ie 475 advanced manufacturing costing techniques lecture notes #2 cost concepts

TRANSCRIPT

IE 475

Advanced Manufacturing Costing Techniques

Lecture Notes #2

Cost Concepts

2

Module Learning Objectives

After completing this module, IE 475 students should be able to: Understand the strategic role of basic cost concepts Explain the cost driver concepts at the activity, volume,

structural, and executional levels Explain the cost concepts used in product and service

costing Demonstrate how costs flow through the accounts Prepare an income statement for both a manufacturing firm

and a merchandising firm Explain the cost concepts related to the use of cost

information in planning and decision making

3

Basic Definitions

A cost is

incurred when aresource is used for

some purpose

A cost isincurred when a

resource is used forsome purpose

Costs may be collected intogroups called cost pools

Costs may be collected intogroups called cost pools

A cost object is any product, service, or unit towhich costs are assigned forsome management purpose.

A cost object is any product, service, or unit towhich costs are assigned forsome management purpose.

4

Basic Definitions (cont.)

Cost assignment Process of assigning costs to cost pools or from cost

pools to cost objects Direct cost

Can be conveniently and economically traced directly to a cost pool or a cost object

Indirect cost Has no convenient or economical way to be traced

from the cost to the cost pool or from the cost pool to the cost object

5

Basic Definitions (cont.)

Cost allocation Assignment of indirect costs to cost pools and cost

objects Allocation bases

Cost drivers used to allocate costs

6

Costs, Cost Pools, CostObjects, and Cost Drivers

Electric Motor

Materials Handling

Supervision

PackingMaterials

AssemblyAssembly

PackingPacking

Dishwasher

Washing Machine

FinalInspection

7

Costs, Cost Pools, CostObjects, and Cost Drivers (cont.)

8

Direct Materials

Direct materials include The cost of materials in the product

Less purchase discounts but including freight and related charges

Reasonable allowance for scrap and defective units

+ FLOURFLOUR+MILKMILKSUGARSUGAR =

9

Indirect Materials

Materials used in manufacturing that are not physically part of the finished product

Sweeping

CompoundCleaning

Material

10

Direct and Indirect Labor Costs

Direct labor Includes the labor used to manufacture the product or

to provide the serviceIndirect labor

Includes supervision, quality control, inspection, purchasing and receiving, and other manufacturing support costs

11

Other Indirect Costs Other indirect costs such

as building and equipment depreciation,property taxes, insurance, and utilities . . . .

. . . . are combined with indirectlabor and indirect materials into

a single cost pool called . . . .

FactoryFactoryOverheadOverheadFactoryFactory

OverheadOverhead

12

Prime Cost and Conversion Cost

Manufacturing costs are oftencombined as follows:

DirectMaterials

DirectMaterials

DirectLaborDirectLabor

FactoryOverheadFactory

Overhead

13

Identifying Cost Drivers

A critical first step in achieving a competitive advantage is to identify the key cost drivers in the firm or organization

What is a cost driver? Any factor that has the effect of changing the level of

total cost Examples

14

Cost Drivers

Cost drivers play two major roles in cost management: Enable the assignment of costs to cost objects Explain cost behavior

The four types of cost drivers are: Activity-based Volume-based Structural Executional

15

Types of Cost Drivers Activity-basedActivity-based

Volume-basedVolume-based

StructuralStructural

ExecutionalExecutional

Identified using activity analysis, a detailed description of specific

activities performed inthe firm’s operations.

Relationship between costs andvolume measures such as unitsproduced, direct labor hours,or quantity of materials used.

16

Activity-based Cost Drivers

Pennsylvania Blue Shield

17

Volume-based Cost Drivers

Many cost drivers are volume-based

The cost driver is the amount produced or the quantity of service provided The more you produce, the more cost you incur

An important concept associated with volume-based cost drivers is that of the relevant range

18

Volume-based Cost Drivers (cont.)

The relevant range is the range of the cost driver in which the actual value of the cost driver is

expected to fall, and for which the relationship is assumed to be

approximately linear

Volume-based Cost Drivers (cont.)

19

20

Volume-based Cost Drivers (cont.)

Linear Approximation for Actual Cost Behavior

21

Volume-based Cost Drivers (cont.)

Total Variable Cost

$6,600

$6,500

$3,000

3,500 3,600Units of the Cost Driver

Total Cost

Variable cost is the change in totalcost associated with each change in the

quantity of the cost driver

Total CostTotal Cost

22

Volume-based Cost Drivers (cont.)

