ifrs business combinations cases véronique - ibr … 3 business combinations identifying the...

TRANSCRIPT

IFRS 3 Business combinations

Cases

Instituut van de Bedrijfsrevisoren 1 20 November 2009

IFRS 3 – Business combinations

Cases

Véronique Weets

IFRS 3 Business combinations

Cases

Instituut van de Bedrijfsrevisoren 2 20 November 2009

TABLE OF CONTENT

Table of content ..................................................................................................................................................... 2

IFRS 3 ‐ Business combinations ............................................................................................................................... 3

Identifying the acquirer ...................................................................................................................................... 3

Goodwill .............................................................................................................................................................. 6

Measurement period .......................................................................................................................................... 7

Comprehensive case ........................................................................................................................................... 8

Contingent consideration ................................................................................................................................... 9

Bargain purchases ............................................................................................................................................. 10

Business combinations achieved in stages ....................................................................................................... 11

Determining what is part of the business combination transaction ................................................................ 12

Restructurings and liabilities ........................................................................................................................ 12

Employee benefits ........................................................................................................................................ 14

Pre‐existing relationships ............................................................................................................................. 15

Contingent payments to employees or selling shareholders ....................................................................... 16

Share based payments .................................................................................................................................. 17

Intangible assets ............................................................................................................................................... 18

Reverse acquisitions ......................................................................................................................................... 21

Income taxes ..................................................................................................................................................... 23

Impairment of goodwill .................................................................................................................................... 24

IFRS 3 Business combinations

Identifying the acquirer

Instituut van de Bedrijfsrevisoren 3 20 November 2009

IFRS 3 ‐ BUSINESS COMBINATIONS

IDENTIFYING THE ACQUIRER

1. Mocas owns three subsidiaries that are all independent entities; Hara, Neb and Luc. Mocas owns the

following percentage of each subsidiary: Hara 80%, Neb 60%, Luc 55%. Neb purchases Luc.

What IFRS governs the accounting treatment of Neb’s acquisition of Luc?

2. Entity A owns 40 shares of the 100 shares of D. The remaining shares of D are owned by B (55 shares)

and C (5shares). D offers its shareholders the right to sell in their shares at fair value. Only B accepts the offer

and sells 30 shares.

Does the transaction represents a business combination ?

3. An entity may decide to outsource its information technology or call centre operations to a third

party. Before the outsourcing, these functions generally will have been operated as a cost centre for the

business as a whole, rather than as a business per se. Generally, the staff, plant and equipment and other

working capital of the outsourced department are transferred to the third party, and a contractual

arrangement entered into with the third party for the provision of the service to the outsourcing entity on an

ongoing basis.

Does the transaction represents a business combination ?

4. A public limited Entity, owns 50% of B and 49% of C. There is an agreement with the shareholders of C

that the group will control the board of directors (Wiley workbook and guide, 2006, pg 338).

Should C be considered to be a subsidiary in the group accounts ?

5. Entity A wholly‐owns the share capital of Entity B, Entity C and Entity D. In turn Entities B,C and D each

own 17% of Entity E’s share capital (PWC, chapter 24).

Does A control E ?

6. Entity A owns 45% of the voting shares of Entity B. Entity A also has an agreement with other

shareholders that they will always vote a further 20% holding in the same way as Entity A (PWC, chapter 24).

Does A control B ?

7. Three Entities A, B and C invest in Entity D to manufacture footballs. Entity A has considerable

experience in manufacturing footballs and has developed new technology to improve their production. Entity

B and Entity C are both banks that have previously financed Entity A’s operations. Entity A will contribute

technology and know‐how to Entity D, whilst Entity B and Entity C will contribute finance. The share ownership

will be Entity A: 40%, Entity B: 30% and Entity C/ 30%. Each Entity will appoint directors in proportion to their

ownership percentage. An agreement between the shareholders states that all directors will be non‐executive

except for the managing director and the finance director, both of whom will be appointed by Entity A in

recognition of its expertise in the area of football manufacture. The shareholder agreement delegates to Entity

A’s managing director and its finance director the power to set Entity D’s operating policies and operating

budget. However, requests for additional financing must be considered by the board (PWC, chapter 24).

Which entity controls D ?

IFRS 3 Business combinations

Identifying the acquirer

Instituut van de Bedrijfsrevisoren 4 20 November 2009

8. Entity A controls the composition of Entity B’s board. The board of directors of Entity B has seven

members, four appointed by Entity A and three appointed by Entity C. One of the directors of Entity A rarely

attends board meetings and strategic decisions are often taken by the majority vote of the remaining board

members. That is, three from Entity A and three from Entity C (PWC, chapter 24).

Which entity has to consolidate B ?

9. Entity A owns 45% of the shares in Entity B, but controls the composition of its board of directors by

having the power to appoint or remove the majority of Entity B’s directors (PWC, chapter 24).

Should A consolidate B ?

10. Entity A owns 50% of the voting shares of Entity B. The board of directors consist of eight members.

Entity A appoints four directors and two other investors appoint two directors each. One of Entity A’s

nominated directors always serves as chairman of Entity B’s board and has the casting vote at board meetings

(PWC, chapter 24).

Does A control B ?

11. Entity A and Entity B own 80% and 20% respectively of the ordinary shares that carry voting rights at a

general meeting of shareholders of Entity C. Entity A sells one‐half of its interest to Entity D and buys call

options from Entity D that are exercisable at any time at a premium to the market price on issue. If the options

are exercised they would give Entity A its original 80% ownership interest and equivalent voting rights. The

exercise price is not deliberately set so high that the possibility of exercise is remote (IAS 27 IG8).

Which entity controls C ?

12. Entity A,B and C own 40%, 30% and 30% respectively of the ordinary shares that carry voting rights at

a general meeting of shareholders of Entity D. Entity A also owns call options that are exercisable at any time

at the fair value of the underlying shares and if exercised would give it an additional 20% of the voting rights in

Entity D and reduce Entity B’s and Entity C’s interest to 20% each. If the options are exercised Entity A would

have control over more than 50% of the voting power of Entity D (IAS 27, IG 8).

Which entity has to consolidate D ?

13. Entities A, B and C own 25%, 35% and 40% respectively of the ordinary shares that carry voting rights

at a general meeting of shareholders of Entity D. Entities B and C also have share warrants that are exercisable

at any time at a fixed price and provide potential voting rights. Entity A has a call option to purchase these

share warrants at any time for a nominal amount, and, if the call option is exercised, would give Entity A the

potential to increase its ownership interest, and thereby its voting rights, in Entity D to 51% (and dilute Entity

B’s interest to 23% and Entity C’s interest to 26%) (IAS 27, IG 8).

Which entity has to consolidate D ?

14. Entities A, B and C each own 33% of the ordinary shares that carry voting rights at a general meeting

of shareholders of Entity D. Entities A,B and C each have the right to appoint two directors to the board of

directors of Entity D. Entity A also owns call options that are exercisable at a fixed price (that is not excessive)

at any time and if exercised would give it all the voting rights in Entity D. Entity A’s management does not

intend to exercise the call options even if Entities B and C do not vote in the same manner as Entity A (IAS 27,

IG 8).

Does entity A control entity D ?

IFRS 3 Business combinations

Identifying the acquirer

Instituut van de Bedrijfsrevisoren 5 20 November 2009

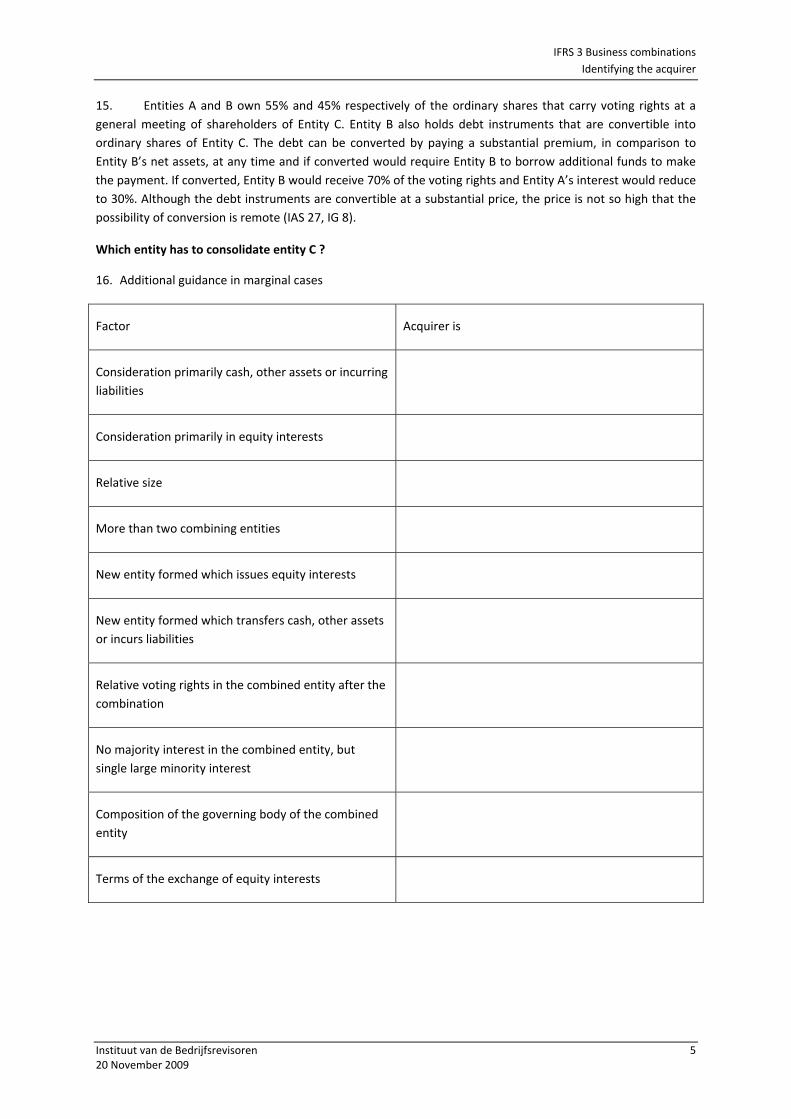

15. Entities A and B own 55% and 45% respectively of the ordinary shares that carry voting rights at a

general meeting of shareholders of Entity C. Entity B also holds debt instruments that are convertible into

ordinary shares of Entity C. The debt can be converted by paying a substantial premium, in comparison to

Entity B’s net assets, at any time and if converted would require Entity B to borrow additional funds to make

the payment. If converted, Entity B would receive 70% of the voting rights and Entity A’s interest would reduce

to 30%. Although the debt instruments are convertible at a substantial price, the price is not so high that the

possibility of conversion is remote (IAS 27, IG 8).

