ibf - updates - 2007 (q1 & q2 v1.0)

DESCRIPTION

The following 55+ pages represent a summary of relevant information from the first and second quarter of 2007.TRANSCRIPT

Copyright © 2007 by Institute of Business and Finance. All rights reserved. v1.0

INSTITUTE OF BUSINESS & FINANCE

QUARTERLY

UPDATES

2007 Q1 & Q2

Quarterly Updates

Table of Contents

MUTUAL FUNDS

DISTURBING RETURN FIGURES 1.1

YEAR-END WINDOW DRESSING 1.1

PICKING THE NEXT TOP PERFORMERS 1.2

A RANDOM WALK 1.2

LARGEST FUND COMPANIES 1.4

CORRELATIONS TO THE S&P 500 REVISITED 1.5

STYLE BOXES 1.6

FOCUSED FUNDS AND RISK 1.7

LIFECYCLE FUNDS 1.8

TARGET-DATE FUNDS EXPAND 1.8

MORE AGGRESSIVE LIFE CYCLE FUNDS 1.9

LONG-SHORT FUNDS 1.10

DIVERSIFICATION BENEFITS 1.10

FREQUENCY OF PORTFOLIO REBALANCING 1.12

VALUE LINE HYPE 1.12

ODDS OF BEATING AN INDEX 1.13

MIXED PERFORMANCE RANKINGS 1.15

ACTIVE VS. PASSIVE MANAGEMENT 1.16

SIDE-BY-SIDE MANAGEMENT 1.17

MANAGER-INVESTED MUTUAL FUNDS 1.19

B SHARES REVIEWED BY SEC 1.25

SHAREHOLDER PROXY VOTING 1.26

SECURITIES LENDING PRACTICES 1.27

FUND DIRECTOR PAY 1.28

DIRECTORS AND 12B-1 FEES 1.28

STOCKS AND MUTUAL FUNDS 1.29

ETFS

ETF UPDATE 2.1

THE LARGEST ETFS 2.4

ETFS WITH LOW EXPENSE RATIOS 2.5

ETF PRICE DISPARITIES 2.6

SECTOR VOLATILITY 2.7

BUYING AND SELLING ETFS 2.8

UITS AND CLOSED-END FUNDS

UIT AND NEW FUND CRITICISM 3.1

CLOSED-END FUND ASSET INCREASE 3.1

CLOSED-END COVERED CALL FUNDS 3.2

REITS

REIT UPDATE 4.1

INTERNATIONAL REITS 4.2

STOCKS

DOW MILESTONES 5.1

DOW DROPS 5.2

S&P 500 AND DJIA RETURNS 5.3

SMALL CAP STOCKS 5.4

QUALIFYING DIVIDENDS 5.4

BUFFET WARNING 5.4

DIVIDEND-PAYING BONUS 5.5

VALUE PLAY 5.5

VALUE VS. GROWTH STOCKS

ROLLING PERIODS: GROWTH VS. VALUE 6.1

REVISITING GROWTH AND VALUE 6.2

SMALL CAP VALUE 6.7

GROWTH VS. VALUE 6.8

2006 INDEX RETURNS 6.9

BONDS

CUSHION AGAINST STOCK DECLINES 7.1

STOCKS VS. BONDS 7.1

2006 HIGH-YIELD BOND FACTS 7.2

BOND MARKETS, INDEXES, AND FUNDS 7.3

GLOBAL INVESTING

WORLD’S FINANCIAL ASSETS 8.1

EMERGING MARKET DEBT 8.2

2006 GLOBAL INDEX RETURNS 8.2

REDUCED GLOBAL CORRELATION 8.3

EAFE COMPOSITION 8.4

GLOBAL SMALL CAP BENEFITS 8.6

DOMESTIC GLOBAL DIVERSIFICATION 8.7

COVERED CALL WRITING

SPDRS AND COVERED CALL WRITING 9.1

EQUITY-INDEXED ANNUITIES

EQUITY-INDEXED ANNUITIES (EIAS) 10.1

FINANCIAL PLANNING

OPTIMAL REBALANCING 11.1

PREDICTED MARKET MELTDOWN 11.4

DISTRIBUTION OF RETURNS 11.5

INVESTING IN A HOUSE 11.6

AMERICA THE BANKRUPT? 11.7

CPI SPENDING CATEGORIES 11.7

GOLD VS. HERSHEY BARS 11.9

HEDGE FUND DISASTERS 11.10

HEDGE FUND WARNING 11.11

CALCULATING A LUMP SUM 11.11

ENDING UP WITH $1,000,000 11.12

GOALS AND RISK TOLERANCE TEST 11.12

RETIREMENT PLANNING

RECONSIDERING THE ROTH 401(K) 12.1

HEALTH SAVINGS PLANS 12.2

529 PLANS 12.3

RETIREMENT PLAN INCREASES FOR 2007 12.3

RETIREMENT REALITY 12.7

BENEFITS OF PATIENCE 12.8

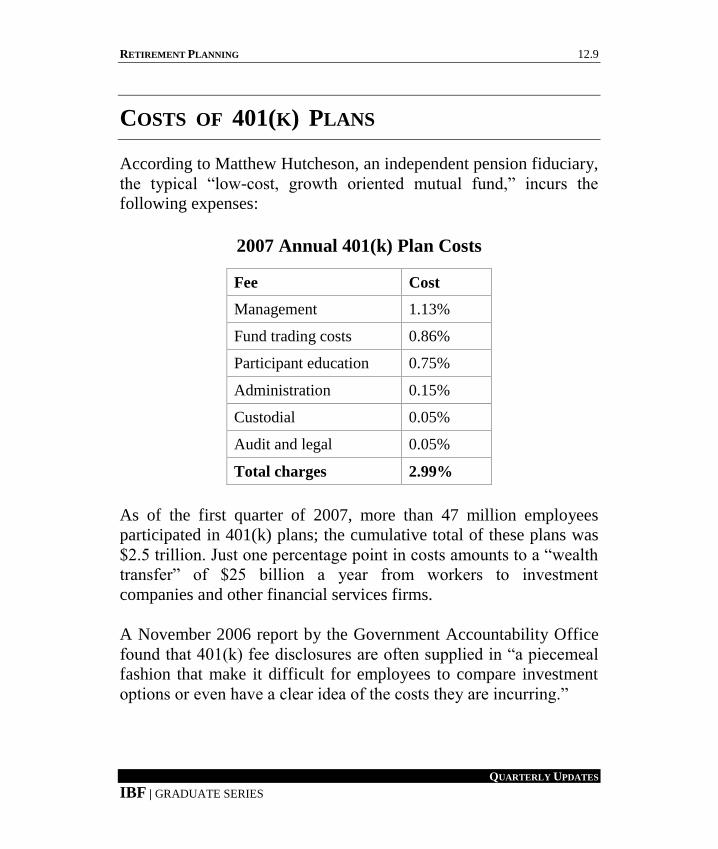

COSTS OF 401(K) PLANS 12.9

RETIREMENT STATISTICS 12.10

MAXIMUM SOCIAL SECURITY BENEFIT 12.10

PEOPLE WORKING LONGER 12.11

INFLATION MEASUREMENTS 12.11

LONG-TERM CARE PARTNERSHIP 12.15

DISCLOSURE PROTECTION FOR ORGAN DONORS 12.17

FULLY FUNDED PENSION PLANS 12.18

NEW MEDICAID RULES 12.18

TAXES

2007 TAX BREAKS 13.1

TAX DOCUMENTS 13.2

FREE TAX PREPARATION AND FILING 13.3

TAX FACTS 13.3

APPEAL TO CHILDREN 13.5

FEDERAL RESERVE COMIC BOOKS 13.6

YOUNG INVESTORS 13.6

QUARTERLY

UPDATES

MUTUAL FUNDS

MUTUAL FUNDS 1.1

QUARTERLY UPDATES

IBF | GRADUATE SERIES

1.DISTURBING RETURN FIGURES

According to DALBAR, the average equity mutual fund investor

experienced annualized returns of just 3.9% over the 20-year period

ending December 31st, 2005. During this same period, inflation

averaged 3% a year, while a buy-and-hold investment in the S&P

500 returned 11.9% a year.

YEAR-END WINDOW DRESSING

For roughly the last week or two of the year, many mutual and hedge

fund managers sell off poorly performing securities and replace them

with the quarter’s best performers. Over the past 16 years, the S&P

500’s top-performing stocks of the first 11 weeks or so of the fourth

quarter have outperformed the overall index by an average of 2.6%

in the final week; this strategy has worked every year.

The Thomson Financial study suggests the efficiency comes from

buying all of the top 50 performers and then selling them just before

the first trading day of the next year. Another strategy worth

considering is to buy stocks that are among the market’s worst 10%

performers. Over the past 16 years, these stocks have beaten the

S&P 500 by 1.8% in the first week of the new year (vs. 0.7% for the

top-performing stocks).

1.2 MUTUAL FUNDS

QUARTERLY UPDATES

IBF | GRADUATE SERIES

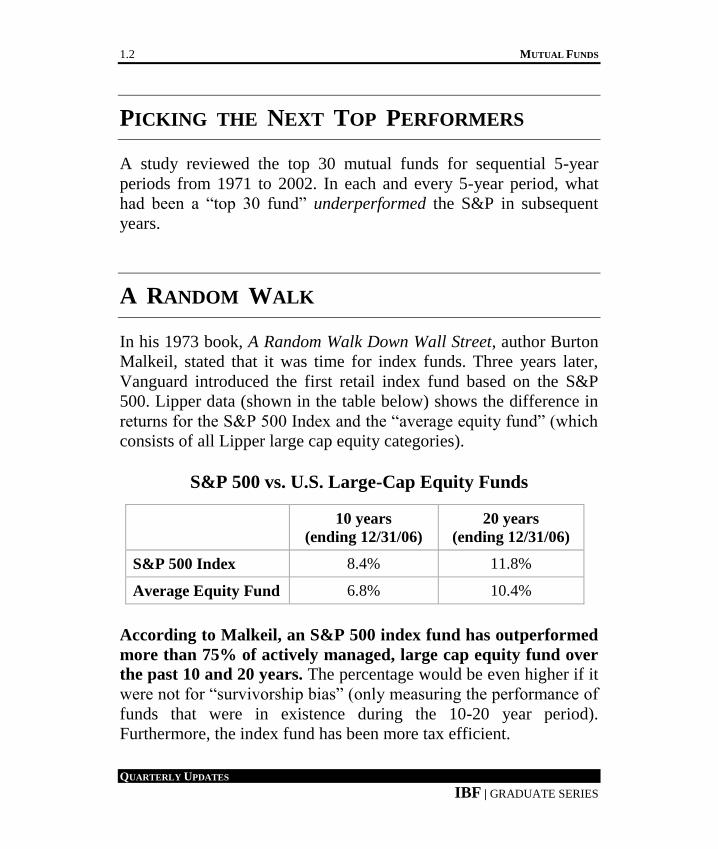

PICKING THE NEXT TOP PERFORMERS

A study reviewed the top 30 mutual funds for sequential 5-year

periods from 1971 to 2002. In each and every 5-year period, what

had been a “top 30 fund” underperformed the S&P in subsequent

years.

