ifc in sub-saharan africa

TRANSCRIPT

IFC in Sub-Saharan Africa FKI-IMF Conference

November 07, 2013

IBRD

International Bank

for Reconstruction

and Development

IDA

International

Development

Association

IFC

International Finance

Corporation

MIGA

Multilateral

Investment and

Guarantee Agency

Est. 1945 Est. 1960 Est. 1956 Est. 1988

Role To promote

institutional, legal and

regulatory reform

To promote

institutional, legal and

regulatory reform

To promote private

sector development

To reduce political

investment risk

Clients Governments of member

countries with per

capita income between

$1,025 and $6,055

Governments of poorest

countries with per

capita income of less

than $1,025

Private companies in

182 member countries

Foreign investors in

member countries

Products • Technical Assistance

• Loans

• Policy Advice

• Technical Assistance

• Interest Free Loans

• Policy Advice

• Equity / Quasi-Equity

• Long-term Loans

• Risk Management

• Advisory Services

Political Risk Insurance

IFC is the private sector arm of the WBG – Multilateral with a Private Sector Focus

IFC and the World Bank Group

2

IFC: Over $97 Billion Invested Since 1956

• Largest multilateral source of loan/equity financing for the emerging

markets private sector

• Founded in 1956 with 184 member countries

• AAA-rated by S&P and Moody’s

• Equity, quasi-equity, loans, risk management and local currency products

• Takes market risk with no sovereign guarantees

• Promoter of environmental, social, and corporate governance standards

• Resources and know-how of a global development bank with the

flexibility of a merchant bank

• Holds equity in over 756 companies worldwide, 185 of which are funds

3

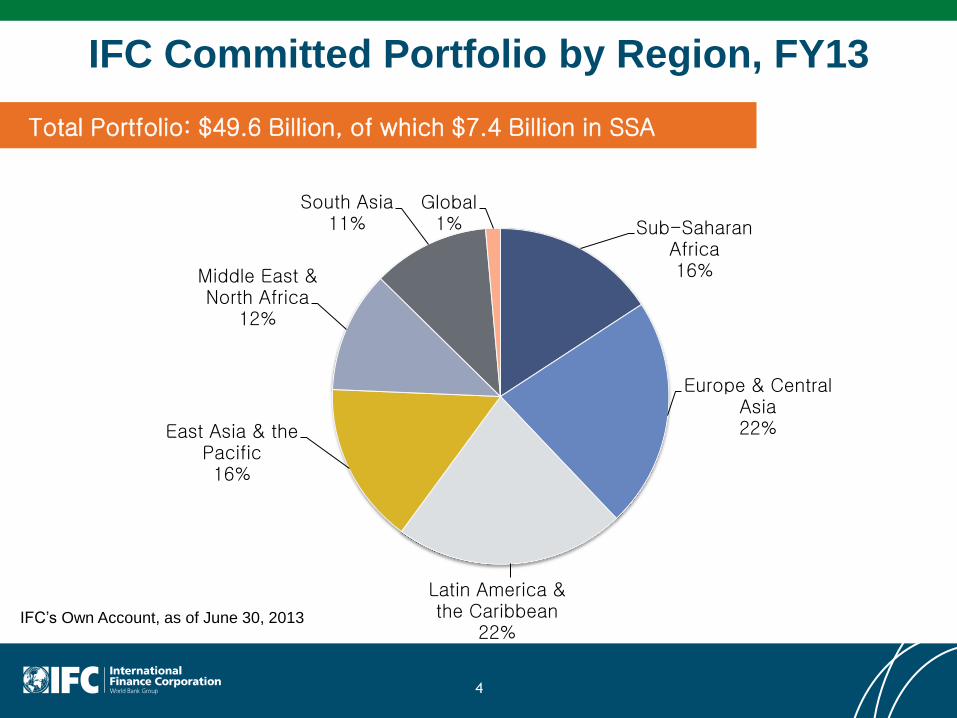

IFC Committed Portfolio by Region, FY13

4

Total Portfolio: $49.6 Billion, of which $7.4 Billion in SSA

Sub-Saharan Africa 16%

