hsbc holdings plc environmental, social and governance ......hsbc at a glance retail banking and...

TRANSCRIPT

HSBC Holdings plc Environmental, Social and Governance (ESG) UpdateSupporting sustainable growthApril 2018

Our cover imageThe Singapore Supertrees are a cluster of large tree-like structures constructed in the heart of Singapore. Many of the Supertrees are embedded with environmentally sustainable functions – including generating solar energy, collecting rainwater, and acting as vertical gardens with more than 150,000 plants. These innovative structures create a green respite in the centre of the urban centre.

Our photo competition winnersThe cover of this report showcases one of the images taken by one of our employees. The image was selected from more than 2,100 submissions to a Group-wide photography competition. Launched in June 2017, HSBC NOW Photo is an ongoing project that encourages our people to capture and share the diverse world around them with a camera.

Hong Kong Stock Code: 5

HSBC Holdings plcIncorporated in England on 1 January 1959 with limited liability under the UK Companies ActRegistered in England: number 617987

Environmental, Social and Governance (ESG) Update HSBC Holdings plc 2

Contents

1 Group Chief Executive’s statement 5

2 Customers 8

3 Employees 21

4 Supporting sustainable growth 28

5 Governance 37

6 Links and information 41

3Contents

About

The information set out in this document, taken together with the information relating to ESG issues detailed in our HSBC Holdings plc Annual Report and Accounts 2017 and the information available in the links below, aims to provide you with key ESG information and data relevant to our operations for the year ended 31 December 2017 and in order to comply with the Environmental, Social and Governance Reporting Guide contained in Appendix 27 to The Rules Governing the Listing of Securities on the Stock Exchange of Hong Kong Limited (‘ESG Guide’).

To the extent that we have not complied with the relevant provisions in the ESG Guide it is because we have chosen to focus on the issues that we consider are material to our stakeholders and on which we can have an impact. We will continue to develop and refine our reporting and disclosures on ESG issues in line with feedback received from stakeholders, and in order to comply with the ESG Guide.

Unless the context requires otherwise, ‘HSBC Holdings’ means HSBC Holdings plc and ‘HSBC’, the ‘Group’, ‘we’, ‘us’ and ‘our’ refer to HSBC Holdings together with its subsidiaries. Within this document the Hong Kong Special Administrative Region of the People’s Republic of China is referred to as ‘Hong Kong’. When used in the terms ‘shareholders’ equity’ and ‘total shareholders’ equity’, ‘shareholders’ means holders of HSBC Holdings ordinary shares and those preference shares and capital securities issued by HSBC Holdings classified as equity. The abbreviations ‘$m’, ‘$bn’ and ‘$tn’ represent millions, billions (thousands of millions) and trillions of US dollars, respectively.

Environmental, Social and Governance (ESG) Update HSBC Holdings plc 4

This ESG report, the third we have produced, outlines the measures we are taking to live up to our responsibilities today, and illustrates our ongoing commitment to open, honest and meaningful non-financial disclosure.

It covers a number of topics, from the way we engage with our employees and address their concerns, to our impact on the environment, and customer satisfaction across all our businesses.

It provides an update on metrics that we have disclosed previously, and also a number of new items. These include new commitments to extend education and employment-linked training, both for our employees and for one million people across the globe, and details of how we are applying advanced analytics and AI to improve our customer service and enhance our ability to fight financial crime. We are also meeting our reporting obligations under the terms of the UN Global Compact, and renewing our commitment to the Compact’s 10 principles.

There are areas of our ESG performance in which we have made genuine strides. We have transformed – and continue to strengthen – our ability to detect and deter financial crime. We have been a leading international voice in calling for better climate-related disclosure, while also making good progress in mitigating our own impact on the environment. We have materially improved the way we listen to customers, and have used that data to improve our services.

The report shines a light on those successes, but also highlights where we still have work to do. We are committed to improving aspects of our performance where we can and must do better.

We have much further to go in improving customer satisfaction and making it easier for our customers to work with us. We are now reporting on customer satisfaction in all four of our global businesses, and are working hard to make our services faster, less complex and more transparent.

There are also issues for us to tackle around conduct. We have remediation plans in place where work needs to be done, and we are investing heavily to ensure the necessary controls and processes are present and robust. More broadly, we continue to pursue the highest standards of conduct throughout the business.

We can also do better by our employees. Our disclosures highlight our progress, but there are still processes and ways of working that make it harder for all our people to do their jobs and fulfil their potential. We are committed to removing those barriers, and to making HSBC a more diverse and inclusive organisation – particularly at a senior leadership level.

It is critical we get these things right. Our future success is determined by our ability to address these issues and by our impact on people and the planet more generally.

As Group Chief Executive, my priority is to ensure HSBC meets its wider obligations and to set the highest standards of transparency. Where things are working, we will ensure standards do not slip. But where there is work to be done, we will do so with determination and clarity of purpose, and in a spirit of openness and honesty.

The views of our stakeholders will continue to be of paramount importance as we carry out that work, and as we strive to improve the quality and quantity of our non-financial disclosure. We will continue to listen and to learn, and to incorporate feedback into future Updates.

I hope you find this report helpful. John M Flint Group Chief Executive

Group Chief Executive’s statement

Throughout our 153-year history, HSBC has worked hard to meet its obligations to society and to help its customers and communities to thrive.

5Group Chief Executive’s statement

Our values define who we are as an organisation and make us distinctive.

We are open to different ideas and cultures, and value diverse perspectives.

We are connected to our customers, communities, regulators and each other; caring about individuals and their progress.

We are dependable, standing firm for what is right and delivering on commitments.

Open Connected Dependable

HSBC’s purpose and values

HSBC aims to be where the growth is, enabling business to thrive and economies to prosper, and ultimately helping people to fulfil their hopes and realise their ambitions.

Environmental, Social and Governance (ESG) Update HSBC Holdings plc 6

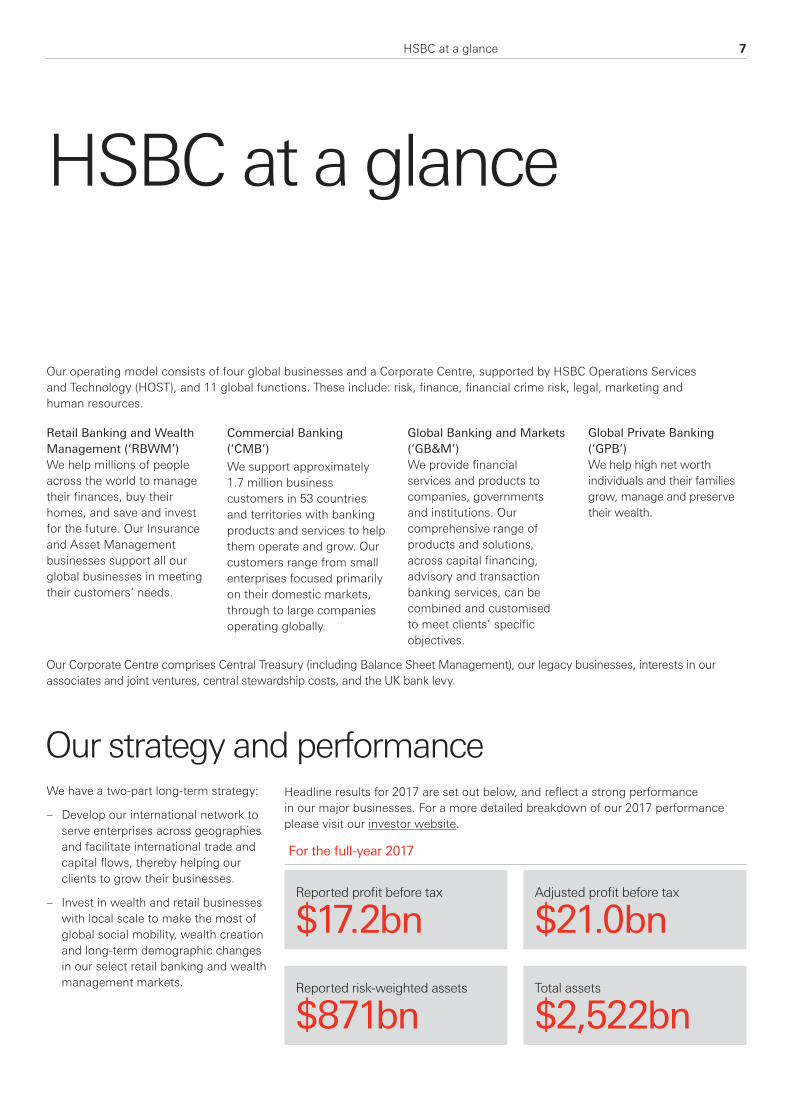

HSBC at a glance

Retail Banking and Wealth Management (‘RBWM’)We help millions of people across the world to manage their finances, buy their homes, and save and invest for the future. Our Insurance and Asset Management businesses support all our global businesses in meeting their customers’ needs.