Which entity has to consolidate entity C ?

16. Additional guidance in marginal cases

Factor Acquirer is

Consideration primarily cash, other assets or incurring

liabilities

Consideration primarily in equity interests

Relative size

More than two combining entities

New entity formed which issues equity interests

New entity formed which transfers cash, other assets

or incurs liabilities

Relative voting rights in the combined entity after the

combination

No majority interest in the combined entity, but

single large minority interest

Composition of the governing body of the combined

entity

Terms of the exchange of equity interests

IFRS 3 Business combinations

Goodwill

Instituut van de Bedrijfsrevisoren 6 20 November 2009

GOODWILL

1. Consider the following information (ACCA, pg 2308)

At 31 December 20X5 Parent Subsidiary Cu CU

Non‐current assets Tangibles 1 000 800Cost of investment in Subsidiary 1 200

Net current assets 400 200

2 600 1 000

Issued capital 100 900Retained earnings 2 500 100

2 600 1 000

Parent bought 100% of Subsidiary on 31 December 20X5

Subsidiary's reserves are CU 100 at the date of acquisition

Calculate the goodwill and prepare the consolidated balance sheet at 31 December 20X5

2. Mocas purchased 75% of the capital of Haraf for CU 250 000 on 1 July 20X0. at this date the equity of

Haraf was:

CU

Share capital 100 000General reserve 60 000Retained earnings 40 000

At this date Haraf had not recorded any goodwill, and all identifiable assets and liabilities were recorded at fair

value except for the following cases:

Carrying amount Fair value CU CU

Inventory 70 000 100 000 Plant (cost CU 170 000) 150 000 190 000 Land 50 000 100 000

The tax rate is 30%.

Calculate the goodwill and determine the journal entries related to the business combination

a. If the non‐controlling interest is measured at its fair value of 80 000

b. If the non‐controlling interest is measured at its proportionate share in the net assets of Haraf

IFRS 3 Business combinations

Measurement period

Instituut van de Bedrijfsrevisoren 7 20 November 2009

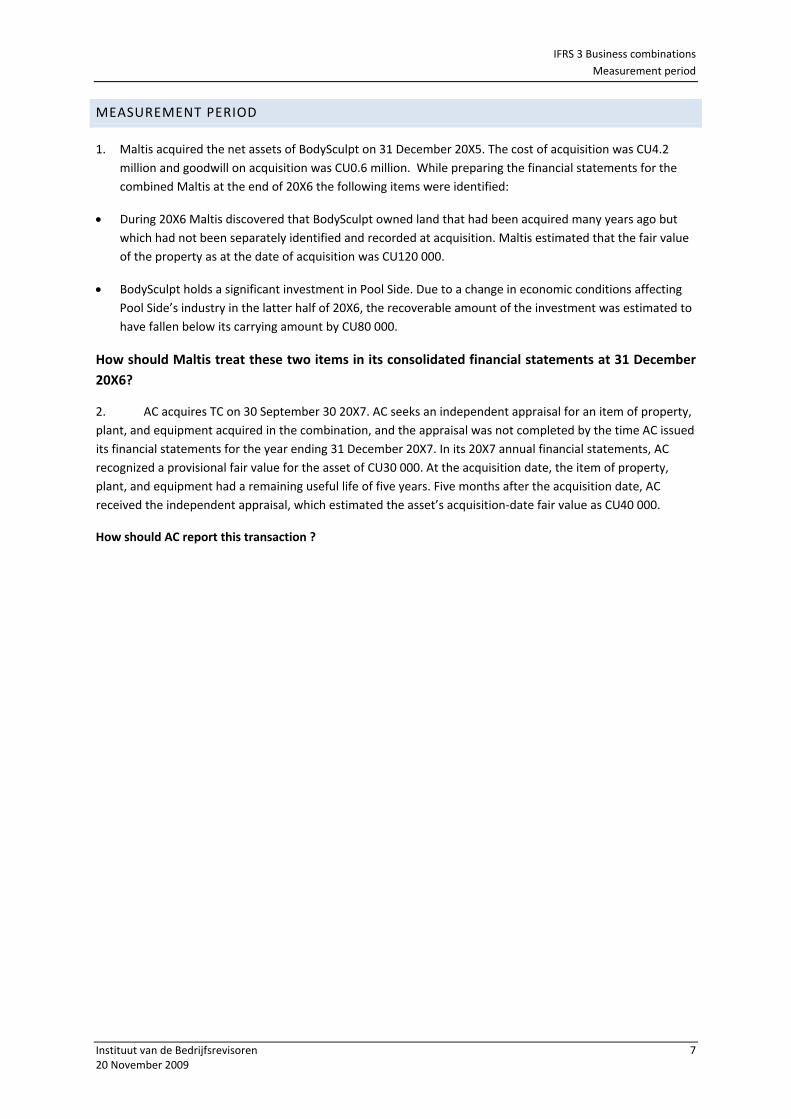

MEASUREMENT PERIOD

1. Maltis acquired the net assets of BodySculpt on 31 December 20X5. The cost of acquisition was CU4.2

million and goodwill on acquisition was CU0.6 million. While preparing the financial statements for the

combined Maltis at the end of 20X6 the following items were identified:

During 20X6 Maltis discovered that BodySculpt owned land that had been acquired many years ago but

which had not been separately identified and recorded at acquisition. Maltis estimated that the fair value

of the property as at the date of acquisition was CU120 000.

BodySculpt holds a significant investment in Pool Side. Due to a change in economic conditions affecting

Pool Side’s industry in the latter half of 20X6, the recoverable amount of the investment was estimated to

have fallen below its carrying amount by CU80 000.

How should Maltis treat these two items in its consolidated financial statements at 31 December

20X6?

2. AC acquires TC on 30 September 30 20X7. AC seeks an independent appraisal for an item of property,

plant, and equipment acquired in the combination, and the appraisal was not completed by the time AC issued

its financial statements for the year ending 31 December 20X7. In its 20X7 annual financial statements, AC

recognized a provisional fair value for the asset of CU30 000. At the acquisition date, the item of property,

plant, and equipment had a remaining useful life of five years. Five months after the acquisition date, AC

received the independent appraisal, which estimated the asset’s acquisition‐date fair value as CU40 000.

How should AC report this transaction ?

IFRS 3 Business combinations

Comprehensive case

Instituut van de Bedrijfsrevisoren 8 20 November 2009

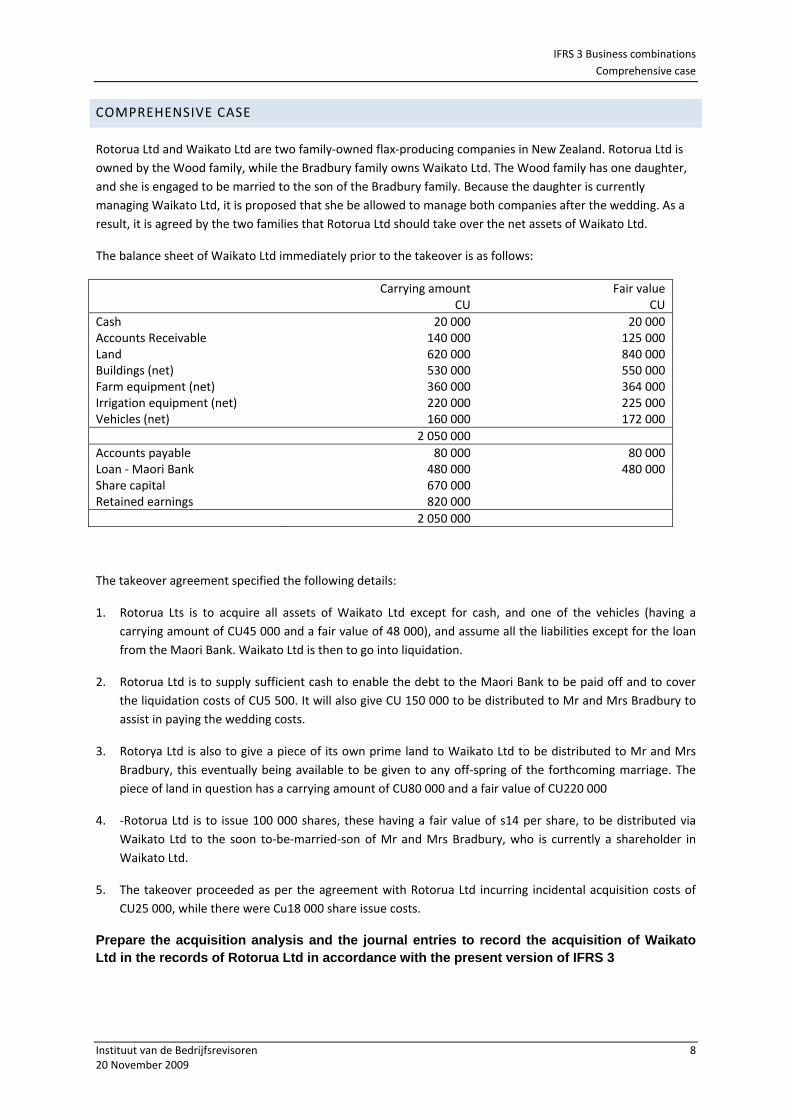

COMPREHENSIVE CASE

Rotorua Ltd and Waikato Ltd are two family‐owned flax‐producing companies in New Zealand. Rotorua Ltd is

