hossein abdoh tabrizi maysam radpour june 2011. table of contents bonds; risk & return tradeoff...

TRANSCRIPT

DURATION & CONVEXITY

Hossein Abdoh TabriziMaysam Radpour

June 2011

Table of Contents

• Bonds; risk & return tradeoff

• Maturity effect; interest rate volatility risk

• Duration

• Convexity

Risk & return tradeoff

Bonds

Types of bonds based on option granted to the issuer or bondholder

Without option

Option-free bonds

Option for issuer

Callable bonds

Option for bondholder

Putable bonds

Factors effect bond return

Who is the Issuer?• issuer

How long does it take to mature?• Maturity

How easy may it be traded?• liquidity

How much is reinvestment rate of return?• Reinvestment rate

How much is tax?• Tax

Risks of return

• Default risk

Does the issuer do it’s obligations?

• Interest rate volatility risk

How much is the interest rate volatile?

• Reinvestment risk

What is the rate of periodical payments return?

• Liquidity risk

Is there an active secondary market?

Interest rate volatility risk

Maturity Effects

Price volatility in option-free bonds

There is a reverse

relationship

between yield

to maturity and

price .

Price

Yield to maturity

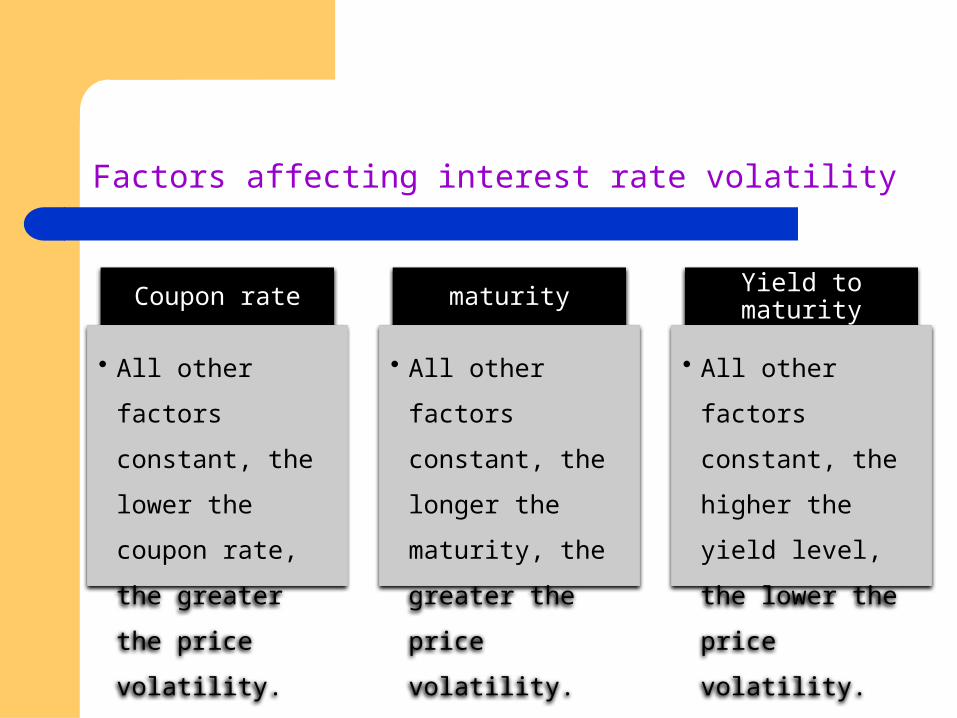

Factors affecting interest rate volatility

Coupon rate

• All other factors

constant, the lower

the coupon rate,

the greater the

price volatility.

maturity

• All other factors

constant, the

longer the maturity,

the greater the

price volatility.

Yield to maturity

• All other factors

constant, the

higher the yield

level, the lower the

price volatility.

Percentage price change for Four Hypothetical BondsInitial yield for all four bonds is 6%

Percentage price change

9% 20-year 9% 5-year 6% 20-year 6% 5-year New yield

25.04 8.57 27.36 8.98 4.00%11.53 4.17 12.55 4.38 5.00%5.54 2.06 6.02 2.16 5.50%1.07 0.41 1.17 0.43 5.90%0.11 0.04 0.12 0.04 5.99%-0.11 -0.04 -0.12 -0.04 6.01%-1.06 -0.41 -1.15 -0.43 6.10%-5.13 -2.01 -5.55 -2.11 6.50%-9.89 -3.97 -10.68 -4.16 7.00%

-18.40 -7.75 -19.79 8.11 8.00%

Duration

Duration is a measure of interest rate volatility risk:

• Duration is the measure of fixed income securities price sensitivity versus interest rate changes.

• Duration encompasses the three factors (coupon, maturity and yield level) that affects bond’s price volatility.

Duration

Duration is a proxy for maturity:

• Duration is a proxy better than maturity and may be considered as effective maturity of fixed income securities.