Our strategy and performance

Commercial Banking (‘CMB’)We support approximately 1.7 million business customers in 53 countries and territories with banking products and services to help them operate and grow. Our customers range from small enterprises focused primarily on their domestic markets, through to large companies operating globally.

Global Banking and Markets (‘GB&M’)We provide financial services and products to companies, governments and institutions. Our comprehensive range of products and solutions, across capital financing, advisory and transaction banking services, can be combined and customised to meet clients’ specific objectives.

Global Private Banking (‘GPB’)We help high net worth individuals and their families grow, manage and preserve their wealth.

We have a two-part long-term strategy:

– Develop our international network to serve enterprises across geographies and facilitate international trade and capital flows, thereby helping our clients to grow their businesses.

– Invest in wealth and retail businesses with local scale to make the most of global social mobility, wealth creation and long-term demographic changes in our select retail banking and wealth management markets.

For the full-year 2017

Reported profit before tax

$17.2bnReported risk-weighted assets

$871bn

Adjusted profit before tax

$21.0bnTotal assets

$2,522bn

Headline results for 2017 are set out below, and reflect a strong performance in our major businesses. For a more detailed breakdown of our 2017 performance please visit our investor website.

Our operating model consists of four global businesses and a Corporate Centre, supported by HSBC Operations Services and Technology (HOST), and 11 global functions. These include: risk, finance, financial crime risk, legal, marketing and human resources.

Our Corporate Centre comprises Central Treasury (including Balance Sheet Management), our legacy businesses, interests in our associates and joint ventures, central stewardship costs, and the UK bank levy.

7HSBC at a glance

Customers

We are working to make things simpler, faster and better for our customers. We conduct research and invest in technology to analyse and anticipate emerging market trends. However, listening to customers and asking their opinion on our service is core to understanding their needs and concerns.

This section discusses customer satisfaction across our four global businesses, and highlights the actions we are taking to drive continuous improvement. See Figure 1 for a breakdown of customer numbers and profits generated.

Taking responsibility for the service we provide We define conduct as delivering fair outcomes for customers and not disrupting the orderly and transparent operation of financial markets. As stated in our Annual Report and Accounts 2017, operating with high standards of conduct is central to our long-term success and ability to serve customers. We have clear policies, frameworks and governance in place to protect them. These cover the way we behave, design products and services, train and incentivise employees, and interact with customers and each other. Our Conduct Framework guides activities to strengthen our business and increases our understanding of how the decisions we make affect customers and other stakeholders.

Details of our Conduct Framework are available at www.hsbc.com, and more information on our legal proceedings and regulatory matters can be found in Note 34 of the Annual Report and Accounts 2017.

121

301

299

16

6.5

Adjusted profit before tax ($bn)

Adjusted risk-weighted

assets ($bn)

6.8

5.8

0.3

37m

Number of customers

(approx.)

RBWM

1.7mCMB

4,100GB&M

45kGPB

For further details, see Annual Report and Accounts 2017

Executive summary We have made significant improvements to the way we listen to customers and their feedback has helped improve our products and services. However, there’s more we can do to simplify processes, improve the digital experience and ensure we deliver fair outcomes to all our customers. We will continue delivering on our conduct agenda in Global Banking and Markets to ensure all employees live up to our high standards. In addition, we remain committed to resolving outstanding investigations stemming from former practices within Global Private Banking.

Figure 1: details of our customer groups

Environmental, Social and Governance (ESG) Update HSBC Holdings plc 8

Acting on customer feedback has helped make our services more accessible and transparent. It has also prompted us to streamline and improve our processes, which provides customers with a better experience.

Below, we have highlighted some examples of how customer feedback has driven improvements across our four global businesses. The following sections explore the approach taken in each of the businesses in more detail.

Acting on feedback

1 Making banking more accessibleRBWM customers said:

Logging on to our online and mobile banking was too complex.What we did

Made it easier for customers to access their accounts, while ensuring robust security. For example:

– we have introduced biometric (Touch ID & Voice ID) verification to make it easier for customers to access their accounts, with 40% of logins not requiring passwords

– we are providing specialised training to our people so they can better support customers using digital banking and give them advice about how to access accounts and keep them secure

2 Making fees and charges transparentRBWM customers said:

It was sometimes difficult to understand when and why they would be charged for our services.What we did

We enhanced our direct communication with customers to help them understand their finances and avoid fees and charges:

– in the UK we have sent customers more than 600,000 overdraft alerts and 500,000 advance warnings of possible fees

– RBWM complaints in this area fell by 5% in 2017

CMB customers said:

They were not satisfied with our rates and charges.What we did

Improved transparency and introduced clearer communications, resulting in a 37% reduction in complaints in this area. Examples of improvements:

– balances are now displayed more clearly on Business Internet Banking

– in the UK, we have introduced an automatic retry process for un-cleared cheques to help customers avoid charges due to insufficient funds in accounts

3 Tackling complexityRBWM customers said:HSBC’s processes and procedures were too complicated.What we did

Changed the way we operate to make banking easier. For example:

– in the UK, we have made it an easier process for people to get a mortgage – reducing the application period from five weeks to two weeks

– we have implemented Live Sign which gives customers the ability to sign and agree documents electronically

– in Hong Kong, 99% of accounts are now opened via an employee tablet in branch

CMB customers said:

It took too much time to complete tasks, such as opening an account. What we did

Continued to streamline our processes. For example, we have:

– launched an online tool for Know Your Customer (KYC) so small businesses without Relationship Managers can provide the information needed for regulatory checks without visiting a branch

– introduced a simpler registration process for HSBCnet and better customer support through virtual assistant and Live Chat

GB&M customers said:

Our processes could be frustrating and time-consuming.What we did

Assembled dedicated teams to make processes simpler, better and faster. For example:

– our new ‘confirmation.com’ platform lets our customers and their auditors obtain annual balance confirmations from our branches worldwide on a single platform, simplifying a previously labour-intensive annual process. It has been trialled in key countries and will be rolled out globally in 2018

– in the UK, Global Banking employees can now use ‘MyDeal’ to access key information in real-time, and in one place, when working on Debt Capital Markets and Equity Capital Markets deals – freeing them up to spend more time with customers

GPB customers said:

The due diligence related to opening and maintaining customer accounts was complicated.What we did

We are working to improve the customer experience, by:

– simplifying and digitising the paperwork for opening accounts

– examining whether and how we are able to share, with customer permission, Know Your Customer data across business lines

9Customers

Retail Banking and Wealth Management (RBWM) strives to build long-lasting, trusted relationships with our customers. We know we can only achieve this by understanding what is important to them and using this insight to improve the banking service we offer.

How we listen to our customersWe use a number of sources to listen to our customers, in order to get the clearest picture of the experience we deliver.

