how do firms combine different internationalisation modes? a multivariate probit approach

TRANSCRIPT

ORI GIN AL PA PER

How do firms combine different internationalisationmodes? A multivariate probit approach

Pinuccia Calia • Maria Rosaria Ferrante

Published online: 28 August 2013

� Kiel Institute 2013

Abstract Most of the literature on the relationship between firm’s participation in

international markets and firm heterogeneity focuses on export and foreign direct

investment. This paper considers a wider range of forms of internationalisation that

firms could combine into different patterns. With the purpose of analysing the

selection of heterogeneous firms into different internationalisation patterns, we

jointly model the decisions on the forms of internationalisation through a multi-

variate probit. This model allows us to avoid any a priori assumption about the

firm’s behaviour. In this context we study the complementarity/substitutability

relationships between forms of internationalisation. The results obtained show that:

(i) neglecting some forms could lead to an incomplete representation about the

firm’s internationalisation strategy, (ii) different firm’s characteristics influence the

choice of internationalisation pattern, i.e. some types of firm are more prone to

choosing one type of process over another, (iii) complementarity between forms of

internationalisation seems to be preferred over substitution, but some heterogeneity

also arises in this context.

Keywords Forms of internationalisation � Firm heterogeneity � Complementarity/

substitutability relationship � Multivariate choice model � Maximum

simulated likelihood

JEL Classification C35 � F13 � F23 � L24

P. Calia � M. R. Ferrante (&)

Department of Statistics, University of Bologna, Via Belle Arti, 41, 40126 Bologna, BO, Italy

e-mail: [email protected]

P. Calia

e-mail: [email protected]

123

Rev World Econ (2013) 149:663–696

DOI 10.1007/s10290-013-0162-5

1 Introduction

In the last decade, international trade has become one of the fastest growing

economic activities worldwide. This remarkable expansion of firms across national

borders has stimulated new theoretical developments and a considerable amount of

empirical literature, emphasising the role of firm heterogeneity in decisions relating

to the internationalisation process (for a review, see Greenaway and Kneller 2007,

and Wagner 2007, 2012).

The literature mainly focuses on forms of internationalisation such as export and

foreign direct investments (FDI) but, in the last decades, offshoring (for a review see

Wagner 2011) and non-equity forms of internationalisation have experienced a

rapid growth (Chen 2003; Palmberg and Pajarinen 2005). Besides it has been

observed that industrialised countries, in addition to the offshoring of materials, also

engage in the international outsourcing of services (Amiti and Wei 2005, 2006). In

other words, alongside the more traditional forms of internationalisation, a firm

deciding on its internationalisation process may adopt other forms of international

activity, such as strategic alliances, commercial penetration, cooperative agreements

and service outsourcing.

Despite the complexity of firm internationalisation patterns in the age of

globalization, in the literature on internationalisation we find a limited number of

empirical studies that have attempted to jointly consider a broader set of forms of

internationalisation beyond export.1

In terms of the econometric tools used to jointly model firm internationalisation

choices, multiple-choice models (ordered or unordered) have generally been used.

Benfratello and Razzolini (2009) adopt a multinomial logit model for the categories

of ‘‘no internationalisation’’, ‘‘only export’’ and ‘‘export plus horizontal FDI’’ so

they accumulate two categories by excluding the ‘‘only horizontal FDI’’ one. Also

Bougheas and Gorg (2008) estimate a multinomial logit model for the categories of

‘‘export’’, ‘‘international outsourcing of production’’ and ‘‘ownership of foreign

plant’’ by excluding some combination of them from the analysis. Basile et al.

(2003) consider the categories ‘‘export’’, ‘‘export and penetration operations’’, and

‘‘export, penetration operations and FDI’’, by modelling them with a univariate

ordered probit, thereby assuming that the three categories are ordered and that the

internationalisation process is cumulative. Recently, Oberhofer and Pfaffermayr

(2012) use a bivariate probit to model the choice between export and FDI. In the real

world, the set of choices available to a firm consist of ‘‘no internationalisation’’ and

of all the possible combinations of different internationalisation modes (where

combinations can be defined by considering two modes, three modes, and so on).

For example, if we consider modes as being export, penetration operations and FDI,

and for each mode we denote the ‘‘absence’’/‘‘presence’’ categories respectively

with 0 and 1 codes, a firm can choose the following patterns: (a) (0,0,0), indicating a

domestic firm, (b) (1,0,0) denoting firms performing only export, (c) (1,1,0)

characterising firms jointly performing export and penetration operations, and so on

1 See Basile et al. (2003); Benfratello and Razzolini (2009); Castellani and Zanfei (2007); Tomiura

(2007); Bougheas and Gorg (2008); Oberhofer and Pfaffermayr (2012).

664 P. Calia, M. R. Ferrante

123

until the category (1,1,1) that denotes firms performing all the modes considered. In

this context, choices are exhaustive and mutually exclusive and the firm chooses

only one combination of the whole set of modes available: the one that maximises

its profit function. Multiple-choice models as multinomial logit or probit become

cumbersome when a large number of forms of internationalisation is considered,

because the different forms can be combined and each combination defines a choice

representing a category of the outcome variable. Note that the number of possible

combinations to be modelled for the example presented above is equal to 9, but this

number quickly increases with the number of internationalisation modes considered

(i.e. 4 modes results in 16 choices). The solution adopted in the above-mentioned

empirical literature in order to limit the number of choices to be modelled, consists

in disregarding the information about some forms of internationalisation, or in

formulating an a priori selection of the combination of forms to be considered. The

only exception is Oberhofer and Pfaffermayr (2012): the bivariate probit can predict

all patterns of internationalisation that arise from export and FDI.

Turning to the dimensions defining the heterogeneity of firms, the literature has

largely focused on productivity. Recently, the role of other characteristics of firms

besides productivity have been stressed, including innovative behaviour, proprietary

assets, skill composition, organisational choices, accumulation of technology

(Helpman 2006).

This paper contributes to explanations of the nature of firm internationalisation

processes and of their connection to firm heterogeneity in two ways.

Firstly, to better represent the behaviour of firms, we consider a wide range of

forms of internationalisation, adding to the more traditional export modes such as

commercial penetration operations and agreements, the offshoring of production

and the outsourcing of services abroad. In this framework, we illustrate the

relevance of considering a pattern of choices that is as wide as possible in the study

of firm internationalisation strategy. We show that neglecting some choices can lead

to a partial description.

Secondly, in order to take into account the entire set of available combinations of

different forms of internationalisation and the relationships between them, we

analyse the complexity of internationalisation processes in a multivariate frame-

work. To this end, we use a multivariate probit model (MVP) that provides us with

some advantages compared to other discrete choice models already used in the

literature. In this light, our approach is similar to that taken by Oberhofer and

Pfaffermayr (2012). These authors consider two forms of internationalisation and

the resulting model is estimated with standard techniques. In the MVP model, every

internationalisation mode corresponds to a binary choice (yes/no) and an equation is

specified for each of them. In this way the number of outcome variables considered

corresponds to the number of modes, and the simultaneous choice of some modes

can be addressed through joint probabilities. At the same time, we do not need to

establish an order within the patterns of internationalisation or to exclude some

patterns from the analysis in order to limit the number of choices to be modelled.

We draw directly from predictions about how different internationalisation options

are associated and how these patterns combine with the various dimensions of firm

heterogeneity. Besides, different binary choices are modelled jointly through

A multivariate probit approach 665

123

correlations between disturbances, and this improves model estimates when

correlations are significantly different from zero. In addition, we highlight how

predictions are sensitive to the set of forms of internationalisation included in the

estimated model. By exploiting the output produced by the estimation of the MVP

model, which includes the estimated joint and conditional probabilities and their

connection with the covariates, we can address the question of complementarity

versus substitutability relationships between internationalisation modes, even if we

are limited to a simplified setting where the host market features are overcome. We

can also highlight which types of firm are more prone to choosing one type of

strategy over another.

For our analysis, we rely on data for years 2001–2003 provided by a sample

survey on Italian manufacturing firms with more than ten employees conducted

every 3 years by Capitalia Observatory,2 a very rich micro-level dataset that

includes information about various forms of international involvement. We use a

large range of covariates besides productivity to describe the heterogeneity of firms.

The paper is organised as follows: in Sect. 2 we provide a review of the literature

on the international involvement of firms; Sect. 3 presents the MVP model; Sect. 4

contains a description of the data and some descriptive statistics; Sect. 5 describes

the model specification; in Sect. 6, we present the model estimates and the results

concerning the relationship between heterogeneity and internationalisation patterns;

and Sect. 7 concludes.

2 A review of the theoretical and empirical literature

In his pioneering paper, Melitz (2003) builds a dynamic theoretical industry model

that considers the interaction between the heterogeneity of firms within the same

industry and export. Helpman et al. (2004) extend the Melitz model, highlighting

that only the most productive firms engage in foreign activity and that, among firms

that serve the foreign market, only the most productive engage in FDI. An extensive

stream of empirical literature has grown from these theoretical developments,

testing the relationship between internationalisation modes and firm heterogeneity,

with the latter typically represented by productivity. A number of studies show a

ranking of performance indicators across firms internationally involved and firms

serving only domestic markets (Head and Ries 2003; Helpman et al. 2004; Girma

et al. 2004, 2005, Greenaway and Kneller 2007). This literature focuses almost

exclusively on export and offshoring (mainly realised through FDI). For other forms

of international activity, empirical evidence is available to a much lesser extent

(Wagner 2010), whereas the study of the whole set of different options available to

firms would be essential to fully understand the behaviour of firms that operate in

the global market.