• Duration is standardized weighted average of bond’s term to maturity where the weights are the present value of the cash flows.

Duration is elasticity

Duration is a proxy that shows bond’s

percentage price change when yield

changes.

y

PP

dy

PdPdurationModified

Price equation of an option-free bond

P: priceC: periodical coupon interestY: yield to maturityM: maturity value (face value)N: number of periods

n21 )y1(

MC

)y1(

C

)y1(

CP

First derivative of price equation

The first derivative of price equation shows the approximate change in

price when small change in yield occurs.

n21 )y1(

)MC(n

)y1(

C2

)y1(

C1

)y1(

1

dy

dP

Macaulay duration, Modified duration

Perce

ntage

of

price

chang

e

Macau

lay

duratio

n

Modifi

ed

duratio

n

n21 )y1(

)MC(n

)y1(

C2

)y1(

C1

P

1

)y1(

1

P

1

dy

dP

n21 )y1(

)MC(n

)y1(

C2

)y1(

C1

P

1durationMacaulay

n21 )y1(

)MC(n

)y1(

C2

)y1(

C1

P

1

)y1(

1durationModified

Example 1: Duration calculation

Duration for a 9% 5-year bond selling to yield 6% with semiannual coupon payments and face value of 100$ is:

PV× t Present value Cash flow Period4.3689 4.3689 4.5 18.4834 4.2417 4.5 2

12.3544 4.1181 4.5 315.9928 3.9982 4.5 419.4087 3.8817 4.5 522.6121 3.7687 4.5 625.6124 3.6589 4.5 728.4187 3.5523 4.5 831.0399 3.4489 4.5 9

777.5781 77.7578 104.5 10945.8694 112.7953 Total

8.38 Macaulay duration (in half years)

4.19 Macaulay duration (in years)

4.07 Modified duration (in years)

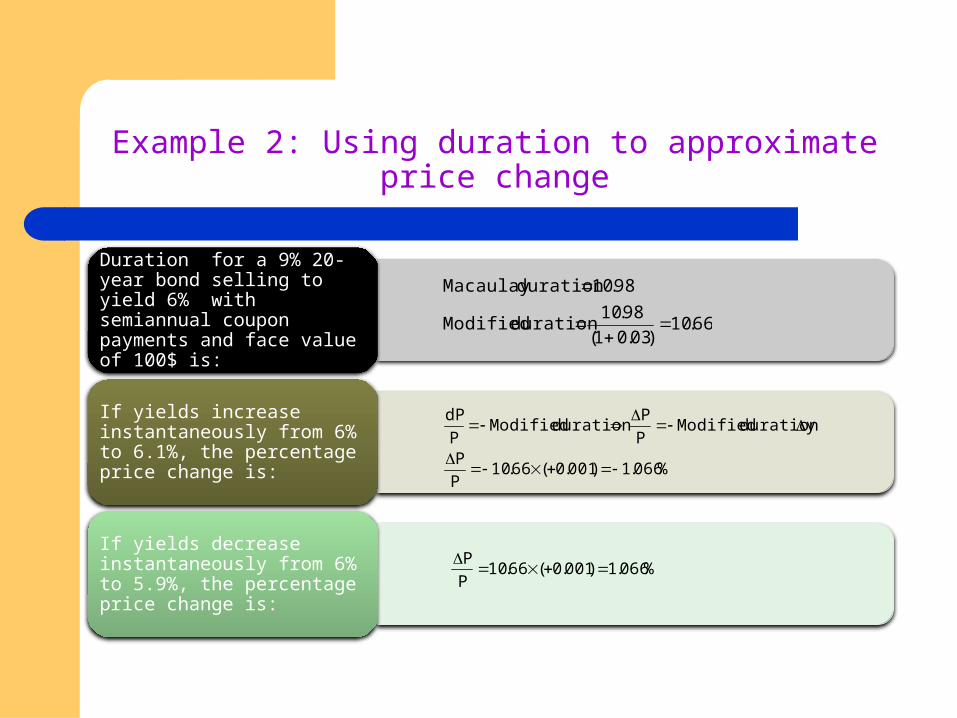

Example 2: Using duration to approximate price change

Duration for a 9% 20-year bond selling to yield 6% with semiannual coupon payments and face value of 100$ is:

If yields increase instantaneously from 6% to 6.1%, the percentage price change is:

If yields decrease instantaneously from 6% to 5.9%, the percentage price change is:

66.10)03.01(

98.10durationModified

98.10durationMacaulay

%066.1)001.0(66.10P

P

ydurationModifiedP

PdurationModified

P

dP

%066.1)001.0(66.10P

P

When duration does not work well?

When there are large movements in yield, duration is not adequate to approximate price reaction.

• Duration will overestimate the price change when the yield rises.

• Duration will underestimate the price change when the yield falls.

Example 3: When duration does not work well?

