how to lead, support and enhance title iv & grant management compliance presented by:michelle...

TRANSCRIPT

1

How to Lead, Support and Enhance Title IV & Grant Management

Compliance

Presented by: Michelle Spriggs Patricia Gallagher

Susan Jenks Beard

1 2

Presenters

• Michelle Spriggs, CPA, MBA– Director, CBIZ Tofias & Mayer Hoffman

McCann P.C.

• Patricia Gallagher, CPA– Associate VP for Financial Affairs, Franklin W.

Olin College of Engineering

• Susan Jenks Beard– Director of Financial Aid, Wheaton College

2 3

Agenda

• Federal spending• The regulatory environment• Key risks with grants management and

Title IV compliance• Common A-133 findings• Preparing for a successful A-133 audit• Selecting an A-133 auditor• Best practices for detection and

remediation

3 4

Prime Award FederalSpending FY 2012

$0$100$200$300$400

$344.5

$68$3.8

Fed

era

l S

pen

din

g (i

n b

illion

s)

Source: USAspending.gov

4 5

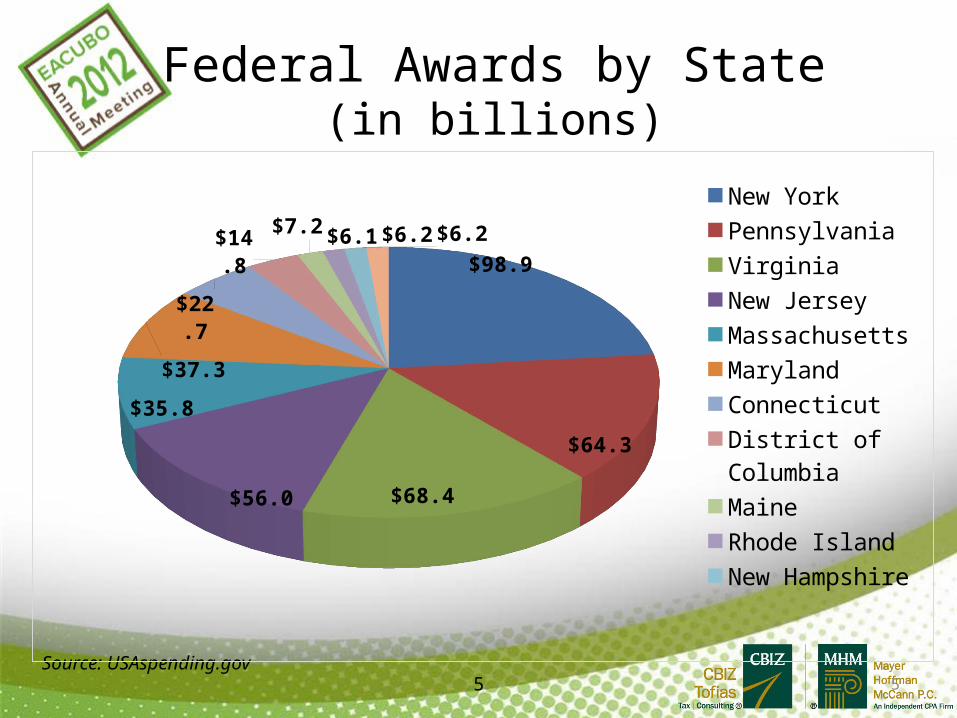

Federal Awards by State(in billions)

Source: USAspending.gov

$98.9

$64.3

$68.4$56.0

$35.8

$37.3

$22.7

$14.8

$7.2

$6.1 $6.2 $6.2

New YorkPennsylvaniaVirginiaNew JerseyMassachusettsMarylandConnecticutDistrict of Co-lumbiaMaineRhode IslandNew HampshireDelaware

5 6

Changing Regulatory Environment

“Transparency Promotes Accountability.”

