hy 2016 - asx · hy 2016 results presentation a visionary adventure leisure company ... investor...

TRANSCRIPT

HY 2016 Results Presentation

A visionary adventure leisure company formed to build and operate world class indoor skydiving facilities across the region

For

per

sona

l use

onl

y

Disclaimer

2

This presentation has been prepared by Indoor Skydive Australia Group Limited (ISA Group) and provides general background information about the Company’s activities. That information is current at the date of this presentation. The information is a summary and does not purport to be complete. This presentation is not (and should be construed as) an offer, invitation, solicitation or recommendation with respect to the subscription for, purchase or sale of any security in any jurisdiction, and neither this document nor anything in it shall form the basis of any contract or commitment. The presentation is not intended to be relied upon as advice to investors or potential investors and does not take into account the investment objectives, financial situation or needs of any particular investor which need to be considered, with or without professional advice, when deciding whether an investment is appropriate.

ISA Group has prepared this presentation based on information available to it, including information derived from publically available sources that have not been independently verified. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, correctness or reliability of the information, opinions and conclusions expressed in this presentation.

Any statements or assumptions in this presentation as to future matters may prove to be incorrect and the differences may be material. This presentation should not be relied upon as a recommendation of or forecast by the Company. To the maximum extent permitted by law, none of the Company, its directors, employees or agents , or any other person accepts any liability, including without limitation, any liability arising from fault or negligence on the part of any of them or any other person, for any loss arising from the use of this presentation or its content or otherwise arising in connection with it.

The financial information disclosed in this presentation has been prepared on a statutory and pro forma basis consistent with the financial information prepared in the Company’s accounts. Due care and attention should be undertaken when considering and analysing the financial performance of the Company. All references to dollars are to Australian currency unless otherwise stated. The distribution of this presentation in jurisdictions outside Australia may be restricted by law and you should observe such restrictions.

For

per

sona

l use

onl

y

Contents 1. Overview

2. Results & Analysis 3. Strategy 4. Current Focus 5. Outlook 6. Summary 7. Appendices F

or p

erso

nal u

se o

nly

Utilisation Remains Strong: 66%

1. Overview

* Comprises Penrith iFLY Downunder Facility - iFLY Gold Coast opening post period end 4

Highlights

VWT Operations Revenue Contribution*: $3.6m

VWT Operational EBITDA Margin*: 55%

Cost of Sales Decreased

Delivery of Rollout continues – Gold Coast Opening

International IT Systems Development

Debt Facility in place

For

per

sona

l use

onl

y

Dec 2015 HY only (‘000)

June 2015 FY (‘000)

Dec 2014 HY only (‘000)

Consolidated Revenue $3,905 $6,588 $3,185

Consolidated EBITDA* $33 ($833) ($1,597)

Consolidated NPAT ($190) ($1,750) ($1,995)

