horticultural value chain development & financing strategies for zimbabwe's smallholder...

TRANSCRIPT

Horticultural Value Chain Development Financing Strategies for Smallholder Irrigation Communities

Lessons from ZimAIED AgriTrade Revolving Credit Facility

in Zimbabwe

RENETH MANO

[email protected]; [email protected]

Cell:0773056440

2

OUTLINE

1. Background and financial needs of Smallholder Sector

2. IRD Financial Project Experiences and Partners

3. IRD Smallholder Agric Value Chain Development Concept

4. ZIMAIED AGRITRADE RCF MODEL: Results & Experience

5. Financial Inclusion

6. AGRITRADE Direct Lending to Horticultural Farmers – Experiences & Challenges:

7. Conclusions and Policy Insights

3

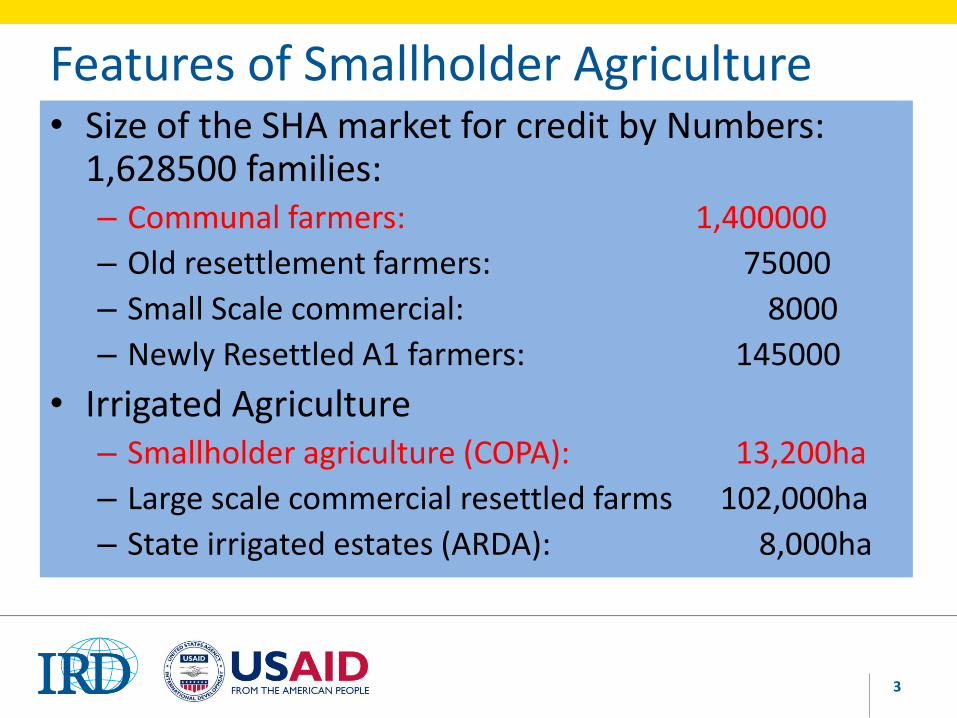

Features of Smallholder Agriculture • Size of the SHA market for credit by Numbers:

