ifc’s debt capital market strategy in “frontier...

TRANSCRIPT

IFC’s Debt Capital Market

Strategy in “Frontier Markets”

The Nigerian Debt Capital Markets Workshop

Lagos, October 2015.

IFC and the World Bank Group

2

Overview of IFC

• End extreme poverty: the percentage of

people living with less than $1.25 a day to fall to

no more than 3% globally by 2030

• Promote shared prosperity: foster income

growth of the bottom 40% of population in

developing countries

Conciliation and

arbitration

of investment disputes

International Centre

for Settlement of

Investment Disputes

Provides loans, equity,

and advisory services to

private sector in

developing countries

International

Finance

Corporation

Provides loans to middle-

income and credit-worthy

low-income country

governments

International Bank

for Reconstruction

and Development

Interest-free loans and

grants to governments of

poorest countries

International

Development

Association

Guarantees of foreign

direct investment’s non-

commercial

risks

Multilateral

Investment

Guarantee Agency

The World Bank Group has adopted two ambitious goals:

• Owned by 184 member countries

• A member of the World Bank Group

India9.1%

India9.1%

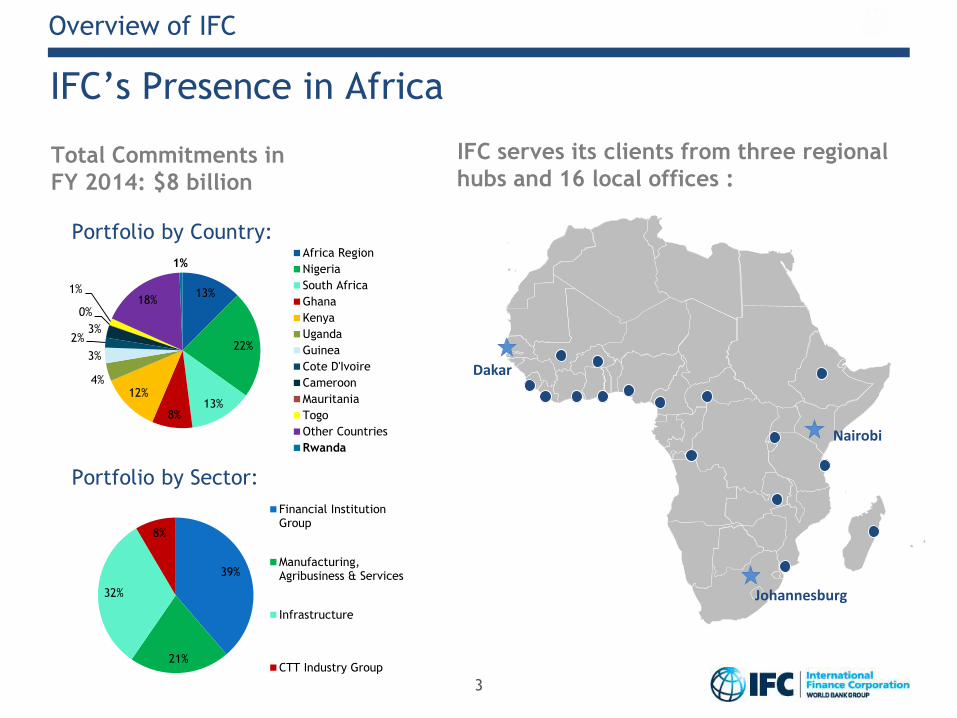

IFC’s Presence in Africa

3

Financial StrengthOverview of IFC

IFC serves its clients from three regional

hubs and 16 local offices :

Dakar

Johannesburg

Nairobi

Total Commitments in

FY 2014: $8 billion

Portfolio by Country:

Portfolio by Sector:

13%

22%

13%8%

12%4%

3%

2%3%

0%

1%18%

1%Africa Region

Nigeria

South Africa

Ghana

Kenya

Uganda

Guinea

Cote D'Ivoire

Cameroon

Mauritania

Togo

Other Countries

Rwanda

39%

21%

32%

8%

Financial InstitutionGroup

Manufacturing,Agribusiness & Services

Infrastructure

CTT Industry Group

Overview of IFC

444

• IFC views DCM as one of the 3 types of infrastructure critical to developing a country: • physical infrastructure (road, power, water, telecommunications, etc.); • social infrastructure (investing in their own people’s health and education); and • financial infrastructure (a platform for channeling national saving towards investments

into economically vital sectors)

• Commercial banks’ ALM structures and increasingly Basel’s requirements will restrict domestic banks activities to the short to medium term segment of the financing need of the economy.

• Capital markets are pivotal to funding long-term investments by mobilizing patient savings from institutional investors into transformational projects.