owned by the Wood family, while the Bradbury family owns Waikato Ltd. The Wood family has one daughter,

and she is engaged to be married to the son of the Bradbury family. Because the daughter is currently

managing Waikato Ltd, it is proposed that she be allowed to manage both companies after the wedding. As a

result, it is agreed by the two families that Rotorua Ltd should take over the net assets of Waikato Ltd.

The balance sheet of Waikato Ltd immediately prior to the takeover is as follows:

Carrying amount

CU Fair value

CU

Cash 20 000 20 000Accounts Receivable 140 000 125 000Land 620 000 840 000Buildings (net) 530 000 550 000Farm equipment (net) 360 000 364 000Irrigation equipment (net) 220 000 225 000Vehicles (net) 160 000 172 000

2 050 000

Accounts payable 80 000 80 000Loan ‐ Maori Bank 480 000 480 000Share capital 670 000Retained earnings 820 000

2 050 000

The takeover agreement specified the following details:

1. Rotorua Lts is to acquire all assets of Waikato Ltd except for cash, and one of the vehicles (having a

carrying amount of CU45 000 and a fair value of 48 000), and assume all the liabilities except for the loan

from the Maori Bank. Waikato Ltd is then to go into liquidation.

2. Rotorua Ltd is to supply sufficient cash to enable the debt to the Maori Bank to be paid off and to cover

the liquidation costs of CU5 500. It will also give CU 150 000 to be distributed to Mr and Mrs Bradbury to

assist in paying the wedding costs.

3. Rotorya Ltd is also to give a piece of its own prime land to Waikato Ltd to be distributed to Mr and Mrs

Bradbury, this eventually being available to be given to any off‐spring of the forthcoming marriage. The

piece of land in question has a carrying amount of CU80 000 and a fair value of CU220 000

4. ‐Rotorua Ltd is to issue 100 000 shares, these having a fair value of s14 per share, to be distributed via

Waikato Ltd to the soon to‐be‐married‐son of Mr and Mrs Bradbury, who is currently a shareholder in

Waikato Ltd.

5. The takeover proceeded as per the agreement with Rotorua Ltd incurring incidental acquisition costs of

CU25 000, while there were Cu18 000 share issue costs.

Prepare the acquisition analysis and the journal entries to record the acquisition of Waikato Ltd in the records of Rotorua Ltd in accordance with the present version of IFRS 3

IFRS 3 Business combinations

Contingent consideration

Instituut van de Bedrijfsrevisoren 9 20 November 2009

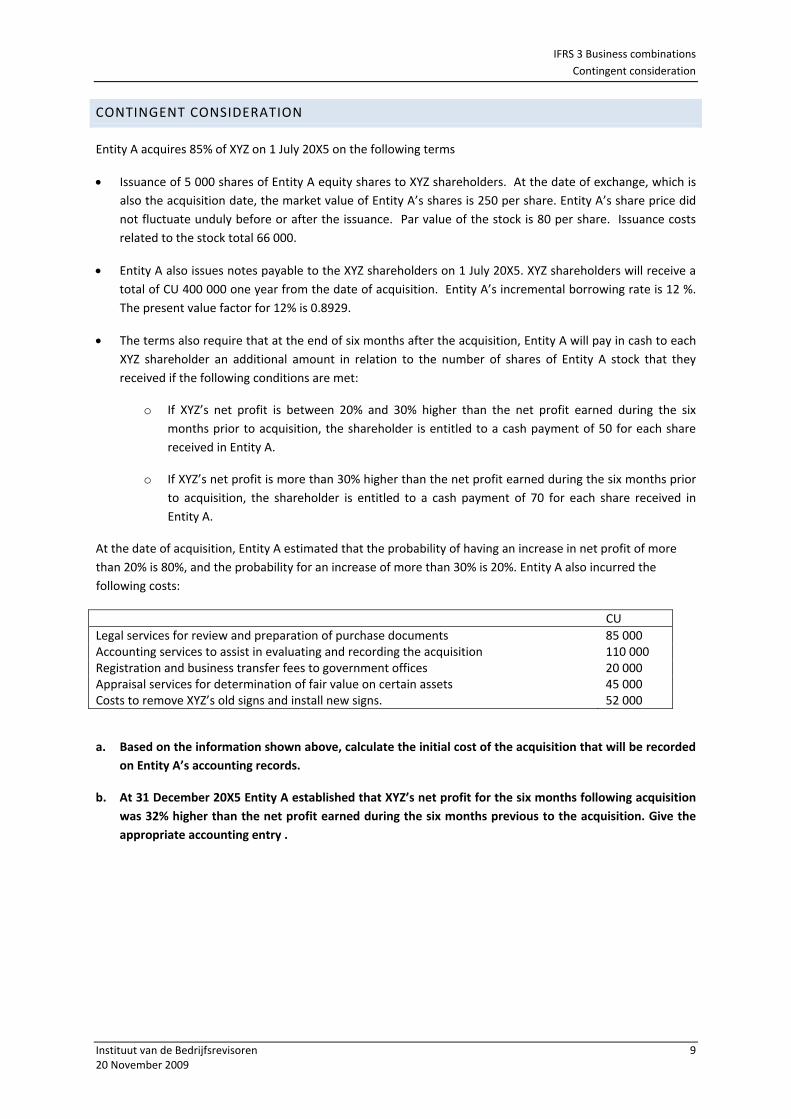

CONTINGENT CONSIDERATION

Entity A acquires 85% of XYZ on 1 July 20X5 on the following terms

Issuance of 5 000 shares of Entity A equity shares to XYZ shareholders. At the date of exchange, which is

also the acquisition date, the market value of Entity A’s shares is 250 per share. Entity A’s share price did

not fluctuate unduly before or after the issuance. Par value of the stock is 80 per share. Issuance costs

related to the stock total 66 000.

Entity A also issues notes payable to the XYZ shareholders on 1 July 20X5. XYZ shareholders will receive a

total of CU 400 000 one year from the date of acquisition. Entity A’s incremental borrowing rate is 12 %.

The present value factor for 12% is 0.8929.

The terms also require that at the end of six months after the acquisition, Entity A will pay in cash to each

XYZ shareholder an additional amount in relation to the number of shares of Entity A stock that they

received if the following conditions are met:

o If XYZ’s net profit is between 20% and 30% higher than the net profit earned during the six

months prior to acquisition, the shareholder is entitled to a cash payment of 50 for each share

received in Entity A.

o If XYZ’s net profit is more than 30% higher than the net profit earned during the six months prior

to acquisition, the shareholder is entitled to a cash payment of 70 for each share received in

Entity A.

At the date of acquisition, Entity A estimated that the probability of having an increase in net profit of more

than 20% is 80%, and the probability for an increase of more than 30% is 20%. Entity A also incurred the

following costs:

CU

Legal services for review and preparation of purchase documents 85 000 Accounting services to assist in evaluating and recording the acquisition 110 000 Registration and business transfer fees to government offices 20 000 Appraisal services for determination of fair value on certain assets 45 000 Costs to remove XYZ’s old signs and install new signs. 52 000

a. Based on the information shown above, calculate the initial cost of the acquisition that will be recorded

on Entity A’s accounting records.

b. At 31 December 20X5 Entity A established that XYZ’s net profit for the six months following acquisition

was 32% higher than the net profit earned during the six months previous to the acquisition. Give the

appropriate accounting entry .

