how to reduce risk, error and complexity in the accounts...

TRANSCRIPT

WHITE PAPER HOW TO REDUCE RISK, ERROR AND COMPLEXITY

IN THE ACCOUNTS PAYABLE PROCESS

Based on a benchmark study of 250 companies with a total of more than 950 billion euro in Accounts Payable data worldwide, this

white paper provides insight into the most commonly seen errors and risks in the Accounts Payable process

How to reduce risk, error and complexity

in the Accounts Payable process

Based on a benchmark study of 250 companies with a total of more

than 950 billion euro in Accounts Payable data worldwide, this white

paper provides insight into the most commonly seen errors and risks

in the Accounts Payable process.

Introduction

In today’s volatile business environment, Finance strives to have a flexible and

responsive finance function in order to support the business in making the smartest and

fastest decision. Recent research by Free University Amsterdam shows that

organizations which strive to have a flexible and proactive finance function:

Exercise control over several leading indicators instead of many KPIs,

Implement rolling forecasting,

Use trend information and relative performance indicators,

Value knowledge sharing, learning and collaboration within the finance

organization

From this perspective finance professionals want, among other things, to review and

improve their performance based on hard, objective data. According to research by the

Aberdeen Group (2009), CFOs’ challenges in improving financial performance are

reducing costs (73%),

optimizing working capital (70%),

forecasting financial performance (53%) and,

reducing errors (43%).

Financials therefore have, among other things, an inherent interest in management

information in the following areas:

Historical and current payment performance

Types of payment errors that occur

Cost control, profitability

Contract Compliance

Payment terms, DPO

Extent of contamination of the vendor master file

Supplier behaviour and risks associated with the supply base

Based on hard, objective data this white paper offers insight into the causes and effects

of the most common errors and risks in the Accounts Payable process. The study is

based on the results of a benchmark of 250 companies with a total of more than 950

billion euro in Accounts Payable data in various industries and countries worldwide.

Brief overview of this white paper:

Supplier behaviour and risks associated with the supply

Industries with the largest number of suppliers with small invoices

Industries that have the most suppliers with the same bank account number

Industries with the highest percentage of inactive suppliers among the total

number of suppliers.

Risks associated with the suppliers location

Extent of contamination of the vendor master file

Insight into the most common errors that occur in the vendor master file

Top five industries with highest error rates in Accounts Payable

Insight into the most common errors per top five industry

Short-term and long-term solutions to resolve and prevent the most common

errors

About the author:

Founded in 2000, Transparent is an international financial-services provider

specializing in data mining of Accounts Payable. The company has rapidly grown into a

global operation, with operations in the Netherlands, Germany, Belgium, India, France,

the United Kingdom, Italy and the United States of America.

Our services include the analysis of outgoing payments and associated processes with

the aim to convert payment data into detailed management information. Alongside the

analysis, we identify, verify and collect undue payments on a no-recovery no-fee basis.

The results are presented in an easy-to-read dashboard and used by Transparent to

provide clients with management information and advice regarding their Accounts

Payable processes.

CFOs’ of blue-chip and medium-sized companies around the globe rely on Transparent

to provide them with enterprise-level transparency of their payment processes and with

sensible improvement recommendations. Moreover, many of our clients have seen an

immediate profit increase upon engaging our contingency-based recovery services. Our

analysis is robust, fast, risk-free, and doesn’t consume our clients’ resources, due to our

excellent technology deployment and fully-industrialized process.

For more information about the benchmark, including a customized benchmark,

our services and/or other inquiries, please feel free to contact:

Or contact us directly via:

Mr. Joep van den Brink, MSc.

Marketing Manager

http://nl.linkedin.com/in/joepvandenbrink

www.transparent.eu

+31 (0) 20 4684 648

Even if you believe that your Accounts Payable process is fully in order, a scan of your

outgoing payments can give surprising results. This could be because contamination of

the supplier database has increased historically. On the one hand there is a real risk of

errors occurring in the payment process, while on the other hand there is also the extra

workload due to payment corrections to consider. In today’s volatile business

environment, managers responsible for the Accounts Payable process want the

following questions answered:

How efficient is my Accounts Payable process?

How does my Accounts Payable process compare with those of my competitors

or other parts of my organization?

What are the risks attached to my suppliers?

How can I improve my Accounts Payable process?

Several issues that can be taken into consideration:

Supplier behaviour and risks associated with supply

Accounts payable is all about managing your relationships with your suppliers. If you

understand your suppliers’ behaviour, issues such as rare errors and workload can be

reduced or even prevented.

