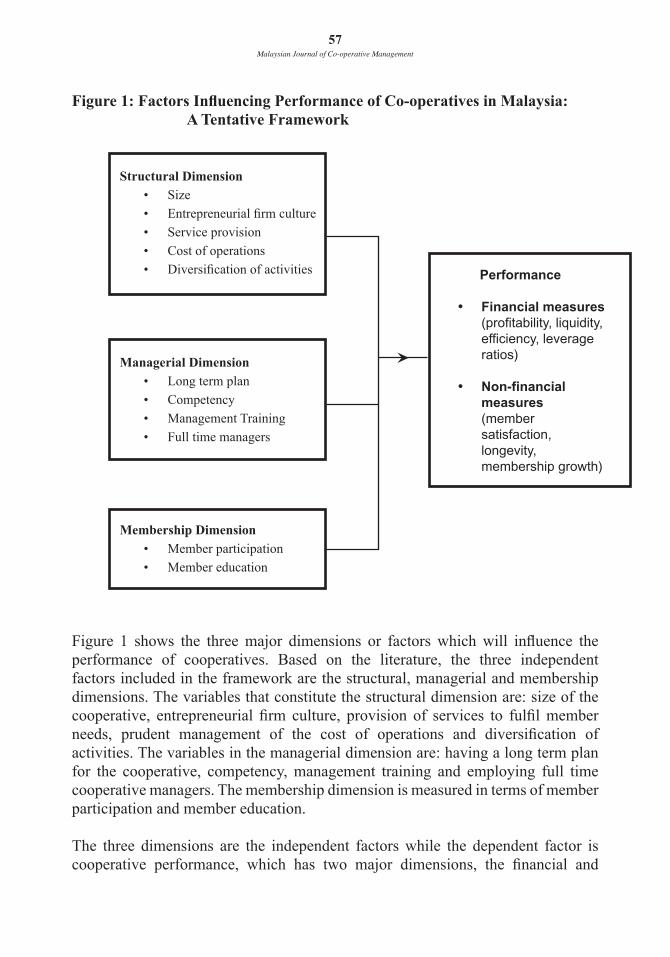

Factors Influencing the Performance of Cooperatives in Malaysia:

A Tentative FrameworkSushila Devi Rajaratnam, Nurizah Noordin, Mohd Shahron Anuar Said,

Rafedah Juhan & Farahaini Mohd Hanif 43 - 63

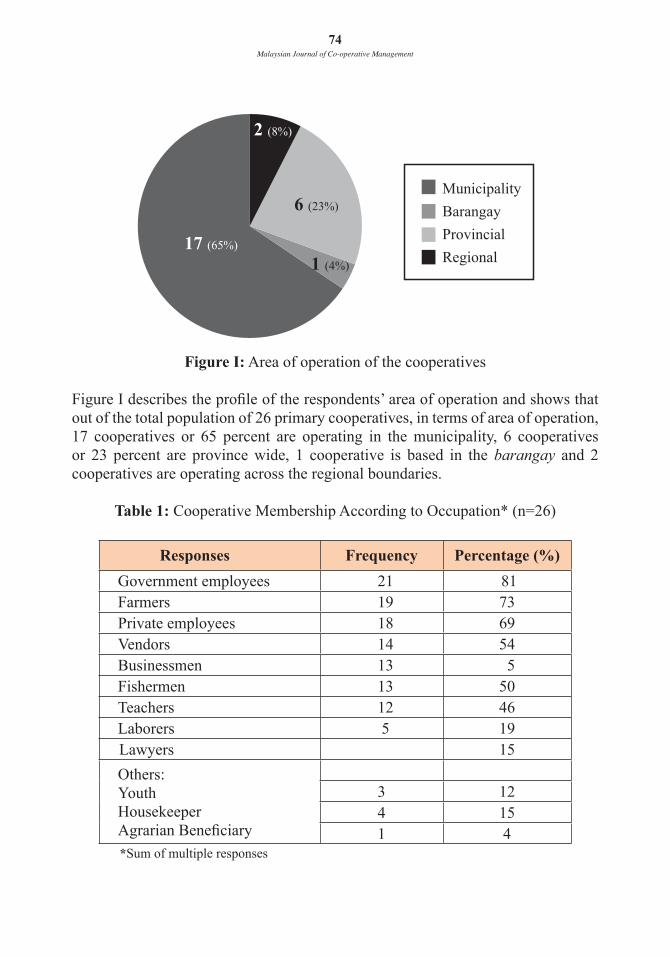

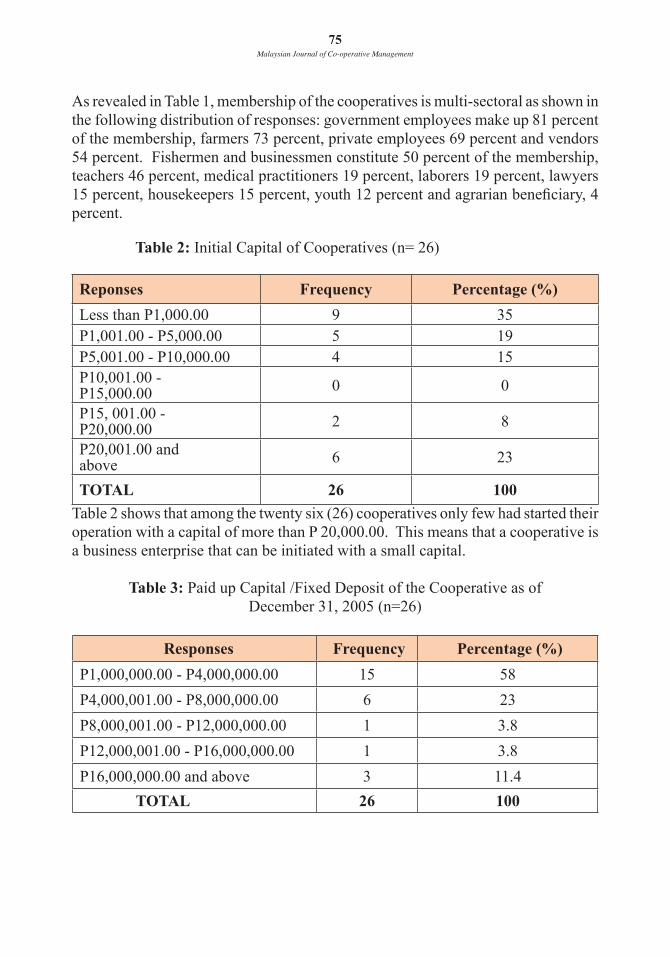

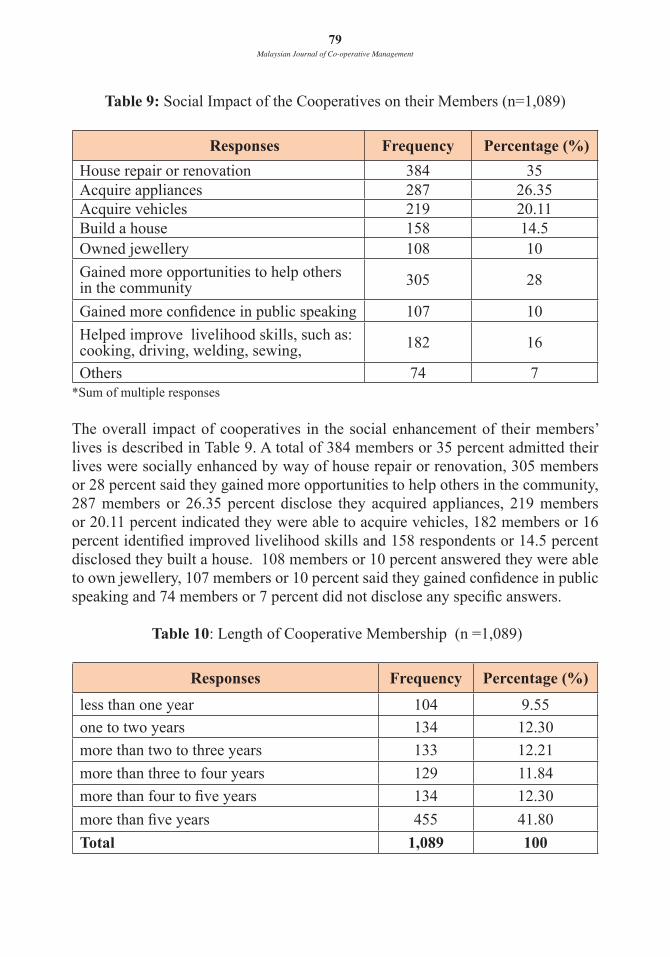

Impact of Negros Oriental Credit Cooperatives and Multipurpose Cooperatives Providing Credit Services on the Socio-Economic Life of their Members: An AssessmentNora Pinero Patron 65 - 82

Malaysian Journal of Co-operative Management1

Malaysian Journal of Co-operative Management1

LITERASI KOMPUTER DALAM KALANGAN ANGGOTA LEMBAGA DAN KAKITANGAN

KOPERASI DI MALAYSIA

Siti Fatimah Sajadi Maktab Kerjasama Malaysia

(Co-operative College of Malaysia)

ABSTRACT

This study identified the level of computer literacy among board members and

employees of cooperatives in Malaysia as well as some of the factors that influenced

their level of computer literacy. The study targeted all cooperatives in Malaysia,

excluding school cooperatives, which had at least one administrative employee.

A total of 619 cooperatives were identified and questionnaires were mailed to

the respondents who were board members and employees in these cooperatives.

Respondents’ perceptions based on a 5-point Likert scale was used to gauge their

level of computer literacy.

Overall, the study revealed that 49% of the employees and board members who

responded had high level of computer literacy. Computer literacy was higher

among employee respondents as compared to the board members who responded.

In addition, the factors which influenced the level of computer literacy were

gender, age, educational level, computer ownership, experience in computer usage,

attending computer courses and work experience. The study found that the level

of computer literacy was higher among respondents who were women, less than 35

years old, possessed high educational qualification, with prior work experience,

owned a computer, were experienced in computer usage and had attended computer

courses.

2Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

3

ABSTRAK

Kajian ini mengenal pasti tahap literasi komputer di kalangan Ahli Lembaga Koperasi (ALK) dan kakitangan koperasi di Malaysia serta mengkaji faktor-faktor yang mempengaruhi tahap literasi komputer di kalangan ALK dan kakitangan koperasi. Sasaran kajian ini adalah kesemua koperasi di Malaysia kecuali koperasi sekolah dan koperasi mempunyai sekurang-kurangnya seorang kakitangan pentadbiran. Sebanyak 619 koperasi telah dikenal pasti dan borang soal selidik telah dihantar secara pos kepada responden yang merupakan ALK dan kakitangan di koperasi. Persepsi responden terhadap tahap literasi komputer mereka diukur berdasarkan kepada Skala Likert Lima Titik.

Secara keseluruhannya, kajian ini menunjukkan 49% responden di kalangan ALK dan kakitangan koperasi mempunyai tahap literasi komputer yang tinggi yang mana kakitangan koperasi memiliki tahap literasi komputer yang lebih tinggi berbanding dengan ALK. Selain itu, faktor-faktor yang mempengaruhi tahap literasi komputer terdiri daripada jantina, umur, tahap pendidikan, pemilikan komputer, pengalaman menggunakan komputer, kehadiran ke kursus komputer dan pengalaman kerja. Kajian ini turut mendapati tahap literasi komputer yang tinggi adalah di kalangan perempuan, golongan muda yang berusia 35 tahun ke bawah, memiliki kelulusan pendidikan tinggi, mempunyai pengalaman kerja, memiliki komputer, mempunyai pengalaman menggunakan komputer dan telah menghadiri kursus komputer.

PENGENALAN

Di Malaysia, kerajaan mempunyai wawasan agar sektor koperasi menjadi sektor ketiga selepas sektor awam dan swasta dalam menyumbang kepada pembangunan ekonomi negara menjelang tahun 2010 (Mohamed Khalid Nordin, 2007). Dalam gerakan koperasi pula, Anggota Lembaga Koperasi (ALK) dan kakitangan koperasi merupakan tonggak utama yang memberi sumbangan secara langsung kepada kejayaan sesuatu koperasi. Untuk memastikan gerakan koperasi terus maju dan dapat bersaing dengan sektor yang lain, koperasi memerlukan ALK dan kakitangan yang berilmu pengetahuan dan mempunyai kompetensi atau kemahiran tertentu. Kini, di era maklumat, pengetahuan dan kemahiran asas komputer merupakan antara syarat untuk ALK dan kakitangan memperoleh ilmu dan menjalankan kerja dengan efisien dan berkesan.

2Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

3

Rasional Kajian Dasar-dasar ICT adalah antara dasar-dasar yang diberikan penumpuan khusus oleh kerajaan Malaysia dalam meningkatkan prestasi serta pembangunan negara. Dalam era ekonomi berasaskan pengetahuan kini, tenaga kerja perlu melengkapkan diri dengan kemahiran teknologi untuk bersaing di persekitaran global dan mampu menggunakan ICT untuk meningkatkan produktiviti (Abdul Manaf Bohari,2006).

Di koperasi, tugas-tugas pentadbiran secara manual seperti surat menyurat, laporan, book keeping, kerja-kerja pengurusan fail, dan lain-lain tugas perkeranian akan lebih lancar jika dilaksanakan menggunakan komputer. Penggunaan sistem-sistem komputer seperti sistem keanggotaan, sistem kewangan dan sebagainya juga perlu di dalam melancarkan kerja-kerja pentadbiran dan pengurusan di sesebuah organisasi (termasuk koperasi).Koperasi yang tidak mengikut perkembangan teknologi akan tertinggal ke belakang dan tidak akan mampu bersaing dalam keadaan semasa yang kompetitif. Dengan senario semasa ini, timbul persoalan sama ada ALK dan kakitangan koperasi mempunyai kemahiran komputer demi memastikan koperasi mampu berdaya saing dan berdaya maju sehingga seterusnya mencapai wawasan kerajaan supaya koperasi menjadi sektor ketiga dalam pembangunan ekonomi negara. Justeru, adalah wajar menjalankan kajian ini bagi mengetahui tahap literasi asas komputer ALK dan kakitangan koperasi yang meliputi pengetahuan dan kemahiran asas dalam menggunakan komputer.

Objektif Kajian

Kajian ini bertujuan untuk menilai tahap literasi komputer dalam kalangan ALK dan kakitangan koperasi. Di samping itu, kajian ini juga bertujuan mengenal pasti faktor-faktor yang mempengaruhi tahap literasi komputer ALK dan kakitangan koperasi.

SOROTAN KAJIAN

Terdapat banyak kaedah digunakan oleh penyelidik untuk mengukur tahap literasi komputer berdasarkan kemajuan teknologi apabila komputer mikro mula digunakan (Aienlyetal., 2000). Du (2004), telah menggunakan soal selidik berasaskan web iaitu Computer Skill and Use Assessment untuk mengukur kompetensi komputer pelajar baru bagi kursus jarak jauh di Mid-Southwestern State Universitiy di Amerika Syarikat. Smith (2004) menggunakan Computer Self-Efficacy Assessment (CSEA) untuk mengkaji tahap literasi komputer pelajar dengan mengukur tahap keyakinan dalam melakukan tugas-tugas menggunakan komputer.

4Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

5

Selain itu, Connelly (2003) telah mencipta satu pengukuran literasi komputer berbentuk ujian iaitu Computer Literacy Measure For Prospective Employees (CLMPE) terhadap pelajar, graduan dan bukan pelajar di Austin State University untuk membantu industri kecil mengenal pasti dan memilih bakal pekerja mereka.

Dickerson (2005) pula telah menggunakan ujian atas talian iaitu Skills Assessment Manager (SAM) oleh Thomson Course Technology untuk mengkaji tahap literasi pelajar baru University of North Carolina.

Meckelborg (2003) telah mengkaji keberkesanan mengukur tahap literasi komputer berdasarkan empat kaedah ukuran; (1) soal selidik pengalaman komputer, (2) soal selidik mengenai vocabulary dengan penilaian sendiri, (3) soal selidik kemahiran komputer dengan penilaian sendiri dan (4) ujian pengetahuan secara bertulis. Hasil analisis, beliau mendapati semua kaedah pengukuran yang digunakan adalah sangat berkesan (nilai kebolehpercayaan tinggi).

Sehubungan itu, kajian ini menggunakan soal selidik dengan Skala Likert Lima Titik untuk mengukur tahap literasi komputer dengan merujuk kepada aspek-aspek (1) pengetahuan asas mengenai ciri-ciri dan keupayaan komputer, (2) keupayaan mengguna aplikasi komputer tertentu dan (3) keupayaan menggunakan komputer untuk melaksanakan tugas-tugas tertentu di koperasi.

METODOLOGI KAJIAN

Data kajian dikumpulkan menggunakan borang soal selidik yang diisi sendiri oleh responden yang terdiri daripada ALK dan kakitangan pentadbiran koperasi. Koperasi sasaran ialah koperasi dewasa (bukan koperasi sekolah) dan mempunyai sekurang-kurangnya seorang kakitangan pentadbiran. Sebanyak 619 buah koperasi memenuhi kriteria tersebut. Bagi setiap koperasi, seramai enam ALK dan antara seorang hingga sepuluh orang kakitangan dipilih sebagai responden. Kajian ini adalah berdasarkan data dari Jabatan Pembangunan Koperasi (kini Suruhanjaya Koperasi Malaysia) yang dikemas kini sehingga 31 Disember 2006. Analisis kajian ini pula berasaskan penilaian diri sendiri (persepsi) responden.