IFRS 3 Business combinations

Bargain purchases

Instituut van de Bedrijfsrevisoren 10 20 November 2009

BARGAIN PURCHASES

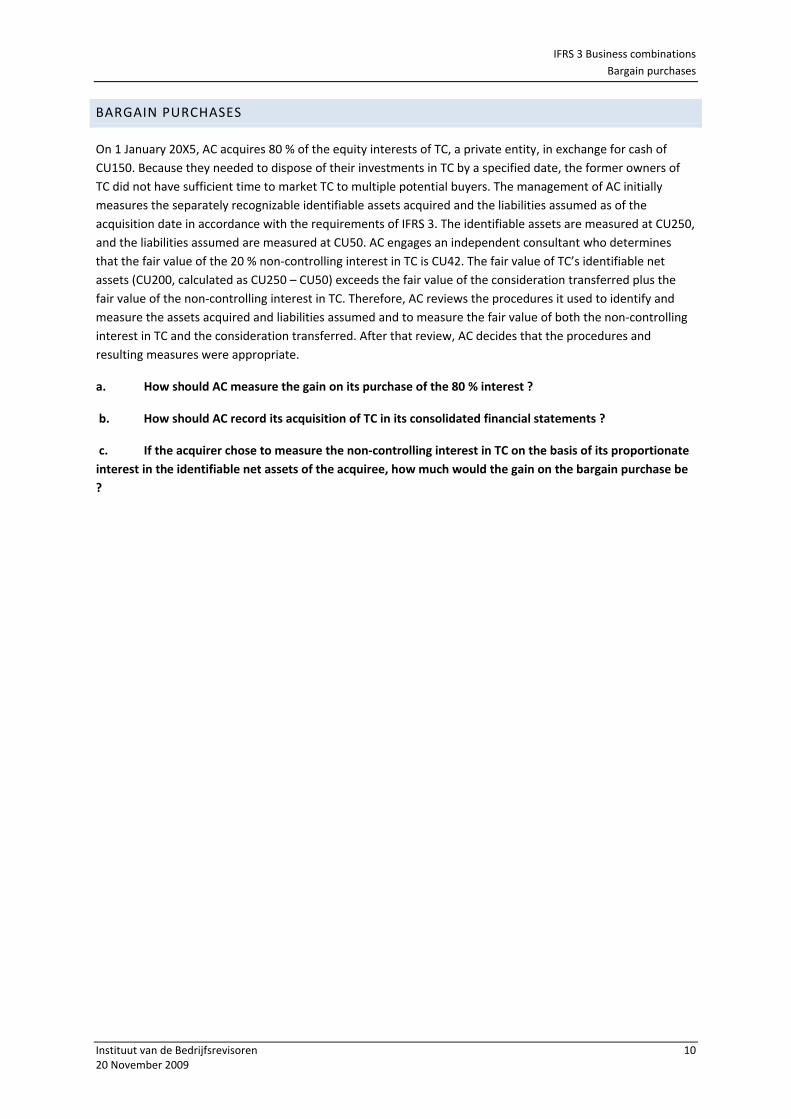

On 1 January 20X5, AC acquires 80 % of the equity interests of TC, a private entity, in exchange for cash of

CU150. Because they needed to dispose of their investments in TC by a specified date, the former owners of

TC did not have sufficient time to market TC to multiple potential buyers. The management of AC initially

measures the separately recognizable identifiable assets acquired and the liabilities assumed as of the

acquisition date in accordance with the requirements of IFRS 3. The identifiable assets are measured at CU250,

and the liabilities assumed are measured at CU50. AC engages an independent consultant who determines

that the fair value of the 20 % non‐controlling interest in TC is CU42. The fair value of TC’s identifiable net

assets (CU200, calculated as CU250 – CU50) exceeds the fair value of the consideration transferred plus the

fair value of the non‐controlling interest in TC. Therefore, AC reviews the procedures it used to identify and

measure the assets acquired and liabilities assumed and to measure the fair value of both the non‐controlling

interest in TC and the consideration transferred. After that review, AC decides that the procedures and

resulting measures were appropriate.

a. How should AC measure the gain on its purchase of the 80 % interest ?

b. How should AC record its acquisition of TC in its consolidated financial statements ?

c. If the acquirer chose to measure the non‐controlling interest in TC on the basis of its proportionate

interest in the identifiable net assets of the acquiree, how much would the gain on the bargain purchase be

?

IFRS 3 Business combinations

Business combinations achieved in stages

Instituut van de Bedrijfsrevisoren 11 20 November 2009

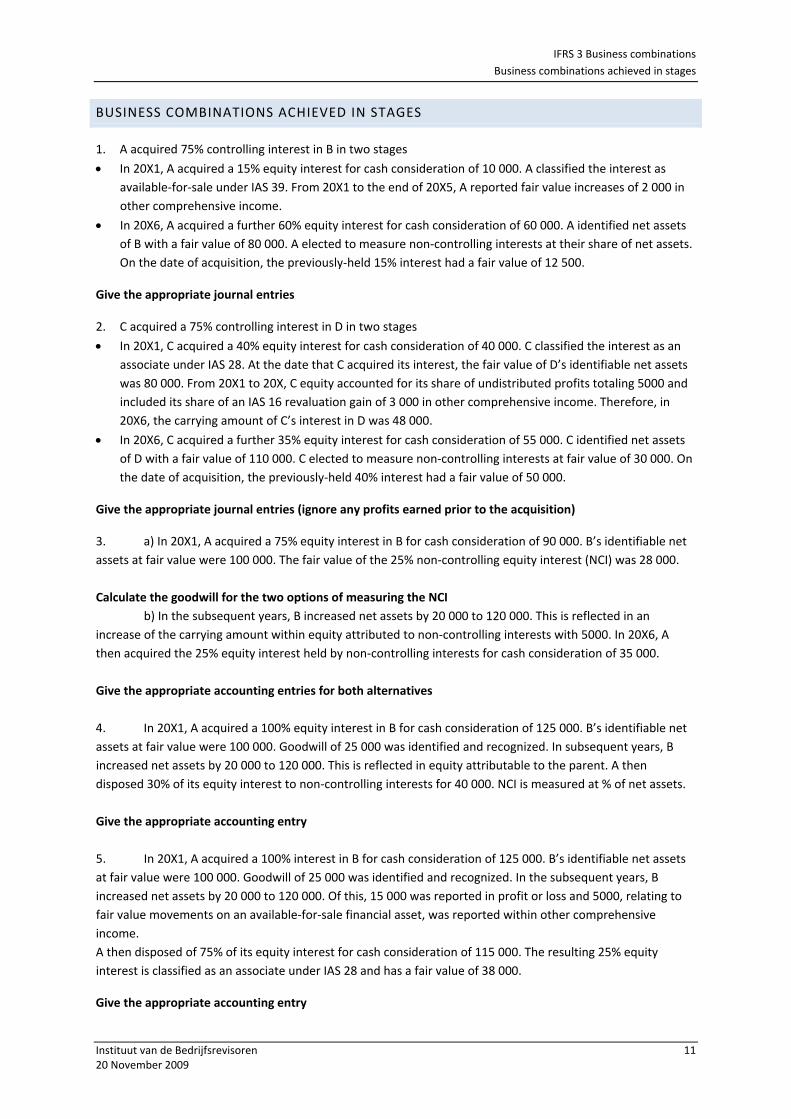

BUSINESS COMBINATIONS ACHIEVED IN STAGES

1. A acquired 75% controlling interest in B in two stages

In 20X1, A acquired a 15% equity interest for cash consideration of 10 000. A classified the interest as

available‐for‐sale under IAS 39. From 20X1 to the end of 20X5, A reported fair value increases of 2 000 in

other comprehensive income.

In 20X6, A acquired a further 60% equity interest for cash consideration of 60 000. A identified net assets

of B with a fair value of 80 000. A elected to measure non‐controlling interests at their share of net assets.

On the date of acquisition, the previously‐held 15% interest had a fair value of 12 500.

Give the appropriate journal entries

2. C acquired a 75% controlling interest in D in two stages

In 20X1, C acquired a 40% equity interest for cash consideration of 40 000. C classified the interest as an

associate under IAS 28. At the date that C acquired its interest, the fair value of D’s identifiable net assets

was 80 000. From 20X1 to 20X, C equity accounted for its share of undistributed profits totaling 5000 and

included its share of an IAS 16 revaluation gain of 3 000 in other comprehensive income. Therefore, in

20X6, the carrying amount of C’s interest in D was 48 000.

In 20X6, C acquired a further 35% equity interest for cash consideration of 55 000. C identified net assets

of D with a fair value of 110 000. C elected to measure non‐controlling interests at fair value of 30 000. On

the date of acquisition, the previously‐held 40% interest had a fair value of 50 000.

Give the appropriate journal entries (ignore any profits earned prior to the acquisition)

3. a) In 20X1, A acquired a 75% equity interest in B for cash consideration of 90 000. B’s identifiable net

assets at fair value were 100 000. The fair value of the 25% non‐controlling equity interest (NCI) was 28 000.

Calculate the goodwill for the two options of measuring the NCI

b) In the subsequent years, B increased net assets by 20 000 to 120 000. This is reflected in an

increase of the carrying amount within equity attributed to non‐controlling interests with 5000. In 20X6, A

then acquired the 25% equity interest held by non‐controlling interests for cash consideration of 35 000.

Give the appropriate accounting entries for both alternatives

4. In 20X1, A acquired a 100% equity interest in B for cash consideration of 125 000. B’s identifiable net

assets at fair value were 100 000. Goodwill of 25 000 was identified and recognized. In subsequent years, B

increased net assets by 20 000 to 120 000. This is reflected in equity attributable to the parent. A then

disposed 30% of its equity interest to non‐controlling interests for 40 000. NCI is measured at % of net assets.

Give the appropriate accounting entry

5. In 20X1, A acquired a 100% interest in B for cash consideration of 125 000. B’s identifiable net assets

at fair value were 100 000. Goodwill of 25 000 was identified and recognized. In the subsequent years, B

increased net assets by 20 000 to 120 000. Of this, 15 000 was reported in profit or loss and 5000, relating to

fair value movements on an available‐for‐sale financial asset, was reported within other comprehensive

income.