1,628500 families: – Communal farmers: 1,400000

– Old resettlement farmers: 75000

– Small Scale commercial: 8000

– Newly Resettled A1 farmers: 145000

• Irrigated Agriculture – Smallholder agriculture (COPA): 13,200ha

– Large scale commercial resettled farms 102,000ha

– State irrigated estates (ARDA): 8,000ha

4

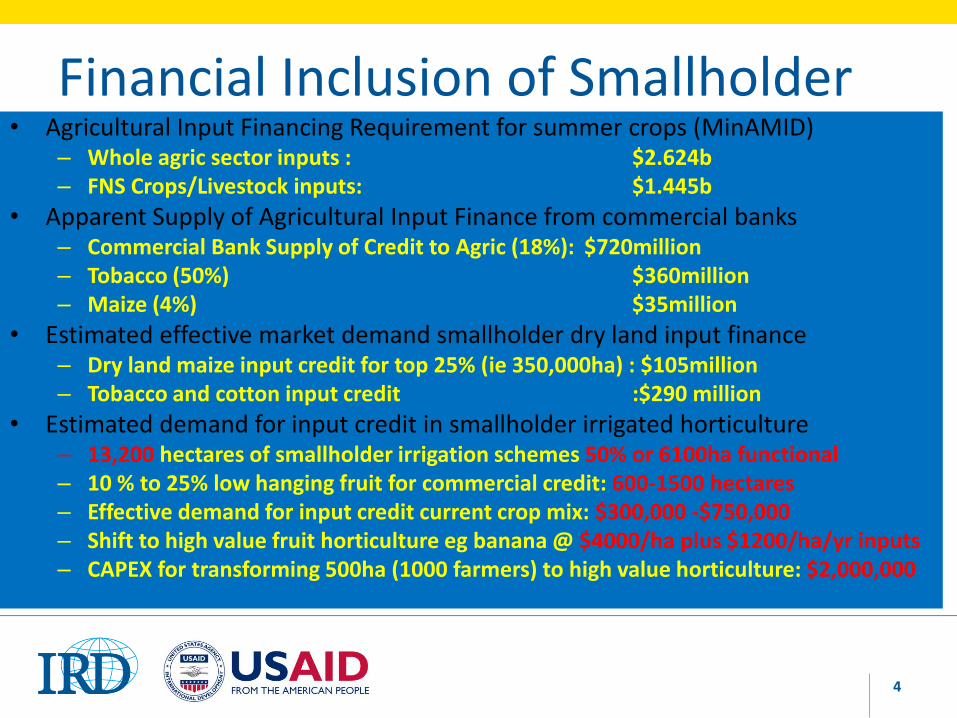

Financial Inclusion of Smallholder • Agricultural Input Financing Requirement for summer crops (MinAMID)

– Whole agric sector inputs : $2.624b – FNS Crops/Livestock inputs: $1.445b

• Apparent Supply of Agricultural Input Finance from commercial banks – Commercial Bank Supply of Credit to Agric (18%): $720million – Tobacco (50%) $360million – Maize (4%) $35million

• Estimated effective market demand smallholder dry land input finance – Dry land maize input credit for top 25% (ie 350,000ha) : $105million – Tobacco and cotton input credit :$290 million

• Estimated demand for input credit in smallholder irrigated horticulture – 13,200 hectares of smallholder irrigation schemes 50% or 6100ha functional – 10 % to 25% low hanging fruit for commercial credit: 600-1500 hectares – Effective demand for input credit current crop mix: $300,000 -$750,000 – Shift to high value fruit horticulture eg banana @ $4000/ha plus $1200/ha/yr inputs – CAPEX for transforming 500ha (1000 farmers) to high value horticulture: $2,000,000