Customer recommendation surveysIn 2017, we surveyed two million customers on how likely they were to recommend HSBC as a bank to their friends and families, as well as their satisfaction with our various channels. Additional technologies have helped this understanding. For example, we now have Speech Analytics in 19 markets, providing real-time insight on customers’ experiences of our contact centres.

In 2017, we saw an increase in customers likely to recommend us. Improved customer service, particularly in how we take ownership of problems and provide user-friendly interactions, have been key contributors to our performance. Customers are also increasingly recommending us for understanding them, especially their goals and ambitions (see Figure 2).

While we are recommended for being easily accessible in the UK and Hong Kong, this remains an area of focus in markets where we have less presence. We will continue improving and promoting alternative ways to interact with customers.

Retail Banking and Wealth Management

Recommendation scores*

2017 2016

UK 62 50

Hong Kong 61 39

France 68 47

US 57 52

Canada 56 49

Mexico 92 84

Singapore 63 52

Malaysia 79 79

China 81 91

UAE 88 79

Figure 2: RBWM customer recommendation

Between 2016 and 2017, the methodology used to survey consumers has changed in a number of markets. Surveys have now migrated from telephone to email, which is a contributing factor to the large change in the results between 2016 and 2017.

*% of customers providing an 8 or above score out of 10. This is an indication of how likely they are to recommend HSBC.

With 70% of business owners using the same bank for their business and personal finances, we saw an opportunity to better serve and grow the relationship for those managing firms with turnovers between $3m and $5m.

To ensure we built a proposition around their specific needs, we spoke to more than 1,600 customers in nine markets through interviews, focus groups and surveys. It revealed that personal and business lives were blended for small business owners – and they wanted this recognised by their bank. This resulted in HSBC Fusion.

HSBC Fusion is a dedicated banking service that gives customers greater control over their business and personal finances. This includes access to funding, advice and new opportunities, such as a centralised user experience for online banking and a new mobile app for easy access to administrative tools for accounting, taxes and expense management. HSBC Fusion was launched in 2017 in Malta, Mexico and China, and is expected to launch in a further five markets this year.

HSBC FUSION

Environmental, Social and Governance (ESG) Update HSBC Holdings plc 10

Customer satisfaction surveysSince 2016, satisfaction levels in branch have improved. In 2017, Relationship Management maintained or improved generally high satisfaction levels, while those in contact centres and online banking have declined (see Figure 3).

The decline in satisfaction in our online banking service and contact centre is due to the launch of a new global online banking system and enhanced security features. We invested in the new system to support the increased demand for digital services as the ways in which our customers interact with us, and their expectations for ease and range of functionality, is changing. This has resulted in a fall in the use of our branches and contact centre contact, and an increase in the use of digital.

However, the pace of change resulted in higher complaints. Our online banking and contact centres were under pressure due to a higher than normal volume of calls.

Branch Contact centre Relationship Manager Online banking

2017 2016 2017 2016 2017 2016 2017 2016

% of customers providing an 8 or above score out of 10*

UK 86% 86% 70% 71% 79% 75% 71% 81%

Hong Kong 87% 83% 90% 96% 71% 71% 49% 63%

France 74% 74% 68% 74% 70% 68% 72% 75%

US 87% 85% 72% 63% 80% 80% 57% 66%

Canada 82% 84% 66% 73% 85% 86% 34% 56%

Mexico 90% 89% 82% 81% 91% 93% 81% 82%

Singapore 73% 63% 88% 87% 62% 62% 46% 54%

Malaysia 71% 69% 64% 70% 73% 67% 61% 63%

China 93% 91% 94% 96% 73% 77% 46% 60%

UAE 70% 69% 66% 71% 66% 62% 69% 70%

*2016 Contact centre scores were measured on a 5 point rating scale, this was changed to an 11 point rating scale in 2017 with the exceptions of the US, Canada and Singapore.

Figure 3: RBWM customer satisfaction scores

We have learnt from this and have invested to support our call centres to ensure they are well trained to help our customers. We are now seeing satisfaction improve as we continue to provide support and updates to our customers.

While contact centre customer satisfaction has either declined or remained stable, overall dissatisfaction with contact centre accessibility and time to answer calls has improved. We are investing significantly to respond to new customer needs driven by greater digital capabilities. All our contact centre employees are receiving new training and support under the banner of ‘customer obsessed’, with a greater focus on coaching and development, quality improvement, and problem resolution. Our priority in 2018 is to resolve more problems the very first time customers get in touch.

11Customers

Figure 5: RBWM complaint themes

Process and procedures44%

Other* 23%

Service21%

Fees and charges10%

Product features and benefits2%

2016 36%

2016 22%

2016 27%

2016 12%

2016 3%

*including PPI complaints in the UK

When things go wrong We ensure customers’ complaints are recorded and understood to learn what has gone wrong and why. The ways in which we deal with complaints - and the speed they are resolved - can also make a big difference to customers.

RBWM received approximately one million complaints in 2017 from our ten largest markets. This was a 6% increase in volume from 2016, with complaints as a percentage of customer base now at 3.6%. Higher complaint volumes were driven in part by the launch of the new global online banking system, discussed in the prior section. The key complaint themes related to process and procedures, service, and fees and charges (see Figures 4 and 5).

In 2017, we resolved 71% of all complaints on the same or next working day (excluding UK PPI complaints). We use insight gathered from complaints and analysis of the root causes to drive improvements in our markets.

Taking responsibility for the experience we deliver We have clear procedures and governance in place to support our customers. Senior leaders have ultimate responsibility and are held accountable for customer service standards. These are monitored through key metrics aligned to performance objectives that target the delivery of fair outcomes and experiences for our customers.

In 2017, through our conduct programme we identified and embedded changes to enhance our approach to understanding our customers. These included:

– Launching new procedures to ensure potentially vulnerable customers are correctly identified and supported.

– Launching new conduct training for all global product managers.

– Enhancing the way we capture and analyse customer exit reasons to improve our products and services, and rebuild customer relationships.

Products designed with customers in mindWe assess product and pricing changes against a global customer-focused framework, which provides improved consistency and clarity for our customers. In 2017, there were 156 new products and 119 feature or channel changes in our markets that were approved globally. This included two new lower carbon funds by Global Asset Management which will be delivered in 2018.

Delivering the right products requires giving suitable training and tools to those designing the solutions. With this in mind, we have launched the Product Management Academy which has delivered training to more than 700 of our people more than 30 countries to ensure a consistent approach to embedding customer thinking in the design process.

Figure 4: RBWM annual complaint volumes – top 10 markets

Market Complaint volumes (000)

Complaints per 1,000 customers per month

2017 2016 2017 2016

UK* 457.7 511.8 3.3 3.5

Hong Kong 41.5 43.3 0.7 0.7

France 60.2 63.9 6.0 6.6

US 53.8 47.0 3.4 2.6

Canada 24.9 16.9 2.7 1.8

Mexico 357.3 252.4 4.5 3.8

Singapore 10.8 6.6 1.6 0.9

Malaysia 5.5 10.0 0.5 0.8

China 4.3 3.5 0.7 0.8

UAE 26.6 32.1 6.8 7.8

*Based on Financial Conduct Authority definitions and including First Direct.

A complaint is defined as ‘any expression of dissatisfaction, whether up-held or not, from (or on behalf of) a former, existing or prospective customer relating to the provision of, or failure to provide, a specific product or service activity’.

Environmental, Social and Governance (ESG) Update HSBC Holdings plc 12

In 2017, HSBC introduced new software to support our social media listening with improved global capabilities. The platforms give us:

– Access to global social media content from a variety of sources, getting us closer to feedback from customers and helping understand our competitor and brand position.

– The ability to engage real-time with customers, helping us to identify, understand, and resolve issues, and feedback to customers on what we’ve done.

– Analytical capabilities to research publicly available social media data, gaining insights that can influence business decisions and develop thought leadership.

