ifo institute for economic research ict, skills and german industry productivity – the...

TRANSCRIPT

Ifo Institute for Economic Research

ICT, SKILLS AND GERMAN INDUSTRY PRODUCTIVITY– The Interdependency of High-Skilled Labor and ICT Investments

Thomas Strobel

The 2008 World Congress on National Accounts and Economic Performance Measures for Nations, Washington D.C., 05-15-2008

Ifo Institute for Economic Research

Motivation

• Labor productivity growth:

– US experienced two productivity surges 1995 & 2000

– Germany experienced dual productivity declines

• Sources of US productivity surges:

– ICT-producing and -using industries (e.g. Stiroh, 2002; Stiroh & Botsch, 2007)

• Germany:

– Much weaker ICT (using/producing) effects, unable to offset demise of other industries (Eicher & Roehn, 2007, Eicher & Strobel, 2008)

Ifo Institute for Economic Research

Motivation

• What if we look at the interaction of ICT and skills? What can we learn about German industry performance and productivity contributions? – Capital-skill complementarity: Griliches (1969)

extended to ICT capital-skill complementarity (e.g. Brynjolfsson et al., 2002)

– Skill-biased technological change (e.g. Acemoglu, 1998, 2002, Aghion, 2002, and Hornstein et al. 2005, O’Mahony et al., 2002)

• Focus: High-skill intensity of industries– Share of high-skilled hours worked in total hours worked ( EU KLEMS)

– High skilled = university graduates

– Available for 14 industries, higher aggregates are imputed at lower sectoral levels of aggregation

– Industry classification: High-skill-intensive are those who are above the median

Ifo Institute for Economic Research

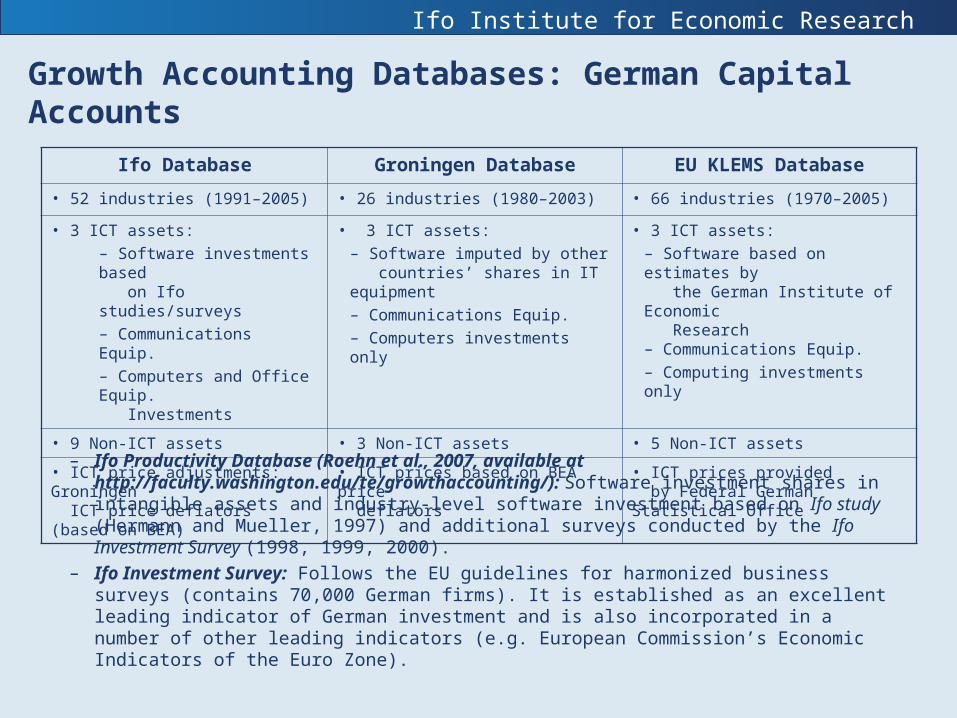

Growth Accounting Databases: German Capital Accounts

Ifo Database Groningen Database EU KLEMS Database

• 52 industries (1991–2005) • 26 industries (1980–2003) • 66 industries (1970–2005)

• 3 ICT assets:– Software investments based on Ifo studies/surveys – Communications Equip.– Computers and Office Equip.

Investments

• 3 ICT assets:– Software imputed by other countries’ shares in IT equipment– Communications Equip. – Computers investments only

• 3 ICT assets:– Software based on estimates by the German Institute of Economic Research– Communications Equip. – Computing investments only

• 9 Non-ICT assets • 3 Non-ICT assets • 5 Non-ICT assets

• ICT price adjustments: Groningen ICT price deflators (based on BEA)

• ICT prices based on BEA price deflators

• ICT prices provided by Federal German Statistical Office

– Ifo Productivity Database (Roehn et al., 2007, available at http://faculty.washington.edu/te/growthaccounting/): Software investment shares in intangible assets and industry-level software investment based on Ifo study (Hermann and Mueller, 1997) and additional surveys conducted by the Ifo Investment Survey (1998, 1999, 2000).

– Ifo Investment Survey: Follows the EU guidelines for harmonized business surveys (contains 70,000 German firms). It is established as an excellent leading indicator of German investment and is also incorporated in a number of other leading indicators (e.g. European Commission’s Economic Indicators of the Euro Zone).