5

IRD EXPERIENCES: PROJECT PARTNERS

• ZIMBABWE PROJECTS

REVALUE PROJECT

ZIMAIED AGRITRADE RCF

DAIRYFIN RCF

• REGIONAL PROJECTS

GHANA/MALI/SWAZILAND

• ZIMAIED AGRITRADE FUNDING PARTNER

–USAID • ZIMAIED AGRITRADE

Investment Partners

– 3 Commercial banks

– 1 state owned bank

– 5 MFI members of ZMWF

6

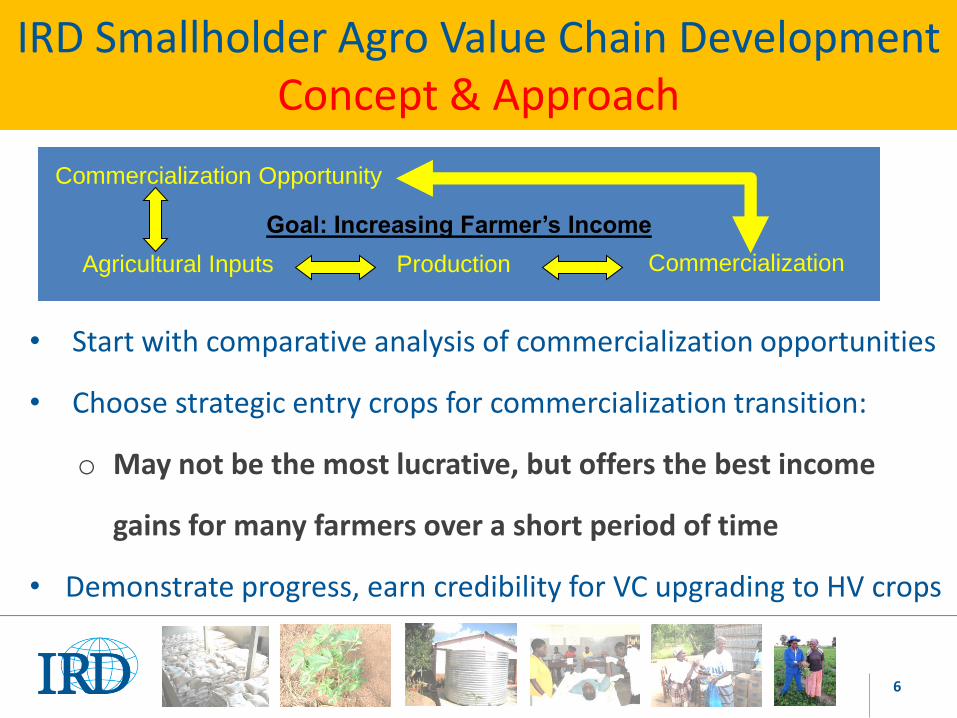

IRD Smallholder Agro Value Chain Development Concept & Approach

• Start with comparative analysis of commercialization opportunities

• Choose strategic entry crops for commercialization transition:

o May not be the most lucrative, but offers the best income

gains for many farmers over a short period of time

• Demonstrate progress, earn credibility for VC upgrading to HV crops

Goal: Increasing Farmer’s Income

Agricultural Inputs Production Commercialization

Commercialization Opportunity

7

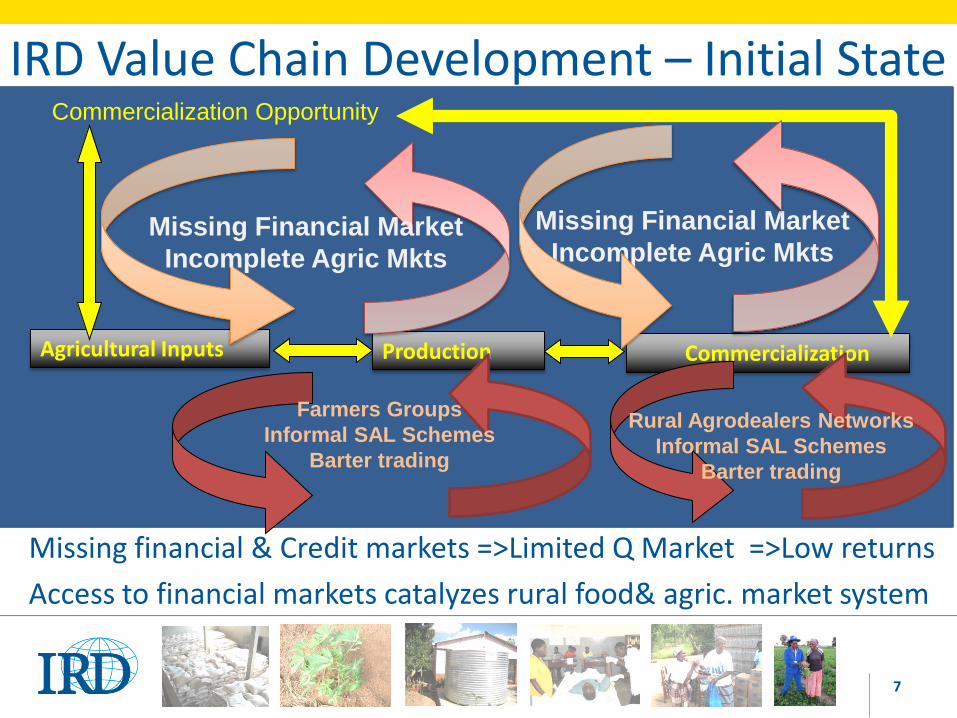

IRD Value Chain Development – Initial State

Agricultural Inputs Production Commercialization

Commercialization Opportunity

Missing Financial Market

Incomplete Agric Mkts

Missing financial & Credit markets =>Limited Q Market =>Low returns

Access to financial markets catalyzes rural food& agric. market system

Farmers Groups

Informal SAL Schemes

Barter trading

Rural Agrodealers Networks

Informal SAL Schemes

Barter trading

Missing Financial Market

Incomplete Agric Mkts

8

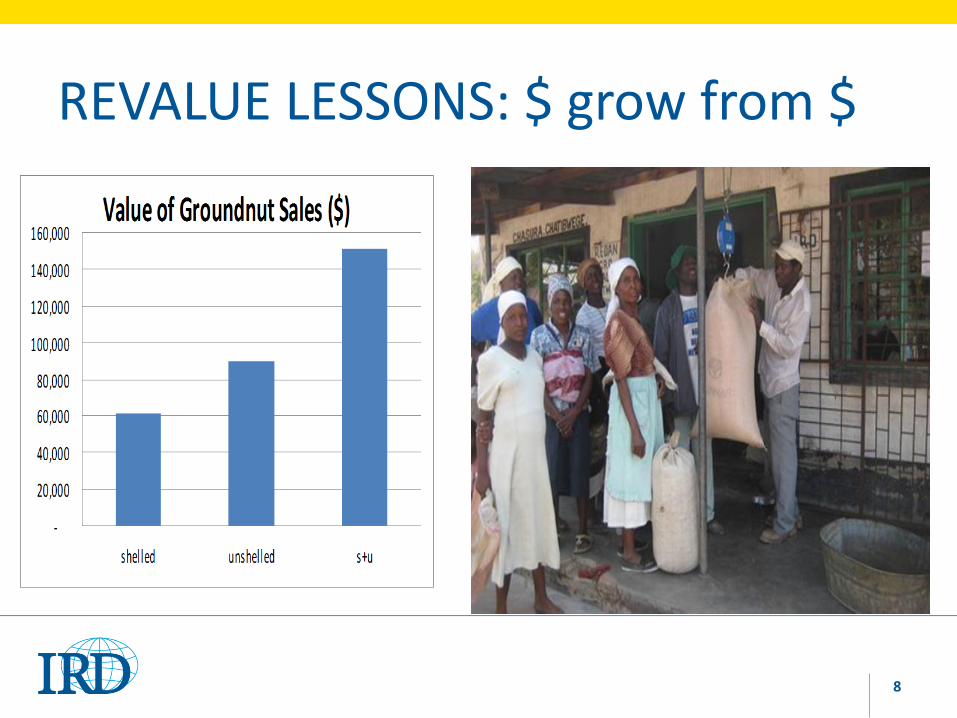

REVALUE LESSONS: $ grow from $

9

10

ZIMAIED AgriTrade Revolving Credit Facility

Experiences and Current Results

Credit for private agribusiness engagement

with

Smallholder farming communities

in

communal areas and irrigation schemes

11

AgriTrade Background: Year 2009-12

• Under-capitalized buyers of smallholder farmers’ produce

• De-capitalized financial institutions with limited access to deposits

• Food aid and free inputs programs driving farm decision

• No credit providers DIRECTLY LENDING to smallholder Limited

contract farming opportunities for SH irrigation farmers

• Smallholder horticultural farmers TRAPPED in low input-low value

partially market-driven farming system

12

AgriTrade Introduction What is AgriTrade? A commercial credit facility that provides liquidity for

agribusinesses working with smallholder farmers. What is financed? Agribusinesses working with smallholder farmers to:

- Buy produce - Sell agricultural inputs - Buy small processing equipment - Establish contract farming

Who is leading? Partner Financial Institutions.