A RANDOM WALK

In his 1973 book, A Random Walk Down Wall Street, author Burton

Malkeil, stated that it was time for index funds. Three years later,

Vanguard introduced the first retail index fund based on the S&P

500. Lipper data (shown in the table below) shows the difference in

returns for the S&P 500 Index and the “average equity fund” (which

consists of all Lipper large cap equity categories).

S&P 500 vs. U.S. Large-Cap Equity Funds

10 years

(ending 12/31/06)

20 years

(ending 12/31/06)

S&P 500 Index 8.4% 11.8%

Average Equity Fund 6.8% 10.4%

According to Malkeil, an S&P 500 index fund has outperformed

more than 75% of actively managed, large cap equity fund over

the past 10 and 20 years. The percentage would be even higher if it

were not for “survivorship bias” (only measuring the performance of

funds that were in existence during the 10-20 year period).

Furthermore, the index fund has been more tax efficient.

MUTUAL FUNDS 1.3

QUARTERLY UPDATES

IBF | GRADUATE SERIES

In 1970 there were 355 equity funds, only 117 were still in

existence at the end of 2006. Of the surviving 117 funds, 57

underperformed the S&P 500, 38 had equivalent returns, and 22

outperformed the index. Looking at the funds that either closely

matched or outperformed the S&P 500, 27 outperformed the index

by 0-1%, 16 by 1%, two by 2%, one by 3%, and one by 4%.

Malkeil acknowledges that the Fundamental Index has done well

during the early 2000s, but that such performance has been due to

the fundamental index’s bias toward value and small cap. The author

further points out that there have certainly been times when “the

market makes mistakes—it goes crazy sometimes.” As an example,

at the height of the market bubble in 2000, Cisco represented 4% of

the S&P 500, yet it represented just 0.02% of the economy. In 1999,

Amazon had a market value over $30 billion, even though it had yet

to ever make a profit. In fact, its losses for 1999 were over $600

million. At its height, technology stocks represented a third of

the S&P 500 (according to TheStreet.com, telecom and technology

combined represented 45% of the S&P 500 as of March 2000).

According to Malkeil, “My argument for indexing was based on my

belief that our equity markets are remarkably efficient. When

information arises about the stock market or individual stocks, that

information gets reflected without delay—switching from stock to

stock in an attempt to provide superior performance—is unlikely to

be effective, especially when you add in trading costs and taxes.”

1.4 MUTUAL FUNDS

QUARTERLY UPDATES

IBF | GRADUATE SERIES

LARGEST FUND COMPANIES

According to Lipper, the 30 largest mutual fund families manage

more than 75% of the industry’s assets; the top 10 companies

control 47% and the biggest 60 oversee nearly 91% of all mutual

fund assets. The table below shows the top 10 fund companies, as of

the end of the third quarter 2006 (note: “b” = billion and “t” =

trillion).

Largest Mutual Fund Companies [as of 9-30-2006]

Company

Open-

End

Closed-

End

Variable

Annuities

Total

%

Fidelity $1 t $0 $60 b $1.1 t 11%

Vanguard $1 t $0 $10 b $1.0 t 10%

American Funds $925 b $0 $85 b $1.0 t 10%

Franklin / Templeton $280 b $4.3 b $30 b $315 b 3%

BlackRock / Merrill $250 b $31 b $9 b $290 b 3%

Bank of America / Fleet $230 b $0.9 b $5.9 b $240 b 2%

Morgan Stanley $195 b $16 b $17 b $225 b 2%

Allianz / PIMCO $200 b $12 b $14 b $225 b 2%

JP Morgan / Chase $220 b $0.7 b $0.6 b $225 b 2%

Legg Mason / Citibank $200 b $8.7 b $9 b $220 b 2%

Industry Total $8.9 t $240 b $1.1 t $10.3 t 100%

MUTUAL FUNDS 1.5

QUARTERLY UPDATES

IBF | GRADUATE SERIES

CORRELATIONS TO THE S&P 500 REVISITED

A review of the past handful of years shows that the correlation

coefficient of a number of categories with the S&P 500 has

increased. As an example, from February 2000 to February 2006,

nine of the 10 different sectors in the S&P 500 (e.g., financials,

consumer cyclicals, energy, etc.) showed a correlation of at least

75% with the overall market. By contrast, in 2000, only two

sectors moved in such close step with the S&P 500. The table below

shows five-year correlations to the S&P for four different categories.

5-Year Correlations to the S&P 500

[Feb. 2000 and Feb. 2006]

Index 2000 correlation 2006 correlation

Hedge funds 35% 96%

MSCI EAFE 32% 96%

Russell 2000 62% 94%

Goldman Commodity -14% 33%

1.6 MUTUAL FUNDS

QUARTERLY UPDATES

IBF | GRADUATE SERIES

STYLE BOXES

Morgan Stanley, Morningstar, Russell, Standard & Poor’s, and

Wilshire have very different definitions of market capitalization.

Among just these five services, the definition of “large cap”

stocks ranges anywhere from 67% to 92% of total U.S. stock

market capitalization. These five services have different definitions

of “small cap.” The differences range from 3% of total market

capitalization (Morningstar) up to 12% (Morgan Stanley). Russell

does not recognize “mid cap” stocks per se, but does designate the

smallest 25% of their large cap index as “mid cap.”

Only half of what Morningstar classifies as “mid cap” is

categorized the same way by S&P. Morningstar and S&P disagree

about 30% of the time as to what is “mid cap.” The two companies

also disagree as to what is “growth” and “value” 20% of the time.

About 50% of Morningstar’s “mid cap” stocks are smaller than the

largest “small cap” S&P stocks.

S&P re-categorizes stocks twice a year during the second and

fourth quarters. During these quarters, an average of one in nine

stocks changes categories; 90% of these changes come as a result of

re-categorizing a growth stock as a value play, or vice versa—only

10% is size reclassification.

MUTUAL FUNDS 1.7

QUARTERLY UPDATES

IBF | GRADUATE SERIES

Critics of the nine equity style boxes point out that diversifying

across 13 widely-recognized asset classes, such as stocks, bonds,

money market, international, etc, is seven times more effective

than diversifying across the nine different stock categories. The

critics believe that potentially 74% of portfolio volatility can be

eliminated in this way (vs. only 11% amongst the different domestic

stock categories). In short, those who question stock style boxes

believe that U.S. stocks, regardless of size or being classified as

growth, value, or blend, are a single asset class, not six or nine.

FOCUSED FUNDS AND RISK

Focused funds that have low turnover tend to also have low

volatility. For example, mutual funds that were in the quartile with

the fewest stocks and in their category’s lowest-turnover quartile had

a lower standard deviation than the category average in over 75% of

rolling one-, three-, five-, and 10-year periods combined.

For the 2000, 2001, and 2002 calendar years, as a group,

concentrated funds performed better than their non-concentrated

peers. In 2001, funds in the most-concentrated quartile had

performance in the top 39% of their category’s average; the least

concentrated quartile averaged a 54% ranking.

1.8 MUTUAL FUNDS

QUARTERLY UPDATES

IBF | GRADUATE SERIES

LIFECYCLE FUNDS

Lifecycle fund assets increased by over 60% in 2006. Some financial

advisors are concerned that the equity exposure many of these funds

for those about to retire is too high (e.g., “2010 funds” have stock

exposures as high as 63% in the case of Charles Schwab and T.

Rowe Price). A University of Maryland finance professor

recommends using three lifecycle funds. For example, someone

retiring in 2015 could buy a 2015 fund to cover the first 10 years of

retirement, a 2025 fund to pay for the years from ages 75 to 85, and

a 2035 fund for the final years.

TARGET-DATE FUNDS EXPAND

As of early May 2007, there were 34 mutual fund companies that

offered one or more target-date funds. This $150 billion asset

category has increased in popularity partially because of the federal

pension bill, wherein target-date funds are frequently the default

option for 401(k) plan participants.

Besides growing in popularity, target-date funds have also expanded

the number of investment categories they invest in; emerging market

stocks, REITs, TIPS, private equity, commodities, leveraged loans,

and/or long-short funds are now being used by more and more of

these funds.

MUTUAL FUNDS 1.9

QUARTERLY UPDATES

IBF | GRADUATE SERIES

MORE AGGRESSIVE LIFE CYCLE FUNDS

A number of life cycle funds have increased their stock allocation

from 80% to 90% for younger investors. One life cycle fund for

those just retiring has 55% in common stocks and 10% in REITs; the

fund shifts to 25% in stocks, 10% in REITs, and 65% in fixed

income for those age 80. The fund company’s research found that a

1% higher annual return beginning at age 25 could fund “more than

10 additional years of retirement spending.”

When determining the appropriate asset mix for your older clients,

think of their Social Security payments as a fixed-rate annuity; this

means that most retirees will end up with a larger percentage

allocated to fixed income than they think. One way to calculate this

percentage is to add up all projected Social Security payments,

discounted by a present value percentage.

Other mutual fund life cycle studies reach four additional

conclusions: (1) investors tend to pick portfolios that are more

aggressive than their ages warrant; (2) when a couple retires, it

should be expected that at least one of them will reach their 90s; (3)

the biggest risk to retirees is outliving their assets; and (4) life cycle

funds are likely to grow at an even more robust rate after the passage

of the Pension Protection Act of 2006 (which encourages companies

to automatically enroll workers into qualified retirement plans—a

life cycle fund could be the default selection if the employee does

not pick another option).

1.10 MUTUAL FUNDS

QUARTERLY UPDATES

IBF | GRADUATE SERIES

LONG-SHORT FUNDS

Long-short funds ($14 billion in assets as of July 2006) are

sometimes confused with market neutral funds. Market neutral funds

balance their short and long positions, giving them a net market

exposure of zero; long-short funds either have a consistent long bias

or adjust their long-short mix tactically over time.

Long-short funds give smaller investors access to certain hedge

fund strategies and although they are less expensive than hedge

funds, costs can still be high. Some long-short funds have an

expense ratio as high as 4% (vs. 1.5% for the average domestic stock

fund). Over the past three years (ending 12/31/2006), long-short

funds averaged 7.5% annually.

DIVERSIFICATION BENEFITS

Many advisors have seen an “element chart” of investment

returns, asset category performance rankings over each of the

past several years. What few advisors have seen is such a chart

that includes not only growth and value plays, but REITs, mid

cap issues, and, most importantly, the ranking of a “diversified

portfolio” (defined as an equal weighting in each of the nine

asset classes ranked below).