Ifo Institute for Economic Research

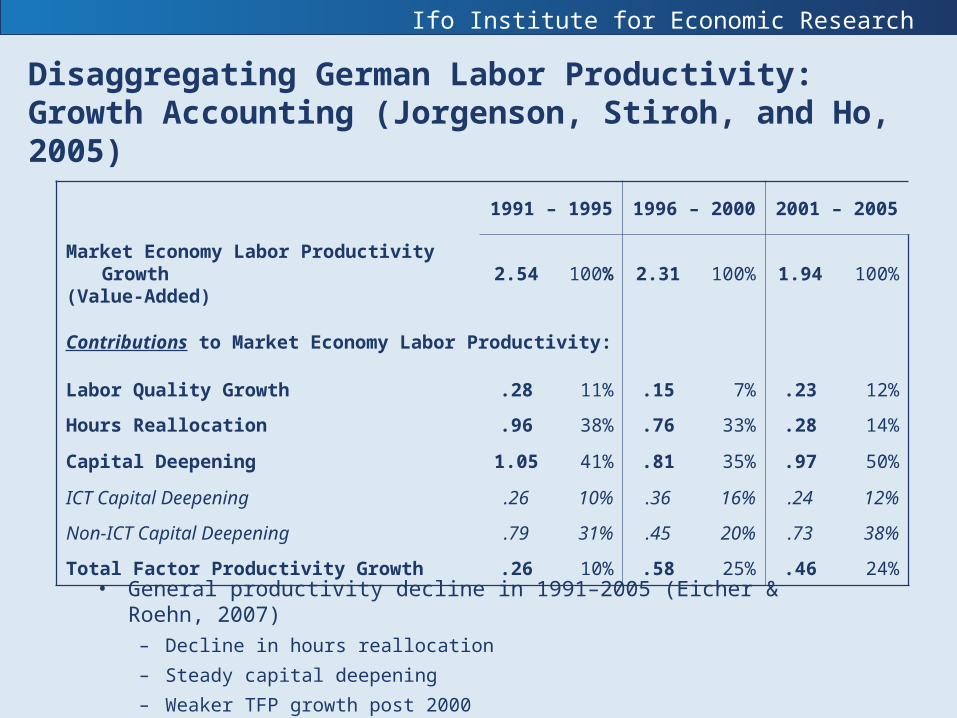

• General productivity decline in 1991–2005 (Eicher & Roehn, 2007)– Decline in hours reallocation

– Steady capital deepening

– Weaker TFP growth post 2000

1991 – 1995 1996 – 2000 2001 – 2005

Market Economy Labor Productivity Growth(Value-Added)

2.54 100% 2.31 100% 1.94 100%

Contributions to Market Economy Labor Productivity:

Labor Quality Growth .28 11% .15 7% .23 12%

Hours Reallocation .96 38% .76 33% .28 14%

Capital Deepening 1.05 41% .81 35% .97 50%

ICT Capital Deepening .26 10% .36 16% .24 12%

Non-ICT Capital Deepening .79 31% .45 20% .73 38%

Total Factor Productivity Growth .26 10% .58 25% .46 24%

Disaggregating German Labor Productivity: Growth Accounting (Jorgenson, Stiroh, and Ho, 2005)

Ifo Institute for Economic Research

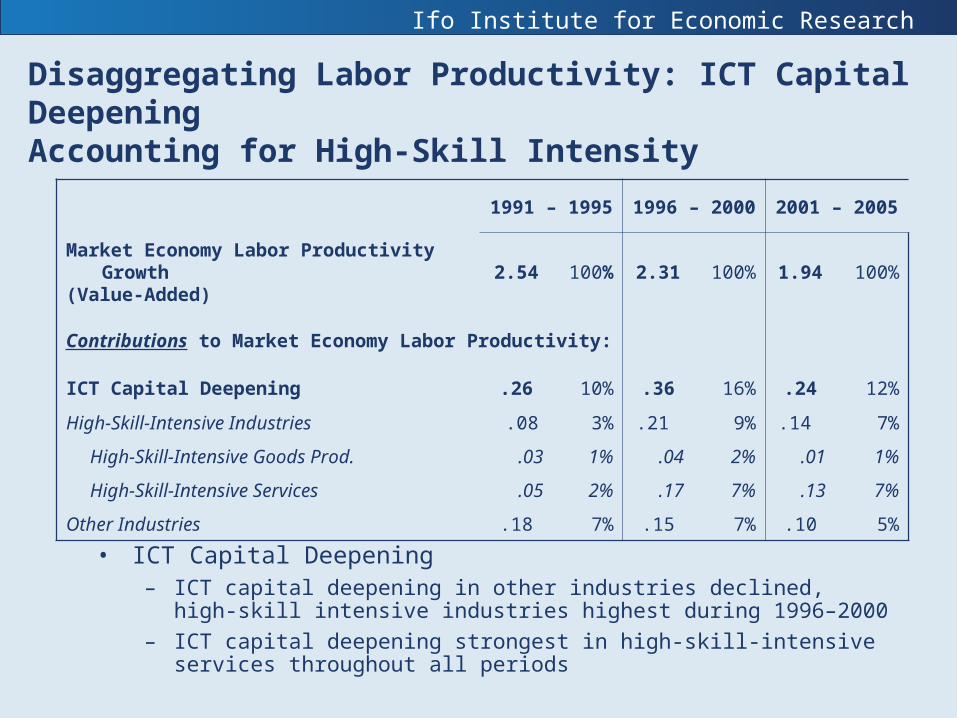

Disaggregating Labor Productivity: ICT Capital DeepeningAccounting for High-Skill Intensity

1991 – 1995 1996 – 2000 2001 – 2005

Market Economy Labor Productivity Growth(Value-Added)

2.54 100% 2.31 100% 1.94 100%

Contributions to Market Economy Labor Productivity:

ICT Capital Deepening .26 10% .36 16% .24 12%

High-Skill-Intensive Industries .08 3% .21 9% .14 7%

High-Skill-Intensive Goods Prod. .03 1% .04 2% .01 1%

High-Skill-Intensive Services .05 2% .17 7% .13 7%

Other Industries .18 7% .15 7% .10 5%

• ICT Capital Deepening– ICT capital deepening in other industries declined, high-skill intensive

industries highest during 1996–2000

– ICT capital deepening strongest in high-skill-intensive services throughout all periods