A then disposed of 75% of its equity interest for cash consideration of 115 000. The resulting 25% equity

interest is classified as an associate under IAS 28 and has a fair value of 38 000.

Give the appropriate accounting entry

IFRS 3 Business combinations

Determining what is part of the business combination

Instituut van de Bedrijfsrevisoren 12 20 November 2009

DETERMINING WHAT IS PART OF THE BUSINESS COMBINATION TRANSACTION

RESTRUCTURINGS AND LIABILITIES

1. Company A acquires company B, effective 1 March 20X5. At the date of acquisition, company A

intends to close a division of company B. As at the date of acquisition, management has developed and the

board has approved the main features of the restructuring plan and, based on available information, best

estimates of the costs have been made. As at the date of acquisition, a public announcement of company A’s

intentions has been made and relevant parties have been informed of the planned closure. Within in a week of

the acquisition being effected, management commences the process of informing unions, lessors, institutional

investors and other key shareholders of the broad characteristics of its restructuring program. A detailed plan

for the restructuring is developed within three months and implemented soon thereafter.

Should company A create a provision for restructuring as part of its acquisition accounting entries?

How would your answer change if all the circumstances are the same as those above except that company A

decided that, instead of closing a division of company B, it would close down one of its own facilities?

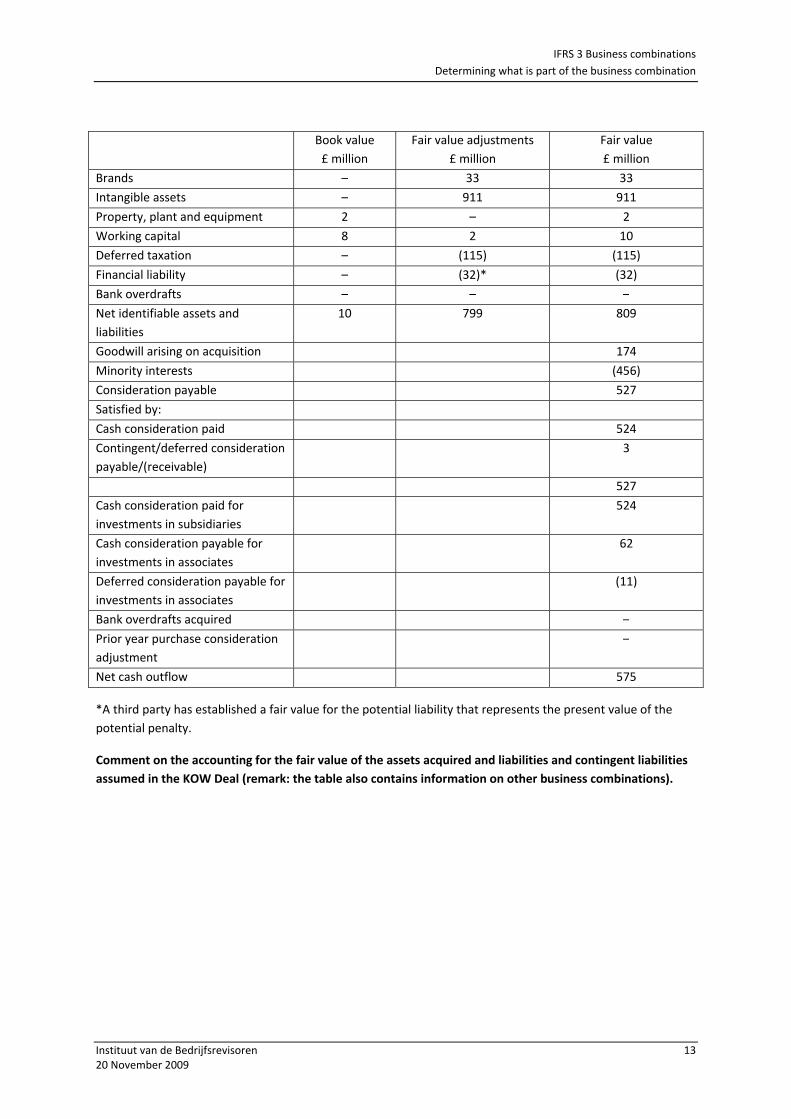

2. On 9 June 2008, Diageo completed the acquisition of Ketel One Worldwide BV (KOW), a 50:50

company based in the Netherlands, which owns the exclusive and perpetual global rights to market, sell and

distribute Ketel One vodka products. Diageo paid £471 million for a 50% equity stake in KOW. Additional costs

relating to the acquisition of £2 million are expected to be incurred in the year ending 30 June 2009.

Diageo controls the operating and financial policies of the company and consolidates 100% of KOW with a 50%

minority interest. The Nolet Group has an option to sell their 50% equity stake in the company to Diageo for

$900 million (£452 million) plus interest from 9 June 2011 to 9 June 2013. If the Nolet Group exercises this

option but Diageo chooses not to buy their stake, Diageo will pay $100 million (£50 million) and the Nolet

Group may then pursue a sale of their stake to a third party, subject to rights of first offer and last refusal on

Diageo’s part. Fair value adjustments include the recognition of worldwide distribution rights into perpetuity

of Ketel One vodka products of £911 million, the establishment of a deferred tax liability of £116 million and

the creation of a financial liability at fair value of £32 million for the potential amount payable to the Nolet

Group. Goodwill of £166 million arose on the acquisition (Diageo, annual report 2008).

IFRS 3 Business combinations

Determining what is part of the business combination

Instituut van de Bedrijfsrevisoren 13 20 November 2009

Book value

£ million

Fair value adjustments

£ million

Fair value

£ million

Brands – 33 33

Intangible assets – 911 911

Property, plant and equipment 2 – 2

Working capital 8 2 10

Deferred taxation – (115) (115)

Financial liability – (32)* (32)

Bank overdrafts – – –

Net identifiable assets and

liabilities

10 799 809

Goodwill arising on acquisition 174

Minority interests (456)

Consideration payable 527

Satisfied by:

Cash consideration paid 524

Contingent/deferred consideration

payable/(receivable)

3

527

Cash consideration paid for

investments in subsidiaries

524

Cash consideration payable for

investments in associates

62

Deferred consideration payable for

investments in associates

(11)

Bank overdrafts acquired –

Prior year purchase consideration

adjustment

–

Net cash outflow 575

*A third party has established a fair value for the potential liability that represents the present value of the

potential penalty.

Comment on the accounting for the fair value of the assets acquired and liabilities and contingent liabilities

assumed in the KOW Deal (remark: the table also contains information on other business combinations).

IFRS 3 Business combinations

Determining what is part of the business combination

Instituut van de Bedrijfsrevisoren 14 20 November 2009

EMPLOYEE BENEFITS

TC appointed a candidate as its new CEO under a ten‐year contract. The contract required TC to pay the

candidate 5 million if TC is acquired before the contract expires. AC acquires TC eight years later. The CEO was

still employed at the acquisition date and will receive the additional payment under the existing contract.

Should company A create a provision for this payment as part of its acquisition accounting entries?

Would your answer change if TC entered into the agreement with the CEO at the suggestion of AC during the

negotiations for the business combination, and the payment is contingent on the CEO remaining in

employment for 3 years following a successful acquisition?

IFRS 3 Business combinations

Determining what is part of the business combination

Instituut van de Bedrijfsrevisoren 15 20 November 2009

PRE‐EXISTING RELATIONSHIPS

AC purchases electronic components from TC under a five‐year supply contract at fixed rates. Currently, the

fixed rates are higher than the rates at which AC could purchase similar electronic components from another

supplier. The supply contract allows AC to terminate the contract before the end of the initial five‐year term

but only by paying a 6 million penalty. With three years remaining under the supply contract, AC pays 50

million to acquire TC, which is the fair value of TC based on what other market participants would be willing to

pay.

Included in the total fair value of TC is 8 million related to the fair value of the supply contract with AC. The 8

million represents a 3 million component that is ‘at market’ because the pricing is comparable to pricing for

current market transactions for the same or similar items (selling effort, customer relationships and so on) and

a 5 million component for pricing that is unfavorable to AC because it exceeds the price of current market

transactions for similar items.TC has no other identifiable assets or liabilities related to the supply contract

before the business combination.

What amount will be included in the consideration transferred to TC for the acquisition ?

IFRS 3 Business combinations

Determining what is part of the business combination

Instituut van de Bedrijfsrevisoren 16 20 November 2009

CONTINGENT PAYMENTS TO EMPLOYEES OR SELLING SHAREHOLDERS

Determine for the following features in contingent payment transactions entered into by the acquirer to

remunerate employees or former owners of the acquiree for future services whether they give an indication

that the cost of the contingent payment is part of the business combination transaction or whether they give

an indication that the cost of the contingent payment should be treated as post‐combination remuneration

cost.

