i wish … i could understand how monkeys can pick up stocks in an efficient market!!!

DESCRIPTION

I wish … I could understand how monkeys can pick up stocks in an efficient market!!!. It is interesting to understand the concept of Efficient Markets. Now, I think I am getting about efficient markets. A Debate. In the last class, we started with the debate on Efficient Markets!!!!!!!!. - PowerPoint PPT PresentationTRANSCRIPT

I wish … I could understand how monkeys can pick up stocks in an efficient market!!!

It is interesting to understand the concept of Efficient Markets. Now, I think I am getting about efficient markets.

In the last class, we started with the debate on Efficient Markets!!!!!!!!

A Debate...A Debate...

First, we put argument FOR THE EFFICIENT MARKETS

Yes!!! Stock markets are efficient.

EFFICIENT MARKET ...

… … … … implies that as new information implies that as new information becomes available, it is becomes available, it is quickly quickly analyzedanalyzed by the market, and all by the market, and all necessary price necessary price adjustments occur adjustments occur rapidlyrapidly..

In an efficient security market, prices In an efficient security market, prices are determined so as to reflect all are determined so as to reflect all available economic information.available economic information.

A theory that puts forward A theory that puts forward

the idea and a framework the idea and a framework

related to Efficient Security related to Efficient Security

Market is popularly known Market is popularly known

as as EFFICIENT MARKET EFFICIENT MARKET

HYPOTHESISHYPOTHESIS ..

A theory that puts forward A theory that puts forward

the idea and a framework the idea and a framework

related to Efficient Security related to Efficient Security

Market is popularly known Market is popularly known

as as EFFICIENT MARKET EFFICIENT MARKET

HYPOTHESISHYPOTHESIS ..

EFFICIENT MARKETS ARE

HAVING DIFFERENT SHADES.

Fama has defined the following three forms of efficiency in a security market:

WEAK FORM OF EMH

SEMI - STRONG FORM OF EMH

STRONG FORM OF EMH

WEAK FORM MARKET WEAK FORM MARKET EFFICIENCY EFFICIENCY

A weak form efficient market hypothesis assumes that current share prices reflect all stock market information including the historical sequence of prices, price changes, trading volume, and any other market information.

This hypothesis implies: there is no relation between past prices and future

prices no trading rule that depends upon past share prices

can predict future share prices past prices do not provide any information that can be

used to outperform the market share prices follow random walk

SEMI-STRONG FORM SEMI-STRONG FORM MARKET EFFICIENCYMARKET EFFICIENCY

The Semi-Strong form efficient market hypothesis asserts that security prices adjust rapidly to the release of all new public information.

It means that the share prices reflect all public information.

This hypothesis implies that - it encompasses weak form hypothesis. If an investor acts on the basis of an information after

it has become public, then he can not derive above average profit.

The prices adjust either before the announcement or during the announcement but not after the announcement.

STRONG FORM MARKET STRONG FORM MARKET EFFICIENCYEFFICIENCY

Strong Form Efficient Market Hypothesis contends that stock prices reflect all information - public or private.

It implies that no group of investors has a monopolistic access to information relevant to formation of prices and thus, can not exploit it.

None can consistently derive above average profits.

It encompasses both weak and Semi-strong form of efficient markets.

It requires not only efficient markets but also perfect markets where all information is available to all investors.