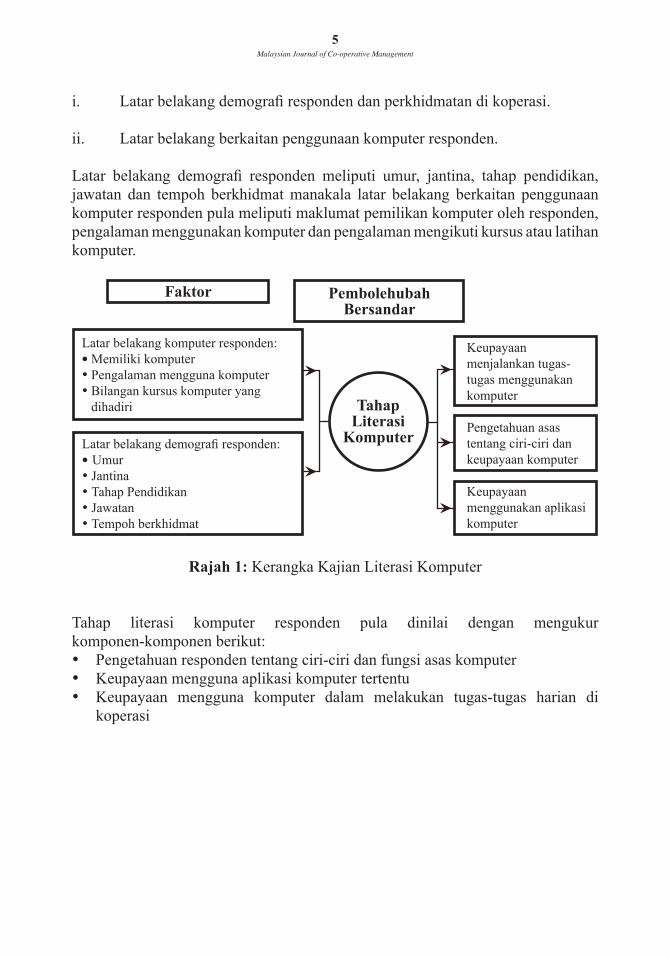

Kerangka Kajian

Kerangka kajian ini yang dirumuskan dalam Rajah 1 disesuaikan daripada kajian-kajian terdahulu. Diandaikan literasi komputer mempunyai hubung kait dengan dua faktor berikut:

4Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

5

i. Latar belakang demografi responden dan perkhidmatan di koperasi.

ii. Latar belakang berkaitan penggunaan komputer responden.

Latar belakang demografi responden meliputi umur, jantina, tahap pendidikan, jawatan dan tempoh berkhidmat manakala latar belakang berkaitan penggunaan komputer responden pula meliputi maklumat pemilikan komputer oleh responden, pengalaman menggunakan komputer dan pengalaman mengikuti kursus atau latihan komputer.

Rajah 1: Kerangka Kajian Literasi Komputer

Tahap literasi komputer responden pula dinilai dengan mengukur komponen-komponen berikut:• Pengetahuan responden tentang ciri-ciri dan fungsi asas komputer• Keupayaan mengguna aplikasi komputer tertentu• Keupayaan mengguna komputer dalam melakukan tugas-tugas harian di

koperasi

Faktor PembolehubahBersandar

Latar belakang komputer responden:• Memiliki komputer•Pengalaman mengguna komputer•Bilangan kursus komputer yang

dihadiri

Latar belakang demografi responden:• Umur•Jantina•Tahap Pendidikan•Jawatan•Tempoh berkhidmat

Keupayaan menjalankan tugas-tugas menggunakan komputer

Pengetahuan asas tentang ciri-ciri dan keupayaan komputer

Keupayaan menggunakan aplikasi komputer

TahapLiterasi

Komputer

6Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

7

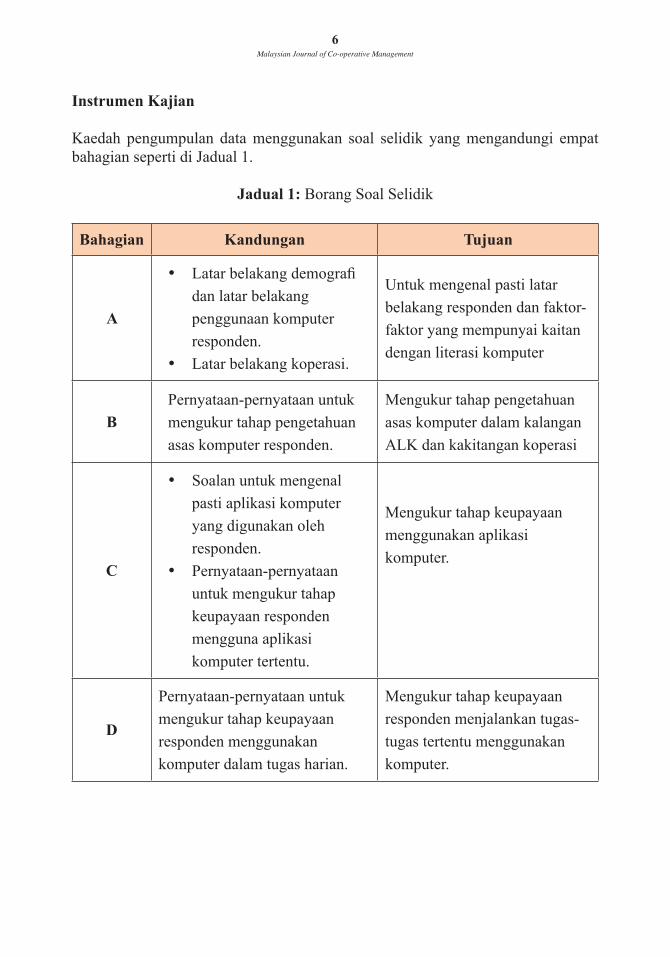

Instrumen Kajian

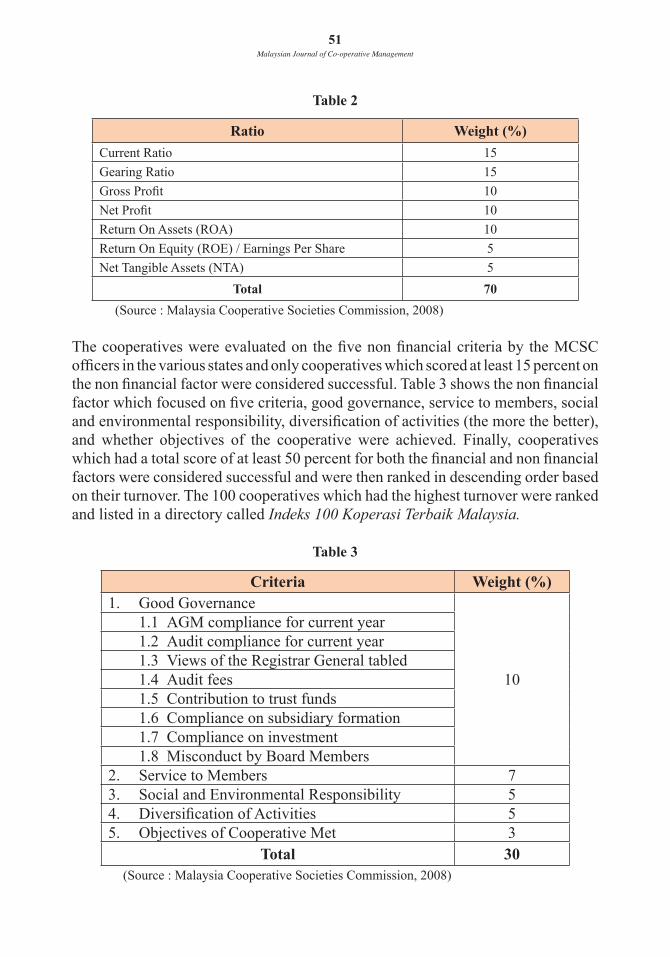

Kaedah pengumpulan data menggunakan soal selidik yang mengandungi empat bahagian seperti di Jadual 1.

Jadual 1: Borang Soal Selidik

Bahagian Kandungan Tujuan

A

• Latar belakang demografi

dan latar belakang

penggunaan komputer

responden.

• Latar belakang koperasi.

Untuk mengenal pasti latar

belakang responden dan faktor-

faktor yang mempunyai kaitan

dengan literasi komputer

BPernyataan-pernyataan untuk

mengukur tahap pengetahuan

asas komputer responden.

Mengukur tahap pengetahuan

asas komputer dalam kalangan

ALK dan kakitangan koperasi

C

• Soalan untuk mengenal

pasti aplikasi komputer

yang digunakan oleh

responden.

• Pernyataan-pernyataan

untuk mengukur tahap

keupayaan responden

mengguna aplikasi

komputer tertentu.

Mengukur tahap keupayaan

menggunakan aplikasi

komputer.

D

Pernyataan-pernyataan untuk

mengukur tahap keupayaan

responden menggunakan

komputer dalam tugas harian.

Mengukur tahap keupayaan

responden menjalankan tugas-

tugas tertentu menggunakan

komputer.

6Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

7

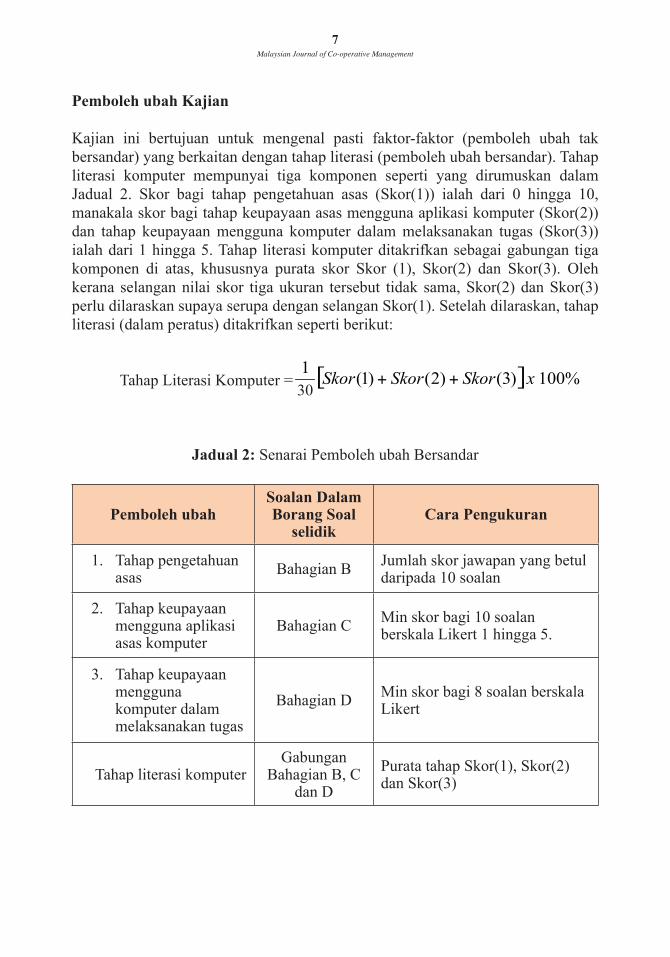

Pemboleh ubah Kajian

Kajian ini bertujuan untuk mengenal pasti faktor-faktor (pemboleh ubah tak bersandar) yang berkaitan dengan tahap literasi (pemboleh ubah bersandar). Tahap literasi komputer mempunyai tiga komponen seperti yang dirumuskan dalam Jadual 2. Skor bagi tahap pengetahuan asas (Skor(1)) ialah dari 0 hingga 10, manakala skor bagi tahap keupayaan asas mengguna aplikasi komputer (Skor(2)) dan tahap keupayaan mengguna komputer dalam melaksanakan tugas (Skor(3)) ialah dari 1 hingga 5. Tahap literasi komputer ditakrifkan sebagai gabungan tiga komponen di atas, khususnya purata skor Skor (1), Skor(2) dan Skor(3). Oleh kerana selangan nilai skor tiga ukuran tersebut tidak sama, Skor(2) dan Skor(3) perlu dilaraskan supaya serupa dengan selangan Skor(1). Setelah dilaraskan, tahap literasi (dalam peratus) ditakrifkan seperti berikut:

Tahap Literasi Komputer = [ ] %100)3()2()1(301

xSkorSkorSkor ++

Jadual 2: Senarai Pemboleh ubah Bersandar

Pemboleh ubahSoalan Dalam Borang Soal

selidikCara Pengukuran

1. Tahap pengetahuan asas Bahagian B Jumlah skor jawapan yang betul

daripada 10 soalan

2. Tahap keupayaan mengguna aplikasi asas komputer

Bahagian C Min skor bagi 10 soalan berskala Likert 1 hingga 5.

3. Tahap keupayaan mengguna komputer dalam melaksanakan tugas

Bahagian D Min skor bagi 8 soalan berskala Likert

Tahap literasi komputerGabungan

Bahagian B, C dan D

Purata tahap Skor(1), Skor(2) dan Skor(3)

30

8Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

9

ANALISIS KAJIAN

Analisis Demografi Responden

Sebanyak 2,040 (35%) borang soal selidik daripada sejumlah 5,837 telah dikembalikan. Walaupun bilangan responden ALK (1,164 orang – 57%) melebihi bilangan responden kakitangan (862 orang - 42.3%, dan 14 orang - 0.7% tidak menyatakan jawatan), namun kadar maklum balas kakitangan (38.6%) lebih baik berbanding ALK (32.7%). Secara keseluruhannya, majoriti responden adalah lelaki (62.1%), berketurunan Melayu (87.3%) dan berpendidikan paling tinggi Sijil Pelajaran Malaysia (SPM) (65.2%). Didapati juga lebih separuh (55.5%) berusia 45 tahun ke atas dan telah berkhidmat dengan koperasi masing-masing kurang daripada 10 tahun (53.5%). Lebih separuh (56.8%) responden memiliki komputer, berpengalaman menggunakan komputer sekurang-kurangnya 10 tahun (50.2%) dan paling ramai memperoleh kemahiran secara tidak formal (35.7% semasa bekerja, diikuti dengan 33.1% belajar sendiri dan 18.7% belajar dari rakan).

Ciri-ciri demografi responden ALK agak berbeza dengan kakitangan. Didapati majoriti responden ALK adalah lelaki, manakala majoriti dalam kalangan responden kakitangan adalah perempuan. Secara purata pula, responden ALK jauh lebih berusia dan mempunyai tahap pendidikan lebih rendah berbanding responden kakitangan.

Tahap Literasi Komputer

Tahap Literasi Komputer Keseluruhan

Skor bagi tahap literasi komputer merupakan gabungan skor daripada Bahagian B, C dan D soal selidik yang telah dibincangkan secara berasingan di atas. Skor setiap bahagian dilaraskan supaya mempunyai pemberat yang sama apabila digabungkan. Ia diukur dalam bentuk peratus dan untuk tujuan perbandingan dipecahkan kepada lima kategori seperti dalam Jadual 3.

8Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

9

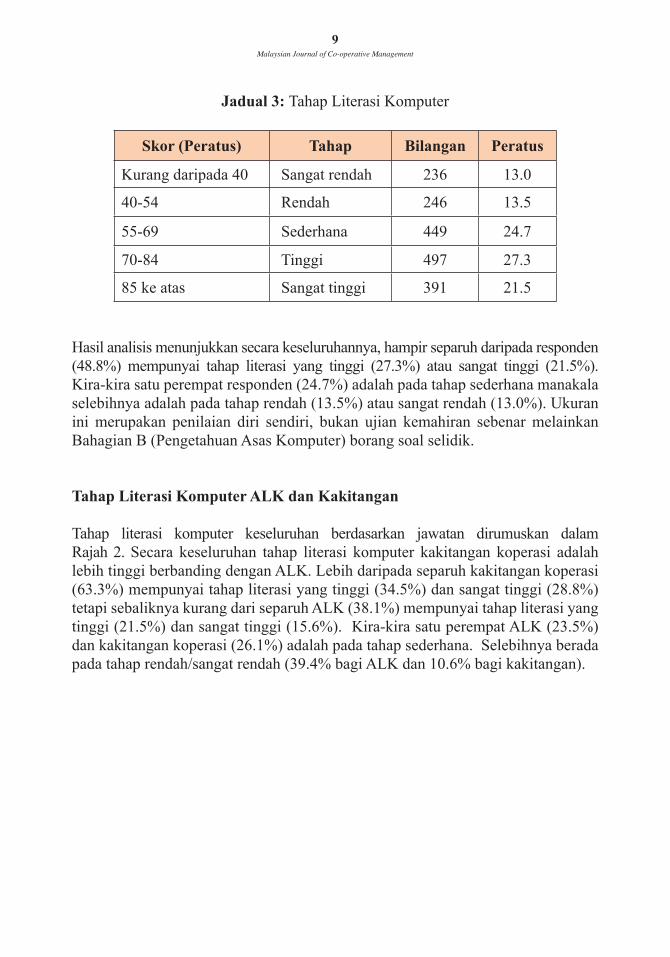

Jadual 3: Tahap Literasi Komputer

Skor (Peratus) Tahap Bilangan Peratus

Kurang daripada 40 Sangat rendah 236 13.0

40-54 Rendah 246 13.5

55-69 Sederhana 449 24.7

70-84 Tinggi 497 27.3

85 ke atas Sangat tinggi 391 21.5

Hasil analisis menunjukkan secara keseluruhannya, hampir separuh daripada responden (48.8%) mempunyai tahap literasi yang tinggi (27.3%) atau sangat tinggi (21.5%). Kira-kira satu perempat responden (24.7%) adalah pada tahap sederhana manakala selebihnya adalah pada tahap rendah (13.5%) atau sangat rendah (13.0%). Ukuran ini merupakan penilaian diri sendiri, bukan ujian kemahiran sebenar melainkan Bahagian B (Pengetahuan Asas Komputer) borang soal selidik.