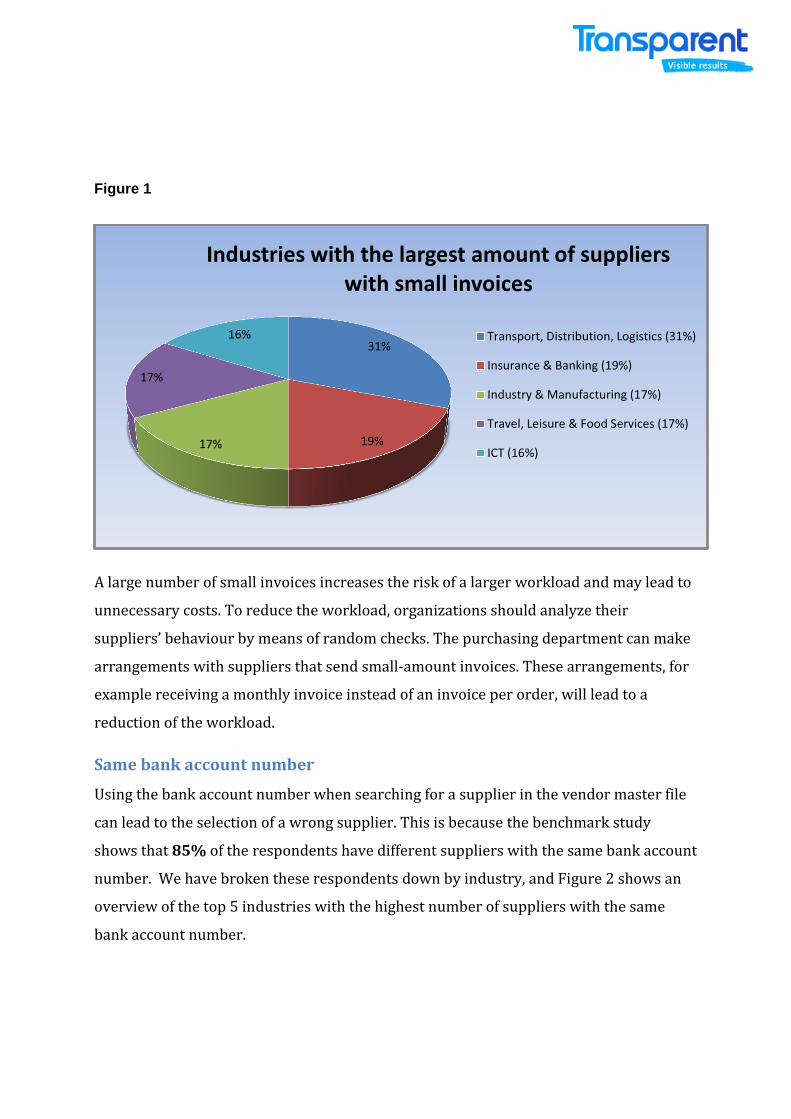

Small invoices

During our benchmark study we noticed that a substantial number of suppliers sent

small-amount invoices. The number of suppliers with small-amount invoices is the

largest in the industries shown in Figure 1. With an average of 121 suppliers with

small-amount invoices, the Transport, Distribution and Logistics industry (31%) ranks

number one.

Figure 1

A large number of small invoices increases the risk of a larger workload and may lead to

unnecessary costs. To reduce the workload, organizations should analyze their

suppliers’ behaviour by means of random checks. The purchasing department can make

arrangements with suppliers that send small-amount invoices. These arrangements, for

example receiving a monthly invoice instead of an invoice per order, will lead to a

reduction of the workload.