• IFC, though the joint World Bank / IFC advisory programs and the WBG’s global practices, conduct markets’ assessments, inform and support institutional reforms towards adopting internationally accepted best practices, and contribute to improving the capacity of markets’ participants.

• IFC’s Treasury sets up local currency bond programs under which it issues notes in a number of countries and facilitates corporate issuances to increase bonds’ supply, risk-reward options, and diversification options to investors in emerging markets.

Domestic Capital Markets – A Critical Infrastructure Pillar

5

IFC’s DCM Strategy: Issuer and Investor

Issuer“Supranational AAA”

Strategic Intervention

Investor“Corporate & Municipality Debt”

Strategic & Opportunistic Intervention

Onshore Bonds Offshore BondsAnchor

InvestmentCredit

Enhancement

Onshore

Eurobond Securitizations

Partial Credit

Guarantee

666

• Besides the need to source funding for its local currency pipeline, IFC has striven through its capital markets outreach to achieve the following impacts:

• increase non-government bond issuances in domestic markets and develop credits layers from increased corporates’ and municipalities’ issuances;

• increase domestic and international investors’ participations in local currency issuances;

• improve the capacity of regulators and markets’ participants; and

• contribute to extending and deepening the yield curve and the credit culture.

IFC’s DCM Strategy – Being mindful of the targeted impacts

777

Description

• Programs under which IFC may issue debt instruments with maturities of 3 months or longer in various jurisdictions

• The Programs’ documentation and application are reviewed and approved by local regulators and the bond is listed on the local stock exchange

• IFC launched in 2012 a Pan African Domestic Medium Term Notes Program that initially included Botswana, Ghana, Kenya, Namibia, Rwanda, South Africa, Uganda and Zambia, and is currently being extended to the CFA franc zone and Nigeria

Purpose

• raise local currency funding to finance IFC’s project in local currency and help domestic companies avoid exposure to cross-currency risk; and/or

• develop liquid and deep bond market ensuring diversified sources of funding to meet business needs.

Benefits to local markets

• Introduction of a new asset class of highest credit quality

• Setting a risk-free benchmark

• Diversification of domestic and foreign institutional investors

• Assist in accelerating development of non-sovereign sector of bond market

• Significant contribution to further development of the African financial markets