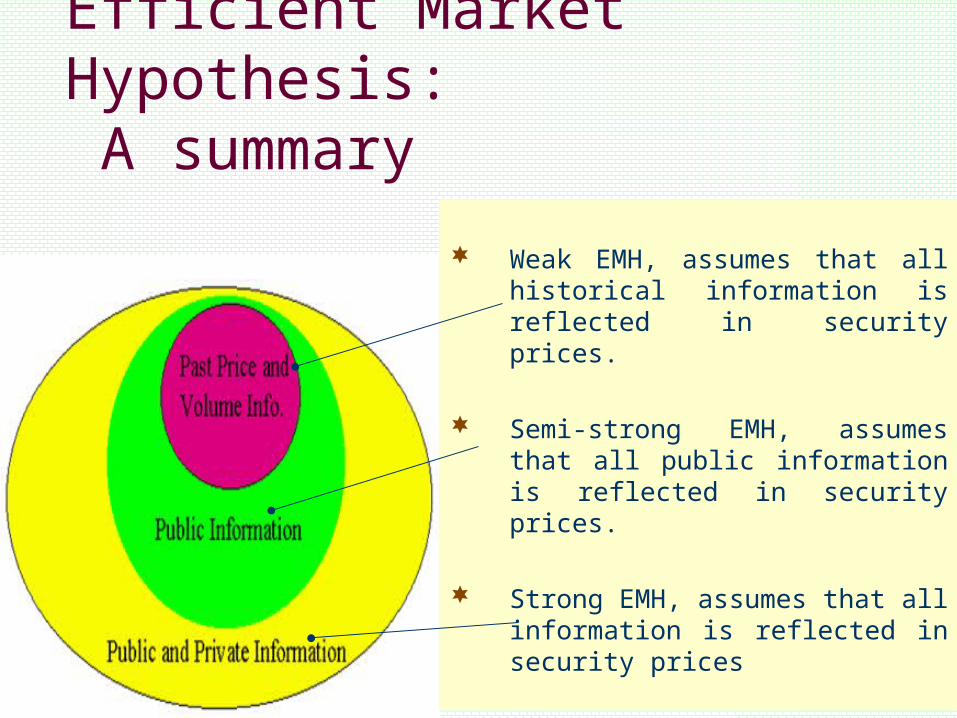

Efficient Market Hypothesis: A summary

Weak EMH, assumes that all historical information is reflected in security prices.

Semi-strong EMH, assumes that all public information is reflected in security prices.

Strong EMH, assumes that all information is reflected in security prices

Efficient Market Hypothesis: A summary (continued…)

Weak EMH

You cannot beat themarket by using historical information on prices & volumes.

Historical price &volumeinformation is reflected in the current price of stock.

Semi-Strong EMH

You cannot beat the market by using any public information.

All public information is reflected in the current price of stock.

Strong EMH

You cannot beat the market by using any public or private information.

All public & private information is reflected in the current price of stock.

If the markets are efficient, then simply

throw a dart and select a security !!!

But, will it be so simple???

What kind of investment strategy

under Efficient Markets…?

Two types of investment strategies are broadly identified:ACTIVE; and

PASSIVE.

If the market is efficient, then the PASSIVE Investment Strategy will be relevant.

One may use INDEX-FUND for investment purposes.

But, still an investment manager has a

role to play even in an efficient market.

Follow Passive Investment Strategies but still perform actively the following tasks-Ensure the correct amount of

diversification of the portfolio managed.

Maintain the desired level of risk of the

portfolio.

Try to minimize the transaction costs.

Try to seek tax advantages.

Innovate

Now, we put argument AGAINST THE EFFICIENT MARKETS

Yes!!! Stock markets are not efficient.

Evidence against EFFICIENT MARKETS….

There are certain evidences available which go against the concept of EMH and they are the sources of PUZZLINGPUZZLING those who believe strongly in EMH.

Believers of EMH say them as anomalies and hence, we shall be calling them as puzzling anomalies.

PUZZLING ANOMALIES

QUESTION EMH? These anomalies can be grouped

under the following heads:

1. SEASONAL ANOMALIES

2. EVENT ANOMALIES

3. FIRM ANOMALIES

4. ACCOUNTING ANOMALIES

5. MARKET ANOMALIES

SEASONAL ANOMALIES

SEASONAL ANOMALIES

These anomalies are associated with the calendar or time. The following are some of the seasonal anomalies.

a. January Effect

b. Day-of-the-week Effect

c. Time-of-the-day Effect

JANUARY EFFECT …

It is observed that the January Effect is tied to tax-loss selling at the end of the year. The hypothesis in this regard is that many people sell shares that have declined in price during the previous months to realize their capital losses so as to reduce the tax liability. And, the money realized is used to buy shares in the month of January. It is specially true for small-cap companies.

This effect is well documented by Jay R. Ritter in 1988 and he showed that the ratio of share purchases to sales of individual investors reaches an annual low at the end of December and an annual high at the beginning of January.

Day-of-the-Week Effect …

French (1980) originally observed that stock returns are higher on average on the last trading day of the week (Friday) and lower on the first (Monday).

After that, many studies document that the average return on Friday is abnormally high and the average return on Monday is abnormally low. This is known as the '' weekend effect'' or ''day-of-the week effect'' phenomenon.

Such an anomaly has also been observed even in India.

TIME-OF-THE-DAY EFFECT

On average, the market tends to be up in the first 45 minutes of trading and down in the last 15 minutes of trading.

EVENT ANOMALIES

EVENT ANOMALIES

These anomalies are associated with some easily identified events. The following are some of the event anomalies.

a. Insider trading effect

b. Analysts’ recommendations effect

INSIDER TRADING INSIDER TRADING EFFECTEFFECT

On average, stocks with high volume of purchases from insider tend to rise in price.