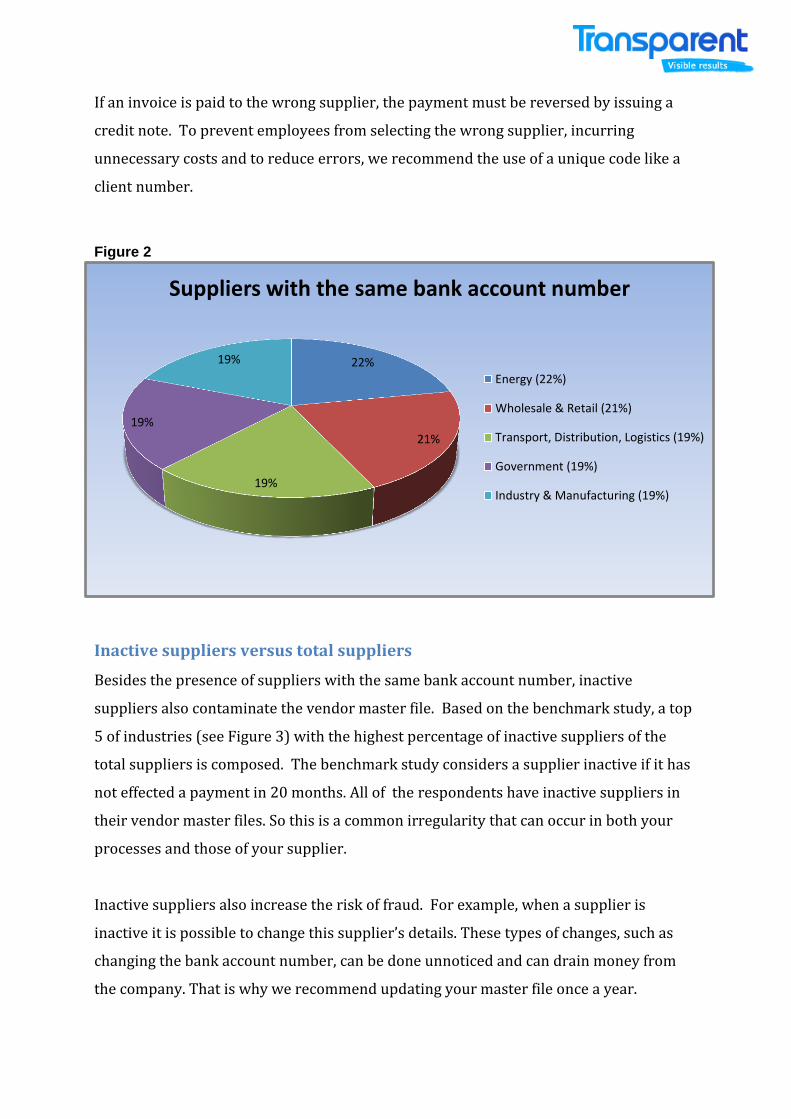

Same bank account number

Using the bank account number when searching for a supplier in the vendor master file

can lead to the selection of a wrong supplier. This is because the benchmark study

shows that 85% of the respondents have different suppliers with the same bank account

number. We have broken these respondents down by industry, and Figure 2 shows an

overview of the top 5 industries with the highest number of suppliers with the same

bank account number.

31%

19% 17%

17%

16%

Industries with the largest amount of suppliers with small invoices

Transport, Distribution, Logistics (31%)

Insurance & Banking (19%)

Industry & Manufacturing (17%)

Travel, Leisure & Food Services (17%)

ICT (16%)

If an invoice is paid to the wrong supplier, the payment must be reversed by issuing a

credit note. To prevent employees from selecting the wrong supplier, incurring

unnecessary costs and to reduce errors, we recommend the use of a unique code like a

client number.

Figure 2

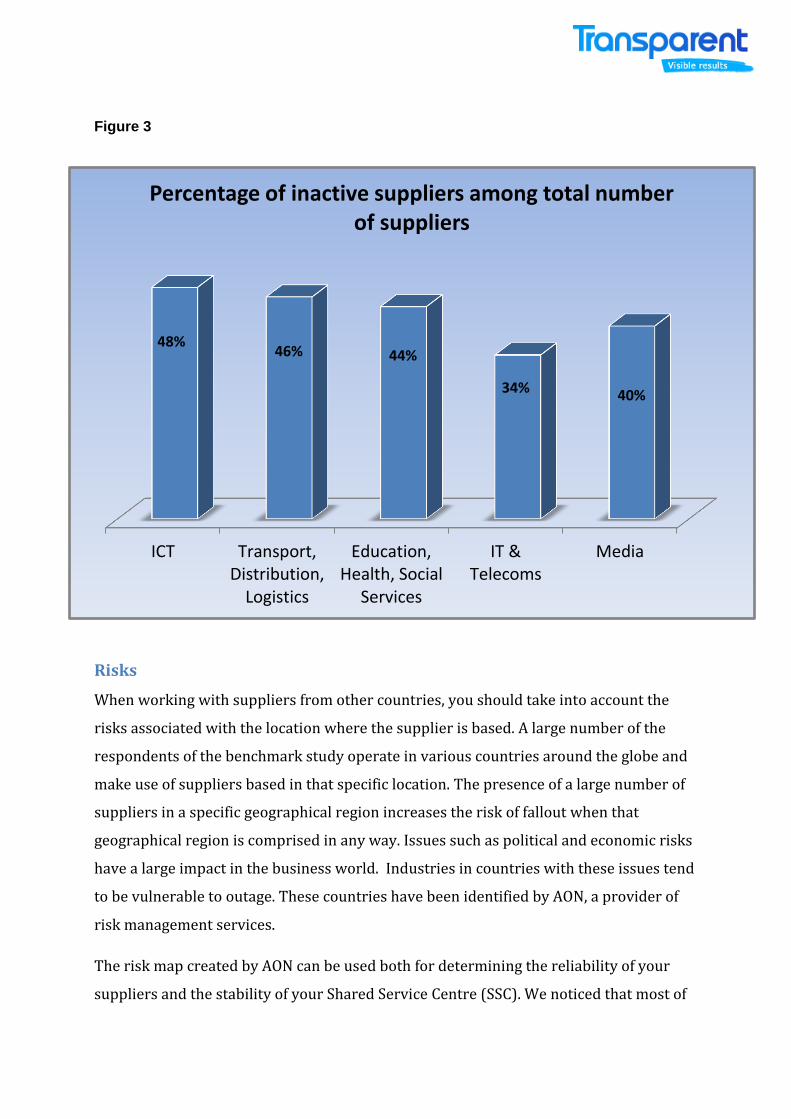

Inactive suppliers versus total suppliers

Besides the presence of suppliers with the same bank account number, inactive

suppliers also contaminate the vendor master file. Based on the benchmark study, a top