Part of the business

combination transaction

Post combination

remuneration

Contingent payment is automatically forfeited if

employment terminates

Period of required employment is longer than period

for contingent payment

Other remuneration is at reasonable level as compared

with other key personnel of the combined entity

Selling shareholders who do not become employees

receive lower contingent payments per share than the

other selling shareholders

Selling shareholders who continue as key employees

owned only a small number of shares in the acquiree

and all selling shareholders receive the same amount of

contingent consideration on a per‐share basis

Selling shareholders who owned substantially all of the

shares in the acquiree continue as key employees

Initial consideration transferred at the acquisition date

is based on the low end of a range established in the

valuation of the acquiree and the contingent formula

relates to that valuation approach

Contingent payment formula is consistent with prior

profit‐sharing arrangements

Contingent payment is a specified percentage of

earnings

Contingent payment is determined on the basis of a

multiple of earnings

In connection with the acquisition and the contingent

payment arrangement, the acquirer entered into a

property lease arrangement with a significant selling

shareholder. The lease payments are significantly

below market.

IFRS 3 Business combinations

Determining what is part of the business combination

Instituut van de Bedrijfsrevisoren 17 20 November 2009

SHARE BASED PAYMENTS

1. AC acquires TC. AC issues replacement awards of CU110 (market‐based measure) at the acquisition

date for TC awards of CU100 (market‐based measure) at the acquisition date. No post‐combination services

are required for the replacement awards and TC's employees had rendered all of the required service for the

acquiree awards as of the acquisition date.

What amount will be included in the consideration transferred to TC for the acquisition ?

2. AC acquires TC. AC exchanges replacement awards that require one year of post‐combination service

for share‐based payment awards of TC, for which employees had completed the vesting period before the

business combination. The market‐based measure of both awards is CU100 at the acquisition date. When

originally granted, TC's awards had a vesting period of four years. As of the acquisition date, the TC employees

holding unexercised awards had rendered a total of seven years of service since the grant date.

What amount will be included in the consideration transferred to TC for the acquisition ?

3. AC exchanges replacement awards that require one year of post‐combination service for share‐based

payment awards of TC, for which employees had not yet rendered all of the service as of the acquisition date.

The market‐based measure of both awards is CU100 at the acquisition date. When originally granted, the

awards of TC had a vesting period of four years. As of the acquisition date, the TC employees had rendered

two years' service, and they would have been required to render two additional years of service after the

acquisition date for their awards to vest. Accordingly, only a portion of the TC awards is attributable to pre‐

combination service.

What amount will be included in the consideration transferred to TC for the acquisition ?

4. Assume the same facts as in Example 3 above, except that AC exchanges replacement awards that

require no post‐combination service for share‐based payment awards of TC for which employees had not yet

rendered all of the service as of the acquisition date. The terms of the replaced TC awards did not eliminate

any remaining vesting period upon a change in control. (If the TC awards had included a provision that

eliminated any remaining vesting period upon a change in control, the guidance in Example 1 would apply.)

The market‐based measure of both awards is CU100. Because employees have already rendered two years of

service and the replacement awards do not require any post‐combination service, the total vesting period is

two years.

What amount will be included in the consideration transferred to TC for the acquisition ?

IFRS 3 Business combinations

Intangible assets

Instituut van de Bedrijfsrevisoren 18 20 November 2009

INTANGIBLE ASSETS

1. The following are examples of identifiable intangible assets acquired in a business combination. Some

of the examples may have characteristics of assets other than intangible assets.

Intangible assets are identifiable if they have a contractual basis or if they are separable. Intangible assets

identified as having a contractual basis might also be separable but separability is not a necessary condition for

an asset to meet the contractual‐legal criterion.

Explain for the following intangible assets why they meet the definition of an identifiable asset.

Marketing‐related intangible assets

Trademarks, trade names, service

marks, collective marks and

certification marks

Internet domain names

Customer‐related intangible assets

Customer lists

Order or production backlog

Customer contracts and the related

customer relationships

Non‐contractual customer

relationships

Artictic‐related intangible assets

Plays, operas and ballets

Books, magazines, newspapers and

other literary works

Musical works such as compositions,

song lyrics and advertising jingles

IFRS 3 Business combinations

Intangible assets

Instituut van de Bedrijfsrevisoren 19 20 November 2009

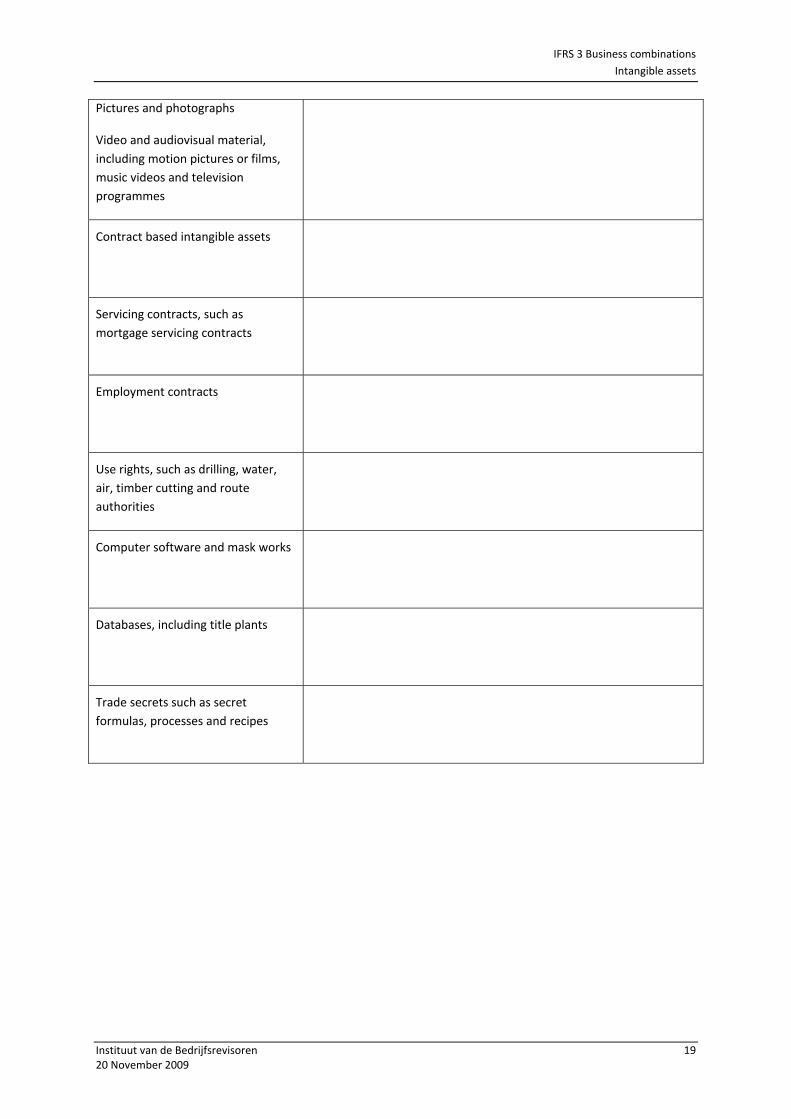

Pictures and photographs

Video and audiovisual material,

including motion pictures or films,

music videos and television

programmes

Contract based intangible assets

Servicing contracts, such as

mortgage servicing contracts

Employment contracts

Use rights, such as drilling, water,

air, timber cutting and route

authorities

Computer software and mask works

Databases, including title plants

Trade secrets such as secret

formulas, processes and recipes

IFRS 3 Business combinations

Intangible assets

Instituut van de Bedrijfsrevisoren 20 20 November 2009

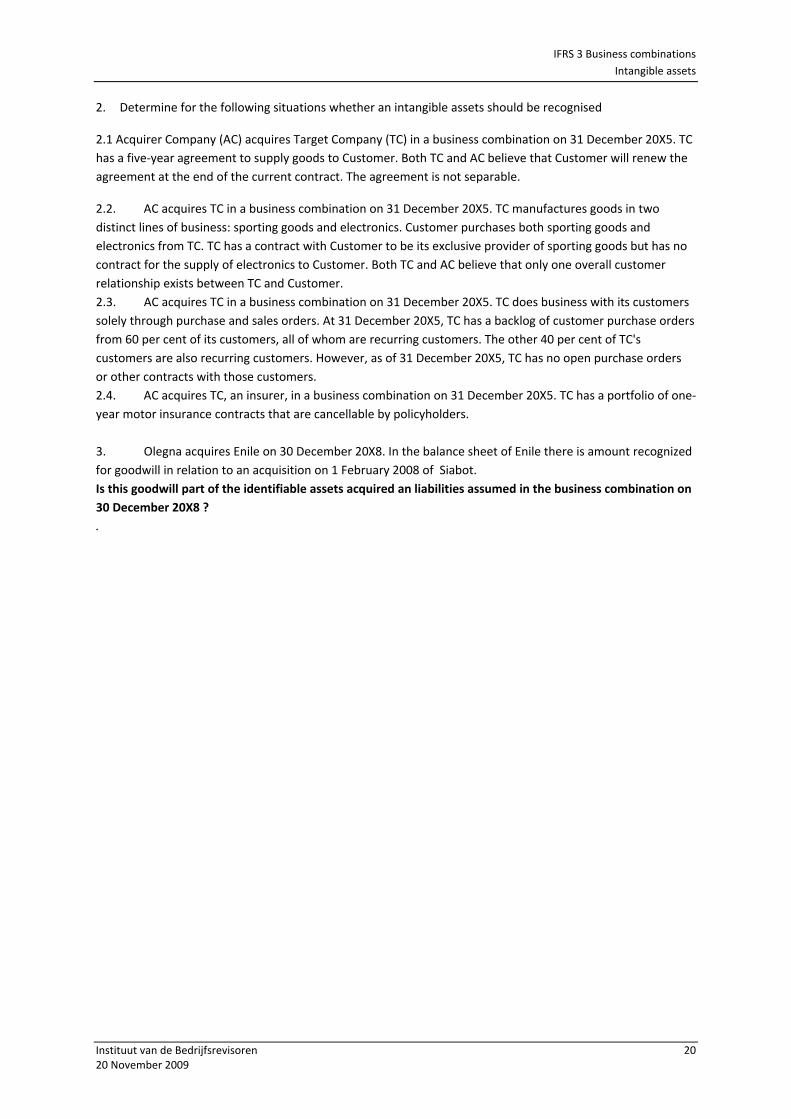

2. Determine for the following situations whether an intangible assets should be recognised

2.1 Acquirer Company (AC) acquires Target Company (TC) in a business combination on 31 December 20X5. TC

has a five‐year agreement to supply goods to Customer. Both TC and AC believe that Customer will renew the

agreement at the end of the current contract. The agreement is not separable.

