ieej © 20 20 , all rights reserved · reference 17.3 23.1 29.1 12.8 15.7 18.7 21.7 0 10 20 30 40...

TRANSCRIPT

1

IEEJ © 2020, All rights reserved

2

IEEJ © 2020, All rights reserved

Ken Koyama, IEEJ, February 19th 2020

Energy consumption Changes (2017-2050)

Reference Scenario

0

1,000

2,000

3,000

4,000

5,000

1980 1990 2000 2010 2020 2030 2040 2050

Mtoe

Industry

Transport

Buildings, etc.

Non-energy use

Gen. & trans. losses

Other transf.

387

500

868

892

1,058

1,079

0.9%

1.4%

0.8%

0.7%

1.0%

0.9%

Other transf.

Non-energy use

Industry

Buildings, etc.

Transport

Gen. & trans. losses

Mtoe CAGR

Source: “IEEJ Outlook 2020” (IEEJ, October 2019)

Outlook for World Final Energy DemandTransportation sector is an important source for the growth

3

IEEJ © 2020, All rights reserved

Ken Koyama, IEEJ, February 19th 2020

By region By sector

0

20

40

60

80

100

120

140

1980 1990 2000 2017 2030 2040 2050

Mb/d

Intl. bunkers

Oceania

Africa

Oth. Europe/Eurasia

Advanced Europe

Middle East

Asia

Latin America

North America

64 67

76

92

104

112118

0

20

40

60

80

100

120

140

1980 1990 2000 2017 2030 2040 2050

Mb/d

Transformation

Non-energy use

Buildings, etc.

Transport

Industry

Source: “IEEJ Outlook 2020” (IEEJ, October 2019)

Outlook for World Oil Demand by region/sectorAsia and Transportation drives the growth

Reference Scenario

4

IEEJ © 2020, All rights reserved

Ken Koyama, IEEJ, February 19th 2020

StockNew sales

96%

63%

43%38%

14%

22%

25% 36%

31%

8%

14%

13%

20%

6%

17%12%

34%

0%

20%

40%

60%

80%

100%

2017 2030 2050 2030 2050

Reference ATS

Fuel cell vehicle

Battery electric

vehicle

Plug-in hybrid

vehicle

Hybrid vehicle

Natural gas

vehicle

Conventional

engine vehicle

97%

78%

49%

64%

20%

13%

25%

23%

35%

4%

12%

7%

18%

3%13%

5%

26%

2017 2030 2050 2030 2050

Reference ATS

Advanced Technologies Scenario

Source: “IEEJ Outlook 2020” (IEEJ, October 2019)

Outlook for World Share of Passenger VehicleATS sees 80% plus ZEVs in 2050

5

IEEJ © 2020, All rights reserved

Ken Koyama, IEEJ, February 19th 2020

New sale-basis Stock-basis

Fuel efficiency of passenger vehicle

Note: Litres of gasoline equivalent

21.8

27.8

33.8

14.1

17.9

21.0

23.9

0

10

20

30

40

2017 2030 2040 2050

km/L

Advanced

Technologies

Reference

17.3

23.1

29.1

12.8

15.7

18.7

21.7

0

10

20

30

40

2017 2030 2040 2050

km/L

Advanced

Technologies

Reference

Source: “IEEJ Outlook 2020” (IEEJ, October 2019)

Outlook for World Fuel Efficiency of Passenger VehicleATS sees 34% improvement of fuel efficiency (stock base) in 2050

Advanced Technologies Scenario

6

IEEJ © 2020, All rights reserved

Ken Koyama, IEEJ, February 19th 2020

By region By energy source

Note: Solid lines stand for Advanced Technologies Scenario anddotted lines stand for Reference Scenario.

Source: “IEEJ Outlook 2020” (IEEJ, October 2019)

Advanced Technologies Scenario

Outlook for World Primary Energy DemandATS sees “Oil Demand Peak” and other important change in energy mix

