how wealthy are residential solar...

TRANSCRIPT

How Wealthy Are Residential Solar Customers?

Household Income and Solar Adoption in the U.S.

Shayle Kann

Head of GTM Research

Attila Toth

CEO, PowerScout

April 2017

1Residential Solar Income Analysis - April 2017

v

We provide critical market intelligence on:

GTM NEWS GTM EVENTS GTM RESEARCH

Solar Power

Energy Storage

Grid Edge

Learn more at www.gtmresearch.com

About GTM Research

GTM Research is the

leading market analysis and

advisory firm on the

transformation of the

global electricity industry.

vIn-Depth Market Reports

Analyst Access

Data and Forecasts

All our subscriptions include:

2Residential Solar Income Analysis - April 2017

2

Free customized benefits report

Machine learning-driven predictive analytics

Curated list of products and service providers

Superb content, optimized for mobile and social

Multiple up-sell opportunities As seen on:

About PowerScout

The First AI-Enabled

Marketplace for

Sustainable Smart home

Improvement

3Residential Solar Income Analysis - April 2017

How wealthy are residential solar customers?

This question has surfaced repeatedly, most often when policymakers or regulators are considering solar incentives and/or changes to electricity rates. In

particular, battles over net energy metering (NEM) have often included charged debates over whether solar is for the wealthy or for the masses. In response to

one such dispute in Nevada, for example, the Wall Street Journal editorial board called net metering “regressive political income redistribution."

These statements on both sides have rarely been backed by data, and instead have relied on a general impression of who solar customers might be.

Previous analyses have attempted to answer this question by using ZIP code-level data on solar adoption. Examples of previous work come from:

• The Center for American Progress (2013)

• Kevala Analytics (2015)

While these analyses provide valuable information, the methodologies employed do not account for the (sometimes wide) income variations within ZIP codes.

By contrast, this report presents – for the first time – household-level data on the relationship between residential solar and household income. While the

findings are broadly consistent with previous research, a number of key differences emerge.

Introduction

4Residential Solar Income Analysis - April 2017

• PowerScout identified solar households by analyzing satellite images using its proprietary Convolutional Neural Network (CNN) machine-

learning algorithm. The CNN model was trained with hundreds of thousands of labeled images of homes with and without solar panels

until the model was able to distinguish between the two types.

• We then matched the 521,449 positively identified solar homes to their income band, and compared the distribution of solar

installations to the distribution of the general state population.

• We used GTM Research data on total solar market size to determine sample representation of state and national solar markets.

We believe this sample is statistically significant for the states analyzed.

Our Methodology

5Residential Solar Income Analysis - April 2017

The Result: Our Data

Residential Solar Market Coverage in This Analysis

• We focused on four leading residential solar states: California,

Massachusetts, New Jersey and New York. Together, these states account for

65% of all residential solar installations to date.

• We identified over 521,000 solar installations in these four states,

representing 62% of those markets and 41% of all solar projects nationwide.

• Our coverage was greatest in California, where we identified over two-

thirds of all residential solar installations, and least comprehensive in

Massachusetts, where we identified one-fourth of all current projects.

• We believe these samples to be representative of each state’s overall solar

installation pool without any systemic bias.