Ifo Institute for Economic Research

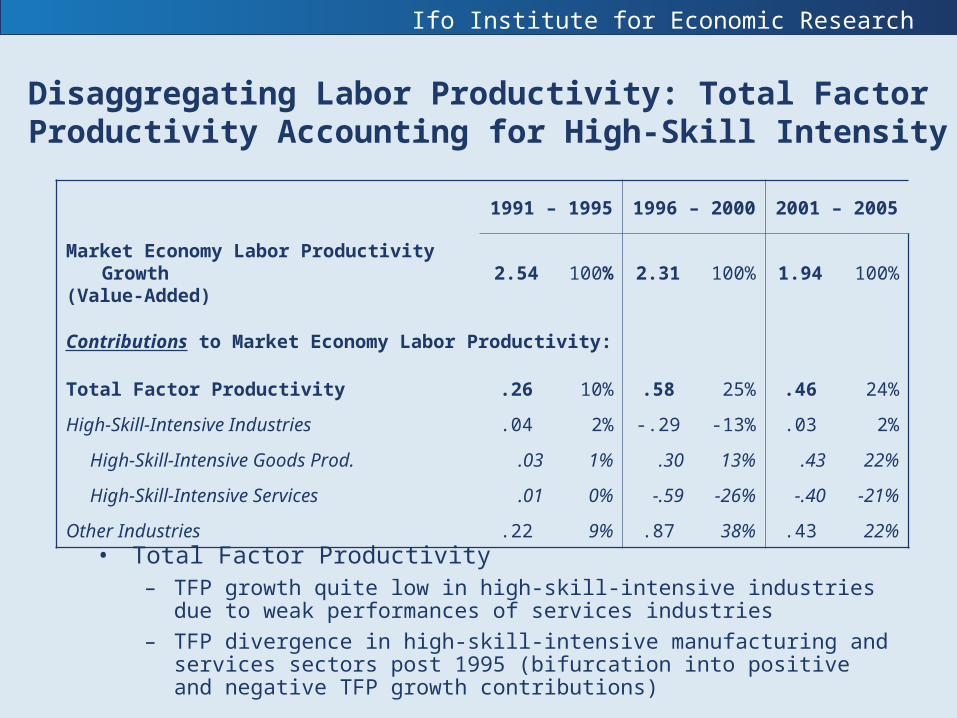

Disaggregating Labor Productivity: Total Factor Productivity Accounting for High-Skill Intensity

1991 – 1995 1996 – 2000 2001 – 2005

Market Economy Labor Productivity Growth(Value-Added)

2.54 100% 2.31 100% 1.94 100%

Contributions to Market Economy Labor Productivity:

Total Factor Productivity .26 10% .58 25% .46 24%

High-Skill-Intensive Industries .04 2% -.29 -13% .03 2%

High-Skill-Intensive Goods Prod. .03 1% .30 13% .43 22%

High-Skill-Intensive Services .01 0% -.59 -26% -.40 -21%

Other Industries .22 9% .87 38% .43 22%

• Total Factor Productivity– TFP growth quite low in high-skill-intensive industries due to weak

performances of services industries

– TFP divergence in high-skill-intensive manufacturing and services sectors post 1995 (bifurcation into positive and negative TFP growth contributions)

Ifo Institute for Economic Research

Disaggregating Labor Productivity:Accounting for High-Skill Intensity

• Descriptive trends

– High-skill-intensive industries:

Higher ICT capital deepening, but

lower TFP growth, especially due to services

– Other industries:

Falling ICT capital deepening and

stronger TFP growth during 1995–2000, but weaker again post 2000

• Formal testing (on a more disaggregate level)

– Are there statistically significant differences from ICT capital deepening on productivity growth for high-skill-intensive compared to other industries?

– Econometric testing approaches

Ifo Institute for Economic Research

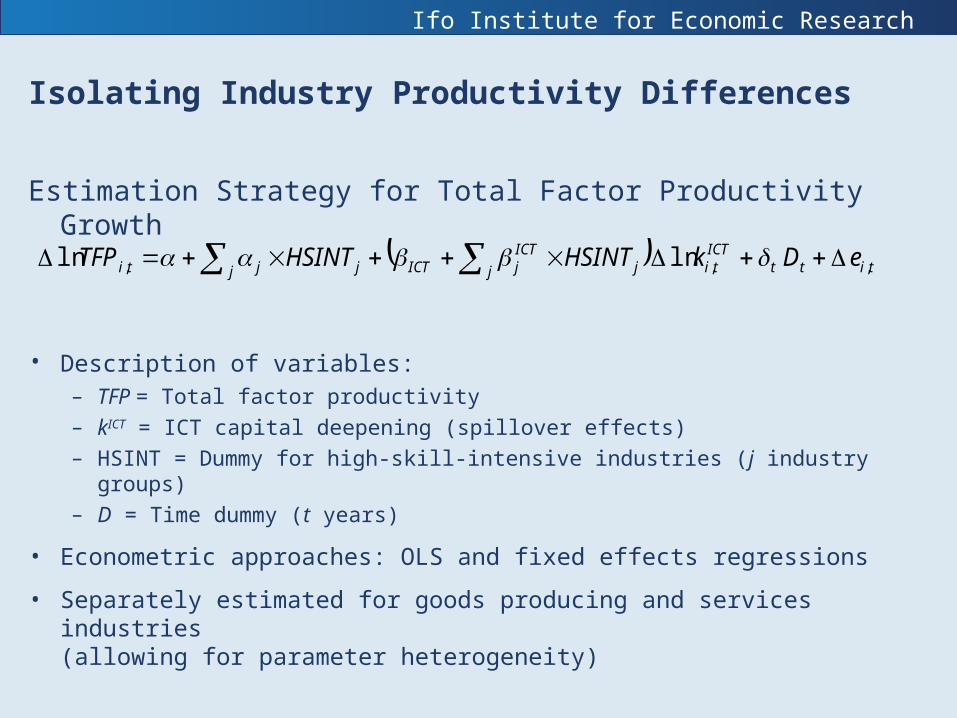

Isolating Industry Productivity Differences

Estimation Strategy for Total Factor Productivity Growth

• Description of variables: – TFP = Total factor productivity– kICT = ICT capital deepening (spillover effects)

