how buyers of consulting firms will spend their m&a ... · the perspective of both strategic...

TRANSCRIPT

Growing equity, realizing value

Management Consulting

Engineering

Media Agencies

IT Services

Human Resources

Private Equity

How buyers of consulting firms will spend their M&A budgets in 2017Vital research for owners of knowledge-intensive services businesses.

The Buyers Research Report2 Contents

Contents

Foreword 3

Key buyer insights 4

M&A activity expectations and demands 7

Buyer propensity for acquisitions 7

Buyer demands by capability 8

Buyer demand by sector 11

Buyer demands by region 13

Private equity M&A activity and acquisition demands 15

Consulting segment overviews 22

Management consulting 22

IT consulting 24

Media 26

Engineering consulting 28

Human Resources consulting 30

Buyer evaluation, valuation insights, deal structuring & investment appraisal 34

Buyer evaluation of acquisition opportunities & minimum acceptable KPIs 34

Buyer adjusted EBITDA valuation metric analysis 39

Buyer approach to deal structuring & earn-outs 42

Buyer approach to investment appraisal 44

Conclusion 48

About the survey & scoring methodology 51

Appendix 53

© Equiteq Ltd. 2016 3Foreword

Foreword

We are pleased to present the findings from our third annual survey amongst global buyers of knowledge-intensive services businesses.

For the third year in a row Equiteq has commissioned a comprehensive survey of the market landscape to deliver current, actionable intelligence that isn’t available from any other source. This report examines the trends impacting businesses in each of our five segments: Management consulting, IT consulting, Media & Marketing, Engineering consulting and Human Resources.

For the first time, our review contains analysis from the perspective of both strategic buyers and private equity firms. Notably, private equity respondents demonstrated a willingness to pay higher prices than strategic buyers. They also demonstrated an interest in Intellectual Property rich consulting businesses and appetite for businesses with a financial services or healthcare sector focus.

Demand for acquisitions remains very strong yet there appears to be a reduction in growth of new acquisition opportunities coming to market. This may be a momentary slowdown, or it might suggest the start of a period of increasing competition for assets, supporting stronger pricing power for selling shareholders of knowledge-intensive services businesses.

It is also clear that the convergence trend in adjacent segments of the knowledge outsourcing world is mature to the point where it is a normal component of operational and M&A growth in the sector. This means that while most strategic buyers prioritized expanding their existing capabilities, all respondents indicated an appetite to acquire outside of their core segment. There was notable demand amongst Human Resources buyers to acquire in Management consulting and a convergence in demands between:

• Management consulting, IT consulting and Media buyers; and

• IT consulting and Engineering consulting buyers.

I would like to extend my thanks to the participants of our survey, who provided us with real world views of senior executives and M&A leads within buyers globally.

David Jorgenson CEO, Equiteq

This report has surveyed an important and representative cross-section of the entire buyer landscape for the consulting and knowledge-intensive services industry.

Whether you are running a Management consultancy, IT services firm, Marketing agency, Engineering consulting practice, or Human Resources business, there is one common denominator – you are presiding over an asset that is predominately rich in human capital.

In the last five years over 10,000 transactions have taken place in this space. Over 80% of these deals are below $100m and approximately 35% are in the $10m to $100m range. Private equity buyers make up 10% of transactions that are over $20m in value.

The ecosystem of buyers transcends a number of categories, ranging from global strategic acquirers, operating within and outside of professional services, to financial buyers that make investments within the business services sector.

The Buyers Research Report4 Key buyer insights

BuyERS SEEInG A SloWDoWn In GRoWTH oF nEW oPPoRTunITIES

CoMInG To MARKET:

RoBuST ACquISITIon DEMAnD

No. of acquisitions expected to be made in next 2-3 years

(as strong as prior year)

% of buyers expect acquisitions to be either a primary driver of growth

or equal in importance to organic growth (87% last year)

Average acquisition budget ($72m last year)

Proportion of buyers seeing less opportunities than last year

8%86%

$70m

$

3.8

25% 2015 2016

Proportion of buyers seeing more opportunities than last year

39% 31% 2015 2016

What are the market dynamics supporting robust valuations? (More on page 7)

Key buyer insights

What market convergence trends are generating premium valuations from acquirers in different consulting segments? (More on page 8)

What are the hottest sectors and regions? (More on pages 11 and 13)

Energy in very high demand amongst Engineering consulting buyers.

Financial Services in high or moderate demand across other consulting buyer groups.

Healthcare in high demand amongst private equity buyers.

North America, followed by Europe & ME and Asia-Pacific, is highlighted as the region where global buyers will be most acquisitive.

PoTEnTIAlFoR PREMIuMVAluATIonS

$

(Data refers to average of strategic acquirers.)

Equiteq Consulting Segments

Management consulting

IT consulting

Engineering consulting

HR consulting Media

© Equiteq Ltd. 2016 5Key buyer insights

What does Private Equity think? (More on page 15)

Management consulting, IT consulting and Media capabilities in high demand.

Interested in consulting propositions across sectors enhanced by intellectual property (IP).

Consulting capabilities focused on the financial and healthcare sectors are considered highly attractive.

What are the deep-dive trends in your sector?

Management consulting capabilities are in demand across buyer groups. Management consulting buyers demonstrate a strong interest in enhancing their offering with IP relating to unique methods and analytics tools. (More on page 22)

IT consulting buyers have the largest budgets for acquisitions, which we expect to be focused on expertise relating to software with clear client ROI, cloud applications and related integration services and consulting. (More on page 24)

Media buyers expect to be the most acquisitive over the next few years, reflecting the evolution of digital marketing, which continues to transform Media client’s businesses. (More on page 26)

Engineering consulting is the only segment where almost half of buyers are being presented with more new opportunities than last year. The segment is reinforced by robust market fundamentals supporting growth and consolidation in the overall E&C industry. (More on page 28)

HR consulting buyers target lower valuation metrics and KPIs. However, trends in the industry highlight specific HR consulting capabilities underpinned by solid market drivers. (More on page 30)

How will buyers evaluate your firm? (More on page 34)

(Average minimum KPIs acceptable across buyers that we surveyed.)

12% 45%

31%

Rev. Growth Gross Margin

The average equity IRR target by PE

280Rev. per

employee ($k):

How will buyers structure your deal? (More on page 42)

44% of consideration typically offered up-front. Earn-out to retain key people normally lasts around 3 years.

How will buyers value your firm? (More on page 39)

On average, private equity investor respondents are prepared to pay higher prices than strategic buyer groups, but are more discerning over financial metrics and depth of IP.

(Average EV/ EBITDA metrics based on an illustrative 20% EBITDA margin opportunity presented at three EBITDA growth rates.)

Buyer adjusted Enterprise Value/ EBITDA valuation metric analysis

6.410-20% EBITDA

growth p.a.7.5

20-30% EBITDA

growth p.a.8.2

30-40% EBITDA

growth p.a.

How will buyers approach investment appraisal? (More on page 44)

The use of NPV analysis is preferred amongst strategic buyers, while equity IRR analyses are typically used by private equity.

$

44%

yR1 yR2 yR3

PRIVATEEquITy

The Buyers Research Report6 Section Heading

The section heading goes here like this if needed.

Christine Parry, leadership Development Consultancy.

Sold.