LocationSolar

Households Analyzed

Total Solar Households

% of All Installations

Covered

CA 444,783 642,446 69%

NJ 28,445 60,628 47%

MA 15,588 62,088 25%

NY 32,633 70,072 47%

Total: Four States 521,449 835,234 62%

Total: National 521,449 1,278,494 41%

Residential Solar Income Analysis - April 2017

Findings and Analysis

7Residential Solar Income Analysis - April 2017

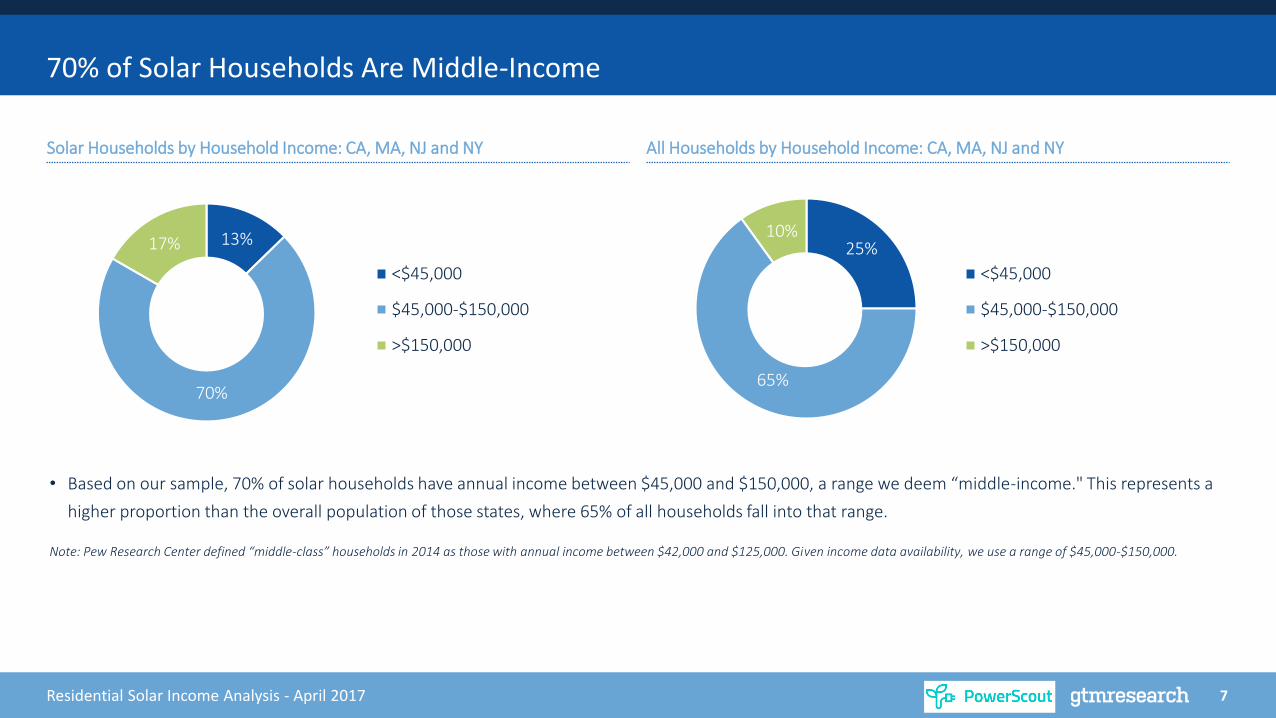

70% of Solar Households Are Middle-Income

Solar Households by Household Income: CA, MA, NJ and NY All Households by Household Income: CA, MA, NJ and NY

• Based on our sample, 70% of solar households have annual income between $45,000 and $150,000, a range we deem “middle-income." This represents a

higher proportion than the overall population of those states, where 65% of all households fall into that range.

Note: Pew Research Center defined “middle-class” households in 2014 as those with annual income between $42,000 and $125,000. Given income data availability, we use a range of $45,000-$150,000.

13%

70%

17%

<$45,000

$45,000-$150,000

>$150,000

25%

65%

10%

<$45,000

$45,000-$150,000

>$150,000

8Residential Solar Income Analysis - April 2017

Overall Distribution of Solar Households vs. General Population in CA, MA, NJ and NY

But Solar Households Do Tend to Skew Higher-Income Than the General Population

39.0%

44.3%

16.7%

55.6%

34.5%

9.9%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

<$74,999 $75,000-$149,999 >$149,999

Perc

enta

ge o

f H

ou

seh

old

s

Household Income

Solar Households All Households

• In our sample, 61% of solar households had annual an income of at least $75,000, as compared to 44% of the overall population of those states.