Europe & Central Asia 22%

Latin America & the Caribbean

22%

East Asia & the Pacific 16%

Middle East & North Africa

12%

South Asia 11%

Global 1%

IFC’s Own Account, as of June 30, 2013

IFC’s Three Businesses

IFC

Investment

Services

IFC

Advisory

Services

IFC Asset

Management

Company

Loans

Equity

Other forms of

financing

Resource

Mobilization

Advice

Problem-solving

Training

Wholly owned

subsidiary of IFC

Private equity fund

manager

Invests third-party

capital alongside IFC

5

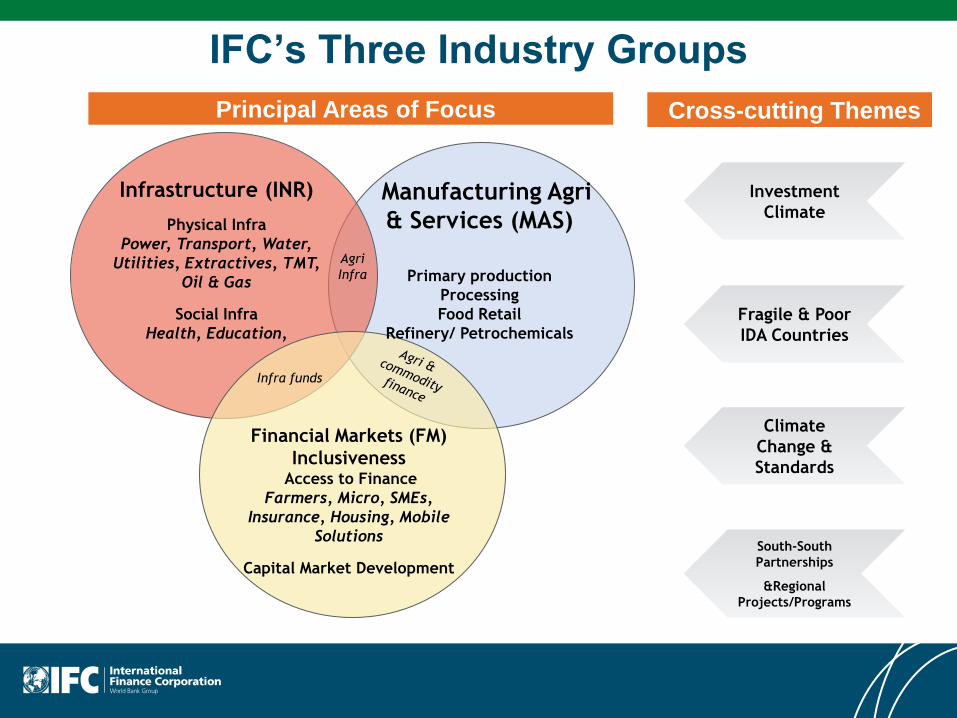

Infrastructure (INR)

Physical Infra

Power, Transport, Water,

Utilities, Extractives, TMT,

Oil & Gas

Social Infra

Health, Education,

Manufacturing Agri

& Services (MAS)

Primary production

Processing

Food Retail

Refinery/ Petrochemicals

Infra funds

Agri

Infra

Financial Markets (FM)

Inclusiveness Access to Finance

Farmers, Micro, SMEs,

Insurance, Housing, Mobile

Solutions

Capital Market Development

IFC’s Three Industry Groups

Fragile & Poor

IDA Countries

Climate

Change &

Standards

Investment

Climate

South-South

Partnerships

&Regional

Projects/Programs

Principal Areas of Focus Cross-cutting Themes

7

…with proximity to our clients

IFC Hub Offices

IFC Country Offices

ATLANTIC

OCEAN

Mediterranean

Sea

INDIAN

OCEAN

Johannesburg Maputo

Antananarivo

Lusaka

Freetown

Nairobi Kigali

Douala

N’Djamena

Lagos Accra

Ouagadougou

Abidjan

Dakar

Cairo Amman

Jerusalem Beirut

Algiers

Rabat

Sana’a

Dubai

Monrovia

Kinshasa

Addis Ababa

Dar es-Salaam

Bujumbura

Bamako

Bangui Juba

Tunis

Abuja

Conakry

Infra

A2F

AGRI/M&S

Africa Committed Portfolio

8

INR 35%

MAS 27%

FM 38%

IFC’s Own Account, as of June 30, 2013

Risk MGT 1%

Guaranty 12%

Loan 52% Quasi Equity

1%

Quasi Loan 12%

Equity 22%

Committed by Industry Group Committed by Product

Africa Committed Portfolio (cont’d)