In the following, we briefly review the literature where, besides the most

frequently analysed export and FDI, other forms of internationalisation have been

considered and we mainly focus on the few studies that deal with the interaction

2 Capitalia was one of the largest Italian banks. It was recently acquired by the Unicredit group.

666 P. Calia, M. R. Ferrante

123

between the different forms. Furthermore, we also illustrate, where present, the

main results obtained in these studies in terms of determinants of the various

internationalisation modes.

Barba Navaretti et al. (2011) report the results of a survey conducted in the

framework of the European Community FP7 project ‘‘European Firms In a Global

Economy’’ (EFIGE) and involving seven European countries. The authors, besides

FDI, consider international outsourcing, achieved through arm’s-length agreements

with companies located abroad. The empirical evidence shows that, in all countries,

the majority of firms choose only one of the two modes and the low percentage of

firms engaging in both modes varies from country to country (from 13 % in Austria

to 0 % in Hungary). The estimate of a linear probability model explaining the

choice between FDI and international outsourcing shows that firm size is a dominant

factor.

Basile et al. (2003) propose a ‘‘foreign expansion index’’, which, by assuming the

categories of ‘‘export’’, ‘‘export and penetration operations’’, and ‘‘export,

penetration operations and FDI’’, accumulates various internationalisation modes.

The most important factors explaining variations in the index, detected by

estimating a univariate ordered probit model, are: firm size, vertical and horizontal

relations with other firms, various types of innovation and firm location.

A theoretical model that allows for a wide set of alternative forms of

internationalisation is proposed in Bougheas and Gorg (2008). These authors

estimate a multinomial logit on some selected combinations of export, FDI and

international outsourcing, using, as covariates, labour productivity, whether or not

the firm performs R&D activity and whether or not it provides formal training. The

results obtained show that the choice only to export relative to a purely domestic

plant is not related to productivity, but otherwise is positively related to size, R&D

and to training. They also find that the choice of whether to engage in all three

activities simultaneously is positively related to all the considered covariates, as is

the choice of whether to engage in exporting and FDI, but not in outsourcing.

Besides, they find that the choice of exporting and outsourcing, but not FDI, with

respect to the domestic choice, is not related to productivity or training activity. The

results obtained also prove the disadvantages of neglecting some of the alternatives.

In a descriptive statistical framework, Tomiura (2007) compares the productivity

of firms realizing FDI, export, and international outsourcing and investigates the

complementarity between the various globalization modes. The obtained results

show that foreign outsourcers and exporters tend to be less productive than the firms

active in FDI or in multiple globalization modes but more productive than domestic

firms. These findings are robust even controlling for other firms characteristics.

Castellani and Zanfei (2007) analyse the relationship between firm performance

and internationalisation. They distinguish between domestic firms, exporters and

two types of multinational firms, those engaged in international production and

those that control only non-manufacturing activities in foreign markets. This latter is

considered to be a sort of intermediate category between export and the creation of

foreign manufacturing affiliates. Turning to the relationship between firm hetero-

geneity and internationalisation forms, results show that the highest productivity

premium and the highest R&D efforts and innovative performances characterize

A multivariate probit approach 667

123

firms with manufacturing activities abroad. However, multinationals with a lower

involvement in foreign markets, i.e. with only non-manufacturing activities abroad,

do show levels of productivity that are lower than those of multinationals with

manufacturing activities abroad, but are higher than those of exporters; innovation

does not differently characterize the internationalisation modes.

Grandinetti and Mason (2012) investigate the relationships between export, FDI,

international alliances and international outsourcing by assuming that the last three

internationalisation modes mentioned can be considered as a determining factor for

export performance. They find that, besides strategic and organizational covariates,

also FDI, alliances and outsourcing have a significant and positive effect on export

intensity (measured by the export sales ratio).

In the study of the variety of modes whereby firms can serve a foreign market, the

relationship of substitution versus complementarity between the various forms may

be addressed. Following the proximity-concentration trade-off paradigm (Brainard

1997) a firm tends to invest abroad when transport costs are high and economies of

scale are small. Helpman et al. (2004) develop a model where firms choose between

export and FDI, concluding that firms enter the international market with ‘‘light’’

and indirect forms of internationalisation, denoted by low sunk costs and by a low

international commitment. When firms are able to assume higher risks associated

with international activities, they abandon these indirect forms by substituting them

for forms requiring higher experience, investments and commitment. Summarizing,

the more productive firms substitute their export through FDI. The alternative

hypothesis of a complementary internationalisation process suggests that firms

gradually accumulate different and more demanding forms to enlarge their

international involvement. Another line of thought in the literature states that, in

a single-product setting, exports and FDI are substituted, whereas complementarity

refers to multi-product firms, and exports and FDI become positively correlated if

there are horizontal and vertical complementarities across product lines (Head and

Ries 2004; Helpman 2006). The hypothesis of substitutive versus complementary/

cumulative internationalisation processes has been explicitly addressed by Basile

et al. (2003) in an empirical framework. This study, to the best of our knowledge, is

the only one that, besides export and FDI, also considers penetration operations, as a

form of internationalisation midway between the polar cases. The result obtained

acts in support of a cumulative process.

In Oberhofer and Pfaffermayr (2012) the substitution/complementarity assump-

tion is evaluated by considering that the optimal model for a firm serving the foreign

market can differ between host countries. Distant markets, requiring higher

transportation costs, may be served through FDI, whereas small markets nearby tend

to be served through export. As generally happens in firm level data sets, they have

not information on which country ‘‘hosts’’ export so the empirical analysis evaluates

the influence of firm characteristics on the internationalisation strategy. The results

obtained show that the majority of firms tend to simultaneously adopt different

strategies. Nevertheless, they observe that an increase in productivity determines an

increase (decrease) in the probability of only investing abroad (exporting), and this

supports the substitution relationship.

668 P. Calia, M. R. Ferrante

123

3 A statistical model for internationalisation choices

To model the whole set of internationalisation forms we adopt a MVP, where a

binary choice (yes/no) corresponds to each internationalisation category depending

on a function of covariates specified through different equations and allowing the

simultaneity of internationalisation choices. MVP dates back to Ashford and

Sowden (1970) and it finds applications in the context of limited dependent variable

models and simultaneous equation models (Maddala 1983). Because a firm could

simultaneously pursue more than one mode of internationalisation, the main

advantage of this model is that we do not need to select a priori the

internationalisation patterns to be modelled. No restrictions on the structure of

relationships among alternatives (i.e. on correlations between disturbances) are

required in the MVP, whereas this kind of restriction is imposed in multiple-choice

models. Relationships among forms of internationalisation are modelled through

correlation parameters that have to be estimated. These correlations tell us if there

are unobserved factors, besides those explicitly considered, that simultaneously

affect different choices around foreign expansion. Further, the MVP model allows

the use of a different set of covariates for each alternative, whereas, in the ordered

probit model the covariate set is the same for each alternative.

Formally, considering M internationalisation categories for each observation,

there are M equations each describing a latent dependent variable which

corresponds to the observed binary outcome (the observation subscript has been

suppressed for notational convenience):

y�m ¼ b0mxm þ em m ¼ 1; . . .;M

ym ¼ 1 if y�m [ 0 and 0 otherwiseð1Þ

where xm is a vector of p covariates for the m-th equation (m = 1, …, M), b0m is the

corresponding vector of parameters, and e ¼ ½em�m¼1;...;M is the error term vector

distributed as multivariate normal, with a zero mean and variance–covariance

matrix V. The leading diagonal elements of V are normalised to one and the off-

diagonal elements are the correlations qmj ¼ qjm for m, j = 1,…, M and m = j. If

we assume that em are distributed independently and identically with a univariate

normal distribution, Eq. (1) defines M univariate probit models (UVP). The

assumption of the independence of the error terms means that information about the

firm’s choice of the mode of internationalisation does not affect the prediction of the

probability of choosing another mode of internationalisation for the same firm. If the

unobserved correlations among outcomes are ignored, each of the M equations in

(1) could be estimated separately by a UVP. However, neglecting correlations leads

to inefficient estimated coefficients and could produce biased results in significance

tests. In principle, a MVP is an extension of the standard bivariate probit to more

than two outcome variables. The practical obstacle to this extension is the evalu-

ation of higher-order multivariate normal integrals, an M-dimensional integral

without a closed analytical form (Greene 2003).

The probability of the observed outcomes for any observation is the joint

cumulative distribution UMðl ; XÞ; where UMð�Þ is the M-variate standard normal

A multivariate probit approach 669

123

cumulative distribution function with arguments l and X that vary with

observations; for each observation, l ¼ ðj1b01x1; j2b

02x2; . . .; jMb0mxMÞ are

upper integration points, jM are sign variables defined as jm ¼ 2ym � 1; being

equal to 1 or -1 depending on whether the observed binary outcomes equal 1 or 0,

and m = 1, …, M. Matrix X has constituent elements Xmj; where Xmm ¼ 1 and

Xmj ¼ Xjm ¼ jjjmqjm:

Recently, methods of producing quite accurate estimates of multivariate normal

integrals based on simulation have been proposed.3 The estimates of the equation

parameters and correlation terms are obtained through the simulated maximum

likelihood (SML) estimator which results by maximising the simulated log-

likelihood function (Hajivassiliou and Ruud 1994; Cappellari and Jenkins 2003,

2006):

~‘ ¼Xn

i¼1

log ~UMðli; XiÞ ð2Þ

where each individual term ~UMðli; XiÞ is a simulation of a multivariate normal

probability calculated using the Geweke–Hajivassiliou–Keane (GHK) simulator

(Borsch-Supan and Hajivassiliou 1993; Keane 1994) at each iteration of the max-

imisation process for a given value of the parameters.