IFC Issuances in Domestic Markets – A Mean to a Purpose

8

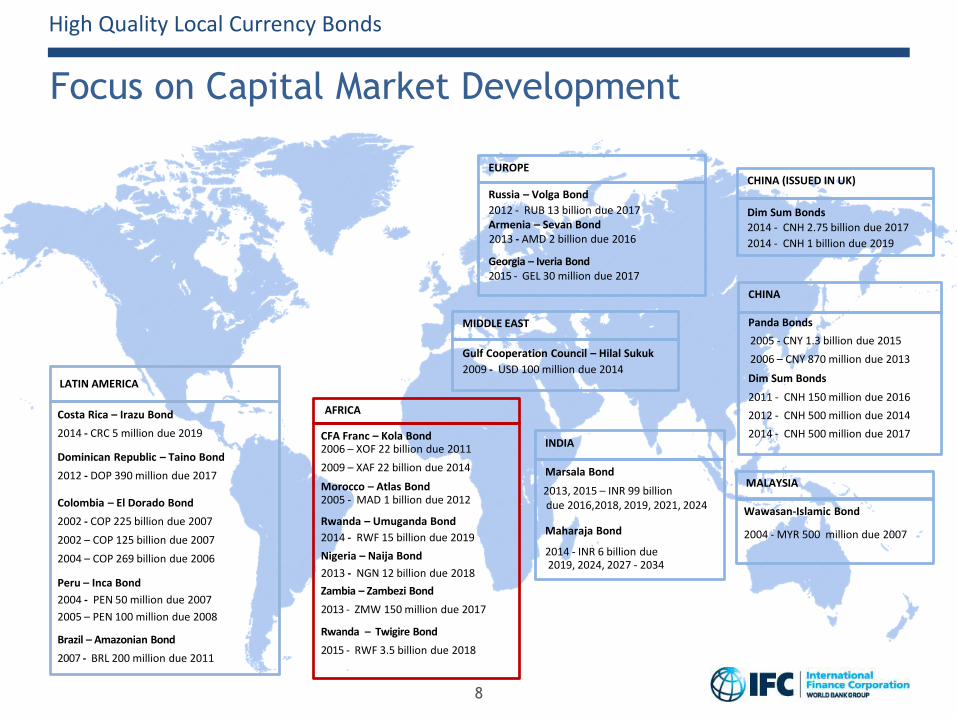

Focus on Capital Market Development

CHINA

Panda Bonds

2005 - CNY 1.3 billion due 2015

2006 – CNY 870 million due 2013

Dim Sum Bonds

2012 - CNH 500 million due 2014

2011 - CNH 150 million due 2016

2014 - CNH 500 million due 2017INDIA

Marsala Bond

2013, 2015 – INR 99 billiondue 2016,2018, 2019, 2021, 2024

Maharaja Bond

2014 - INR 6 billion due2019, 2024, 2027 - 2034

MALAYSIA

Wawasan-Islamic Bond

2004 - MYR 500 million due 2007

AFRICA

CFA Franc – Kola Bond 2006 – XOF 22 billion due 2011

2009 – XAF 22 billion due 2014

Rwanda – Umuganda Bond

2014 - RWF 15 billion due 2019

Nigeria – Naija Bond

2013 - NGN 12 billion due 2018

Zambia – Zambezi Bond

2013 - ZMW 150 million due 2017

Morocco – Atlas Bond2005 - MAD 1 billion due 2012

CHINA (ISSUED IN UK)

Dim Sum Bonds

2014 - CNH 1 billion due 2019

2014 - CNH 2.75 billion due 2017

LATIN AMERICA

Costa Rica – Irazu Bond

2014 - CRC 5 million due 2019

Dominican Republic – Taino Bond

2012 - DOP 390 million due 2017

Colombia – El Dorado Bond

2002 - COP 225 billion due 2007

2002 – COP 125 billion due 2007

2004 – COP 269 billion due 2006

Peru – Inca Bond

2004 - PEN 50 million due 2007

2005 – PEN 100 million due 2008

Brazil – Amazonian Bond

2007 - BRL 200 million due 2011

MIDDLE EAST

Gulf Cooperation Council – Hilal Sukuk

2009 - USD 100 million due 2014

High Quality Local Currency Bonds

Rwanda – Twigire Bond

2015 - RWF 3.5 billion due 2018

EUROPE

Russia – Volga Bond

Armenia – Sevan Bond2012 - RUB 13 billion due 2017

2013 - AMD 2 billion due 2016

Georgia – Iveria Bond2015 - GEL 30 million due 2017

9

Basics

• Support to a bond issuance by committing to purchase a portion of the notes issued afterdue diligence and credit approval

• Sign a commitment agreement, and IFC’s anchor investment can then be announced to themarket during the roadshow

Benefits to Investors

• IFC’s public support of the issuance reduces pricing uncertainty

• Investors derive comfort from IFC due diligence and “stamp of approval”

Benefits to Issuers

• Like a partial underwriting, an IFC anchor investment ensures a successful issuance

• IFC’s public endorsement will help to boost subscription levels and reduce the clearing yield

• IFC can support the structuring and marketing process as needed

IFC Investor – Anchor Investments

10

Anchor Investments (Case Studies)

Corporate Debt Investments

Zambia (Onshore Bond)

IFC Anchor Investment

• ZMW 60m (approx. US$ 9.4m)

• Pre-committed private placement

• IFC’s first anchor investment in Africa, and IFC’s first ZMW denominated corporate bond investment

Highlights

• Diversification of funding sources

• IFC supported the issuance by sharing its own issuance experiences, in close collaboration with the lead managers and legal advisors.

Issuer Bayport Financial Services Ltd, Zambia

Issuance Status Senior Secured

Pricing Date 16 April 2014

Settlement Date 25 April 2014

Size ZMW 172m (approx. US$ 27m)

Maturity 25 April 2018

Tenor 4 years

Coupon 2.50% over 182-T-Bill (Tranche 1) and 1.52% over 364 T-bill (Tranche 2)

Listing Lusaka Stock Exchange

Arranger: Barclays Bank Zambia, ABSA

Sponsoring Broker & Placing Agent:

Stockbrokers Zambia

Governing Law: Zambian Law

Nigeria (Eurobond)

IFC Anchor Investment

IFC Anchor Investment

• USD 50mm, amounting to 17% of the total issuance

• Pre-committed participation in public offering

Highlights

• Seven Energy’s inaugural high yield Eurobond issue

• First international Eurobond high yield issue by a non-listed Nigerian corporation

• IFC’s anchor investment contributed to mitigating the execution risk amidst volatile markets

• Investor base diversification and international outreach with investors from Africa, the US, Europe and Asia

Issuer Seven Energy Finance Ltd

Issuance Status Senior Secured

Issue Rating B- / B- (S&P, Fitch)

Issue Format 144A / Reg S

Pricing Date 2 October 2014

Settlement Date 10 October 2014

Size USD 300 million

Final Maturity 11 October 2021 final maturity

Non-Call 11 October 2018

Re-Offer Price / Yield 98.781% / 10.500% p.a.

Coupon 10.250% p.a.