9

IFC’s Own Account, as of June 30, 2013

Committed by Country (US$ m) 1

,46

1

1,3

34

90

0

84

9

70

2

22

0

19

1

18

2

16

7

13

2

12

5

11

3

10

8

10

3

96

75

72

62

62

54

42

39

36

28

27

25

24

23

22

20

19

15

13

11

8

6

5

5

3

3

3

1

0

0

0

200

400

600

800

1,000

1,200

1,400

1,600

Afr

ica

Reg

ion

Nig

eria

Sou

th A

fric

a

Gh

ana

Ken

ya

Uga

nd

a

Gu

inea

Co

te D

'Ivo

ire

Cam

ero

on

Mau

rita

nia

Togo

Mo

zam

biq

ue

Mau

riti

us

Tan

zan

ia

East

ern

Afr

ica

Reg

ion

Sen

egal

An

gola

Zam

bia

Wes

tern

Afr

ica

Reg

ion

Eth

iop

ia

Rw

and

a

Sou

ther

n A

fric

a R

egio

n

Mal

i

Ch

ad

Mad

agas

car

Mal

awi

Ben

in

Bo

tsw

ana

Bu

rkin

a Fa

so

Seyc

hel

les

Co

ngo

, Dem

ocr

atic

Rep

ub

lic o

f

Lib

eria

Cen

tral

Afr

ica

Reg

ion

Bu

run

di

Gam

bia

, Th

e

Nam

ibia

Sou

th S

ud

an

Sier

ra L

eon

e

Co

ngo

, Rep

ub

lic o

f

Cen

tral

Afr

ican

Rep

ub

lic

Swaz

ilan

d

Nig

er

Zim

bab

we

Sud

an

10

Opportunities

Strong macroeconomic trends set to continue…

11

2.6

2.2

5.5

5.2

5.7

0

1

2

3

4

5

6

Real Growth in GDP Annual Average % change

16.9

27.4

10.1 8.6

6.0

0

5

10

15

20

25

30

Inflation Annual Average % change

Robust growth Lower inflation FDI ex. RSA at new peak

9.2

12.2

10.1

12.0

13.9

21.6

26.8

29.4

26.6

33.1

34.0

0

5

10

15

20

25

30

35

40

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

FDI Inflows into SSA ex. RSA US$ billion

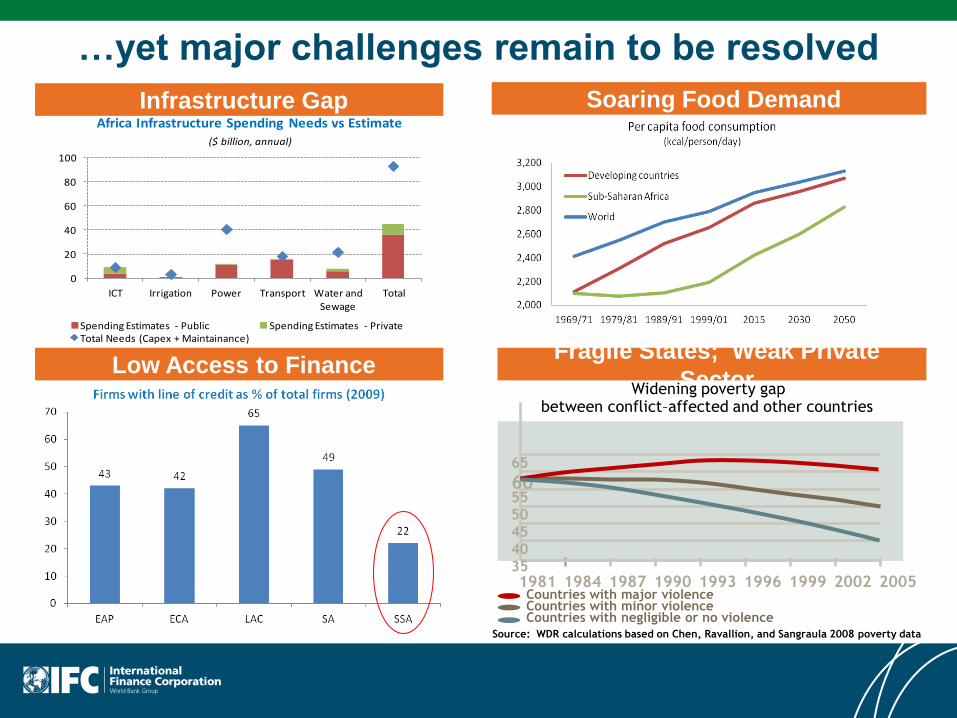

0

20

40

60

80

100

ICT Irrigation Power Transport Water and Sewage

Total

Africa Infrastructure Spending Needs vs Estimate($ billion, annual)