One important hypothesis to test is that all cross-equation correlation coefficients

are simultaneously equal to zero. If this is the case, we could equivalently fit

M independent univariate probits for each form of internationalisation. On the

contrary, if the null hypothesis is rejected, fitting M independent probits leads to

unbiased but not efficient estimates. A correlation coefficient between a pair of

choices different from zero, after controlling for firm characteristics, indicates that

there are unobserved factors affecting both choices.

4 The data

The data come from the 9th wave (covering the years 2001–2003) of the ‘‘Survey on

manufacturing firms’’ conducted every 3 years by the Capitalia Observatory.4 The

survey has a long history dating back to 1968.

The target population consists of Italian manufacturing firms with more than ten

employees; firms with more than 500 employees are sampled in entirety whereas

firms with less than 500 employees are selected on the basis of a sample. In order to

guarantee representativeness the sample is stratified by five classes of size (based on

the number of employees), four classes of activity sector (defined by the Pavitt

classification), and two classes of geographical location (North, Centre-South). The

size and the composition of the sample for firms with less than 500 employees are

obtained by the Neyman allocation using as auxiliary variable the mean value added

in the stratum in the year 2001. Capitalia ensures the accuracy of survey data in

3 See Greene (2003) for a brief textbook exposition.4 ‘‘Survey on Italian Enterprises. Report on the productive system and industrial policy’’, Observatory on

Small and Medium Enterprises, Capitalia, IX Report, 2005 (in Italian).

670 P. Calia, M. R. Ferrante

123

several ways: pilot surveys are realized in order to verify the accuracy of the

planned survey methods, a sub-sample of firms is re-interviewed with the aim of

checking the reliability of collected data, checks of logical and internal coherence of

data are performed, correction for missing data arising from total and partial non-

responses is adopted. Detailed information on the survey and on the sample design

are presented on a report published by Capitalia. The sample consists of 4,289 firms.

The survey data are linked to firm’s balance sheet data for each year of the period

2001–2003 covered by the survey, available for 3,450 firms.

The survey collects detailed quantitative and qualitative information on

ownership and businesses relationships, labour force, investments, innovation and

R&D, internationalisation, markets, and finance. Several studies with application in

different fields use data provided by the Capitalia survey.5 Moreover, since a wide

and detailed section of the questionnaire is devoted to internationalisation choices, a

number of paper focusing on different aspects of internationalisation of Italian firms

are based on this data set (among others, Antonietti and Cainelli 2008; Basile et al.

2003; Benfratello and Razzolini 2009; Sterlacchini 2001).

In order to identify the different modes that firms operate in the international

markets we follow the review of the empirical literature on firms’ foreign activities

presented by Crino (2009):

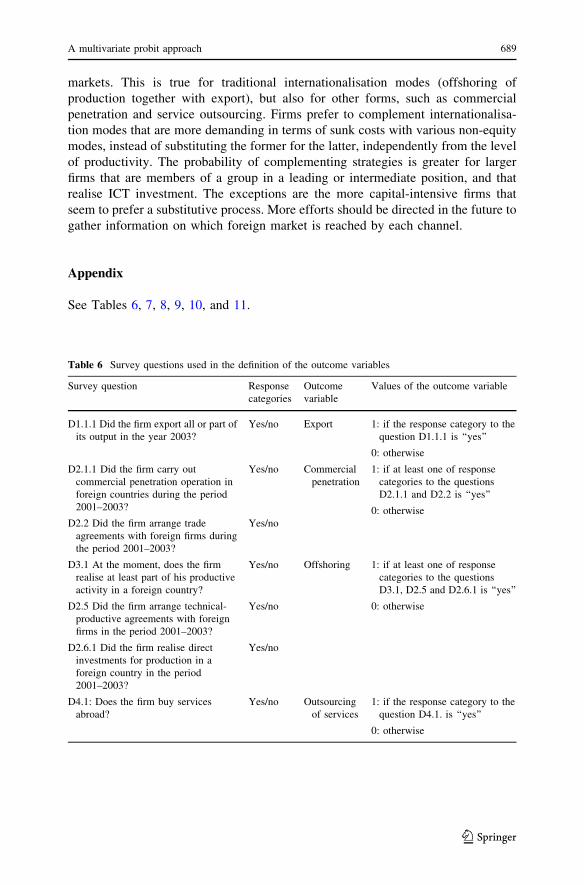

(a) export, EXP (y1);

(b) commercial penetration operations and agreements, COMM (y2), concerning

the set up of sales outlets abroad directly in charge of the firm, sales outlets in

charge of foreign local traders, sales outlets handled by foreign firms

belonging to the group, other promotional initiatives, and trade arrangements

with foreign firms;

(c) offshoring of production (or material offshoring), which relates to foreign

relocation of purely productive stages of intermediate or final goods, that can

take place through FDI or through arm’s length contracts with foreign

unaffiliated parties (as subcontracting, manufacturing contracts, licensing of

activities, etc.), OFFPROD (y3); data do not provide enough information to

distinguish between offshoring via FDI or through arm’s length contracts with

foreign unaffiliated parties (referred to in the literature as international

outsourcing).

(d) outsourcing of services abroad, which pertains to the acquisition of business

services, like transportation, insurance, communications, financial services,

computer-related services, R&D services, and engineering and design from

abroad, SERVOUT (y4).

In Table 6 of the ‘‘Appendix’’ we report the survey questions used to gather

information for the definition of the dependent variables.

Each variable, considered as binary choice (yes/no), is the dependent variables of

one out of four equations defining the MVP model. All the variables are measured

5 See Benfratello et al. (2008); Bianco and Nicodano (2006); Filatotchev et al. (2003); Hall et al. (2009);

Minetti and Zhu (2011); Parisi et al. (2006).

A multivariate probit approach 671

123

with reference to the time span 2001–2003, except for export which is measured at

2003.

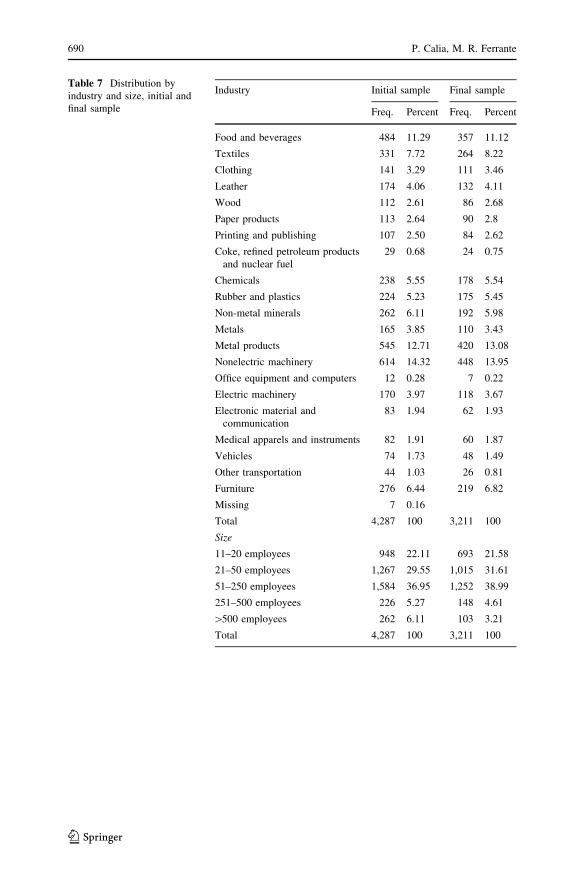

The original sample size of 4,289 is reduced due to two reasons. Since we use a

measure of total factor productivity (TFP) as a covariate this imply conditioning

only on observations with accounting data (3,450 out of 4,289). Besides, because of

missing data on outcome variables and covariates, the final sample has 3,211 firms.

To evaluate the representativeness of the final sample, we compare the distributions

of the initial and the final sample by industry and size. Results (Table 7 in the

‘‘Appendix’’) show that distributions are sufficiently similar.

The estimated percentages of firms taking on each form of internationalisation

show that the majority of the firms export (69 %) and about the 31 % of them conduct

commercial penetration operations and agreements. The percentage of firms that take

on production offshoring is quite small, representing the 7 % of the total, the least-

chosen mode, whereas a larger portion of firms (12 %) outsources services abroad.

In order to verify the representativeness of the sample in terms of the percentage

of exporting firms, we also calculate the percentage of exporting manufacturing

firms with more than ten employees in the population combining information on

exporting firm’s population provided by the Italian Institute for Foreign Trade and

information in the Archive of Active Enterprises provided by the Italian Statistical

Institute (ISTAT 2004). We find a percentage of exporting firms equal to 65 %, a

value close to our estimate. These figures are consistent with those in Minetti and

Zhu (2011) who report a percentage of exporting firms for Italian manufacturing

firms with more than ten employees which ranges between 63 and 70 % for each

year between 1998 and 2005.