SOCIAL MEDIA LISTENING

Our contenthas been‘liked’

active

Wehave

socialmedia

accounts

122

131kposting

we have receivedinboundmessages500k

257k

pieces of contentin 2017

2.8 million & and responded to

queries81kSHARED

times

times

Figure 6: investing in digital

$2.3bn

41% of RBWM

in digital transformation across our global businesses between 2015-2017

Globally

We have invested

customers are digitally active

FIVE YEARS

333%Over the past

we have seen a

increase in mobilebanking customers

The future of digital banking MobileAn increasing number of customers prefer to do their banking digitally. We are continually enhancing the features on our mobile banking apps by listening to customer demand and tailoring services for each market in which we operate. The new mobile banking app satisfaction ratings are strong in the UK and Hong Kong with both achieving 4.7 out of 5 on the Apple App store. Our strategy is to look at global technology trends in multiple markets and to invest in the technologies that will be most beneficial to customers.

Digital messagingWe are providing more personalised, tailored and relevant messaging through digital and non-digital channels.

We can determine when customers are searching on our website for solutions to their financial needs, and provide real-time digital messages to assist. These messages can be personalised based on our deep customer understanding and distributed across multiple channels in a coordinated and automated way. Features such as nudges or push notifications are also used to keep customers updated on their enquiries, while reducing effort and providing financial guidance. These types of messages will help support customers through key journeys across products and propositions. This has already been used in the UK with 300,000 online banking messages sent in 2017, helping customers who have attracted banking charges in the last 12 months to avoid fees in the future.

FINTECH PARTNERSHIPS

HSBC is working with fintechs to make banking simpler, better and faster for customers. We have allocated $200m to invest in fintech and enterprise start-ups, and have a number of successful partnerships.

We have also supported The FinTech Innovation Lab since 2013 and participate in Hong Kong, London, Dubai and New York. This programme invites entrepreneurs to pitch their financial technology (fintech) ideas to banks. The bank works with shortlisted entrepreneurs during a 12 week mentoring programme.

Artificial intelligenceUsing artificial intelligence and machine learning, the customer journey is being improved with a more personalised service. This technology will also help us to engage with our customers in a more timely, accessible and relevant manner. For example, advance analytics is used to predict which customers using online banking may call the contact centre. We can pre-empt this with in channel assistance (Live Chat) to reduce customer effort and provide immediate assistance.

13Customers

Financial inclusionIn Hong Kong, we have trained branch employees in basic sign language skills and produced a series of simple guides to help senior citizens adapt to the new Internet Banking platform.

Improvements to our mobile app Easy Invest have earned us a 2017 Good Practice Award in Hong Kong from the Design for All Foundation, a not-for-profit international body. The app has accessibility features and assistive technology on mobile devices.

We have deployed more than 2,600 talking ATM machines globally. These enable our visually impaired customers to transact through connected headphones, with the instructions being read out to them. Most notably, in the UK, USA, Australia and India, we provide this talking functionality at every HSBC ATM.

The UK was selected as a finalist in the Financial Innovation Awards 2017, under ‘Best Financial Inclusion Initiative’ category for offering Video British Sign Language (BSL) Interpretation and Relay Service to our customers. Since its launch a year ago, the service has been used more than 700 times by our BSL communicating customers. This is a success in improving some of the key journeys our customers experience, such as mortgage applications and fraud interactions.

Financial well-being We have developed a global programme to improve awareness among customer-facing employees of the appropriate money advice solutions to assist customers with financial difficulty. The programme helps identify customers in need of additional support and directs them to the most appropriate area to meet their needs.

We are delivering financial well-being seminars to help increase financial capability. These seminars provide guidance on establishing and maintaining a budget, information on savings, and education on frauds and scams.

In Singapore, we launched a debt consolidation programme to help consumers combine outstanding balances from their existing unsecured credit facilities, enabling them to save on interest.

HSBC actively supports the ‘Take Five to stop Fraud’ initiative in the UK, which raises awareness of the techniques used by fraudsters. We have implemented messages in the new beneficiary set up process to help protect customers’ personal data.

To learn more about our commitment to increasing financial capability, see page 33.

Diversity and inclusionWe have seen changes to traditional family structures, such as de facto relationships where a growing number of people in society choose to delay marriage or not get married. In some markets there remains a misalignment in the cover the insurance industry is able to provide to customers, particularly regarding relationship status and financial dependants. Our country teams are reviewing existing products while working within legal and regulatory environments.

In Hong Kong, our travel and medical products offer a family discount to married couples, same sex partners, and de facto relationships. In Singapore, our travel policy now recognises partner relationships (same sex and de facto), while in the UK and Mexico we expanded the definition of children to more broadly cover financial dependants. This enables adopted children and foster children to be beneficiaries. In the UK, we have also introduced gender neutral titles to reflect societal changes.

We are in the process of expanding this work in our other product lines in RBWM.

Supporting customers As part of our ambition to support and protect customers, we are working on a number of initiatives.

Environmental, Social and Governance (ESG) Update HSBC Holdings plc 14

Commercial Banking (CMB) serves the full range of businesses from start-ups to large corporates and operates in 53 markets. We serve approximately 1.7 million customers globally who typically operate internationally, or aspire to do so, and value HSBC’s global network and connectivity.

How we listen to our customersWe have increased our listening capabilities by improvingexisting insight programmes and introducing software and tools to help us stay better connected with customers. Our insight includes complaints analysis and social media.

‘Moments of Truth’ surveysCMB continued the roll out of event driven surveys in 2017. This is an ‘always-on’ approach to gathering customer feedback about key interactions such as the account opening experience, initial set-up and usage of HSBCnet, interactions with our Global Trade and Receivables Finance teams, applying for Credit, and when Relationship Managers change.

We gather scores and comments to identify issues needing action and track key performance indicators to measure the impacts of changes made. We now have more than 90 surveys live, spanning 35 markets.

In 2017, we gathered feedback from more than 8,000 customers and have completed 20 improvements, with a further 55 underway, focused on the customer experience across these key interactions. This has resulted in improved customer satisfaction. See the case study for an example of how this approach has improve the customer experience.

Online panelsWe have implemented online customer panels that have more than 200 active members in the UK, Hong Kong, China, Australia, UAE, Mexico and the US. These provide fast feedback, allowing us to make improvements to the layout and functionality of our digital services. In 2017, they helped us improve the customer on-boarding experience, integrate accounting software, review digital lending, upgrade our mobile app, trial video conferencing, and even change the way we communicate with customers.

Commercial Banking

The ‘Moments of Truth’ survey highlighted issues with the account opening process as only 25% of customers in India rated it as ‘Excellent’. Analysis revealed the main cause of dissatisfaction was how long it took to open an account. An internal review highlighted some delays were caused by multiple internal checks. A pilot to streamline the process and consolidate checking brought this down from up to 25 days to four days. The ‘Excellent’ rating in India subsequently increased to 67% by the end of 2017.

INDIA – NEW ACCOUNT OPENING

CASE STUDY

Taking responsibility for the experience we deliver CMB’s formal Conduct Programme concluded in 2017 and the resulting governance, frameworks, policies and communications are now embedded. Conduct metrics measuring potential impacts on our customers and markets are regularly reviewed and appropriate actions taken. For example, sales quality testing results are closely monitored to ensure that the products and services offered to customers meet their needs.

There is ongoing training for all employees, and both established and evolving governance, to highlight customer issues in decision-making forums. Pricing and billing continues to be an area of focus to ensure a balanced exchange of value with our customers. A Global Pricing Executive Committee has been established and a new global pricing framework will be introduced. Effective communications are core to ensuring all employees understand how to deliver our conduct commitments.

Examples of employees making the right decisions in the interests of customers during 2017 featured in articles and broadcasts across internal communications channels. These stories, supported by online training, newsletters and globally broadcast talks by internal and external speakers on various Conduct issues, will continue in 2018.

