how does the market react to cooling measures? the case of

TRANSCRIPT

How does the market react to cooling measures?The case of Singapore

T. Xie1 S.-K. Chao2 R. Schulz3 W. K. Hardle4

1Singapore Management University

2Purdue University

3University of Aberdeen

4Humboldt University of Berlin

February 22, 2017

To buy or not to buy?

Macro-prudential Policies Post-crisis

I Monetary policy became a “blunt tool”I Central banks turned to macro-prudential policies

I e.g. loan-to-value ratio, stamp duties, etcI mostly aimed at housing market

I Objectives of MPPs

1. to promote the resilience of the financial system by mandatinghigher levels of liquidity, capital and collateralisation

2. to restrain the build-up of financial imbalances by slowingcredit and asset price growth

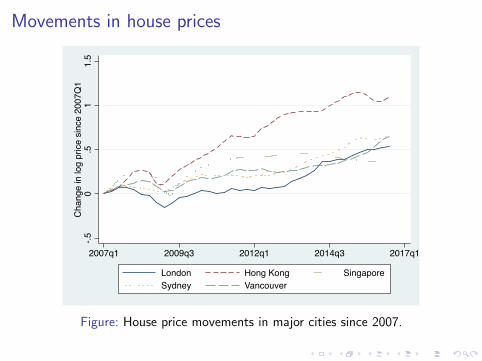

Movements in house prices

-.50

.51

1.5

Cha

nge

in lo

g pr

ice

sinc

e 20

07Q

1

2007q1 2009q3 2012q1 2014q3 2017q1

London Hong Kong SingaporeSydney Vancouver

Figure: House price movements in major cities since 2007.

How does macro-prudential policies work?

I Lean against the wind (Zhang and Zoli 2016)

I Discretion vs rule (Kuttner and Shim 2016)

I House price indices still show upward trends

Monetary vs macro-prudential policies

I Interest rate affects consumption and investmentsI hence the inflation

I LTV, DSTI ratios affect demand for loansI affect the demand for housing only indirectlyI hence the house price more indirectly

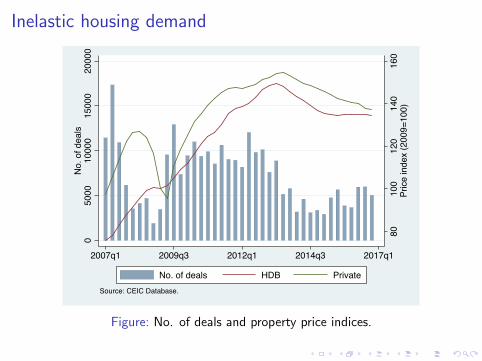

Inelastic housing demand

8010

012

014

016

0Pr

ice

inde

x (2

009=

100)

050

0010

000

1500

020

000

No.

of d

eals

2007q1 2009q3 2012q1 2014q3 2017q1

No. of deals HDB PrivateSource: CEIC Database.

Figure: No. of deals and property price indices.

Outline

I Motivation

I Singapore’s context

I Methodology and data

I Results

I Conclusion

Singapore’s housing market

I Public housing sector is dominant (Phang 2001)I Singapore citizens can afford their first homes

I Prone to foreign speculation (Chow and Xie 2016)I Free mobility of capital in and out of the real estate sectorI Foreign investors have freedom in acquiring private properties

in Singapore

I Challenge to policy makersI Housing market needs to remain attractive to investorsI At the same time affordable to local residents and

fundamentally healthy

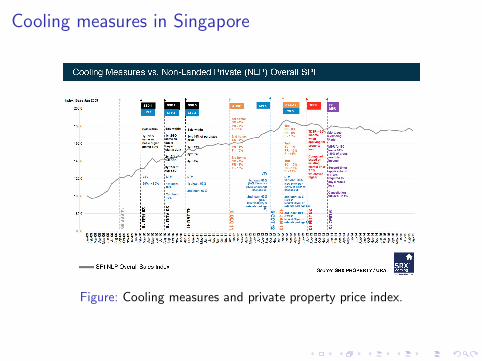

Cooling measures in Singapore

Figure: Cooling measures and private property price index.

Cooling measures in Singapore

Figure: Cooling measures and private property price index.