© Equiteq Ltd. 2016 7M&A activity expectations and demands

M&A activity expectations and demands

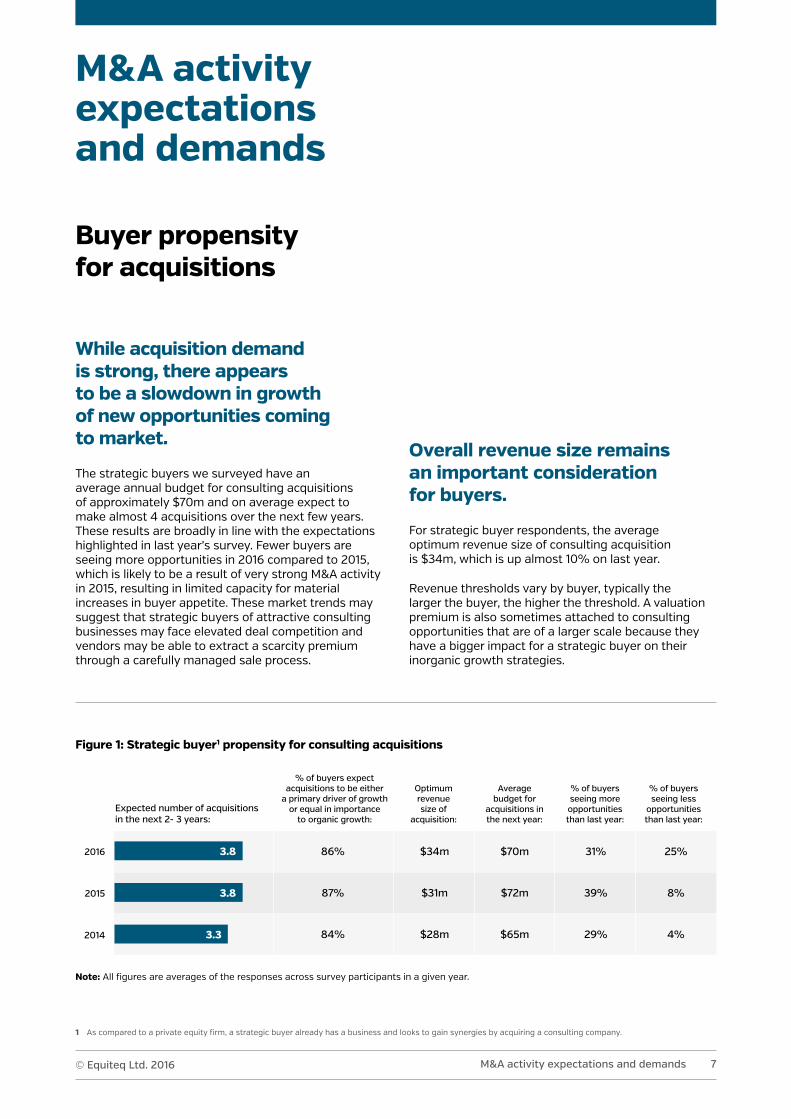

Buyer propensity for acquisitions

While acquisition demand is strong, there appears to be a slowdown in growth of new opportunities coming to market.

The strategic buyers we surveyed have an average annual budget for consulting acquisitions of approximately $70m and on average expect to make almost 4 acquisitions over the next few years. These results are broadly in line with the expectations highlighted in last year’s survey. Fewer buyers are seeing more opportunities in 2016 compared to 2015, which is likely to be a result of very strong M&A activity in 2015, resulting in limited capacity for material increases in buyer appetite. These market trends may suggest that strategic buyers of attractive consulting businesses may face elevated deal competition and vendors may be able to extract a scarcity premium through a carefully managed sale process.

overall revenue size remains an important consideration for buyers.

For strategic buyer respondents, the average optimum revenue size of consulting acquisition is $34m, which is up almost 10% on last year.

Revenue thresholds vary by buyer, typically the larger the buyer, the higher the threshold. A valuation premium is also sometimes attached to consulting opportunities that are of a larger scale because they have a bigger impact for a strategic buyer on their inorganic growth strategies.

Figure 1: Strategic buyer1 propensity for consulting acquisitions

2014

2015

2016

Expected number of acquisitions in the next 2- 3 years:

note: All figures are averages of the responses across survey participants in a given year.

1 As compared to a private equity firm, a strategic buyer already has a business and looks to gain synergies by acquiring a consulting company.

% of buyers expect acquisitions to be either

a primary driver of growth or equal in importance

to organic growth:

Optimum revenue size of

acquisition:

Average budget for

acquisitions in the next year:

% of buyers seeing more opportunities than last year:

% of buyers seeing less

opportunities than last year:

3.8 86%

87%

84%

$34m

$31m

$28m

$70m

$72m

$65m

31%

39%

29%

25%

8%

4%

3.8

3.3

The Buyers Research Report8 M&A activity expectations and demands

Buyer demands by capability

Demand is strong across the board, however Media firms plan to make the most acquisitions and IT firms have the biggest acquisition budgets.

Our research indicates that although there is robust acquisition demand across all buyer groups, Media buyers have the strongest expectations for future acquisition activity and IT consulting buyers have the largest budgets for acquisitions. Buyers, along with their clients, in both of these industries are facing both opportunity and disruption from technological change. This is driving strong demand for acquisitions that bring cutting-edge capabilities on-board.

Table 1: Breakdown of acquisition activity by strategic buyer group

note: The figures in the table relate to average responses to an array of questions relating to future acquisition activity for each buyer group.

Buyer group

Managementconsulting

ITconsulting

Mediaconsulting

Engineeringconsulting

HRconsulting

No. of acquisitions expected to be undertaken in the next 2- 3 years: 3.6 3.6 5.0 4.3 3.3

The proportion of buyers expecting acquisitions to be a primary

driver of growth:21% 24% 19% 34% 13%

Average budget for acquisitions in the next year ($m): 53 93 66 83 49

Optimum size of acquisition ($m): 33 41 31 36 24

The proportion of buyers seeing more opportunities than last year: 24% 37% 28% 47% 25%

Almost half of the Engineering consulting buyers we surveyed said that they were seeing more opportunities than last year, a higher proportion than any other buyer group. We expect this to be driven by the recovery of the broader Engineering & Construction (E&C) industry, which is benefiting from robust macro-economic fundamentals and stabilizing oil prices.

© Equiteq Ltd. 2016 9M&A activity expectations and demands

Buyers are looking for growth opportunities by expanding their service lines to capture wallet share and enter new markets.

Although a range of factors contribute to how strategically attractive a company is to a potential buyer, acquirers will place a strong emphasis on evaluating the specific consulting capabilities that they will be acquiring. This might be driven by a desire to expand on a core competency, complement existing services or acquire a separate new service line.

Our research suggests that most buyer groups prioritize expanding their existing core capabilities, however all respondents also demonstrated an interest in acquiring capabilities within adjacent consulting segments. We want to highlight three convergence trends that we observed, which is changing some consulting segment boundaries:

1. Media, IT and Management consulting respondents demonstrate interest in each other’s segments;

2. Engineering and IT consulting buyers are demanding capabilities within each other’s segments; and

3. Human resources consulting buyers are interested in acquiring traditional Management consulting capabilities.

note: Each buyer was asked to rank the consulting capabilities they considered important for acquisition. See page 51 for further detail on scoring methodology.

Figure 2: Heat map of Equiteq’s proprietary weighted scoring of consulting capability demand by strategic buyer group

High Demand (score: 19+)

Medium Demand (score: 15-18)

Low Demand (score: 14 or less)

Buyer group

Managementconsulting

ITconsulting

Mediaconsulting

Engineeringconsulting

HRconsulting

Management consulting

IT consulting

Media consulting

Engineering consulting

HR consulting

Con

sult

ing

capa

bilit

ies

dem

ande

d

HR consulting and Management consultingThis trend may represent the strong opportunities within HR consulting around organizational redesign and executive coaching. Acquiring a premium strategic consulting capability offers this buyer group with access to the C-suite at clients and a better chance of offering these adjacent HR consulting services.

The Buyers Research Report10 M&A activity expectations and demands

This convergence creates the potential for sellers to achieve a premium valuation through synergy potential with different consulting segments.

Figure 3: Consulting segment convergence

Management consulting, Media and IT consulting The lines between marketing, technology and business advisory are becoming less clear. Many buyers are developing their customer-focused consulting services into a holistic advisory offering, which connects marketing with business strategy and operations, along with a strong knowledge of a client’s technologies.

Engineering consulting and IT consultingBuyers in both segments are observing new market trends relevant to their E&C clients, such as the use of building information modelling (BIM), digital transport and E&C-focused big data analytics. Pressures on profit margins in E&C has forced companies in the industry to increasingly use BIM to automate work. Digital transport and big data are also improving the dissemination of information to improve efficiencies.

Equiteq Consulting Segments

Management consulting

IT consulting

Engineering consulting

HR consulting Media

Relevant market activityThere have been a string of deals acquiring business advisory capabilities from buyers such as Heidrick & Struggles and GP Strategies.

Relevant market activityThere have been several acquisitions of creative agencies amongst leading Management consulting and IT consulting buyers, including Accenture, Deloitte, PwC and IBM.

Relevant market activityThe perceived opportunity from some of these trends is expected to have driven Accenture’s acquisition of Schlumberger Business Consulting, the management consulting unit of Schlumberger. It was also relevant to the acquisition of our client, Noah Consulting, a leading advanced information management service provider for the oil and gas industry, by Indian outsourcing firm, Infosys.

© Equiteq Ltd. 2016 11M&A activity expectations and demands

Buyer demand by sector

The four hottest sector verticals are Financial Services, Energy, Healthcare and Retail.

In addition to specific consulting services, many acquirers are attracted by underlying client sector verticals. This could be driven by a desire to enable expansion in their share of markets, underpinned by strong long-term drivers for growth or to extract synergies by cross-selling their existing services and products into the target’s clients within that sector.

The results of our survey show that most survey respondents prioritize consulting acquisitions that are diversified across sector. Nonetheless, the financial services and energy sectors score highly in importance amongst those respondents looking for opportunities with a sector specialism.