H. Glenn Walker, Executive Director of the Recovery Accountability and Transparency Board, to the AICPA National Governmental Accounting and Auditing Update Conference – August 2010

6 7

Changing Regulatory Environment (Cont.)

• Congressional interest

– 2008 audit quality hearings– Focus on for-profit institutions is trickling

down to not-for-profit institutions– Senator Grassley initiating audits for

specific situations that he feels warrant attention

7 8

Changing Regulatory Environment (Cont.)

• Presidential interest

– 2009 Executive Order– 2011 Memorandum• Reduce payment errors• Eliminate fraud, abuse, waste• Improve effectiveness of single audits

towards identifying improper payments• Identify opportunities to reform grant

policies and streamline or eliminate single audit requirements where minimal value

8 9

Changing Regulatory Environment (Cont.)

• GAO evaluated the single audit concept

– Congress should designate a federal entity to evaluate and comprehensively monitor the single audit process

– Assess the efficiency and effectiveness of how agencies carry out their single audit responsibilities

– Consider simplified alternatives to small entities

– Achieve a balance between risk and cost effective accountability

9 10

Changing Regulatory Environment (Cont.)

• More government oversight coming our way

– OMB considering a Grants Governance Board– Each federal agency to appoint a Chief

Financial Assistance Officer and Single Audit Coordinator

– OMB to establish a senior position to coordinate federal agency efforts

– OMB is considering comments for potential changes to cost circulars

10 11

Changing Regulatory Environment (Cont.)

• DOE announcement letter 1/17/12

– Bolstering enforcement of due date regulations for financial and compliance audits

– Late reporting is deemed indicative of a lack of financial responsibility and administrative capacity and may indicate mismanagement of Title IV funds

11 12

Changing Regulatory Environment (Cont.)

• DOE announcement letter 1/17/12 (Cont.)

– Institution may be sited for a past performance violation

– Will cause failure of financial responsibility requirements

– Continued participation in the Title IV program will require:• Provisional certification• Posting of LOC at 10% of Title IV funds received• Use of heightened cash payment method

12 13

Changing Regulatory Environment (Cont.)

• Revised incentive compensation rules in effect July 1, 2011 prohibiting incentive compensation to individuals or entities involved in recruiting students or making awards of student aid– compliance with these rules needs to be

monitored on a consistent basis

• OMB issued a Q&A on Federal Funding Accountability and Transparency Act (FFATA) compliance testing

13 14

Changing Regulatory Environment (Cont.)

• US Court of Appeals for the District of Columbia upheld a lower court ruling that struck down part of the state authorization requirement in the Department of Education’s program integrity rules

• US District Court of Columbia recently vacated most of the gainful employment rules

14 15

Changing Regulatory Environment (Cont.)

• Other areas of focus– Third party servicers• NSLDS reporting• Perkins loans administration

– Title IV refunds• Incorrect calculations • Late returns

– Travel and expense reporting– Documentation deficiencies – policies and

procedures not documented or up-to-date

15 16

Changing Regulatory Environment (Cont.)

• Future changes to the Single Audit regulations

– Increase the audit threshold to $1 million– Create a new category of audit requirement

for expenditures between $1 million and $3 million

– No significant changes for expenditures over $3 million

– 9 month due date of A-133 audit likely to become 6 months

16 17

What Keeps You Up at Night

How will a noncompliance matter impact the institution’s reputation and future funding?

Is the system we are using providing me with the appropriate data to make informed decisions?- i.e. detailed monthly budget to actual reporting for accountability

17 18

What Keeps You Up at Night

The amount of time it takes to administer the programs we have can be cumbersomeHow can we do a better job modeling the right behaviors to ensure compliance across all departments?

Do program managers understand how to manage their budgets?

18 19

What Keeps You Up at Night

What is going on in my decentralized institution that they aren’t telling me?How do I know those who are responsible for Title IV and grants compliance are fulfilling their responsibilities?- Especially when they do not report to me

19 20

What Keeps You Up at Night

How are others being crossed trained to insure no interruption of service when changes in personnel occur?