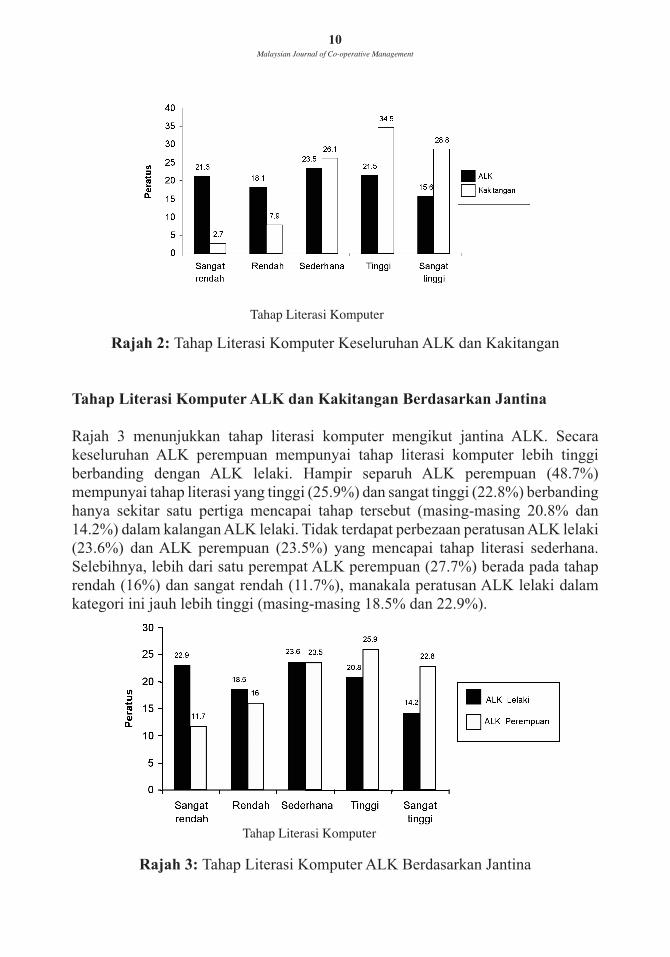

Tahap Literasi Komputer ALK dan Kakitangan

Tahap literasi komputer keseluruhan berdasarkan jawatan dirumuskan dalam Rajah 2. Secara keseluruhan tahap literasi komputer kakitangan koperasi adalah lebih tinggi berbanding dengan ALK. Lebih daripada separuh kakitangan koperasi (63.3%) mempunyai tahap literasi yang tinggi (34.5%) dan sangat tinggi (28.8%) tetapi sebaliknya kurang dari separuh ALK (38.1%) mempunyai tahap literasi yang tinggi (21.5%) dan sangat tinggi (15.6%). Kira-kira satu perempat ALK (23.5%) dan kakitangan koperasi (26.1%) adalah pada tahap sederhana. Selebihnya berada pada tahap rendah/sangat rendah (39.4% bagi ALK dan 10.6% bagi kakitangan).

10Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

11

Rajah 2: Tahap Literasi Komputer Keseluruhan ALK dan Kakitangan

Tahap Literasi Komputer ALK dan Kakitangan Berdasarkan Jantina

Rajah 3 menunjukkan tahap literasi komputer mengikut jantina ALK. Secara keseluruhan ALK perempuan mempunyai tahap literasi komputer lebih tinggi berbanding dengan ALK lelaki. Hampir separuh ALK perempuan (48.7%) mempunyai tahap literasi yang tinggi (25.9%) dan sangat tinggi (22.8%) berbanding hanya sekitar satu pertiga mencapai tahap tersebut (masing-masing 20.8% dan 14.2%) dalam kalangan ALK lelaki. Tidak terdapat perbezaan peratusan ALK lelaki (23.6%) dan ALK perempuan (23.5%) yang mencapai tahap literasi sederhana. Selebihnya, lebih dari satu perempat ALK perempuan (27.7%) berada pada tahap rendah (16%) dan sangat rendah (11.7%), manakala peratusan ALK lelaki dalam kategori ini jauh lebih tinggi (masing-masing 18.5% dan 22.9%).

Rajah 3: Tahap Literasi Komputer ALK Berdasarkan Jantina

Tahap Literasi Komputer

Tahap Literasi Komputer

10Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

11

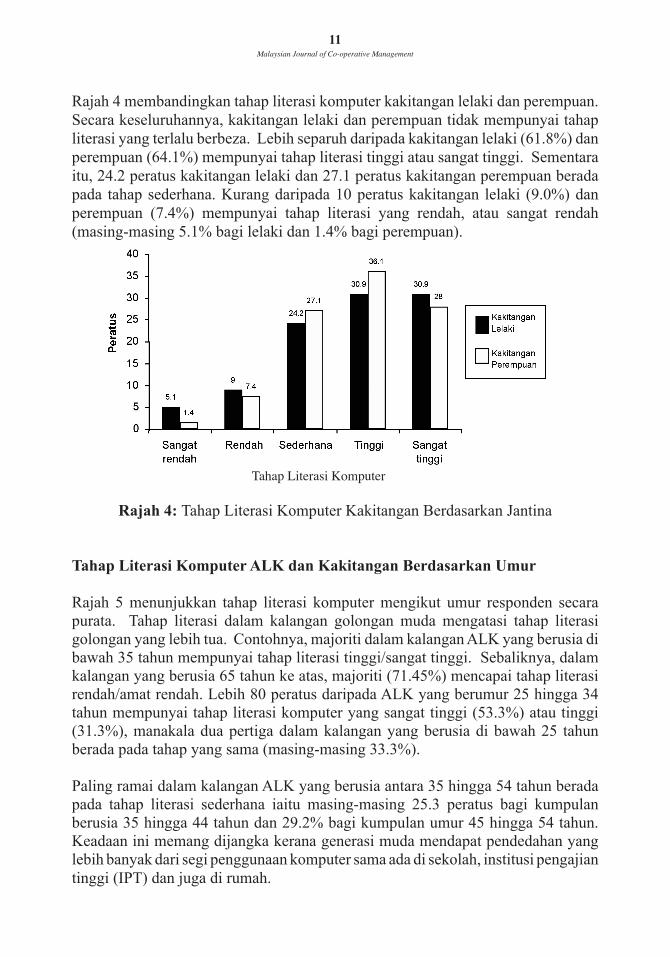

Rajah 4 membandingkan tahap literasi komputer kakitangan lelaki dan perempuan. Secara keseluruhannya, kakitangan lelaki dan perempuan tidak mempunyai tahap literasi yang terlalu berbeza. Lebih separuh daripada kakitangan lelaki (61.8%) dan perempuan (64.1%) mempunyai tahap literasi tinggi atau sangat tinggi. Sementara itu, 24.2 peratus kakitangan lelaki dan 27.1 peratus kakitangan perempuan berada pada tahap sederhana. Kurang daripada 10 peratus kakitangan lelaki (9.0%) dan perempuan (7.4%) mempunyai tahap literasi yang rendah, atau sangat rendah (masing-masing 5.1% bagi lelaki dan 1.4% bagi perempuan).

Rajah 4: Tahap Literasi Komputer Kakitangan Berdasarkan Jantina

Tahap Literasi Komputer ALK dan Kakitangan Berdasarkan Umur

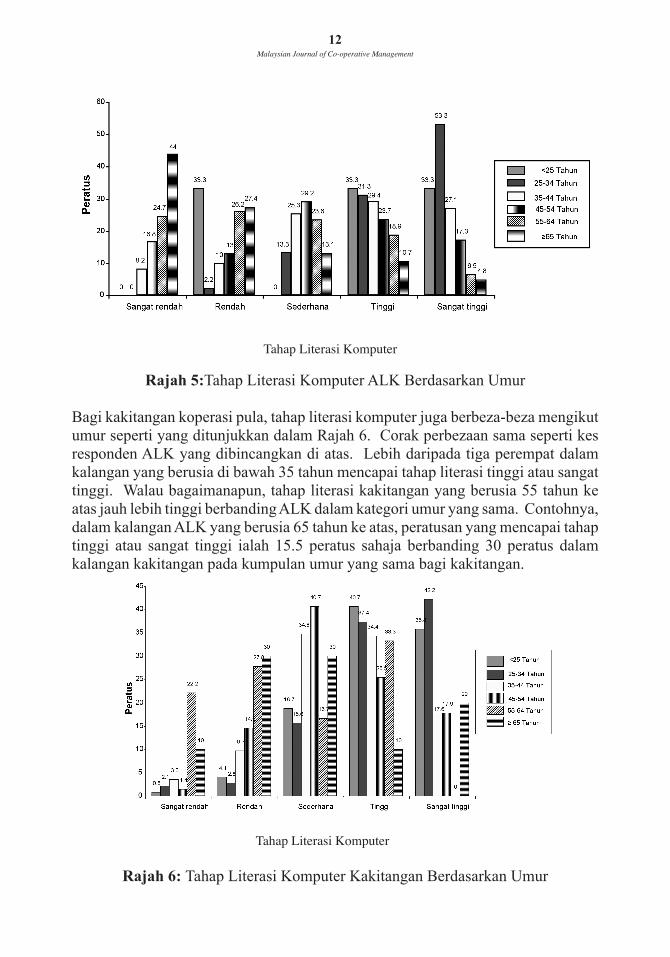

Rajah 5 menunjukkan tahap literasi komputer mengikut umur responden secara purata. Tahap literasi dalam kalangan golongan muda mengatasi tahap literasi golongan yang lebih tua. Contohnya, majoriti dalam kalangan ALK yang berusia di bawah 35 tahun mempunyai tahap literasi tinggi/sangat tinggi. Sebaliknya, dalam kalangan yang berusia 65 tahun ke atas, majoriti (71.45%) mencapai tahap literasi rendah/amat rendah. Lebih 80 peratus daripada ALK yang berumur 25 hingga 34 tahun mempunyai tahap literasi komputer yang sangat tinggi (53.3%) atau tinggi (31.3%), manakala dua pertiga dalam kalangan yang berusia di bawah 25 tahun berada pada tahap yang sama (masing-masing 33.3%).

Paling ramai dalam kalangan ALK yang berusia antara 35 hingga 54 tahun berada pada tahap literasi sederhana iaitu masing-masing 25.3 peratus bagi kumpulan berusia 35 hingga 44 tahun dan 29.2% bagi kumpulan umur 45 hingga 54 tahun. Keadaan ini memang dijangka kerana generasi muda mendapat pendedahan yang lebih banyak dari segi penggunaan komputer sama ada di sekolah, institusi pengajian tinggi (IPT) dan juga di rumah.

Tahap Literasi Komputer

12Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

13

Rajah 5:Tahap Literasi Komputer ALK Berdasarkan Umur

Bagi kakitangan koperasi pula, tahap literasi komputer juga berbeza-beza mengikut umur seperti yang ditunjukkan dalam Rajah 6. Corak perbezaan sama seperti kes responden ALK yang dibincangkan di atas. Lebih daripada tiga perempat dalam kalangan yang berusia di bawah 35 tahun mencapai tahap literasi tinggi atau sangat tinggi. Walau bagaimanapun, tahap literasi kakitangan yang berusia 55 tahun ke atas jauh lebih tinggi berbanding ALK dalam kategori umur yang sama. Contohnya, dalam kalangan ALK yang berusia 65 tahun ke atas, peratusan yang mencapai tahap tinggi atau sangat tinggi ialah 15.5 peratus sahaja berbanding 30 peratus dalam kalangan kakitangan pada kumpulan umur yang sama bagi kakitangan.

Rajah 6: Tahap Literasi Komputer Kakitangan Berdasarkan Umur

Tahap Literasi Komputer

Tahap Literasi Komputer

12Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

13

Tahap Literasi Komputer ALK dan Kakitangan Berdasarkan Tahap Pendidikan

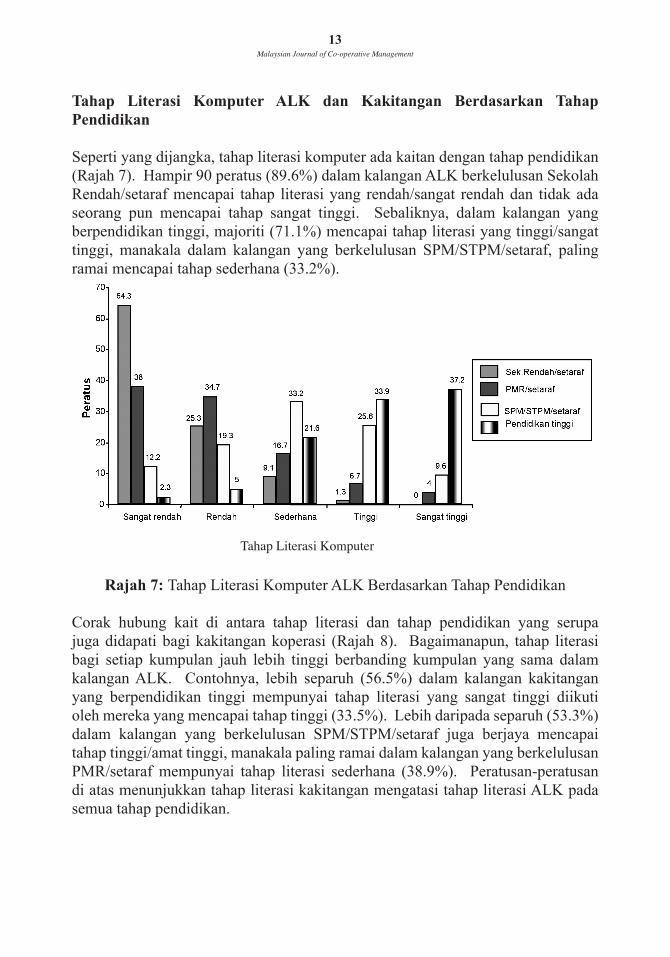

Seperti yang dijangka, tahap literasi komputer ada kaitan dengan tahap pendidikan (Rajah 7). Hampir 90 peratus (89.6%) dalam kalangan ALK berkelulusan Sekolah Rendah/setaraf mencapai tahap literasi yang rendah/sangat rendah dan tidak ada seorang pun mencapai tahap sangat tinggi. Sebaliknya, dalam kalangan yang berpendidikan tinggi, majoriti (71.1%) mencapai tahap literasi yang tinggi/sangat tinggi, manakala dalam kalangan yang berkelulusan SPM/STPM/setaraf, paling ramai mencapai tahap sederhana (33.2%).

Rajah 7: Tahap Literasi Komputer ALK Berdasarkan Tahap Pendidikan

Corak hubung kait di antara tahap literasi dan tahap pendidikan yang serupa juga didapati bagi kakitangan koperasi (Rajah 8). Bagaimanapun, tahap literasi bagi setiap kumpulan jauh lebih tinggi berbanding kumpulan yang sama dalam kalangan ALK. Contohnya, lebih separuh (56.5%) dalam kalangan kakitangan yang berpendidikan tinggi mempunyai tahap literasi yang sangat tinggi diikuti oleh mereka yang mencapai tahap tinggi (33.5%). Lebih daripada separuh (53.3%) dalam kalangan yang berkelulusan SPM/STPM/setaraf juga berjaya mencapai tahap tinggi/amat tinggi, manakala paling ramai dalam kalangan yang berkelulusan PMR/setaraf mempunyai tahap literasi sederhana (38.9%). Peratusan-peratusan di atas menunjukkan tahap literasi kakitangan mengatasi tahap literasi ALK pada semua tahap pendidikan.

Tahap Literasi Komputer

14Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

15

Rajah 8: Tahap Literasi Komputer Kakitangan Berdasarkan Tahap Pendidikan

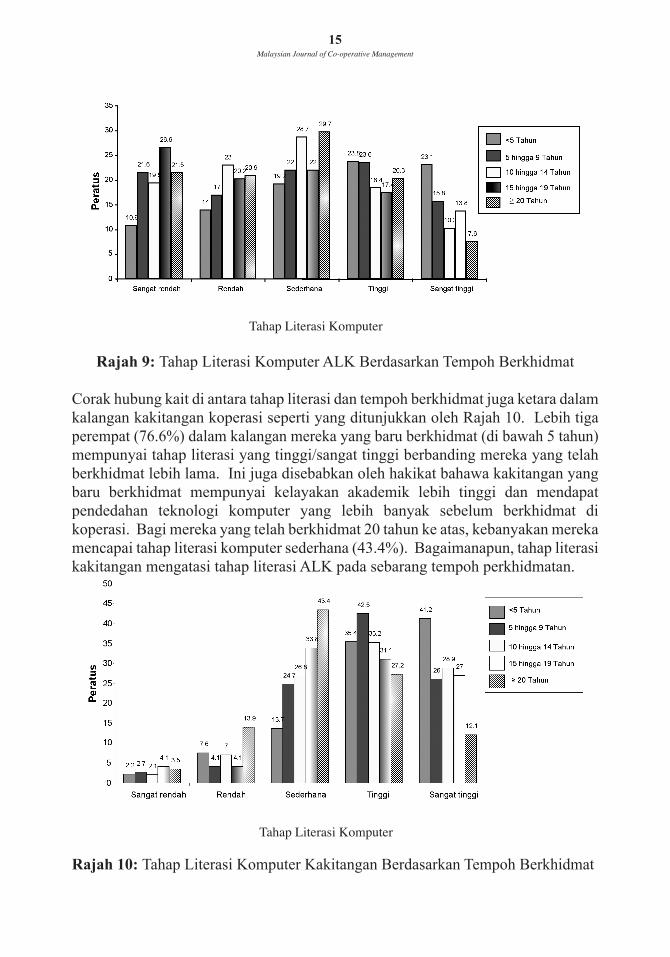

Tahap Literasi Komputer ALK dan Kakitangan Berdasarkan Tempoh Berkhidmat

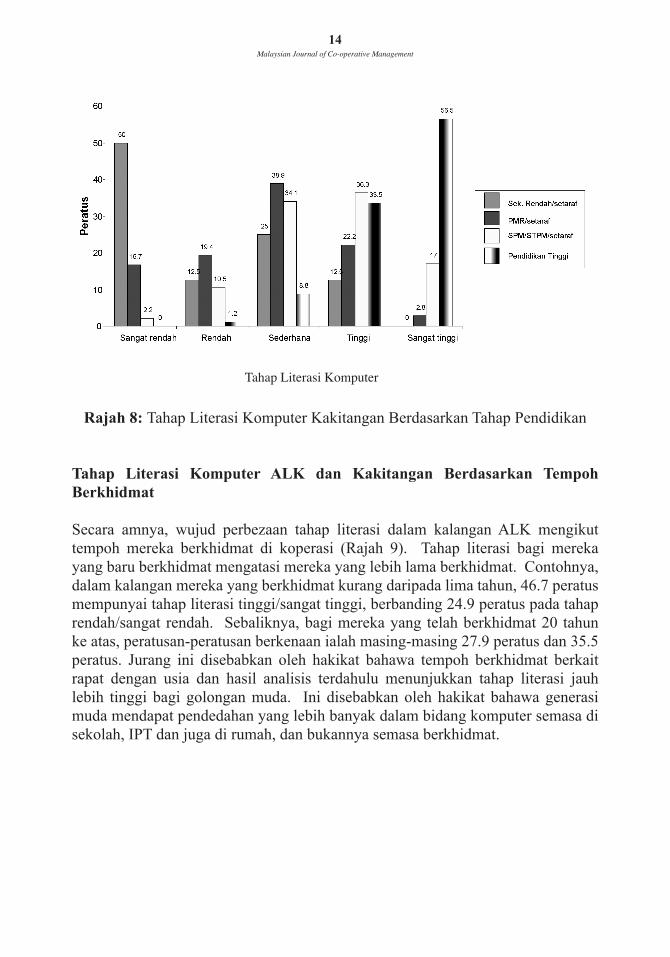

Secara amnya, wujud perbezaan tahap literasi dalam kalangan ALK mengikut tempoh mereka berkhidmat di koperasi (Rajah 9). Tahap literasi bagi mereka yang baru berkhidmat mengatasi mereka yang lebih lama berkhidmat. Contohnya, dalam kalangan mereka yang berkhidmat kurang daripada lima tahun, 46.7 peratus mempunyai tahap literasi tinggi/sangat tinggi, berbanding 24.9 peratus pada tahap rendah/sangat rendah. Sebaliknya, bagi mereka yang telah berkhidmat 20 tahun ke atas, peratusan-peratusan berkenaan ialah masing-masing 27.9 peratus dan 35.5 peratus. Jurang ini disebabkan oleh hakikat bahawa tempoh berkhidmat berkait rapat dengan usia dan hasil analisis terdahulu menunjukkan tahap literasi jauh lebih tinggi bagi golongan muda. Ini disebabkan oleh hakikat bahawa generasi muda mendapat pendedahan yang lebih banyak dalam bidang komputer semasa di sekolah, IPT dan juga di rumah, dan bukannya semasa berkhidmat.