15Customers

Figure 7: CMB annual complaint volumes (000) – top 8 markets

2017 2016

UK* 43.1 37.8

Hong Kong 4.1 3.2

Asia Pacific 1.1 1.2

Europe 4.8 6.6

Middle East and North Africa 1.8 2.4

Latin America 1.2 1.2

US 1.2 0.9

Canada 0.4 0.8

*Volumes for the UK are received complaints from eligible complainants aligned to the current FCA reporting. Volume of complaints for all other markets, complaint reason breakdowns and commentary are based on total volumes of resolved complaints.

Others29%

Operations26%

Contact centre12%

Internet banking6%

Branch8%

Fees, rates and charges7%

2016 32% 2016 10%

2016 25% 2016 10%

2016 10%

Processes and procedures12%

2016 5%

2016 8%

Figure 8: CMB complaint themes

When things go wrongIn 2017, CMB handled more than 57,000 complaints – a 7% increase on 2016 - with 75% coming from customers in the UK, 7% in Hong Kong and 7% in France. Operational complaints remained the highest in volume and these are related to the regular transactions that our customers do most frequently - like making payments and changing the details of their accounts. Complaints arise when we are too slow or make mistakes.

The largest increase in complaints was related to our requests for customers to provide more information about themselves and their businesses as part of more rigorous procedures implemented by the bank to prevent financial crime. If customers don’t provide the details needed, we sometimes restrict their use of our services. In certain cases their accounts will be closed to guard against the risks of fraud and money laundering.

As well as addressing the root causes of the complaints, we are rolling out a global online training programme aimed at customer-facing teams. The training improves our ability to recognise complaints and emphasises the importance of recording, understanding and resolving them (see Figures 7 and 8).

Environmental, Social and Governance (ESG) Update HSBC Holdings plc 16

Figure 9: GBM customer survey results

Global Banking and Markets

Global Banking and Markets (GB&M) helps multinational customers to grow and manage their businesses through a wide range of products and services. These are designed to address customers’ universal banking needs.

We continually strive to earn our customers’ trust and make it easier for them to do business with us. We are working on better understanding their needs, strengthening our controls, improving our service offering and technology, and ensuring our team embraces and lives up to our core values and conduct agenda. We made good progress in 2017 but we know there is still much more to do.

How we listen to customersOur customers are international, often with sophisticated needs, and always with high expectations of customer service. They have clear views on the service we offer, so improving how we listen and react to their opinions and concerns is at the centre of our thinking.

– We have implemented a number of bespoke surveys that capture our customers’ feelings about the service we provide. Information on our Global Banking biannual customer engagement survey, and HSBC Securities Services survey, can be seen in Figure 9.

– We subscribe to market insight to receive information on competitive positioning across the trade, cash management, and banking markets.

– We receive relationship feedback through our client planning process, and sometimes via complaints. We are updating our complaints tracking to ensure we have consistent standards in place.

When things go wrongWe receive some of the most powerful feedback from complaints. Following the roll out of our new Customer Feedback policy in late 2015, we have improved our underlying systems and processes to allow for greater transparency and improved reporting of our customers’ concerns.

Our people are trained to ensure customer concerns and complaints are handled as consistently and quickly as possible, and all complaints are monitored and reported in our governance forums.

Our Client Escalation Committee is made up of senior managers and strives to improve the quality of service for our customers, as well as dealing with issues when they arise. The Chair will assign an executive from the committee to sponsor each case and ensure the agreed action plan is completed. The committee encourages issues to be escalated and addressed before they result in frustration, ensures employee conduct is delivering fair outcomes for our customers, and identifies the root cause of repeat issues that need to be addressed.

HSBC Securities Servicescustomer engagement survey

In 2017six of the seven

Every year we measure seven aspects of engagement

engagement metricsshowed a positive trend

considered their relationshipwith HSBC good or excellent

96%

82%Overall

felt our service had stayed the same or improved64%

considered HSBC as one of their top 3 banks in 2017

Global Banking biannual customer engagement survey

AdvocacyRapportEmotionLoyaltyValueTrustSatisfaction

to recommendour services77% likely

17Customers

Improving our culture Although we have made progress, we are enhancing and accelerating progress made in strengthening and remediating our systems and controls and broader compliance culture through a newly established Global Banking and Markets Conduct Committee, led by our Global Banking and Markets CEO. Market experts are providing input. The agenda focuses on Culture and Behaviours, Customers (including Suitability, Conflicts of Interest, Pricing and Transparency), Markets (covering Market Conduct, Trade Execution and Competition), Governance and Controls, and Strategy and Business Planning. Progress is being tracked and reported through our own governance channels, as well as being reported to the DoJ, FRB and our regulators in line with our agreements with them all. Conduct is core to how we operate and manage our business. We have already implemented improvements to algorithmic trading to manage risk around benchmark orders, and updated our policies for sales, order handling, managing confidential customer information and conflicts of interest, pre-hedging and market abuse. We have engaged external firms to audit our internal controls and to enhance our voice, trade and audio surveillance. We have created global and regional conduct governance forums to provide supervision and oversight over the implementation and effectiveness of our conduct agenda. An extensive plan is in place, and we aim to deliver this as fast and efficiently as we can. Our success will determine how well we deliver the right outcomes for our customers and stakeholders, consistently and reliably, for many years to come.

Key areas of focus include:

– Customer-facing improvements: We are focusing on suitability and appropriateness, new product approval, pricing and transparency. Ensuring customers have the right products at a fair price.

– Surveillance: We have a major programme to install the latest technology and surveillance methods and to build out the supporting team.

– People: We are embedding conduct considerations into the full employee life cycle, including hiring, training, performance management and reward, promotions and exits. Building a stronger speak-up culture, together with our whistleblowing programme, are important aims of this approach. We also believe a more diverse workforce would help us to deliver better outcomes to our customers. See Employee section for more details, including a case study on improving gender balance on page 24.

Values, culture and market integrityWe are continually working on improving our conduct agenda. Major changes over the last four years, covering training, communication, incentives, policies, procedures, surveillance technology, reporting and monitoring have undoubtedly improved our culture, our behaviour and our discipline. The recent conclusion of two long-running investigations into historical practices were clear reminders of how ensuring the highest standards of professional conduct to deliver fair outcomes for customers and to protect the orderly and transparent operation of the markets remains paramount:

– On 29 September 2017, the Federal Reserve Board (FRB) fined HSBC $175.3m in relation to unsafe and unsound practices in our foreign exchange trading business covering the period from 2008 to 2013. The related Consent Order highlighted that the bank failed to detect and address conduct by certain traders, including misusing confidential customer information, as well as using electronic chat-rooms, to communicate with competitors about their trading positions. The FRB’s Order requires us to improve our controls and compliance risk management concerning both foreign exchange and wider designated wholesale markets for commodities and interest rate products.

– On 18 January 2018, HSBC also entered into a three-year Deferred Prosecution Agreement with the US Department of Justice (DoJ) to resolve its investigation into HSBC’s historical foreign exchange sales and trading activities within our Global Markets business. The conduct described in the agreement occurred in 2010 and 2011 and we paid $101.5m in fines and restitution.

HSBC has acknowledged its failings and, since the historical conduct described in these agreements, introduced a number of measures designed to make the control environment more robust. We have dedicated, and continue to dedicate, significant resources to strengthen our systems and controls. Improvements to our conduct agenda started more than three years ago and are already in place. However, we continue to look for ways to enhance our controls and to embed the culture that is at the heart of good conduct. We know we still have much more to do. HSBC is committed to ensuring fair outcomes for its customers and protecting the orderly and transparent operation of the markets. The investigations focused specifically on our markets activity, but they have also given us good reason to look again at every aspect of our conduct within the Global Banking and Markets business. They were clear and specific reminders of the importance for us to continue improving. More than ever, this is a top priority for our senior management team, as well as for every employee.

