ifrs 9 and basel iii - acumen information...

TRANSCRIPT

IFRS 9 and Basel III

Marc Buklis MBA CFA

Managing Director, Consulting and Deals

PricewaterhouseCoopers LLP

June 10, 2015

IFRS 9 - Basel III

1

June 2015

Agenda and Introduction

Regulatory Initiatives - Timeline

IFRS 9 Key Highlights

OSFI and BCBS Guidance

IFRS 9 and Capital - Integration

Questions and Follow up

Marc E. Buklis, Managing Director, Consulting and Deals, PricewaterhouseCoopers LLP

Mr. Buklis is a Managing Director with PwC's Canadian consulting practice, with a specialization in risk, compliance and technology. Marc has nearly 20 years' experience working with financial institutions on regulatory initiatives for capital, liquidity and compliance. Marc has worked with large banking organizations in Canada, the United State and Australia to understand regulatory requirements and to implement solutions fit to each client's needs. Mr. Buklis speaks regularly on regulatory risk, compliance and technology implementation matters. Mr. Buklis has an MBA from the Joseph L. Rotman School at the University of Toronto (1998) and a BA in Economics from the University of Toronto (1993). He is a CFA Charterholder.

This presentation has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this presentation without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this presentation, and, to the extent permitted by law, PwC does not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this presentation or for any decision based on it.

© 2015 PwC. All rights reserved. PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details.

IFRS 9 - Basel III

2

June 2015

Regulatory Initiatives - Timeline

December 2017

BCBS 239 – DSIB Deadline

January 2013

Basel III Capital Reporting

July 2014

Final Standard – IFRS 9

November 2017

Effective Date – IFRS 9 DSIB

January 2015

LCR Reporting

NCCF Reporting

January 2016

BCBS 239 – GSIB Deadline

3

June 2015 IFRS 9 - Basel III

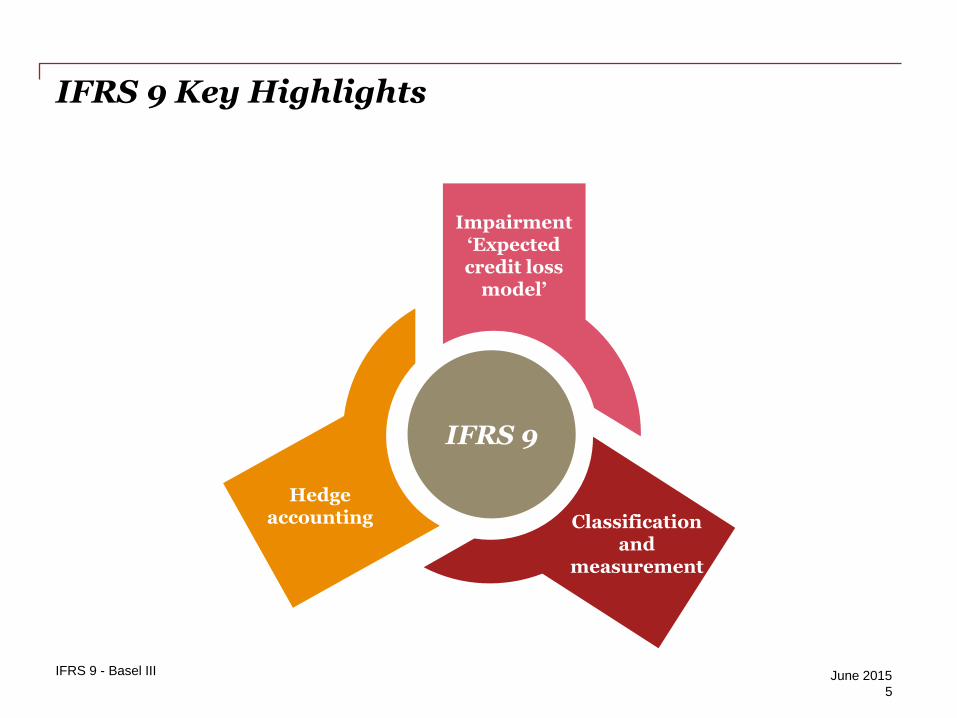

IFRS 9 Key Highlights

IFRS 9 - Basel III

4

June 2015

IFRS 9 Key Highlights

IFRS 9

Impairment ‘Expected credit loss

model’

Hedge accounting Classification

and measurement

5

June 2015 IFRS 9 - Basel III

IFRS 9 Classification and Measurement: Equity Instruments

Cost exemption for unquoted equity removed.