MUTUAL FUNDS 1.11

QUARTERLY UPDATES

IBF | GRADUATE SERIES

Yearly Asset Category Rankings [1992-2006]

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

SV

29%

FS 33%

FS 8%

LG 38%

RE 36%

LG 37%

LG 42%

SG 42%

RE 26%

RE 15%

IB 10%

SG 49%

RE 30%

FS 14%

RE 34%

HY

16%

SV

24%

LG

3%

LV

37%

LG

24%

MC

32%

FS

20%

LG

28%

SV

23%

SV

14%

RE

5%

SV

46%

SV

22%

MC

13%

FS

27%

RE 12%

LV 19%

RE 1%

SG 31%

LV 22%

SV 32%

MC 19%

FS 27%

MC 18%

IB 8%

HY -1%

FS 39%

FS 21%

RE 8%

SV 23%

MC

12%

RE

19% DP

0%

MC

31%

SV

21%

LV

30%

LV

14%

MC

15%

IG

12%

HY

5%

SV

-11%

RE

38%

MC

16% DP

7%

LV

21%

LV 11%

HY 17%

LV -1%

SV 26%

MC 19%

DP

21%

DP

9%

DP

13%

LC 6%

MC -1%

DP

-12%

MC 36%

DP

16%

LV 6%

DP

17%

DP

10%

DP

17%

HY

-1% DP

26%

DP

17%

RE

19%

IB

9%

LV

13% DP

2%

DP

-1%

MC

-15% DP

33%

LV

16%

SV

5%

SG

13%

SG 8%

MC 14%

SV -2%

HY 19%

HY 11%

SG 13%

HY 2%

HY 2%

HY -6%

SG -9%

FS -16%

LV 32%

SG 14%

SG 4%

HY 12%

IG

7%

SG

13%

SG

-2%

IG

18%

SG

11%

HY

13%

SG

1%

IG

-1%

FS

-14%

LV

-12%

LV

-21%

HY

29%

HY

11%

LG

3%

LG

11%

LG

5%

IG

10%

IG

-3%

RE

18%

FS

6%

IG

10%

SV

-6%

SV

-1%

LG

-22%

LG

-13%

LG

-24%

LG

-26%

LG

6%

HY

3%

MC

10%

FS

-12%

LG

-2%

MC

-4%

FS

12%

IG

4%

FS

2%

RE

-19%

RE

-6%

SG

-22%

FS

-21%

SG

-30%

IG

4%

IG

4%

IG

2%

IG

4%

SV = Russell 2000 Value Index MC = S&P MidCap 400 Index IG = Lehman Aggregate Bond Index

SG = Russell 2000 Growth Index FS = EAFE Index RE = FTSE NAREIT REIT Index

LG = S&P 500 / Barra Growth Index HY = Lehman High-Yield Index DP = equal parts of other 9 indexes

LV = S&P 500 / Barra Value Index

Observations

Large growth ranked at the top or bottom—never in the middle.

REITs ranked number one more than any other category.

Quality bonds ranked last more than any other category.

The diversified portfolio always landed in the middle.

1.12 MUTUAL FUNDS

QUARTERLY UPDATES

IBF | GRADUATE SERIES

FREQUENCY OF PORTFOLIO REBALANCING

According to the Financial Planning Association (FPA), the

optimal interval for rebalancing is 15-17 months, on average.

Research shows that if a portfolio is rebalanced more than about

once every 16 months, winners are sold off too quickly. An October

2006 study by the Pension Research Council at Wharton showed that

only 10% of 401(k) participants studied rebalanced their accounts on

either an active or a passive basis (e.g., using a lifecycle or target

retirement fund). The study, which looked at over one million 401(k)

participants, showed that passive rebalancing increased returns by

84 basis points annually, versus just 26 basis points for those

who rebalanced on their own.

VALUE LINE HYPE

The Value Line Web site states, “A stock portfolio with #1 Ranked

stocks for Timeliness from The Value Line Investment Survey,

beginning in 1965 and updated at the beginning of each year, would

have shown a gain of 19,715% through December 31st, 2004. This

gain would have beaten the S&P 500 by more than 15 to 1 for the

same time span.

MUTUAL FUNDS 1.13

QUARTERLY UPDATES

IBF | GRADUATE SERIES

ODDS OF BEATING AN INDEX

For the five-year period ending December 31st, 2006, only 15% of

large value managers beat their respective index; 90% of large

growth managers beat their index. One group of managers is not any

smarter or intuitive than the other. The disparity shows that most

funds are less “style-pure” than “style specific” (e.g., large value

funds hold stocks other than those classified as “large value,”

whereas a large value index would have virtually all, if not all, of its

holdings in “large value”). For example, the typical large cap

growth fund has the following composition.

Composition of the Average U.S. Large Cap Growth Fund

49% large growth 10% mid-cap growth < 1% small blend

27% large blend 4% mid-cap blend < 1% small growth

6% large value < 1% small value

If new benchmarks are calculated using the actual weightings, 35%

of large cap growth managers outperformed their “index” over the

past five years ending December 31st, 2006; 38% in the case of large

cap value managers. For the three-year period ending 12/31/2006,

24% of small growth funds beat their weighted benchmark versus

39% of large growth funds. Such results may cast some doubt on

whether or not the common assumption that small caps are a better

arena for active management.

1.14 MUTUAL FUNDS

QUARTERLY UPDATES

IBF | GRADUATE SERIES

Looking at just annual returns, the pattern remains consistent within

a fairly narrow range. In 1998, 44% of mutual funds in the nine style

box categories (e.g., large cap growth, large cap value, large cap

blend, mid-cap growth, etc.). In 1999, when technology stocks

soared, 50% of the funds beat their custom benchmark; the same

results occurred for 2000 and 2001 and actually increased to 57% in

2002 (probably due to the large cash holdings that year when the

market dropped). When the market rebounded in 2003, only 35% of

actively managed funds outperformed their custom benchmark. In

2004, the number rose to 42%, 47% in 2005, and then fell to 35% for

the 2006 calendar year.

Over 90% of domestic stock funds have geometric mean market

capitalizations below that of the S&P 500; thus, these funds could

outperform the S&P 500 when small and mid cap stocks are in favor,

and underperform when large blue chips do well.

Not only has independent research come up with a dramatically

lower return figure than Value Line’s claim, recent data would

appear to support the independent research. The flagship Value Line

mutual fund (VLIFX) uses the same criteria that guide The Value

Line Investment Survey (according to the fund’s prospectus). Yet,

the fund has only outperformed the S&P 500 twice over the past 10

years. The fund’s 10-year record as of May 30th, 2006 was 6%

annually, versus 9% for the S&P 500. Over the past 15 years, the

fund averaged 9.1% versus 10.9% for the S&P 500.

MUTUAL FUNDS 1.15

QUARTERLY UPDATES

IBF | GRADUATE SERIES

MIXED PERFORMANCE RANKINGS

A 2007 study by DeiMeo Schneider shows that roughly 90% of

mutual fund managers whose performance ranking in the top quartile

for 10 years ending December 31st, 2006 also had performance that

was below its category’s median for at least three or more of those

10 years. It turns out that just over 50% of pension managers

whose 10-year record was in the top quartile experienced below

median results for at least five consecutive years during the same

10 years.

The results become even more extreme within certain categories.

Over two-thirds of the top quartile foreign equity fund managers and

just under 75% of the top quartile medium-term bond fund managers

underperformed their category’s median returns for three years or

more during the 10-year period. There was at least a five-year

continuous stretch of underperformance for 72% of mid-cap blend,

71% of REIT, and 70% for emerging market equity managers whose

performance ranked in the top quartile for the same 10 years ending

December 31st, 2006.

Overall, the study showed that, on average, 22% of top-quartile

managers were in the bottom half of their peer groups during any

given three-year period. Based on these findings, it appears that at

any given time, close to a quarter of the top-performing pension

fund managers and mutual fund managers will experience a

three-year stretch of underperformance at any given quarterly

review.

1.16 MUTUAL FUNDS

QUARTERLY UPDATES

IBF | GRADUATE SERIES

ACTIVE VS. PASSIVE MANAGEMENT

Advocates of passive management (index funds) rarely talk about

accurate benchmark comparisons. For example, the average large

cap value fund has only about 40% of its assets in large cap value

stocks; the balance is in a variety of other stocks such as small and

mid cap growth as well as value.

Over the past five years ending March 31st, 2007, only 15% of the

large cap value stock funds outperformed their benchmark. Using

“custom” benchmarks (meaning an index that is comprised of

equities that a particular asset category’s management actually

invests in), 35-47% of the managers outperform their “actual” index.

The editor of a Vanguard newsletter uses active management for his

core portfolio. The editor suggests using actively-managed funds for

those you have “the greatest confidence in; use passive index funds

in those categories you cannot find a super-compelling active

management.”

MUTUAL FUNDS 1.17

QUARTERLY UPDATES

IBF | GRADUATE SERIES

SIDE-BY-SIDE MANAGEMENT

A number of mutual fund managers are serving two masters: the

fund(s) they oversee and one or more hedge funds. Mutual funds

sharing managers with hedge funds include Ameriprise, Nationwide,

Pioneer, and Vanguard. There are 125 individual portfolio

managers simultaneously running mutual funds and hedge

funds. Total mutual fund assets potentially affected by this possible

conflict of interest is $450 billion.

In 2003, the U.S. House of Representatives approved a measure,

later shelved, that would have barred someone from running a hedge

fund and mutual fund at the same time. Early in 2007, an SEC

official testifying in front of Congress said such a practice “presents

significant conflicts of interest that could lead the adviser to favor

the hedge fund over other clients.” Indeed, there are a number of

ways such favoritism could occur:

1. sell shares of a security in a hedge fund before a similar sale

in the mutual fund;

2. instead of assigning a trade to a specific fund at the time of

execution, a manager could “cherry pick” trades (e.g., trade in

the morning and assign it to the hedge fund or mutual fund

later in the day depending on its performance);

3. managers who have access to a limited number of hot IPOs

might favor the hedge fund over the mutual fund (since the

hedge fund has higher management fees plus a typical 20%

performance incentive fee); and

4. shorting stocks in a hedge fund while holding a long position

in a mutual fund could cause the stock’s price to drop.

1.18 MUTUAL FUNDS

QUARTERLY UPDATES

IBF | GRADUATE SERIES

The SEC does not dictate how managers should address these

potential conflicts of interest. Academic studies are divided on

whether or not mutual fund investors are well served or hurt by

multiple-role (side-by-side) management.

A study by William & Mary’s Mason School of Business and the

Wharton School looked at more than 450 mutual funds run by

companies who also managed hedge funds between 1994 and 2004.

The study found that in such instances, the mutual fund investors

underperformed their peer group by 1.2% a year. A Loyola

University Chicago, University of California, and University of

Illinois study reviewed 200 mutual funds run by side-by-side

managers (who also ran hedge funds) with a similar investment style

and found that the mutual funds outperformed their peers by 1.5%

annually from 1990 through 2005.

Starting in 2006, the SEC began to require funds to disclose

other types of accounts run by the manager and total assets

affected. Such information is found in the fund’s statement of

additional information (SAI). To find out what types of funds are

managed by a fund company, advisors and investors can search

www.adviser info.sec.gov.

MUTUAL FUNDS 1.19

QUARTERLY UPDATES

IBF | GRADUATE SERIES

MANAGER-INVESTED MUTUAL FUNDS

Mutual fund managers who own shares of the funds they oversee

outperform, on average, funds that are not partially owned by

management. A 2006 study done by three business schools looked at

the total returns of 1,300 stock and bond funds. The study looked at

managers who owned shares (43% of the 1,300 funds) versus funds

with no management ownership (57%).