Data

I SRX data for private and HDB transactions spanning fromJan 1, 2007 to Jun 30, 2016

I PriceI SizeI Geo-locationI Property type

I Monthly consumer price index from the CEIC Database

I We calculate the log real price per square foot

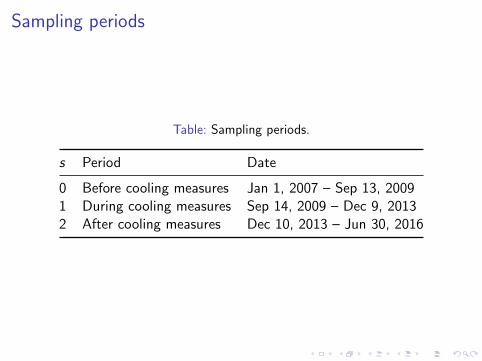

Sampling periods

Table: Sampling periods.

s Period Date

0 Before cooling measures Jan 1, 2007 – Sep 13, 20091 During cooling measures Sep 14, 2009 – Dec 9, 20132 After cooling measures Dec 10, 2013 – Jun 30, 2016

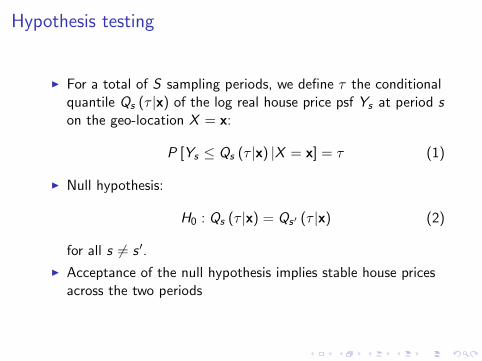

Hypothesis testing

I For a total of S sampling periods, we define τ the conditionalquantile Qs (τ |x) of the log real house price psf Ys at period son the geo-location X = x:

P [Ys ≤ Qs (τ |x) |X = x] = τ (1)

I Null hypothesis:

H0 : Qs (τ |x) = Qs′ (τ |x) (2)

for all s 6= s ′.

I Acceptance of the null hypothesis implies stable house pricesacross the two periods

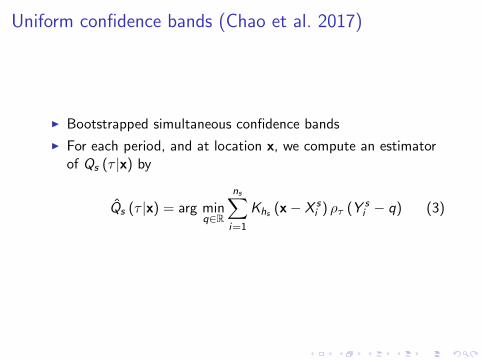

Uniform confidence bands (Chao et al. 2017)

I Bootstrapped simultaneous confidence bands

I For each period, and at location x, we compute an estimatorof Qs (τ |x) by

Qs (τ |x) = arg minq∈R

ns∑i=1

Khs (x− X si ) ρτ (Y s

i − q) (3)

Uniform confidence bands

I Hardle, Ritov, and Wang 2015 and Chao et al. 2017

I The simultaneous confidence set with nominal level α:

Cs (X0) :={

(x, q) ∈ X0 × R : q ∈[Qs (τ |x)± cτ,nξ

∗α

]}(4)

where cτ,n is the scaling factor

cτ,n :=

√√√√ τ(1− τ)

ns |hs |fX s (x)f 2Y s |X s

(Qs(τ |x)|x

) (5)

I The null hypothesis is rejected when two confidence sets(s 6= s ′) are disjoint:

Cs (X0) ∩ Cs′ (X0) = ∅ (6)