Spending Estimates - Public Spending Estimates - PrivateTotal Needs (Capex + Maintainance)

…yet major challenges remain to be resolved

Infrastructure Gap Soaring Food Demand

Low Access to Finance Fragile States; Weak Private

Sector

1981 1984 1987 1990 1993 1996 1999 2002 2005 35

60

40 45 50 55

65

Countries with major violence Countries with minor violence Countries with negligible or no violence

between conflict–affected and other countries Widening poverty gap

Source: WDR calculations based on Chen, Ravallion, and Sangraula 2008 poverty data

13

Track record

14

Some key clients By Sectors

Power

Renewable Energy Utilities and

Gas

Transport

vuelavuelavuelavuelavuelavuela

New Global Sponsors Expected to be Key Players

in Emerging Markets Power

15

Emerging markets countries are originating significant global players

Global Sponsor

Home

Country

Selected International Countries

of Operation Total Assets (US$bn)

China Laos, Nepal, Pakistan, Sudan,

Mozambique $62

Brazil Argentina, Nicaragua, Uruguay $64

Russia Armenia, Georgia, Kazakhstan, Lithuania,

Moldova, Turkey $16

China Brazil, Cambodia, Indonesia, Vietnam $375

India Indonesia, Mauritius, South Africa,

Vietnam1 $781

Source: Company filings and websites, GlobalData 1 Countries based on Tata Power operations. Total assets represent assets for Tata Group.

16

Our projects: a snapshot

Africa

•Mix of global sponsors and regional / local leading companies;

• Senior debt, subordinated debt and equity.

Senegal

Dakar Toll Road

A Loan: €10 million

C Loan: €11 million

Parallel loans: €40

million

Lender

November 2010

Equity: $800,000

Senegal

Shareholder

June 2011

Comasel Louga

A Loan: $125 million

Parallel loans: $220

million

Côte

d’Ivoire

Azito Phase 3

Lender

October 2012

Cameroon

A Loan:€64 million

Parallel loans: €70

million

Mandated Lead

Arranger

December 2011

KPDC

South Africa

Abengoa Khi Solar One

A Loan: $57 million

Parallel loans:$220

million

Blended Finance:$15

million

Mandated Lead

Arranger

November 2012

C Loan: $12 million

Kenya

KPLC

A Loan:$50 million

Lender

August 2012

Equity:$24 million

Kenya

Shareholder

April 2012

Kenya Airways

Kenya

Thika Power

A Loan: €28 million Parallel loans: €56

million

Lender

May 2012

Equity: $4 million

Rwanda

Lake Kivu IV

Shareholder

November 2009

Lender

March 2010

A loan $25 million

Corporate Loan

AKFED Aviation

Africa Region

Lome Container

Terminal

A Loan: €85 million

Parallel loans: €170

million

Lender

June 2011

Togo

A Loan:$25 million

Equity:$10 million

Uganda

Lender/Shareholder

June 2009

November 2012

Umeme Ltd

17

Case Study

18

Dakar-Diamniadio Toll Road

• A 30-year develop, build, finance and operate concession of a 25 km toll road from Dakar to Diamniadio

• Sponsor: Eiffage

• Total Project Cost: EUR230 m

• Closing: November 15, 2010

• IFC Role: Global Coordinator & lead financier

Tranche Product Amount Tenor

A Loan Senior Debt

IFC’s Account

EUR12.5

million

15 years

C Loan Subordinated Debt

IFC’s Account

EUR10 million 15 years

Parallel

loans

Senior loans EUR37.5

million

13.5-15

years

Co-financiers

Project Description

19

IFC Added Value

September/November 10 July 10 April 10 Feb 10

Board Approval

Financial Closure

Commitment

Credit Approval

Legal

Documentation

Appraisal

Negotiations Initial Discussion

Management

Committee Approval

Mandate Letter

1) ‘Making the Cash Flow Work’: (i) Long Tenor Senior Debt Tranche (15 years); and

(ii) 15-y Subordinated Loan with a 10-year grace period

2) Strengthening the Concession Contract

3) Dealing with traffic risk

4) Dealing with Environmental & Social Issues (≈ 30,000 people to relocate)

5) Identifying and fixing issues specific to the local context based on past experience

6) Creating a momentum, fixing issues and reaching closing under a tight time schedule