Manager-owned funds had a mean return of 8.7% vs. 6.2% for

funds with no management ownership; the highest percentage of

management ownership was with U.S. stock funds and lowest

with foreign bond funds.

As of the beginning of 2007, of the 500 mutual funds most highly

recommended by Morningstar, more than 150 managers had each

invested more than $1 million in their funds. The most extreme

example of management ownership was Bill D’Alonzo who

oversees Brandywine (BRWIX) and Brandywine Blue (BLUEX); he

had 100% of his liquid net worth invested in these two funds. Other

examples include: Selected American (SLASX) and Selected Special

(SLSSX), two funds whose employees and those affiliated with the

fund collectively owned over $2 billion worth of shares; Longleaf

employees and directors owned over $500 million of their funds;

Chuck Royce had $50 million of his own money invested in Royce

Total Return (RYTRX) and Royce Premier (RYPRX).

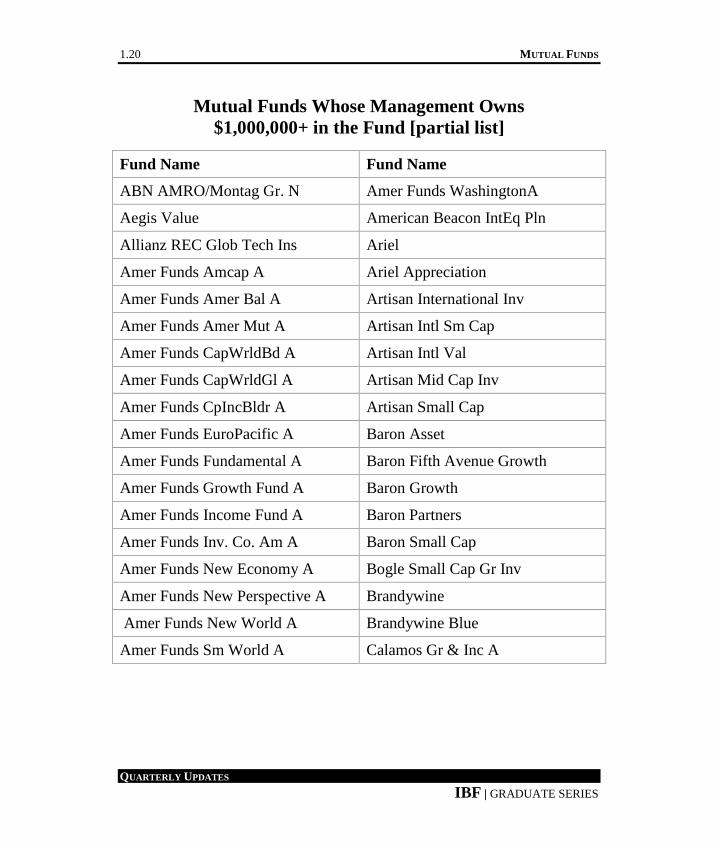

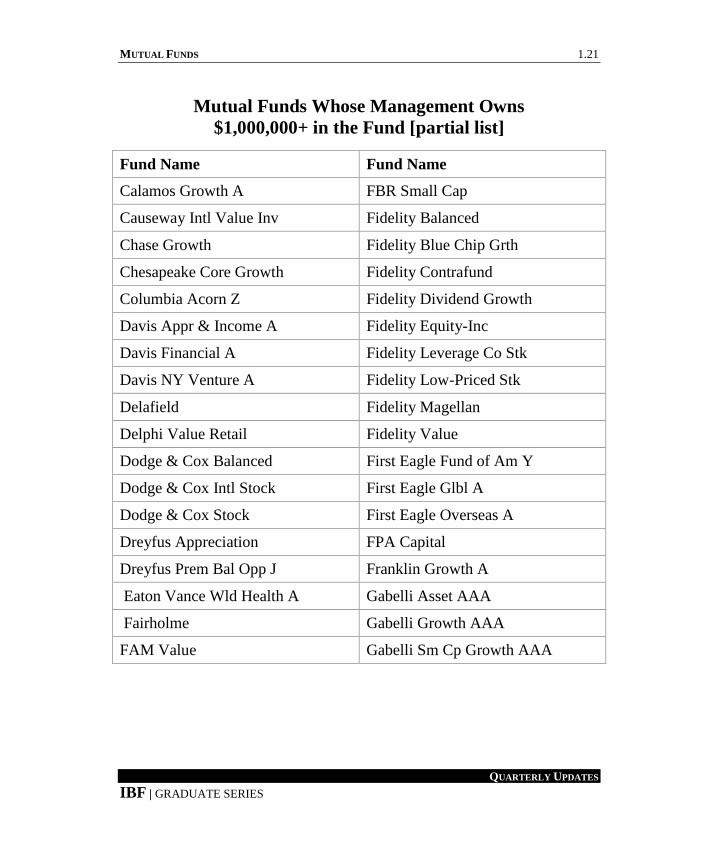

The extensive table below shows over 170 mutual funds whose

management owns over $1 million in their fund.

1.20 MUTUAL FUNDS

QUARTERLY UPDATES

IBF | GRADUATE SERIES

Mutual Funds Whose Management Owns

$1,000,000+ in the Fund [partial list]

Fund Name Fund Name

ABN AMRO/Montag Gr. N Amer Funds WashingtonA

Aegis Value American Beacon IntEq Pln

Allianz REC Glob Tech Ins Ariel

Amer Funds Amcap A Ariel Appreciation

Amer Funds Amer Bal A Artisan International Inv

Amer Funds Amer Mut A Artisan Intl Sm Cap

Amer Funds CapWrldBd A Artisan Intl Val

Amer Funds CapWrldGl A Artisan Mid Cap Inv

Amer Funds CpIncBldr A Artisan Small Cap

Amer Funds EuroPacific A Baron Asset

Amer Funds Fundamental A Baron Fifth Avenue Growth

Amer Funds Growth Fund A Baron Growth

Amer Funds Income Fund A Baron Partners

Amer Funds Inv. Co. Am A Baron Small Cap

Amer Funds New Economy A Bogle Small Cap Gr Inv

Amer Funds New Perspective A Brandywine

Amer Funds New World A Brandywine Blue

Amer Funds Sm World A Calamos Gr & Inc A

MUTUAL FUNDS 1.21

QUARTERLY UPDATES

IBF | GRADUATE SERIES

Mutual Funds Whose Management Owns

$1,000,000+ in the Fund [partial list]

Fund Name Fund Name

Calamos Growth A FBR Small Cap

Causeway Intl Value Inv Fidelity Balanced

Chase Growth Fidelity Blue Chip Grth

Chesapeake Core Growth Fidelity Contrafund

Columbia Acorn Z Fidelity Dividend Growth

Davis Appr & Income A Fidelity Equity-Inc

Davis Financial A Fidelity Leverage Co Stk

Davis NY Venture A Fidelity Low-Priced Stk

Delafield Fidelity Magellan

Delphi Value Retail Fidelity Value

Dodge & Cox Balanced First Eagle Fund of Am Y

Dodge & Cox Intl Stock First Eagle Glbl A

Dodge & Cox Stock First Eagle Overseas A

Dreyfus Appreciation FPA Capital

Dreyfus Prem Bal Opp J Franklin Growth A

Eaton Vance Wld Health A Gabelli Asset AAA

Fairholme Gabelli Growth AAA

FAM Value Gabelli Sm Cp Growth AAA

1.22 MUTUAL FUNDS

QUARTERLY UPDATES

IBF | GRADUATE SERIES

Mutual Funds Whose Management Owns

$1,000,000+ in the Fund [partial list]

Fund Name Fund Name

Gateway Fund Legg Mason Opp Prim

Harbor Capital App Instl Legg Mason Value Prim

Harbor Intl Instl LKCM Small Cap Equity Ins

Homestead Value Longleaf Partners

Hussman Strategic Growth Longleaf Partners Intl

ICAP Equity Longleaf Partners Sm-Cap

ICAP International Loomis Sayles Bond Ret

ICAP Select Equity Lord Abbett Affiliated A

Janus Marsico Focus

Janus Contrarian Fund Marsico Growth

Janus Enterprise Masters’ Select Equity

Janus Mid Cap Val Inv Matrix Advisors Value

Janus Orion Meridian Growth

Janus Overseas Meridian Value

Janus Sm Cap Val Instl Merrill Global Alloc A

Janus Twenty Muhlenkamp

Jensen J Mutual Shares A

Kalmar Gr Val Sm Cp Nicholas

MUTUAL FUNDS 1.23

QUARTERLY UPDATES

IBF | GRADUATE SERIES

Mutual Funds Whose Management Owns

$1,000,000+ in the Fund [partial list]

Fund Name Fund Name

Nicholas II I Royce Value Service

Northeast Investors RS Emerging Growth

Oak Value RS MidCap Opport

Oakmark Equity & Inc I Schneider Value

Oakmark Global I Selected American S

Oakmark I Sequoia

Oakmark International I Skyline Spec Equities

Oakmark Intl Small Cap I Sound Shore

Oakmark Select I T. Rowe Price Eq Inc

Osterweis Fund T. Rowe Price Gr Stk

Pioneer A T. Rowe Price Mid Gr

Pioneer High Yield A T. Rowe Price New Horiz

PRIMECAP Odyssey Agg Gr T. Rowe Price Sm Val

PRIMECAP Odyssey Growth Third Avenue Intl Value

Royce Opportunity Inv Third Avenue RealEst Val

Royce Premier Inv Third Avenue Sm-Cap Val

Royce Special Equity Inv Third Avenue Value

Royce Total Return Inv Thompson Plumb Growth

1.24 MUTUAL FUNDS

QUARTERLY UPDATES

IBF | GRADUATE SERIES

Mutual Funds Whose Management Owns

$1,000,000+ in the Fund [partial list]

Fund Name Fund Name

Thornburg Intl Value A Vanguard PRIMECAP Core

Thornburg Value A Vanguard Selected Value

Torray Vanguard Wellesley Inc

Turner Small Cap Growth Vanguard Wellington

Tweedy, Browne American Vanguard Windsor II

Tweedy, Browne Glob Val Wasatch Micro Cap

Van Kampen Comstock A Wasatch Small Cap Growth

Van Kampen Eq and Inc A Wasatch Ultra Growth

Van Kampen Growth & IncA Weitz Hickory

Vanguard Cap Opp Weitz Partners Value

Vanguard Capital Value Weitz Value

Vanguard Explorer Wesport R

Vanguard Health Care WF Adv Common Stk Z

Vanguard PRIMECAP WF Adv Opportunity Inv

MUTUAL FUNDS 1.25

QUARTERLY UPDATES

IBF | GRADUATE SERIES

B SHARES REVIEWED BY SEC

During 2006, the NASD imposed more than $40 million of fines on

brokerage firms for improperly selling B and C mutual fund shares.

During the early part of 2007, the SEC acknowledged that one of its

key arguments no longer exists; the agency had assumed A shares

were always better than B shares. The NASD commission now

believes that cost alone is not the only decision in making

investment recommendations.