Summarizing, we conclude that the Capitalia survey can be considered

adequately representative of the population of firms with more than ten employees.

This does not mean that the sample is representative of the whole population of

Italian manufacturing firms since micro firms (with less than 10 employees) are

excluded from the target population. Consequently the results we present in this

paper cannot be generalised to the whole population of Italian manufacturing firms,

also considering that the number of micro firms is large in the Italian case.

The sampling distribution of the more frequently chosen patterns of internation-

alisation is reported in Table 1.

The first nine combinations (ordered by frequency) account for 98 % of all the firms.

Of these firms, 22 % do not engage in any form of internationalisation while 32 % are

only exporters. Firms exporting and conducting commercial penetration constitute

21 % of the firms and another 8 % have also outsourced services abroad. Other

combinations of modes of internationalisation are less frequent, but the majority of

them involve exporting. Under the category ‘‘Others’’ are combinations with a

frequency smaller than 1 % that, as a whole, accounts for about the 2.2 % of the firms.

5 The model specification

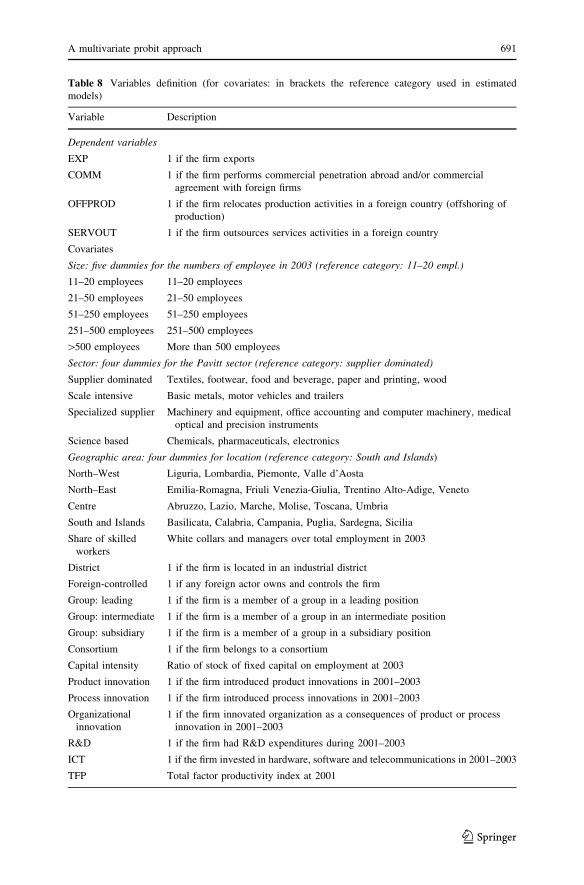

In this section we briefly discuss the choice of the covariates. Detailed definition of

outcome variables and covariates are reported in Tables 6 and 8 of the ‘‘Appendix’’.

672 P. Calia, M. R. Ferrante

123

Basic structural characteristics are size, economic activity, and geographical

location.6 Although it is believed that a firm should be large to compete in the global

market and the empirical evidence generally confirms this expectation, still some

results are no so clear cut. For example, limiting ourselves to the Italian case,

Sterlacchini (2001) finds a positive relation between export and size extending only

until an upper limit above which the size of a firm does not increase its export

propensity, while Basile et al. (2003) find that the effect of size is very small for

firms engaging in export, commercial penetration, and FDI and even negative for

firms engaging only in export. To account for different effects of the size level, we

use a five-class specification for the numbers of employees in the year 2003; the

same that is used for stratification in the sample design (classes are defined in

Table 7 of the ‘‘Appendix’’). In this way we control also for the different sampling

rates in the strata. The Pavitt classification,7 rather than the NACE-based industry

classification, is used in order to control for the sample design. However, the Pavitt

classification is meaningful itself because it identifies sectoral patterns of

technological change that are strongly industry-specific (Sterlacchini 2001). Four

dummies are used to indicate activity in the sectors Supplier dominated, Scale

intensive, Specialized suppliers, and Science based. We use four classes of

geographical location (North-West, North-East, Centre, South and Islands) and a

dummy for location in industrial districts. Evidence of a positive effect of the firm’s

location in an industrial district on export performance has been found in Becchetti

Table 1 Distribution of

pattern of internationalisation

y1 = EXP, y2 = COMM,

y3 = OFFPROD,

y4 = SERVOUT

y1, y2, y3, y4 Number Freq. Cum. percent

1 0 0 0 1,029 32.05 32.05

0 0 0 0 701 21.83 53.88

1 1 0 0 662 20.62 74.5

1 1 0 1 269 8.38 82.88

1 0 0 1 169 5.26 88.14

1 1 1 0 105 3.27 91.41

1 1 1 1 82 2.55 93.96

1 0 1 0 81 2.52 96.48

0 1 0 0 42 1.31 97.79

Others 71 2.21 100.00

Tot 3,211 100.00

6 Some authors (see, e.g. Aw and Lee 2008; Oberhofer and Pfaffermayr 2012) find that firm age have a

crucial role in explaining the firms decision to serve foreign markets. We also include, in a first exercise,

the age of the firm in the regressions together with the other covariates but its coefficient was never

significant. For this reason and because of the presence of missing data in this variable that should lead to

lost observations from our sample, we decide to not include it in our final model. As for other results in

our analysis (see next in the paper), the lack of any effect of firm age on the decision to serve foreign

market could have one possible explanation in the absence of micro-firms in our sample, which usually

are younger than larger firms.7 The Pavitt taxonomy is a classification of economic sectors based on technological opportunities,

innovations, R&D intensity, and knowledge. For details on categories, see Table 8 of the ‘‘Appendix’’.

A multivariate probit approach 673

123

et al. (2007). All structural variables are measured with reference to the end of year

2003.

Internationalisation is expected to be positively associated with an higher

proportion of skilled workers because it usually requires more white collar activities

or because of skill upgrading due to the offshoring of low-skill production activities

(Lipsey 2002). However, a negative sign may arise when the choice of offshoring or

outsourcing originates from the lack of in-house specialised skills or equipment

(Abraham and Taylor 1996). This variable is measured by the share of white collars

to total employment at 2003. We also consider an indicator of capital intensity (the

ratio of fixed assets to employment measured at 2003). As far as offshoring and

outsourcing are concerned, a negative association with capital intensity implies that

firms are more willing to outsource labour-intensive activities (Antonietti and

Cainelli 2008).

Foreign-owned firms are likely to be part of international networks and linked to

other affiliates overseas; this may facilitate the commercial penetration of

international markets as well as the outsourcing of services or production activities

(Girma et al. 2004, Cusmano et al. 2010). Foreign ownership is introduced as a

dummy variable which indicates whether one or more foreign subjects control the

company and own any share of its equity. Group membership might provide firms

with the necessary marketing and financial resources to internationalise (Sterlac-

chini 2001, Benfratello and Razzolini 2009). We define three dummies which

identify the membership to a business group depending on the firm’s position within

the group (leading, intermediate, subsidiary). By joining a consortium, partners are

able to exploit economies of scale and scope that cannot be pursued by individual

firms (Basile et al. 2003). A dummy is used to indicate whether a firm joins a

consortium.

The relationship with productivity has been already discussed in Sect. 2.

Different measures of the TFP have been used in literature depending on the amount

of available information. We adopt the approach proposed by Levinsohn and Petrin

(2003). The TFP is measured at the firm level by estimating a two factor Cobb–

Douglas production function separately for groups of industries defined by the

NACE (rev. 1) classification at two-digit level, with value added as output, total

costs of labour as labour input and the book value of fixed and intangible assets as

capital input. All variables are provided by balance sheets for years 2001, 2002 and

2003, and deflated by proper index numbers. Estimated firm-specific TFP is scaled

with respect to industry mean so that it provides a relative measure of how specific

firm TFP diverges from the average. We use TFP estimates at 2001 in order to

circumvent endogeneity problems in the model.

The literature has recently revealed the role of technological innovation in

improving exports and FDI (Castellani and Zanfei 2007). Basile et al. (2003) find

that innovative activities have positive effects on other forms of internationalisation

as well (commercial penetration and trade and technical agreement). We measure

innovative activity with different variables: a dummy for formal R&D expenditures

in the period 2001–2003, two dummies for innovation in products or processes

introduced during 2001–2003, a dummy for organisational innovation due to

product or process innovation introduced in the same time span, a dummy for

674 P. Calia, M. R. Ferrante

123

investment in information and communication technologies (ICT) during

2001–2003.8

Sample averages and standard deviations of covariates are reported in Table 9 of

the ‘‘Appendix’’ for each group of firms which engage in different forms of

internationalisation and for the group of domestic firms. For each group the sample

consists mainly of firms with less than 250 employees (the 80 % or more), located

in the North (the 57 % or more) and which operate in the supplier-dominated

(traditional) sectors (the 47 % or more). However we can point out some differences

between groups. In general, as expected, firms which operate in international

markets are larger, and more frequently than domestic firms invest in R&D (54 % or

more), ICT (72 % or more), innovate products (48 % or more) and process (46 % or

more). The percentages are smaller for exporter than for other forms of

internationalisation but still higher than for domestic firms. Moreover, foreign-

owned firms and members of business group are more frequent among offshoring

and outsourcing firms: even 13 % of foreign-owned firms for outsourcing and

47–48 % of members of business group for offshoring and service outsourcing.