6

IFRS 9 - Basel III

Is the equity instrument held for trading?

Has the entity elected fair value through OCI?

Fair value through OCI with no recycling and no

impairment

Fair value through profit or loss

Yes

No

Yes

No

June 2015

Amortised cost FV-OCI

IFRS 9 Classification and Measurement: Debt Instruments

Fair value through

P&L

Do contractual cash flows represent solely payments of principal and interest?

Does the company apply the fair value option to eliminate an accounting mismatch?

Yes

Yes

No

No

No

No

Yes

No

Yes

Yes

IFRS 9 - Basel III

7

Is objective of the entity’s business model to hold the financial assets to collect contractual cash flows?

Is the financial asset held to achieve an objective by both collecting contractual cash flows and selling financial assets?

June 2015

Documenting the business model (incl

sales)

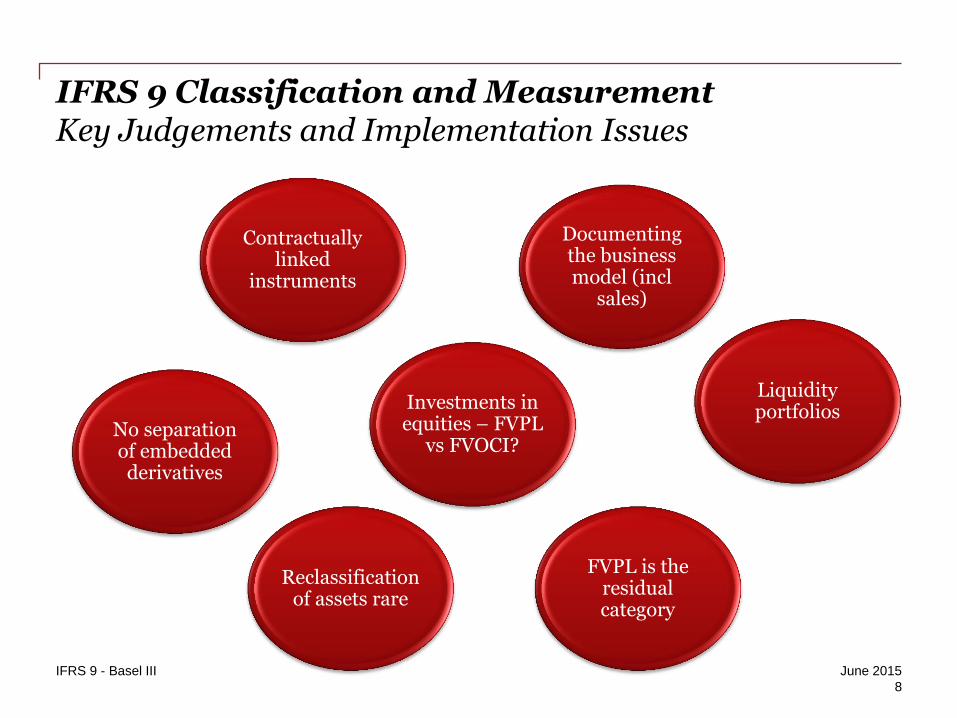

IFRS 9 Classification and Measurement Key Judgements and Implementation Issues

No separation of embedded derivatives

FVPL is the residual category

Contractually linked

instruments

Liquidity portfolios

Reclassification of assets rare

Investments in equities – FVPL

vs FVOCI?