ANALYSTS’ RECOMMENDATIONS EFFECT

On average, a stock that is highly recommended by analysts tends to drop in price.

FIRM ANOMALIES

FIRM ANOMALIES

These anomalies are associated with firm-specific characteristics. The following are some of the firm anomalies.

a.Small firm (or Size) effect

b.Neglected firm effect

c.Institutional holding effect

SIZE EFFECT…

The Size Effect is also known as SMALL FIRM EFFECT.

Such an effect was originally documented by Rolf Banz in 1981 in US.

According to it, it was observed that the smallest-size firms portfolio outperforms the largest-size firms portfolio by an average of 4.3% annually even on a risk-adjusted basis.

Had there been an EFFICIENT STOCK MARKET, such anomalies could not exist.

NEGLECTED FIRM EFFECT

On average, stocks that are not closely followed by many analysts tend to yield higher returns than the ones that are.

INSTITUTIONAL HOLDING EFFECT

On average, stocks owned by only a

few institutions tend to provide higher

returns.

ACCOUNTING ANOMALIES

ACCOUNTING ANOMALIES

These anomalies are associated with the release of accounting information. The following are some of the accounting anomalies.

a. Small P/E effect

b. Earnings surprises effect

c. Dividend yield

SMALL P/E EFFECT…

S. Basu (1977) discovered that

portfolios of low Price/Earnings Ratio

shares have higher returns than

that of those portfolios having high

P/E Ratio.

It was found that the P/E Ratio Effect

holds up even if the returns are

adjusted for portfolio beta.

Such an anomaly has been

observed even in India.

EARNINGS SURPRISES EFFECTEARNINGS SURPRISES EFFECT

Earnings surprise is a relatively large deviation from an earnings forecast.

It has been observed that on the average, the prices of stocks with higher than expected earnings announcements tend to continue to rise even after the announcement.

And, this leads to an anomaly.

DIVIDEND YIELD EFFECT

Researches have suggested that cash dividend yields have a positive but marginally significant effect on the market value of equity shares which means that on average, stocks with high dividend yield tends to outperform stocks with low dividend yield.

Cash dividend effects of such kind

can be considered an anomaly in the efficient market theory.

MARKET ANOMALIES

MARKET ANOMALIES

These anomalies are associated with the market behaviour and market psychology. The following are some of the market anomalies.

1. Book Value to Market Value Ratio Effect

2. Reversal Effect

3. Market Momentum Effect

BOOK VALUE TO MARKET VALUE RATIO EFFECT…

Fama and French (1992) showed that a powerful predictor of returns across securities is the ratio of the book value of the firm’s equity to the market value of equity.

Their research have shown that the decile with the highest book-to-market ratio had an average monthly return of 1.65% (over the period July 1963 through December 1990), while the lowest-ratio decile averaged only 0.72% per month.

It indicates that the share with higher book-value to market value ratio are relatively under-priced.

REVERSAL EFFECT Debondt and Thaler (1985), and Chopra, Lakonishok and

Ritter (1992) found through their researches strong tendencies for poorly performing stocks in one period to experience sizable reversals over the subsequent period, while the best-performing stocks in a given period tend to follow with poor performance in the following period.

In brief, researches have shown “REVERSAL EFFECT” in which losers rebound and winners fade back over a period of time which means it is a long-term tendency.

The Reversal Effect would imply that a contrarian investment strategy should be profitable. It is believed that such a Reversal Effect takes place because returns shows a strong tendency of mean reversal.

MARKET MOMENTUM EFFECT Unlike the Reversal Effect, the Momentum

Effect means a tendency in the markets that a ‘good share’ will continue to perform better while a ‘bad share’ will continue to perform badly.

Researchers have believed that the markets show a strong tendency of momentum over a short horizon of time.

Jegadeesh and Titmen (1993) showed using 3- to 12- months holding periods that stocks exhibit a momentum property in which good or bad recent performance continues.

Even studies in India show the momentum property in Indian shares.

What can we say at the end about the

EFFICIENCY OF STOCK MARKETS???

An overly doctrinaire belief in efficient market hypothesis can paralyze the investor and make it appear that no research effort can be justified. Such an extreme view is probably

unwarranted. There are enough anomalies There are enough anomalies in the empirical evidence to justify the in the empirical evidence to justify the search for under-priced securities that search for under-priced securities that clearly goes onclearly goes on…………………….. ……………………..

Finally….

WHAT HAPPENED TO MONKEYS…!!??WHAT HAPPENED TO MONKEYS…!!??

You’re Fired!