The energy sector stands out as scoring highly in importance, primarily amongst Engineering consulting buyer respondents who typically have a substantial E&C client base serving this sector. We discuss the trends relating to energy, along with the retail-focus amongst HR and Media consultants, as part of our deep dives into specific consulting segments on pages 22 to 31.

note: Each buyer was asked to rank the sector verticals they considered important for acquisition. See page 51 for further detail on scoring methodology.

Equiteq weighted scoring

Con

sult

ing

capa

bilit

y

Figure 4: Equiteq proprietary weighted scoring of sector demands across survey participants

Retail

Other

Healthcare

Energy

Financial services

Diversified

0 5 3010 3515 20 25

30

17

16

13

13

11

The Buyers Research Report12 M&A activity expectations and demands

note: See page 51 for further detail on scoring methodology.

Figure 5: Equiteq proprietary weighted scoring of sector demand by strategic buyer group

Very High Demand (score: 27+)

High Demand (score: 20-26)

Medium Demand (score: 13-20)

Low Demand (score: 13 or less)

Buyer group

Managementconsulting

ITconsulting

Mediaconsulting

Engineeringconsulting

HRconsulting

Diversified

Financial Services

Energy

Healthcare

Retail

Sect

or f

ocus

Demand for consulting services focused on the financial services sector is underpinned by increasing digital disruption, regulation and cyber security.

The demand for financial services specialisms is highest amongst IT consulting and Media buyer respondents. This is driven by opportunities to service large financial institutions dealing with fintech and challenger banks’ market entry, increased regulatory demands and cyber security concerns. Digital banking is continuing to change all aspects of financial services, driving traditional financial institutions to rapidly implement technological changes. This year it was also reported that US regulators plan to require banks to adopt baseline safeguards to protect against cyber-threats. This comes after a number of recent high-profile cyber-attacks on financial institutions including an attempt earlier in the year to transfer almost $1bn from the accounts of the Bangladesh Central Bank at the US Federal Reserve. Demand for this sector focus is also robust for

Management consulting buyers. We expect this to be driven by demand for consulting capabilities related to the analysis and evaluation of new complex financial regulations, compounded by stronger enforcement across various jurisdictions since the financial crisis. In Europe specifically, some consulting buyers have told us that they are also setting up Brexit consulting teams. These specialist teams will, amongst other things, assist banks in connection with preparing contingency plans for the UK leaving the EU and how it will impact their ability to “passport” services into the rest of Europe.

Source: Strategic choices for banks in the digital age, McKinsey & Co.

Source: PwC’s 17th Global CEO Survey

If the last epoch in retail banking was defined by a boom-to-bust expansion of consumer credit, the current one will be defined by digital…. Banks have three to five years at most to become digitally proficient.

More than 70% of Banking & Capital Markets CEOs see cyber security as a threat to growth.

© Equiteq Ltd. 2016 13M&A activity expectations and demands

2 To remove the bias from responses from regional heads, we have only considered the results of survey participants that have a global responsibility at their organization.

Buyer demands by region

Acquisition appetite amongst survey participants is stronger in developed markets.

Naturally, trade buyers often focus their acquisitions on countries and regions where they already have a presence, as this supports integration and synergies with their existing business. Nonetheless, high-profile cross-border consulting acquisitions are common and enable foreign buyers to penetrate new markets, gain new clients and grow revenues with existing global accounts.

Most large consulting firms that we speak with confirm interest in “gateway countries” like Singapore or Hong Kong and highlight emerging market growth in up-and-coming markets like China as an increased priority in connection with their global strategy. However, our survey findings suggest that acquisition demand is typically focused on developed markets.

Almost 75% of respondents with a global responsibility at their buyer highlighted that North America or Europe & the Middle East was their priority for consulting acquisitions. Most strategic buyers are already established in these regions, which typically offers more mature consulting opportunities with lower investment risk profiles, enhanced with the latest skills relating to cutting-edge technologies and approaches. Although buyers score North America, Europe & the Middle East as largely equal important regions for acquisitions, those buyers focused on acquisitions in the former region have far higher acquisition expectations.

Acquisition appetite is more variable in the Asia-Pacific region, due to large differences of maturity between countries. Japanese buyers have become highly active buyers of consulting business across the globe. There is also considerable activity within developed markets in the region, for instance, Australia, Singapore and Hong Kong.

note: Each buyer was asked to rank the regions they considered important for acquisition. Emerging markets within each continent are included within the emerging market statistics only. Heat map is based on the proportion of global buyers focused on acquisitions in a given region. See page 51 for further detail on scoring methodology.

Figure 6: Equiteq proprietary weighted scoring of regional demand across respondents with a global responsibility

Very High Demand (Region is of high importance for acquisitions and high expected numbers of acquisitions to occur in region)

High Demand (Region is of high importance for acquisitions and moderate expected numbers of acquisitions to occur in region)

Medium Demand (Region is of moderate importance for acquisitions and moderate expected numbers of acquisitions to occur in region)

Low Demand (Region is of low importance for acquisitions and moderate expected numbers of acquisitions to occur in region)

north America

Average acquisitions by buyers focused on region

Scoring of importance given to region

Europe & Middle East

Average acquisitions by buyers focused on region

Scoring of importance given to region

Emerging Markets

Average acquisitions by buyers focused on region

Scoring of importance given to region

Asia-Pacific

Average acquisitions by buyers focused on region

Scoring of importance given to region

5.3 2.4 2.2 2.3

30 32 16 22

The Buyers Research Report14 M&A activity expectations and demands

The findings suggest north America as the region expected to see the most acquisition activity.

Buyers focused on making acquisitions in North America comprised predominantly of IT and Engineering consulting buyers. North America is still considered to be ahead of the curve in the adoption of the latest technologies, driving demand for new IT consulting capabilities within the region. Furthermore, consulting spend amongst E&C clients in the region is expected to increase, as economic conditions remain strong and the region’s oil producers recover following the turmoil of last year.

The majority of respondents consider acquisitions in Europe & the Middle East as also being of high importance.

Post-Brexit market data and recent business surveys suggest that the UK’s vote to leave the EU has not led to a slow-down in UK and European acquisitions. Our regular dialogue with buyers suggests that they are currently treating the aftermath of the UK’s vote to leave the EU as business as usual. Some foreign buyers may also consider a depreciated sterling as an opportunity to deploy increased purchasing power in UK acquisitions.

The Asia-Pacific region as a whole is a lower priority for acquisitions, although there are some highly active M&A markets within the region.

Although our survey indicates that Asia-Pacific is a lower priority for acquisitions, we observe that Japanese services firms of various sizes are increasingly acquisitive of consulting firms in Asia and elsewhere across the globe. This is driven by a combination of a lack of domestic growth opportunities, a strong yen and strong balance sheets for acquisitions.

Furthermore, it should be noted that Australia, as well South East Asia and Hong Kong, are standing out as dynamic M&A markets, fueled by the presence of quality services firms across segments. Buyers expressing an interest in Asia-Pacific will typically focus on larger opportunities with a business strongly rooted locally, but built upon international management standards.

© Equiteq Ltd. 2016 15M&A activity expectations and demands

Private equity M&A activity and acquisition demands

Private equity are acquisitive and offer additional options for sellers of consulting businesses.

We continue to observe strong demand amongst private equity (PE)3 firms for consulting acquisitions. Therefore, for the first time, we have included PE buyers into our survey.

PE buyers differ from trade buyers in that the former acquire strictly to realize a cash return on their invested equity, usually in 3 to 5 years. Strategic buyers typically acquire to realize long-term strategic value by combining a consulting acquisition with their existing operations. As a result, PE buyers will look for specific traits in a consulting acquisition and selling to a PE buyer will have different implications as compared with selling to a trade buyer.

PE have substantial capital available for consulting acquisitions. Budgets and optimum revenue size for acquisitions amongst financial buyers varies considerably depending on the fund making the purchase and whether the acquisition is a platform investment or bolt-on to an existing one. PE is a flexible source of capital and can be used to finance a full exit to the management team or a partial exit that enables owners to retain an interest in the equity upside. This partial exit can be used to accelerate growth through acquisitions.

3 Private equity are sometimes referred to as financial buyers or investments firms within this report.

PRIVATEEquITy

The Buyers Research Report16 M&A activity expectations and demands

Alex Stirling, Managing Director, The Carlyle Group (following Carlyle’s buyout of a majority stake in PA Consulting)

We have invested in the sector [consulting] before and looked at a number of consulting firms because we believe the sector has strong tail winds caused by regulatory and technological change.

We expect that interest in these three segments of the market is supported by high-profile precedent deals amongst large, multinational PEs in these sectors. This includes successful exits and recent landmark investments from the likes of CVC, Carlyle, Berkshire Partners, Blackstone Group and TPG Capital.

Nevertheless, the vast majority of financial buyers are generalists, with a broad interest in business services. We therefore expect that they will continue to demonstrate strong interest across all consulting segments, targeting opportunities that have specific attributes. These include strong management teams, robust long-term drivers for growth and barriers to entry that are maintained by proprietary expertise which is retained and leveraged through intellectual property (IP).