Completed in eight months door-to-door: a record for such a complex, first of its kind

deal

20

Contour Global Togo

•Project: a 100 MW tri-fuel (Heavy Fuel Oil/Gas/Diesel)

thermal power plant on a 25-year Build Own Operate

Transfer concession

• Total Project Cost: $190 million

• Closing: March 31, 2010

• IFC Role: subordinated lender and shareholder

•Co-financier: OPIC

• IFC’s Value Addition:

1) Engaging the Government of Togo on the broader Togolese electricity sector jointly with the World

Bank and other Development Finance Institutions

2) Leading structuring and negotiations

3) Making the cashflows work by providing a mix of equity and subordinated debt

Co-financier

Project Description

21

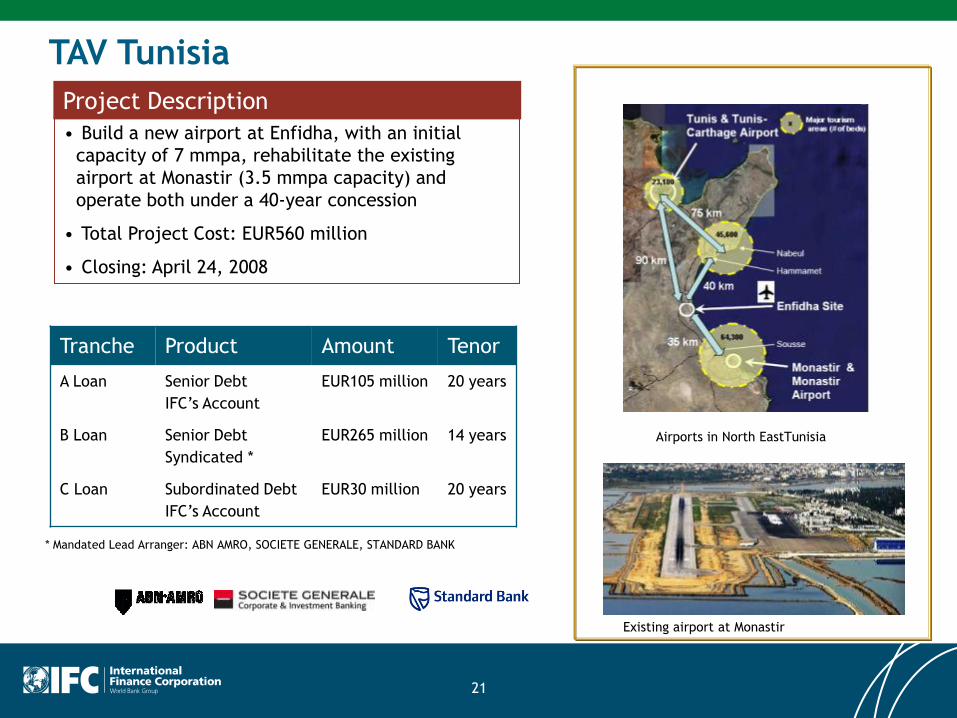

TAV Tunisia

Project Description

• Build a new airport at Enfidha, with an initial

capacity of 7 mmpa, rehabilitate the existing

airport at Monastir (3.5 mmpa capacity) and

operate both under a 40-year concession

• Total Project Cost: EUR560 million

• Closing: April 24, 2008

Existing airport at Monastir

Airports in North EastTunisia

Tranche Product Amount Tenor

A Loan Senior Debt

IFC’s Account

EUR105 million 20 years

B Loan Senior Debt

Syndicated *

EUR265 million 14 years

C Loan Subordinated Debt

IFC’s Account

EUR30 million 20 years

* Mandated Lead Arranger: ABN AMRO, SOCIETE GENERALE, STANDARD BANK

22

IFC Added Value

April – May 08 April 08 Mars 08 Feb 08

Financial Closure

Commitment and

First Disbursement

Legal

Documentation

IFC Board Approval

Appraisal

Negotiations

Credit Approval

Initial Discussion

Management

Committee Approval

Mandate Letter

1) ‘Making the Cash Flow Work’: (i) Very Long Senior Debt Tranche; and

(ii) Subordinated Loan with a 15-year grace period

2) Strengthening the Concession Contract

3) Mitigating country related/political risk

4) Creating a momentum, fixing issues and reaching closing under a tight time schedule

Completed in three months:

23

New Product that may be attractive to Korean Industrial

players

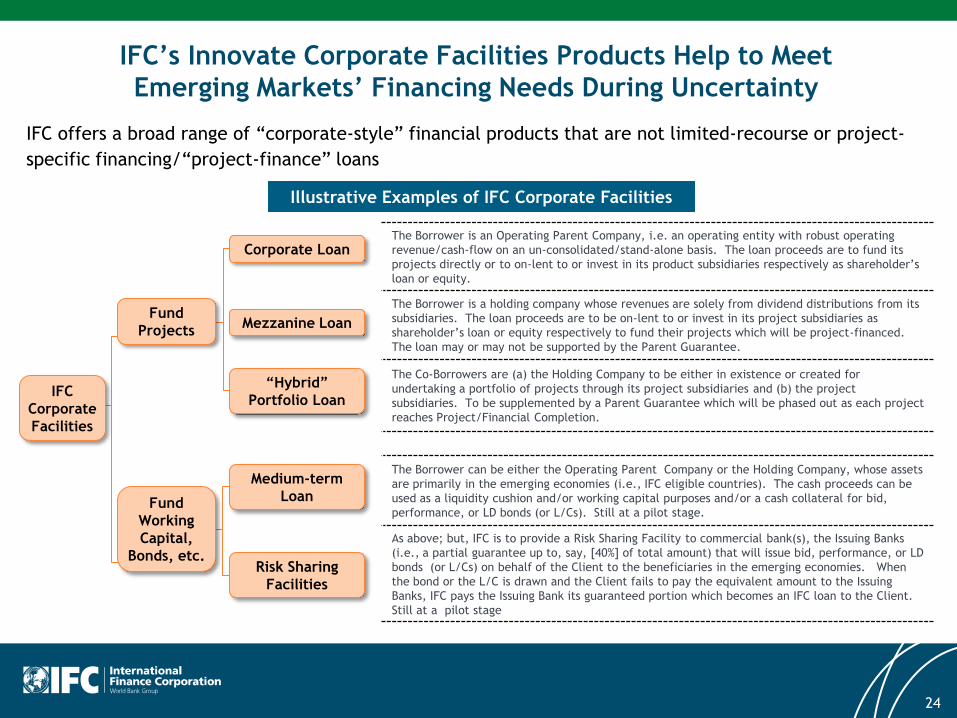

IFC’s Innovate Corporate Facilities Products Help to Meet

Emerging Markets’ Financing Needs During Uncertainty

IFC offers a broad range of “corporate-style” financial products that are not limited-recourse or project-

specific financing/“project-finance” loans

24

Illustrative Examples of IFC Corporate Facilities

The Borrower is an Operating Parent Company, i.e. an operating entity with robust operating

revenue/cash-flow on an un-consolidated/stand-alone basis. The loan proceeds are to fund its

projects directly or to on-lent to or invest in its product subsidiaries respectively as shareholder’s

loan or equity.

The Borrower is a holding company whose revenues are solely from dividend distributions from its

subsidiaries. The loan proceeds are to be on-lent to or invest in its project subsidiaries as

shareholder’s loan or equity respectively to fund their projects which will be project-financed.

The loan may or may not be supported by the Parent Guarantee.

The Co-Borrowers are (a) the Holding Company to be either in existence or created for

undertaking a portfolio of projects through its project subsidiaries and (b) the project

subsidiaries. To be supplemented by a Parent Guarantee which will be phased out as each project

reaches Project/Financial Completion.

The Borrower can be either the Operating Parent Company or the Holding Company, whose assets

are primarily in the emerging economies (i.e., IFC eligible countries). The cash proceeds can be

used as a liquidity cushion and/or working capital purposes and/or a cash collateral for bid,

performance, or LD bonds (or L/Cs). Still at a pilot stage.

As above; but, IFC is to provide a Risk Sharing Facility to commercial bank(s), the Issuing Banks

(i.e., a partial guarantee up to, say, [40%] of total amount) that will issue bid, performance, or LD

bonds (or L/Cs) on behalf of the Client to the beneficiaries in the emerging economies. When

the bond or the L/C is drawn and the Client fails to pay the equivalent amount to the Issuing

Banks, IFC pays the Issuing Bank its guaranteed portion which becomes an IFC loan to the Client.

Still at a pilot stage

IFC

Corporate

Facilities

Fund

Working

Capital,

Bonds, etc.

Fund

Projects

Corporate Loan

Mezzanine Loan

“Hybrid”

Portfolio Loan

Medium-term

Loan

Risk Sharing

Facilities