– HSINT = Dummy for high-skill-intensive industries (j industry groups)– D = Time dummy (t years)

• Econometric approaches: OLS and fixed effects regressions

• Separately estimated for goods producing and services industries (allowing for parameter heterogeneity)

tittICTtij j

ICTjICTj jjti eDkHSINTHSINTTFP ,,, lnln

Ifo Institute for Economic Research

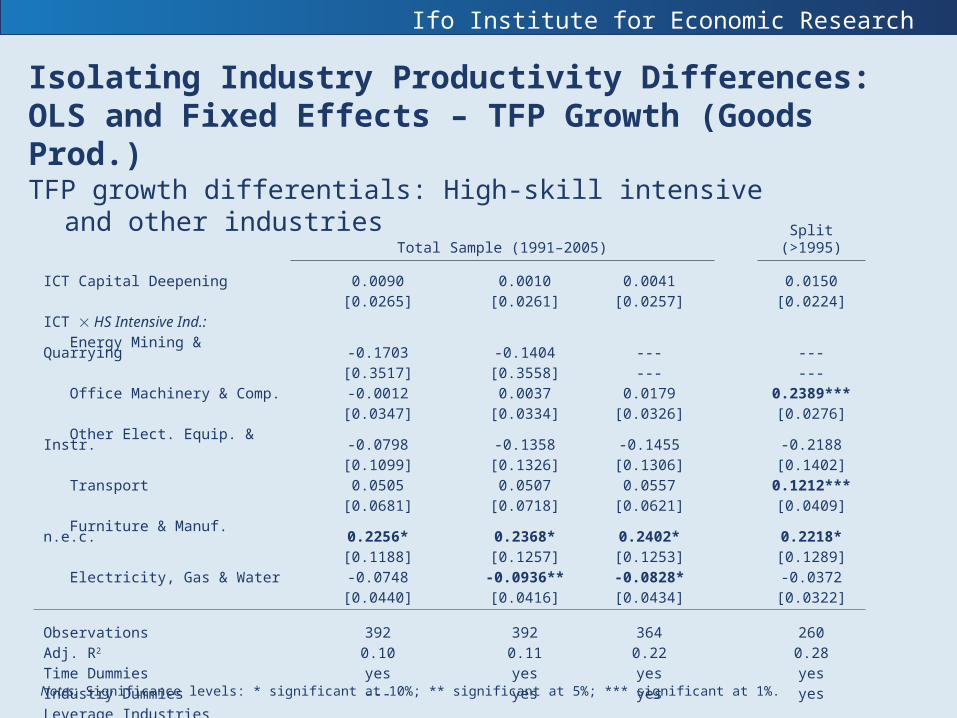

Isolating Industry Productivity Differences:OLS and Fixed Effects – TFP Growth (Goods Prod.)

TFP growth differentials: High-skill intensive and other industriesTotal Sample (1991–2005) Split (>1995)

ICT Capital Deepening 0.0090 0.0010 0.0041 0.0150

[0.0265] [0.0261] [0.0257] [0.0224]

ICT HS Intensive Ind.:

Energy Mining & Quarrying -0.1703 -0.1404 --- ---

[0.3517] [0.3558] --- ---

Office Machinery & Comp. -0.0012 0.0037 0.0179 0.2389***

[0.0347] [0.0334] [0.0326] [0.0276]

Other Elect. Equip. & Instr. -0.0798 -0.1358 -0.1455 -0.2188

[0.1099] [0.1326] [0.1306] [0.1402]

Transport 0.0505 0.0507 0.0557 0.1212***

[0.0681] [0.0718] [0.0621] [0.0409]

Furniture & Manuf. n.e.c. 0.2256* 0.2368* 0.2402* 0.2218*

[0.1188] [0.1257] [0.1253] [0.1289]

Electricity, Gas & Water -0.0748 -0.0936** -0.0828* -0.0372

[0.0440] [0.0416] [0.0434] [0.0322]

Observations 392 392 364 260

Adj. R2 0.10 0.11 0.22 0.28

Time Dummies yes yes yes yes

Industry Dummies --- yes yes yes

Leverage Industries excluded --- --- yes yes

Notes: Significance levels: * significant at 10%; ** significant at 5%; *** significant at 1%.

Ifo Institute for Economic Research

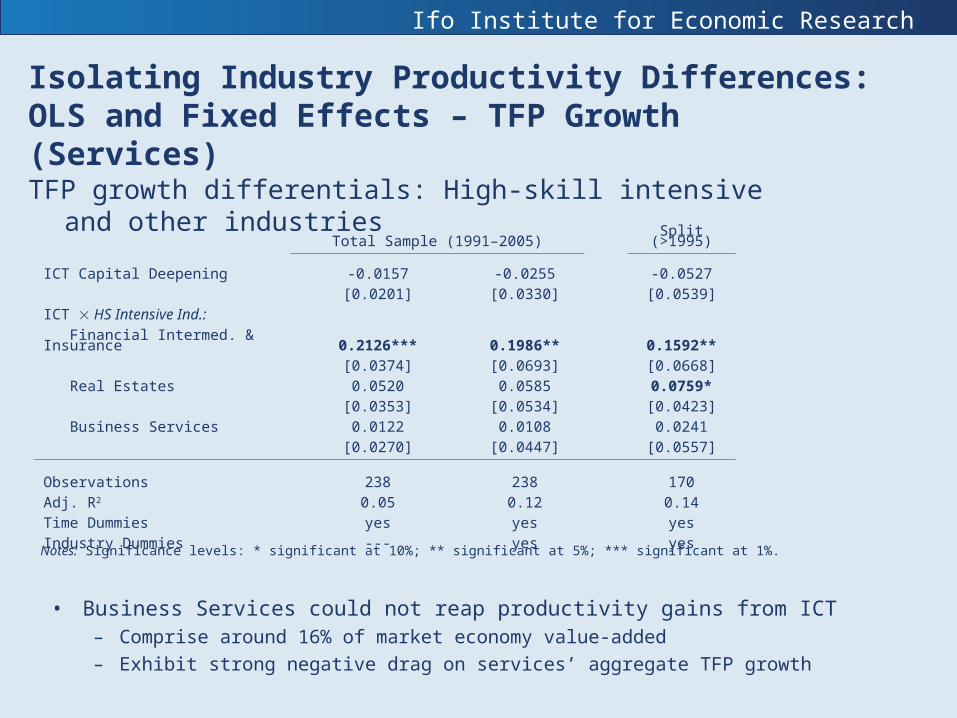

Isolating Industry Productivity Differences:OLS and Fixed Effects – TFP Growth (Services)