How can those who are responsible keep up with the changing regulatory environment?

How do I know my auditors are competent and will be collaborative and work with me to solve problems – not make new ones?

20 21

What Grants ComplianceManagement IS

• Collaborative effort among all departments within the institution that has an impact on grant compliance

• Don’t forget SFA department and their role

Grant Complia

nce Office

Finance Office

Human Resourc

es

Programmatic Staff

21 22

What Grants Compliance Management IS NOT

• An effort placed solely on the shoulders of one individual or department– Grant compliance officer– Grants accountant– Program director– SFA department

• An “enigma” the institution perceives as having no relation to securing new funds

• Someone else’s responsibility

22 23

Obstacles to Compliance

• Inadequate resources– Staff training, professional development

• Poorly defined roles and responsibilities

• Nonexistent or outdated policies and procedures related to federal grants management

• Poor information systems

• Poor conception of the importance of compliance and internal controls

23 24

Systems Management

EffectiveFinancial

Management

2WrittenPolicies &

Procedures

1RegulatoryRequirements

3Documentof

Expenses

4ManagingCash

5EfficientAccounting

System6BudgetControls

7Time &Activity

Documentation

8MatchingRequirements &

In-kind Contribution

9Reporting

10Internal

24 25

Goals of the A-133Audit Process

• Remain in good standing with federal government and pass-through entities

• Minimize impact on your institution– Avoid repercussions from a bad audit–Minimize audit costs– Identify problematic areas

• Keep good reputation in the community

25 26

A-133 Findings Summary

Year Total # of programs/

clusters reported

Percentage with findings

reported

Increase in programs/

clusters reported

Change in rate of

findings

2010 730,953 16.39% 17.82% -1.78%

2009 620,416 18.17% 7.15% 1.43%

2008 578,997 16.74% 0.24% -1.99%

2007 577,628 18.73%

Summary of findings reported on Data Collection Forms during 2007-2010

*Information obtained from the Federal Audit Clearinghouse

26 27

Top 5 A-133 FindingsSummary of findings reported on Data Collection Forms during 2007-2010

*Summarized using information obtained from the Federal Audit Clearinghouse

Allowable Costs/Cost PrinciplesReporting

Other

Procurement/Suspension/Debarment

Equipment/Real Property Mgmt.0

2,0004,0006,0008,000

10,00012,00014,00016,00018,00020,000

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

18,757

15,573

13,313

9,5988,398

17%

14%

12%

9%

8%

Average # of Annual Findings Reported Percentage

27 28

Common A-133 Findings

• Time and effort reporting

– Salaries are charged based on actual time incurred and not budgeted time

– Documentation exists based on level of effort performed• Can be timesheet or other documentation

directly from the individual on a periodic basis verifying actual time spent and charged

28 29

Common A-133 Findings (Cont.)

• Time and effort reporting (Cont.)

– HHS and NSF OIGs expressed concern and being aggressive in areas of noncompliance

– Several high-profile universities fined– Auditor work being reviewed

29 30

Common A-133 Findings (Cont.)

• Subrecipient monitoring

– Area of federal focus (i.e. FFATA reporting)– Comprehensive written policy needed

• Consideration of for-profit and foreign subs• Procedures when A-133 reports are not

required by subs

– Annual risk assessment – at a minimum– Quality of the A-133 audit review process– Quality of follow-up actions

30 31

Common A-133 Findings (Cont.)

• Procurement

– Documentation of bid or sole source decision• Material and services• Subrecipient selection

– Name of a vendor or subrecipient in an award application or proposal is not indicative of federal approval of such

– Review of debarment of vendors or subrecipients

31 32

Preparing for a Successful A-133 Audit

• Proper scheduling of fieldwork– Coordination with multiple departments

• Timeline for deliverables for all

• Explicit PBC listing– Ask questions to know what your auditor

is looking for

32 33

Preparing for a Successful A-133 Audit (Cont.)