Tahap Literasi Komputer

14Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

15

Rajah 9: Tahap Literasi Komputer ALK Berdasarkan Tempoh Berkhidmat

Corak hubung kait di antara tahap literasi dan tempoh berkhidmat juga ketara dalam kalangan kakitangan koperasi seperti yang ditunjukkan oleh Rajah 10. Lebih tiga perempat (76.6%) dalam kalangan mereka yang baru berkhidmat (di bawah 5 tahun) mempunyai tahap literasi yang tinggi/sangat tinggi berbanding mereka yang telah berkhidmat lebih lama. Ini juga disebabkan oleh hakikat bahawa kakitangan yang baru berkhidmat mempunyai kelayakan akademik lebih tinggi dan mendapat pendedahan teknologi komputer yang lebih banyak sebelum berkhidmat di koperasi. Bagi mereka yang telah berkhidmat 20 tahun ke atas, kebanyakan mereka mencapai tahap literasi komputer sederhana (43.4%). Bagaimanapun, tahap literasi kakitangan mengatasi tahap literasi ALK pada sebarang tempoh perkhidmatan.

Rajah 10: Tahap Literasi Komputer Kakitangan Berdasarkan Tempoh Berkhidmat

Tahap Literasi Komputer

Tahap Literasi Komputer

16Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

17

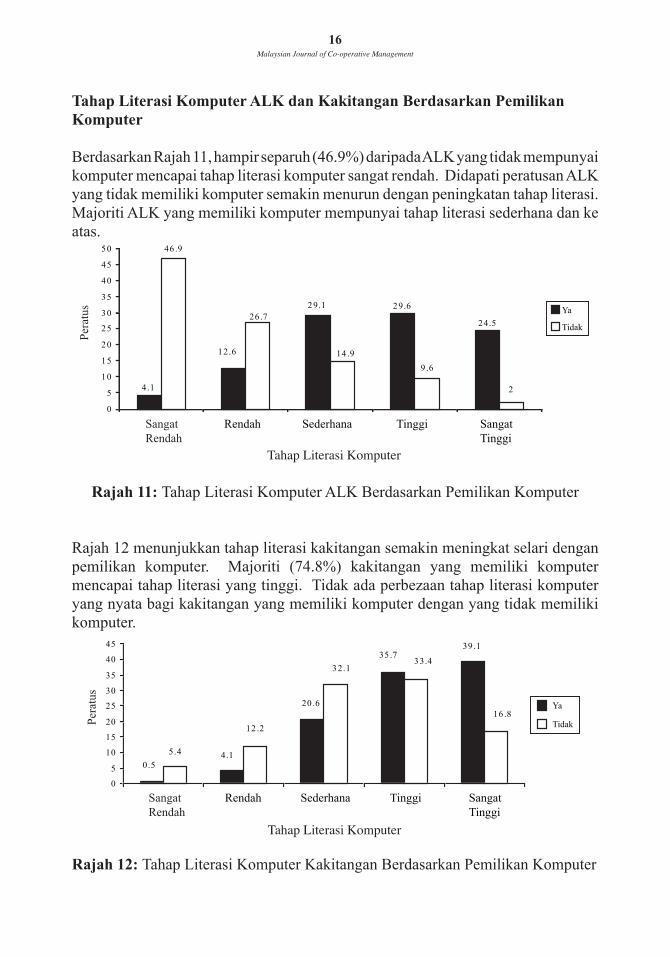

Tahap Literasi Komputer ALK dan Kakitangan Berdasarkan Pemilikan Komputer

Berdasarkan Rajah 11, hampir separuh (46.9%) daripada ALK yang tidak mempunyai komputer mencapai tahap literasi komputer sangat rendah. Didapati peratusan ALK yang tidak memiliki komputer semakin menurun dengan peningkatan tahap literasi. Majoriti ALK yang memiliki komputer mempunyai tahap literasi sederhana dan ke atas.

Rajah 11: Tahap Literasi Komputer ALK Berdasarkan Pemilikan Komputer

Rajah 12 menunjukkan tahap literasi kakitangan semakin meningkat selari dengan pemilikan komputer. Majoriti (74.8%) kakitangan yang memiliki komputer mencapai tahap literasi yang tinggi. Tidak ada perbezaan tahap literasi komputer yang nyata bagi kakitangan yang memiliki komputer dengan yang tidak memiliki komputer.

Rajah 12: Tahap Literasi Komputer Kakitangan Berdasarkan Pemilikan Komputer

Peratus

2 4.5

29.629.1

4.1

12.6

2

9 .6

14 .9

26 .7

46 .9

0

5

10

15

20

25

30

35

40

45

50

Ya

Tidak

Rendah Sederhana Tinggi SangatTinggi

SangatRendah

Tahap Literasi Komputer

Peratus

39 .135 .7

20 .6

0.54.1

16 .8

33.432.1

12 .2

5.4

0

5

10

15

20

25

30

35

40

45

Ya

Tidak

Rendah Sederhana Tinggi SangatTinggi

SangatRendah

Tahap Literasi Komputer

16Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

17

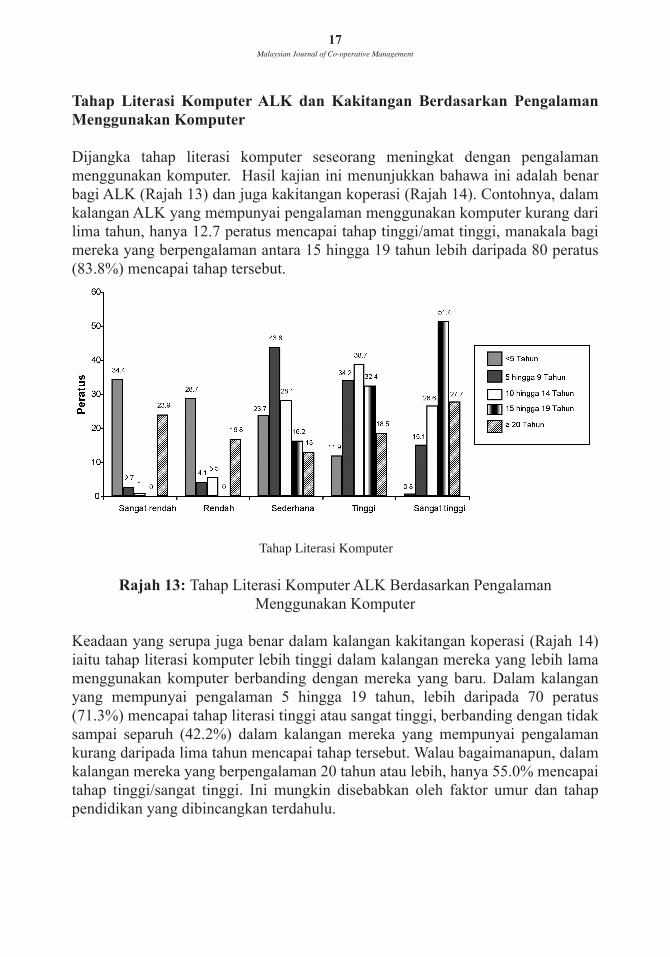

Tahap Literasi Komputer ALK dan Kakitangan Berdasarkan Pengalaman Menggunakan Komputer

Dijangka tahap literasi komputer seseorang meningkat dengan pengalaman menggunakan komputer. Hasil kajian ini menunjukkan bahawa ini adalah benar bagi ALK (Rajah 13) dan juga kakitangan koperasi (Rajah 14). Contohnya, dalam kalangan ALK yang mempunyai pengalaman menggunakan komputer kurang dari lima tahun, hanya 12.7 peratus mencapai tahap tinggi/amat tinggi, manakala bagi mereka yang berpengalaman antara 15 hingga 19 tahun lebih daripada 80 peratus (83.8%) mencapai tahap tersebut.

Rajah 13: Tahap Literasi Komputer ALK Berdasarkan PengalamanMenggunakan Komputer

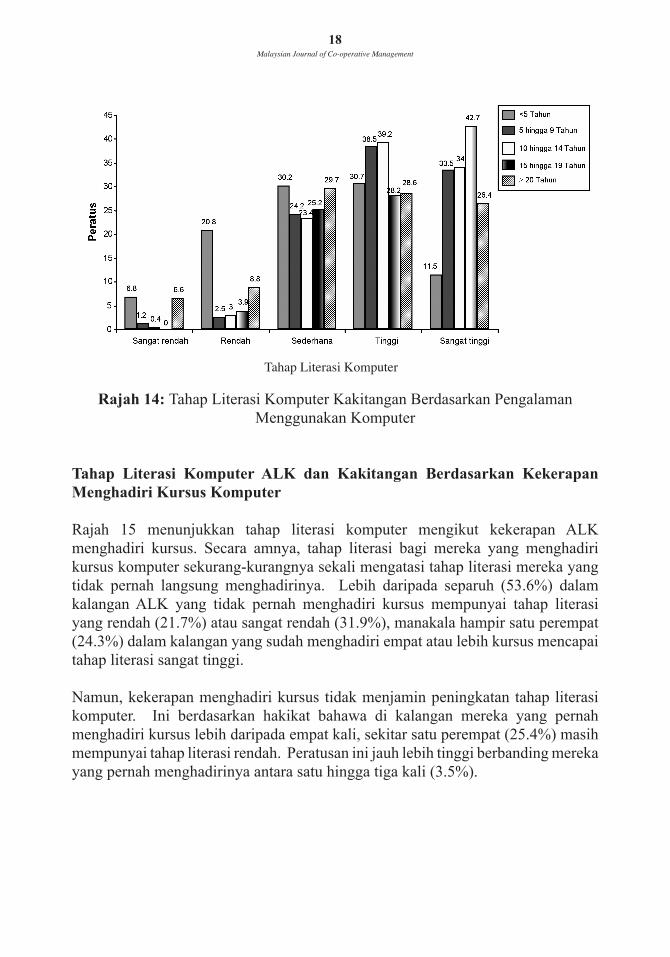

Keadaan yang serupa juga benar dalam kalangan kakitangan koperasi (Rajah 14) iaitu tahap literasi komputer lebih tinggi dalam kalangan mereka yang lebih lama menggunakan komputer berbanding dengan mereka yang baru. Dalam kalangan yang mempunyai pengalaman 5 hingga 19 tahun, lebih daripada 70 peratus (71.3%) mencapai tahap literasi tinggi atau sangat tinggi, berbanding dengan tidak sampai separuh (42.2%) dalam kalangan mereka yang mempunyai pengalaman kurang daripada lima tahun mencapai tahap tersebut. Walau bagaimanapun, dalam kalangan mereka yang berpengalaman 20 tahun atau lebih, hanya 55.0% mencapai tahap tinggi/sangat tinggi. Ini mungkin disebabkan oleh faktor umur dan tahap pendidikan yang dibincangkan terdahulu.

Tahap Literasi Komputer

18Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

19

Rajah 14: Tahap Literasi Komputer Kakitangan Berdasarkan PengalamanMenggunakan Komputer

Tahap Literasi Komputer ALK dan Kakitangan Berdasarkan Kekerapan Menghadiri Kursus Komputer

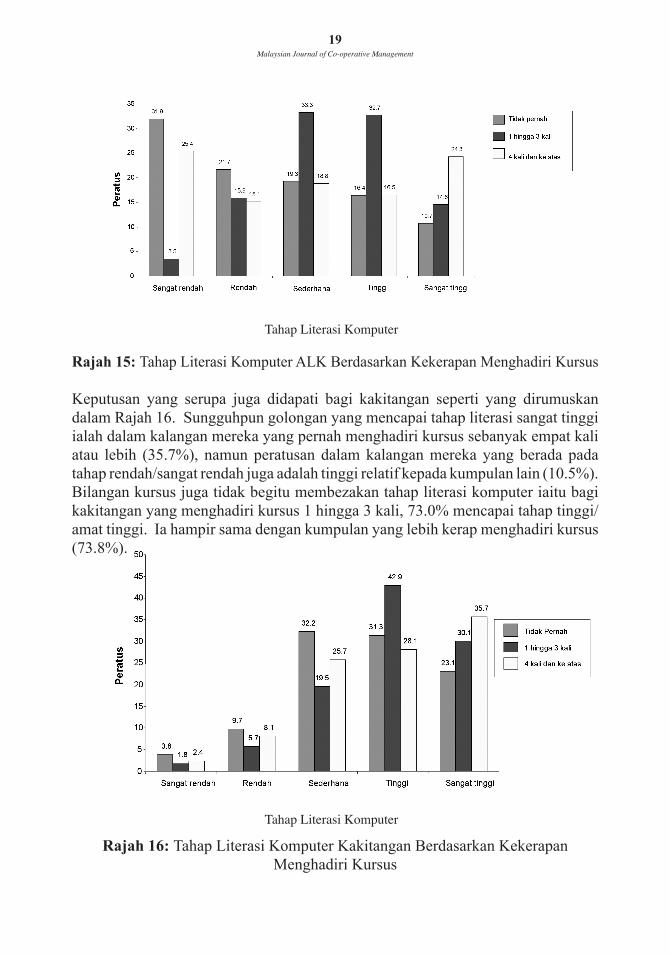

Rajah 15 menunjukkan tahap literasi komputer mengikut kekerapan ALK menghadiri kursus. Secara amnya, tahap literasi bagi mereka yang menghadiri kursus komputer sekurang-kurangnya sekali mengatasi tahap literasi mereka yang tidak pernah langsung menghadirinya. Lebih daripada separuh (53.6%) dalam kalangan ALK yang tidak pernah menghadiri kursus mempunyai tahap literasi yang rendah (21.7%) atau sangat rendah (31.9%), manakala hampir satu perempat (24.3%) dalam kalangan yang sudah menghadiri empat atau lebih kursus mencapai tahap literasi sangat tinggi.

Namun, kekerapan menghadiri kursus tidak menjamin peningkatan tahap literasi komputer. Ini berdasarkan hakikat bahawa di kalangan mereka yang pernah menghadiri kursus lebih daripada empat kali, sekitar satu perempat (25.4%) masih mempunyai tahap literasi rendah. Peratusan ini jauh lebih tinggi berbanding mereka yang pernah menghadirinya antara satu hingga tiga kali (3.5%).

Tahap Literasi Komputer

18Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

19

Rajah 15: Tahap Literasi Komputer ALK Berdasarkan Kekerapan Menghadiri Kursus

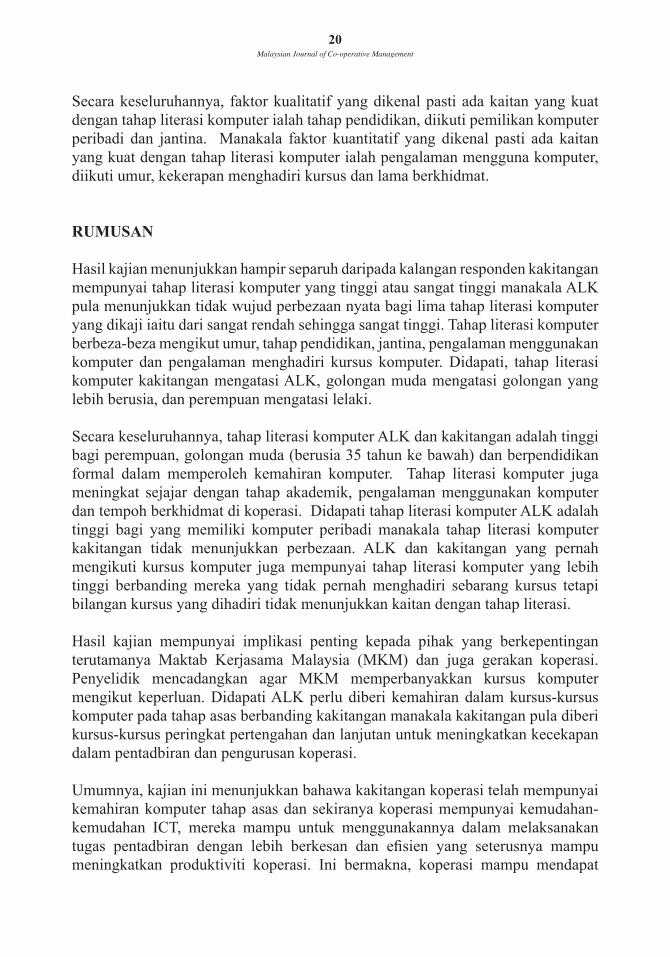

Keputusan yang serupa juga didapati bagi kakitangan seperti yang dirumuskan dalam Rajah 16. Sungguhpun golongan yang mencapai tahap literasi sangat tinggi ialah dalam kalangan mereka yang pernah menghadiri kursus sebanyak empat kali atau lebih (35.7%), namun peratusan dalam kalangan mereka yang berada pada tahap rendah/sangat rendah juga adalah tinggi relatif kepada kumpulan lain (10.5%). Bilangan kursus juga tidak begitu membezakan tahap literasi komputer iaitu bagi kakitangan yang menghadiri kursus 1 hingga 3 kali, 73.0% mencapai tahap tinggi/amat tinggi. Ia hampir sama dengan kumpulan yang lebih kerap menghadiri kursus (73.8%).