VWT Operational EBITDA $1,992 $3,056 $1,269

Cashflow from operations $1,550 $683 $241

Net Tangible Assets/Share $0.24 $0.25 $0.25

2. Results & Analysis

* Reported EBITDA includes the effect of share based payments 5

For

per

sona

l use

onl

y

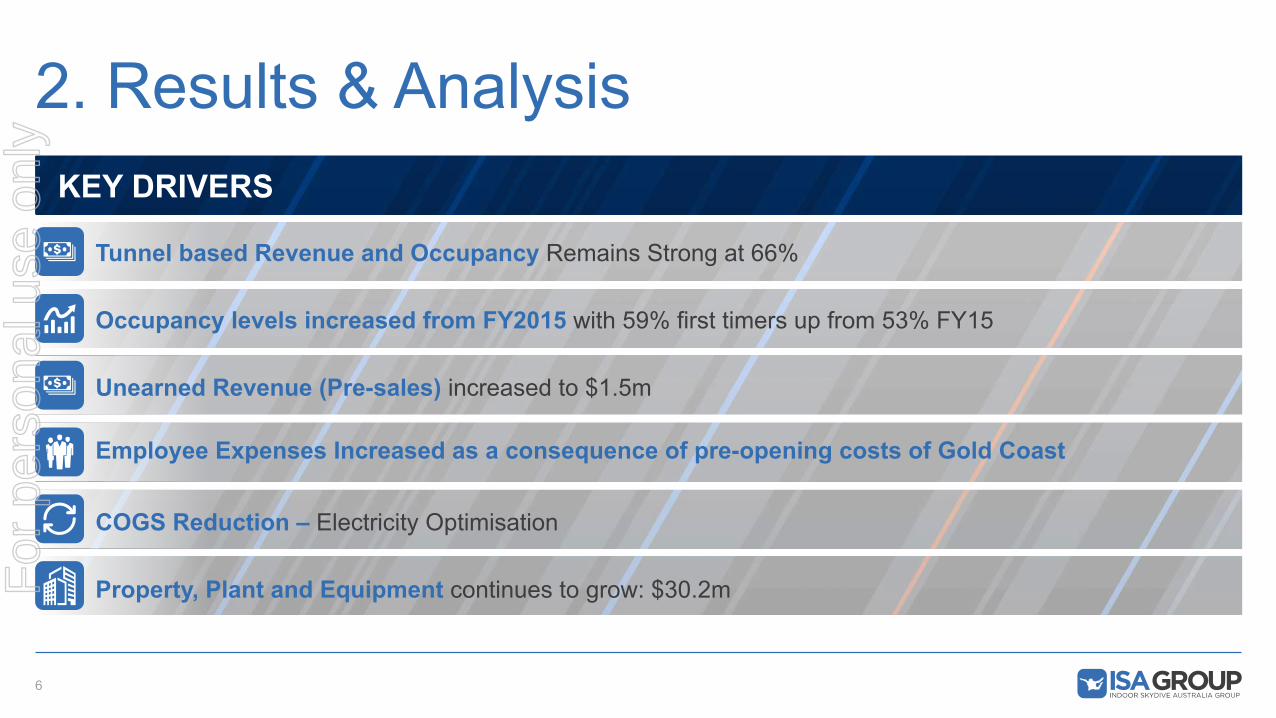

2. Results & Analysis

6

Tunnel based Revenue and Occupancy Remains Strong at 66%

Occupancy levels increased from FY2015 with 59% first timers up from 53% FY15

Unearned Revenue (Pre-sales) increased to $1.5m

COGS Reduction – Electricity Optimisation

Property, Plant and Equipment continues to grow: $30.2m

KEY DRIVERS

Employee Expenses Increased as a consequence of pre-opening costs of Gold Coast

For

per

sona

l use

onl

y

2. Results & Analysis

7

First timers Professional Groups / Events Merchandise

Average Weekday Revenue Mix Average Weekend Revenue Mix Average Weekly Revenue Mix

Unique Visitors – 20,790 (6 months)