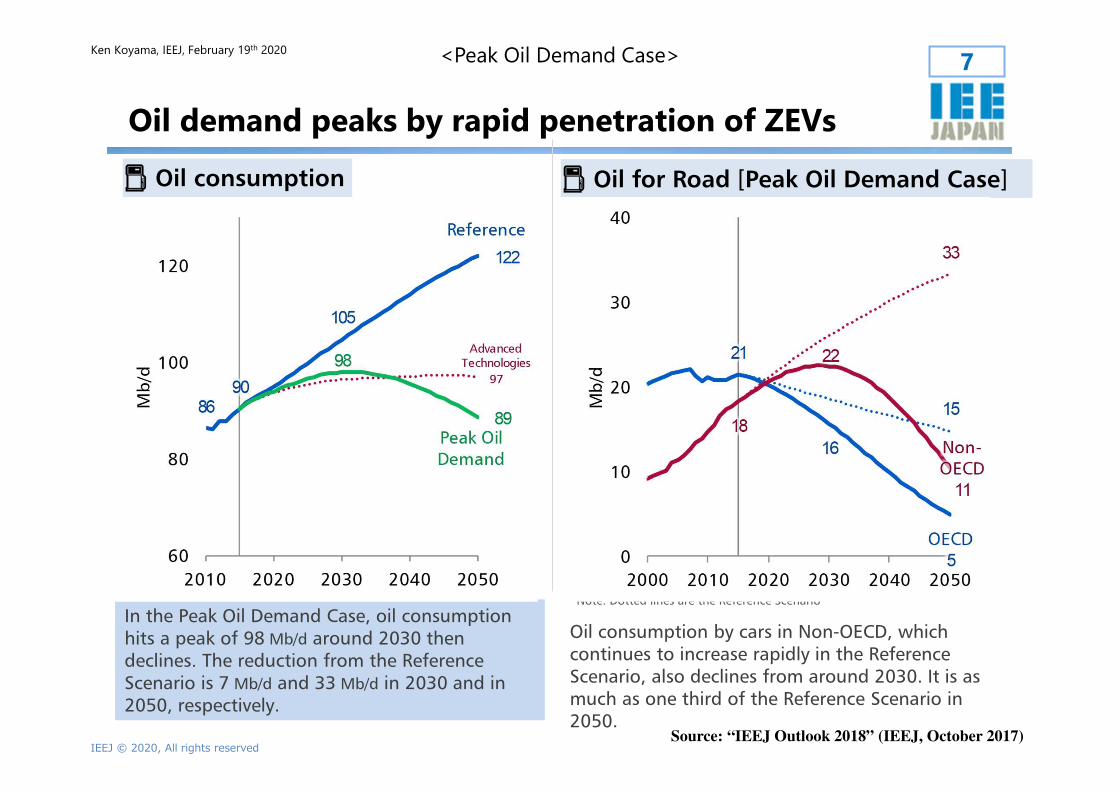

7

IEEJ © 2020, All rights reserved

Ken Koyama, IEEJ, February 19th 2020

Oil demand peaks by rapid penetration of ZEVs

Oil consumption by cars in Non-OECD, which continues to increase rapidly in the Reference Scenario, also declines from around 2030. It is as much as one third of the Reference Scenario in 2050.

⛽ Oil consumption ⛽ Oil for Road [Peak Oil Demand Case]

In the Peak Oil Demand Case, oil consumption hits a peak of 98 Mb/d around 2030 then declines. The reduction from the Reference Scenario is 7 Mb/d and 33 Mb/d in 2030 and in 2050, respectively.

Note: Dotted lines are the Reference Scenario

<Peak Oil Demand Case>

Source: “IEEJ Outlook 2018” (IEEJ, October 2017)

8

IEEJ © 2020, All rights reserved

Ken Koyama, IEEJ, February 19th 2020

Economic impacts of peak oil demand

Although the Middle East obtains the relative gain, its net oil export decreases of $1.6 trillion or 13% of nominal GDP is significant.

On the other hand, the most benefiting country from net oil import decreases is India, the second largest oil consumer, followed by China, which has more car fleet than in any other countries. The United States has little impact despite of its consumption scale since it is almost oil self-sufficient.

⛽ Changes in net oil exports/imports and ratios to nominal GDP [2050]

Note: Europe excludes the former Soviet Union

<Peak Oil-Demand Analysis>

Source: “IEEJ Outlook 2018” (IEEJ, October 2017)

9

IEEJ © 2020, All rights reserved

Ken Koyama, IEEJ, February 19th 2020

Reference material

10

IEEJ © 2020, All rights reserved

Ken Koyama, IEEJ, February 19th 2020

By sector By energy source

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1980 1990 2000 2017 2030 2040 2050

Mtoe

Non-energy use

Buildings, etc.

Transport

Industry

5,369

6,264

7,030

9,717

11,420

12,39213,035

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1980 1990 2000 2017 2030 2040 2050

Mtoe

Others

Electricity

Natural gas

Oil

Coal

Source: “IEEJ Outlook 2020” (IEEJ, October 2019)

Outlook for World Final Energy Demand by sector/energyTransportation/oil is an important source for the growth

Reference material

Reference Scenario

11

IEEJ © 2020, All rights reserved

Ken Koyama, IEEJ, February 19th 2020

By energy sourceBy sector

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1980 1990 2000 2017 2030 2040 2050

Mtoe

Non-energy use

Buildings, etc.

Transport

Industry

1,133

1,554

1,992

3,793

4,828

5,369

5,751

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1980 1990 2000 2017 2030 2040 2050

Mtoe

Others

Electricity

Natural gas

Oil

Coal

Source: “IEEJ Outlook 2020” (IEEJ, October 2019)

Outlook for Asian Final Energy Demand by sector/energyTransportation/oil is an important source for the growth

Reference material

Reference Scenario

12

IEEJ © 2020, All rights reserved

Ken Koyama, IEEJ, February 19th 2020

Outlook for Asian Oil demand by country/sectorTransportation in emerging Asia drives the growth

By region By sector

0

10

20

30

40

50

1980 1990 2000 2017 2030 2040 2050

Mb/d

Others

Korea

Japan

ASEAN

India

China

10

13

19

29

38

43

48

0

10

20

30

40

50

1980 1990 2000 2017 2030 2040 2050

Mb/d

Transformation

Non-energy use

Buildings, etc.

Transport

Industry

Source: “IEEJ Outlook 2020” (IEEJ, October 2019)

Reference material

Reference Scenario