Rajah 16: Tahap Literasi Komputer Kakitangan Berdasarkan KekerapanMenghadiri Kursus

Tahap Literasi Komputer

Tahap Literasi Komputer

20Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

21

Secara keseluruhannya, faktor kualitatif yang dikenal pasti ada kaitan yang kuat dengan tahap literasi komputer ialah tahap pendidikan, diikuti pemilikan komputer peribadi dan jantina. Manakala faktor kuantitatif yang dikenal pasti ada kaitan yang kuat dengan tahap literasi komputer ialah pengalaman mengguna komputer, diikuti umur, kekerapan menghadiri kursus dan lama berkhidmat.

RUMUSAN

Hasil kajian menunjukkan hampir separuh daripada kalangan responden kakitangan mempunyai tahap literasi komputer yang tinggi atau sangat tinggi manakala ALK pula menunjukkan tidak wujud perbezaan nyata bagi lima tahap literasi komputer yang dikaji iaitu dari sangat rendah sehingga sangat tinggi. Tahap literasi komputer berbeza-beza mengikut umur, tahap pendidikan, jantina, pengalaman menggunakan komputer dan pengalaman menghadiri kursus komputer. Didapati, tahap literasi komputer kakitangan mengatasi ALK, golongan muda mengatasi golongan yang lebih berusia, dan perempuan mengatasi lelaki.

Secara keseluruhannya, tahap literasi komputer ALK dan kakitangan adalah tinggi bagi perempuan, golongan muda (berusia 35 tahun ke bawah) dan berpendidikan formal dalam memperoleh kemahiran komputer. Tahap literasi komputer juga meningkat sejajar dengan tahap akademik, pengalaman menggunakan komputer dan tempoh berkhidmat di koperasi. Didapati tahap literasi komputer ALK adalah tinggi bagi yang memiliki komputer peribadi manakala tahap literasi komputer kakitangan tidak menunjukkan perbezaan. ALK dan kakitangan yang pernah mengikuti kursus komputer juga mempunyai tahap literasi komputer yang lebih tinggi berbanding mereka yang tidak pernah menghadiri sebarang kursus tetapi bilangan kursus yang dihadiri tidak menunjukkan kaitan dengan tahap literasi.

Hasil kajian mempunyai implikasi penting kepada pihak yang berkepentingan terutamanya Maktab Kerjasama Malaysia (MKM) dan juga gerakan koperasi. Penyelidik mencadangkan agar MKM memperbanyakkan kursus komputer mengikut keperluan. Didapati ALK perlu diberi kemahiran dalam kursus-kursus komputer pada tahap asas berbanding kakitangan manakala kakitangan pula diberi kursus-kursus peringkat pertengahan dan lanjutan untuk meningkatkan kecekapan dalam pentadbiran dan pengurusan koperasi.

Umumnya, kajian ini menunjukkan bahawa kakitangan koperasi telah mempunyai kemahiran komputer tahap asas dan sekiranya koperasi mempunyai kemudahan-kemudahan ICT, mereka mampu untuk menggunakannya dalam melaksanakan tugas pentadbiran dengan lebih berkesan dan efisien yang seterusnya mampu meningkatkan produktiviti koperasi. Ini bermakna, koperasi mampu mendapat

20Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

21

faedah-faedah dari program-program ICT yang dilaksanakan sama ada oleh kerajaan atau agensi-agensinya. Walaupun ALK tidak memerlukan kemahiran komputer untuk melaksanakan tugas-tugas pentadbiran tetapi kemahiran ALK untuk memperoleh maklumat menggunakan ICT adalah amat penting terutama di dalam membuat keputusan pengurusan. Gabungan kemahiran menggunakan komputer oleh ALK dan kakitangan akan mewujudkan koperasi yang mantap dan mampu mencapai wawasan kerajaan untuk menjadi sektor ketiga yang menyumbang kepada pembangunan ekonomi negara.

Kajian Lanjutan

Terdapat pelbagai cara untuk mengukur tahap literasi seperti yang telah dinyatakan di dalam sorotan kajian. Bagi kajian ini, tahap literasi diukur dengan menggunakan soal selidik yang berdasarkan penilaian diri sendiri. Terdapat kemungkinan dapatan kajian kurang tepat. Oleh itu, untuk memantapkan dapatan kajian ini, dicadangkan supaya kaedah ujian amali di makmal komputer pula digunakan untuk mengukur tahap literasi komputer ALK dan kaki tangan koperasi. Selain itu, kajian akan datang pula dicadangkan untuk memberi fokus kepada koperasi seperti kesan literasi komputer terhadap prestasi koperasi dan juga latar belakang kemudahan ICT di koperasi.

RUJUKAN

Abdul Manaf Bohari. (2006). ICT dari perspektif profesional : Isu-isu pengurusan dan Organisasi. Prentice Hall.

Ainley, J., Fraillon, J. & Haber, J. (2006). Assessing student technology literacy at a National Level. Paper presented at the National Educational Computing Conference, San Diego. Dicapai dari http://www.iste.org/Content/NavigationMenu/Research/NECC_Research_Paper_Archives/NECC_2006/Haber_Jon_NECC06.pdf

Al-Daihani, S., M. & Rehman, S. (2006). A study of the information literacy capabilities of the Kuwaiti police officers. Kuwait : Emerald Group Publishing Limited. Dicapai dari http://www.emeraldinsight.com/KuwaitPolice.pdf

Anderson, M. A. (2000). Assessing teacher technology skills. ProQuest Education Journals, 25. Dicapai pada 12 Mac 2007 dari http://proquest.umi.com.newdc.oum.edu.my/pqdweb?index=21&did=63318448&SrchMode=1&sid=2&Fmt=3&VInst=PROD&VType=PQD&RQT=309&VName=PQD&TS=1233305866&clientId=56581

22Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

23

Connelly, J., A. (2003). Computer literacy in the digital age : development of the computer literacy measure for prospective employees (CLMPE). USA : ProQuest Information and Learning Company. Dicapai dari http://proquest.umi.com/pqdlink?did=766620671&Fmt=7&clientId =79356&RQT=309&VName=PQD

Davies, J., E. (2002). Assessing and predicting ICT literacy in education undergraduates. Paper presented at the annual meeting of SITE, March 2002, Nashville, TN. Dicapai dari http://www.quasar.ualberta.ca/IT/research/Szabo/Site2001.pdf

Dickerson, J., G. (2005). Analysis of computing skills and differences between demographic groups: A basis for curriculum development in computer technology courses at UNC-Wilmington. Dicapai dari http://www.lib.ncsu.edu/theses/available/etd-06292005- 102215/unrestricted/etd.pdf

Du, Y. (2004). The relationship between students’ computer competency and perception of Enjoyment and Difficulty Level in Web-based Distance Learning. Education Libraries, 27 (2), 5-12. Dicapai dari http://units.sla.org/division/ded/educationlibraries/27-2.pdf

European Commission, Enterprise and industry directorate-general. (2006, 30 Jun). Effect of ICT capital on economic growth. Dicapai pada 12 Mac 2007, dari http://ec.europa.eu/enterprise/ict/policy/ict/ict-cap-eff.pdf

Huang, S., M. (2005). Technology proficiency of college level language teachers in Taiwan : Effect on their technology utilization and expectation for students’ technology proficiency. Dicapai dari http://worldcat.org/oclc/67523735

International ICT Literacy Panel (2000). Digital transformation a framework for ICT literacy. U.S.A : Educational Testing Service. Dicapai dari http://www.ets.org/ictliteracy/digital1.html

Jabatan Pembangunan Koperasi (2003). Dasar koperasi negara. Kuala Lumpur : Jabatan Pembangunan Koperasi.

Karsten R. & Roth R., M. (1998). Computer self-efficacy: A practical indicator of student computer competency in introductory IS courses. Dicapai dari http://www.learning-quest.com/software/compefficacy.pdf

Khirul Bahri Basaruddin (2005, 31 Julai). Tingkat prestasi koperasi. Berita Minggu, p.2.

22Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

23

Markauskaite, L. (2006). Towards an integrated analytical framework of information and communications technology literacy: From intended to implemented and achieved dimensions. Information Research, 11(3) paper 252. Dicapai pada 30 Mac 2007, dari http://InformationR.net/ir/11-3/paper252.html.

Mathews, J., G. (1998). Predicting teacher perceived technology use : Needs assessment model for small rural schools. Dicapai dari http://www.eric.ed.gov/ERICDocs/data/ericdocs2sql/content_storage_01/0000019b/80/15/6a/d0.pdf

McDonald D., S. (2004). Computer Literacy Skills for Computer Information Systems Majors: A Case Study. Journal of Information Systems Education (ProQuest Education Journals), 15 (1), 19-33.

Meckelborg, A. (2003). Assessing Computer Literacy in Adult ESL Learners. Proquest education journal. Dicapai pada 27 Februari 2008, dari http://proquest.umi.com.newdc.oum.edu.my/pqdweb?did=766710521&sid=8&Fmt=2&clientId=56581&RQT=309&VName=PQD

Mohamed Khalid Nordin. (2007). Keusahawanan, dasar, pembangunan dan pembudayaan; nafas baru untuk koperasi, Vol 1. Putrajaya : Kementerian Pembangunan Usahawan dan Koperasi.

Nor Azan Mat Zin (2000). Gender differences in computer literacy level among undergraduate students in Universiti Kebangsaan Malaysia (UKM). Dicapai dari http://www.ejisdc.org/ojs2/index.php/ejisdc/article/viewFile/3/3

Organization for Economic Co-operation and Development. (2003). The sources of economic growth in OECD countries. Dicapai pada 20 April 2007 dari http://www.oecd.org/document/32/0,3343,en_2649_34325_2506528_1_1_1_37443,00.html

Norlaili Mansor. (2006, Ogos). Hari koperasi negara 2006 : Wawasan PM memperkukuhkan gerakan koperasi sekolah. Pelancar Online. Dicapai pada 9 Januari 2007, dari http://www.angkasa.coop/pelancar/index.php?p=aug003-2006

Oliver, R. & Towers, S. (2000). Benchmarking ICT literacy in tertiary learning settings. In R. Sims, M. O’Reilly & S. Sawkins (Eds). (Learning to choose: Choosing to learn.) Proceedings of the 17 th Annual ASCILITE Conference (pp 381-390). Lismore, NSW: Southern Cross University Press. Dicapai dari http://elrond.scca.ecu.edu.au/oliver/2000/aciliteict.pdf

24Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

25

Patrikas, E. O. & Newton, R. A. (1999). Computer literacy among entering allied health students and faculty. Technology Horizons in Education Journal. Dicapai pada 27 Februari 2008 dari http://www.thejournal.com/articles/14498_1

Pejabat Perdana Menteri. (2007, 23 Okt). Pelancaran M.S.C. Malaysia Cybercentre @ Meru Raya. Dicapai pada 10 November 2007, dari http://www.pmo.gov.my/website/webdbase.nsf/w_4?openForm&url=http://www.pmo.gov.my/WebNotesApp/Abdullah.nsf/KoleksiUcapanForm?OPenform&tajuknyer=All%20Speeches,%20Statement%20and%20Press%20Release%20By%20PM&lang=1

Smith, B., N. (1996). Assessing the computer literacy of undergraduate college students. Dicapai dari http://findarticles.com/p/articles/mi_qa3673/is_199601/ai_n8743567/print

Smith, S., M. (2004). Software Skills Acquisition: Confidence vs. Competence. Information technology, learning, and performance journal. 22 (2), 33-40.

Unit Perancang Ekonomi, Jabatan Perdana Menteri (2006). Rancangan Malaysia kesembilan 2006-2010 (ms 148-149). Putrajaya : Unit Perancang Ekonomi.

Unit Perancang Ekonomi, Jabatan Perdana Menteri. (2006, September). Ucapan bajet 2007 : Melaksanakan misi nasional ke arah mencapai wawasan negara. Dicapai pada 12 Februari 2007, dari http://www.epu.jpm.my/bajet/bmbajet2007.pdf

AUTHOR’S BACKGROUND

Siti Fatimah Sajadi is the Head of the Information Technology and Communications Centre, Co-operative College of Malaysia (CCM). She obtained her Masters in Information Technology from Universiti Teknologi MARA (UiTM) in 2004, Diploma in Systems Analysis from UiTM in 1990 and Bachelor in Economics from Universiti Kebangsaan Malaysia in 1987. She joined CCM in 1994 and is an experienced trainer in ICT based training. She is also involved in research studies and regularly writes articles for CCM publications.

Malaysian Journal of Co-operative Management25

DANA KOPERASI:SUMBER DAN KECENDERUNGAN PENGGUNAAN

Hj. Ramlan KamsinMaktab Kerjasama Malaysia Cawangan Sarawak

(Co-operative College of Malaysia, Sarawak Branch)

ABSTRACT

This exploratory study identified the major sources of cooperative funds and their

uses as well as how their net profits were distributed after the necessary statutory

deductions had been made. A total of 274 co-operatives in Peninsular Malaysia

participated in the study. The profile of the cooperatives were identified from the

feedback obtained through questionnaires to the cooperatives, while data on the

sources and uses of funds as well as the distribution of net profits were sourced from

the annual reports of the cooperatives, from 2003 to 2005.

The findings indicated that 83% of the funds of co-operatives were from internal

sources, specifically from members’ share capital as compared to only 17% from

external financing by financial institutions. Furthermore, 57% of the cooperatives’

funds were utilised to finance investment in assets, the most popular activity as

compared to only 29% being used to undertake economic activities. In terms of

the distribution of net profits, 60% of the cooperatives gave dividends on members’

share capital, 52% of the cooperatives paid honoraria to board members and 50%

of the cooperatives set up funds for their members’ benefit.

26Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

27

ABSTRAK

Kajian exploratori ini telah mengenal pasti sumber dan penggunaan dana koperasi serta cara bagaimana koperasi mengagihkan untung bersihnya selepas peruntukan statutori telah dibuat. Sebanyak 274 koperasi telah menyertai kajian ini. Profil koperasi telah dikenal pasti melalui maklum balas daripada soal selidik kepada koperasi manakala data mengenai sumber dan penggunaan dana serta pengagihan untung bersih koperasi diperoleh daripada laporan tahunan koperasi-koperasi tersebut daripada tahun 2003 hingga 2005.

Penemuan kajian ini mendapati 83% daripada dana koperasi adalah dari sumber dalaman, khususnya modal syer anggota berbanding hanya 17% dari pembiayaan oleh institusi kewangan. Tambahan lagi, 57% daripada dana koperasi digunakan untuk membiayai pelaburan dalam aset, yang merupakan aktiviti paling popular berbanding hanya 29% yang digunakan untuk menjalankan aktiviti ekonomi. Dari aspek pulangan pendapatan dari aktiviti koperasi pula menunjukkan bahawa aktiviti kontrak, perumahan dan perladangan merupakan aktiviti yang menunjukkan keuntungan yang tertinggi. Dari aspek pengagihan untung bersih koperasi menunjukkan bahawa 60% koperasi memberi dividen atas modal syer anggota, 52% koperasi membayar honorarium kepada ALK dan 50% mewujudkan tabung kumpulan wang untuk anggotanya.

PENGENALAN

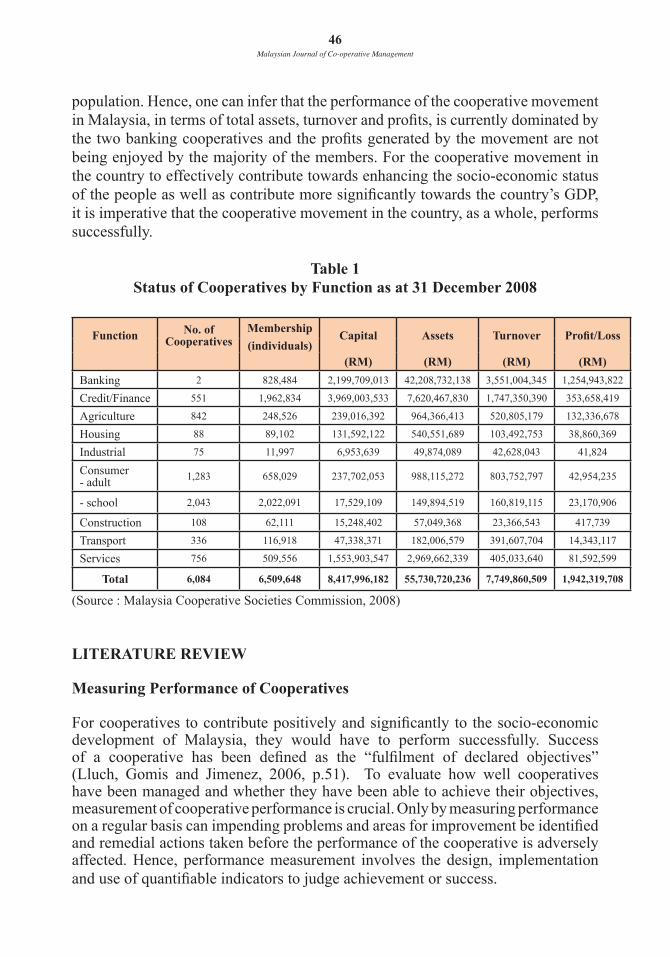

Koperasi adalah sebuah pertubuhan berautonomi yang ditubuhkan secara sukarela oleh individu untuk memenuhi keperluan ekonomi, sosial dan budaya mereka dengan mengamalkan prinsip koperasi. Dasar Koperasi Negara yang dibentuk pada tahun 2004 telah mengenal pasti kebanyakan koperasi bermodal kecil dan kurang berdaya saing disebabkan oleh saiz anggota yang kecil, anggota yang tidak aktif dan Anggota Lembaga Koperasi (ALK) yang tidak berani untuk menanggung risiko. Kerajaan melalui Kementerian Pembangunan Usahawan dan Koperasi berharap 600 koperasi dapat dimantapkan dalam Rancangan Malaysia Ke-9 agar gerakan koperasi lebih berdaya saing dan berdaya maju bagi memberi faedah kepada anggota dan masyarakat selaras dengan matlamat penubuhannya. Kerajaan juga berhasrat agar koperasi menjadi sektor ketiga penting selepas sektor awam dan swasta dalam menyumbang kepada pertumbuhan ekonomi negara. Dari segi perangkaan sehingga 31 Disember 2008, terdapat 6,084 koperasi di Malaysia dengan keanggotaan seramai 6.5 juta orang yang mewakili 30% daripada jumlah penduduk, modal syer/yuran berjumlah RM8.4 bilion, aset berjumlah RM55.7 bilion, jumlah pusingan perniagaan (turnover) sebanyak RM7.7 bilion serta untung berjumlah RM1.9 bilion.

26Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

27

Penyataan Masalah

Menurut Suruhanjaya Koperasi Malaysia (SKM), pada tahun 2009 didapati sumbangan gerakan koperasi kepada KDNK negara kurang memberangsangkan iaitu sekitar 1% sahaja berbanding gerakan koperasi di luar negara yang menyumbang sehingga 10-30%. Sehubungan itu, kerajaan mensasarkan agar koperasi akan dapat memberi sumbangan sehingga 4% kepada KDNK negara menjelang 2013 dengan purata jualan tahunan setiap koperasi meningkat ke RM800 ribu hingga RM1.5 juta. Bagi mencapai hasrat ini, koperasi perlu berubah dengan meningkatkan sumber modal dan menceburi aktiviti yang lebih berdaya maju serta berdaya saing. Oleh itu, koperasi perlu mengenal pasti aktiviti ekonomi yang boleh meningkatkan pendapatan berskala yang lebih besar dengan menggunakan dana yang dimilikinya. Kajian ini diharapkan akan dapat membantu koperasi mengenal pasti sumber dana dan aktiviti ekonomi yang wajar diceburi berdasarkan pengalaman koperasi lain yang juga terlibat dalam kajian ini.

Objektif, Kepentingan dan Skop Kajian

Kajian ini secara amnya bertujuan untuk mengenal pasti sumber dana koperasi dan menentukan penggunaan dana oleh koperasi. Kajian ini turut membuat penilaian terhadap pulangan aktiviti yang memberi hasil yang paling lumayan serta mengenal pasti pengagihan untung bersih yang diperoleh oleh koperasi. Hasil kajian ini boleh dijadikan sebagai panduan khususnya kepada koperasi baru untuk menceburi aktiviti ekonomi berdasarkan arah aliran (trend) dan pengalaman koperasi lain. Bagi koperasi sedia ada pula, kajian ini akan dapat membantu mereka untuk menceburi aktiviti baru yang berpotensi dan memberi pulangan yang besar kepada koperasi. Hasil kajian juga memberi maklumat asas kepada perancang dan pembuat dasar khususnya kepada pihak kementerian yang baru iaitu Kementerian Perdagangan Dalam Negeri, Koperasi dan Kepenggunaan (KPDNKK), SKM dan Maktab Kerjasama Malaysia (MKM) serta kepada pihak yang terlibat secara langsung atau tidak langsung terhadap gerakan koperasi untuk memperoleh maklumat berkaitan dengan sumber dana dan penggunaan dana oleh gerakan koperasi di Malaysia. Walau bagaimanapun kajian ini agak terbatas kerana wujudnya unsur kerahsiaan dan kurangnya kerjasama yang diberikan oleh koperasi untuk membekalkan maklumat kewangan yang diperlukan di samping format laporan tahunan 2003-2005 yang tidak seragam.

28Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

29

SOROTAN KAJIAN

Di Malaysia masih belum terdapat banyak kajian terperinci yang dijalankan mengenai sumber dan penggunaan dana oleh koperasi. Menurut Ng (2002), koperasi perlu tumbuh dan berkembang untuk membolehkannya berdaya saing dan berdaya maju. Selain menggunakan sumber dana dalaman, koperasi turut menghadapi masalah untuk mendapatkan sumber pembiayaan dari sumber luar khususnya dari institusi perbankan. Ghani (1980) pula menyatakan bahawa koperasi menggunakan dananya untuk memberi pinjaman kepada anggota selaras dengan tujuan penubuhan koperasi. Fauzi (2000) menjelaskan bahawa kebanyakan koperasi menghadapi masalah kewangan yang mana hasil kajiannya menunjukkan 86% koperasi menghadapi masalah ketidakcukupan modal kerana sumber utama modal koperasi hanya diperoleh dari sumber dalaman khususnya melalui syer anggota, fi dan untung terkumpul yang terhad. Menurut Henny (1996) pula, anggota mempunyai peranan penting untuk menyumbangkan modal bagi memajukan kegiatan koperasi. Jumlah tabungan modal ini sangat bergantung kepada simpanan secara sukarela yang mana hasil kajiannya membuktikan peningkatan pemberian dividen tidak dapat menarik minat anggota untuk meningkatkan sumbangan modal.

Hasil kajian oleh Chukwu (1992) menyatakan bahawa modal koperasi perlulah diuruskan mengikut keperluannya, jika keperluan jangka pendek ianya perlulah diperoleh dari sumber jangka pendek dan sebaliknya bagi membolehkan koperasi dapat memenuhi obligasi liabilitinya mengikut ketentuan masa yang telah ditetapkan. Menurut Pischke (1996), keperluan modal luar adalah perlu bagi memenuhi pertumbuhan perniagaan koperasi pada kadar yang meningkat. Dalam kajiannya berhubung pembentukan modal koperasi mendapati, adalah menjadi cabaran koperasi untuk mendapatkan modal dan biasanya koperasi kekurangan modal untuk beroperasi terutamanya koperasi pertanian. Kurangnya perhatian terhadap pembentukan modal telah memberikan kesan buruk kepada perniagaan. Hanya dengan bantuan penyediaan sumber modal, koperasi akan mampu bersaing dan berkembang maju. Menurut Hasniza (2006), Industri Kecil dan Sederhana (IKS) lebih suka menggunakan sumber kewangan sendiri untuk memulakan perniagaan. Dalam tempoh berkembang, mereka mengambil pinjaman jangka sederhana dari bank dan mengambil pinjaman jangka panjang pula dalam tempoh matang. Menurut Hasniza lagi, kebanyakan IKS membelanjakan dananya untuk modal kerja. Bagaimanapun, tahap peruntukan untuk penyelidikan dan pembangunan, teknologi maklumat dan komunikasi, dan pembangunan sumber manusia adalah berbeza-beza menurut kitaran hayat perniagaan. Dengan melihat kepada untung bersih koperasi pula ia telah diagih-agihkan mengikut keutamaan seperti mana yang dikehendaki oleh seksyen 57 Akta Koperasi 1993.

28Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

29

METODOLOGI DAN PENGUMPULAN DATA

Daripada 5,003 jumlah koperasi yang didaftarkan sehingga Februari 2007 (SKM, 2007), hanya 1,648 koperasi telah dipilih sebagai sampel kajian iaitu dengan mengecualikan koperasi yang tidak aktif, koperasi yang ditubuhkan pada tahun 2003-2007, koperasi yang tidak mengadakan mesyuarat agung pada tahun 2004, koperasi sekolah, koperasi di Sabah dan Sarawak serta koperasi menengah, koperasi gabungan, koperasi bank dan koperasi atasan. Kajian ini memerlukan setiap koperasi yang dipilih sebagai sampel membekalkan Laporan Tahunan Koperasi dari tahun 2003 hingga 2005 di samping borang soal selidik yang turut diberikan kepada koperasi.

Bahagian pertama kajian ini menerangkan demografi koperasi manakala bahagian kedua pula menjelaskan maklumat mengenai kewangan koperasi. Laporan Tahunan Koperasi dari tahun 2003 hingga 2005 digunakan bagi melihat sumber dana, pengagihan penggunaan dana untuk membiayai aktiviti koperasi, perolehan pendapatan serta pengagihan untung bersih koperasi. Data diproses dengan menggunakan perisian aplikasi SPSS (Statistical Package for the Social Sciences) dan dianalisis dengan menggunakan statistik deskriptif. Selain itu, cross tabulation juga telah digunakan dalam menganalisis data kajian ini.

PENEMUAN KAJIAN

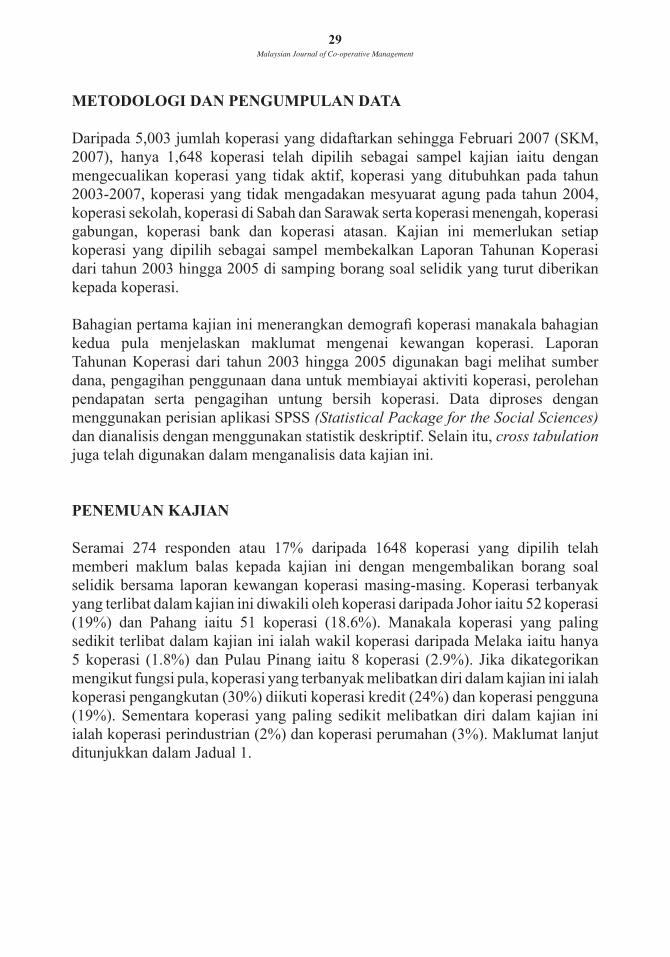

Seramai 274 responden atau 17% daripada 1648 koperasi yang dipilih telah memberi maklum balas kepada kajian ini dengan mengembalikan borang soal selidik bersama laporan kewangan koperasi masing-masing. Koperasi terbanyak yang terlibat dalam kajian ini diwakili oleh koperasi daripada Johor iaitu 52 koperasi (19%) dan Pahang iaitu 51 koperasi (18.6%). Manakala koperasi yang paling sedikit terlibat dalam kajian ini ialah wakil koperasi daripada Melaka iaitu hanya 5 koperasi (1.8%) dan Pulau Pinang iaitu 8 koperasi (2.9%). Jika dikategorikan mengikut fungsi pula, koperasi yang terbanyak melibatkan diri dalam kajian ini ialah koperasi pengangkutan (30%) diikuti koperasi kredit (24%) dan koperasi pengguna (19%). Sementara koperasi yang paling sedikit melibatkan diri dalam kajian ini ialah koperasi perindustrian (2%) dan koperasi perumahan (3%). Maklumat lanjut ditunjukkan dalam Jadual 1.

30Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

31

Jadual 1 : Anggota Koperasi Mengikut Fungsi yang Terlibat dalam Kajian

FungsiKoperasi

Julat Bilangan AnggotaJUMLAH %

< =250 251 - 500 501 - 750 751 - 1000 >=1001

Pengangkutan 24 32 8 1 18 83 30.3

Kredit/Kewangan 26 18 8 6 9 67 24.4

Pengguna 15 15 8 2 13 53 19.3

Perkhidmatan 7 5 1 1 10 24 8.8

Perladangan 6 6 3 1 7 23 8.4

Pembinaan 4 5 1 1 0 11 4

Perumahan 3 1 2 1 0 7 2.6

Perindustrian 3 1 1 0 1 6 2.2

88 83 32 13 58 274 100

Secara majoritinya, 62.4% koperasi yang dikaji memiliki anggota di bawah 500 orang dan majoriti kelulusan akademik tertinggi yang dimiliki oleh Anggota Lembaga Koperasi (ALK) dalam kajian ini adalah di peringkat SPM (66%) dan berumur lebih 50 tahun (79%) dengan memperoleh elaun kurang RM50 (75%). Ini menggambarkan kebanyakan koperasi yang terlibat dalam kajian ini ditadbir oleh ALK yang berumur lebih 50 tahun dengan kelulusan akademik tertinggi adalah SPM, berkhidmat lebih 10 tahun (85%) dan memperoleh elaun kurang dari RM50.

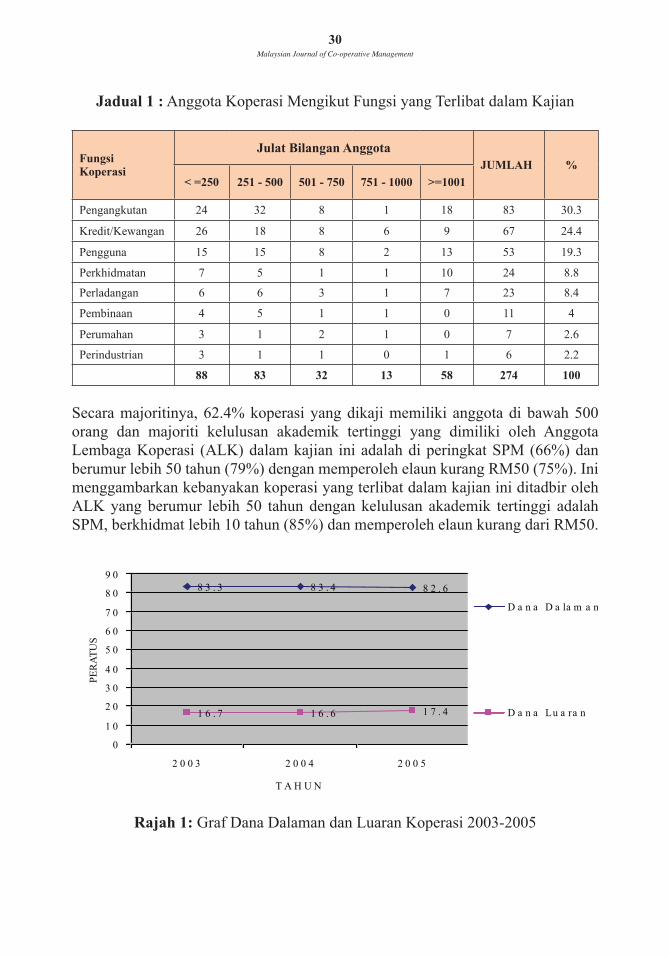

Rajah 1: Graf Dana Dalaman dan Luaran Koperasi 2003-2005

8 3 . 3 8 3 . 4 8 2 . 6

1 6 . 7 1 6 . 6 1 7 . 4

0

1 0

2 0

3 0

4 0

5 0

6 0

7 0

8 0

9 0

2 0 0 3 2 0 0 4 2 0 0 5

T A H U N

PERATUS

D a n a D a la m a n

D a n a Lu a ra n

30Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

31

Sumber Dana Koperasi

Berdasarkan Rajah 1, majoriti koperasi yang terlibat dalam kajian ini bagi tahun 2005 memiliki 83% sumber dananya dari sumber dalaman berbanding 17% dari dana luaran. Sepanjang tempoh kajian didapati peratusan dana yang diperoleh dari sumber luaran telah meningkat walaupun tidak begitu ketara khususnya bagi koperasi fungsi perumahan, perladangan, pembinaan dan pengangkutan. Ini menunjukkan bahawa koperasi menggunakan dana luarannya untuk mengembangkan aktiviti perniagaan selaras dengan perkembangan koperasi.

Kesemua 274 koperasi yang dikaji memiliki sumber dana dalaman dari modal syer yang disumbangkan oleh anggota dengan purata (min) sehingga 83%. Penemuan ini menyokong kajian Fauzi (2000) yang menunjukkan bahawa modal syer menyumbangkan 63% kepada sumber dana dalaman koperasi. Bagaimanapun bagi koperasi berfungsi industri, sumbangan syer anggotanya adalah yang paling sedikit (minimum RM1190) berbanding koperasi berfungsi kredit yang menyumbangkan syer maksimum sehingga RM25 juta. Majoriti (median) syer anggota koperasi yang dikaji ialah RM137,347. Lebih separuh (51%) koperasi yang dikaji memiliki dana kurang daripada RM500 ribu.

Sementara itu dana dari sumber luaran bagi tahun 2005 pula menunjukkan bilangan koperasi yang menggunakan dana ini sebanyak 201 koperasi (73.4%) sahaja. Kajian menunjukkan bilangan koperasi yang tidak menggunakan dana ini berkurangan dari 77 koperasi (2003) kepada 75 koperasi (2004) dan 73 koperasi (2005). Kajian ini turut mendapati koperasi cenderung mendapatkan sumber pembiayaan dari institusi kewangan diikuti sumber pembiayaan dari anggotanya dalam bentuk simpanan anggota. Manakala sumber pembiayaan dari Tabung Modal Pusingan (TMP) pula menunjukkan bahawa bilangan koperasi yang menggunakan perkhidmatan ini meningkat sepanjang tahun kajian. Koperasi yang berfungsi pengangkutan merupakan peminjam TMP terbanyak diikuti oleh koperasi berfungsi perumahan. Koperasi berfungsi perindustrian yang terlibat dalam kajian ini pula tidak menggunakan langsung kemudahan ini.

Oleh itu, bagi menghadapi cabaran menjadikan koperasi sebagai sektor ketiga penting penyumbang ekonomi negara, koperasi perlu meningkatkan sumber dana khususnya dari sumber dalaman untuk membiayai aktiviti dan menjana pendapatan dari aktiviti tersebut. Menurut Dasar Koperasi Negara, koperasi memiliki modal kecil kerana anggota yang tidak aktif. Ini menggambarkan bahawa agak sukar untuk anggota menambah modal syer minimumnya. Walaupun koperasi berkeupayaan memberi pulangan dividen yang tinggi namun pemberian tersebut tidak dapat menarik minat anggota untuk meningkatkan tabungan mereka (Henny, 1996). Sehubungan itu, adalah penting kesedaran di kalangan anggota dipertingkatkan agar mereka

32Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

33

memahami peranan mereka sebagai penyumbang modal kepada koperasi, misalnya melalui program pendidikan anggota. Koperasi juga boleh mempertimbangkan untuk menaikkan had minimum syer anggota dengan membawa usul tersebut ke mesyuarat agung bagi mendapat mandat anggota. Dengan berbekalkan modal yang mencukupi akan memudahkan koperasi merancang dan menjalankan aktiviti untuk menjana ekonomi koperasi dan seterusnya menyumbang dalam pembangunan ekonomi negara.