For

per

sona

l use

onl

y

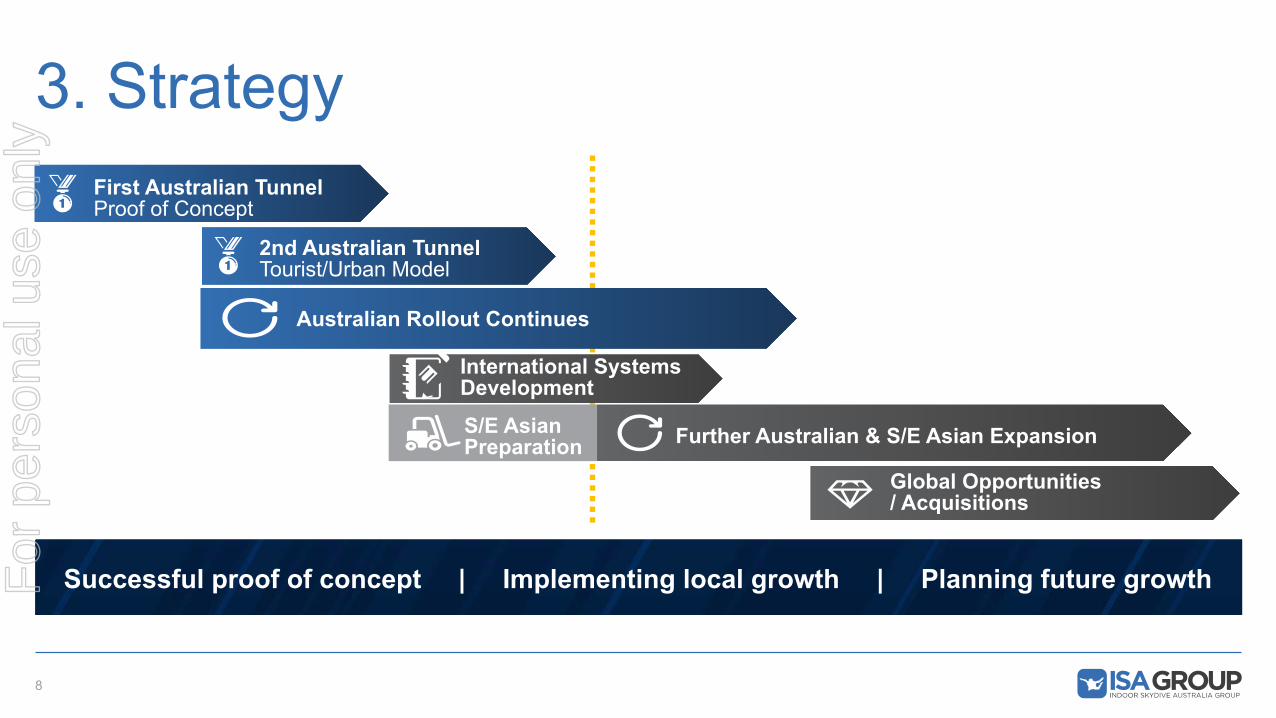

3. Strategy

8

Successful proof of concept | Implementing local growth | Planning future growth

First Australian Tunnel Proof of Concept

Australian Rollout Continues

International Systems Development

Global Opportunities / Acquisitions

S/E Asian Preparation Further Australian & S/E Asian Expansion

2nd Australian Tunnel Tourist/Urban Model

For

per

sona

l use

onl

y

4. Current Focus

9

§ Proof of Concept Sydney and Gold Coast

§ Growth in market segments

§ Business Model Blueprint

§ International capable IT Systems

Australian Tunnel Operations

§ Fabrication Complete

§ DA Approved

§ Site established

§ Early works to commence Mar 16

§ Open Last Qtr16 (construction risks)

Perth Construction

Contingencies: § Currency

§ Construction risk

§ Economic downturn

Managed by:

§ Project Timeline Management

§ Cost Management

§ Debt

Resulting in: § Growth Platform

§ Stable Operations

§ Economies of Scale

§ Corporate overhead absorption

Further Expansion § Additional Australian

Projects

§ Partnership Projects: Australia & NZ (SkyVenture Projects)

§ S/E Asia

§ Hong Kong

§ Acquisitions For

per

sona

l use

onl

y

10

Driving Performance 4. Current Focus

• 12ft Chamber • High foot traffic

location • International

Tourist • Corporate Events

• 16ft Chamber • Western Sydney • Specialist Military/

Professional • Skydiver Training

• 14ft Chamber • Highly Visible Site • 5 min from CBD • Opening late 2016

For

per

sona

l use

onl

y

5. Outlook – Global Industry

11

80+ Vertical Wind Tunnels in Operation World Wide*

20+ New Wind Tunnels Opened in 2015*

Global Growth of 50% expected in the next 12 months

Increased technology and efficiency as further credible manufacturers enter the market.

*Source - indoorskydivingsource.com

Proven Business Model – expanding successful operations world wide.

For

per

sona

l use

onl

y

6. Summary

12

Clear strategy for growth

Dynamic Board of Directors

Strong management team

Expertise in planning and execution

Proven to deliver

Flexibility in engagement / manufacturers / technology For

per

sona

l use

onl

y

7. Appendices

13

Stephen Baxter Non-Executive Director

Wayne Jones Director & Chief Executive Officer

Ken Gillespie AC, DSC, CSM Chairman

Danny Hogan MG Director & Chief Operations Officer

Malcolm Thompson Alternative Director for Stephen Baxter

David Murray AO Non-Executive Director

Indoor Skydive Australia Group Board

For

per

sona

l use

onl

y

7. Appendices

14

Brett Sheridan Chief Marketing Officer

Fiona Yiend General Counsel & Company Secretary

Danny Hogan Executive Director & Chief Operations Officer

Wayne Jones Executive Director & Chief Executive Officer

Stephen Burns Chief Financial Officer

Indoor Skydive Australia Group Executive Team

For

per

sona

l use

onl

y

7. Appendices

15

Wind Tunnels – Long Term, High Growth, Global Market – 15 Year CAGR 25%

Global Wind Tunnel Market – Installed Capacity

0

20

40

60

80

100

120

140

160

<1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Global Wind Tunnel Market - Installed Capacity