5 of industries (see Figure 3) with the highest percentage of inactive suppliers of the

total suppliers is composed. The benchmark study considers a supplier inactive if it has

not effected a payment in 20 months. All of the respondents have inactive suppliers in

their vendor master files. So this is a common irregularity that can occur in both your

processes and those of your supplier.

Inactive suppliers also increase the risk of fraud. For example, when a supplier is

inactive it is possible to change this supplier’s details. These types of changes, such as

changing the bank account number, can be done unnoticed and can drain money from

the company. That is why we recommend updating your master file once a year.

22%

21%

19%

19%

19%

Suppliers with the same bank account number

Energy (22%)

Wholesale & Retail (21%)

Transport, Distribution, Logistics (19%)

Government (19%)

Industry & Manufacturing (19%)

ICT Transport,Distribution,

Logistics

Education,Health, Social

Services

IT &Telecoms

Media

48% 46% 44%

34% 40%

Percentage of inactive suppliers among total number of suppliers

Figure 3

Risks

When working with suppliers from other countries, you should take into account the

risks associated with the location where the supplier is based. A large number of the

respondents of the benchmark study operate in various countries around the globe and

make use of suppliers based in that specific location. The presence of a large number of

suppliers in a specific geographical region increases the risk of fallout when that

geographical region is comprised in any way. Issues such as political and economic risks

have a large impact in the business world. Industries in countries with these issues tend

to be vulnerable to outage. These countries have been identified by AON, a provider of

risk management services.

The risk map created by AON can be used both for determining the reliability of your

suppliers and the stability of your Shared Service Centre (SSC). We noticed that most of

the respondents operate SSCs abroad: in the United Kingdom, Poland, Brazil, Portugal,

Hungary, India and other Asian countries.

Based on AON’s risk map, we conclude that the United Kingdom, Poland, Portugal,

Hungary and Brazil have a low probability of political and economic risks. In contrast,

countries in Africa and Asia, including India, have a high probability of political and

economic risks. In sum, when setting up an SSC or searching for suppliers, the above-

mentioned risks associated with the location should be taken into serious consideration.

Extent of contamination of the vendor master file

In an effort to make the company more flexible and responsive, organizations are

restructuring and professionalizing the organization. This could lead to, among other

things:

The automation of the back office and Accounts Payable process

Companies migrate their ERP systems to improve companywide communication

Mergers and acquisitions

SSC are set up and/or companies are outsourcing back-office processes

These changes can have a major impact on your data in the vendor master file and may

cause a decline in the quality of your supplier database. The impact of a contaminated

vendor master file must not be underestimated. Pollution and incomplete data in the

vendor master file could lead to serious errors and undue payments. It is therefore

important to check if your master vendor file is polluted.

The benchmark study shows that the following causes are quite common and could lead

to errors in the vendor master file.

The use of different ERP systems

VAT input task not claimed

Typing errors or manual errors: same supplier spelled incorrectly, or inaccurate

contact details

Large number of errors occur involving a parent company and subsidiary

Recent merger and acquisition have taken place

Duplicate payment:Original & Copy

Financial Statements Duplicate payment:Mutiple supplier

records

57%

32%

11%

Most common errors in the Accounts Payable process

According to the benchmark study, the most common errors in the vendor master file

which could lead to the following payment errors are:

Duplicate Payments – Original & Copy (accounts for 57%)

A supplier has sent both the original invoice and a copy, and payment has been

received for both invoices without being refunded.

Financial Statements (accounts for 32%)

An overview returned by the supplier listing the outstanding items containing an

unknown credit amount. This credit amount is still to be reclaimed.

Duplicate payment – Multiple Supplier Records (accounts for 11%)

A supplier is listed twice in the payment system; as a result, a payment has been

received twice by a supplier without the supplier returning the second payment.

Duplicate payment:Payment to wrong

vendor

Duplicate payment:Different invoices

Unposted creditmemo/chargeback

Erroneous Pay – Overpayment

4% 4%

2% 2%

Less frequent errors in the Accounts Payable process

Other errors that are less common but still produce a substantial error rate:

Duplicate payment - Payment to wrong vendor (accounts for 4%)

A payment has been collected twice by different suppliers without this amount

being returned by one of both suppliers.

Duplicate payment - Different invoices (accounts for 4%)

A supplier has charged twice for the same delivery or service with different

invoices.