TFP growth differentials: High-skill intensive and other industriesTotal Sample (1991–2005) Split (>1995)

ICT Capital Deepening -0.0157 -0.0255 -0.0527

[0.0201] [0.0330] [0.0539]

ICT HS Intensive Ind.:

Financial Intermed. & Insurance 0.2126*** 0.1986** 0.1592**

[0.0374] [0.0693] [0.0668]

Real Estates 0.0520 0.0585 0.0759*

[0.0353] [0.0534] [0.0423]

Business Services 0.0122 0.0108 0.0241

[0.0270] [0.0447] [0.0557]

Observations 238 238 170

Adj. R2 0.05 0.12 0.14

Time Dummies yes yes yes

Industry Dummies --- yes yes

Notes: Significance levels: * significant at 10%; ** significant at 5%; *** significant at 1%.

• Business Services could not reap productivity gains from ICT – Comprise around 16% of market economy value-added

– Exhibit strong negative drag on services’ aggregate TFP growth

Ifo Institute for Economic Research

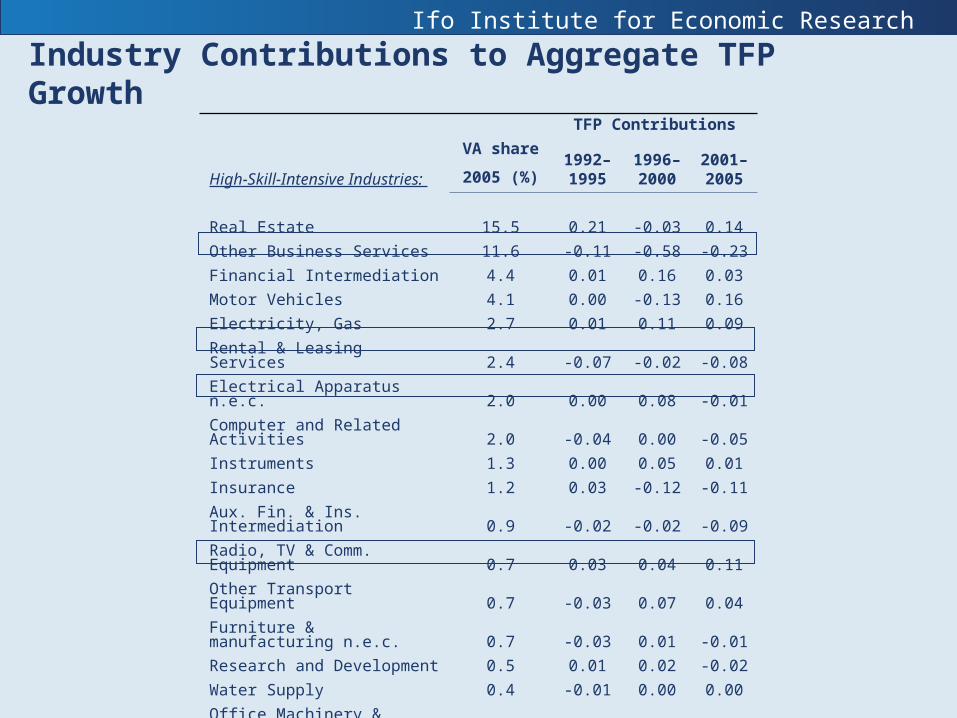

Industry Contributions to Aggregate TFP Growth

High-Skill-Intensive Industries:

VA share

2005 (%)

TFP Contributions

1992–1995

1996–2000

2001–2005

Real Estate 15.5 0.21 -0.03 0.14

Other Business Services 11.6 -0.11 -0.58 -0.23

Financial Intermediation 4.4 0.01 0.16 0.03

Motor Vehicles 4.1 0.00 -0.13 0.16

Electricity, Gas 2.7 0.01 0.11 0.09

Rental & Leasing Services 2.4 -0.07 -0.02 -0.08

Electrical Apparatus n.e.c. 2.0 0.00 0.08 -0.01

Computer and Related Activities 2.0 -0.04 0.00 -0.05

Instruments 1.3 0.00 0.05 0.01

Insurance 1.2 0.03 -0.12 -0.11

Aux. Fin. & Ins. Intermediation 0.9 -0.02 -0.02 -0.09

Radio, TV & Comm. Equipment 0.7 0.03 0.04 0.11

Other Transport Equipment 0.7 -0.03 0.07 0.04

Furniture & manufacturing n.e.c. 0.7 -0.03 0.01 -0.01

Research and Development 0.5 0.01 0.02 -0.02

Water Supply 0.4 -0.01 0.00 0.00

Office Machinery & Computers 0.2 0.03 0.11 0.06

Mining & Quarrying, ex. Energy 0.1 0.01 0.00 -0.01

Energy Mining & Quarrying 0.1 0.03 -0.03 -0.02

Recycling 0.1 0.00 0.00 -0.01

Ifo Institute for Economic Research

Conclusion

• There is an ICT-skill complementarity for German industries

– High-skill-intensive industries have higher ICT capital deepening, especially in the services sectors

– ICT capital deepening in other (non-high-skill-intensive) industries is steadily declining

• ICT and skills enhanced industries’ productivity performance

– There are productivity increasing effects from ICT capital deepening in high-skill-intensive goods producing and services industries, especially post 1995 (cp. TFP growth regressions)

– Negative total factor productivity growth in high-skill-intensive services (cp. growth accounting exercises) is due to weak performance of Business Services

– Potential explanations

• Measurement of services output

• Regulations might hinder ICT diffusion (Nicoletti et al., 2006)

• Share of high-skilled workers too low (e.g. brain drain)

Ifo Institute for Economic Research

Thank You for Your Attention!