June 2015 IFRS 9 - Basel III

8

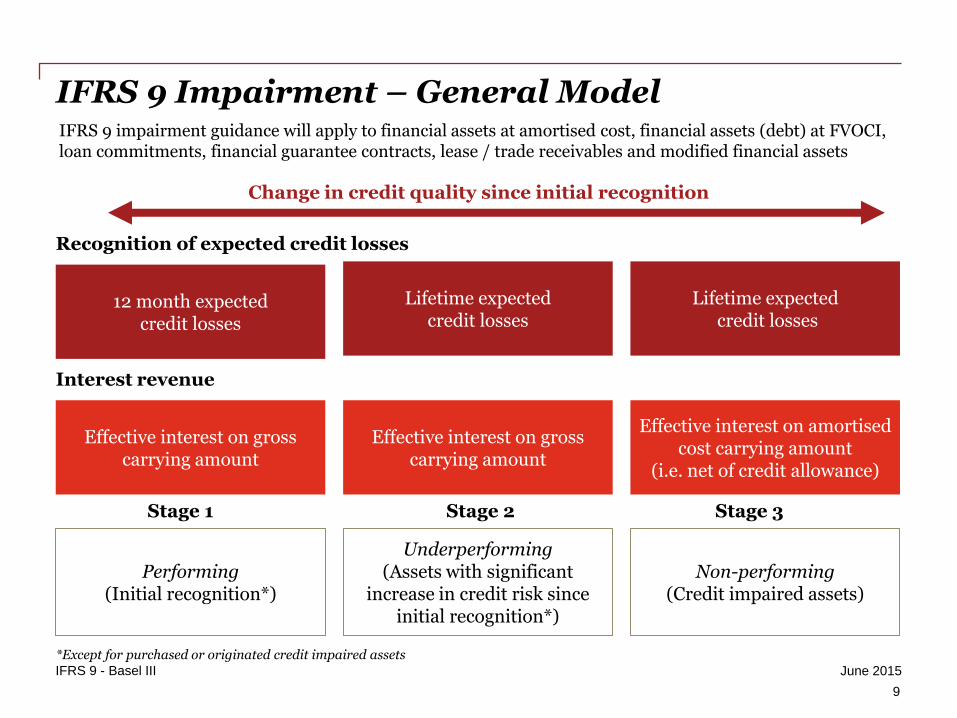

IFRS 9 Impairment – General Model

9

Effective interest on gross carrying amount

12 month expected credit losses

Recognition of expected credit losses

Interest revenue

Change in credit quality since initial recognition

Stage 1 Stage 2 Stage 3

Performing (Initial recognition*)

Underperforming (Assets with significant

increase in credit risk since initial recognition*)

Non-performing (Credit impaired assets)

Effective interest on gross carrying amount

Lifetime expected credit losses

Effective interest on amortised cost carrying amount

(i.e. net of credit allowance)

Lifetime expected credit losses

*Except for purchased or originated credit impaired assets IFRS 9 - Basel III June 2015

IFRS 9 impairment guidance will apply to financial assets at amortised cost, financial assets (debt) at FVOCI, loan commitments, financial guarantee contracts, lease / trade receivables and modified financial assets

IFRS 9 Impairment General model – significant increase in credit risk Key Judgements and Implementation Issues

10

Top down versus bottom

up

Level of segmentation /granularity

Mapping internal and

external credit grades

Basel PDs vs IFRS 9 PDs

IFRS 9 - Basel III June 2015

IFRS 9 Impairment General model – significant increase in credit risk Key Judgements and Implementation Issues

11

Regulatory PD IFRS 9 PD

Through the cycle

(‘TTC’)

Point in time (‘PiT’)

Hard to reconcile!