Unposted credit memo/chargeback (accounts for 2%)

An unknown credit amount to be paid by the supplier which is not entered in the

system. This credit amount will be checked and reclaimed.

Erroneous Pay – Overpayment (accounts for 2%)

The supplier has received an amount that is higher than that originally invoiced.

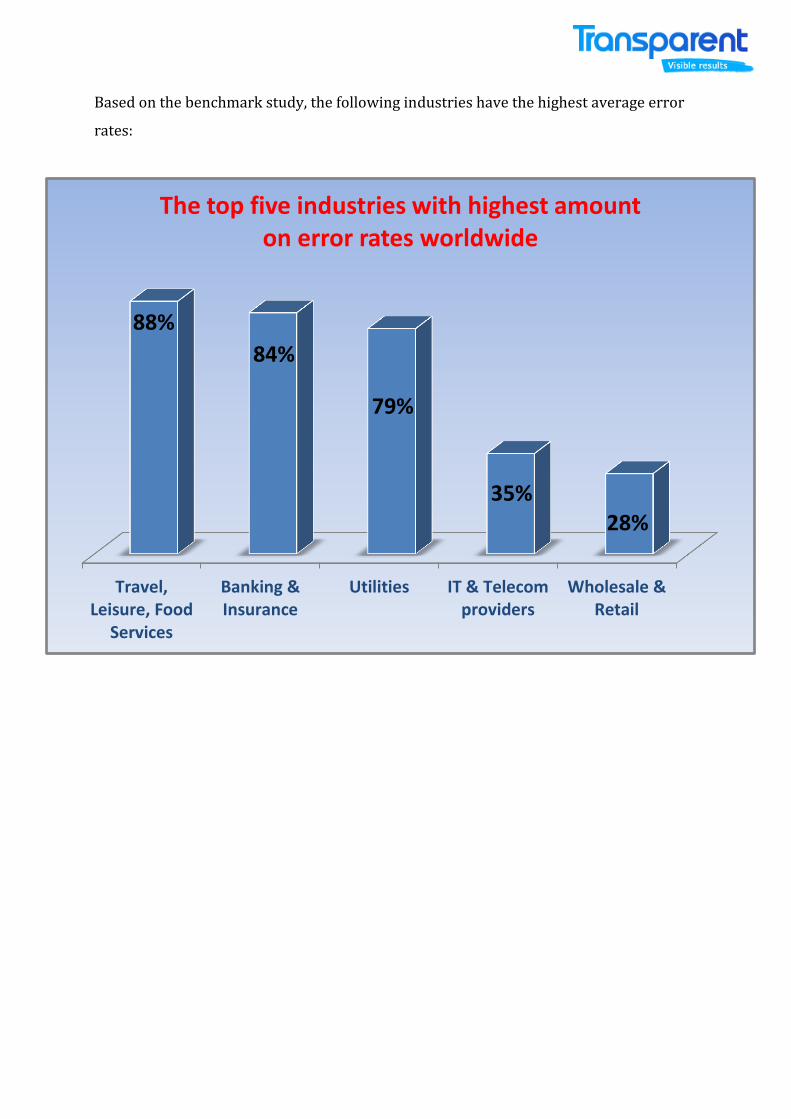

Travel,Leisure, Food

Services

Banking &Insurance

Utilities IT & Telecomproviders

Wholesale &Retail

88%

84%

79%

35% 28%

The top five industries with highest amount on error rates worldwide

Based on the benchmark study, the following industries have the highest average error

rates:

DuplicatePayments:

Original & Copy

FinancialStatements

DuplicatePayments:Payment to

wrong vendor

DuplicatePayments:Multiplesupplierrecords

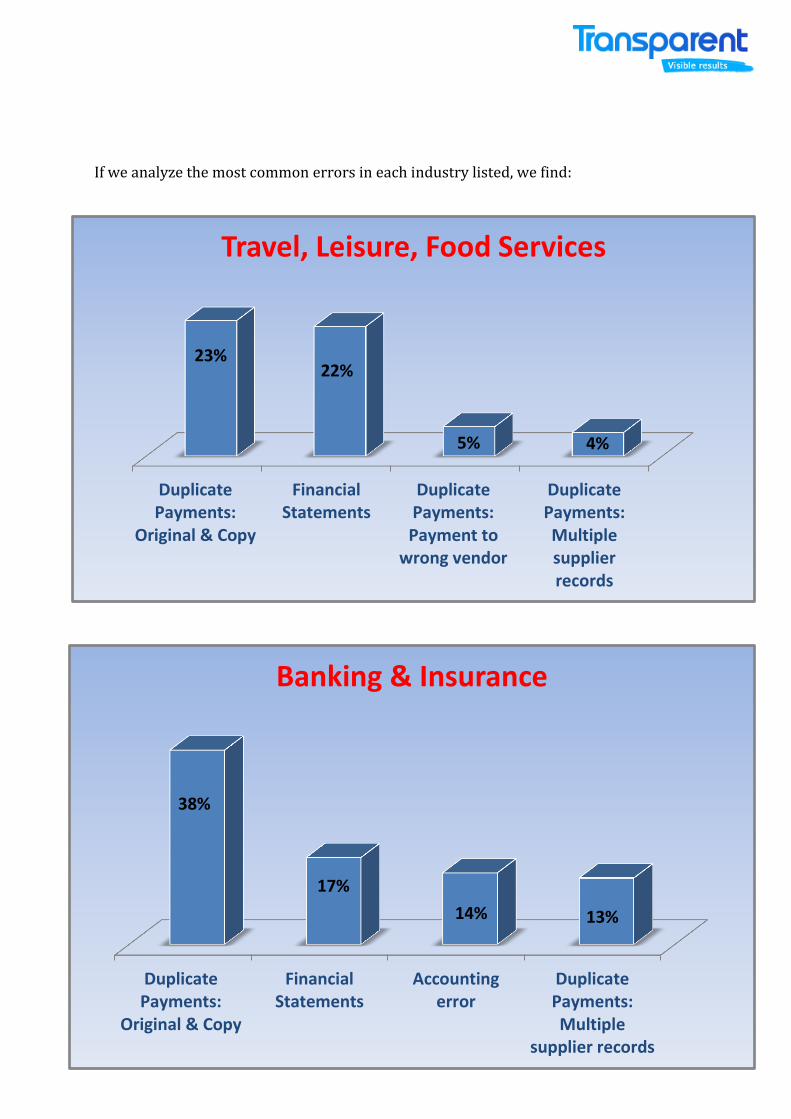

23% 22%

5% 4%

Travel, Leisure, Food Services

DuplicatePayments:

Original & Copy

FinancialStatements

Accountingerror

DuplicatePayments:Multiple

supplier records

38%

17%

14% 13%

Banking & Insurance

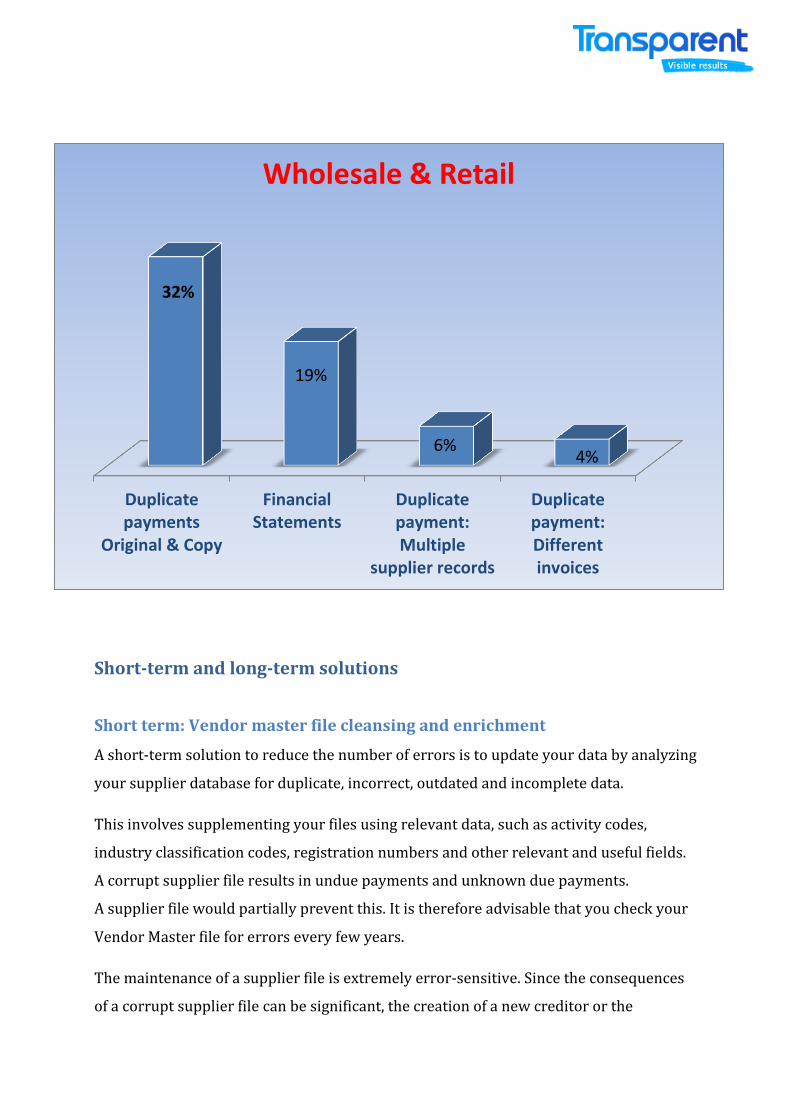

If we analyze the most common errors in each industry listed, we find:

Duplicatepayments:

Original & Copy

FinancialStatements

Duplicatepayment:Multiplesupplierrecords

Erroneous payOverpayment

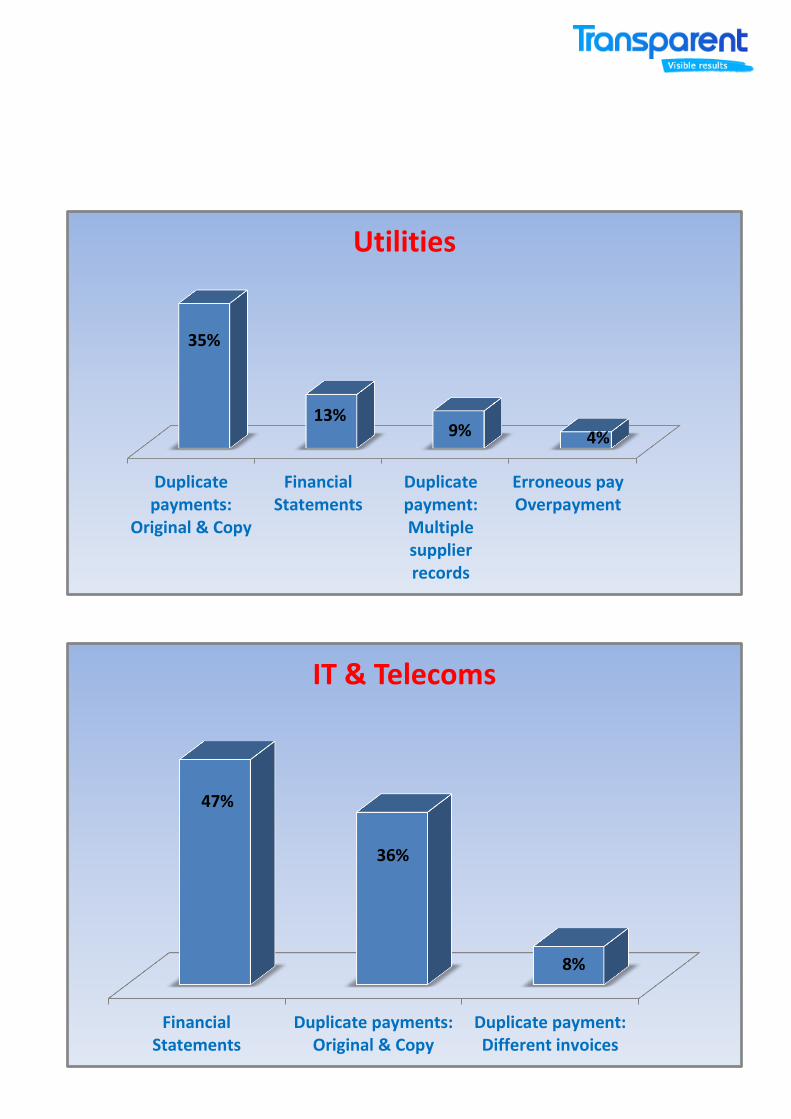

35%

13% 9% 4%

Utilities

FinancialStatements

Duplicate payments:Original & Copy

Duplicate payment:Different invoices

47%

36%

8%

IT & Telecoms

Duplicatepayments

Original & Copy

FinancialStatements

Duplicatepayment:Multiple

supplier records

Duplicatepayment:Differentinvoices

32%

19%

6% 4%

Wholesale & Retail

Short-term and long-term solutions

Short term: Vendor master file cleansing and enrichment

A short-term solution to reduce the number of errors is to update your data by analyzing

your supplier database for duplicate, incorrect, outdated and incomplete data.

This involves supplementing your files using relevant data, such as activity codes,

industry classification codes, registration numbers and other relevant and useful fields.

A corrupt supplier file results in undue payments and unknown due payments.

A supplier file would partially prevent this. It is therefore advisable that you check your

Vendor Master file for errors every few years.

The maintenance of a supplier file is extremely error-sensitive. Since the consequences

of a corrupt supplier file can be significant, the creation of a new creditor or the

modification of existing Accounts Payable data must remain the responsibility of a

restricted number of persons. The responsibilities of these individuals may not include

invoice input, purchase orders or the authorization of invoices. Additions to the supplier

file must be reported to management for verification and approval.

Short term: Suppliers with small-amount invoices

Making arrangements with suppliers that send small-amount invoices can also prevent

anomalies. If these suppliers send one invoice which consists of multiple small invoices,

instead of one invoice per order, the workload will be reduced.

Short term: Payment terms check

Another way to make the Accounts Payable process more efficient is to have a clear

overview of the payment terms of your suppliers. When an organisation has many

suppliers with different payment terms it is easily possible to overlook interest and

discounts. For example when the payment term of a supplier is 60 days and the invoice

is paid within 28 days, you miss interest on (60-28) 32 days. To provide insight in the

different payment terms of suppliers we recommend you to do a payment term check.