Private equity rank Management consulting, IT consulting and Media as important capabilities, although the buyer group is expected to demonstrate interest across the knowledge-intensive services market.

note: Each buyer was asked to rank the capabilities they considered important for acquisition. See page 51 for further detail on scoring methodology.

Figure 7: Equiteq proprietary weighted scoring of capability demands for private equity

0

5

10

15

20

30

25

IT consulting

24

Management consulting

26

Media consulting

22

Engineering consulting

17

HR consulting

11

© Equiteq Ltd. 2016 17M&A activity expectations and demands

Financial buyers have higher business performance expectations than strategic buyers, but are willing to pay more for premium performance.

Our research shows that PE respondents seek higher average acceptable minimum KPIs, such as growth and margins, on acquisition opportunities. They also place more importance on consulting opportunities that are enhanced by IP, particularly software and revenue generating IP. However, it should be noted that these more elevated investment requirements are reflected in significantly higher average valuation metrics as compared with other buyer groups that we surveyed.

Table 2: Private equity KPI expectations and target valuation metrics

Private equity Strategic buyers

Annual revenue growth rate (%) 14% 11%

Gross margin (%) 52% 44%

Revenue per employee ($k) 370 269

Utilization (%) 71% 66%

Targeted current year EBITDA multiple for an illustrative fixed 20% EBITDA margin

consulting business:7.4x 6.2x

note: Data reflects average responses. The responses relate to questions on the minimum acceptable KPIs required and the target valuation metrics for an illustrative consulting investment.

The Buyers Research Report18 M&A activity expectations and demands

Private equity have a particularly strong interest in consulting capabilities focused on the financial services and healthcare industries.

PE buyers frequently tell us that they target investments in industries underpinned by long-term drivers for non-discretionary demand. The results of our survey demonstrate strong interest in two sectors supported by this market dynamic.

As previously discussed, growth in consulting to financial services is underpinned by changes in the competitive and regulatory landscape, as well as concerns over cyber security. For PE, healthcare is also a strong sector for investment given that it is defensive in nature and is underpinned by three powerful long-term trends – an ageing global population, unfunded demand and rising costs, and clinical innovation.

In North America the U.S. healthcare services sector has also benefited from the reforms created by the Affordable Care Act. PE interest in this area has been significant, especially for healthcare consulting businesses enhanced by advanced analytics capabilities. The most notable deals this year were EQT’s acquisition of Press Ganey and Veritas Capital’s acquisition of Verisk Analytics’ healthcare services business.

Figure 8: Equiteq proprietary weighted scoring of sector demands for private equity versus strategic acquirers

0

5

10

15

25

20

35

30

Private equity

Strategic acquirers

Diversified

31 30

Healthcare

20

12

Retail

8

15

Other

6

12

Financial services

20

16

Energy

1417

note: Each buyer was asked to rank the sectors they considered important for acquisition. See page 51 for further detail on scoring methodology.

© Equiteq Ltd. 2016 19M&A activity expectations and demands

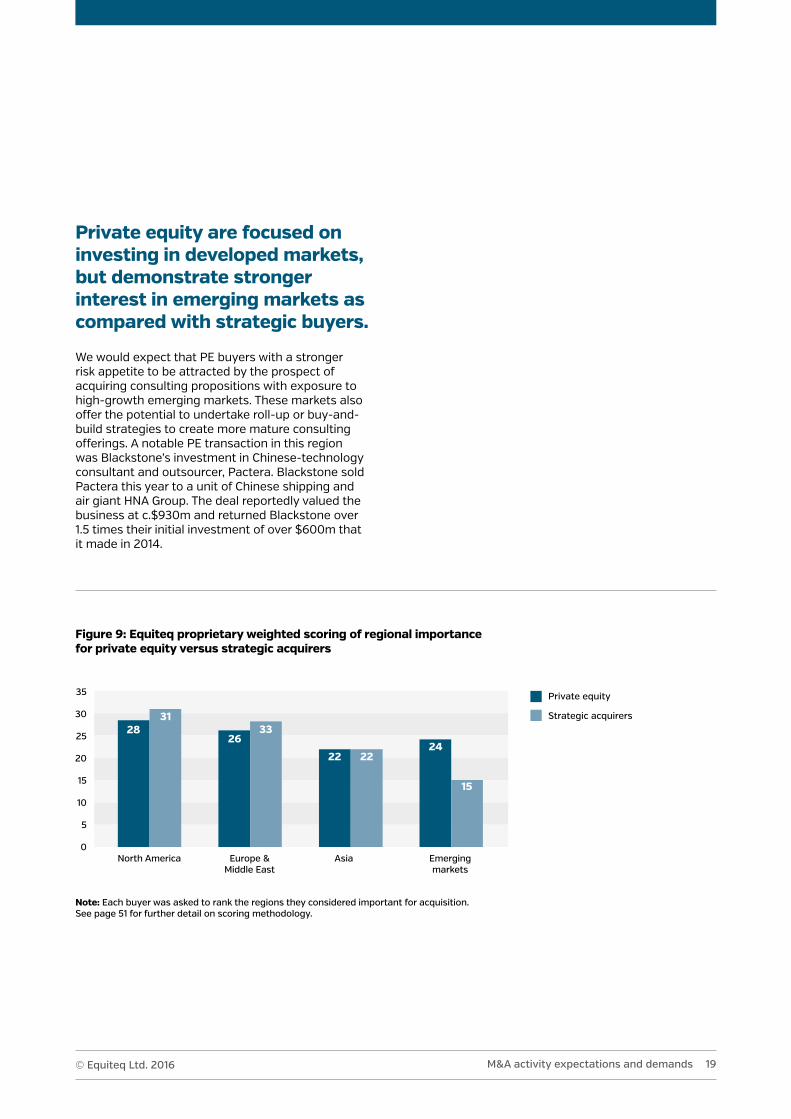

Private equity are focused on investing in developed markets, but demonstrate stronger interest in emerging markets as compared with strategic buyers.

We would expect that PE buyers with a stronger risk appetite to be attracted by the prospect of acquiring consulting propositions with exposure to high-growth emerging markets. These markets also offer the potential to undertake roll-up or buy-and-build strategies to create more mature consulting offerings. A notable PE transaction in this region was Blackstone’s investment in Chinese-technology consultant and outsourcer, Pactera. Blackstone sold Pactera this year to a unit of Chinese shipping and air giant HNA Group. The deal reportedly valued the business at c.$930m and returned Blackstone over 1.5 times their initial investment of over $600m that it made in 2014.

Figure 9: Equiteq proprietary weighted scoring of regional importance for private equity versus strategic acquirers

0

5

10

15

25

20

35

30

North America Europe & Middle East

Asia Emerging markets

2826

2224

3133

22

15

note: Each buyer was asked to rank the regions they considered important for acquisition. See page 51 for further detail on scoring methodology.

Private equity

Strategic acquirers

The 2016 Buyers Reaserch Report20 Section Heading

The section heading goes here like this if needed.

Insight 1Buyers’ expectations over the next three years

© Equiteq Ltd. 2016 21Section Heading

nick Kent, Management Consultancy.

Sold.

The Buyers Research Report22 Consulting segment overviews

Consulting segment overviews

Management consulting

Management consulting capabilities, which can enable substantial revenue synergies for strategic buyers, are in high-demand across all buyer groups.

Traditional management consulting capabilities have strong cross sector appeal. One driver is that engagements often result in a long tail of activity to implement and embed change. Many strategic buyers in sectors other than management consulting view management consulting work as the precursor to their own offerings. This dynamic often leads management consultancies to be viewed as “tip of spear” acquisitions to allow acquirers to enter new markets.

Management consulting buyers are acquisitive, but have lower M&A expectations compared to other strategic buyer groups.

From our discussions with some of the leading players in this segment, many tell us that they place a high importance on cultural affinity with a resulting selective approach to acquisitions. This is balanced with the need to use M&A as vehicle for growth in niche capabilities.

Management consulting buyer respondents are more likely to use a balanced scorecard of qualitative and quantitative measures to evaluate an acquisition opportunity - with 32% adopting this approach compared to 24% across buyers. Using a balanced scorecard approach may reflect the industry’s long experience of using this method as a strategy performance management tool.

Management consulting buyers demonstrate a strong interest in enhancing their consulting offering with IP relating to unique methods and tools.

Demand for methods and tools amongst Management consulting respondents is driven by a desire to differentiate their consulting offering and enhance profit margins. This is typically achieved by leveraging automated methodologies and analytics tools to productize aspects of a consulting engagement.