Penggunaan Dana

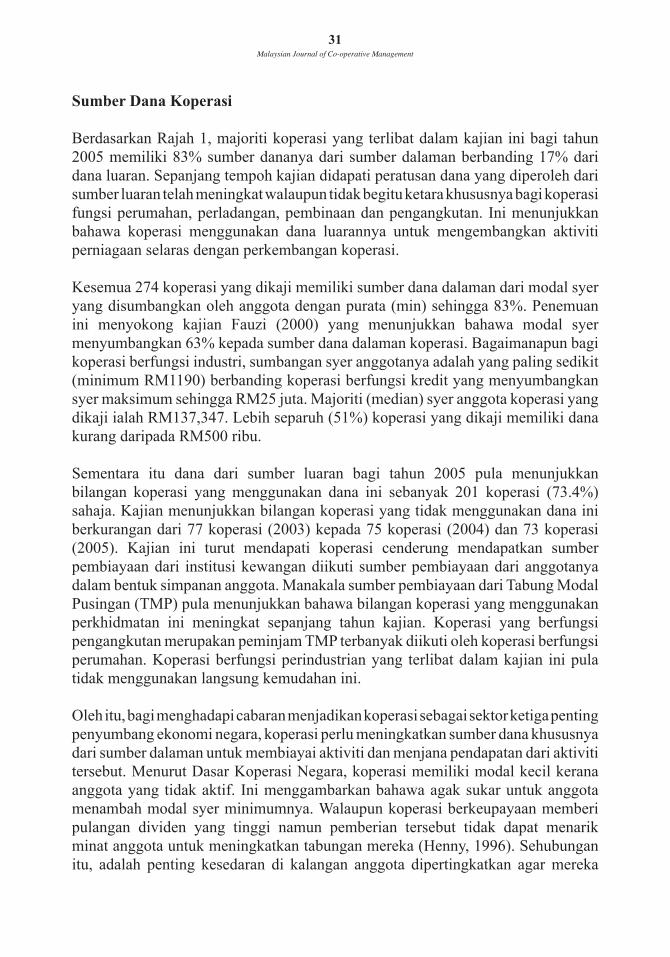

Dengan merujuk kepada Rajah 2, kajian ini menunjukkan pada tahun 2005 koperasi cenderung menggunakan dananya untuk membiayai pelaburan aset (57%) berbanding aktiviti ekonomi (29%) khususnya bagi koperasi berfungsi perladangan, perumahan, pengguna dan pengangkutan. Sepanjang tahun kajian didapati penggunaan dana untuk belanja aktiviti ekonomi dilihat berkurangan berbanding penggunaan dana untuk pelaburan aset yang turun naik tetapi tidak begitu ketara.

Rajah 2: Penggunaan Dana Koperasi (2003 hingga 2005)

Sepanjang tempoh kajian, bilangan koperasi yang melabur dalam pembelian aset telah meningkat dengan nisbah pulangan atas aset atau return on assets (ROA) menunjukkan pulangan yang tinggi. Bilangan koperasi yang mendapat ROA melebihi 1 juga menunjukkan kadar yang meningkat. Ini menandakan koperasi mendapat hasil pulangan yang tinggi untuk setiap ringgit pelaburan dalam asetnya.

0

10

20

30

40

50

60

2003 56.2 33 10.8

2004 58.8 30.5 13.7

2005 57 29.1 13.9

PELABURANASET

AKTIVITI BELANJA AM

PER

AT

US

32Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

33

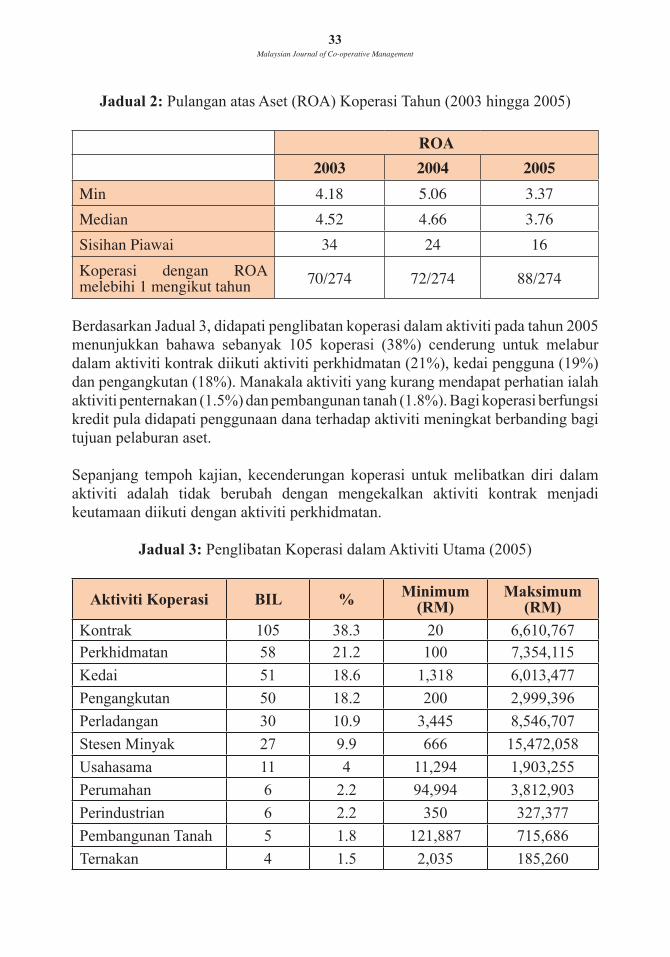

Jadual 2: Pulangan atas Aset (ROA) Koperasi Tahun (2003 hingga 2005)

ROA2003 2004 2005

Min 4.18 5.06 3.37Median 4.52 4.66 3.76Sisihan Piawai 34 24 16Koperasi dengan ROA melebihi 1 mengikut tahun 70/274 72/274 88/274

Berdasarkan Jadual 3, didapati penglibatan koperasi dalam aktiviti pada tahun 2005 menunjukkan bahawa sebanyak 105 koperasi (38%) cenderung untuk melabur dalam aktiviti kontrak diikuti aktiviti perkhidmatan (21%), kedai pengguna (19%) dan pengangkutan (18%). Manakala aktiviti yang kurang mendapat perhatian ialah aktiviti penternakan (1.5%) dan pembangunan tanah (1.8%). Bagi koperasi berfungsi kredit pula didapati penggunaan dana terhadap aktiviti meningkat berbanding bagi tujuan pelaburan aset.

Sepanjang tempoh kajian, kecenderungan koperasi untuk melibatkan diri dalam aktiviti adalah tidak berubah dengan mengekalkan aktiviti kontrak menjadi keutamaan diikuti dengan aktiviti perkhidmatan.

Jadual 3: Penglibatan Koperasi dalam Aktiviti Utama (2005)

Aktiviti Koperasi BIL % Minimum(RM)

Maksimum (RM)

Kontrak 105 38.3 20 6,610,767Perkhidmatan 58 21.2 100 7,354,115

Kedai 51 18.6 1,318 6,013,477

Pengangkutan 50 18.2 200 2,999,396

Perladangan 30 10.9 3,445 8,546,707

Stesen Minyak 27 9.9 666 15,472,058

Usahasama 11 4 11,294 1,903,255

Perumahan 6 2.2 94,994 3,812,903

Perindustrian 6 2.2 350 327,377

Pembangunan Tanah 5 1.8 121,887 715,686

Ternakan 4 1.5 2,035 185,260

34Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

35

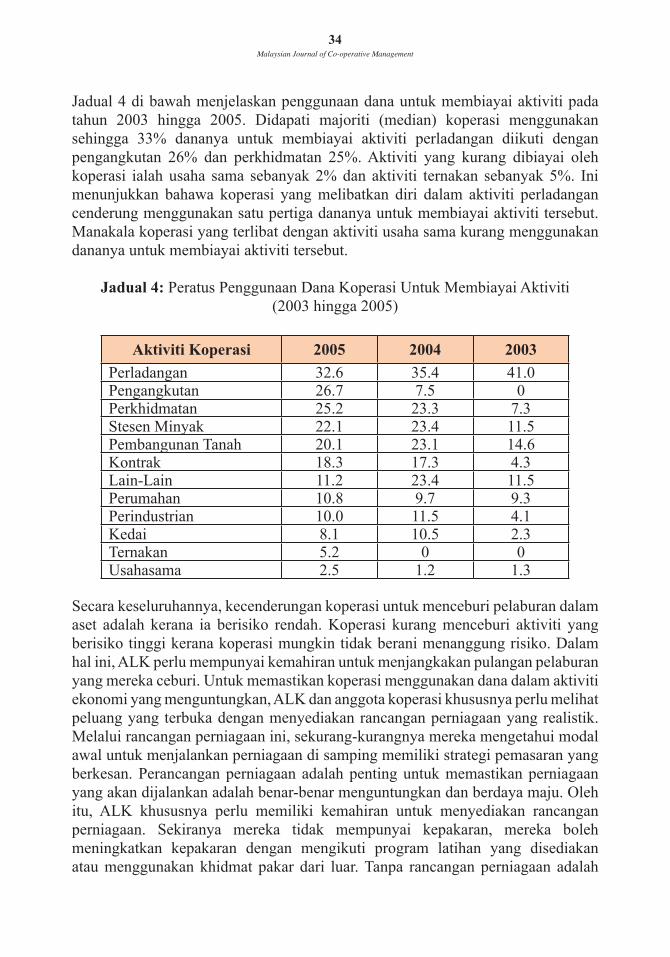

Jadual 4 di bawah menjelaskan penggunaan dana untuk membiayai aktiviti pada tahun 2003 hingga 2005. Didapati majoriti (median) koperasi menggunakan sehingga 33% dananya untuk membiayai aktiviti perladangan diikuti dengan pengangkutan 26% dan perkhidmatan 25%. Aktiviti yang kurang dibiayai oleh koperasi ialah usaha sama sebanyak 2% dan aktiviti ternakan sebanyak 5%. Ini menunjukkan bahawa koperasi yang melibatkan diri dalam aktiviti perladangan cenderung menggunakan satu pertiga dananya untuk membiayai aktiviti tersebut. Manakala koperasi yang terlibat dengan aktiviti usaha sama kurang menggunakan dananya untuk membiayai aktiviti tersebut.

Jadual 4: Peratus Penggunaan Dana Koperasi Untuk Membiayai Aktiviti(2003 hingga 2005)

Aktiviti Koperasi 2005 2004 2003

Perladangan 32.6 35.4 41.0Pengangkutan 26.7 7.5 0Perkhidmatan 25.2 23.3 7.3Stesen Minyak 22.1 23.4 11.5Pembangunan Tanah 20.1 23.1 14.6Kontrak 18.3 17.3 4.3Lain-Lain 11.2 23.4 11.5Perumahan 10.8 9.7 9.3Perindustrian 10.0 11.5 4.1Kedai 8.1 10.5 2.3Ternakan 5.2 0 0Usahasama 2.5 1.2 1.3

Secara keseluruhannya, kecenderungan koperasi untuk menceburi pelaburan dalam aset adalah kerana ia berisiko rendah. Koperasi kurang menceburi aktiviti yang berisiko tinggi kerana koperasi mungkin tidak berani menanggung risiko. Dalam hal ini, ALK perlu mempunyai kemahiran untuk menjangkakan pulangan pelaburan yang mereka ceburi. Untuk memastikan koperasi menggunakan dana dalam aktiviti ekonomi yang menguntungkan, ALK dan anggota koperasi khususnya perlu melihat peluang yang terbuka dengan menyediakan rancangan perniagaan yang realistik. Melalui rancangan perniagaan ini, sekurang-kurangnya mereka mengetahui modal awal untuk menjalankan perniagaan di samping memiliki strategi pemasaran yang berkesan. Perancangan perniagaan adalah penting untuk memastikan perniagaan yang akan dijalankan adalah benar-benar menguntungkan dan berdaya maju. Oleh itu, ALK khususnya perlu memiliki kemahiran untuk menyediakan rancangan perniagaan. Sekiranya mereka tidak mempunyai kepakaran, mereka boleh meningkatkan kepakaran dengan mengikuti program latihan yang disediakan atau menggunakan khidmat pakar dari luar. Tanpa rancangan perniagaan adalah

34Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

35

sukar untuk koperasi menjangkakan sama ada dana yang dilaburkan akan memberi pulangan seperti mana diharapkan. Di samping itu, ALK juga perlu meningkatkan amalan tadbir urus bagi memastikan tindakan mereka adalah mewakili anggota dan bergerak pada landasan yang betul mengikut perundangan koperasi. Dengan adanya tadbir urus yang baik, koperasi dapat ditadbir dan diurus ke arah mencapai matlamat penubuhannya.

Perolehan Pendapatan

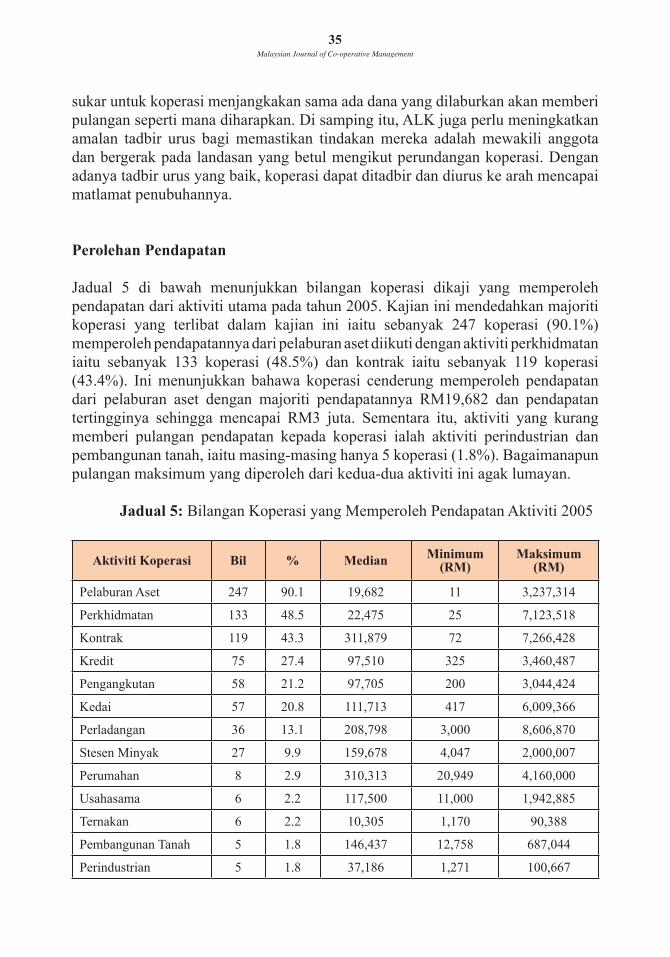

Jadual 5 di bawah menunjukkan bilangan koperasi dikaji yang memperoleh pendapatan dari aktiviti utama pada tahun 2005. Kajian ini mendedahkan majoriti koperasi yang terlibat dalam kajian ini iaitu sebanyak 247 koperasi (90.1%) memperoleh pendapatannya dari pelaburan aset diikuti dengan aktiviti perkhidmatan iaitu sebanyak 133 koperasi (48.5%) dan kontrak iaitu sebanyak 119 koperasi (43.4%). Ini menunjukkan bahawa koperasi cenderung memperoleh pendapatan dari pelaburan aset dengan majoriti pendapatannya RM19,682 dan pendapatan tertingginya sehingga mencapai RM3 juta. Sementara itu, aktiviti yang kurang memberi pulangan pendapatan kepada koperasi ialah aktiviti perindustrian dan pembangunan tanah, iaitu masing-masing hanya 5 koperasi (1.8%). Bagaimanapun pulangan maksimum yang diperoleh dari kedua-dua aktiviti ini agak lumayan.

Jadual 5: Bilangan Koperasi yang Memperoleh Pendapatan Aktiviti 2005

Aktiviti Koperasi Bil % Median Minimum(RM)

Maksimum(RM)

Pelaburan Aset 247 90.1 19,682 11 3,237,314

Perkhidmatan 133 48.5 22,475 25 7,123,518

Kontrak 119 43.3 311,879 72 7,266,428

Kredit 75 27.4 97,510 325 3,460,487

Pengangkutan 58 21.2 97,705 200 3,044,424

Kedai 57 20.8 111,713 417 6,009,366

Perladangan 36 13.1 208,798 3,000 8,606,870

Stesen Minyak 27 9.9 159,678 4,047 2,000,007

Perumahan 8 2.9 310,313 20,949 4,160,000

Usahasama 6 2.2 117,500 11,000 1,942,885

Ternakan 6 2.2 10,305 1,170 90,388

Pembangunan Tanah 5 1.8 146,437 12,758 687,044

Perindustrian 5 1.8 37,186 1,271 100,667

36Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

37

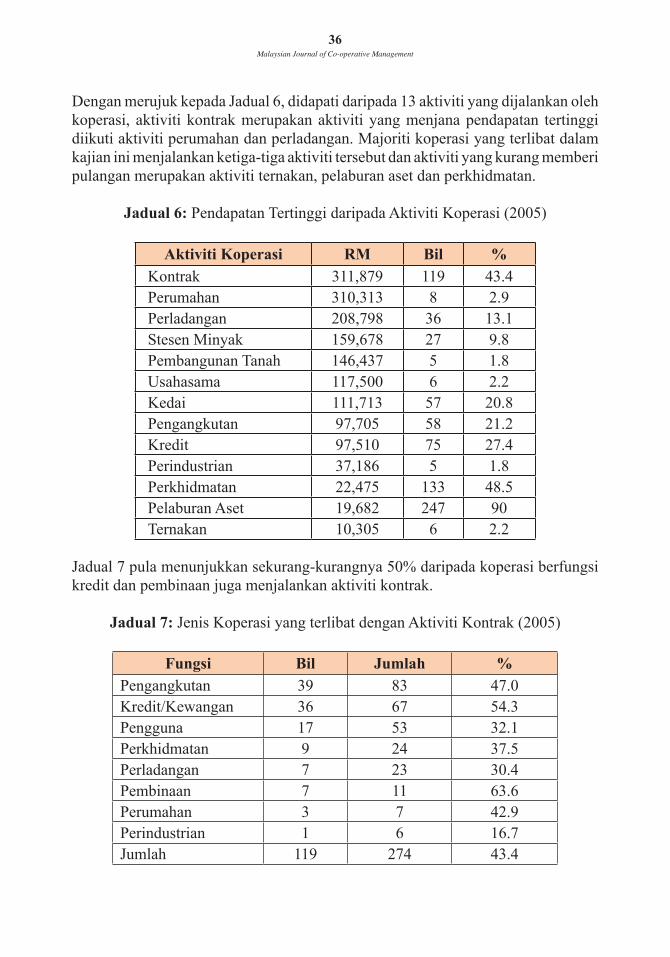

Dengan merujuk kepada Jadual 6, didapati daripada 13 aktiviti yang dijalankan oleh koperasi, aktiviti kontrak merupakan aktiviti yang menjana pendapatan tertinggi diikuti aktiviti perumahan dan perladangan. Majoriti koperasi yang terlibat dalam kajian ini menjalankan ketiga-tiga aktiviti tersebut dan aktiviti yang kurang memberi pulangan merupakan aktiviti ternakan, pelaburan aset dan perkhidmatan.