Most of the lawsuits against brokerage firms were based on one of

three things: (1) failure to tell clients that A shares can be cheaper

than B shares, (2) fraud, and/or (3) suitability. In a 2007 case

dropped by the SEC, the agency acknowledged that even at the

$250,000 breakpoint, B shares may not be more expensive for the

client than A shares.

Because of regulatory concern, brokerage firms have generally

limited B share sales to $50,000 or less. Shares of B shares had

fallen to 3% of the market in 2006, down from 10% in 2001. One

broker, now retired, spent $400,000 in legal fees and lost $1.6

million in deferred compensation in 2001 when his broker-dealer

fired him over the sale of B shares. In late 2005, a NYSE arbitration

panel ordered the firm to pay all deferred compensation plus legal

fees.

1.26 MUTUAL FUNDS

QUARTERLY UPDATES

IBF | GRADUATE SERIES

SHAREHOLDER PROXY VOTING

During 2006, there were 1,400 filings by mutual funds asking

shareholders to vote on fund changes. The number of filings

represents about 20% of all mutual funds. During the first quarter of

2007, roughly 340 were seeking shareholder votes, according to

governance tracker the Corporate Library. The top issues voting

upon by shareholders have been issues dealing with directors and/or

trustees, investment restrictions and policies, and sub-advisor

agreements.

Fund companies want shareholders to vote as soon as possible for

such changes. If the necessary number of votes is not obtained, more

shareholder solicitation is required and this costs the fund, and

specifically its shareholders, more money. Among the most popular,

and worrisome proposals, are changes to investment limits,

loosening limits on borrowing and lending, requesting greater

flexibility in real estate and commodity investments, and taking

bigger positions in stocks or foreign holdings.

Despite investors’ concerns about proxy voting, shareholders rarely

show up at an announced meeting. For example, only 50 Dodge &

Cox investors showed up a few years ago to a meeting; only one

shareholder attended the $4.3 billion Alger Funds’ January meeting.

MUTUAL FUNDS 1.27

QUARTERLY UPDATES

IBF | GRADUATE SERIES

SECURITIES LENDING PRACTICES

Mutual funds and ETFs lend some of the securities in their portfolios

in exchange for interest payments and collateral, which provides

additional returns for fund investors (well under 1/10th of 1%).

Although this practice is not new, the explosive growth of hedge

funds engaged in short selling has greatly increased the demand for

borrowed securities.

When a hedge fund, or any investor, enters a short sale (betting a

stock will fall), they are selling a stock they have borrowed in hopes

of buying it a lower price later, replacing the borrowed shares and

pocketing the difference. Lending occurs through an agent that finds

brokerage firms needing to borrow the securities. The agent takes a

split of the money earned from the lending—from 10-30% of the

interest charge. What remains is then added to the portfolio’s cash

reserves.

The SEC issues guidelines that funds and ETFs must follow when

setting up securities-lending agreements. The requirements are more

stringent if the fund does its lending through an agent affiliated with

the fund management company.

1.28 MUTUAL FUNDS

QUARTERLY UPDATES

IBF | GRADUATE SERIES

FUND DIRECTOR PAY

As measured by asset size, the largest fund companies had a median

annual compensation of $172,000 for a director in 2006. For 2005,

the median annual compensation for the large fund companies was

$147,000 per director. The average cost to shareholders was 15.4¢

per $10,000 in assets. The figure was 16.1¢ in 2005.

A survey of over 330 fund families found that over 80% of fund

directors are independent; 60% of the time in the case of the fund’s

chairperson, up from 50% in 2005.

DIRECTORS AND 12B-1 FEES

An association of independent mutual fund directors has prepared

guidelines to help fund directors assess fees. The May 2007 report

follows an earlier announcement in 2007 that the SEC was

reviewing the rule that allows such fees.

MUTUAL FUNDS 1.29

QUARTERLY UPDATES

IBF | GRADUATE SERIES

STOCKS AND MUTUAL FUNDS

Today’s S&P 500 was created in 1913 by Alfred Cowles in order to

“portray the average experience of U.S. stock market investors.” In

2005, about 41% of the revenue for the S&P 500 companies came

from operations outside the U.S. GE expects that 49% of its global

revenue for 2007 will come from countries other than the U.S. At

the end of 2006, the top 10 stocks in the S&P 500 represented

20% of the index’s total value and performance.

The number of households with more than $5,000 in stock fell from

40% to 35% from 2001 to 2004. In 2001, the top 10% of all U.S.

households owned 75% of all taxable stock; the wealthiest 1%

owned 29%. For each $1 increase in stock wealth boosts

consumption by 4.5¢, while each $1 increase in housing wealth

increases consumption by 7¢. Mutual funds represent approximately

25% of the financial assets owned by homeowners.

QUARTERLY

UPDATES

ETFS

ETFS 2.1

QUARTERLY UPDATES

IBF | GRADUATE SERIES

2.ETF UPDATE

The first table below shows exchange-traded fund (ETF) asset

growth over each of the past several years.

ETFs: Number and Assets (in billions) [5/15/07]

Year # Assets Year # Assets

2002 109 $10.2 2005 206 $30.2

2003 116 $15.1 2006 335 $41.8

2004 152 $22.7 2007 (2nd

qtr.) 500 $50.0

The next table shows the largest ETF management companies. The

percentage figures indicate the percentage of the entire ETF

marketplace managed by each company; Barclays oversees just

under 60% of the entire ETF industry assets.

2.2 ETFS

QUARTERLY UPDATES

IBF | GRADUATE SERIES

Market Share of ETF Companies

Management Co. % of Whole

Barclays Global Investors Fund 59.6%

State Street Global Advisors 23.4%

BNY Hamilton 6.3%

Vanguard Group 5.7%

Powershares Capital 2.3%

Rydex Funds 0.9%

WisdomTree 0.5%

Victoria Bay Asset Management 0.5%

DB Commodity Services 0.3%

Van Eck Corporation 0.2%

First Trust Advisors 0.1%

Claymore Advisors 0.1%

Fidelity Distributors 0.1%

There is expected to be roughly 800 ETFs by the end of 2007. There

are currently 32 ETFs that focus on technology, 35 investing in

natural resources, 39 devoted to health care, and 22 focused on the

financial sector.

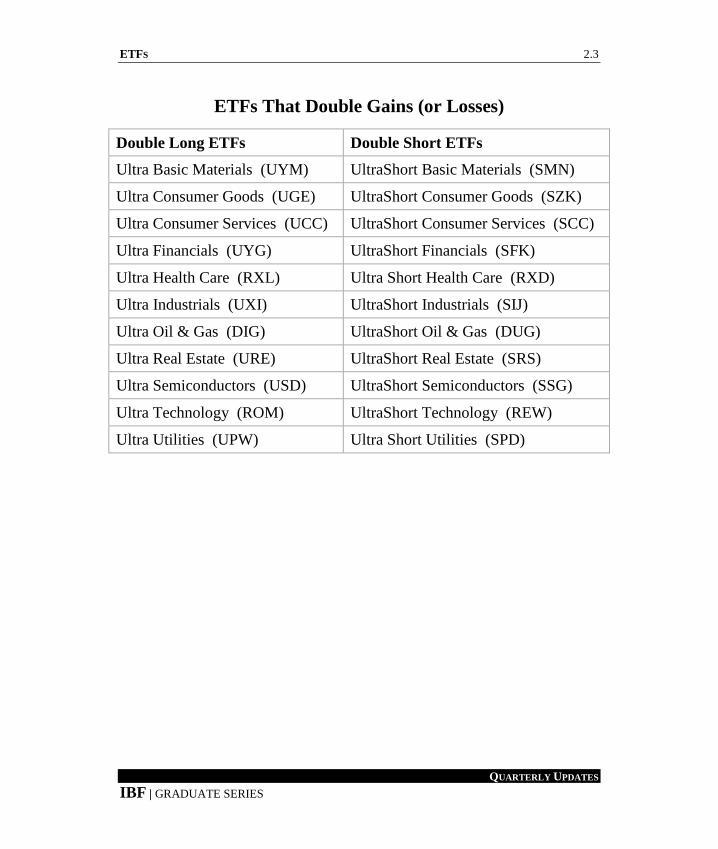

If you have high-risk investors, consider the “double” ETF funds

listed below. These funds, with an average expense ratio of just

under 1%, are designed to double an investor’s gains (or losses),

whether the market (or sector) goes up (long) or drops (short). All of

these ETFs trade on the AMEX.

ETFS 2.3

QUARTERLY UPDATES

IBF | GRADUATE SERIES

ETFs That Double Gains (or Losses)

Double Long ETFs Double Short ETFs

Ultra Basic Materials (UYM) UltraShort Basic Materials (SMN)

Ultra Consumer Goods (UGE) UltraShort Consumer Goods (SZK)

Ultra Consumer Services (UCC) UltraShort Consumer Services (SCC)

Ultra Financials (UYG) UltraShort Financials (SFK)

Ultra Health Care (RXL) Ultra Short Health Care (RXD)

Ultra Industrials (UXI) UltraShort Industrials (SIJ)

Ultra Oil & Gas (DIG) UltraShort Oil & Gas (DUG)

Ultra Real Estate (URE) UltraShort Real Estate (SRS)

Ultra Semiconductors (USD) UltraShort Semiconductors (SSG)

Ultra Technology (ROM) UltraShort Technology (REW)

Ultra Utilities (UPW) Ultra Short Utilities (SPD)

2.4 ETFS

QUARTERLY UPDATES

IBF | GRADUATE SERIES

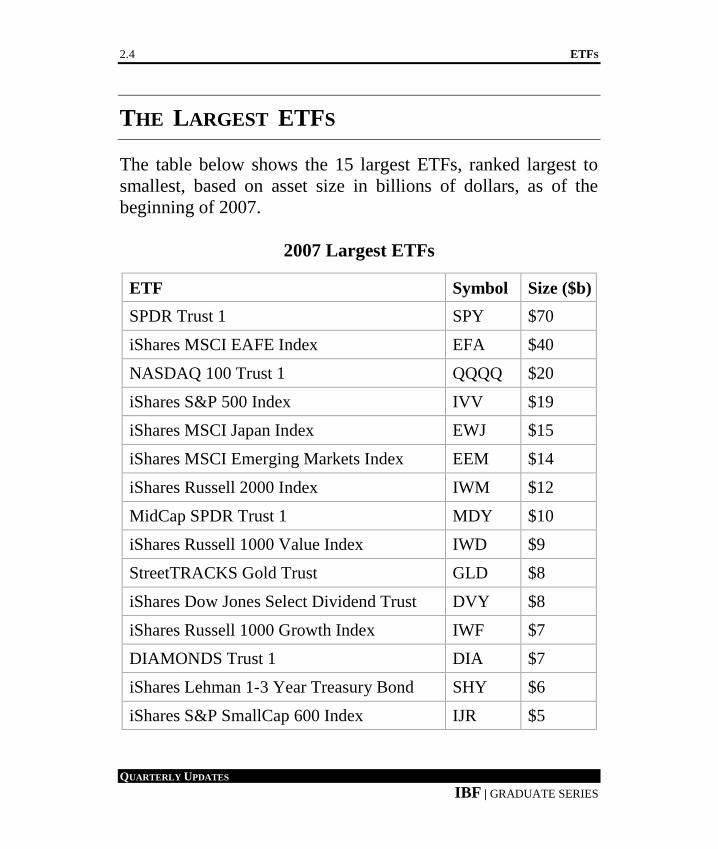

THE LARGEST ETFS

The table below shows the 15 largest ETFs, ranked largest to

smallest, based on asset size in billions of dollars, as of the

beginning of 2007.