2.2. AC acquires TC in a business combination on 31 December 20X5. TC manufactures goods in two

distinct lines of business: sporting goods and electronics. Customer purchases both sporting goods and

electronics from TC. TC has a contract with Customer to be its exclusive provider of sporting goods but has no

contract for the supply of electronics to Customer. Both TC and AC believe that only one overall customer

relationship exists between TC and Customer.

2.3. AC acquires TC in a business combination on 31 December 20X5. TC does business with its customers

solely through purchase and sales orders. At 31 December 20X5, TC has a backlog of customer purchase orders

from 60 per cent of its customers, all of whom are recurring customers. The other 40 per cent of TC's

customers are also recurring customers. However, as of 31 December 20X5, TC has no open purchase orders

or other contracts with those customers.

2.4. AC acquires TC, an insurer, in a business combination on 31 December 20X5. TC has a portfolio of one‐

year motor insurance contracts that are cancellable by policyholders.

3. Olegna acquires Enile on 30 December 20X8. In the balance sheet of Enile there is amount recognized

for goodwill in relation to an acquisition on 1 February 2008 of Siabot.

Is this goodwill part of the identifiable assets acquired an liabilities assumed in the business combination on

30 December 20X8 ?

.

IFRS 3 Business combinations

Reverse acquisitions

Instituut van de Bedrijfsrevisoren 21 20 November 2009

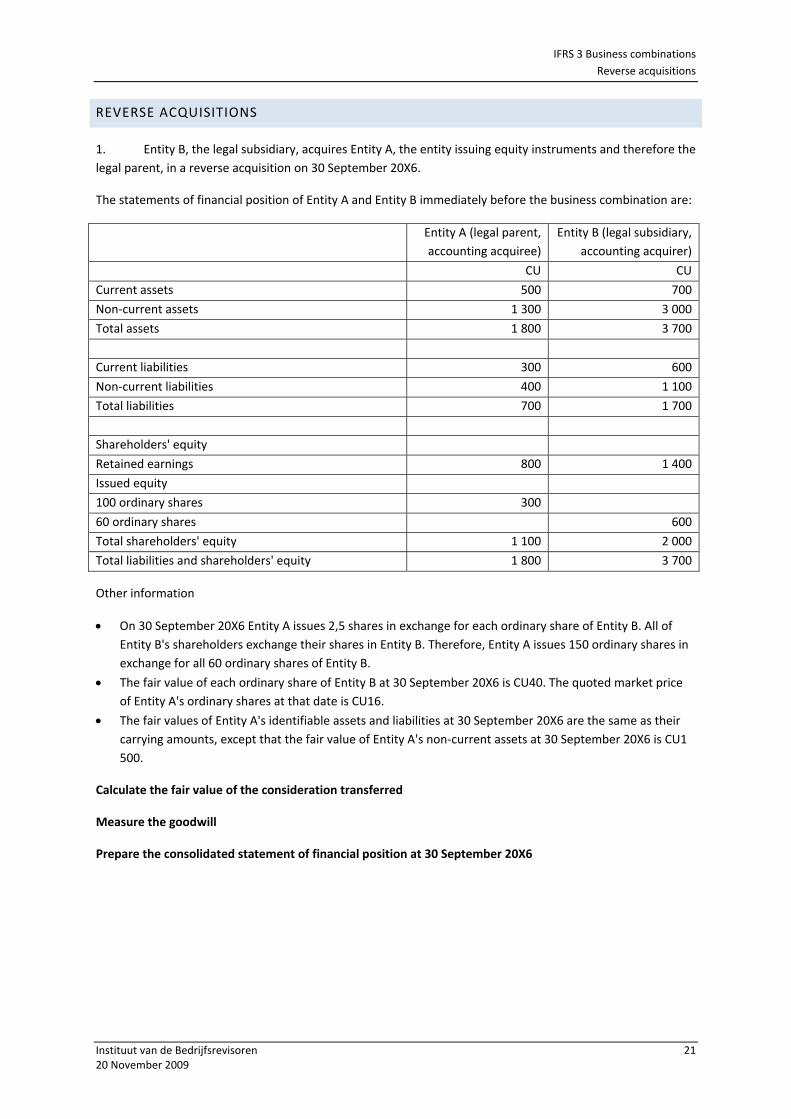

REVERSE ACQUISITIONS

1. Entity B, the legal subsidiary, acquires Entity A, the entity issuing equity instruments and therefore the

legal parent, in a reverse acquisition on 30 September 20X6.

The statements of financial position of Entity A and Entity B immediately before the business combination are:

Entity A (legal parent,

accounting acquiree)

Entity B (legal subsidiary,

accounting acquirer)

CU CU

Current assets 500 700

Non‐current assets 1 300 3 000

Total assets 1 800 3 700

Current liabilities 300 600

Non‐current liabilities 400 1 100

Total liabilities 700 1 700

Shareholders' equity

Retained earnings 800 1 400

Issued equity

100 ordinary shares 300

60 ordinary shares 600

Total shareholders' equity 1 100 2 000

Total liabilities and shareholders' equity 1 800 3 700

Other information

On 30 September 20X6 Entity A issues 2,5 shares in exchange for each ordinary share of Entity B. All of

Entity B's shareholders exchange their shares in Entity B. Therefore, Entity A issues 150 ordinary shares in

exchange for all 60 ordinary shares of Entity B.

The fair value of each ordinary share of Entity B at 30 September 20X6 is CU40. The quoted market price

of Entity A's ordinary shares at that date is CU16.

The fair values of Entity A's identifiable assets and liabilities at 30 September 20X6 are the same as their

carrying amounts, except that the fair value of Entity A's non‐current assets at 30 September 20X6 is CU1

500.

Calculate the fair value of the consideration transferred

Measure the goodwill

Prepare the consolidated statement of financial position at 30 September 20X6

IFRS 3 Business combinations

Reverse acquisitions

Instituut van de Bedrijfsrevisoren 22 20 November 2009

Assume that Entity B's earnings for the annual period ended 31 December 20X5 were CU600 and that the

consolidated earnings for the annual period ended 31 December 20X6 were CU800. Assume also that there

was no change in the number of ordinary shares issued by Entity B during the annual period ended 31

December 20X5 and during the period from 1 January 20X6 to the date of the reverse acquisition on 30

September 20X6.

Calculate the earnings per share

2. Assume the same facts as above, except that only 56 of Entity B's 60 ordinary shares are exchanged.

Calculate the fair value of the consideration transferred

Measure the non controlling interest

Prepare the consolidated statement of financial position at 30 September 20X6

IFRS 3 Business combinations

Income taxes

Instituut van de Bedrijfsrevisoren 23 20 November 2009

INCOME TAXES

Mocas purchased 75% of the capital of Haraf for CU 250 000 on 1 July 20X0. at this date the equity of Haraf

was:

CU

Share capital 100 000

General reserve 60 000

Retained earnings 40 000

At this date Haraf had not recorded any goodwill, and all identifiable assets and liabilities were recorded at fair

value except for the following cases:

Carrying amount Fair value

Cu CU

Inventory 70 000 100 000

Plant (cost CU 170 000) 150 000 190 000

Land 50 000 100 000

The tax rate is 30%.

Calculate the goodwill and determine the journal entries related to the business combination. Assume that

the minority interest is measured based on the interest in the fair value of the net assets.