Management consulting other strategic buyers

No. of acquisitions expected to be made in next 2-3 years: 3.6 4.1

Average budget for acquisitions: $53m $73m

© Equiteq Ltd. 2016 23Consulting segment overviews

Management consulting buyers - Key findings

10-20% EBITDA

growth p.a.:

20-30% EBITDA

growth p.a.:

30-40% EBITDA

growth p.a.:

6.2x 7.3x 7.9x

note: Data reflects average results.

Acquisition activity: Target valuation metrics:

Minimum acceptable KPIs: Targeted deal structures:

3.6

11% 42%

41%

12%

$53m

$270k 46%

65%

2.5 yEARS

15%

No. of acquisitions expected to be made

in next 2-3 years

Rev. Growth

Upfront

Gross Margin

Fixed Deferred

Average budget for acquisitions

Rev. per employee

Deferred Earn-out

Utilization rate

Earn-out period

Equity ownership of key management

Adjusted EBITDA Multiples for consistent 20% adjusted EBITDA margin opportunities

at the following growth rates:

The Buyers Research Report24

IT consulting

IT consulting buyers have large budgets for acquisitions, which we expect to be focused on consulting and integration services relating to software with clear client RoI and the latest cloud-based applications.

The high propensity to do deals amongst IT consulting respondents, along with the strong demand for IT consulting capabilities amongst other buyer groups, reinforces why this is one of the most active consulting sectors for M&A activity.

The impact of cloud based platforms and the spawning of new app providers coincides with the wave of high-profile restructurings and deal activity involving legacy technology giants such as Hewlett Packard Enterprises and Intel Corporation. This year, we also saw the completion of the landmark $67bn takeover of EMC by Dell. Dell is seeing a decline in Personal Computing and is seeking to reinvent itself by accessing the more lucrative data storage and cloud infrastructure markets.

According to recent estimates from Gartner, the global public cloud services market is set to grow 17% in 2016 to $208.6bn. This growth potential is driving demand amongst technology consultants for skillsets related to the latest business cloud offerings, particularly those provided by the current leaders in the space - Amazon, Microsoft, IBM and Google.

The demand for these latest innovative technologies is likely to have been reflected in the higher minimum acceptable KPIs and targeted valuation metrics amongst IT consulting buyers that we surveyed.

IT consulting other strategic buyers

No. of acquisitions expected to be made in next 2-3 years: 3.6 4.1

Average budget for acquisitions: $93m $63m

Consulting segment overviews

© Equiteq Ltd. 2016 25Consulting segment overviews

IT consulting buyers - Key findings

10-20% EBITDA

growth p.a.:

20-30% EBITDA

growth p.a.:

30-40% EBITDA

growth p.a.:

6.5x 7.6x 8.2x

note: Data reflects average results.

Acquisition activity: Target valuation metrics:

Minimum acceptable KPIs: Targeted deal structures:

3.6

13% 47%

45%

14%

$93m

$280k 39%

62%

3.1 yEARS

16%

No. of acquisitions expected to be made

in next 2-3 years

Rev. Growth

Upfront

Gross Margin

Fixed Deferred

Average budget for acquisitions

Rev. per employee

Deferred Earn-out

Utilization rate

Earn-out period

Equity ownership of key management

Adjusted EBITDA Multiples for consistent 20% adjusted EBITDA margin opportunities

at the following growth rates:

The Buyers Research Report26

Media

Media buyers expect to be highly acquisitive over the next few years and target high KPIs on their investments.

Media buyers that we surveyed have substantially higher volume M&A expectations for the next few years as compared with other buyer groups.

Media respondents also highlight higher minimum KPI targets for their acquisitions. These KPI demands are reflected in stronger targeted valuation metrics, albeit with expectations of lower upfront cash components as compared with other buyer groups.

We expect the acquisition trends to reflect the evolution of digital marketing, which continues to transform Media client’s businesses.

Industry transformation in this segment is being led by the digital disruption of business models, particularly as it relates to how companies interact with their customers. This is driving executives to demand a more sophisticated marketing service, which involves a knowledge of business consulting and a client’s technologies. From our discussions with market participants, we also observe notable demand for cutting-edge capabilities related to digital advertising, real-time marketing and micro-targeting that leverages the latest digitally derived insight and data science methods.

The findings of our survey highlight that Media buyers consider opportunities focused on the retail industry vertical, along with financial services, as being particularly important. We already discussed some of the competitive pressures from fintech, which are creating opportunities for IT and Media consultants within this sector. Retail is also increasingly being impacted by digital technology, such as the use of smartphones, online outlets and social media to advertise and shop. Many on-premise retailers are therefore turning to Media consultants to help them develop their digital marketing efforts to better compete against new micro, digital only players penetrating the market.

A notable finding from our research was the importance of thought leadership as a type of IP. Media buyer respondents highlighted thought leadership as their most important type of IP, whereas all other strategic buyer groups ranked it as one of their least important. The importance Media buyers place on thought leadership is most likely tied to the rapid rise of new technologies and engagement methodologies in this space.

Media other strategic buyers

No. of acquisitions expected to be made in next 2-3 years: 5.0 3.6

Average budget for acquisitions: $66m $71m

Consulting segment overviews

© Equiteq Ltd. 2016 27Consulting segment overviews

Media buyers - Key findings

10-20% EBITDA

growth p.a.:

20-30% EBITDA

growth p.a.:

30-40% EBITDA

growth p.a.:

7.1x 8.0x 8.7x

note: Data reflects average results.

Acquisition activity: Target valuation metrics:

Minimum acceptable KPIs: Targeted deal structures:

5.0

12% 38%

50%

22%

$66m

$305k 40%

66%

2.9 yEARS

14%

No. of acquisitions expected to be made

in next 2-3 years

Rev. Growth

Upfront

Gross Margin

Fixed Deferred

Average budget for acquisitions

Rev. per employee

Deferred Earn-out

Utilization rate

Earn-out period

Equity ownership of key management

Adjusted EBITDA Multiples for consistent 20% adjusted EBITDA margin opportunities

at the following growth rates:

The Buyers Research Report28

Engineering consulting

Engineering consulting buyers are the most focused buyer group on inorganic growth. Additionally, in contrast to other segments, a large proportion of these buyers are being presented with more opportunities than last year.

Our research findings suggest an increasingly active M&A market for Engineering consulting.

This appears to be reinforced by robust market fundamentals supporting growth and consolidation in the overall E&C industry. Some of these fundamentals include high infrastructure and housing demand, transport digitization trends, stabilising oil prices and favourable population demographic trends.

Engineering consulting buyers rank the energy sector as particularly important.

A substantial proportion of the E&C industry operate within the energy sector and it is therefore a natural sector focus for Engineering consultants. Valuation expectations in the sector have been conservative since the steep falls in oil prices that were experienced at the beginning of 2014. The stabilization in oil prices this year around $50 per barrel is supporting demand for operationally-focused consulting businesses focused on the sector4.

The convergence in capability demands amongst Engineering and IT consulting respondents is also highly relevant to the energy sector. In particular, the technological advancements relating to data analytics are increasingly being used by oil companies to streamline production and reduce their costs.

Engineering consulting other strategic buyers

% of respondents expecting growth to be mainly via acquisition: 34% 19%

% of respondents seeing more opportunities than last year: 47% 28%

Consulting segment overviews

4 Energy sector-focused operational consulting companies that we speak with typically consider oil prices above $50 per barrel supportive of discretionary spend amongst clients for consulting services.

Arthur Hanna, Energy industry leader of Accenture Strategy (Following Accenture’s acquisition of Schlumberger Business Consulting)

The upstream energy sector faces a range of challenges and opportunities, from delivering complex capital projects to exploiting technological advances.

© Equiteq Ltd. 2016 29Consulting segment overviews

Engineering consulting buyers - Key findings

10-20% EBITDA

growth p.a.:

20-30% EBITDA

growth p.a.:

30-40% EBITDA

growth p.a.:

5.8x 7.1x 7.8x

note: Data reflects average results.

Acquisition activity: Target valuation metrics:

Minimum acceptable KPIs: Targeted deal structures:

4.3

10% 41%

43%

21%

$83m

$250k 38%

67%

2.8 yEARS

12%

No. of acquisitions expected to be made

in next 2-3 years

Rev. Growth

Upfront

Gross Margin

Fixed Deferred

Average budget for acquisitions

Rev. per employee

Deferred Earn-out

Utilization rate

Earn-out period

Equity ownership of key management

Adjusted EBITDA Multiples for consistent 20% adjusted EBITDA margin opportunities

at the following growth rates:

The Buyers Research Report30

Human Resources consulting

Acquisition expectations, targeted valuation metrics and acceptable KPIs are lower compared with other buyer groups that we surveyed.

The lower acquisition expectations and lower KPI requirements relative to other segments are reflected in lower target valuation metrics. This suggests HR consulting is an overall slower growth market segment with a less active M&A market.