2007 Largest ETFs

ETF Symbol Size ($b)

SPDR Trust 1 SPY $70

iShares MSCI EAFE Index EFA $40

NASDAQ 100 Trust 1 QQQQ $20

iShares S&P 500 Index IVV $19

iShares MSCI Japan Index EWJ $15

iShares MSCI Emerging Markets Index EEM $14

iShares Russell 2000 Index IWM $12

MidCap SPDR Trust 1 MDY $10

iShares Russell 1000 Value Index IWD $9

StreetTRACKS Gold Trust GLD $8

iShares Dow Jones Select Dividend Trust DVY $8

iShares Russell 1000 Growth Index IWF $7

DIAMONDS Trust 1 DIA $7

iShares Lehman 1-3 Year Treasury Bond SHY $6

iShares S&P SmallCap 600 Index IJR $5

ETFS 2.5

QUARTERLY UPDATES

IBF | GRADUATE SERIES

ETFS WITH LOW EXPENSE RATIOS

The table below shows the 15 lowest expense ratio ETFs, as of

the beginning of 2007.

2007 Lowest Expense Ratio ETFs

ETF Symbol Expense

Vanguard Large Cap VV 0.09

iShares S&P 500 Index IVV 0.09

SPDR Trust 1 SPY 0.10

iShares Lehman 7-10 Year Treasury Bond IEF 0.15

iShares iBoxx $ Invest. Grade Corp. Bond LQD 0.15

iShares Lehman 1-3 Year Treasury Bond TIP 0.15

iShares Lehman 20+ Year Treasury Bond TLT 0.15

iShares Russell 1000 Index IWB 0.15

DIAMONDS Trust 1 DIA 0.17

iShares S&P 500 Growth Index IVW 0.18

iShares S&P 500 Value Index IVE 0.18

NASDAQ 100 Trust 1 QQQQ 0.20

iShares Lehman Aggregate Bond AGG 0.20

iShares Lehman TIPS Bond TIP 0.20

iShares NYSE 100 Index NY 0.20

2.6 ETFS

QUARTERLY UPDATES

IBF | GRADUATE SERIES

ETF PRICE DISPARITIES

Often times, some of the most actively traded issues on the NYSE

and other U.S. markets are ETFs. Barclays estimates that on any

given day, 80% of the trading of its ETFs are traded by large

investors such as hedge funds. As of May 2007, there were about

500 ETFs in the U.S., valued at $500 billion (vs. 8,100 traditional

mutual funds valued at $10.5 trillion). Although ETFs are expected

to closely track an underlying index, this is not always the case

during extreme days in the market.

For example, on February 27th

, 2007, an ETF managed by Barclays

that tracks the Chinese stock market closed down 9.9% in the U.S.,

even though the underlying index had fallen 2.1% during Chinese

trading hours. The index fell an additional 3.1% the next day in

China (but the Barclay’s iShares rose 4.3%). However, had U.S.

investors sold the Barclays ETF just before the close of trading on

February 27th

, their loss would have been 9.9%, not the actual loss of

the index, 2.1%. On the positive side, purchasers of the Barclays

ETF would have bought at a 7.8% discount (9.9% - 2.1%), resulting

in a substantial gain for owning the ETF shares for less than a day.

Another example is the precious metals ETF offered by Powershares

Capital Management. On Februrary 27th

, the ETF ended the day

3.3% below the actual value of the fund’s holdings. The iShares

emerging markets ETF lost 8.1%, even though the index was down

just 3.1%. As a result, a seller of $10,000 of the Barclay’s iShares

would have received $500 less than if the fund had actually tracked

the index.

ETFS 2.7

QUARTERLY UPDATES

IBF | GRADUATE SERIES

There are disparities even for ETFs that track just U.S. stocks. The

Russell 2000 Index (small company stocks) fell 3.75% on February

27th

, 2007, versus 4.70% for the actual index. In this case, a large

part of the disparity (almost 1%) was because like other ETFs, this

Russell ETF trades for 15 minutes longer than regular stocks. For all

of February 27th

, 89 of the 421 ETFs tracked by Morningstar fell

short of their portfolio value by more than 1% (+/-1/2% is considered

normal). Of those 89 ETFs, 60 fell short by more than 2%.

There are three lessons to be learned from these index and ETF

disparities. First, when there is a panic, the pricing of a number of

ETFs can be quite different than the underlying index (somewhat

similar to the premium-discount difference with most closed-end

funds). Second, advisors should think twice about selling any

investment, and in particular an ETF or CEF, during periods of high

short-term volatility. Third, it is extremely likely that any disparity,

no matter how narrow or wide, is likely to be corrected within one or

two days, thereby making moot any attempt to sensationalize such

price differences.

SECTOR VOLATILITY

The most volatile sector ETFs are, from highest to lowest risk, are:

1. Technology 6. Materials

2. Financial (includes REITs) 7. Energy

3. Healthcare 8. Consumer Staples

4. Consumer Discretionary 9. Utilities

5. Industrial

2.8 ETFS

QUARTERLY UPDATES

IBF | GRADUATE SERIES

BUYING AND SELLING ETFS

The majority of all stock and ETF trades are:

1. Market order—You get the best price currently available;

most orders are market orders.

2. Limit order—You place a buy order, indicating that you are

willing to pay $X per share or less. If you place a sell limit

order, you are indicating that you want $Y per share or more.

If someone is not willing to sell you shares for $X or less, the

order is not filled; similarly, if someone is not willing to buy

your shares for $Y or more, you will end up not selling the

shares.

3. Stop-loss (or stop) order—The order goes into effect as soon

as the price per share of the stock (or ETF) hits a certain

price. Once this price is reached, the stop-loss order becomes

a market order. This type of order is frequently used to limit

price declines if the security’s price falls.

4. Short sale—You believe the price per share of a stock or

ETF is going to fall. Shares of a stock or ETF are borrowed

by your brokerage firm on your behalf (note: you will be

paying an ongoing interest charge for the borrowing). If the

price of the security falls after the short sale, you have a gain;

if the price of the security rises, you have a loss. At some

point in the future, the investor will decide to buy the stock or

ETF and thereby repay the original borrowed shares.

QUARTERLY

UPDATES

UITS AND

CLOSED-END FUNDS

UITS AND CLOSED-END FUNDS 3.1

QUARTERLY UPDATES

IBF | GRADUATE SERIES

3.UIT AND NEW FUND CRITICISM

Some newly launched mutual funds as well as UITs rely on

historical data to increase sales and help market their portfolios.

Critics argue that these new offerings simply keep shifting the

composition of the funds’ proposed holdings until they find one that

happens to have worked over the necessary range of dates.

CLOSED-END FUND ASSET INCREASE

For the first quarter of 2007, more than $13 billion was raised

through closed-end fund IPOs, more than was raised for all of 2006.

At the end of 2006, the closed-end fund (CEF) industry managed

$420 billion in assets. As of the end of the first quarter of 2007, the

median discount for all CEFs was 2.3%; about 35% of all CEFs

trade at a premium over their NAV.

CEF IPOs

Year # of IPOs $ (billions)

2006 21 $11

2005 47 $21

2004 50 23

2003 48 28

2002 77 16

3.2 UITS AND CLOSED-END FUNDS

QUARTERLY UPDATES

IBF | GRADUATE SERIES

A number of sources believe that CEF IPOs are not good for

investors since the majority of them end up trading at a discount

to NAV. These same critics believe that the IPO market for CEFs

largely rely on unsophisticated income-oriented investors. In January

2007, the IPO for Alpine Total Dynamic Dividend Fund raised over

$4 billion.

CLOSED-END COVERED CALL FUNDS

Closed-end covered-call funds have the objective of generating high

income by selling call options on stocks in their portfolios. These

types of funds first appeared in 2004 and accounted for 85% of IPO

money going into closed-end funds. Even though these are equity

funds, a number of analysts consider them to be a “fixed-income

application.”

The goal of a closed-end covered-call fund manager is to achieve the

highest premium income possible while forfeiting the least amount

of equity upside. Critics feel that these funds cap returns in bull

markets (since good-performing stocks will be called away), and in a

crash or severe correction do not generate enough option-writing

income to offset the decline. In some respects, these funds perform

best, at least comparatively speaking, when the market is flat or

rising slightly.

The Chicago Board Options Exchange (CBOE) currently licenses

four buy-write indexes. The table below lists the six largest closed-

end covered-call funds. As of the third quarter of 2006, all six of

these funds were selling at a discount that ranged from 3% to 9%.

UITS AND CLOSED-END FUNDS 3.3

QUARTERLY UPDATES

IBF | GRADUATE SERIES

The Largest Closed-End Covered-Call Funds

NFJ Dividend, Interest &

Premium Strategy

Nuveen Equity Premium

Opportunity

Eaton Vance Tax-Managed

Global Buy-Write

Eaton Vance Tax-Managed Buy-

Write Opportunity

ING Global Equity Dividend &

Premium Opportunity

Black Rock Enhanced Dividend

Achievers

QUARTERLY

UPDATES

REITS

REITS 4.1

QUARTERLY UPDATES

IBF | GRADUATE SERIES

4.REIT UPDATE

After stagnating in 1999, real estate funds went on to average just

under 22% per year for the next seven years (ending 12/31/2006).

This sector category can also provide diversification, when the S&P

500 dropped 9% in 2000, real estate funds gained 27%. The table

below shows return figures for REIT sectors, as of March 1st, 2007.

REIT Sector Returns [ending 3-1-2007]

REIT category 1-year 3-year 5-year 10-year

Apartments 24.1% 29.6% 21.7% 15.9%

Regional Malls 30.8% 28.4% 33.9% 21.4%

Shopping Centers 34.7% 26.7% 29.1% 18.5%

Office Buildings 41.7% 27.3% 22.3% 15.4%

Industrial 24.8% 25.8% 26.0% 17.2%

Health Care 41.1% 18.3% 23.1% 14.9%

Self Storage 29.7% 30.8% 25.6% 18.0%

Lodging / Resorts 24.5% 24.4% 17.1% 5.3%

Manufactured Homes 8.7% 3.4% 8.2% 9.1%

Mortgage REIT Index 7.2% -4.6% 15.1% 6.6%

4.2 REITS

QUARTERLY UPDATES

IBF | GRADUATE SERIES

INTERNATIONAL REITS

From 2003 to 2007, Asia REITs returned an average of 35.4% per

year; 43.5% annually in the case of European REITs (67% in 2006).

In the U.S. there are about 180 REITs registered with the SEC. Japan now has more than 40. Over 20 countries have passed or

considered laws allowing the formation of REITs. The U.K. and

Germany adopted REIT laws in early 2007.