Jadual 6: Pendapatan Tertinggi daripada Aktiviti Koperasi (2005)

Aktiviti Koperasi RM Bil %Kontrak 311,879 119 43.4Perumahan 310,313 8 2.9Perladangan 208,798 36 13.1Stesen Minyak 159,678 27 9.8Pembangunan Tanah 146,437 5 1.8Usahasama 117,500 6 2.2Kedai 111,713 57 20.8Pengangkutan 97,705 58 21.2Kredit 97,510 75 27.4Perindustrian 37,186 5 1.8Perkhidmatan 22,475 133 48.5Pelaburan Aset 19,682 247 90Ternakan 10,305 6 2.2

Jadual 7 pula menunjukkan sekurang-kurangnya 50% daripada koperasi berfungsi kredit dan pembinaan juga menjalankan aktiviti kontrak.

Jadual 7: Jenis Koperasi yang terlibat dengan Aktiviti Kontrak (2005)

Fungsi Bil Jumlah %Pengangkutan 39 83 47.0Kredit/Kewangan 36 67 54.3Pengguna 17 53 32.1Perkhidmatan 9 24 37.5Perladangan 7 23 30.4Pembinaan 7 11 63.6Perumahan 3 7 42.9Perindustrian 1 6 16.7Jumlah 119 274 43.4

36Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

37

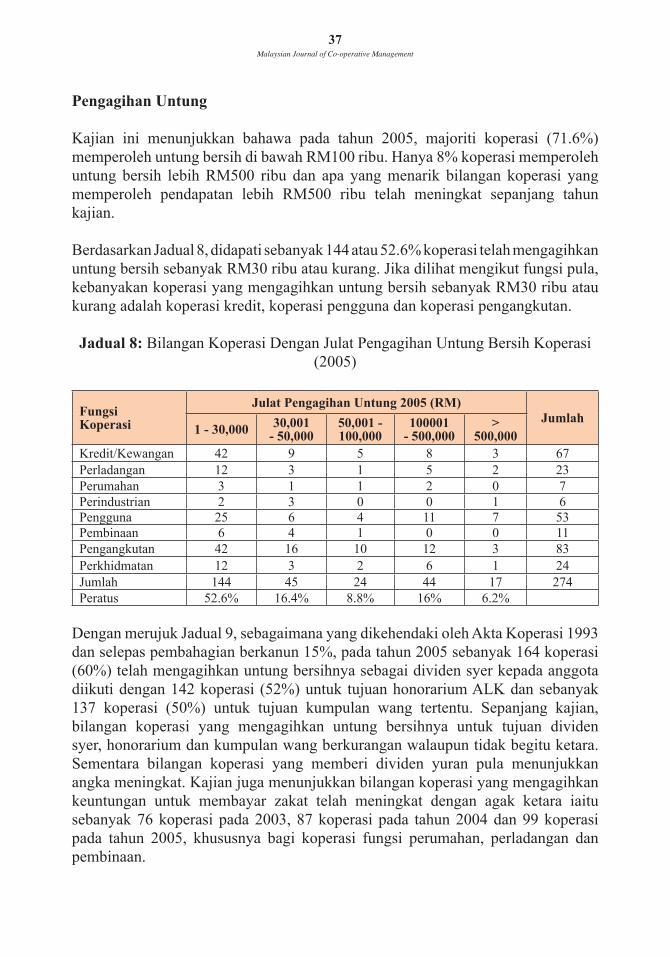

Pengagihan Untung

Kajian ini menunjukkan bahawa pada tahun 2005, majoriti koperasi (71.6%) memperoleh untung bersih di bawah RM100 ribu. Hanya 8% koperasi memperoleh untung bersih lebih RM500 ribu dan apa yang menarik bilangan koperasi yang memperoleh pendapatan lebih RM500 ribu telah meningkat sepanjang tahun kajian.

Berdasarkan Jadual 8, didapati sebanyak 144 atau 52.6% koperasi telah mengagihkan untung bersih sebanyak RM30 ribu atau kurang. Jika dilihat mengikut fungsi pula, kebanyakan koperasi yang mengagihkan untung bersih sebanyak RM30 ribu atau kurang adalah koperasi kredit, koperasi pengguna dan koperasi pengangkutan.

Jadual 8: Bilangan Koperasi Dengan Julat Pengagihan Untung Bersih Koperasi (2005)

Fungsi Koperasi

Julat Pengagihan Untung 2005 (RM)Jumlah

1 - 30,000 30,001 - 50,000

50,001 - 100,000

100001 - 500,000

> 500,000

Kredit/Kewangan 42 9 5 8 3 67Perladangan 12 3 1 5 2 23Perumahan 3 1 1 2 0 7Perindustrian 2 3 0 0 1 6Pengguna 25 6 4 11 7 53Pembinaan 6 4 1 0 0 11Pengangkutan 42 16 10 12 3 83Perkhidmatan 12 3 2 6 1 24Jumlah 144 45 24 44 17 274Peratus 52.6% 16.4% 8.8% 16% 6.2%

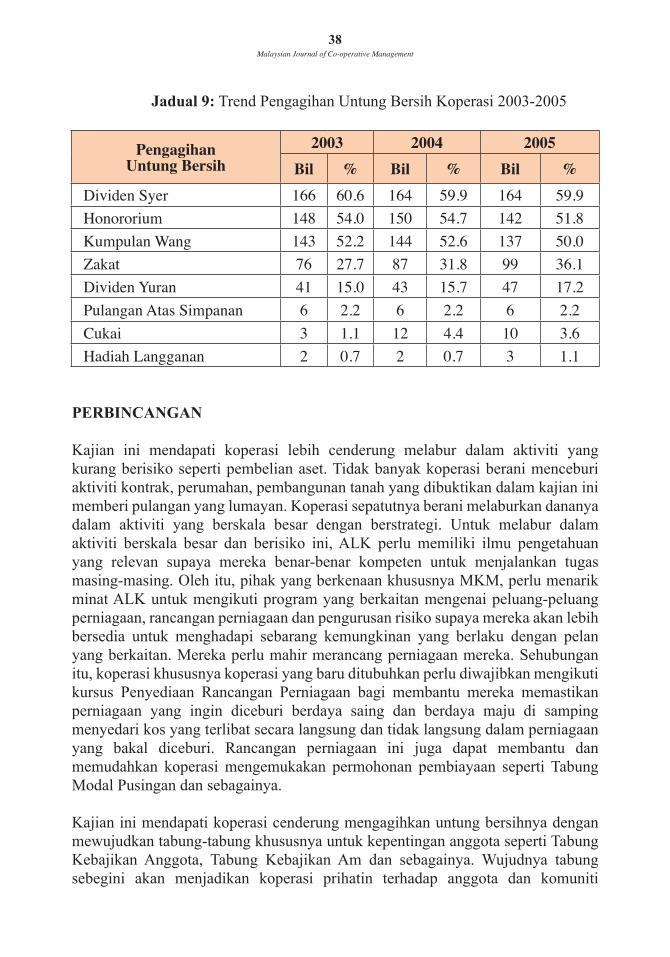

Dengan merujuk Jadual 9, sebagaimana yang dikehendaki oleh Akta Koperasi 1993 dan selepas pembahagian berkanun 15%, pada tahun 2005 sebanyak 164 koperasi (60%) telah mengagihkan untung bersihnya sebagai dividen syer kepada anggota diikuti dengan 142 koperasi (52%) untuk tujuan honorarium ALK dan sebanyak 137 koperasi (50%) untuk tujuan kumpulan wang tertentu. Sepanjang kajian, bilangan koperasi yang mengagihkan untung bersihnya untuk tujuan dividen syer, honorarium dan kumpulan wang berkurangan walaupun tidak begitu ketara. Sementara bilangan koperasi yang memberi dividen yuran pula menunjukkan angka meningkat. Kajian juga menunjukkan bilangan koperasi yang mengagihkan keuntungan untuk membayar zakat telah meningkat dengan agak ketara iaitu sebanyak 76 koperasi pada 2003, 87 koperasi pada tahun 2004 dan 99 koperasi pada tahun 2005, khususnya bagi koperasi fungsi perumahan, perladangan dan pembinaan.

38Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

39

Jadual 9: Trend Pengagihan Untung Bersih Koperasi 2003-2005

PengagihanUntung Bersih

2003 2004 2005Bil % Bil % Bil %

Dividen Syer 166 60.6 164 59.9 164 59.9Honororium 148 54.0 150 54.7 142 51.8Kumpulan Wang 143 52.2 144 52.6 137 50.0Zakat 76 27.7 87 31.8 99 36.1Dividen Yuran 41 15.0 43 15.7 47 17.2Pulangan Atas Simpanan 6 2.2 6 2.2 6 2.2Cukai 3 1.1 12 4.4 10 3.6Hadiah Langganan 2 0.7 2 0.7 3 1.1

PERBINCANGAN

Kajian ini mendapati koperasi lebih cenderung melabur dalam aktiviti yang kurang berisiko seperti pembelian aset. Tidak banyak koperasi berani menceburi aktiviti kontrak, perumahan, pembangunan tanah yang dibuktikan dalam kajian ini memberi pulangan yang lumayan. Koperasi sepatutnya berani melaburkan dananya dalam aktiviti yang berskala besar dengan berstrategi. Untuk melabur dalam aktiviti berskala besar dan berisiko ini, ALK perlu memiliki ilmu pengetahuan yang relevan supaya mereka benar-benar kompeten untuk menjalankan tugas masing-masing. Oleh itu, pihak yang berkenaan khususnya MKM, perlu menarik minat ALK untuk mengikuti program yang berkaitan mengenai peluang-peluang perniagaan, rancangan perniagaan dan pengurusan risiko supaya mereka akan lebih bersedia untuk menghadapi sebarang kemungkinan yang berlaku dengan pelan yang berkaitan. Mereka perlu mahir merancang perniagaan mereka. Sehubungan itu, koperasi khususnya koperasi yang baru ditubuhkan perlu diwajibkan mengikuti kursus Penyediaan Rancangan Perniagaan bagi membantu mereka memastikan perniagaan yang ingin diceburi berdaya saing dan berdaya maju di samping menyedari kos yang terlibat secara langsung dan tidak langsung dalam perniagaan yang bakal diceburi. Rancangan perniagaan ini juga dapat membantu dan memudahkan koperasi mengemukakan permohonan pembiayaan seperti Tabung Modal Pusingan dan sebagainya.

Kajian ini mendapati koperasi cenderung mengagihkan untung bersihnya dengan mewujudkan tabung-tabung khususnya untuk kepentingan anggota seperti Tabung Kebajikan Anggota, Tabung Kebajikan Am dan sebagainya. Wujudnya tabung sebegini akan menjadikan koperasi prihatin terhadap anggota dan komuniti

38Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

39

sekitarnya. Oleh itu, ALK perlu menjadikan koperasi mereka istimewa di kalangan anggota dan secara tidak langsung akan menarik minat anggota untuk terus setia dan menyokong aktiviti yang dijalankan.

Kajian ini tidak mengkaji secara mendalam sumber dan penggunaan dana koperasi. Sehubungan itu, adalah dicadangkan kajian ini diteruskan dengan menjalankan kajian kuantitatif pula yang memberi fokus kepada faktor-faktor yang mempengaruhi penggunaan dana bagi membiayai aktiviti ekonomi koperasi supaya penemuan kajian dapat membantu koperasi memperbaiki kelemahan pentadbiran dan pengurusan seterusnya mampu meningkatkan pulangan pendapatan ke satu tahap yang lebih tinggi lagi.

Kajian ini juga mendapati majoriti ALK kurang menghadiri kursus sedangkan kursus adalah penting untuk meningkatkan kemahiran dan kompetensi mereka. Sehubungan itu, wajarlah pihak yang berkaitan khususnya MKM memainkan peranan untuk menarik minat ALK bagi mengikuti program latihan berkaitan bagi membuka minda mereka supaya dapat mentadbir koperasi sebagaimana usahawan mengurus perniagaannya. SKM juga boleh memainkan peranan dengan mewajibkan setiap ALK mengikuti kursus sekurang-kurangnya 7 hari setahun sebagaimana yang diwajibkan kepada kakitangan di sektor awam. Bagi membolehkan koperasi ditadbir oleh ALK yang berilmu dan kompeten, calon ALK yang hendak bertanding hendaklah disyaratkan telah mengikuti sejumlah program latihan berkaitan koperasi di institusi latihan koperasi. Syarat ini perlu dimasukkan dalam aturan pemilihan ALK dalam mesyuarat agung koperasi. Langkah ini adalah langkah proaktif bagi melahirkan barisan pimpinan koperasi yang berilmu dan kompeten untuk mentadbir koperasi bukan sekadar memenuhi syarat dengan mengikuti kursus wajib sahaja tanpa ada minat untuk mengikuti kursus-kursus yang lain bagi meningkatkan bina upaya ALK.

Walaupun majoriti koperasi memperoleh sebahagian besar sumber dananya dari sumber dalaman, sumbangan minimum RM100 anggota terhadap koperasi perlu ditingkatkan. Sehubungan itu, program kesedaran berkoperasi khususnya program pendidikan anggota boleh memainkan peranan untuk memberi pendedahan dan kefahaman supaya anggota koperasi menambah sumbangan masing-masing. Prinsip koperasi menuntut anggota menyumbangkan modal. Semakin banyak sumbangan yang diberi oleh anggota maka semakin banyaklah dana yang dikumpulkan oleh koperasi untuk digunakan bagi membiayai kegiatan ekonomi ke arah mencapai matlamat penubuhan koperasi. Oleh itu anggota yang baru menyertai koperasi perlu diwajibkan mengikuti program pendidikan anggota bagi membolehkan mereka memainkan peranan dengan lebih berkesan lagi. Koperasi juga perlu membincangkan agenda latihan dan pendidikan dalam mesyuarat bulanan ALK supaya tahap kefahaman koperasi di kalangan anggota dan ALK dapat ditingkatkan.

40Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

41

Senarai latihan yang diikuti oleh anggota dan ALK perlu dimuatkan dalam buku laporan tahunan koperasi untuk dinilai sendiri oleh anggota dalam mesyuarat agung.

KESIMPULAN

Kajian ini telah menunjukkan kebanyakan koperasi memperoleh sebahagian besar sumber dananya (83%) dari sumber dalaman. Situasi ini menjadi petunjuk khususnya kepada koperasi baru agar berdikari menggunakan kekuatan anggota untuk mengumpul dana sendiri seperti mana yang dituntut oleh prinsip koperasi. Kebanyakan koperasi cenderung menggunakan dana untuk membiayai pelaburan dalam aset (57%) berbanding dengan aktiviti ekonomi lain (29%). Kajian ini dapat membantu koperasi baru melihat bahawa aktiviti paling popular yang diceburi oleh majoriti koperasi ialah pelaburan dalam aset (90%) dan perkhidmatan (50%). Manakala aktiviti kontrak merupakan aktiviti yang menjana pendapatan tertinggi untuk koperasi diikuti aktiviti perumahan dan perladangan. Selain itu, majoriti 60% koperasi mengutamakan pengagihan untung bersihnya untuk memberi dividen atas modal syer anggota, 52% koperasi mengagihkannya sebagai honorarium ALK dan 50% koperasi mewujudkan kumpulan wang tertentu.

Berdasarkan penemuan kajian ini, penyelidik mencadangkan agar kajian seterusnya dijalankan dengan mengkaji faktor-faktor yang mempengaruhi anggota untuk menyumbangkan dana kepada koperasi. Memandangkan koperasi mempunyai kekurangan dana, ini menyebabkan koperasi menghadapi kesukaran untuk menjalankan aktivitinya. Penemuan kajian ini juga akan dapat membantu koperasi baru khususnya untuk meningkatkan dana dengan menggunakan kekuatan anggota di samping memperbaiki pengurusan dan pentadbirannya ke arah mengamalkan tadbir urus koperasi yang lebih baik dan berkesan.

Sekiranya cadangan penyelidik diberi perhatian dan diambil tindakan oleh pihak yang terlibat khususnya ALK, penyelidik percaya, koperasi masa hadapan bakal dibarisi oleh anggota yang benar-benar memahami koperasi yang dianggotainya. ALK pula akan lebih berilmu dan kompeten untuk mentadbir koperasi menuju hala tuju yang lebih jelas dan fokus iaitu meningkatkan tahap ekonomi anggota berdasarkan prinsip koperasi. Koperasi pula akan lebih berupaya menceburi aktiviti ekonomi yang berskala besar dan lebih menguntungkan bagi memberi pulangan terbaik untuk anggota selaras dengan matlamat penubuhan koperasi

40Malaysian Journal of Co-operative Management Malaysian Journal of Co-operative Management

41

RUJUKAN

Akta Koperasi 1993 (Akta 502) dan peraturan-peraturan (hingga 25hb Januari 2003). (2003). Kuala Lumpur : International Law Book Services.Kuala Lumpur : International Law Book Services.

A. Ghani Othman. (1980). Mobilisation and investment of funds for cooperative development in Malaysia. Paper presented at the ASEAN Coperative Organization Conference 16-20 March 1980. Manila.

Jabatan Pembangunan Koperasi.(2005). Garis panduan penyeliaan koperasi. Kuala Lumpur: Jabatan Pembangunan Koperasi.

Hasniza Mohd Taib. (2006). Sources and utilization of fund among SMEs. Paper(2006). Sources and utilization of fund among SMEs. PaperPaper presented at The Malaysian Finance Associations 8th Annual Conference 8-9th

May

2006. Kota Kinabalu : Universiti Malaysia Sabah.