9Residential Solar Income Analysis - April 2017

Overall Distribution of Solar Households vs. General Population in CA, MA, NJ and NY

Households With Income Between $100k and $150k Are the Biggest Solar Demographic

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

< $10,000 $15,000 -$19,999

$25,000 -$29,999

$35,000 -$39,999

$45,000 -$49,999

$55,000 -$59,999

$65,000 -$74,999

$100,000 -$149,999

$175,000 -$199,999

>= $250,000

Perc

enta

ge o

f H

ou

seh

old

s

Household Income

Solar Households All Households

10Residential Solar Income Analysis - April 2017

Overall Distribution of Solar Households vs. General Population in CA, MA, NJ and NY

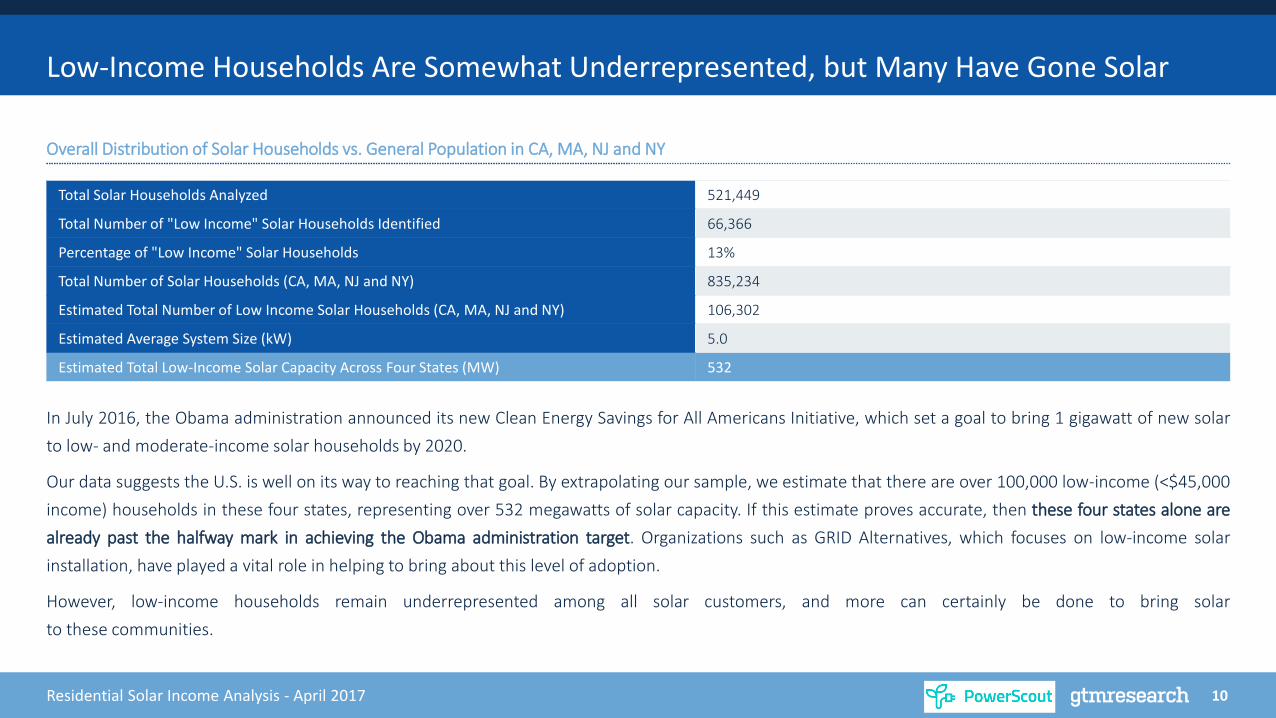

Low-Income Households Are Somewhat Underrepresented, but Many Have Gone Solar

In July 2016, the Obama administration announced its new Clean Energy Savings for All Americans Initiative, which set a goal to bring 1 gigawatt of new solar

to low- and moderate-income solar households by 2020.

Our data suggests the U.S. is well on its way to reaching that goal. By extrapolating our sample, we estimate that there are over 100,000 low-income (<$45,000

income) households in these four states, representing over 532 megawatts of solar capacity. If this estimate proves accurate, then these four states alone are

already past the halfway mark in achieving the Obama administration target. Organizations such as GRID Alternatives, which focuses on low-income solar

installation, have played a vital role in helping to bring about this level of adoption.