Notably, HR buyers have higher utilization expectations than all the other buyer groups. However, we typically observe that material variations occur amongst organizations in how this KPI is calculated, which can make it difficult to draw comparisons on specific utilization rate targets between buyers. Nevertheless, this trend may be attributed to less client facing time spent amongst this buyer group on business development, given the indications that there is slower growth in HR consulting than other consulting segments.

Our survey highlights consulting businesses focused on the retail industry as being of high importance amongst HR consulting buyers. We expect this to be driven by the dependence of the sector on client facing staff who are enabled by strong human resources processes, along with the more current drivers of digital transformation impacting how sales functions interact with customers.

Trends that we are observing in the industry highlight specific HR consulting capabilities that are underpinned by solid market drivers.

Although our research findings indicate that acquisition expectations amongst buyers in this consulting segment are lower than other segments, we are observing strong demand amongst HR buyers for specific capabilities. Recent HR focused industry surveys5 highlight that the vast majority of executives see the redesign of their organization around highly empowered teams, new models of management and leadership as a critical priority for them. This appears to be driving demand for related capabilities amongst regular HR consulting buyers, such as Heidrick & Struggles and GP Strategies.

We are also frequently told by IT buyers that they want to develop HR consulting capabilities related to technology solutions which simplify processes using people analytics. Workday is still considered to be a leader in the HR SaaS segment and its partners are in high demand across buyer groups. This was observed by Accenture’s landmark acquisition of leading Workday partner, DayNine Consulting. The deal positions Accenture to become one of the largest certified Workday partners. The demand for technology capabilities amongst HR buyers was not observed in our survey results, which may be due to the limited number of Workday partners and therefore related acquisition opportunities.

HR consulting other strategic buyers

No. of acquisitions expected to be made in next 2-3 years: 3.3 4.1

The % of buyers expecting to grow mainly by acquisition: 13% 25%

Consulting segment overviews

5 Deloitte University Press: Global Human Capital Trends 2015 and 2016 surveys.

© Equiteq Ltd. 2016 31Consulting segment overviews

HR consulting buyers - Key findings

10-20% EBITDA

growth p.a.:

20-30% EBITDA

growth p.a.:

30-40% EBITDA

growth p.a.:

5.6x 6.6x 7.7x

note: Data reflects average results.

Acquisition activity: Target valuation metrics:

Minimum acceptable KPIs: Targeted deal structures:

3.3

9% 47%

42%

17%

$49m

$240k 36%

70%

2.9 yEARS

13%

No. of acquisitions expected to be made

in next 2-3 years

Rev. Growth

Upfront

Gross Margin

Fixed Deferred

Average budget for acquisitions

Rev. per employee

Deferred Earn-out

Utilization rate

Earn-out period

Equity ownership of key management

Adjusted EBITDA Multiples for consistent 20% adjusted EBITDA margin opportunities

at the following growth rates:

The 2016 Buyers Reaserch Report32 Section Heading

The section heading goes here like this if needed.

Insight 1Buyers’ expectations over the next three years

© Equiteq Ltd. 2016 33Section Heading

Marc Jantzen, Performance Improvement Consultancy.

Sold.

The Buyers Research Report34 Buyer evaluation, valuation insights, deal structuring & investment appraisal

notable variations occur in how consulting sector buyers approach the evaluation of an acquisition opportunity.

As we did last year, we asked buyers about their approach for assessing and evaluating deals. Although, this approach will be unique to each buyer, there are interesting trends evident amongst respondents within a given buyer group. Across survey respondents only 24% used a balanced scorecard of qualitative and quantitative measures.

Approximately 70% of PE respondents emphasize the use of quantitative measures when evaluating an acquisition opportunity. This is materially higher than the results for trade buyers that we surveyed. For some strategic acquirers there will be a natural evaluation of qualitative aspects of an opportunity that aren’t relevant to a PE. These will include confirming the validity of expected cross-selling opportunities with new clients, the potential scalability of tools and methodologies across a larger organization and the cultural fit of people within their organization.

A strong understanding of the different measures used to evaluate a consulting opportunity can help to better position a seller’s consulting business with a buyer.

note: The chart is a stacked bar chart showing proportionate results with respect to answers from each buyer group on whether they use quantitative versus qualitative measures to evaluate an initial acquisition opportunity.

Figure 10: Blend of qualitative versus quantitative metrics used to evaluate acquisition opportunities

Only quantitative

Mostly quantitative

Both equally

Mostly qualitative

Only qualitative

100%

80%

60%

40%

20%

0%

20

20

53

7

IT consulting

27

13

50

10

Engineering

20

32

4

36

8

Media & Marketing

32

20

4

4

40

Management consulting

20

45

5

30

Human Resources

60

25

9

10

Private Equity

Buyer evaluation, valuation insights, deal structuring & investment appraisal

Buyer evaluation of acquisition opportunities & minimum acceptable KPIs

© Equiteq Ltd. 2016 35Buyer evaluation, valuation insights, deal structuring & investment appraisal

Profit margins and EBITDA growth continue to be the most important financial attributes of a consulting opportunity in the eyes of a buyer.

In line with last year, profit margins and EBITDA growth are the most important quantitative metrics evaluated across buyers. These metrics are typically considered important reflections of the positioning and strength of an acquisition opportunity. Consultancies which position themselves as premium consulting offerings, typically use their reputation, market position, IP and the quality of their client relationships to command premium fees reflected in their adjusted residual profit margins. Buyers will also expect that businesses with growing market demand and unique scalable IP, will see this through the growth of the consulting company’s EBITDA.

Trends amongst strategic acquirer buyer groups were similar, however PE respondents placed a greater emphasis on revenue growth than trade buyers. This may reflect the views of investment firms that specialize in enabling margin improvements amongst businesses with stagnant or falling profitability.

During a sale process, buyers will spend time scrutinizing budgeted financials and comparing forecast financials against booked work. Sellers should ensure that their financials are comprehensively reviewed before presenting them to a buyer.

Figure 11: Equiteq proprietary weighted scoring of importance of quantitative metrics across buyers

note: Each buyer was asked to rank the quantitative metrics they considered important for an acquisition opportunity. See page 51 for further detail on scoring methodology.

0

10

5

20

15

30

25

40

45

35

Strategic acquirers Private equity

Gross / EBITDA margin

EBITDA growth

Revenue growth

Revenue per director

Revenue per employee

Utilization

Staff leverage

3741

2933

15

23

7

14

14

231

The Buyers Research Report36 Buyer evaluation, valuation insights, deal structuring & investment appraisal

Stronger KPIs are targeted by private equity and trade buyers operating in acquisitive segments.

We often observe that during a sales process, buyers will continually monitor KPIs and consider them a leading indicator as to whether a seller’s business is being well managed. Our exclusive analysis of KPIs considers specific minimum acceptable values of various KPIs used by buyers in assessing a consulting opportunity. An acceptable KPI will vary by buyer and the given acquisition opportunity. Nevertheless, we expect that our findings will be useful benchmarks to review a seller’s performance within the lens of a buyer.

The targeting of higher minimum acceptable KPIs amongst PE respondents is likely to be a reflection of the nature of the investment opportunities that this buyer group typically target. As we discussed, these often are premium consulting offerings that are underpinned by leveragable IP and focused on hot segments of the market. In practice, PE are not strongly guided by rigidly filtering opportunities according to KPIs. Instead, this buyer group typically attributes importance to absolute EBITDA growth, combined with the perceived ability to exit an investment to a strategic buyer in 3 to 5 years.

Minimum acceptable KPIs for IT consulting and Media buyer respondents are also slightly higher than other strategic buyer groups. We expect this to reflect the demand amongst buyers in these segments for opportunities focused on cutting-edge capabilities.

Table 3: Average acceptable minimum KPIs by strategic buyer group

note: Figures in the table show average results with respect to the minimum acceptable key performance indicators (KPIs) for opportunities to be considered as potential acquisitions by survey participants.

IT consulting

Engineeringconsulting

Media consulting

Management consulting

HR consulting

Private equity Overall

Revenue growth 13% 10% 12% 11% 9% 14% 12%

Gross margin 45% 43% 50% 41% 42% 52% 45%

Revenue per employee ($k) 280 250 305 270 240 370 280

Utilization rate 62% 67% 66% 65% 70% 71% 66%

© Equiteq Ltd. 2016 37Buyer evaluation, valuation insights, deal structuring & investment appraisal

Client base and intellectual property continue to be important qualitative aspects of a consulting sector acquisition opportunity.

We frequently observe that buyers look closely at a seller’s client list for blue-chip names with profitable and repeat business. Equally, buyers will want to see that client concentration is diversified and a seller’s business isn’t relying on just one client for most of its revenue.

IP that externalizes a consulting company’s expertise is also perceived as reducing some of the risk relating to the loss of key people. IP is also an important source of synergies if it can be scaled effectively across an organization or developed to provide a complementary revenue stream to the consulting offering.