Environmental, Social and Governance (ESG) Update HSBC Holdings plc 18

73%

5 years +

47%

10 years +

91%

2017

88%

2016

Overall satisfaction increased from 7.8 to 8.3 out of 10

73% of respondents have had a relationship with GPB for more than five years, and 47% for more than 10 years.

91% felt the solutions that we recommended o�ered value for money. This was up from 88% in 2016.

Global Private Banking

Global Private Banking (GPB) aims to support the owners and principals of the Group’s corporate customers, helping them to grow and preserve their personal wealth from generation to generation.

Our customer service teams comprise Relationship Managers, investment counsellors, product and credit specialists, and wealth planners. They develop a thorough understanding of each customer, including their family, business, lifestyle, ambitions and philanthropic activity. Specialists from Global Private Banking and other parts of HSBC, including Commercial Banking and Global Banking and Markets, are then engaged to provide the best possible service from across our global network.

Addressing the pastIn recent years, GPB has taken significant steps to address historical control weaknesses, most notably in Switzerland. This has included the full implementation of the Group’s Global Standards for financial crime risk management and the adoption of a comprehensive tax transparency policy. Where we used to offer banking services to customers in more than 140 countries, GPB now focuses on 34 strategic markets, with customer assets actively managed down by $135bn between 2013 and 2017.

While GPB has resolved a number of legacy issues relating to the past, investigations into former practices are ongoing in a number of countries at the time of publication. In addition, GPB’s role as private bank and trust adviser to high net worth individuals may sometimes result in HSBC Private Banking receiving media attention in customer disputes.

What we expect from our customersAs part of our efforts to manage financial crime risk, today’s GPB customers are required to certify their tax status and undergo regular periodic and event driven reviews, according to their risk category and in line with changes to their circumstances. They are also subject to continuous transaction monitoring and negative news screening.

When things go wrong Given the direct access our customers have to their Relationship Managers, any issues are usually resolved quickly. Where this is not possible, a formal complaints process is invoked and monitored through the GPB Risk Management Meeting.

How we listen to our customersGPB conducts an annual customer engagement survey. In the 2017 survey, more than 800 customers shared their views (see Figure 10 for key findings).

Figure 10: GPB results from 2017 annual customer engagement survey.

19Customers

Taking responsibility for the experience we deliverTreating customers fairly and ensuring a fair exchange of value are fundamental principles for the pricing levels and design of GPB’s products and services. Our standards ensure GPB pricing is fair, properly governed and monitored. Global product heads are responsible for developing and reviewing, at least annually, the fair value exchange criteria for their product types or asset classes.

Over the past two years, GPB has embarked on a global programme to review internal practices to ensure that conduct is being managed effectively. As a result, enhancements have been made across a number of processes, such as improved sales and suitability controls, re-enforced through training initiatives to ensure customers are consistently receiving fair outcomes.

Training our people for good outcomesGPB has developed and launched the role-based learning curriculum for Relationship Managers and other key roles

in customer service teams. The learning focuses on helping colleagues deliver key outcomes specific to their role, such as customer satisfaction, effective management of conduct and risk, and business performance objectives.

GPB has also introduced specific conduct objectives, with a focus on customer outcomes, into the global scorecards for all its people. Customer-facing colleagues are required to demonstrate the delivery of fair outcomes and show products are marketed and sold in line with sales guidelines. Product design teams are asked to demonstrate that products and services are designed to meet the different needs of customers, are competitive, are clear, and offer a fair exchange of value.

Products designed with customers in mindWe are committed to providing the best possible service to customers. This is guided by our product approval process and sales quality standards. This covers everything from assessing the suitability of products and services to ensuring we fulfil our duty.

Environmental, Social and Governance (ESG) Update HSBC Holdings plc 20

Employees

Understanding how our people feel about HSBC is vital. It helps us ensure that we are giving them the right support to fulfil their potential and do the right thing for our customers. Employees are asked for feedback and encouraged to speak up.

We use CultureScope, an award-winning insight tool, to assess how people feel and think about how they behave in the workplace. This is then compared to the behavioural preferences that underpin HSBC’s values of being Dependable, Open and Connected. A close alignment between personal and organisational behaviours indicates a healthy culture.

Our 2017 results revealed encouraging signs in a number of key areas. It showed that our people place a high importance on laws, rules, values, and obligations; that there is an emphasis on long-term delivery and results; and that goals are achieved through partnerships and alliances.

However, CultureScope highlighted other areas where HSBC can do more to support the culture to which it aspires. These include: providing more support and guidance that empowers our people to make decisions; encouraging them to express more of their great ideas and opinions; and helping them make stronger connections between the work that they do and the experiences of our customers.

Executive summary Our people are critical to our success and it is important that we listen to them and encourage them to speak up. We try to foster a culture that encourages and promotes the right behaviour, where people feel empowered to voice their opinions and concerns. We believe gender balance and diversity across the organisation will help to create an environment where people can thrive in their own careers, and enable us to better support our customers and the communities we serve.

Listening to our peopleWe continue to test the views of a representative sample of our people on a range of topics via our monthly employee research, Snapshot. The 2017 results reveal that employee sentiment oncertain key topics has become more positive over the past year but also show that other areas have remained flat or fallen (see Figure 11).

Snapshot results are presented to the Group Management Board and relevant executive committees of the global functions and businesses, regions and countries. This ensures the attitudes and sentiments of our people inform decision-making at all levels of HSBC. Action can then be taken, both locally and globally, to tackle areas of concern.

Feedback from HSBC Exchange is shared and acted on in a similar way. Exchange sessions are safe forum meetings, without agendas, attended by people from across the organisation. They can discuss what matters to them, share views and suggest ideas, while managers and leaders attend to listen.

Our insight shows us that where our people participate in Exchange they are more positive about their experience at HSBC. They feel more able to speak up, are more trusting of managers and leaders, and report higher levels of well-being. It is our intention that all of our people have the opportunity to take part in an Exchange meeting each quarter.

21Employees

All Snapshot results based on Q417 data.

Figure 11: select results from Snapshot survey

65%

72%

66%

53%

76%

64%

58%

74%

70%

61%

69%

68%

56%

76%

63%

58%

76%

72%

2017 2016

I am seeing the positiveimpact of our strategy

I feel confident about HSBC’s future

I trust the senior leadership in my area

in my area makes decisions that take

I feel proud to work for HSBC

I would recommend this company as a great place to work

Conditions in my job allow me to be about as productive as I can be

I feel able to speak up when I seebehaviour which I think is wrong

I believe HSBC is genuine in its commitmentto encourage colleagues to speak up

I believe that the senior leadership

people like me into consideration

speak up

SPOTLIGHT

During 2017, we piloted a ‘Spotlight’ feature, designed to shine the light on a specific global priority for a defined period of time and encourage employees to recognise their colleagues.

The pilot topic was ‘fighting financial crime’ with more than 100,000 recognitions made. Some of the stories were later shared as inspirational case studies on our global intranet, HSBC NOW. This included how our people applied their training and used financial crime controls to protect HSBC and prevent suspected criminals, from sex traffickers to sanctions evaders, entering the financial system.

On average throughout 2017, 43% of our people reported that they had attended one within the previous three months, down two percentage points from the figures quoted last year. To make Exchange meetings mandatory would go against the spirit of the programme. Instead, we encourage managers and employees to arrange them by regularly communicating the clear benefits they provide to individuals, teams and HSBC.

We continue to focus on making improvements and creating a values-based, healthy organisation for everyone.

FOCUS ON FINANCIAL CRIME

CASE STUDY

Commercial Banking launched a two-day bespoke financial crime programme for 6,500 Relationship Managers and Team Leaders in 2017. This programme used HSBC subject matter experts, including those from our Financial Crime Risk, Regulatory Compliance, Sanctions and Tax functions, to create case studies and content, and was co-facilitated by Commercial Banking leaders.