However, low-income households remain underrepresented among all solar customers, and more can certainly be done to bring solar

to these communities.

Total Solar Households Analyzed 521,449

Total Number of "Low Income" Solar Households Identified 66,366

Percentage of "Low Income" Solar Households 13%

Total Number of Solar Households (CA, MA, NJ and NY) 835,234

Estimated Total Number of Low Income Solar Households (CA, MA, NJ and NY) 106,302

Estimated Average System Size (kW) 5.0

Estimated Total Low-Income Solar Capacity Across Four States (MW) 532

11Residential Solar Income Analysis - April 2017

All States Are Not Equal

Household Income: Massachusetts Household Income: New York

Household Income: California Household Income: New Jersey

0%

5%

10%

15%

20%

25%

30%

< $10,000 $20,000 -$24,999

$35,000 -$39,999

$50,000 -$54,999

$65,000 -$74,999

$150,000 -$174,999

>=$250,000

% o

f H

ou

seh

old

s

Solar Households All Households

0%

5%

10%

15%

20%

25%

< $10,000 $20,000 -$24,999

$35,000 -$39,999

$50,000 -$54,999

$65,000 -$74,999

$150,000 -$174,999

% o

f H

ou

seh

old

s

Solar Households All Households

0%

5%

10%

15%

20%

25%

30%

< $10,000 $20,000 -$24,999

$35,000 -$39,999

$50,000 -$54,999

$65,000 -$74,999

$150,000 -$174,999

>=$250,000

% o

f H

ou

seh

old

s

Solar Households All Households

0%

5%

10%

15%

20%

25%

30%

< $10,000 $20,000 -$24,999

$35,000 -$39,999

$50,000 -$54,999

$65,000 -$74,999

$150,000 -$174,999

>=$250,000

% o

f H

ou

seh

old

s

Solar Households All Households

12Residential Solar Income Analysis - April 2017

Percentage of Solar Households Under State Median Income

New Jersey Has the Highest Share of Lower-Income Solar Households; New York Has the Lowest

34% 33%

29%

24%

0%

5%

10%

15%

20%

25%

30%

35%

40%

NJ MA CA NY

% o

f H

ou

seh

old

s

13Residential Solar Income Analysis - April 2017

Percentage of Households With >$250,000 Annual Income

The Wealthiest Households Often Go Solar – Except in New Jersey

10%

5%4%

6%

5%

7%

4% 4%

0%

2%

4%

6%

8%

10%

12%

California New Jersey Massachusetts New York

% o

f H

ou

seh

old

s

Solar Households All Households

14Residential Solar Income Analysis - April 2017

Differences in Solar Income Distribution Between States

It is unclear why the income distribution of solar households is skewed more toward wealthier households in California and New York than it is in

Massachusetts and New Jersey. Some potential explanations:

• Subsidies

◦ In New York, the state provides an additional tax credit (up to $5,000) that is eligible to be claimed by the customer, and thus requires equivalent state

tax liability in order to be monetized.

• Rate Structure

◦ In California, tiered electric rate structures may have provided additional incentive for households with high electric consumption (which tend to be

wealthier) to adopt solar

• Timing of Adoption

◦ In more mature markets (e.g., California), many solar installations occurred when solar system prices were higher and were likely driven by early

adopters (who tend to be wealthier)

• Network/Neighborhood Effects

◦ Various factors above may have been magnified by network/neighborhood effects – people whose neighbors have gone solar are more likely to adopt

solar themselves

15Residential Solar Income Analysis - April 2017

Suggestions for Future Research and Analysis

There are two primary limitations of this analysis:

1. Our limited sample size, which covers a portion of four states rather than the entire national market

◦ Future research should attempt a wider geographic scope to capture more state market diversity

2. Our research is a snapshot, but solar demographics change over time

◦ Future snapshots should compare against this data to determine whether, for example, lower-income households have been

increasingly adopting solar as technology costs fall and financing options proliferate

How Wealthy Are Residential Solar Customers?

April 2017

Household Income and Solar Adoption in the U.S.

Shayle Kann

Head of GTM Research

Attila Toth

CEO, PowerScout