$6,600

$6,500

$3,000

3,500 3,600Units of the Cost Driver

Total Cost

Total Fixed Cost

Fixed cost is the portion ofthe total cost that does not

change with a change in the quantity of the cost driver,within the relevant range.

Fixed cost is the portion ofthe total cost that does not

change with a change in the quantity of the cost driver,within the relevant range.

23

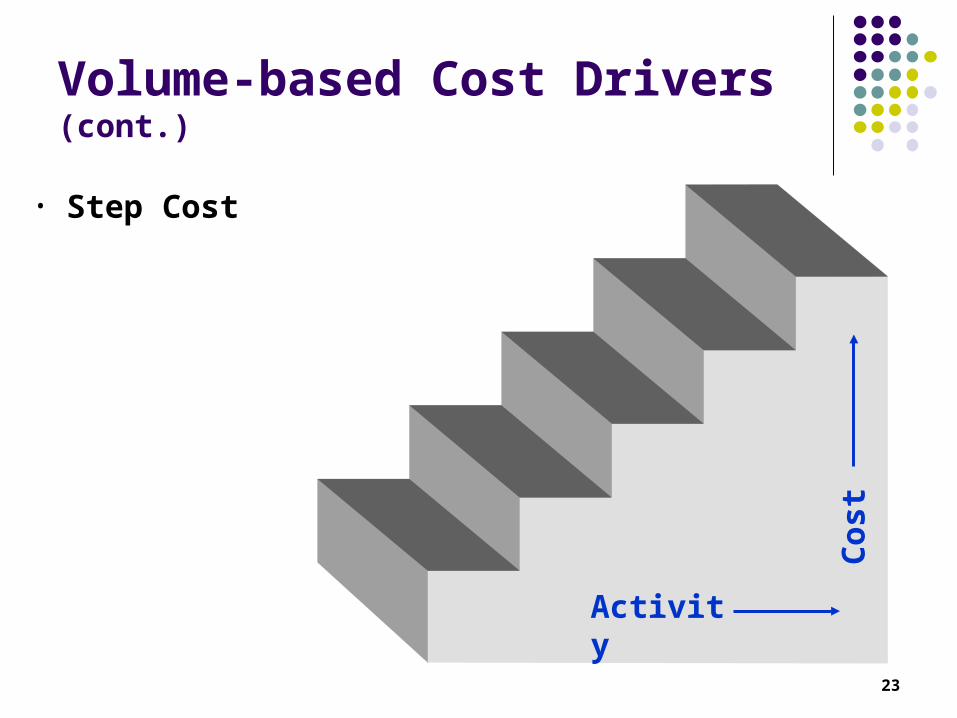

Volume-based Cost Drivers (cont.)

Activity

Co

st

• Step Cost

24

Volume-based Cost Drivers (cont.)

Unit Cost (or average cost) Total manufacturing cost (materials, labor, and overhead) divided

by units of output Useful concept in setting prices and in evaluating product

profitability

Marginal cost Additional cost incurred as the cost driver increases by one unit

Used interchangeably with differential cost or incremental cost Under the assumption of linear cost within the relevant range, the

concept of marginal cost is equivalent to the concept of unit variable cost

Materials: Each unit of final product requires: Mat 1 20 $/unit 2 units of mat 1 Mat 2 10 $/unit 1 unit of mat 2 Mat 3 20 $/unit 3 units of mat 3Labor: 10 $/hr 3 hrs of laborOverhead: Rent 500 $/year Security 100 $/year Electricity 80 $/year Water 60 $/year

Units of Output

Variable Cost

Fixed Cost

Avg Unit Var Cost

Avg Unit Fixed Cost

Avg Unit Cost

0 $0 $0 $0.00 $0.00 $0.001 $140 $740 $140.00 $740.00 $880.002 $280 $740 $140.00 $370.00 $510.003 $420 $740 $140.00 $246.67 $386.674 $560 $740 $140.00 $185.00 $325.005 $700 $740 $140.00 $148.00 $288.006 $840 $740 $140.00 $123.33 $263.337 $980 $740 $140.00 $105.71 $245.718 $1,120 $740 $140.00 $92.50 $232.509 $1,260 $740 $140.00 $82.22 $222.22

10 $1,400 $740 $140.00 $74.00 $214.0011 $1,540 $740 $140.00 $67.27 $207.2712 $1,680 $740 $140.00 $61.67 $201.6713 $1,820 $740 $140.00 $56.92 $196.9214 $1,960 $740 $140.00 $52.86 $192.8615 $2,100 $740 $140.00 $49.33 $189.3316 $2,240 $740 $140.00 $46.25 $186.2517 $2,380 $740 $140.00 $43.53 $183.5318 $2,520 $740 $140.00 $41.11 $181.1119 $2,660 $740 $140.00 $38.95 $178.9520 $2,800 $740 $140.00 $37.00 $177.00

25

Volume-based Cost Drivers (cont.)