Recognising those who live our valuesBy embedding a culture that promotes the right behaviour, we encourage those who live our values.

Our global peer-to-peer recognition programme, ‘At Our Best Recognition’, which is available in more than 50 countries, allows our people to recognise one another for demonstrating our values throughout the year. Individuals receive points which can be redeemed for a wide range of merchandise in a catalogue.

In 2017, more than 700,000 recognitions were made to a total value of nearly $10m.

Environmental, Social and Governance (ESG) Update HSBC Holdings plc 22

Pre-2006

2016TOTAL

1,102

RBWM

52%

Global Functions and HOST

25%

CMB

7%

GB&M

4%

2016 6%2016 56%

2016 4%2016 33%

Not specific to one area

10%GPB

2%2016 1%2016 Nil

2017TOTAL1,585

Figure 13: whistleblowing statistics by business and function line

Figure 12: whisteblowing statistics by themeWhistleblowingHaving a culture where our people feel able to speak up is important. Though individuals are actively encouraged to raise concerns about wrongdoing or unethical conduct through the usual reporting and escalation, we understand that in some circumstances employees would prefer a more discreet way to raise their concerns.

HSBC Confidential, established in 2015, provides a platform that enables employees to raise concerns on any issues, outside the usual escalation channels, in confidence and without fear of retaliation. HSBC Confidential is available to all of our people, past and present, in all global businesses, functions and entities across the world, including secondees, external consultants, contractors and agency employees. Multiple channels have been established to raise issues, including telephone hotlines, online and email, and these channels deal with a broad range of concerns at different severity levels.

HSBC does not condone or tolerate any acts of retaliation against anyone who reasonably believes that the concern that they have raised is true. We consider any retaliation in those circumstances as a disciplinary matter, and all such matters are escalated to senior management. The making of malicious or false claims is also incompatible with our values. Concerns raised are investigated thoroughly and independently, drawing on the expertise of a variety of departments, including Compliance, Human Resources, Legal, Fraud, Information Security, and Internal Audit.

A total of 1,585 cases were raised during 2017, which represents an increase of 44% on the 1,102 in 2016 (see Figures 12 and 13). The year-on-year increase highlights heightened awareness of HSBC Confidential and the ongoing efforts of the Group to encourage employees to speak up. Of the 1,139 cases closed in 2017, 30% were substantiated (2016: 34%) following independent investigation.

Common themes included issues with employees behaviour or conduct, allegations of fraud, and weaknesses with information security. Remedial activity has been undertaken where appropriate. This has included disciplinary action, adjustments to variable pay and/or performance and behaviour ratings.

The Group Audit Committee is taking overall responsibility forreviewing the Group’s whistleblowing policy and procedures,and receives regular updates on relevant concerns raised underthese procedures, together with management actions taken in response.

2017TOTAL1,585

2016TOTAL

1,102

People

63%

Security and fraud

16%

Compliance*

15%

Other

6%

2016 12%2016 62%

2016 5%2016 21%

*Includes Financial Crime Compliance and Regulatory Compliance

23Employees

GENDER PAY

Gender pay has been a particular area of focus since the introduction of UK gender pay gap regulations. Our pay strategy is designed to attract and motivate the very best people, regardless of gender, ethnicity, age, disability or any other factor unrelated to performance or experience.

We are confident in our approach to pay and if we identify any pay differences between men and women in similar roles, which cannot be explained by reasons such as performance/behaviour rating or experience, we make appropriate adjustments.

Our UK Gender Pay Gap disclosure can be found on the Measuring our Impact page at www.hsbc.com

A healthy and diverse workforce

‘ I am committed to building our leadership teams to reflect the gender balance of the customers and societies we serve. It is our responsibility as leaders to enable our people to fulfil their career potential and shape organisations that can thrive.’ John M Flint, Group Chief Executive.

Diversity and inclusion To be truly effective we must create an environment that is diverse and inclusive, where everyone feels they can thrive. Continued success will require a workforce that reflects our customers and the societies we serve. Our definition of diversity goes broader than inherent characteristics to include other differences that make individuals unique, such as cultural fluency, global experience and work styles. We encourage diversity of thought from our leaders and our people so we can deliver on our purpose.

Gender balanceGender balance is an important part of creating a diverse and inclusive environment. HSBC is supporting the 30% Club’s CEO Campaign, with an aspirational diversity target of 30% women in senior roles by the end of 2020. All Group Management Board members are accountable for diversifying their senior leadership population and ensuring succession plans draw on the Group’s broad workforce diversity. In 2017, 26.8% of our senior employees were women, ahead of our goal of 26.3%. For 2018, we are looking to achieve 27.6% or above (see Figure 14 for detailed targets).

We are increasing the focus on gender balance in our recruitment, succession planning and other development plans. These include leadership programmes, sponsorship and mentoring schemes. In addition, we participate in groups and forums such as CEO Action for Diversity & Inclusion™ in the US, and Women Directors in Malta, to share best practices and identify solutions. Balance, our largest global employee resource group, brings employees together on the gender agenda and partners with other diversity networks.

* Combined Executive Committee and Direct Reports was reported for the first time as at 30 June 2017 to the UK’s Hampton Alexander Review and includes the Executive Directors, Group Managing Directors and their direct reports (excluding administrative staff).

**Senior employees refers to employees performing roles classified as 0, 1, 2 or 3 in our Global Career Band Structure.

Figure 14: gender diversity statistics

Male % Female %No. of employees 2016 Female %

Holdings Board

Group Management Board

Combined Executive Committee and Direct Reports*

Senior employees**

All employees 52 5248

73

75

86

7112

12

135

6,540

112,390 122,239

2,393

45

2

5

27 25

25 –

14 8

29 30

ACCELERATING FEMALE LEADERS IN GB&M

CASE STUDY

The priority within GB&M is improving the representation of women at senior levels.

It had emerged that our female talent was less well-known than their male counterparts for managing director level promotions. This prompted last year’s launch of Accelerating Female Leaders, which is a programme to increase their visibility and connectivity. We are already seeing positive trends around promotion rates, while almost two-thirds of participants are engaged in strategic projects.

‘We know that we need to approach our diversity and inclusion opportunities from a number of different angles to drive sustainable change,’ said Samir Assaf, Chief Executive, GB&M. ‘Our Accelerating Female Leaders programme is an important lever in our vision for a more gender-balanced future.’

% figures have been rounded

Environmental, Social and Governance (ESG) Update HSBC Holdings plc 24

Figure 15: estimated gender / parent representation by Global Career Band*

Age diversity The demographic mix of HSBC’s people by age varies significantly by region.

GCB 0-3

Women/not mothers

Mothers

Fathers

Men/Not Fathers

GCB 4-6 GCB 7-8

19%

55%

14%12%

24%

30%

21%

25%

27%

20%

12%

41%

1

4

1

7

19 33 26 18 31

Asia

Europe

Latin America

Middle East

North America

<20 20-29 30-39 40-49 50-59 >60

Age band

30 43 20 6

25 49 22

29 28 2412

36 41 16 6

Parents and carersWe care about work-life choices and believe it’s important to help employees manage family responsibilities. Of those who completed Snapshot this year, 40% identified as being parents of dependent children, with 17% stating they were carers. This is defined as having a non-parental caring responsibility.

It’s our intention to create an inclusive environment that supports our people’s needs - both inside and outside of the workplace. We also recognise these may change at different points in their careers - and for reasons that go beyond family responsibilities.

Senior leadership Overall

White 40.8% Asian 53.9%

Asian 26.5% White 16.7%

Latin American 2.9% Latin American 6.7%

Senior leadership Overall

British 34.7% Chinese 22.0%

Chinese 8.3% Indian 16.4%

French 6.8% British 15.8%

Indian 5.5% Mexican 6.7%

Australian 2.5% French 4.0%

Figure 17: 2017 year-end headcount distribution by ethnicity and nationality*

Top 5 by nationality*

Top 3 by ethnicity*

*includes employees who chose not to disclose their ethnicity/nationality as well as any locations where regulatory restrictions apply. Group Ethnicity is a high level descriptor standardising multiple underlying ethnicity entries.