Offshoring firms, as expected, have smaller capital intensity than domestic firms and

also compared to others forms of internationalisation. It is worthy to note that

among domestic firms we observe a greater frequency of firms operating in scale-

intensive sectors and a lower frequency of firms operating in specialized-supplier

sectors than among internationalised firms. Moreover, domestic firms have a higher

frequency of firms located in South. As far as TFP is concerned, average TFPs of

internationalised firms are greater compared to the average TFP of domestic ones.

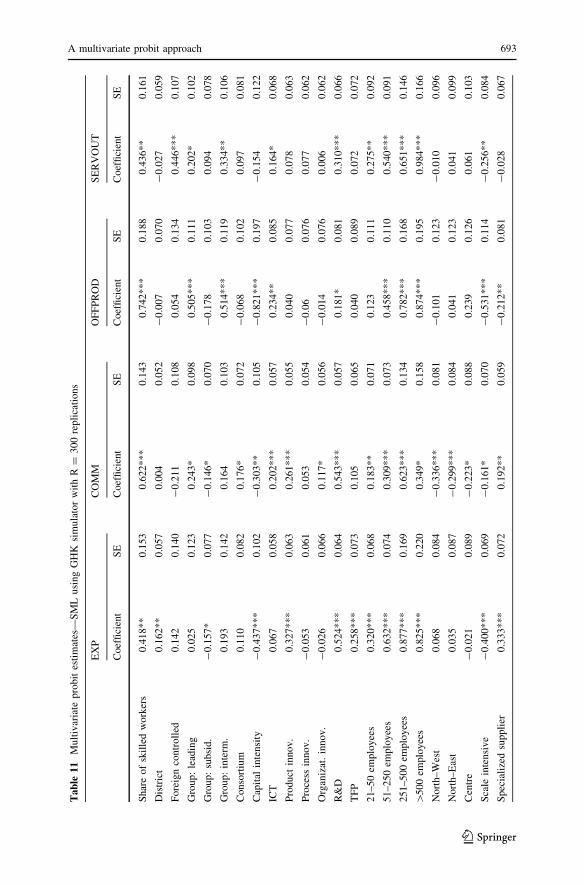

6 Model estimates and results

6.1 Marginal probabilities

Correlation coefficient estimates (Table 10 in the ‘‘Appendix’’) are all positive and

significant and the hypothesis that all correlation coefficients are jointly equal to

zero is rejected.9 This confirms that the MVP model is a better specification than the

four distinct UVP for the observed data. A correlation coefficient different from

zero between a pair of choices means that there are unobservable factors affecting

both choices and reveals an association after controlling for firm characteristics.

After accounting for observable firm heterogeneity, a relevant positive correlation

between some pairs of choices still remains.

Results on estimated MVP coefficients are reported in Table 11 of the

‘‘Appendix’’. Distinct Wald tests for the hypothesis that all the coefficients in each

equation are jointly equal to zero reject the null hypothesis as well as the hypothesis

that the vectors of coefficients are equal across the four equations.

8 The survey collects data on the amount of R&D expenditures and investment in ICT, but we did not use

them due to the large amount of missing data.9 The model has been estimated using STATA (version 9) ml command, with a self-supplied code for the

log-likelihood calculation, and the modules mdraws and mvnp developed by Cappellari and Jenkins

(2006).

A multivariate probit approach 675

123

We summarise the results by focusing on the marginal effects (MEs) on marginal

probabilities for each dependent variable (Table 2). In other words, we consider the

probability of choosing each internationalisation mode, irrespective of the choice of

the remaining modes. Each ME represents the change in probability of success

given a one-unit change in the associated regressor (a change from zero to one for

binary variables). For the m-th equation and the k-th continuous covariate, the

marginal effect is calculated using oEðymjxmkÞ=oxmk ¼/ b0mxm

� �bmk at mean values

for the covariates (Greene 2003). For the k-th binary variable, the difference Pðym ¼1jxmk ¼ 1Þ � Pðym ¼ 1jxmk ¼ 0Þ is calculated holding all other covariates constant

at mean values.10 Here, bmk is the coefficient estimate of the covariate xmk from the

mode-type m equation, and /ð�Þ is the probability density function of a standard

normal distribution with zero mean and unit variance. In the following we refer to

marginal effects as marginal effects at the mean (MEM).

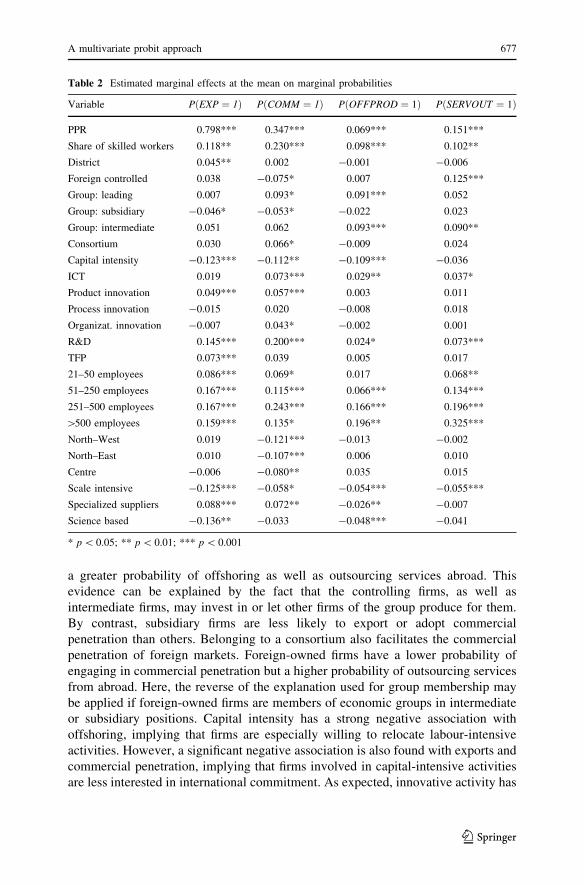

The first row of Table 2 reports the estimated predicted probability (henceforth

PPR) at mean values of the covariates. The probability for each internationalisation

mode generally increases with size.11 The Pavitt sector has significant associations

with export, commercial penetration, and the offshoring of production. Specialised

suppliers are those that mostly export and carry out commercial penetration, while

firms in the supplier-dominated sector (which comprises ‘‘traditional’’ industries)

choose offshore production more frequently than others. It may be argued that firms

in the traditional sectors resort to offshoring in their attempts to reduce production

costs. Scale-intensive firms are less likely to engage in any form of internation-

alisation. There are not significant differences across geographical areas in the

probability of participation in international markets except for commercial

penetration operation and firms located in the South of Italy, more than others,

venture commercial penetration abroad. However, it may happen that the variable

defining the location in an industrial district captures some of the geographical

variability, because most of the districts are located in the North.12 The share of

skilled workers is significantly and positively associated with all internationalisation

modes. Results confirm previous findings that firms located in industrial districts

export more than others, but we do not find significant associations with other

internationalisation modes. Group membership is associated with the internation-

alisation process, but this relationship depends on the firm’s position in the group.

Leading firms in a group have a greater probability of performing commercial

penetration and engaging in offshoring. Firms in the intermediate position also have

10 Because marginal effects are a non-linear combination of model parameters, standard errors (not

reported) were estimated by the Delta method and significance was tested by a Wald test. Detailed results

are available from the authors upon request.11 To check the robustness of estimates to the specification of the size variable, we also estimate the

model using the number of employees instead of the four dummies for the size. The marginal effect (at

mean) of the size is positive and significant on each internationalization choice and increasing at different

level of size, as in the presented results. The sign of the other coefficients and MEMs are all confirmed.12 In a previous estimation exercise not reported here, with no industrial district indicator and a dummy

for investments in fixed capital instead of capital intensity, we found a strong positive association between

locations in the North of Italy and exports.

676 P. Calia, M. R. Ferrante

123

a greater probability of offshoring as well as outsourcing services abroad. This

evidence can be explained by the fact that the controlling firms, as well as

intermediate firms, may invest in or let other firms of the group produce for them.