13

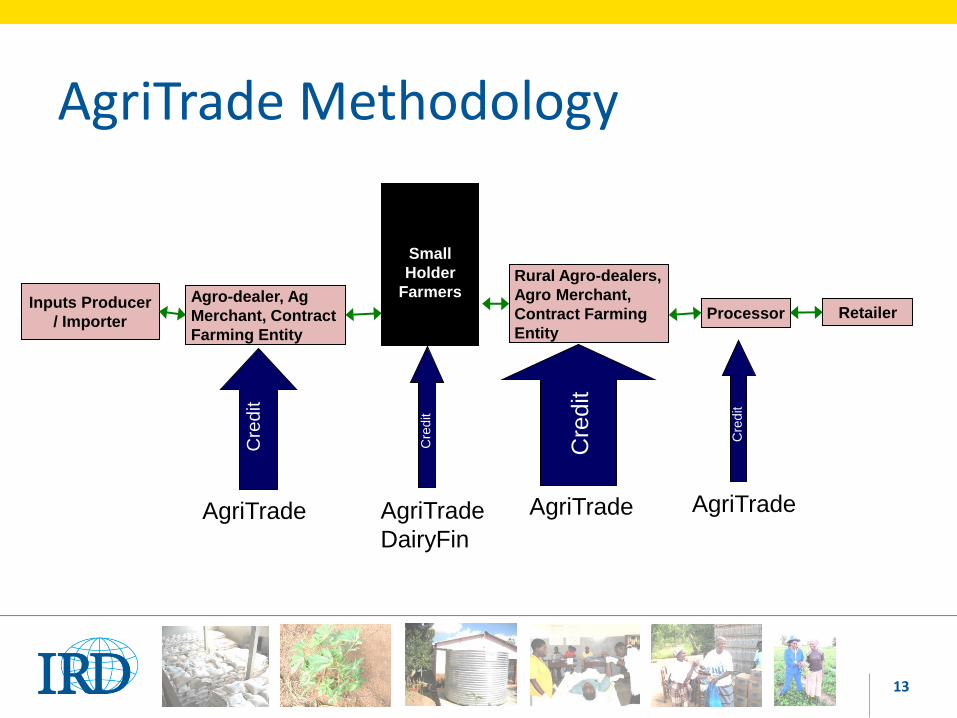

AgriTrade Methodology

Small

Holder

Farmers Rural Agro-dealers,

Agro Merchant,

Contract Farming

Entity

Processor Retailer Inputs Producer

/ Importer

Agro-dealer, Ag

Merchant, Contract

Farming Entity

AgriTrade

Cre

dit

AgriTrade

Cre

dit

AgriTrade

Cre

dit

AgriTrade

DairyFin

Cre

dit

14

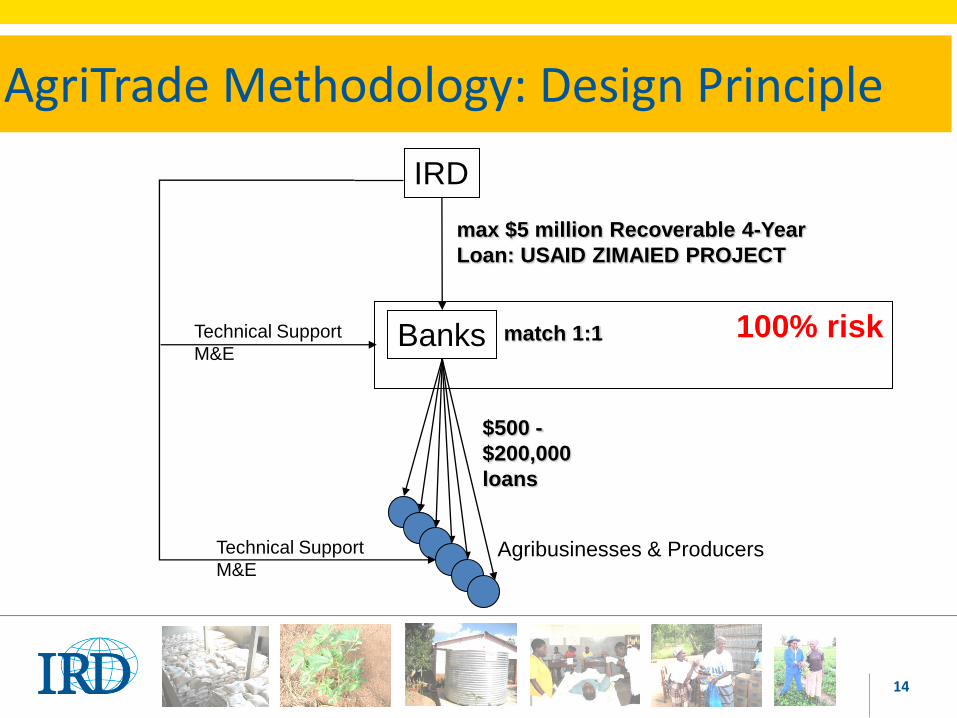

AgriTrade Methodology: Design Principle

IRD

Banks