Ethnic diversityAs a global organisation, HSBC benefits from ethnic diversity. Our people have the opportunity to share demographic information in HSBC’s Snapshot survey, which helps us build a better understanding of the employee experience for different groups.

In the 2017 Snapshot, 8% of our people identified as belonging to an ethnic minority, and 68% of them aspire to move up at least one global career band within HSBC. Initiatives aimed at supporting different ethnic minority groups vary according to location. These include increasing the representation of members of Canada’s indigenous population via specific recruitment efforts. There is also a dedicated leadership programme for UAE nationals, while African-American/Black employees are involved in a reverse mentoring scheme in the US. Our Embrace network of employee resource groups also engages colleagues on issues around ethnicity and race.

* Combining HR headcount by gender and global career band with colleagues who identified as parents of dependent children in Snapshot

The Financial Times’ 100 Leading Ethnic Minority Power List

HSBC employees named on the following:

A Times Top 50 Employer for Women – Third year in a row

Top 30 Ethnic Minority Future Leaders list

Top Global employer in Stonewall’s Workplace Equality Index – Third year in a row. Winner, Global Trans Inclusion Award

Global Top 10 Women and Men lists

HERoes Champions for Women – UK Top 50 (Women)

Company of the Year – European Diversity Awards

Figure 16: 2017 employee age bands by region (%)

Figure 18: HSBC awards in 2017

TOP50

TOP50

HSBC2017

AWARDS

25Employees

Figure 19: key areas of our well-being programme.

Development and progression providing support that helps our people create the careers they want

Wealth and finances equipping our people with the tools they need to take control of their finances

Values and culture ensuring our workplace is values-based and inclusive

Lifestyle and leisure policies and opportunities to help everyone manage their work time effectively as well as enjoy time outside the office

Employee well-beingA healthy workforce is essential to creating a culture that sets HSBC apart and helps our people thrive. HSBC has a global well-being programme to provide all employees with information and resources to make positive choices that enhance their overall health and well-being. We believe that when we look after our people they, in turn, take better care of our business (see Figure 19 for how our well-being programme is delivered).

Everyone at HSBC is responsible for ensuring they are able to work at their best, fostering an environment where well-being is a priority.

After the launch of our global approach to well-being during 2016, we have made significant progress to bring this to life in 2017. Examples include:

– The launch of an HSBC Food Pledge, in partnership with our outsourced catering provider. For example, water hydration stations, vegetarian options, fresh fruit available, drinks available with no added sugar, more low fat milk, nutrition website and introduction of @Eatwell logo on food dishes.

– The introduction of Employee Assistance Programme services in all locations (see Health and Safety on page 39 for more details).

– The provision of financial education seminars including ‘Your Financierge’ (see page 33 for more details).

HSBC global well-being survey To further understand and support our employees’ needs, 2017 saw the second annual HSBC global well-being survey. The research explored mental health, work-related stress, physical health, financial health, career development, flexible working, supportive network and resilience. We had 28% of global employees responding and the results will help shape our well-being programme.

The top contributors to stress are workload, management of processes and systems, lack of growth opportunities, fear of making a mistake, and work extending into personal time. The survey showed that 69% of employees feel equipped to manage their work-related stress through planning and prioritising, support from colleagues and exercise. In addition to the obvious benefits, the research also revealed that these individuals are more likely to recommend our products and services.

There is a strong relationship between positive mental health and resilience. Our insight also indicates that highly resilient employees feel more able to speak up, challenge processes and procedures that they think will be bad for our customers, and feel more productive.

Individuals with a long-term physical health condition report higher work-related stress, higher financial strain and lower levels of positive mental health. These stressors can be partly mitigated through supportive line management, improved resilience and flexible working.

Approximately 65% of employees would like to improve their financial well-being. To learn more about our commitment to our employees’ financial well-being see page 33.

Those who work flexibly are more positive about many well-being factors, including their working relationships and ability the make work-life choices that are right for them. Employees who reported flexible working, high levels of resilience and the ability to manage work-related stress were also more likely to want to stay at HSBC for longer.

of our people report feeling work-related stress.37%

of our people experience positive mental health64%

of our people report a long-term physical health condition21%

of our people are finding it difficult to manage financially16%

of our people across HSBC work flexibly49%

Health and wellness providing resources that enable our employees to be at their physical, mental and emotional best

Environment enhancing our physical working environment

Environmental, Social and Governance (ESG) Update HSBC Holdings plc 26

Learning is one of the keys to success at HSBC. Investing in learning helps our people to excel in their current roles - and thrive in the future. It also helps them implement policies, deliver great things for our customers and aligns behaviours with HSBC’s cultural aspirations.

Our people participated in a wide variety of learning last year, including programmes helping them understand their responsibilities in risk management, fighting financial crime and effectively managing people.

We introduced a more focused and efficient approach to mandatory training, targeting critical areas such as anti-money laundering, bribery and corruption. This approach, as well as the completion of our two-year, ‘At Our Best’ programme, resulted in a reduction of training hours for all our people.

Introducing HSBC University HSBC University, the new home of Learning at HSBC, launched across the Group in October 2017. This encompasses new learning programmes and premises, as well as investments in delivering learning beyond the classroom.

HSBC University gives employees access to relevant, timely and high-quality learning, regardless of their role. Role-specific learning is available by business line and function, designed to support our people from new-to-role through to expert.

The University also has new management programmes to support our strategic leadership needs and connect people across the Group. These programmes are for employees at all levels and include Leadership Essentials and Team Management Essentials, tailored for new people managers, and Leading Businesses and Functions, a strategic programme for our more senior leaders.

Supporting our people managersOur employee insight has consistently highlighted the important role of our people managers. Everyday Performance and Development (EPD) encourages managers to move away from the traditional cycle-based performance management activities. It focuses on more frequent and meaningful conversations about their team’s performance, development, and well-being throughout the year, both formally and informally.

These frequent check-ins result in our people feeling more productive, more able to state their opinions, more trusting of leadership, and more positive about their future with HSBC. Our Q4 2017 Snapshot results indicate that 63% of our people feel these conversations have an effect on their day-to-day achievement of performance objectives.

EPD is one of the critical themes of HSBC University’s People Management Essentials, attended by more than 6000 managers in 2017. We will continue to provide this training to our managers while refreshing and updating content. For example, an Inclusive Hiring Essentials course will be added to the programme in 2018.

E-Learning completions

Instructor-led training

2016 = 11m

Training hours

Training days per FTE

7.2 million

7 million

4.5 million

3 days

Instances of training courses

2016 = 11m

2016 = 622,221

2016 = 5.5m

2016 = 5.5 days

440,548

Developing our people

BUILDING DIGITAL CAPABILITY

Our RBWM leaders recognised the opportunity to improve their digital development. We partnered with industry experts across the globe to explore topics such as exponential growth through digital innovation, customer centricity, and leadership. Participants worked together to apply their new skills on 21 existing business challenges. The programme was extended to nearly 700 leaders across RBWM and supporting functions.

CASE STUDY

Figure 20: training statistics at HSBC

27Employees

Supporting sustainable growth

In our last ESG supplement we introduced our new approach and principles around sustainability in HSBC. Our sustainability approach focuses on three main areas: sustainable finance; sustainable networks and entrepreneurship; and future skills. We continue to prioritise these areas to support sustainable growth within our own organisation and for our customers.

The United Nations Sustainable Development Goals (‘SDGs’) are 17 goals and 169 targets to be achieved by 2030. This is a call to action to protect the planet, end poverty, and ensure peace and prosperity. HSBC has a responsibility to contribute to this globally agreed framework for action. By aligning our values, conduct and business activity, the SDGs set the context for our long-term ambition.