For the previous example, the real and approximate price change when yields change are as follows:

difference Approximate price change (based on duration)

Real price change (based on price equation)

Yield change (in percent)

0.06 -1.66 -1.60 0.10.04 +1.66 +1.70 -0.12.92 -21.32 -18.40 2.03.72 +221.32 +25.04 -2.0

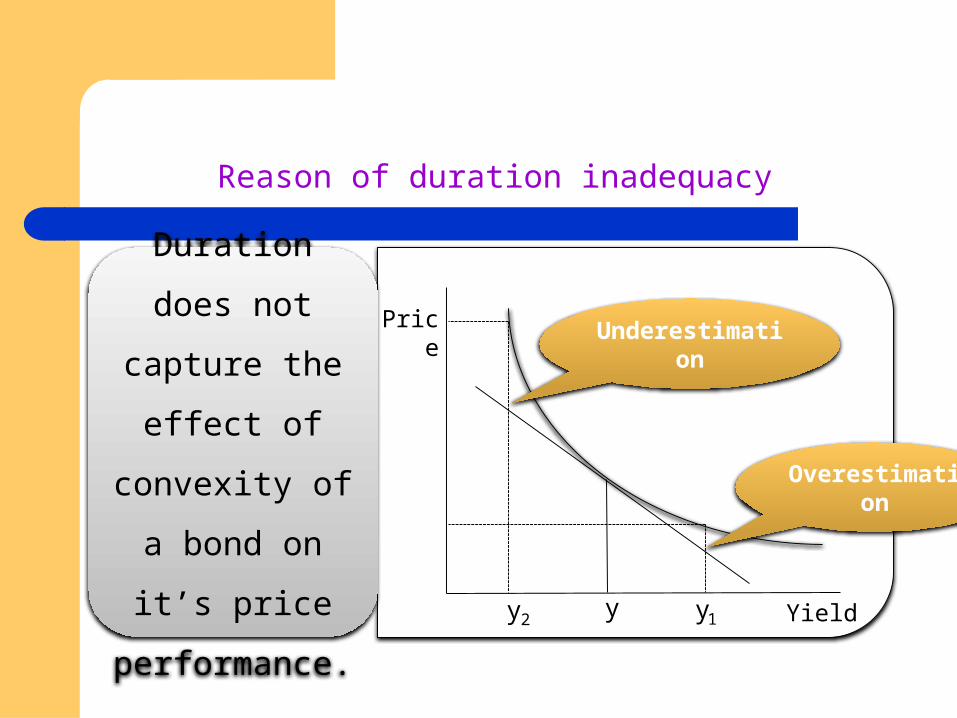

Reason of duration inadequacy

Duration does not

capture the effect of

convexity of a bond

on it’s price

performance.

Price

Yield

Underestimation

Overestimation

1y2y y

Improvement in price change approximation

Taylor series for price equation:

P

Error)dy(

P

1

dy

Pd

2

1dy

P

1

dy

dP

P

dP

ErrordyP

1

dy

Pd

2

1dy

dy

dPdP

22

2

2

2

Convexity calculation

Convexity is the second derivative of the price

equation divided by the price.

n212

2

2

)y1(

)MC)(1n(n

)y1(

C32

)y1(

C21

P

1

)y1(

1

2

1Convexity

P

1

dy

d

2

1Convexity

Example 4: convexity calculation

Convexity for a 9% 5-year bond selling to yield 6% with semiannual coupon payments and face value of 100$ is:

PV × t × (t+1) PV Cash flow Period

8.7378 4.3689 4.5 125.4502 4.2417 4.5 249.4172 4.1181 4.5 379.964 3.9982 4.5 4116.451 3.8817 4.5 5

158.2854 3.7687 4.5 6204.8984 3.6589 4.5 7255.7656 3.5523 4.5 8310.401 3.4489 4.5 9

8553.358 77.7578 104.5 10

9762.729 112.7953 Total

40.792 Convexity (in half years )

10.198 Convexity (in years)

Example 5: Using convexity to approximate price change

Convexity for a 9% 20-year bond selling to yield 6% with

semiannual coupon payments and face value of

100$ is:

If yields increase instantaneously from 6% to 8%, the percentage price

change is:

If yields decrease instantaneously from 6% to 4%, the percentage price

change is:

053.82Convexity

%28.3)02.0(053.82)y()Convexity(P

P 22

%28.3)02.0(053.82)y()Convexity(P

P 22

Using duration and convexity simultaneously

Estimated percentage

price change

)y(MD

2)y(C

Example 6: Comparing approximate price change using duration and convexity and real price change

For a 9% 20-year bond selling to yield 6% with semiannual coupon payments and face value of 100$ if yield changes two

percent then we have:

difference Approximate price change (based on convexity)

Real price change (based on price

equation)

Yield change (in percent)

-0.36 -18.04 -18.40 2

0.44 +24.60 +25.04 -2

THANKS