PE respondents consider IP as a more important attribute of a consulting opportunity than trade buyers. As discussed earlier, PE typically look for opportunities with strong barriers to entry maintained by proprietary expertise which is retained and leveraged through their IP.

Figure 12: Equiteq proprietary weighted scoring of importance of qualitative metrics across buyers – 2015 versus 2016

Figure 13: Equiteq proprietary weighted scoring of importance of qualitative metrics comparing private equity with strategic acquirers

0

0

5

5

10

10

15

15

20

20

25

25

30

30

35

40

Size & quality of client base

Size & quality of client base

Potentially leveragable IP

Potentially leveragable IP

Quality / experience of management

Quality / experience of management

Future growth strategy / direction

Future growth strategy / direction

Uniqueness of market

proposition

Uniqueness of market

proposition

2015

2016

Private equity

Strategic acquirers

27

28

24

36

15

4

17

8

16

23

26

26

25

24

13

15

17

18

19

18

note: Each buyer was asked to rank the qualitative attributes they considered important for an acquisition opportunity. See page 51 for further detail on scoring methodology.

The Buyers Research Report38 Buyer evaluation, valuation insights, deal structuring & investment appraisal

Intellectual property related to thought leadership and benchmarking data has gained increasing importance since last year.

Although IP remains an important consideration amongst buyers, we are frequently told by acquirers that they consider it unclear as to how a target company’s non-registrable IP contributes to the success of their business. This highlights the importance of properly articulating the value of a seller’s IP to their value proposition, whilst considering what aspects will be of value to a buyer.

Figure 14: Equiteq proprietary weighted scoring of four types of intellectual property across buyers – 2015 versus 2016

Figure 15: Equiteq proprietary weighted scoring of four types of intellectual property comparing private equity with strategic acquirers

0

0

10

10

20

20

30

30

40

40

Software

Software

Methodologies

Methodologies

Publications

Publications

Benchmarking

Benchmarking

2015

2016

Private equity

Strategic acquirers

32

36

29

29

22

26

17

10

30

29

28

28

24

24

19

20

note: The bar charts shows a weighted score for each type of IP based on responses with respect to rankings of the most important types of intellectual property. See page 51 for further detail on scoring methodology.

The results of this year’s survey show that software and proprietary methodologies continue to be the most important IP across buyers. Financial buyers like PE rank software and revenue generating IP as particularly important, given its potential to drive rapid EBITDA growth as a complementary revenue stream with limited variable costs.

We also note strong demand for benchmarking databases across strategic buyer survey participants. This may highlight acquisitive demand in buyers who are developing advanced analytics capabilities and aiming to achieve substantial value from certain proprietary datasets relevant to their client’s industries.

Management consulting

IT consulting

HR consulting

Media consulting

Engineering consulting

Private equity Overall

10-20% EBITDA growth p.a.

20-30% EBITDA growth p.a.

30-40% EBITDA growth p.a.

© Equiteq Ltd. 2016 39Buyer evaluation, valuation insights, deal structuring & investment appraisal

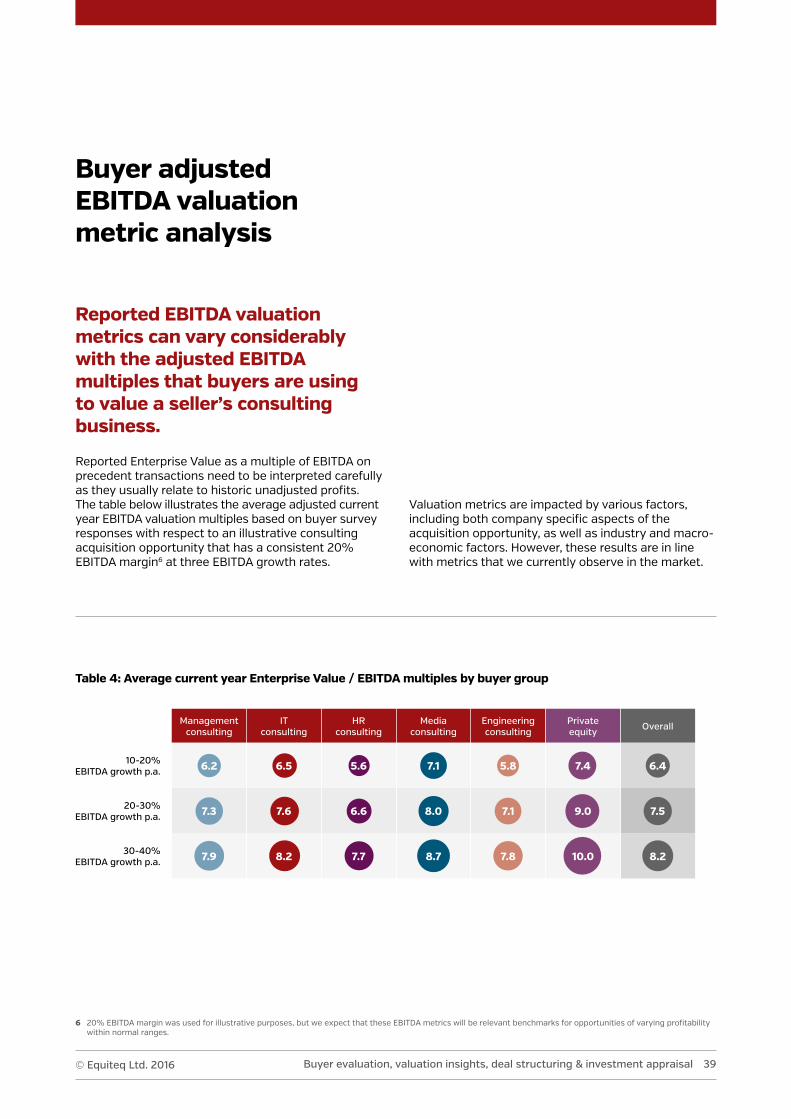

Buyer adjusted EBITDA valuation metric analysis

Reported EBITDA valuation metrics can vary considerably with the adjusted EBITDA multiples that buyers are using to value a seller’s consulting business.

Reported Enterprise Value as a multiple of EBITDA on precedent transactions need to be interpreted carefully as they usually relate to historic unadjusted profits. The table below illustrates the average adjusted current year EBITDA valuation multiples based on buyer survey responses with respect to an illustrative consulting acquisition opportunity that has a consistent 20% EBITDA margin6 at three EBITDA growth rates.

Valuation metrics are impacted by various factors, including both company specific aspects of the acquisition opportunity, as well as industry and macro-economic factors. However, these results are in line with metrics that we currently observe in the market.

6 20% EBITDA margin was used for illustrative purposes, but we expect that these EBITDA metrics will be relevant benchmarks for opportunities of varying profitability within normal ranges.

Table 4: Average current year Enterprise Value / EBITDA multiples by buyer group

10-20% EBITDA growth p.a. 6.2 6.5 5.6 7.1 5.8 7.4 6.4

20-30% EBITDA growth p.a. 7.3 7.6 6.6 8.0 7.1 9.0 7.5

30-40% EBITDA growth p.a. 7.9 8.2 7.7 8.7 7.8 10.0 8.2

The Buyers Research Report40 Buyer evaluation, valuation insights, deal structuring & investment appraisal

on average across our survey participants, private equity investors are prepared to pay higher prices than strategic buyers.

Although PE buyers cannot extract the revenue synergies available to strategic buyers when investing in a new platform, they often have a more rapid value creation plan than most strategic buyers, which can enable them to be more competitive on pricing for the deals they really want to do. These value creation plans may entail a business transformation or a buy-and-build acquisition program which can create the opportunity for substantial returns over the life of the investment. PE can also pay higher prices by utilizing debt financing to boost equity returns. This is especially the case with larger consulting businesses and those with recurring or repeat revenues.

Commercial rationales aside, the PE market is structurally hard wired to invest and there is a lot of capital looking for a home. While remaining highly selective, this weight of capital drives up the value of businesses attractive to financial investors. In addition, PE fund commitments usually terminate after 5 years and this can create significant pressure to deploy capital towards the end of this period and from time-to-time a willingness to stretch the valuation case.

Naturally across buyer groups the trends of our survey also belies a wider range of valuation metrics across individual buyers. We observe that strategic buyers that pay premium multiples for unique consulting businesses often do so because the seller provides value to them above the standalone value of the target. The value premium is therefore often the result of a proportion of the synergy value being shared with the seller. This observation further highlights the importance of positioning the value of a seller’s consulting business within the lens of a prospective buyer.

note: Horizontal stacked bar chart show proportionate range of valuation responses across survey participants.