Listing Irish Stock Exchange

Governing Law New York

Bookrunners Standard Chartered, Deutsche Bank, Morgan Stanley

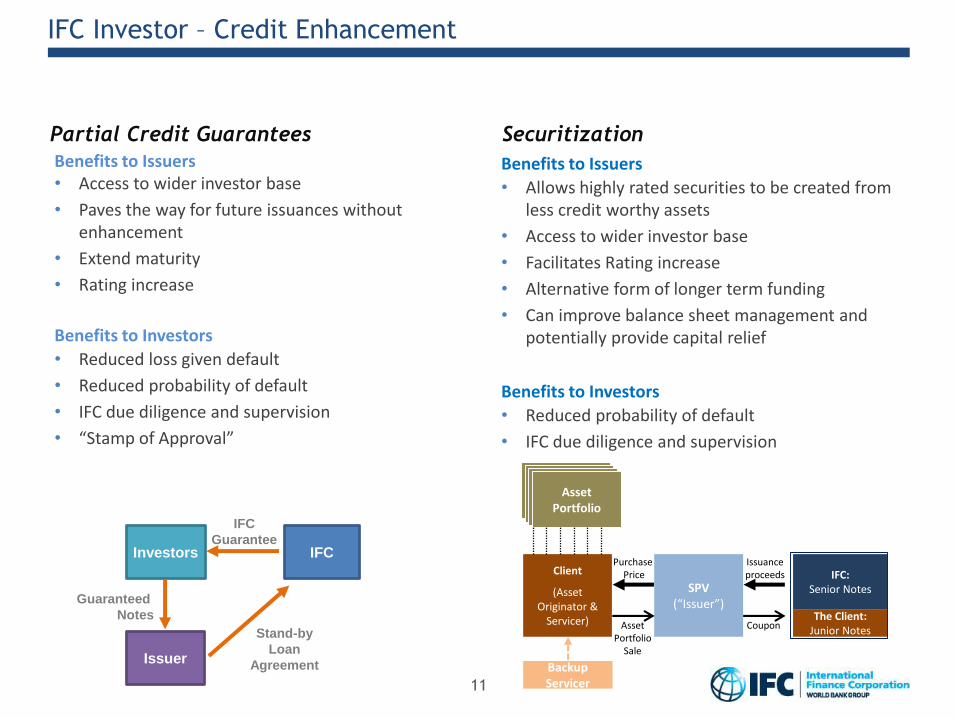

Benefits to Issuers• Access to wider investor base

• Paves the way for future issuances without enhancement

• Extend maturity

• Rating increase

Benefits to Investors

• Reduced loss given default

• Reduced probability of default

• IFC due diligence and supervision

• “Stamp of Approval”

11

Investors

Guaranteed

Notes

IFC

Guarantee

Stand-by

Loan

Agreement

IFC

Issuer

IFC Investor – Credit Enhancement

Benefits to Issuers

• Allows highly rated securities to be created from less credit worthy assets

• Access to wider investor base

• Facilitates Rating increase

• Alternative form of longer term funding

• Can improve balance sheet management and potentially provide capital relief

Benefits to Investors

• Reduced probability of default

• IFC due diligence and supervision

Partial Credit Guarantees Securitization

Coupon

SPV(“Issuer”)

Client

(Asset Originator &

Servicer)

IFC:Senior Notes

The Client:Junior Notes

Backup Servicer

Issuanceproceeds

AssetPortfolio

AssetPortfolio

AssetPortfolio

AssetPortfolio

AssetPortfolio

Sale

Purchase Price

• Fixed or variable rate loans from IFC denominated in local currency financed through

an IFC’s ALM swaps;

• Client Risk Management swaps (interest rate swaps or cross-currency swaps) which

allow clients to hedge existing or new foreign currency denominated liabilities back into

local currency; and

• Structured finance products (i.e., Partial Credit Guarantees, Securitizations, Risk

Sharing Facilities) which enable clients to borrow in local currency from other sources.

12

Other IFC’s Local Currency Products

Disclaimer

This document has been prepared for informational purposes only, and the information herein may be condensed or incomplete. IFC specifically

does not make any warranties or representations as to the accuracy or completeness of these materials. IFC is under no obligation to update these

materials.

This document is not a prospectus and is not intended to provide the basis for the evaluation of any securities issued by IFC. This information does

not constitute an invitation or offer to subscribe for or purchase any of the products or services mentioned. Under no circumstances shall IFC or its

affiliates be liable for any loss, damage, liability or expense incurred or suffered which is claimed to have resulted from use of these materials,

including without limitation any direct, indirect, special or consequential damages, even if IFC has been advised of the possibility of such damages.

For additional information concerning IFC, please refer to IFC’s current “Information Statement”, financial statements and other relevant

information available at www.ifc.org/investors.