By means of Days Payable Outstanding (DPO) Transparent measures the average

number of days an organisation takes to pay its suppliers. It is also possible that the

supplier offers a discount if the invoice is paid earlier than the given timeframe. If this is

the case, paying the invoice earlier than the given payment term can save you money.

Long term: Analysis and process optimization

Of course, companies strive for a long-term solution in optimizing their Accounts

Payable process. Some companies choose to automate their Accounts Payable process or

centralize financial and other processes in shared service centres and/or start using E-

invoicing. These solutions do professionalize the payment process but unfortunately

human errors still occur. Because of the inevitable human factor we have

recommendations which could be easier to implement and will optimize the Accounts

Payable process.

Long term: Continuous monitoring

Continuous monitoring or as we call it Real-Time audit. Transparent uses a state-of-the-

art online dashboard, to provide clients with data in a clear manner. The difference

between a dashboard which is generally used and this kind of dashboard is that clients

can monitor the Accounts Payable process live at any moment in time.

They also receive up-to-date and accurate management information which they can use

to make their Accounts Payable process more efficient.

Long term: Analytics and process improvement

It is recommended that you only use original invoices for a payment. If no original

invoice has been received and the creditor is unable to supply one again, then it is of

great importance to accurately check that a payment has not been previously effected.

That way, you prevent making a payment on the basis of both an original invoice and an

invoice copy. It is also important to periodically examine and discuss unclear, expired

and unsettled purchase orders, invoices and other receipts.

If companies work with different accounting systems and enter invoices in other

divisions, then the probability of undue payments and unknown due payments is

considerably greater. We therefore recommend using a single accounting system (if

possible) and a single division for entering invoices. The already initiated digitization of

the records archive can be of further help for the correct administration of your

payment data.

You can automatically pay the invoices to specific suppliers. You can exercise

control over this by means of a random check.

We recommend that the purchasing department make arrangements with

suppliers that submit large numbers of invoices for small amounts to send a

monthly consolidated invoice instead of daily or per delivery.

It is possible to pay such suppliers a monthly advance against which they strike

off their invoices. The supplier would then submit a statement each month as

well as an annual settlement.

Founded in 2000, Transparent is an international financial-services provider specialised in data

mining of accounts-payable (AP) data. The company has rapidly grown, serving clients globally, with

operations in the Netherlands, Germany, Belgium, India, France, the United Kingdom, Italy and the

United States of America.

Based on hard, objective data we help our clients to reduce risks, errors, complexity and drive costs in AP processes. Alongside the analysis we recover lost working capital on a no-recovery no-fee principal. Transparent proposition

Provide a quality and in-depth measurement of all AP data (free of charge) Benchmark the performance of AP processes against industry peers (free of charge) Provide in-depth analysis and tailored improvement recommendations (free of charge) Identify, verify and collect all undue payments (no-recovery no-fee) Have all this done without any up-front investments or any use of resources, within a matter

of weeks to months The exercise is risk free, effortless and quick, there is nothing to lose and so much to gain!

Transparent approach

Benchmark - All data with a total of more than 950 billion euro in financial data worldwide is stored in a centralized database, which allows us to benchmark our clients performance against their industry peers on more than 30 different benchmarks.

Software - Our data mining software incorporates 10 years of know-how and searches for suspect transactions based on 26 different criteria.

6-eye principle - We manually process the check list, applying triple control in order to guarantee full data insight.

Secure process - Our people are screened (Trigion) and our database and application servers are hosted in a secured environment (RSA).

All data analysed - Our process is fully industrialized, in the sense that we have split it up into various sub-steps. Per step we have assigned a dedicated team of specialists who only oversee their part of the process. A suite of software tools seamlessly integrates the various steps and enforces that each part of the process is completely covered without loose ends. We do not investigate a subset of the data (e.g., only high invoice amounts, or only a cross-section sampling), but all the data.

Statement research - Our Statements department asks our clients’ suppliers for a statement of open credits. This usually involves, for each individual supplier, looking up updated address and telephone numbers, sending several mailings and making multiple phone calls.

International scope - Our international scope requires that we have several language specialists in-house, able to write and speak the foreign languages that are needed when contacting vendors abroad.

Online dashboard - All information is made available to our client in an online, interactive dashboard.

No extra work or efforts - We do all the work, including the actual recovery; we make sure that our customers, apart from providing the ERP data, do not have to allocate any resources for the project.

Data cleansing – Matching: the systematic comparison of your own file with our up-to-date, reliable reference file; Removal of duplication: tracking down suppliers which occur more than once in your file; Correction: amending incorrect data.

Data insight: We offer insight in your data, benchmark your data and discover trends in order to reduce errors, risks & complexity in your AP process.