Figure 16: Range of EV/EBITDA valuation multiple responses by buyer group for an illustrative opportunity with an EBITDA growth of 10-20% per annum

Engineering consulting

IT consulting

Media

Management consulting

HR consulting

Private equity

0 30 40 50 60 70 80 90 10010 20

Less than 5x

5-6x

6-7x

7-8x

8-9x

9-10x

More than 10x

9

31

14

10

20

12

27

25

32

36

23

45

31

27

38

32

35

18

13

9

5

18

1910 19

8 4

31215

© Equiteq Ltd. 2016 41Buyer evaluation, valuation insights, deal structuring & investment appraisal

A positive correlation occurs between acquisition expectations, KPI targets and EBITDA multiple valuation targets by buyer group.

note: Figures in the graph utilize average results for each buyer group. Size of bubbles reflect the average number of expected acquisitions amongst each buyer group. Valuation metrics based on an opportunity with a 20-30% EBITDA growth rate.

Figure 17: Correlation analyses of selected KPIs and adjusted EBITDA valuation metrics

0%

0

0%

5%

100

10%

10%

200

20%

15%

300

30%

20%

500

400

70%

40%

50%

60%

Revenue Growth vs EBITDA Multiple

Revenue per Employee vs EBITDA Multiple

Gross Margin vs EBITDA Multiple

EBITDA Multiple (Avg)

EBITDA Multiple (Avg)

EBITDA Multiple (Avg)

Rev

enue

Gro

wth

Rev

enue

per

em

ploy

ee ($

k)G

ross

Mar

gin

IT

Engineering

Media & Marketing

Management consulting

HR

Private Equity

5.0

5.0

5.0

6.5

6.5

6.5

7.0

7.0

7.0

7.5

7.5

7.5

8.0

8.0

8.0

8.5

8.5

8.5

9.0

9.0

9.0

9.5

9.5

9.5

5.5

5.5

5.5

6.0

6.0

6.0

As discussed, we would expect a unique and attractive consulting acquisition opportunity to reflect stronger KPIs. These opportunities will also experience stronger demand and competition amongst buyers, driving up valuations.

The Buyers Research Report42 Buyer evaluation, valuation insights, deal structuring & investment appraisal

During competitive situations, buyers will typically alter the deal structure and offer more favorable terms for sellers.

Due to the strong appetite amongst acquirers and a limited number of new unique opportunities being brought to market, we typically observe competitive negotiations for attractive consulting businesses. In these situations, deal structures are typically altered before the overall price. This can result in higher upfront payments, a shorter earn-out period and ‘contingent payouts’ being converted to ‘fixed deferred payouts’.

Recent reported empirical data on deal structures in the consulting market7 showed that 60% of the deal price for a consulting firm was typically paid upfront. This discrepancy with the findings of our survey, suggests a competitive seller’s market for consulting companies, with buyers paying more upfront than they would ideally like.

Buyer approach to deal structuring & earn-outs

The deal structures targeted by survey participants remains broadly in line with the results of last year’s survey and earn-outs continue to remain crucial.

A consulting acquisition can be structured in a variety of ways, but typically involves some mixture of upfront cash element, fixed deferred cash and an earn-out offering additional compensation in the future if the business achieves certain financial goals.

The results of our survey suggest that around 45% of consideration is typically offered up-front. Respondents highlight that an earn-out is considered crucial to retain key people and normally lasts around 3 years.

7 The Global Consulting M&A Report 2016, our proprietary analysis of the current state of the consulting M&A market.

note: Chart show average targeted deal structure component proportions for each buyer group surveyed.

Figure 18: Average target deal structure for each buyer group

IT consulting

Management consulting

HR consulting

Media consulting

Engineering consulting

Overall

0 30 40 50 60 70 80 90 10010 20

Upfront

Fixed deferred

Deferred earn-out

44

41

38

47

47

42

22

18

21

37

38

40

3617

14 39

4612

© Equiteq Ltd. 2016 43Buyer evaluation, valuation insights, deal structuring & investment appraisal

Surveyed buyers across industries typically like to see wider management share ownership of at least 12% to 16%.

People are of course the resource that drives the most value in a knowledge-intensive services business. Therefore, most buyers will want to see management quality and cohesion before acquiring a consulting business, as well as loyalty of valuable employees after the deal is closed. The most common mechanism to achieve alignment is for major shareholders to dilute equity and award shares selectively to senior managers.

In line with last year, earn-outs are typically linked with profit.

The key metrics used for earn-outs are gross margin and revenue as these are less affected by integration plans.

Integration is less of an issue for financial buyers that typically maintain acquisitions on a standalone basis and can therefore hold the seller accountable for costs below the gross profit line. As such, PE that we surveyed typically link earn-outs with EBITDA, or seek to de-risk by having vendors roll-over a proportion of proceeds and remain invested.

note: See page 51 for further detail on scoring methodology.

Figure 19: Equiteq proprietary weighted scoring of targets used by buyers to base their earn-outs

0

5

30

10

35

15

40

25

45

20

Gross margin Revenue Rol Retention of key personnel

EBITDA

2014

2015

2016

42 4338

22

1916

14 15 1512 1010 1213

18

note: The heat map uses a weighted score for each investment appraisal method based on responses with respect to rankings of the most important types used by buyers. See page 51 for further detail on scoring methodology.

The Buyers Research Report44 Buyer evaluation, valuation insights, deal structuring & investment appraisal

The use of nPV analysis is preferred amongst strategic buyers, whilst equity IRR analyses are typically used by private equity.

The most important investment appraisal method highlighted across buyers which we surveyed is NPV and IRR analysis. The key difference between both methods is that IRR uses one single discount rate to evaluate every investment. NPV is therefore important for acquirers who are able to discount riskier projected cash flows, such as revenue synergies, at a higher rate to more certain cash flows, such as those expected to be achieved from cost synergies. Trade buyer respondents therefore typically prefer the use of NPV analysis, given that they will typically achieve revenue synergies from integrating an acquisition. These synergies can therefore be discounted at a higher rate in comparison to more certain cashflows to create a more refined investment analysis.

Figure 20: Equiteq proprietary ranking of investment appraisal methods by buyer group

Buyer approach to investment appraisal

As part of a buyer’s assessment of a consulting firm investment, various investment appraisal methods are used at different stages in an acquisition process.

Investment appraisals typically take into account the cost of an investment netted against projected pre-tax cash flows adjusted for the time value of money, which consider expected cost and revenue synergies enabled from an acquisition. The outputs of investment appraisals are important for buyers at various stages in a deal. They will normally be used by a deal sponsor and a buyer’s corporate development team to consider the appropriate purchase price for an acquisition. The deal sponsor and the executive board of the buyer will also review the investment appraisal outputs up to completion and as part of any post-completion review of the investment.

High (score: 25+)

Medium (score: 19-24)

Low (score: 18 or less)

Investment appraisal method

NPV IRR Payback period Rol ROCE

Managementconsulting

IT consulting

HR consulting

Media

Engineering consulting

Private equity

overall

Buy

er g

roup

© Equiteq Ltd. 2016 45Buyer evaluation, valuation insights, deal structuring & investment appraisal

On the other hand a PE buyer is typically unable to achieve revenue synergies from integration. IRR analysis is also the common methodology for measuring a PE’s overall fund performance for the benefit of its investors. An IRR on an investment will therefore typically be modelled with the expectation that it should match or outperform the targeted return for the fund.

The average target equity IRR for surveyed private equity buyers is around 31%.

Corporate buyers and PE that we surveyed reported very similar IRR targets. That PE respondents are willing to pay higher prices and achieve similar IRRs is likely reconciled by using more acquisition debt finance.

The returns for a consulting acquisition will typically be influenced by a variety of factors including specific buyer objectives and risk appetite, as well as industry and macro-economic factors. Nonetheless, we observe a positive correlation between target KPIs, equity IRRs and valuation metric targets across buyer groups.

Investment appraisal method definitions:

net Present Value (nPV): The present value of the difference between the sum of the cash inflows and cash outflows for a given investment.

Equity Internal Rate of Return (Equity IRR): A discount rate that when applied to the cash flows to equity from a specific investment, makes the NPV equal to zero.

Payback Period: The length of time required for an investment’s profits to cover the cost of the initial cash outlay.

Return on Investment (RoI): The net benefit of an investment relative to the initial investment outlay,

Return on Capital Employed (RoCE): The net benefit of an investment relative to the capital employed.

The 2016 Buyers Reaserch Report46 Section Heading

The section heading goes here like this if needed.

Insight 1Buyers’ expectations over the next three years

© Equiteq Ltd. 2016 47Section Heading

The Buyers Research Report48 Conclusion

ConclusionThe results of our survey suggests a market dynamic, which supports strong buyer demand and valuations for unique consulting sector acquisition opportunities.

Potential for premium

valuations for unique consulting

opportunities

Buyers continue to have

substantial budgets for

new consulting acquisitions.