max $5 million Recoverable 4-Year

Loan: USAID ZIMAIED PROJECT

match 1:1 100% risk

$500 -

$200,000

loans

Technical Support

M&E

Technical Support

M&E Agribusinesses & Producers

15

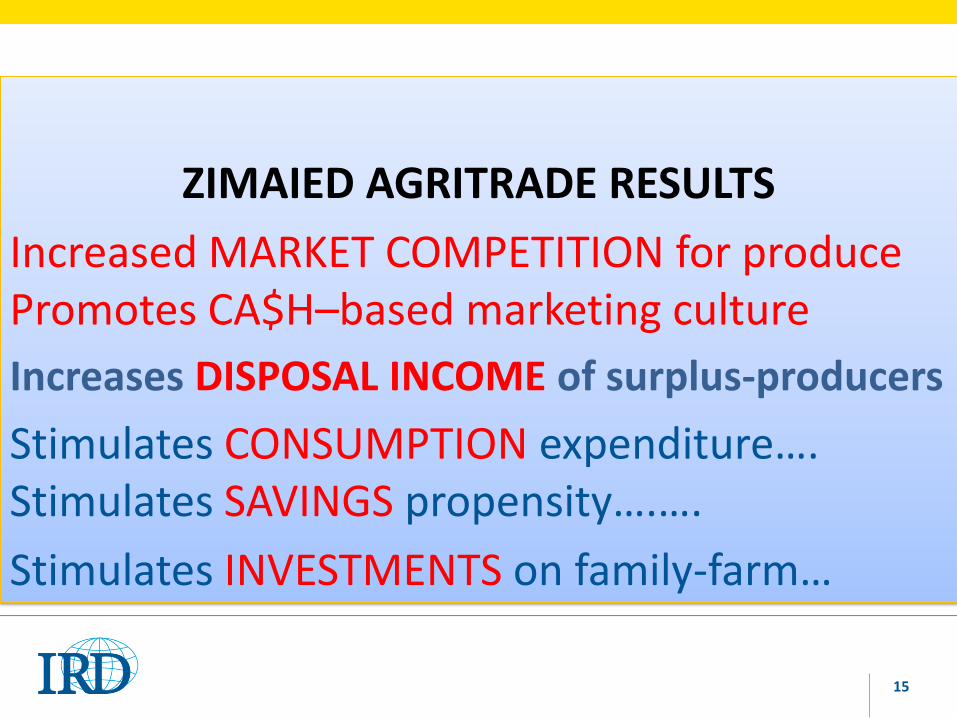

ZIMAIED AGRITRADE RESULTS

Increased MARKET COMPETITION for produce Promotes CA$H–based marketing culture

Increases DISPOSAL INCOME of surplus-producers

Stimulates CONSUMPTION expenditure…. Stimulates SAVINGS propensity….….