IFRS 9 - Basel III June 2015

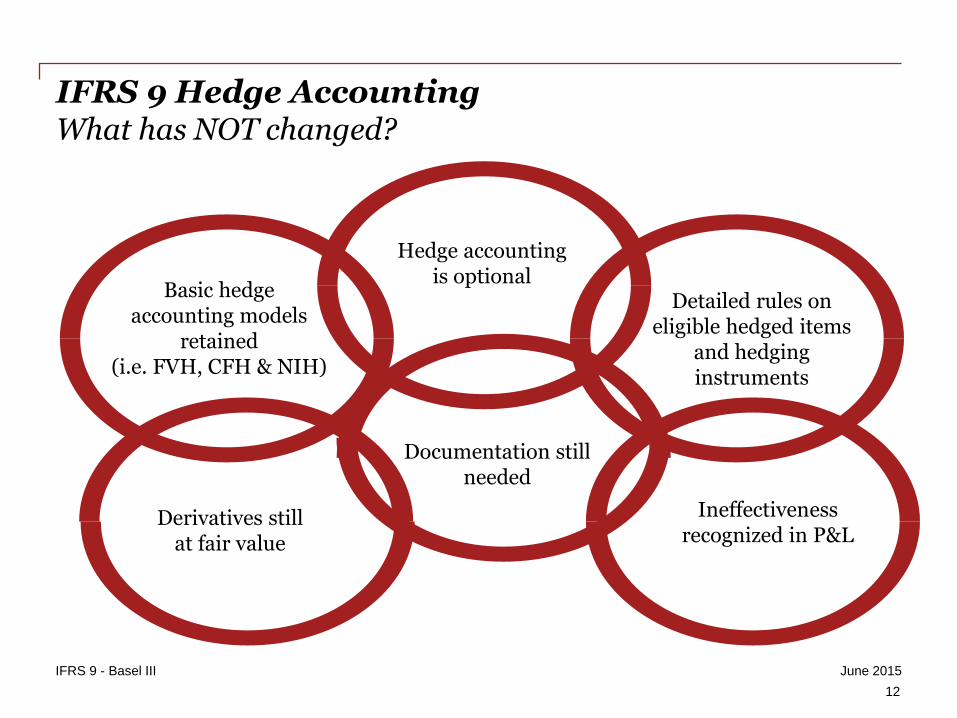

IFRS 9 Hedge Accounting What has NOT changed?

Basic hedge accounting models

retained (i.e. FVH, CFH & NIH)

Hedge accounting is optional

Detailed rules on eligible hedged items

and hedging instruments

Documentation still needed

Derivatives still at fair value

Ineffectiveness recognized in P&L

IFRS 9 - Basel III

12

June 2015

13

80-125% effectiveness threshold is removed

IFRS 9 qualifying criteria

1. Formal designation and documentation

2. Only eligible hedging instruments and hedged

items

3. Meets the hedge effectiveness requirements

3.1 Economic relationship between hedged item and hedging instrument gives rise to offset

3.2 Effect of credit risk does not dominate the value changes

3.3 Hedge ratio results from the quantity of hedged item hedged and hedging item used to hedge

IFRS 9 - Basel III

IFRS 9 Hedge Accounting Qualifying for hedge accounting

June 2015

OSFI and BCBS Guidance

IFRS 9 - Basel III

14

June 2015

OSFI and BCBS Guidance

• OSFI and BCBS continue to develop their guidance.

• OSFI (January 2015) has advised financial institutions to NOT early adopt IFRS 9 except for DSIB’s, due to the expected significant impact.

• OSFI continues to monitor IFRS 9 acceptance and guidance with other jurisdictions and BCBS.

• BCBS Guidance on Accounting for Expected Credit Losses (2015) is currently in draft – and was issued for comment by April 30.1

• The document provides separate guidance on expected credit losses, expected credit losses and capital and IFRS 9 adoption.

• BCBS guidance outlines 11 principles, of which 3 relate to supervisory evaluation of credit risk practices, expected credit losses and capital adequacy. Effectively, capital adequacy rests on credit and accounting processes:

• Principle 9: Banking supervisors should periodically evaluate the effectiveness of a bank’s credit risk practices.

• Principle 10: Banking supervisors should be satisfied that the methods employed by a bank to determine allowances produce a robust measurement of expected credit losses under the applicable accounting framework.

• Principle 11: Banking supervisors should consider a bank’s credit risk practices when assessing a bank’s capital adequacy.