Ifo Institute for Economic Research

Back Up

Ifo Institute for Economic Research

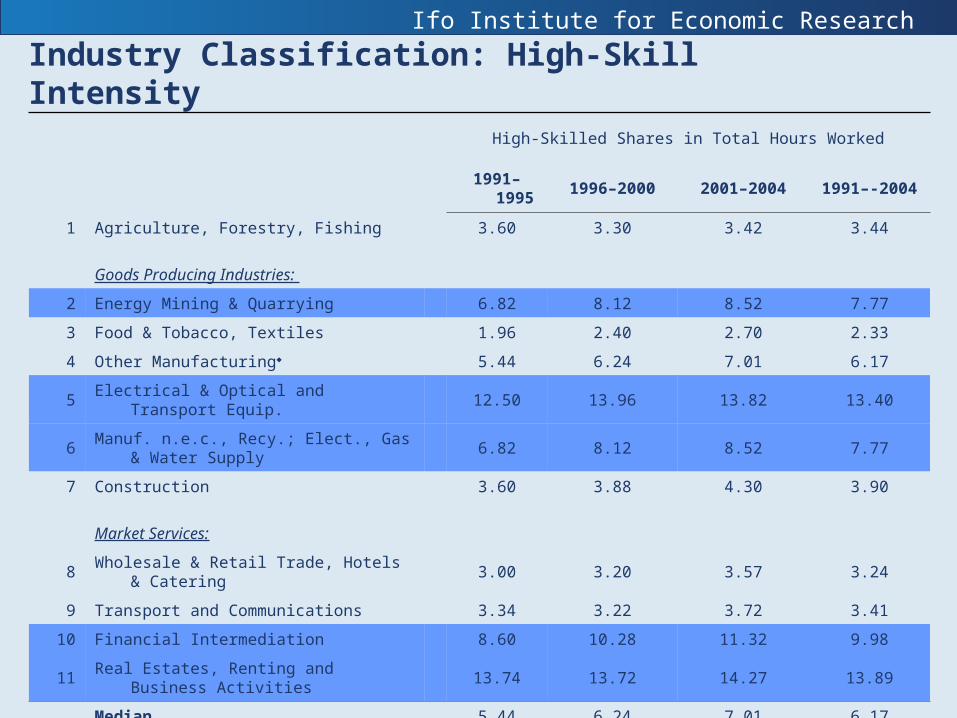

Industry Classification: High-Skill Intensity

High-Skilled Shares in Total Hours Worked

1991–1995 1996–2000 2001–2004 1991–-2004

1 Agriculture, Forestry, Fishing 3.60 3.30 3.42 3.44

Goods Producing Industries:

2 Energy Mining & Quarrying 6.82 8.12 8.52 7.77

3 Food & Tobacco, Textiles 1.96 2.40 2.70 2.33

4 Other Manufacturing♦ 5.44 6.24 7.01 6.17

5 Electrical & Optical and Transport Equip. 12.50 13.96 13.82 13.40

6 Manuf. n.e.c., Recy.; Elect., Gas & Water Supply 6.82 8.12 8.52 7.77

7 Construction 3.60 3.88 4.30 3.90

Market Services:

8 Wholesale & Retail Trade, Hotels & Catering 3.00 3.20 3.57 3.24

9 Transport and Communications 3.34 3.22 3.72 3.41

10 Financial Intermediation 8.60 10.28 11.32 9.98

11 Real Estates, Renting and Business Activities 13.74 13.72 14.27 13.89

Median 5.44 6.24 7.01 6.17

Mean 6.31 6.95 7.38 6.84

Ifo Institute for Economic Research

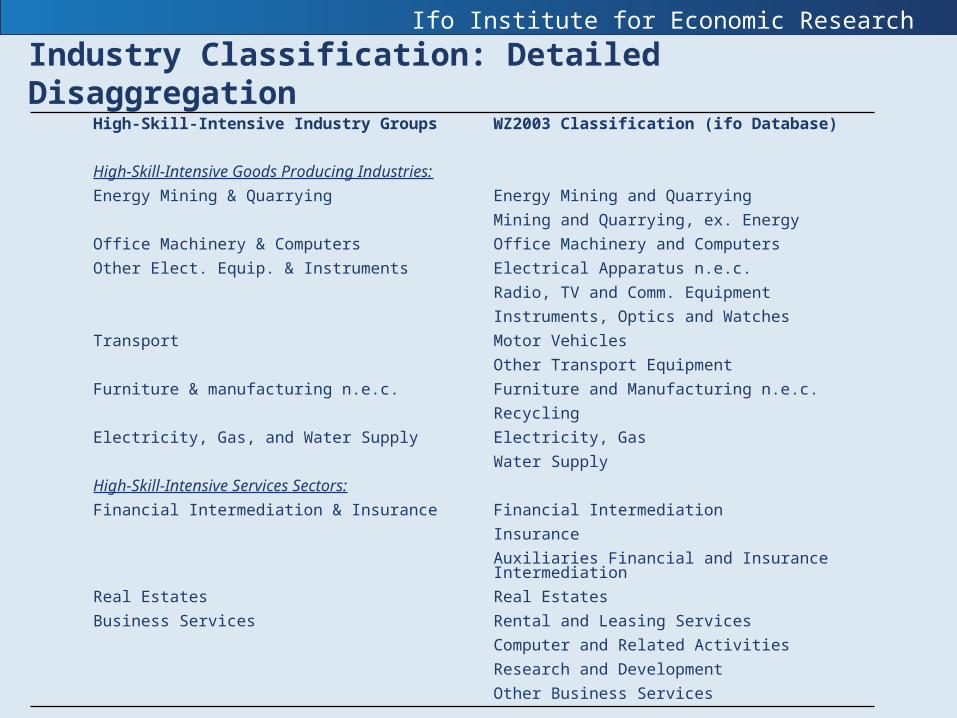

Industry Classification: Detailed Disaggregation High-Skill-Intensive Industry Groups WZ2003 Classification (ifo Database)

High-Skill-Intensive Goods Producing Industries:

Energy Mining & Quarrying Energy Mining and Quarrying

Mining and Quarrying, ex. Energy

Office Machinery & Computers Office Machinery and Computers

Other Elect. Equip. & Instruments Electrical Apparatus n.e.c.