QUARTERLY

UPDATES

STOCKS

STOCKS 5.1

QUARTERLY UPDATES

IBF | GRADUATE SERIES

5.DOW MILESTONES

The Dow Jones Industrial Average (DJIA) began with just 12 stocks

in 1896 when the average had a starting value of 40.94. Since 1928,

there have been 30 stocks in the Dow. The table below shows Dow

milestones.

It took 127 days for the DJIA to move from 12,000 to 13,000. In

1999, it took 24 days to move from 10,1000 to 11,000. But it took

7.5 years to move from 11000 to 12,000. The Great Depression

caused the DJIA to lose 90% of its value. The high it reached on

September 3rd

, 1929, was not surpassed until 1954.

The Dow Hitting 1,000 Point Increments

Dow Date Dow Date

12000 Oct. 19, 2006 5000 Nov 21, 1995

11000 May 3, 1999 4000 Feb 23, 1995

10000 March 29, 1999 3000 Apr. 17, 1991

9000 April 6, 1998 2000 Jan. 8, 1987

8000 July 16, 1997 1000 Nov. 14, 1972

7000 Feb. 13, 1997 start May 26, 1896

6000 Oct 14, 1996

5.2 STOCKS

QUARTERLY UPDATES

IBF | GRADUATE SERIES

DOW DROPS

The table below shows the biggest percentage drops in the Dow

Jones Industrial Average (DJIA) from the beginning of 2003 to

March 17th, 2007. Since 1980, the return on the DJIA has averaged

13.9% per year, versus 13.1% for the S&P 500. There are 10 sectors

in the S&P 500:

DJIA Biggest 1-Day Drops [1-1-2003 through 3-17-2007]

Date % Change Date % Change

3-24-03 3.6% 5-19-03 2.1%

2-27-07 3.3% 1-30-03 2.0%

1-24-03 2.9% 3-13-07 2.0%

3-10-03 2.2%

S&P 500 Sectors

consumer discretionary industrials

consumer staples materials

energy technology

financials telecom

health care utlities

If the technology sector were excluded from the S&P 500, the S&P

500 would be 16% above its 2000 peak. Looking at the entire S&P

500 (including technology stocks), more than 2/3 of the stocks are

above their peak prices reached in 2000.

STOCKS 5.3

QUARTERLY UPDATES

IBF | GRADUATE SERIES

S&P 500 AND DJIA RETURNS

As of May 3rd

, 2007, the S&P 500 was within 2% of its record close

of 1527.5 in March 2000. On the same day, the Dow Jones Industrial

Average (DJIA) hit another all-time record for 2007, closing at

13,241.4. The NASDAQ, which closed at 2,565.5, is still roughly

50% below its 2000 all-time high of over 5,000.

50TH

ANNIVERSARY OF THE S&P 500

From its March 1st, 1957 inception through the end of 2006, the

average annual return of the S&P 500 has been 10.83%. The S&P

500 comprises 83% of the value of all U.S. stocks. Almost 1,000

new companies have been added and deleted from the index since its

inception.

The materials and energy sectors made up half the value of the

original index, compared to 12% in 2007. By a wide margin, the best

performing stock has been Altria (formally Phillip Morris); from

March 1957 through the end of 2006, investors averaged 19.9%

annually. A $10,000 investment grew to $8.4 million (vs. $168,000

if the $10,000 had been invested in the entire index). Of the original

111 surviving companies, 20 outperformed the index by an average

of almost 5% per year.

5.4 STOCKS

QUARTERLY UPDATES

IBF | GRADUATE SERIES

SMALL CAP STOCKS

U.S. small company stocks with market capitalizations of less than

$3.5 billion have averaged 16.5% a year versus 12.2% for the S&P

500 over the past 30 years (ending 6/30/2006). As of the beginning

of 2007, small cap companies represented 78% of all listed

stocks in the U.S. (84% in Japan, 79% in Hong Kong, 74% in the

U.K. and 65% in France).

QUALIFYING DIVIDENDS

Legislation passed in 2004 cut the tax rate on “qualifying” dividends

to a maximum of 15%. For investors, “qualified” means that the

stock (paying the dividend) has to be owned by both the investor and

the mutual fund or ETF for at least 61 of the 121 days surrounding

the ex-dividend date. Income paid out by REITs and some overseas

companies do not qualify for this lower rate.

BUFFET WARNING

During the May 2007 Berkshire Hathaway annual meeting, Warren

Buffet repeated his warning about derivatives and leverage. Buffet

believes that derivatives are the “financial weapons of mass

destruction.” He expects that derivatives and the use of leverage by

traders, investors, and corporations will eventually end in huge

losses. According to Buffet, “The introduction of derivatives has

totally made any regulation of margin requirements a joke.”

STOCKS 5.5

QUARTERLY UPDATES

IBF | GRADUATE SERIES

DIVIDEND-PAYING BONUS

According to a Morgan Stanley report, from 1970 through 2005,

stocks that paid dividends averaged annual returns of 10.2%,

almost six percentage points ahead of non-payers. According to

S&P, 383 companies in the S&P 500 paid dividends in 2006,

compared with 351 in 2001. A decade ago, 427 out of 500 paid

dividends. The average payout ratio is just below 32%. Morgan

Stanley estimates that 40% of the S&P 500’s annual total returns

were from dividends for the period 1926 through 2004. Standard &

Poor’s reports that approximately one out of every nine stocks (59

total) in the S&P 500 has increased its annual dividend for at least 25

consecutive years as of the end of 2006.

VALUE PLAY

Suppose you wanted to buy a quart of milk. Last week you

bought a quart for $1.20. This week it is selling for $13.00 a

quart. How likely is it that you would buy a $13 quart of milk?

Yet, when it comes to buying stock, no one asks what the

“quart” (stock) used to sell for.

From the beginning of 2000 to the end of 2006, the average large

cap value fund had a cumulative return of just under 60%, versus

just 18% for the typical large cap growth fund. The Russell 1000

Value Index was up 22% in 2006, but only 6% of active large cap

value managers beat the index. Even though financial stocks

currently comprise 36% of the Russell 1000 Value Index, few active

money managers will devote that much to financials or any other

single sector.

QUARTERLY

UPDATES

VALUE VS.

GROWTH STOCKS

VALUE VS. GROWTH STOCKS 6.1

QUARTERLY UPDATES

IBF | GRADUATE SERIES

6.ROLLING PERIODS: GROWTH VS. VALUE

The table below shows the number of positive rolling three-year

periods, for different growth and value categories over the past 30

years, ending December 31st, 2006. Over a 30-year period, there are

28, three-year rolling periods.

Positive 3-Year Rolling Periods,

Growth vs. Value Stocks [1977-2006]

Category + Returns % +

Large Growth 25 / 28 yrs. 89%

Large Value 26 / 28 yrs. 93%

Mid Growth 27 / 28 yrs. 96%

Mid Value 28 / 28 yrs. 100%

Small Growth 27 / 28 yrs. 96%

Small Value 28 / 28 yrs. 83%

ALL GROWTH 25 / 28 yrs. 89%

ALL VALUE 26 / 28 yrs. 93%

The table below shows the number of positive rolling five-year

periods, for different growth and value categories over the past 30

years, ending December 31st, 2006. Over a 30-year period, there are

26, five-year rolling periods.

6.2 VALUE VS. GROWTH STOCKS

QUARTERLY UPDATES

IBF | GRADUATE SERIES

Positive 5-Year Rolling Periods,

Growth vs. Value Stocks [1977-2006]

Category + Returns % +

Large Growth 22 / 26 yrs. 85%

Large Value 25 / 26 yrs. 96%

Mid Growth 24 / 26 yrs. 92%

Mid Value 26 / 26 yrs. 100%

Small Growth 24 / 26 yrs. 92%

Small Value 26 / 26 yrs. 100%

ALL GROWTH 22 / 26 yrs. 85%

ALL VALUE 25 / 26 yrs. 96%

In summary, looking at both tables in this section, almost all of the

negative annual returns took place during the 2000-2002 stock

market meltdown. In the case of three- and five-year rolling periods,

all negative periods were the result of the same meltdown.

REVISITING GROWTH AND VALUE

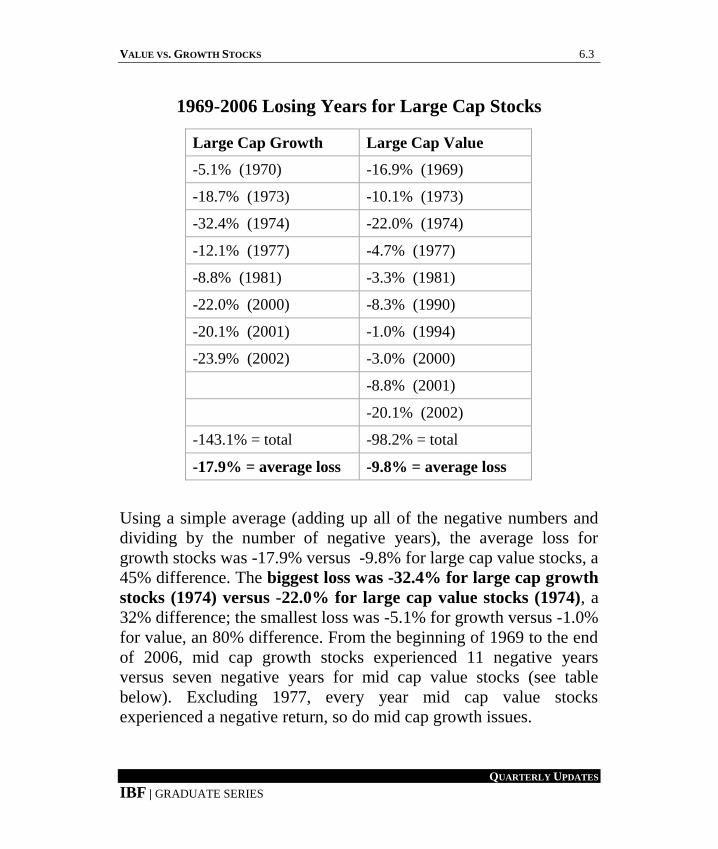

From the beginning of 1969 to the end of 2006, large cap growth

stocks experienced eight negative years versus 10 negative years for

large cap value stocks (see table below). Excluding 1970, every

year large cap growth stocks experienced a negative return, so

did large cap value issues.

VALUE VS. GROWTH STOCKS 6.3

QUARTERLY UPDATES

IBF | GRADUATE SERIES

1969-2006 Losing Years for Large Cap Stocks

Large Cap Growth Large Cap Value

-5.1% (1970) -16.9% (1969)

-18.7% (1973) -10.1% (1973)

-32.4% (1974) -22.0% (1974)

-12.1% (1977) -4.7% (1977)

-8.8% (1981) -3.3% (1981)

-22.0% (2000) -8.3% (1990)

-20.1% (2001) -1.0% (1994)

-23.9% (2002) -3.0% (2000)

-8.8% (2001)

-20.1% (2002)

-143.1% = total -98.2% = total

-17.9% = average loss -9.8% = average loss

Using a simple average (adding up all of the negative numbers and

dividing by the number of negative years), the average loss for

growth stocks was -17.9% versus -9.8% for large cap value stocks, a

45% difference. The biggest loss was -32.4% for large cap growth

stocks (1974) versus -22.0% for large cap value stocks (1974), a

32% difference; the smallest loss was -5.1% for growth versus -1.0%

for value, an 80% difference. From the beginning of 1969 to the end

of 2006, mid cap growth stocks experienced 11 negative years

versus seven negative years for mid cap value stocks (see table

below). Excluding 1977, every year mid cap value stocks

experienced a negative return, so do mid cap growth issues.