Unit Cost (or average cost)

Illustration ofAverage Costs per Unit

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

Ave

rag

e C

ost

Units of Output

Illustration ofAverage Costs per Unit

Avg Unit Var Cost

Avg Unit Fixed Cost

Avg Unit Cost

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

Ave

rag

e C

ost

Units of Output

Illustration ofAverage Costs per Unit

Avg Unit Var Cost

Avg Unit Fixed Cost

Avg Unit Cost

26

Types of Cost Drivers

Activity-basedActivity-based

Volume-basedVolume-based

StructuralStructural

ExecutionalExecutional

Involves strategic plans and decisions: Scale Experience Technology Complexity

Short-term operational decisions: Workforce involvement Production process design Supplier relationships

27

Structural Cost Drivers

Scale How much should be invested?

Experience How much prior experience does the firm have in its

current and planned products and services? Technology

What process technologies are used in manufacturing, and in distributing the product or service?

Complexity What is the firm’s level of complexity?

28

Executional Cost Drivers

Workforce involvement Are the employees dedicated to continual

improvement and quality? Design of the production process

Can the layout of equipment and processes and the scheduling of production be improved?

Supplier relationships Can the cost, quality, or delivery of materials and

purchased parts be improved to reduce overall costs?

29

Value Chain of Product Costs

Product inventory for both manufacturing and merchandising firms is treated as an asset on their balance sheets

So long as the inventory has market value, it is considered an asset until the inventory is sold

Cost of goods sold Cost of the product transferred to the income

statement when inventory is sold

30

Product Costs

Product costs for a manufacturing firm include only the costs necessary to complete the product

31

Period Costs

Period costs are all non-product expenditures for managing the firm and selling the product Period costs are expenses because there is no expectation

that they will produce future value Include primarily the general, selling, and administrative

costs necessary for the management of the company but are not involved directly or indirectly in the manufacturing process

Sometimes referred to as operating expenses or selling and administrative expenses

32

Manufacturing, Merchandising, and Service CostingThree Inventory Accounts

Materials inventory Keeps the cost of the supply of materials used in the

manufacturing process or to provide the service Work-in-Process inventory

Contains all costs put into the manufacture of products that are started but not complete at the financial statement date

Finished goods inventory Holds the cost of goods that are ready for sale

33

Inventory Formula

BeginningInventoryBalance

CostAdded

CostTransferred

Out

EndingInventoryBalance

+ +=

34

Cost Flows in Manufacturing and Merchandising Firms

35

Income Statement for a Manufacturing Firm

Manufacturing firms require a two-part calculation for Cost of Goods Sold

The first part combines the cost flows affecting the Work-in-Process Inventory account to determine the amount of Cost of Goods Manufactured Cost of Goods Manufactured is the cost of goods

finished and transferred out of the Work-in-Process Inventory account this period

The second part combines the cost flows for the Finished Goods Inventory account to determine the amount of the cost of the goods sold and net income

36

Statements for Manufacturing and Merchandising Firms

37

Cost Concepts for Planning andDecision Making

Relevant Cost This concept arises when the decision maker must

choose between two or more options Must determine which option offers the highest benefit

($) A relevant cost has the following two properties:

38

Opportunity Cost

Opportunity Cost is the benefit lost when choosing one option precludes receiving the benefits from an alternative option

Example: If you werenot attending college, andyou could be earning$18,000 per year, then youropportunity cost of attendingcollege for one year is $18,000.

39

Sunk Costs

Sunk costs are costs that have been incurred or committed in the past and are therefore irrelevant

Example: You bought an automobile that cost$10,000 two years ago. The $10,000 cost is sunk because whether you drive it, park it, trade it, or sell it, you cannot change the $10,000 cost.

40

Attributes of Cost Informationfor Decision Making

AccuracyAccuracy TimelinessTimeliness

Costand Value

Costand Value