For

per

sona

l use

onl

y

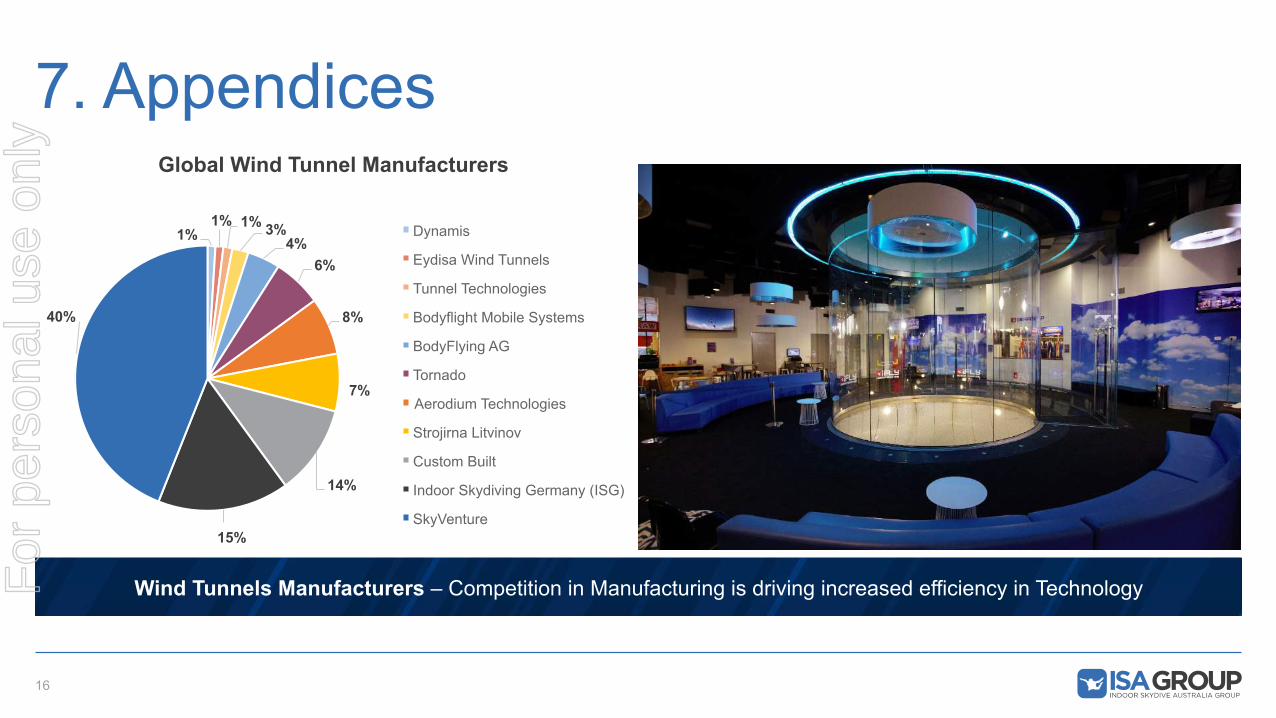

7. Appendices

16

Wind Tunnels Manufacturers – Competition in Manufacturing is driving increased efficiency in Technology

1% 1% 1% 3%

4% 6%

8%

7%

14%

15%

40%

Dynamis

Eydisa Wind Tunnels

Tunnel Technologies

Bodyflight Mobile Systems

BodyFlying AG

Tornado

Aerodium Technologies

Strojirna Litvinov

Custom Built

Indoor Skydiving Germany (ISG)

SkyVenture

Global Wind Tunnel Manufacturers

For

per

sona

l use

onl

y

7. Appendices

17

Strong Share Price Performance – Since listing in Jan 2013

-50%

-25%

0%

25%

50%

75%

100%

125%

150%

175%

200%

225%

250%

275%

300%

325%

350%

375%

400%

18-J

an-1

3

18-F

eb-1

3

18-M

ar-1

3

18-A

pr-1

3

18-M

ay-1

3

18-J

un-1

3

18-J

ul-1

3

18-A

ug-1

3

18-S

ep-1

3

18-O

ct-1

3

18-N

ov-1

3

18-D

ec-1

3

18-J

an-1

4

18-F

eb-1

4

18-M

ar-1

4

18-A

pr-1

4

18-M

ay-1

4

18-J

un-1

4

18-J

ul-1

4

18-A

ug-1

4

18-S

ep-1

4

18-O

ct-1

4

18-N

ov-1

4

18-D

ec-1

4

18-J

an-1

5

18-F

eb-1

5

18-M

ar-1

5

18-A

pr-1

5

18-M

ay-1

5

18-J

un-1

5

18-J

ul-1

5

18-A

ug-1

5

18-S

ep-1

5

18-O

ct-1

5

18-N

ov-1

5

18-D

ec-1

5

18-J

an-1

6

18-F

eb-1

6

Sha

re P

rice

mov

emen

t rel

ativ

e to

18

Jan

2013

Sha

re P

rice

(%)

IDZ CY13 - YTD CY16 Share Price Performance versus Index & Other Listed Consumer Discretionary Companies (Indexed to 18 Jan 2013)

IDZ VRL AAD Index - Consumer Discretionary (XDJ.ASX) Index - ASX 200 (XJO.ASX) Index - Small Ordinaries (XSO.ASX)

For

per

sona

l use

onl

y

Thank you

A visionary adventure leisure company formed to build and operate world class indoor skydiving facilities across the region

For

per

sona

l use

onl

y