• Actively manage the workflow– Assign a point person

• Manage the process– Have regular progress meetings– Discuss emerging concerns

• No surprises!

– Push back when appropriate– Use everything learned for improvements for

next year

33 34

Preparing for a Successful A-133 Audit (Cont.)

• Responding to findings

– Campus “tone at the top” – commitment to get things right

– Identify the real problem• Fix the disease not the symptom

– Obtain buy-in from all involved– Create training opportunities– Start action plans ASAP

34 35

Preparing for a Successful A-133 Audit (Cont.)

• Complete and accurate Schedule of Expenditures of Federal Awards (SEFA)– Pass through entities and identifying numbers– ARRA funds– Clusters

• Programs/clusters > $300k may be audited

• Programs/clusters with ARRA $ may be audited

35 36

Preparing for a Successful A-133 Audit (Cont.)

• Identification of research and development programs– National Science Foundation– Check data collection forms for how

CFDA numbers reported by other institutions

http://harvester.census.gov/sac/

36 37

Preparing for a Successful A-133 Audit (Cont.)

• Understanding and identifying applicable compliance requirements

• Read and understand the grant agreements

• Obtain and review the latest version of A-133 Compliance Supplement

http://www.whitehouse.gov/omb/circulars/a133_compliance_supplement_2012

37 38

Preparing for a Successful A-133 Audit (Cont.)

• Be familiar with applicable cost circulars

– A-21 Cost Principles for Educational Institutionshttp://www.whitehouse.gov/sites/default/files/omb/assets/omb/circulars/a021/a21_2004.pdf

– A-122 Cost Principles for NFP Organizationshttp://www.whitehouse.gov/sites/default/files/omb/assets/omb/circulars/a122/a122_2004.pdf

38 39

Preparing for a Successful A-133 Audit (Cont.)

• Organized files

• Supporting documentation for expenses, eligibility, procurement, subrecipient monitoring

• Appropriate approvals

If it’s not documented…….it didn’t happen!

39 40

Selecting an A-133 Auditor

• Demonstration of qualifications– Number of A-133 clients

• Both the firm and the individuals assigned

– Types of programs and agencies auditing– Are A-133 auditors local – How often is the partner/senior manager in the field– Participation in improvement programs like GAQC

• Look up some of their audits (Mass AG and DCF sites)

40 41

Selecting an A-133 Auditor (Cont.)

• Talk to references– How practical are they to work with– How knowledgeable is the team

• Review results of external peer review

• Members of SFA and Grants Management departments involved in the interview process

41 42

Best Practices for Detection and Remediation

• Create a grants and/or Title IV administration program that incorporates the A-133 compliance requirements and internal controls framework

– Ensure all expenditures approved by program manager

– Documentation sufficient to determine nature of expenditure and allowability kept

42 43

Best Practices for Detection and Remediation (Cont.)

• Expect personnel responsible for these areas to manage awards considering A-133 compliance requirements

• Ensure responsible personnel are keeping abreast of changes in policies or requirements– Attending key conferences and seminars– Members of relevant associations and list

serves

43 44

Best Practices for Detection and Remediation (Cont.)

• Collaborating among departments– Regular budget to actual reviews and

discussions of variances– Promote an environment of open

communication so decisions are not made without considering impact on other areas

• Establish a system of budget control and monitoring

44 45

Best Practices for Detection and Remediation (Cont.)

• Use a strong accounting and performance reporting system– Each grant has its own accounting

record/cost center– Accounting record/cost center tracks

expenditures to approved budget

• Consider an internal audit process

45 46

Education of Governance

46 47

Questions?

•[email protected]•(774) 206-8336

Michelle Spriggs

•[email protected]•(781) 292-2416

Patty Gallagher

•[email protected]•(508) 286-8232

Susan Jenks Beard