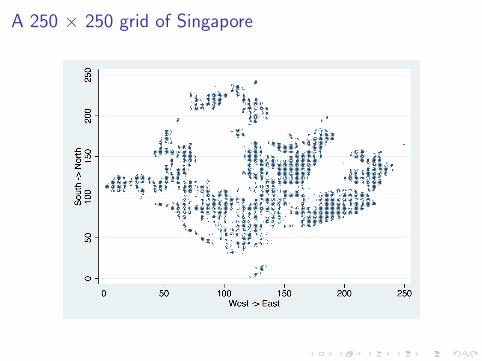

A 250 × 250 grid of Singapore

From west to east

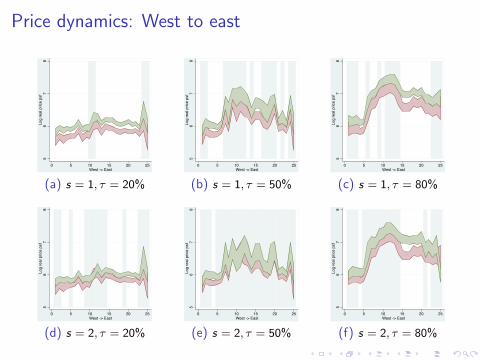

Price dynamics: West to east5

67

8Lo

g re

al p

rice

psf

0 5 10 15 20 25West -> East

(a) s = 1, τ = 20%5

67

8Lo

g re

al p

rice

psf

0 5 10 15 20 25West -> East

(b) s = 1, τ = 50%

56

78

Log

real

pric

e ps

f

0 5 10 15 20 25West -> East

(c) s = 1, τ = 80%

56

78

Log

real

pric

e ps

f

0 5 10 15 20 25West -> East

(d) s = 2, τ = 20%

56

78

Log

real

pric

e ps

f

0 5 10 15 20 25West -> East

(e) s = 2, τ = 50%5

67

8Lo

g re

al p

rice

psf

0 5 10 15 20 25West -> East

(f) s = 2, τ = 80%

Price dynamics: South to north4

68

1012

Log

real

pric

e ps

f

0 5 10 15 20 25South -> North

(g) s = 1, τ = 20%4

68

1012

Log

real

pric

e ps

f

0 5 10 15 20 25South -> North

(h) s = 1, τ = 50%

46

810

12Lo

g re

al p

rice

psf

0 5 10 15 20 25South -> North

(i) s = 1, τ = 80%

46

810

12Lo

g re

al p

rice

psf

0 5 10 15 20 25South -> North

(j) s = 2, τ = 20%

46

810

12Lo

g re

al p

rice

psf

0 5 10 15 20 25South -> North

(k) s = 2, τ = 50%4

68

1012

Log

real

pric

e ps

f

0 5 10 15 20 25South -> North

(l) s = 2, τ = 80%

MRT stations in Singapore

Neighbourhood of an MRT station: Toa Payoh

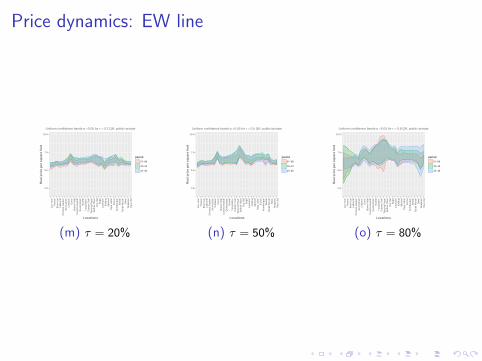

Price dynamics: EW line

2.5

5.0

7.5

10.0

Joo

Koo

nP

ione

erB

oon

Lay

Lake

side

Chi

nese

Gar

den

Juro

ng E

ast

Cle

men

tiD

over

Buo

na V

ista

Com

mon

wea

lthQ

ueen

stow

nR

edhi

llT

iong

Bah

ruO

utra

m P

ark

Tanj

ong

Pag

arR

affle

s P

lace

City

Hal

lB

ugis

Lave

nder

Kal

lang

Alju

nied

Pay

a Le

bar

Eun

osK

emba

ngan

Bed

okTa

nah

Mer

ahS

imei

Tam

pine

sP

asir

Ris

Locations

Rea

l pric

e pe

r sq

uare

foot

period

07−09

10−13

14−16

Uniform confidence bands α =0.05 for τ = 0.2 QR, public+private

(m) τ = 20%

2.5

5.0

7.5

10.0

Joo

Koo

nP

ione

erB

oon

Lay

Lake

side

Chi

nese

Gar

den

Juro

ng E

ast

Cle

men

tiD

over

Buo

na V

ista

Com

mon

wea

lthQ

ueen

stow

nR

edhi

llT

iong

Bah

ruO

utra

m P

ark

Tanj

ong

Pag

arR

affle

s P

lace

City

Hal

lB

ugis

Lave

nder

Kal

lang

Alju

nied

Pay

a Le

bar

Eun

osK

emba

ngan

Bed

okTa

nah

Mer

ahS

imei

Tam

pine

sP

asir

Ris

Locations

Rea

l pric

e pe

r sq

uare

foot

period

07−09

10−13

14−16

Uniform confidence bands α =0.05 for τ = 0.5 QR, public+private

(n) τ = 50%

2.5

5.0

7.5

10.0

Joo

Koo

nP

ione

erB

oon

Lay

Lake

side

Chi

nese

Gar

den

Juro

ng E

ast

Cle

men

tiD

over

Buo

na V

ista

Com

mon

wea

lthQ

ueen

stow

nR

edhi

llT

iong

Bah

ruO

utra

m P

ark

Tanj

ong

Pag

arR

affle

s P

lace