1 BCBS Consultative Document, Guidance on Accounting for Expected Credit Losses, 2015, page 1.

IFRS 9 - Basel III

15

June 2015

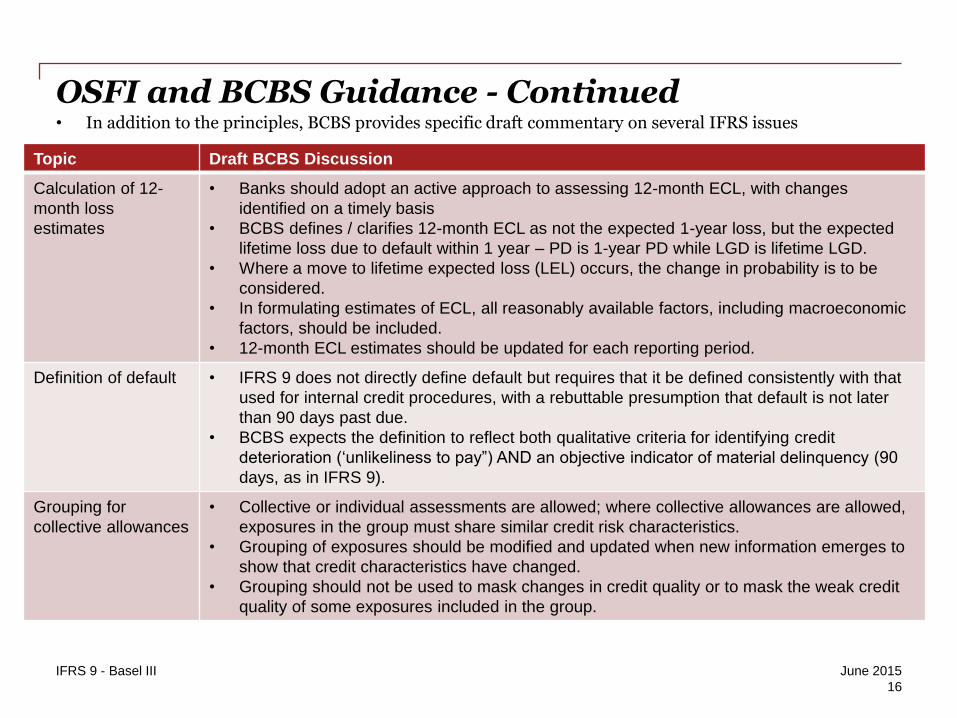

OSFI and BCBS Guidance - Continued

Topic Draft BCBS Discussion

Calculation of 12-

month loss

estimates

• Banks should adopt an active approach to assessing 12-month ECL, with changes

identified on a timely basis

• BCBS defines / clarifies 12-month ECL as not the expected 1-year loss, but the expected

lifetime loss due to default within 1 year – PD is 1-year PD while LGD is lifetime LGD.

• Where a move to lifetime expected loss (LEL) occurs, the change in probability is to be

considered.

• In formulating estimates of ECL, all reasonably available factors, including macroeconomic

factors, should be included.

• 12-month ECL estimates should be updated for each reporting period.

Definition of default • IFRS 9 does not directly define default but requires that it be defined consistently with that

used for internal credit procedures, with a rebuttable presumption that default is not later

than 90 days past due.

• BCBS expects the definition to reflect both qualitative criteria for identifying credit

deterioration (‘unlikeliness to pay”) AND an objective indicator of material delinquency (90

days, as in IFRS 9).

Grouping for

collective allowances

• Collective or individual assessments are allowed; where collective allowances are allowed,

exposures in the group must share similar credit risk characteristics.

• Grouping of exposures should be modified and updated when new information emerges to

show that credit characteristics have changed.

• Grouping should not be used to mask changes in credit quality or to mask the weak credit

quality of some exposures included in the group.

IFRS 9 - Basel III

16

June 2015

• In addition to the principles, BCBS provides specific draft commentary on several IFRS issues

OSFI and BCBS Guidance - Continued

Topic Draft BCBS Discussion

Assessment of

increases in credit

risk since inception

• Impairment calculations must estimate changes in credit quality since inception of the loan:

loan pricing includes credit quality at inception but changes since inception will not be.

• Impairment calculations for financial reporting are an important part of credit risk

management – and the two should thus be integrated.

• Calculations will require both historical and forward looking data. Banks will need systems

capable of consistently handling and systematically assessing the large amounts of

information required and to measure LEL, along with strong governance and controls.

• Banks will need to provide clear policy definitions of what constitutes worsening credit.

• Banks will need to have a clear view – backed by analysis – of the linkages from

macroeconomic factors to credit risk.

Modified /

Renegotiated

Transactions

• BCBS believes that modifications or renegotiations can mask increases in credit risk,

resulting in underestimation of ECL or delayed move to LEL measurement.

• Where renegotiation has been undertaken, banks must be able to demonstrate whether the

renegotiated asset has ‘improved or restored’ the ability to collect interest and principal –

and reflect credit losses accordingly.

Use of Practical

Expedients

• BCBS believes practical expedients in IFRS 9 are inappropriate for large banks

• For example:, and 30-days past due presumption.

• The allowance to limit the information search for measuring ECL, ‘without undo cost

and effort’: Banks should search thoroughly.

• The ‘low credit risk’ exposures exemption from assessment of significant increase in

credit risk since inception: Banks to use this only in exceptional circumstances.

• The 30-days past due presumption: credit risk should be assessed BEFORE

delinquency.