By contrast, subsidiary firms are less likely to export or adopt commercial

penetration than others. Belonging to a consortium also facilitates the commercial

penetration of foreign markets. Foreign-owned firms have a lower probability of

engaging in commercial penetration but a higher probability of outsourcing services

from abroad. Here, the reverse of the explanation used for group membership may

be applied if foreign-owned firms are members of economic groups in intermediate

or subsidiary positions. Capital intensity has a strong negative association with

offshoring, implying that firms are especially willing to relocate labour-intensive

activities. However, a significant negative association is also found with exports and

commercial penetration, implying that firms involved in capital-intensive activities

are less interested in international commitment. As expected, innovative activity has

Table 2 Estimated marginal effects at the mean on marginal probabilities

Variable P EXP ¼ 1ð Þ P COMM ¼ 1ð Þ P OFFPROD ¼ 1ð Þ P SERVOUT ¼ 1ð Þ

PPR 0.798*** 0.347*** 0.069*** 0.151***

Share of skilled workers 0.118** 0.230*** 0.098*** 0.102**

District 0.045** 0.002 -0.001 -0.006

Foreign controlled 0.038 -0.075* 0.007 0.125***

Group: leading 0.007 0.093* 0.091*** 0.052

Group: subsidiary -0.046* -0.053* -0.022 0.023

Group: intermediate 0.051 0.062 0.093*** 0.090**

Consortium 0.030 0.066* -0.009 0.024

Capital intensity -0.123*** -0.112** -0.109*** -0.036

ICT 0.019 0.073*** 0.029** 0.037*

Product innovation 0.049*** 0.057*** 0.003 0.011

Process innovation -0.015 0.020 -0.008 0.018

Organizat. innovation -0.007 0.043* -0.002 0.001

R&D 0.145*** 0.200*** 0.024* 0.073***

TFP 0.073*** 0.039 0.005 0.017

21–50 employees 0.086*** 0.069* 0.017 0.068**

51–250 employees 0.167*** 0.115*** 0.066*** 0.134***

251–500 employees 0.167*** 0.243*** 0.166*** 0.196***

[500 employees 0.159*** 0.135* 0.196** 0.325***

North–West 0.019 -0.121*** -0.013 -0.002

North–East 0.010 -0.107*** 0.006 0.010

Centre -0.006 -0.080** 0.035 0.015

Scale intensive -0.125*** -0.058* -0.054*** -0.055***

Specialized suppliers 0.088*** 0.072** -0.026** -0.007

Science based -0.136** -0.033 -0.048*** -0.041

* p \ 0.05; ** p \ 0.01; *** p \ 0.001

A multivariate probit approach 677

123

a strong and positive association with internationalisation. The probability of

exporting is greater for firms investing in research and development and producing

innovative products. Effects on the probability of engaging in commercial

penetration are even higher: plus 20 % points for firms investing in R&D, plus

about 5 % points for firms producing innovative products and introducing

innovations in organisation, plus 7 % points for firms investing in ICT. Firms

investing in R&D and ICT also have a greater probability of offshoring and

outsourcing services. This may suggest that offshoring is also carried out by firms

whose core activity is not producing innovative products, but who wish to improve

their competitiveness by reducing production costs in low-wage countries. TFP is

found to be significantly and positively associated only with export.13 This last

result seems surprising in view of the recent empirical evidence of significant

productivity differentials between domestic firms, exporters and multinational firms,

so we expect that the higher the productivity, the greater the commitment to

international activity. We have to stress, however, that each marginal probability

evaluates the choice of participating versus not participating in international

markets by means of a specific form. Because productivity does not significantly

affect the chance of offshoring (neither of outsourcing or commercial penetration)

this means that, for example, offshoring firms are not more productive than non-

offshoring firms, but it may be the case that firms not offshoring are still

internationally involved in some way. On the other hand, exporting firms are more

productive than non-exporting firms, but the latter may be not involved at all in

international markets. We will come back to this point in the next section.

Nevertheless, the weak impact of the TFP could also be explained by missing of

micro-firms in the sample, expected to be less productive and more likely to serve

the domestic market only. Furthermore, less productive firms are more likely to exit

the market but we can not control for market exit due to the lack of this information

in our data.

6.2 Comparing marginal and joint probabilities: the ‘‘added value’’ of the MVP

The advantage of the MVP model over the UVP is that it allows us to better evaluate

the relationships between internationalisation forms, taking into account the

correlations between participation decisions via unobservable factors. To give a

reasonable base for comparing the estimated relationships using the MVP model

relative to the UVP approach, we estimate a UVP model for each of the four

international participation modes.

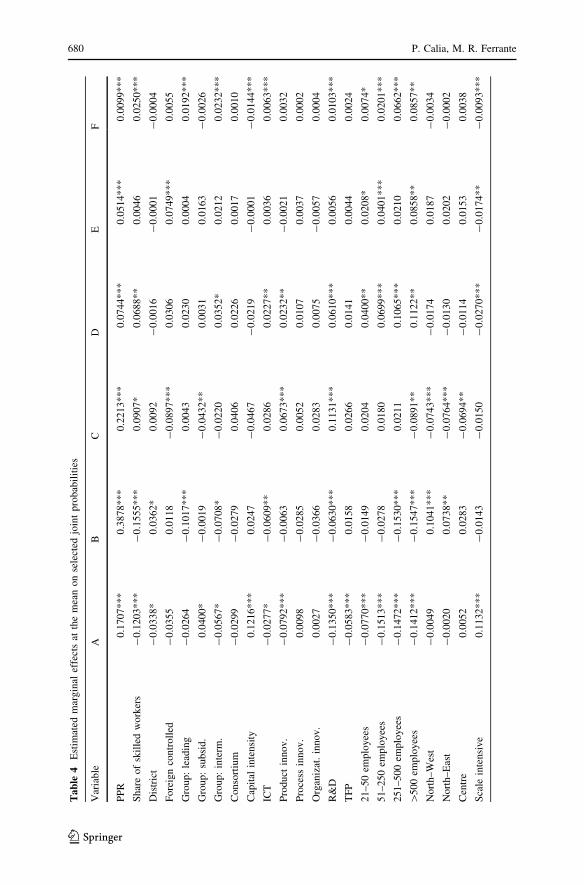

In Table 3 we compare marginal and some joint probabilities predicted by the

MVP and UVP models. The joint probabilities for the latter are obtained as the

product of the estimated marginal probabilities. While we obtain similar predictions

for marginal probabilities from MVP and UVP, we observe different predictions for

most of the joint probabilities. For instance, the predicted probability for not

13 In order to check the robustness of this result for TFP, we use a Tornquist-type index number to

measure the firm’s TFP (Caves et al. 1982) an approach already used in the context of analysis of firms’

internationalization (Delgado et al. 2002; Girma et al. 2005). We re-estimate the model by using this TFP

measure: coefficient does not change sensibly and its significance does not change at all.

678 P. Calia, M. R. Ferrante

123

participating in international markets is 17 % using MVP, as against 10 % by the

UVP model. Furthermore, predicted joint probabilities using MVP are closer to the

observed probabilities reported in Table 1 than those predicted using the UVP

model.

To further highlight the extra insight provided by the MVP model and the

relevance of simultaneously considering the whole set of choices faced by firms, we

show that the MEMs of an explanatory factor can also be very different for marginal

and joint probabilities.

We discuss this point comparing the marginal probability of exporting,14 reported

in Table 2, with the probability of exporting considered jointly with other

internationalisation channels (see Table 4 and description in Sect. 6.3).

As can be seen, the estimated MEMs are quite different. Comparing the marginal

probability of exporting in Table 2 with columns B–F in Table 4, representing

probabilities of exporting considered jointly with different sets of alternatives, we

see that the MEM of many covariates change significance and even sign. The

proportion of skilled workers, product innovation, investment in R&D, size, and

even productivity have a significant positive association with the marginal

probability of exporting, but their effect is very different depending on whether

the firms’ participation in international markets through other channels is considered

or not. While exporting firms as a whole are larger, have more skilled workers, and

Table 3 Predicted marginal and joint probabilities by UVP and MVP model

UVP MVP

Coefficient SE Coefficient SE

P(EXP = 1) 0.7978*** 0.0081 0.7975*** 0.0081

P(COMM = 1) 0.3471*** 0.0090 0.3474*** 0.0089

P(OFFPROD = 1) 0.0682*** 0.0051 0.0687*** 0.0051

P(SERVOUT = 1) 0.1514*** 0.0069 0.1509*** 0.0068

A: P(0000) 0.1044*** 0.0050 0.1707*** 0.0073

B: P(1000) 0.4119*** 0.0077 0.3878*** 0.0098

C: P(1100) 0.2189*** 0.0065 0.2213*** 0.0769

D: P(1101) 0.0391*** 0.0023 0.0744*** 0.0050

E: P(1001) 0.0735*** 0.0034 0.0514*** 0.0040

F: P(1111) 0.0029*** 0.0003 0.0099*** 0.0015

A : PðEXP ¼ 0; COMM ¼ 0; OFFPROD ¼ 0; SERVOUT ¼ 0ÞB : PðEXP ¼ 1; COMM ¼ 0; OFFPROD ¼ 0; SERVOUT ¼ 0ÞC : PðEXP ¼ 1; COMM ¼ 1; OFFPROD ¼ 0; SERVOUT ¼ 0ÞD : PðEXP ¼ 1; COMM ¼ 1; OFFPROD ¼ 0; SERVOUT ¼ 1ÞE : PðEXP ¼ 1; COMM ¼ 0; OFFPROD ¼ 0; SERVOUT ¼ 1ÞF : PðEXP ¼ 1; COMM ¼ 1; OFFPROD ¼ 1; SERVOUT ¼ 1Þ* p \ 0.05; ** p \ 0.01; *** p \ 0.001

14 The estimates of MEMs referred to the remaining probabilities are available from the author upon

request.