IFRS 3 Business combinations

Impairment of goodwill

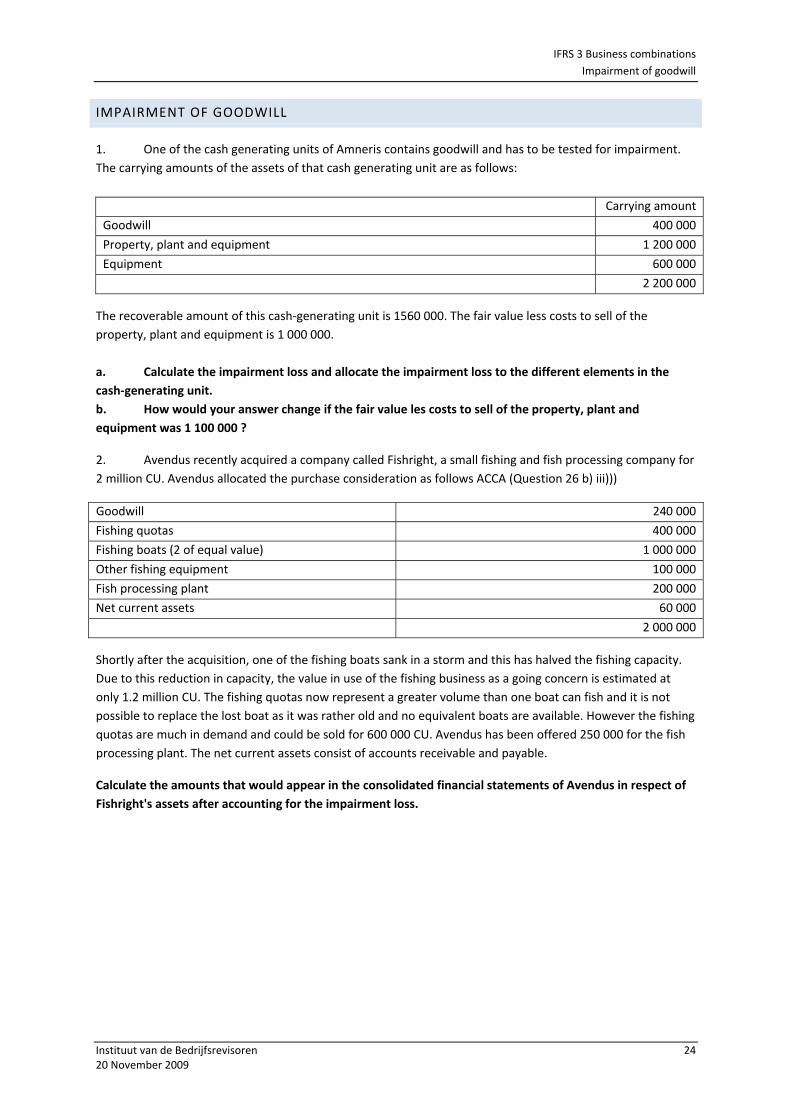

Instituut van de Bedrijfsrevisoren 24 20 November 2009

IMPAIRMENT OF GOODWILL

1. One of the cash generating units of Amneris contains goodwill and has to be tested for impairment.

The carrying amounts of the assets of that cash generating unit are as follows:

Carrying amount

Goodwill 400 000

Property, plant and equipment 1 200 000

Equipment 600 000

2 200 000

The recoverable amount of this cash‐generating unit is 1560 000. The fair value less costs to sell of the

property, plant and equipment is 1 000 000.

a. Calculate the impairment loss and allocate the impairment loss to the different elements in the

cash‐generating unit.

b. How would your answer change if the fair value les costs to sell of the property, plant and

equipment was 1 100 000 ?

2. Avendus recently acquired a company called Fishright, a small fishing and fish processing company for

2 million CU. Avendus allocated the purchase consideration as follows ACCA (Question 26 b) iii)))

Goodwill 240 000

Fishing quotas 400 000

Fishing boats (2 of equal value) 1 000 000

Other fishing equipment 100 000

Fish processing plant 200 000

Net current assets 60 000

2 000 000

Shortly after the acquisition, one of the fishing boats sank in a storm and this has halved the fishing capacity.

Due to this reduction in capacity, the value in use of the fishing business as a going concern is estimated at

only 1.2 million CU. The fishing quotas now represent a greater volume than one boat can fish and it is not

possible to replace the lost boat as it was rather old and no equivalent boats are available. However the fishing

quotas are much in demand and could be sold for 600 000 CU. Avendus has been offered 250 000 for the fish

processing plant. The net current assets consist of accounts receivable and payable.

Calculate the amounts that would appear in the consolidated financial statements of Avendus in respect of

Fishright's assets after accounting for the impairment loss.

IFRS 3 Business combinations

Impairment of goodwill

Instituut van de Bedrijfsrevisoren 25 20 November 2009

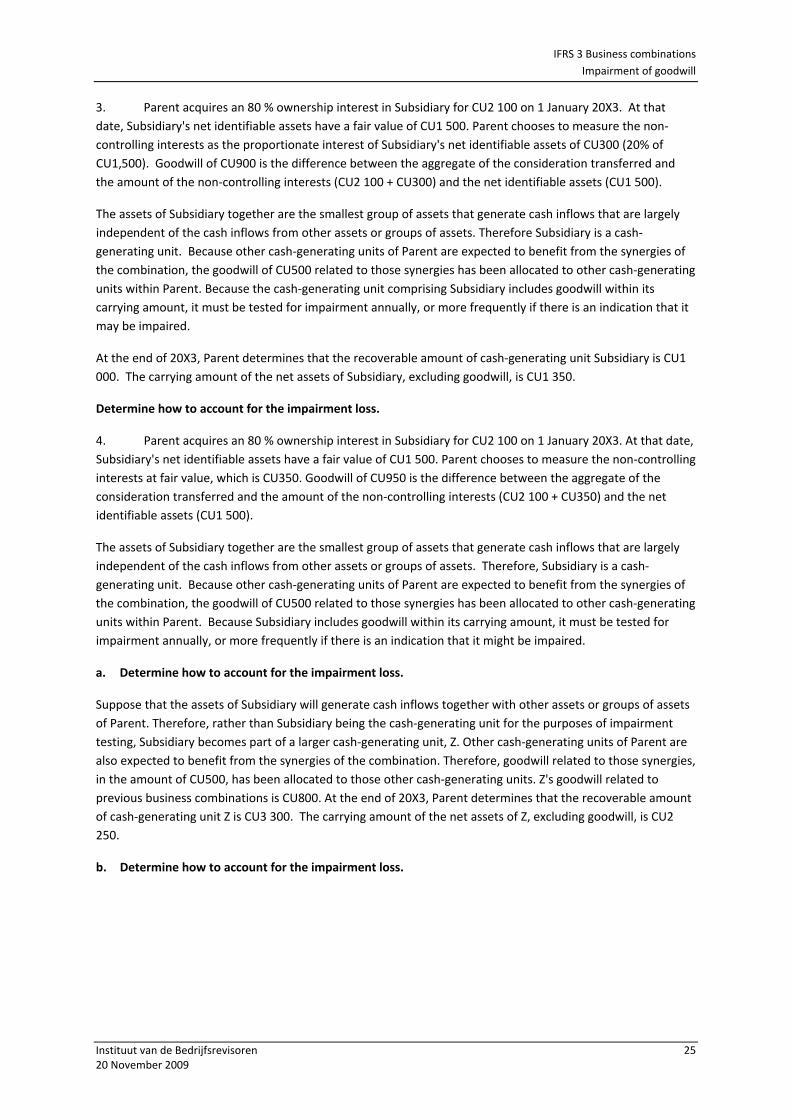

3. Parent acquires an 80 % ownership interest in Subsidiary for CU2 100 on 1 January 20X3. At that

date, Subsidiary's net identifiable assets have a fair value of CU1 500. Parent chooses to measure the non‐

controlling interests as the proportionate interest of Subsidiary's net identifiable assets of CU300 (20% of

CU1,500). Goodwill of CU900 is the difference between the aggregate of the consideration transferred and

the amount of the non‐controlling interests (CU2 100 + CU300) and the net identifiable assets (CU1 500).

The assets of Subsidiary together are the smallest group of assets that generate cash inflows that are largely

independent of the cash inflows from other assets or groups of assets. Therefore Subsidiary is a cash‐

generating unit. Because other cash‐generating units of Parent are expected to benefit from the synergies of

the combination, the goodwill of CU500 related to those synergies has been allocated to other cash‐generating

units within Parent. Because the cash‐generating unit comprising Subsidiary includes goodwill within its

carrying amount, it must be tested for impairment annually, or more frequently if there is an indication that it

may be impaired.

At the end of 20X3, Parent determines that the recoverable amount of cash‐generating unit Subsidiary is CU1

000. The carrying amount of the net assets of Subsidiary, excluding goodwill, is CU1 350.

Determine how to account for the impairment loss.

4. Parent acquires an 80 % ownership interest in Subsidiary for CU2 100 on 1 January 20X3. At that date,

Subsidiary's net identifiable assets have a fair value of CU1 500. Parent chooses to measure the non‐controlling

interests at fair value, which is CU350. Goodwill of CU950 is the difference between the aggregate of the

consideration transferred and the amount of the non‐controlling interests (CU2 100 + CU350) and the net

identifiable assets (CU1 500).

The assets of Subsidiary together are the smallest group of assets that generate cash inflows that are largely

independent of the cash inflows from other assets or groups of assets. Therefore, Subsidiary is a cash‐

generating unit. Because other cash‐generating units of Parent are expected to benefit from the synergies of

the combination, the goodwill of CU500 related to those synergies has been allocated to other cash‐generating

units within Parent. Because Subsidiary includes goodwill within its carrying amount, it must be tested for

impairment annually, or more frequently if there is an indication that it might be impaired.

a. Determine how to account for the impairment loss.

Suppose that the assets of Subsidiary will generate cash inflows together with other assets or groups of assets

of Parent. Therefore, rather than Subsidiary being the cash‐generating unit for the purposes of impairment

testing, Subsidiary becomes part of a larger cash‐generating unit, Z. Other cash‐generating units of Parent are

also expected to benefit from the synergies of the combination. Therefore, goodwill related to those synergies,

in the amount of CU500, has been allocated to those other cash‐generating units. Z's goodwill related to

previous business combinations is CU800. At the end of 20X3, Parent determines that the recoverable amount

of cash‐generating unit Z is CU3 300. The carrying amount of the net assets of Z, excluding goodwill, is CU2

250.

b. Determine how to account for the impairment loss.