IFRS 9 - Basel III

17

June 2015

• In addition to the principles, BCBS provides specific draft commentary on several IFRS issues

IFRS 9 and Capital - Integration

IFRS 9 - Basel III

18

June 2015

IFRS 9 and Basel III Capital – Integration Points

Impairment ‘Expected credit

loss model’

Hedge accounting

Classification and

measurement

19

June 2015 IFRS 9 - Basel III

Definition and Components of

Capital

Credit Risk - Standardised

Market Risk

Credit Risk - IRB

Credit Risk - Securitisation

Counterparty Credit and

Netting

Operational Risk

Basel III – as with Basel II before it – on principle sits on the foundation of each Bank’s prudential credit risk policies and procedures.

IFRS 9 and existing Basel III implementations will thus interact, with IFRS forming part of the foundation.

Specifically, IFRS 9 and Basel III will also interact around provisions, calculation of Expected Credit Loss and Parameters, Valuation and Netting.

In addition to Capital, other regulatory reporting – such as LCR – also draws on financial reporting classification and impairment.

Transition to IFRS 9 will involve assessment of these interactions and the changes necessary.

OCI vs P&L Adjustment and Capital

Provisions

ECL and Parameters

Valuations

Netting and Definitions

IFRS 9 Basel III

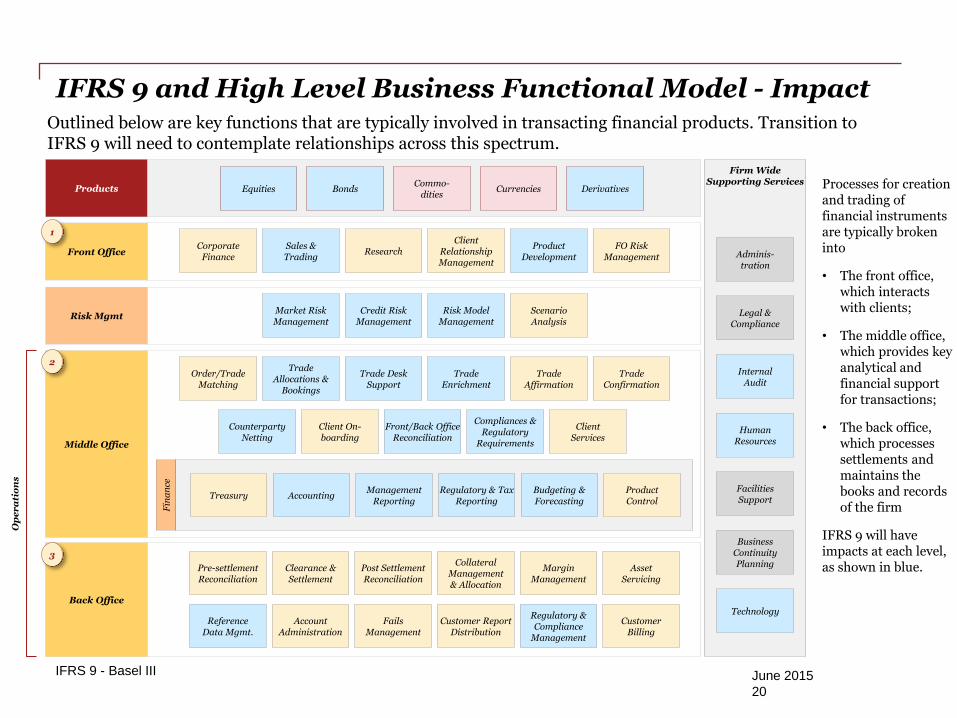

IFRS 9 and High Level Business Functional Model - Impact

Products

Front Office

Middle Office

Back Office

Firm Wide Supporting Services

Equities Bonds Commo-

dities Currencies Derivatives

Corporate Finance

Sales & Trading

Research Client

Relationship Management

Product Development

Order/Trade Matching

Trade Allocations &

Bookings

Trade Desk Support

Trade Enrichment

Trade Affirmation

Trade Confirmation

Counterparty Netting

Client On-boarding

Front/Back Office Reconciliation

Compliances & Regulatory

Requirements

Client Services

Fin

an

ce

Treasury Accounting Management

Reporting Regulatory & Tax

Reporting Budgeting & Forecasting

Product Control

Pre-settlement Reconciliation

Clearance & Settlement

Post Settlement Reconciliation

Collateral Management & Allocation

Margin Management

Asset Servicing

Reference Data Mgmt.