A multivariate probit approach 679

123

Ta

ble

4E

stim

ated

mar

gin

alef

fect

sat

the

mea

non

sele

cted

join

tpro

bab

ilit

ies

Var

iab

leA

BC

DE

F

PP

R0

.170

7*

**

0.3

87

8*

**

0.2

21

3*

**

0.0

74

4*

**

0.0

51

4*

**

0.0

09

9*

**

Sh

are

of

skil

led

wo

rker

s-

0.1

20

3*

**

-0

.15

55

***

0.0

90

7*

0.0

68

8*

*0

.004

60

.02

50

***

Dis

tric

t-

0.0

33

8*

0.0

36

2*

0.0

09

2-

0.0

01

6-

0.0

00

1-

0.0

00

4

Fo

reig

nco

ntr

oll

ed-

0.0

35

50

.01

18

-0

.089

7*

**

0.0

30

60

.074

9*

**

0.0

05

5

Gro

up

:le

adin

g-

0.0

26

4-

0.1

01

7*

**

0.0

04

30

.023

00

.000

40

.01

92

***

Gro

up

:su

bsi

d.

0.0

40

0*

-0

.00

19

-0

.043

2*

*0

.003

10

.016

3-

0.0

02

6

Gro

up

:in

term

.-

0.0

56

7*

-0

.07

08

*-

0.0

22

00

.035

2*

0.0

21

20

.02

32

***

Con

sort

ium

-0

.029

9-

0.0

27

90

.040

60

.022

60

.001

70

.00

10

Cap

ital

inte

nsi

ty0

.121

6*

**

0.0

24

7-

0.0

46

7-

0.0

21

9-

0.0

00

1-

0.0

14

4*

**

ICT

-0

.027

7*

-0

.06

09

**

0.0

28

60

.022

7*

*0

.003

60

.00

63

***

Pro

du

ctin

no

v.

-0

.079

2*

**

-0

.00

63

0.0

67

3*

**

0.0

23

2*

*-

0.0

02

10

.00

32

Pro

cess

inno

v.

0.0

09

8-

0.0

28

50

.005

20

.010

70

.003

70

.00

02

Org

aniz

at.

inno

v.

0.0

02

7-

0.0

36

60

.028

30

.007

5-

0.0

05

70

.00

04

R&

D-

0.1

35

0*

**

-0

.06

30

***

0.1

13

1*

**

0.0

61

0*

**

0.0

05

60

.01

03

***

TF

P-

0.0

58

3*

**

0.0

15

80

.026

60

.014

10

.004

40

.00

24

21

–50

emp

loyee

s-

0.0

77

0*

**

-0

.01

49

0.0

20

40

.040

0*

*0

.020

8*

0.0

07

4*

51

–25

0em

plo

yee

s-

0.1

51

3*

**

-0

.02

78

0.0

18

00

.069

9*

**

0.0

40

1*

**

0.0

20

1*

**

25

1–5

00

emp

loyee

s-

0.1

47

2*

**

-0

.15

30

***

0.0

21

10

.106

5*

**

0.0

21

00

.06

62

***

[5

00

emp

loyee

s-

0.1

41

2*

**

-0

.15

47

***

-0

.089

1*

*0

.112

2*

*0

.085

8*

*0

.08

57

**

No

rth

–W

est

-0

.004

90

.10

41

***

-0

.074

3*

**

-0

.017

40

.018

7-

0.0

03

4

No

rth

–E

ast

-0

.002

00

.07

38

**

-0

.076

4*

**

-0

.013

00

.020

2-

0.0

00

2

Cen

tre

0.0

05

20

.02

83

-0

.069

4*

*-

0.0

11

40

.015

30

.00

38

Sca

lein

ten

siv

e0

.113

2*

**

-0

.01

43

-0

.015

0-

0.0

27

0*

**

-0

.017

4*

*-

0.0

09

3*

**

680 P. Calia, M. R. Ferrante

123

Ta

ble

4co

nti

nu

ed

Var

iab

leA

BC

DE

F

Sp

ecia

lize

dsu

ppli

er-

0.0

69

8*

**

0.0

28

30

.073

2*

**

0.0

12

0-

0.0

07

0-

0.0

02

7

Sci

ence

bas

ed0

.114

1*

*-

0.0

48

7-

0.0

09

2-

0.0

17

9-

0.0

14

9-

0.0

07

4*

**

A:

PðE

XP¼

0;

CO

MM¼

0;

OF

FP

RO

D¼

0;

SE

RV

OU

T¼

0Þ

B:

PðE

XP¼

1;

CO

MM¼

0;

OF

FP

RO

D¼

0;

SE

RV

OU

T¼

0Þ

C:

PðE

XP¼

1;

CO

MM¼

1;

OF

FP

RO

D¼

0;

SE

RV

OU

T¼

0Þ

D:

PðE

XP¼

1;

CO

MM¼

1;

OF

FP

RO

D¼

0;

SE

RV

OU

T¼

1Þ

E:

PðE

XP¼

1;

CO

MM¼

0;

OF

FP

RO

D¼

0;

SE

RV

OU

T¼

1Þ

F:

PðE

XP¼

1;

CO

MM¼

1;

OF

FP

RO

D¼

1;

SE

RV

OU

T¼

1Þ

*p\

0.0

5;

**

p\

0.0

1;

**

*p\

0.0

01

A multivariate probit approach 681

123

are more innovative and productive than firms not exporting (positive and

significant MEMs on marginal probability), the same is true only for exporting

firms which pursue other strategies (columns C–F), while firms that participate in

international markets only through export (column B) are smaller, have fewer

skilled workers, and do not innovate or invest in R&D. In particular, higher

productivity increases the (marginal) probability of exporting and decreases the

chance of not exporting, but does not affect either of the joint probabilities.

To summarise, these results show the advantages of adopting a multivariate

setting in analysing internationalisation strategies and that any conclusion

concerning patterns of internationalisation and their link with firm characteristics

depends on the set of internationalisation modes considered. Looking simulta-

neously at different forms of internationalisation allows us to understand the

relationships between the different modes of participation in international markets

and the influence of a firm’s characteristics on participation better than looking at

each internationalisation mode separately.

6.3 Firm heterogeneity and internationalisation strategies

Now, we turn to the multivariate part of the analysis. The estimate of a MVP

produces a very rich and informative output in terms of joint and conditional

probabilities and of the corresponding MEMs. In this section, we analyse the

selection of heterogeneous firms into different internationalisation patterns.

In Table 4 we report predicted joint probabilities (at mean values of covariates)

of the entire set of the internationalisation modes considered. We focus on the

patterns with the highest occurrence (sample frequency above 5 %). The last

column reports the probability of adopting the entire set of internationalisation

modes. We also present the corresponding MEMs.15

As expected, the PPRs are similar to the observed frequencies in the descriptive

analysis reported in Sect. 4. The estimated MEMs show that the covariates affect the

selection of firms into different internationalisation patterns. The probability of

being domestic (A) is greater for firms that have a smaller share of skilled workers,

are smaller in size, and do not belong to a district. Furthermore, innovating products

and investing in ICT and R&D reduce the probability of being domestic, whereas

this probability increases with capital intensity. Firms in scale-intensive and

science-based sectors are more likely to be domestic than specialised and traditional

firms. Subsidiary firms in a group have a higher probability to be domestic too.

Finally, as expected, less productive firms have a higher probability of being

domestic: this means that the most productive firms have a higher probability of

being internationally involved in some way.

15 Conditional and joint probabilities are highly nonlinear in both parameters and covariates, which

prevent a tractable analytical solution of MEMs and standard errors (SEs) that are then calculated using

simulation and numerical gradients. In particular, we simulate 500 sets of parameters from an asymptotic

multivariate normal distribution, each time calculating the predicted probability, and its numerical

derivatives with respect to the relevant covariates evaluated at the means of all covariates. We thereby

obtain 500 sets of PPR and MEMs, and sample SEs are calculated as estimates of the SEs for the PPR and

MEMs.

682 P. Calia, M. R. Ferrante

123

Only exporters (B) are similar to domestic firms in many respects: the MEMs of

the proportion of skilled workers, firm size, ICT and R&D show the same sign in A

and B. Yet, the chance of participating in international markets only through export

is higher for firms belonging to a district and located in the North, while it is lower

for leading firms in a group.

The probability of adopting both export and commercial penetration abroad

(C) is greater for firms with a higher proportion of skilled workers, which innovate

products and invest in R&D, for firms located in northern regions, and for foreign-

owned and subsidiary firms.

The probability of adopting export, commercial penetration, and the international

outsourcing of services (D) increases with size, proportion of skilled workers,

investment in ICT and R&D, and product innovation. Firms operating in scale-

intensive industries are less likely than other industries to adopt all three forms of

internationalisation.

The probability of both exporting and outsourcing services from abroad (E) is

higher for foreign-owned firms that are larger in size and located in the North, but it

is lower for firms operating in scale-intensive industries.

Finally, the probability of participating in international markets via all four

strategies (F) is greater for large firms with a larger proportion of skilled workers,

investing in ICT and R&D, and which are members of a group in a leading or

intermediate position. Firms with higher capital intensity and that belong to scale-

intensive or science-based industries are less likely to pursue all the internation-

alisation strategies than firms belonging to other sectors.