City

Hal

lB

ugis

Lave

nder

Kal

lang

Alju

nied

Pay

a Le

bar

Eun

osK

emba

ngan

Bed

okTa

nah

Mer

ahS

imei

Tam

pine

sP

asir

Ris

Locations

Rea

l pric

e pe

r sq

uare

foot

period

07−09

10−13

14−16

Uniform confidence bands α =0.05 for τ = 0.8 QR, public+private

(o) τ = 80%

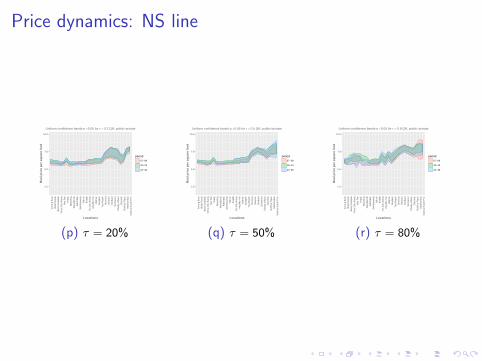

Price dynamics: NS line

2.5

5.0

7.5

10.0

Juro

ng E

ast

Buk

it B

atok

Buk

it G

omba

kC

hoa

Chu

Kan

gYe

w T

eeK

ranj

iM

arsi

ling

Woo

dlan

dsA

dmira

ltyS

emba

wan

gY

ishu

nK

hatib

Yio

Chu

Kan

gA

ng M

o K

ioB

isha

nB

radd

ell

Toa

Pay

ohN

oven

aN

ewto

nO

rcha

rdS

omer

set

Dho

by G

haut

City

Hal

lR

affle

s P

lace

Mar

ina

Bay

Mar

ina

Sou

th P

ier

Locations

Rea

l pric

e pe

r sq

uare

foot

period

07−09

10−13

14−16

Uniform confidence bands α =0.05 for τ = 0.2 QR, public+private

(p) τ = 20%

2.5

5.0

7.5

10.0

Juro

ng E

ast

Buk

it B

atok

Buk

it G

omba

kC

hoa

Chu

Kan

gYe

w T

eeK

ranj

iM

arsi

ling

Woo

dlan

dsA

dmira

ltyS

emba

wan

gY

ishu

nK

hatib

Yio

Chu

Kan

gA

ng M

o K

ioB

isha

nB

radd

ell

Toa

Pay

ohN

oven

aN

ewto

nO

rcha

rdS

omer

set

Dho

by G

haut

City

Hal

lR

affle

s P

lace

Mar

ina

Bay

Mar

ina

Sou

th P

ier

Locations

Rea

l pric

e pe

r sq

uare

foot

period

07−09

10−13

14−16

Uniform confidence bands α =0.05 for τ = 0.5 QR, public+private

(q) τ = 50%

2.5

5.0

7.5

10.0

Juro

ng E

ast

Buk

it B

atok

Buk

it G

omba

kC

hoa

Chu

Kan

gYe

w T

eeK

ranj

iM

arsi

ling

Woo

dlan

dsA

dmira

ltyS

emba

wan

gY

ishu

nK

hatib

Yio

Chu

Kan

gA

ng M

o K

ioB

isha

nB

radd

ell

Toa

Pay

ohN

oven

aN

ewto

nO

rcha

rdS

omer

set

Dho

by G

haut

City

Hal

lR

affle

s P

lace

Mar

ina

Bay

Mar

ina

Sou

th P

ier

Locations

Rea

l pric

e pe

r sq

uare

foot

period

07−09

10−13

14−16

Uniform confidence bands α =0.05 for τ = 0.8 QR, public+private

(r) τ = 80%

Price dynamics: NE line

2.5

5.0

7.5

10.0

Har

bour

fron

t

Out

ram

Par

k

Chi

nato

wn

Cla

rke

Qua

y

Dho

by G

haut

Littl

e In

dia

Farr

er P

ark

Boo

n K

eng

Pot

ong

Pas

ir

Woo

dlei

gh

Ser

ango

on

Kov

an

Hou

gang

Bua

ngko

k

Sen

gkan

g

Pun

ggol

Locations

Rea

l pric

e pe

r sq

uare

foot

period

07−09

10−13

14−16

Uniform confidence bands α =0.05 for τ = 0.2 QR, public+private

(s) τ = 20%

2.5

5.0

7.5

10.0

Har

bour

fron

t

Out

ram

Par

k

Chi

nato

wn

Cla

rke

Qua

y

Dho

by G

haut

Littl

e In

dia

Farr

er P

ark

Boo

n K

eng

Pot

ong

Pas

ir

Woo

dlei

gh

Ser

ango

on

Kov

an

Hou

gang

Bua

ngko

k

Sen

gkan

g

Pun

ggol

Locations

Rea

l pric

e pe

r sq