6.4 VALUE VS. GROWTH STOCKS

QUARTERLY UPDATES

IBF | GRADUATE SERIES

1969-2006 Losing Years for Mid Cap Stocks

Mid Cap Growth Mid Cap Value

-13.6% (1969) -18.6% (1969)

-6.4% (1970) -15.7% (1973)

-32.5% (1973) -20.9% (1974)

-33.1% (1974) -1.0% (1987)

-3.1% (1981) -15.6% (1990)

-6.1% (1984) -1.7% (1994)

-5.1% (1990) -12.8% (2002)

-2.3% (1994)

-18.5% (2000)

-7.2% (2001)

-21.5% (2002)

-149.2% = total -86.3% = total

-13.6% = average loss -12.3% = average loss

Using a simple average (adding up all of the negative numbers and

dividing by the number of negative years), the average loss for

growth stocks was -13.6% versus -12.3% for value stocks, a 10%

difference. The biggest loss was -33.1% for mid cap growth stocks

(1974) versus -20.9% for mid cap value stocks (1974), a 63%

difference; the smallest loss was -2.3% for growth versus -1.7% for

value, a 26% difference.

VALUE VS. GROWTH STOCKS 6.5

QUARTERLY UPDATES

IBF | GRADUATE SERIES

From the beginning of 1969 to the end of 2006, small cap growth

stocks experienced 11 negative years versus eight negative years

for small cap value stocks (see table below). Excluding 1998, every

year small cap value stocks experienced a negative return, so do

small cap growth issues.

1969-2006 Losing Years for Small Cap Stocks

Small Cap Growth Small Cap Value

-19.6% (1969) -19.1% (1969)

-13.7% (1970) -24.4% (1973)

-40.6% (1973) -20.4% (1974)

-28.9% (1974) -4.7% (1987)

-4.9% (1981) -18.7% (1990)

-7.4% (1984) -0.1% (1994)

-7.9% (1987) -4.1% (1998)

-16.3% (1990) -13.3% (2002)

-1.9% (1994)

-22.6% (2000)

-27.8% (2002)

-191.6% = total -104.8% = total

-17.4% = average loss -13.1% = average loss

6.6 VALUE VS. GROWTH STOCKS

QUARTERLY UPDATES

IBF | GRADUATE SERIES

Using a simple average (adding up all of the negative numbers and

dividing by the number of negative years), the average loss for

growth stocks was -17.4% versus -13.1% for value stocks, a 25%

difference. The biggest loss was -40.6% for small cap growth

stocks (1973) versus -24.4% for small cap value stocks (1973), a

40% difference; the smallest loss was -1.9% for growth versus -

0.1% for value, a 95% difference.

Conclusions Whether the comparison is between large, mid, or small cap

issues, value has suffered less than growth from 1969 through

2006; the average loss has been smaller. The largest losses were

always in growth and the smallest losses were always in value

stocks. In the case of mid and small cap stocks, the frequency of

losses has been greater for growth.

Adding up the cumulative returns of growth versus value from

1969 to the end of 2006, value has dramatically outperformed

growth (as shown in the table below); large value outperformed

large growth by almost 2-1, over 3-1 in the case of mid cap value

versus mid cap growth, and over 7-1 in the case of small cap

value versus small cap growth. As a side note, the standard

deviation for large, mid, and small cap value stocks has been

lower than their growth counterparts in the 1970s, 1980s, 1990s,

2000s, and from 1997 through 2006.

VALUE VS. GROWTH STOCKS 6.7

QUARTERLY UPDATES

IBF | GRADUATE SERIES

Growth of $10,000 from 1969 to the end of 2006

LC

Growth

LC

Value

MC

Growth

MC

Value

SC

Growth

SC

Value

$276,070 $539,470 $342,940 $1,429,090 $276,970 $2,338,810

From the beginning of 1928 through the end of 2006, $10,000

invested in small cap value stocks grew to $549,670,000 versus

$13,710,000 for small cap growth stocks (a margin of 39 to 1).

The same dollar invested in large cap value stocks grew to

$76,620,000 versus $9,740,000 for large cap growth stocks (a

margin of 6.7 to 1). Surprisingly, from 1928 through 2006, the

standard deviation for small cap value stocks was only slightly lower

than it was for small cap value stocks; the large cap growth stocks

has less risk (standard deviation of 20) than large cap value stocks

(standard deviation of 27) during the same period

SMALL CAP VALUE

Dartmouth finance professor Kenneth French and University of

Chicago economics professor Eugene Fama, who founded

Dimensional Fund Advisors (DFA) in 1981, developed the “Three

Factor Model” that questioned the validity of William Sharpe’s

capital asset pricing model (CAPM). DFA believes that tilting a

portfolio towards value and small cap stocks leads to better

performance over time. According to their historical studies, value

has outperformed growth by 5.1% annually since 1927.

6.8 VALUE VS. GROWTH STOCKS

QUARTERLY UPDATES

IBF | GRADUATE SERIES

GROWTH VS. VALUE

The table below shows the number of positive annual returns for

different growth and value categories over the past 30 years, ending

December 31st, 2006.

Positive Annual Returns

Growth vs. Value Stocks [1977-2006]

Category + Returns % +

Large Growth 25 / 30 yrs. 83%

Large Value 23 / 30 yrs. 77%

Mid Growth 23 / 30 yrs. 77%

Mid Value 26 / 30 yrs. 87%

Small Growth 22 / 30 yrs. 73%

Small Value 25 / 30 yrs. 83%

ALL GROWTH 24 / 30 yrs. 80%

ALL VALUE 25 / 30 yrs. 83%

VALUE VS. GROWTH STOCKS 6.9

QUARTERLY UPDATES

IBF | GRADUATE SERIES

2006 INDEX RETURNS

The tables below show returns for nine major indexes and the 10

Dow Jones industry groups for the 2006 calendar year.

2006 Index Returns

Index Return Index Return

DJIA 16.3% AMEX 16.9%

DJ World (excl. U.S.) 23.0% S&P 500 13.6%

DJ Wilshire 5000 13.9% Value Line 11.0%

NYSE Composite 17.9% NASDAQ 9.5%

Russell 2000 17.0%

2006 Dow Jones Industry Group Returns

Industry Group Return Industry Group Return

Basic Materials 16.1% Industrials 12.7%

Consumer Goods 12.5% Oil & Gas 20.3%

Consumer Services 13.5% Technology 9.5%

Financials 16.5% Telecommunications 32.2%

Health Care 5.7% Technology 9.5%

QUARTERLY

UPDATES

BONDS

BONDS 7.1

QUARTERLY UPDATES

IBF | GRADUATE SERIES

7.CUSHION AGAINST STOCK DECLINES

The table below shows the benefit of owning tax-free bonds during

stock market declines. From1986-2006, there have been four

instances when the S&P 500 has declined by 15% or more.

S&P 500 Decline

(high to low)

S&P 500

(with dividends)

Lehman Brothers

Municipal Bond Index

8-25-87 to 12-4-87 - 32.8% - 0.8%

7-16-90 to 10-11-90 - 19.2% - 1.4%

7-17-98 to 8-31-98 - 19.1% 1.8%

3-24-00 to 10-9-02 - 47.4% 25.1%

STOCKS VS. BONDS

Even though the 2000-2002 bear market represents the worst

cumulative drop in the S&P 500 over the past 50 years (-49%),

stocks still did better than bonds for the 10-year period ending

December 31st, 2006 (124% for the S&P 500 vs. 83% for the

Lehman Brothers Aggregate bond index).

7.2 BONDS

QUARTERLY UPDATES

IBF | GRADUATE SERIES

2006 HIGH-YIELD BOND FACTS

In 1980, slightly less than a third of U.S. industrial corporations

tracked by Standard & Poor’s were rated junk. By the late 1980s,

more than half were; the number increased to 71% by early 2007.

The S&P 500 includes 70 companies whose bonds are rated below

investment grade.

During the past 20 years, 4.5% of junk bonds have gone into default;

in 1991 and 2002, defaults were more than 10% of outstanding high-

yield bonds. The default rate was just 1.3% for 2006 (only 0.8%

according to Fitch). The table below shows that the number of

companies with high-risk credit ratings (BB or lower) has jumped

since 1980 (note: the table does not include utilities or financial

institutions).

Corporate Bond Ratings in 2006 vs. 1980

S&P Rating 1980 2006

AAA/AA 17% 2%

A 33% 9%

BBB 18% 18%

BB 22% 25%

B 7% 42%

CCC/D 3% 4%

BONDS 7.3

QUARTERLY UPDATES

IBF | GRADUATE SERIES

According to the Financial Times, 1.6% of global junk bond debt

defaulted in 2006; this is the lowest default rate experienced by

global junk bonds since 1981. The historical default rate for junk

bonds is 4.9% annually.

BOND MARKETS, INDEXES, AND FUNDS

The U.S. bond market more than doubled from $10.7 trillion in 1996

to $22.7 trillion by the middle of 2006. The Lehman Brothers

Aggregate Bond Index is comprised of more than 7,000 different

bonds, many of which are illiquid that fund managers cannot buy,

even if they wanted to. However, by copying some of the index’s

broad characteristics, such as sector exposure, interest rate

sensitivity and maturity, bond fund managers can end up with

portfolios that are very similar to the Lehman index.

Indices and averages are cost-free in the sense that their structure

and performance do not include any initial or ongoing costs such as

commissions, management fees, or bid-ask spreads. Since a mutual

fund incurs all of these costs, it can only beat an index by being

different. In the case of bond funds, increased credit risk, yield-curve

positioning, or emphasizing sectors or issues different from the

index are the only ways to outperform.

7.4 BONDS

QUARTERLY UPDATES

IBF | GRADUATE SERIES

R-squared reflects the percentage change of a fund’s fluctuation

that can be explained by the change in its benchmark index. A

fund that highly corresponds to its respective index has an R-squared

in the high 80s or 90s. For the 10-year period ending September

2006, only two of 15 funds with 10-year R-squareds of 98 or higher

outperformed the Lehman Brothers Aggregate Bond Index. Fund

expenses prevented the other 13 possible candidates from

outperforming the index. However, over the past three and five

years, the following funds have been able to outperform the Lehman

index even after taking into account trading costs and expenses:

Metro West Total Return, Dodge & Cox Income, Western Asset

Credit Bond Institutional, Fidelity Mortgage Security, TCW Total

Return Bond I, Harbor Bond Institutional, Fidelity Total Bond,

Managers Fremont Bond, PIMCO Total Return D, T. Rowe Price