Account Administration

Fails Management

Customer Report Distribution

Regulatory & Compliance

Management

Customer Billing

Adminis-tration

Legal & Compliance

Internal Audit

Human Resources

Facilities Support

Business Continuity Planning

Technology

Risk Mgmt

FO Risk Management

Credit Risk Management

Market Risk Management

Risk Model Management

Scenario Analysis

Op

er

ati

on

s

1

2

3

Processes for creation and trading of financial instruments are typically broken into

• The front office, which interacts with clients;

• The middle office, which provides key analytical and financial support for transactions;

• The back office, which processes settlements and maintains the books and records of the firm

IFRS 9 will have impacts at each level, as shown in blue.

20

June 2015 IFRS 9 - Basel III

Outlined below are key functions that are typically involved in transacting financial products. Transition to IFRS 9 will need to contemplate relationships across this spectrum.

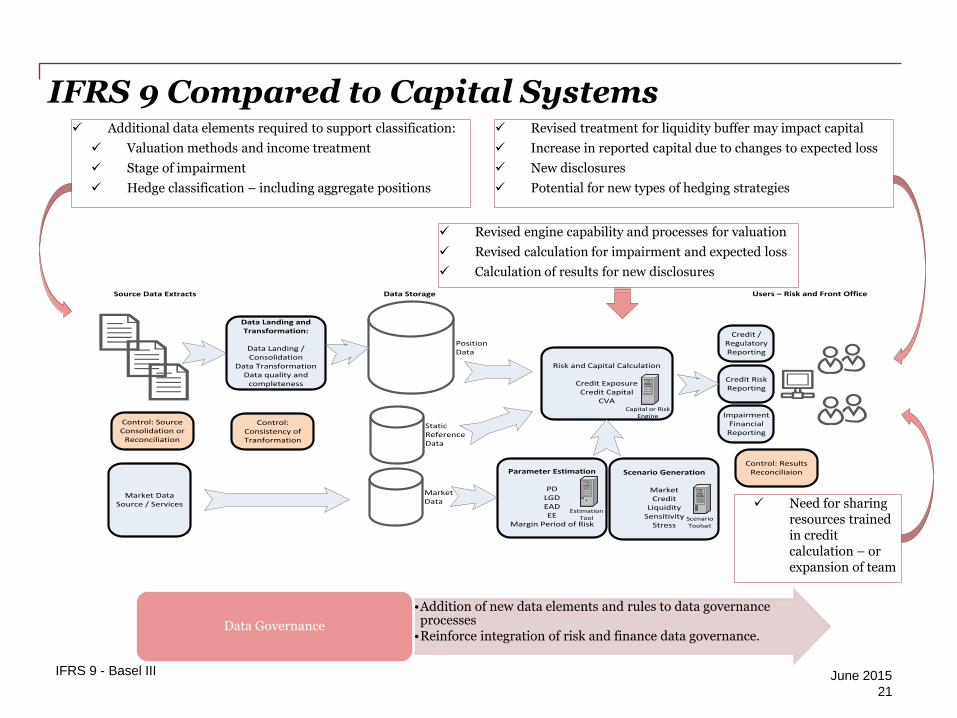

IFRS 9 Compared to Capital Systems Additional data elements required to support classification:

Valuation methods and income treatment

Stage of impairment

Hedge classification – including aggregate positions

Revised treatment for liquidity buffer may impact capital

Increase in reported capital due to changes to expected loss

New disclosures

Potential for new types of hedging strategies

Revised engine capability and processes for valuation

Revised calculation for impairment and expected loss

Calculation of results for new disclosures

•Addition of new data elements and rules to data governance processes

•Reinforce integration of risk and finance data governance. Data Governance

21

June 2015 IFRS 9 - Basel III

Scenario Generation

MarketCredit

LiquiditySensitivity

Stress

Risk and Capital Calculation

Credit ExposureCredit Capital

CVA

Position Data

MarketData

Static Reference Data

ScenarioToolset

Capital or Risk Engine

Data Landing and Transformation:

Data Landing / Consolidation

Data TransformationData quality and

completeness

Parameter Estimation

PDLGDEADEE

Margin Period of Risk

EstimationTool

Source Data Extracts

Market Data Source / Services

Data Storage Users – Risk and Front Office

Credit Risk Reporting

Credit / Regulatory Reporting

Impairment Financial Reporting

Control: Source Consolidation or

Reconciliation

Control: Consistency of Tranformation

Control: Results Reconciliaion

Need for sharing resources trained in credit calculation – or expansion of team

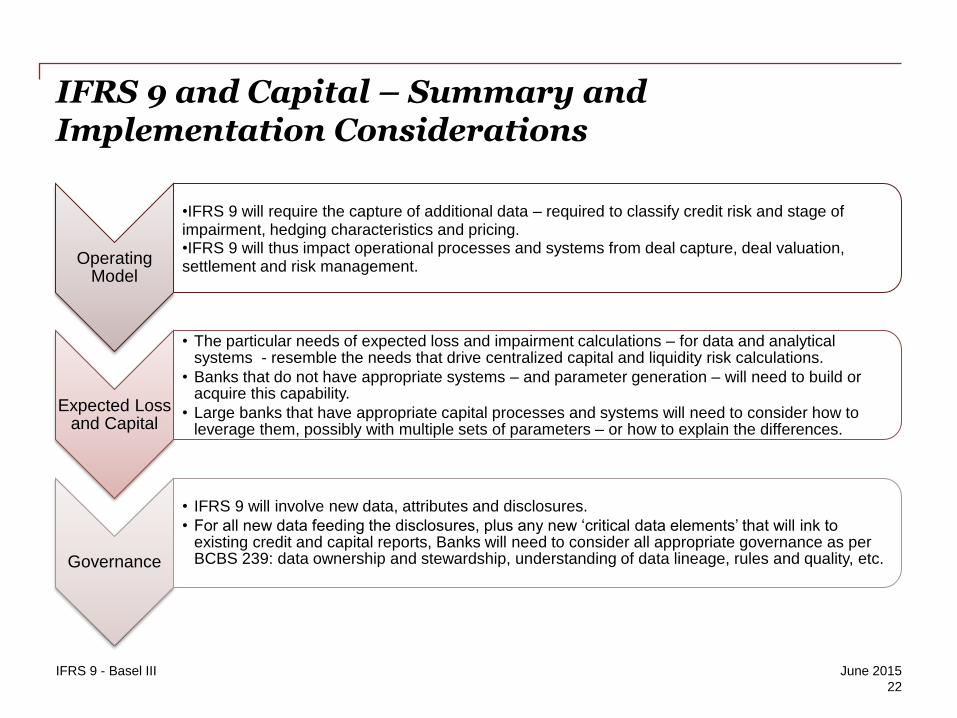

IFRS 9 and Capital – Summary and Implementation Considerations

Operating Model

•IFRS 9 will require the capture of additional data – required to classify credit risk and stage of impairment, hedging characteristics and pricing. •IFRS 9 will thus impact operational processes and systems from deal capture, deal valuation, settlement and risk management.

Expected Loss and Capital

• The particular needs of expected loss and impairment calculations – for data and analytical systems - resemble the needs that drive centralized capital and liquidity risk calculations.

• Banks that do not have appropriate systems – and parameter generation – will need to build or acquire this capability.

• Large banks that have appropriate capital processes and systems will need to consider how to leverage them, possibly with multiple sets of parameters – or how to explain the differences.

Governance

• IFRS 9 will involve new data, attributes and disclosures.

• For all new data feeding the disclosures, plus any new ‘critical data elements’ that will ink to existing credit and capital reports, Banks will need to consider all appropriate governance as per BCBS 239: data ownership and stewardship, understanding of data lineage, rules and quality, etc.

IFRS 9 - Basel III

22

June 2015

Questions and Follow Up Thank you for your time today. For further information, please contact: Marc Buklis, Managing Director, Consulting and Deals PricewaterhouseCoopers LLP [email protected] +1-416-728-0639 or +1-416-687-8611

This presentation has been prepared for general guidance on matters of interest only, and

does not constitute professional advice. You should not act upon the information contained in

this presentation without obtaining specific professional advice. No representation or warranty

(express or implied) is given as to the accuracy or completeness of the information contained

in this presentation, and, to the extent permitted by law, PwC does not accept or assume any

liability, responsibility or duty of care for any consequences of you or anyone else acting, or

refraining to act, in reliance on the information contained in this presentation or for any decision

based on it.

© 2015 PwC. All rights reserved. PwC refers to the PwC network and/or one or more of its

member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for

further details..