uare

foot

period

07−09

10−13

14−16

Uniform confidence bands α =0.05 for τ = 0.5 QR, public+private

(t) τ = 50%

2.5

5.0

7.5

10.0

Har

bour

fron

t

Out

ram

Par

k

Chi

nato

wn

Cla

rke

Qua

y

Dho

by G

haut

Littl

e In

dia

Farr

er P

ark

Boo

n K

eng

Pot

ong

Pas

ir

Woo

dlei

gh

Ser

ango

on

Kov

an

Hou

gang

Bua

ngko

k

Sen

gkan

g

Pun

ggol

Locations

Rea

l pric

e pe

r sq

uare

foot

period

07−09

10−13

14−16

Uniform confidence bands α =0.05 for τ = 0.8 QR, public+private

(u) τ = 80%

Findings

I Cooling measures are more likely to suppress demand forloans, not for housing

I We observe a pattern of substitution effect down the pricedistribution

I Prices of the high-end houses are cooled first

I Prices at the lower percentiles respond to cooling measureswith lags

Upcoming plan

I Use different independent variables:I E.g. distance from MRT stations

I Use specific policy tools as independent variables:I LTV ratioI Debt servicing ratioI Stamp duties

Thank you!

References I

Chao, Shih-Kang et al. (2017). “Confidence Corridors forMultivariate Generalized Quantile Regression”. In: Journal ofBusiness & Economic Statistics 35.1, pp. 70–85. issn:0735-0015. doi: 10.1080/07350015.2015.1054493. url:http://dx.doi.org/10.1080/07350015.2015.1054493.

Chow, Hwee Kwan and Taojun Xie (2016). “Are House PricesDriven by Capital Flows? Evidence from Singapore”. In: Journalof International Commerce, Economics and Policy 07.01,p. 1650006. doi: 10.1142/S179399331650006X. url:http://www.worldscientific.com/doi/abs/10.1142/

S179399331650006X.

References II

Hardle, Wolfgang Karl, Ya’acov Ritov, and Weining Wang (2015).“Tie the straps: Uniform bootstrap confidence bands forsemiparametric additive models”. In: Journal of MultivariateAnalysis 134, pp. 129–145. issn: 0047-259X. doi:10.1016/j.jmva.2014.11.003. url:http://www.sciencedirect.com/science/article/pii/

S0047259X14002395.Kuttner, Kenneth N. and Ilhyock Shim (2016). “Can non-interest

rate policies stabilize housing markets? Evidence from a panel of57 economies”. In: Journal of Financial Stability 26, pp. 31–44.issn: 1572-3089. doi: 10.1016/j.jfs.2016.07.014. url:https://www.sciencedirect.com/science/article/pii/

S1572308916300705.

References III

Phang, Sock-Yong (2001). “Housing Policy, Wealth Formation andthe Singapore Economy”. In: Housing Studies 16.4,pp. 443–459. issn: 0267-3037. doi:10.1080/02673030120066545. url:http://dx.doi.org/10.1080/02673030120066545.

Zhang, Longmei and Edda Zoli (2016). “Leaning against the wind:Macroprudential policy in Asia”. In: Journal of Asian Economics42, pp. 33–52. issn: 1049-0078. doi:10.1016/j.asieco.2015.11.001. url:http://www.sciencedirect.com/science/article/pii/

S1049007815001025.