Radio, TV and Comm. Equipment

Instruments, Optics and Watches

Transport Motor Vehicles

Other Transport Equipment

Furniture & manufacturing n.e.c. Furniture and Manufacturing n.e.c.

Recycling

Electricity, Gas, and Water Supply Electricity, Gas

Water Supply

High-Skill-Intensive Services Sectors:

Financial Intermediation & Insurance Financial Intermediation

Insurance

Auxiliaries Financial and Insurance Intermediation

Real Estates Real Estates

Business Services Rental and Leasing Services

Computer and Related Activities

Research and Development

Other Business Services

Ifo Institute for Economic Research

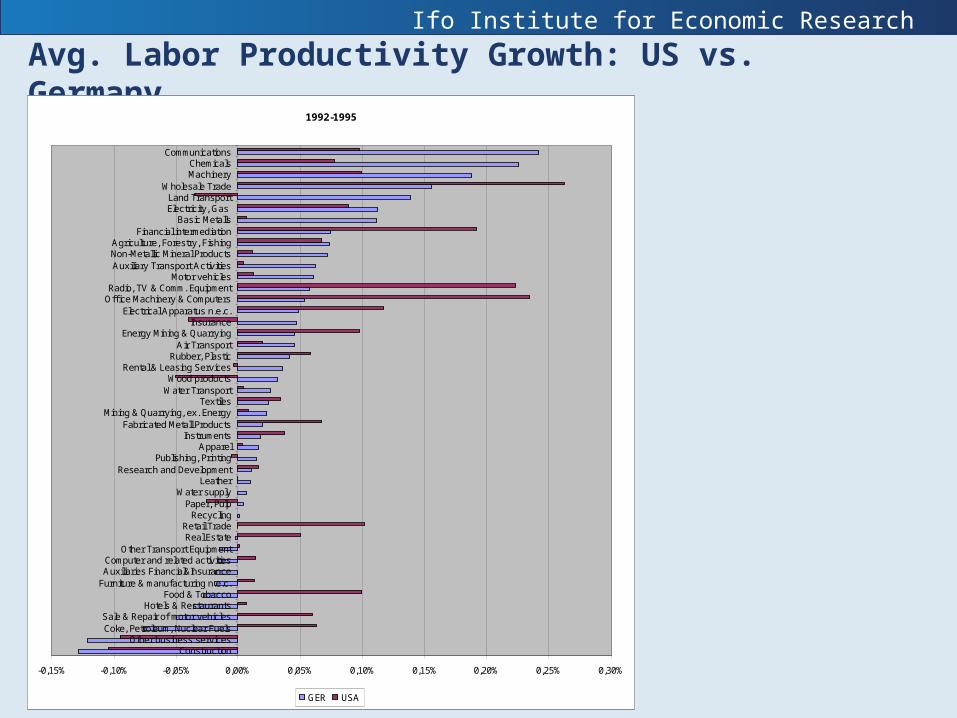

Avg. Labor Productivity Growth: US vs. Germany 1992-1995

-0,15% -0,10% -0,05% 0,00% 0,05% 0,10% 0,15% 0,20% 0,25% 0,30%

ConstructionOther business services

Coke, Petroleum, Nuclear FuelsSale & Repair of motor vehicles

Hotels & RestaurantsFood & Tobacco

Furniture & manufacturing n.e.c.Auxiliaries Financial&InsuranceComputer and related activities

Other Transport EquipmentReal EstateRetail Trade

RecyclingPaper, Pulp

Water supplyLeather

Research and DevelopmentPublishing, Printing

ApparelInstruments

Fabricated Metall ProductsMining & Quarrying, ex. Energy

TextilesWater TransportWood products

Rental & Leasing ServicesRubber, Plastic

Air TransportEnergy Mining & Quarrying

InsuranceElectrical Apparatus n.e.c.

Office Machinery & ComputersRadio, TV & Comm. Equipment

Motor vehiclesAuxiliary Transport ActivitiesNon-Metallic Mineral ProductsAgriculture, Forestry, Fishing