Summarizing, domestic and, to some extent, only exporting firms have, as

expected, a lower proportion of skilled workers and a smaller size. They do not

perform innovative activities, have higher capital intensity, and operate in the scale-

intensive and science-based sectors. Domestic firms are also less productive. Firms

engaging in export and commercial penetration differ from the groups described

above. They have a larger proportion of skilled workers, innovation and R&D

potential, and belong to a group in a leading or intermediate position. Firms

engaging in the outsourcing of services and export are most likely to be foreign-

owned, larger in size, and located in the northern region of the country. Finally,

firms with the most complex internationalisation patterns (which engage in export,

commercial penetration and outsourcing of services or in the whole set of choices

considered) are large firms that belong to a group in a leading or intermediate

position and operate in traditional or specialised-supplier sectors, investing in R&D

and in ICT, but with a lower capital intensity. Productivity lowers the probability of

being domestic but has no particular effects on the choice of any specific pattern of

internationalisation. It appears that productivity affects the choice between

remaining domestic or entering the international markets, but does not affect the

choice between the different internationalisation entry modes. This conclusion

agrees with the results in Sect. 6.2: non-exporting firms are generally domestic, i.e.

do not pursue any internationalisation strategy, whereas firms operating in

international markets are almost all exporting.

A multivariate probit approach 683

123

6.4 Complementarity/substitution of internationalisation modes

In this section we evaluate whether the relationship between internationalisation

strategies can be considered complementary or substitutive. As the available data

does not contain information about internationalisation modes for each foreign

outlet market, we cannot properly test the substitution/complementary assumption

in the sense highlighted by Oberhofer and Pfaffermayr (2012), illustrated in Sect. 2.

We focus on the probabilities of performing a given mode, conditional to whether

the firm performs one or more of the other modes, in a framework where the

differences between foreign markets is overcome.

We first compare the conditional probabilities of carrying out each internation-

alisation mode between exporters and non-exporters:

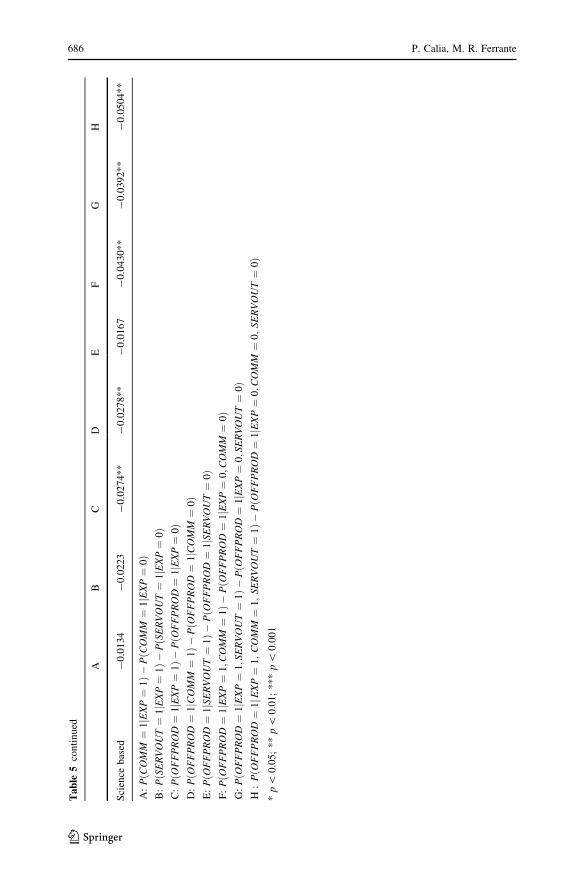

ðA) PðCOMM ¼ 1jEXP ¼ 1Þ � PðCOMM ¼ 1jEXP ¼ 0Þ;ðBÞ PðSERVOUT ¼ 1jEXP ¼ 1Þ � PðSERVOUT ¼ 1jEXP ¼ 0Þ;ðC) PðOFFPROD ¼ 1jEXP ¼ 1Þ � PðOFFPROD ¼ 1jEXP ¼ 0Þ:

These differences can be regarded as the ‘‘treatment effects’’ (TE) of exporting on

the probability of participation in other internationalisation modes. Positive (neg-

ative) value means that exporting makes it more (less) likely to engage in other

internationalisation modes than not exporting. Hence, when the effect is positive,

we interpret this as evidence of complementarity versus the substitutability rela-

tionship between participation strategies (the opposite is true for negative values). In

the same way, we can also look at the TE of engaging in any, or all, of the other

strategies on the probability of offshoring:

ðD) PðOFFPROD ¼ 1jCOMM ¼ 1Þ � PðOFFPROD ¼ 1jCOMM ¼ 0ÞðEÞ PðOFFPROD ¼ 1jSERVOUT ¼ 1Þ � PðOFFPROD ¼ 1jSERVOUT ¼ 0ÞðFÞ PðOFFPROD ¼ 1jEXP ¼ 1; COMM ¼ 1Þ

� PðOFFPROD ¼ 1jEXP ¼ 0; COMM ¼ 0ÞðGÞ PðOFFPROD ¼ 1jEXP ¼ 1;COMM ¼ 1Þ

� PðOFFPROD ¼ 1jEXP ¼ 0; COMM ¼ 0ÞðHÞ PðOFFPROD ¼ 1jEXP ¼ 1; COMM ¼ 1; SERVOUT ¼ 1Þ

� PðOFFPROD ¼ 1jEXP ¼ 0; COMM ¼ 0; SERVOUT ¼ 0Þ:

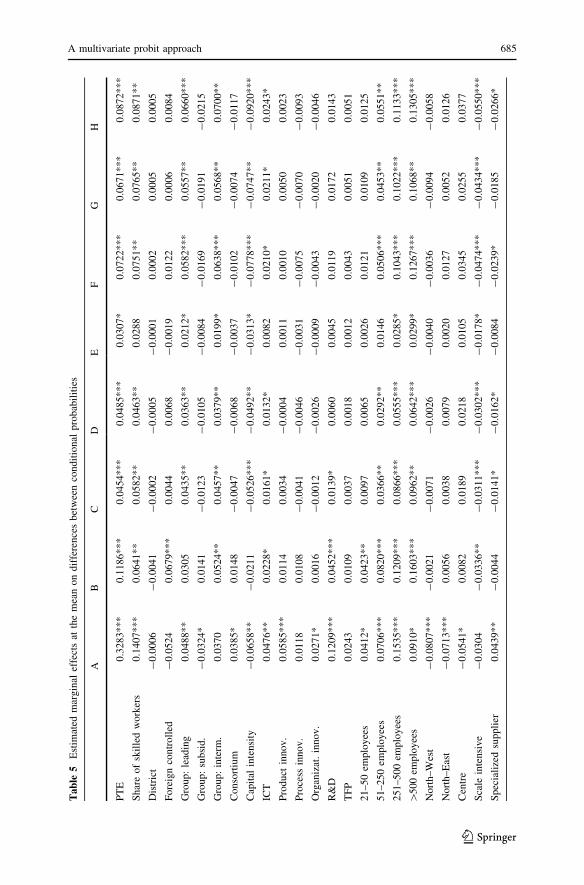

We consider the estimated MEMs of covariates on the TE above as well: a

covariate’s MEM measures the effect of the covariate on the difference in the

probability of adopting a specific internationalisation strategy between firms that

pursue other strategies and firms that do not. To explain the point, we refer to the TE

of exporting on the probability of offshoring (C) and first consider the MEM of

investing in R&D. The estimated MEM, significant and equal to 0.014, means that

the TE of exporting on the probability of offshoring is greater (by 1.4 % points) for

firms that invest in R&D than for firms that do not invest in R&D. As result, firms

that invest in R&D are more likely, compared to firms not investing, to complement

export and offshoring instead of substituting offshoring for export. In contrast,

684 P. Calia, M. R. Ferrante

123

Tab

le5

Est

imat

edm

argin

alef

fect

sat

the

mea

non

dif

fere

nce

sbet

wee

nco

ndit

ional

pro

bab

ilit

ies

AB

CD

EF

GH

PT

E0

.32

83

***

0.1

18

6*

**

0.0

45

4*

**

0.0

48

5*

**

0.0

30

7*

0.0

72

2*

**

0.0

67

1*

**

0.0

87

2*

**

Sh

are

of

skil

led

wo

rker

s0

.14

07

***

0.0

64

1*

*0

.05

82

**

0.0

46

3*

*0

.028

80

.07

51

**

0.0

76

5*

*0

.087

1*

*

Dis

tric

t-

0.0

00

6-

0.0

04

1-

0.0

00

2-

0.0

00

5-

0.0

00

10

.00

02

0.0

00

50

.000

5

Fo

reig

nco

ntr

oll

ed-

0.0

52

40

.067

9*

**

0.0

04

40

.006

8-

0.0

01

90

.01

22

0.0

00

60

.008

4

Gro

up

:le

adin

g0

.04

88

**

0.0

30

50

.04

35

**

0.0

36

3*

*0

.021

2*

0.0

58

2*

**

0.0

55

7*

*0

.066

0*

**

Gro

up

:su

bsi

d.

-0

.03

24

*0

.014

1-

0.0

12

3-

0.0

10

5-

0.0

08

4-

0.0

16

9-

0.0

19

1-

0.0

21

5

Gro

up

:in

term

.0

.03

70

0.0

52

4*

*0

.04

57

**

0.0

37

9*

*0

.019

9*

0.0

63

8*

**

0.0

56

8*

*0

.070

0*

*

Co

nso

rtiu

m0

.03

85

*0

.014

8-

0.0

04

7-

0.0

06

8-

0.0

03

7-

0.0

10

2-

0.0

07

4-

0.0

11

7

Cap

ital

inte

nsi

ty-

0.0

65

8*

*-

0.0

21

1-

0.0

52

6*

**

-0

.049

2*

*-

0.0

31

3*

-0

.07

78

***