Financial intermediationBasic Metalls

Electricity, Gas Land Transport

Wholesale TradeMachineryChemicals

Communications

GER USA

Ifo Institute for Economic Research

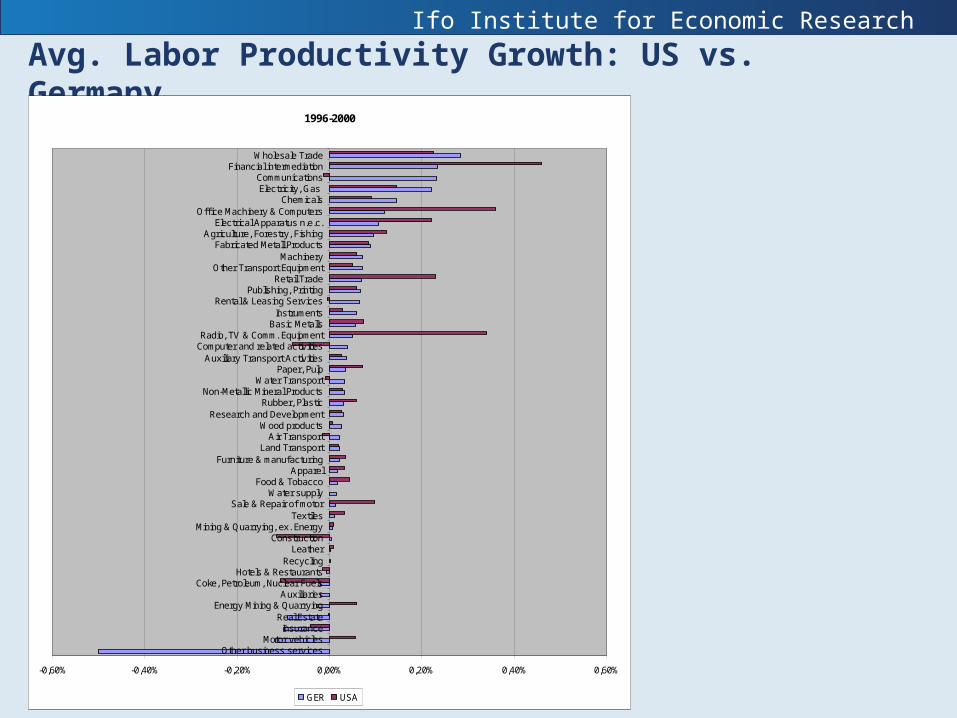

Avg. Labor Productivity Growth: US vs. Germany 1996-2000

-0,60% -0,40% -0,20% 0,00% 0,20% 0,40% 0,60%

Other business servicesMotor vehicles

InsuranceReal Estate

Energy Mining & QuarryingAuxiliaries

Coke, Petroleum, Nuclear FuelsHotels & Restaurants

RecyclingLeather

ConstructionMining & Quarrying, ex. Energy

TextilesSale & Repair of motor

Water supplyFood & Tobacco

ApparelFurniture & manufacturing

Land TransportAir Transport

Wood productsResearch and Development

Rubber, PlasticNon-Metallic Mineral Products

Water TransportPaper, Pulp

Auxiliary Transport ActivitiesComputer and related activitiesRadio, TV & Comm. Equipment

Basic MetallsInstruments

Rental & Leasing ServicesPublishing, Printing

Retail TradeOther Transport Equipment

MachineryFabricated Metall Products

Agriculture, Forestry, FishingElectrical Apparatus n.e.c.

Office Machinery & ComputersChemicals

Electricity, Gas Communications

Financial intermediationWholesale Trade

GER USA

Ifo Institute for Economic Research

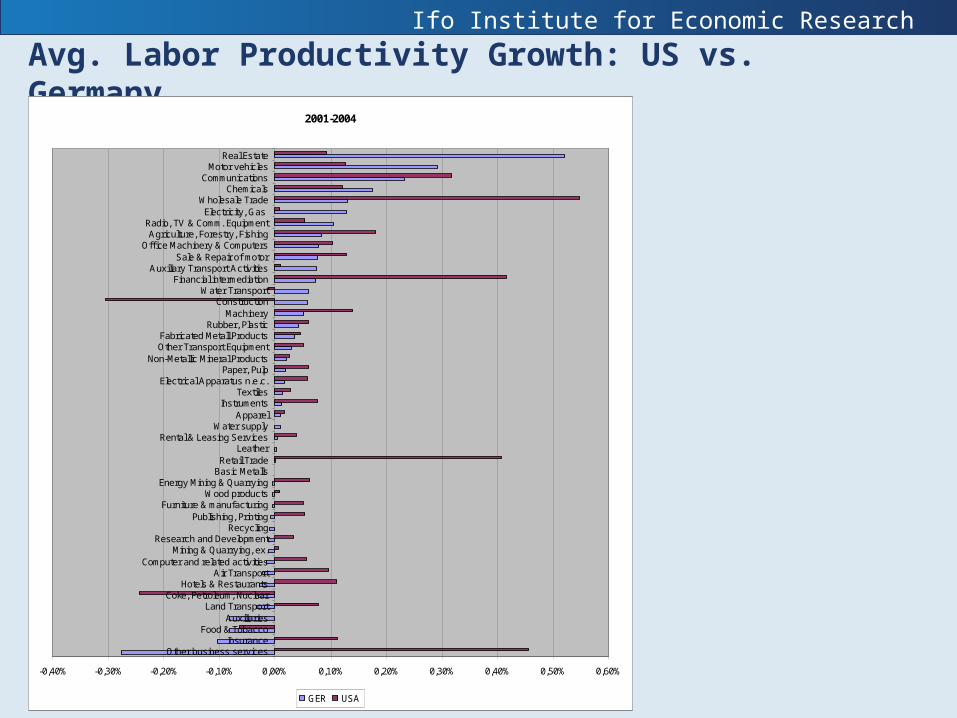

Avg. Labor Productivity Growth: US vs. Germany 2001-2004

-0,40% -0,30% -0,20% -0,10% 0,00% 0,10% 0,20% 0,30% 0,40% 0,50% 0,60%

Other business servicesInsurance

Food & TobaccoAuxiliaries

Land TransportCoke, Petroleum, Nuclear

Hotels & RestaurantsAir Transport

Computer and related activitiesMining & Quarrying, ex.

Research and DevelopmentRecycling

Publishing, PrintingFurniture & manufacturing

Wood productsEnergy Mining & Quarrying

Basic MetallsRetail Trade

LeatherRental & Leasing Services

Water supplyApparel

InstrumentsTextiles

Electrical Apparatus n.e.c.Paper, Pulp

Non-Metallic Mineral ProductsOther Transport EquipmentFabricated Metall Products

Rubber, PlasticMachinery

ConstructionWater Transport

Financial intermediationAuxiliary Transport Activities

Sale & Repair of motorOffice Machinery & Computers

Agriculture, Forestry, FishingRadio, TV & Comm. Equipment

Electricity, Gas Wholesale Trade

ChemicalsCommunications

Motor vehiclesReal Estate

GER USA