Stimulates INVESTMENTS on family-farm…

16

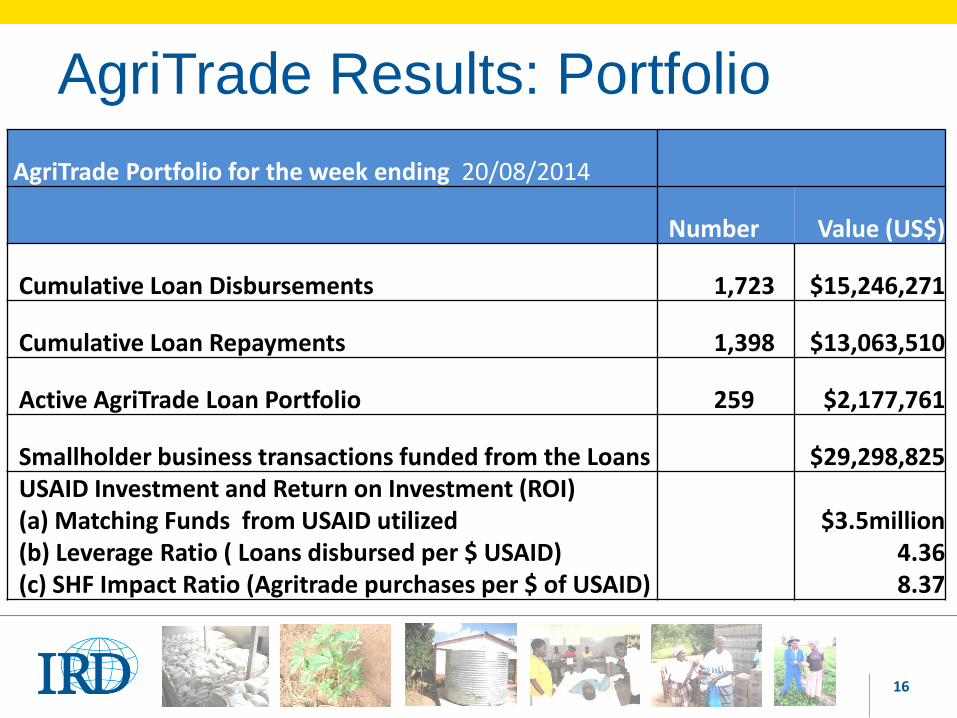

AgriTrade Results: Portfolio

AgriTrade Portfolio for the week ending 20/08/2014

Number Value (US$)

Cumulative Loan Disbursements 1,723 $15,246,271

Cumulative Loan Repayments 1,398 $13,063,510

Active AgriTrade Loan Portfolio 259 $2,177,761

Smallholder business transactions funded from the Loans $29,298,825 USAID Investment and Return on Investment (ROI) (a) Matching Funds from USAID utilized (b) Leverage Ratio ( Loans disbursed per $ USAID) (c) SHF Impact Ratio (Agritrade purchases per $ of USAID)

$3.5million 4.36 8.37

17

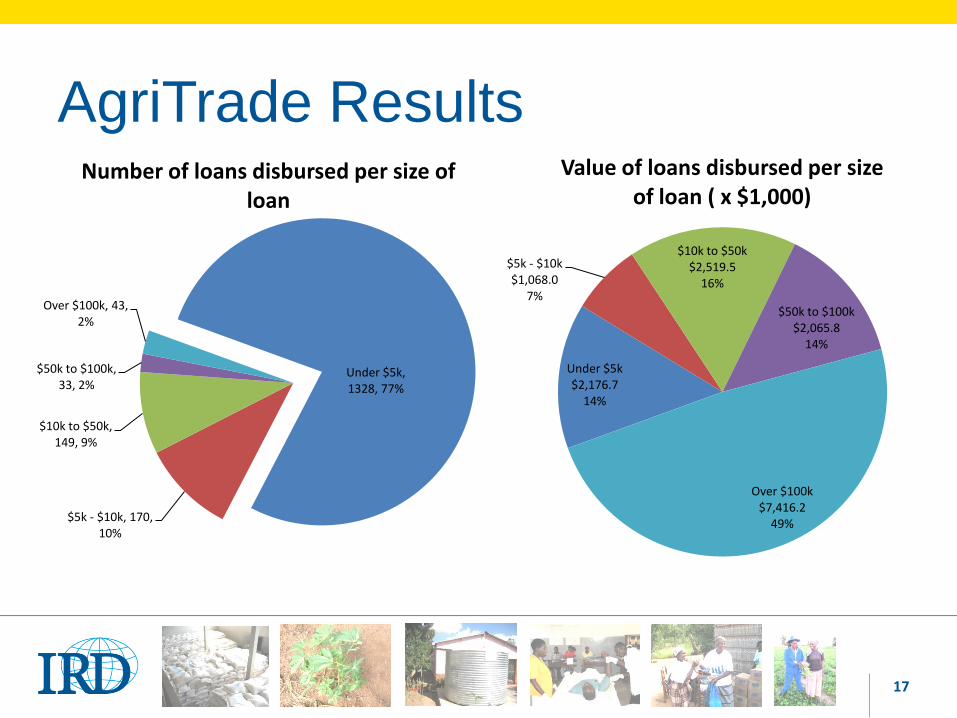

AgriTrade Results

Under $5k $2,176.7

14%

$5k - $10k $1,068.0

7%

$10k to $50k $2,519.5

16%

$50k to $100k $2,065.8

14%

Over $100k $7,416.2

49%

Value of loans disbursed per size of loan ( x $1,000)

Under $5k, 1328, 77%

$5k - $10k, 170, 10%

$10k to $50k, 149, 9%

$50k to $100k, 33, 2%

Over $100k, 43, 2%

Number of loans disbursed per size of loan

18

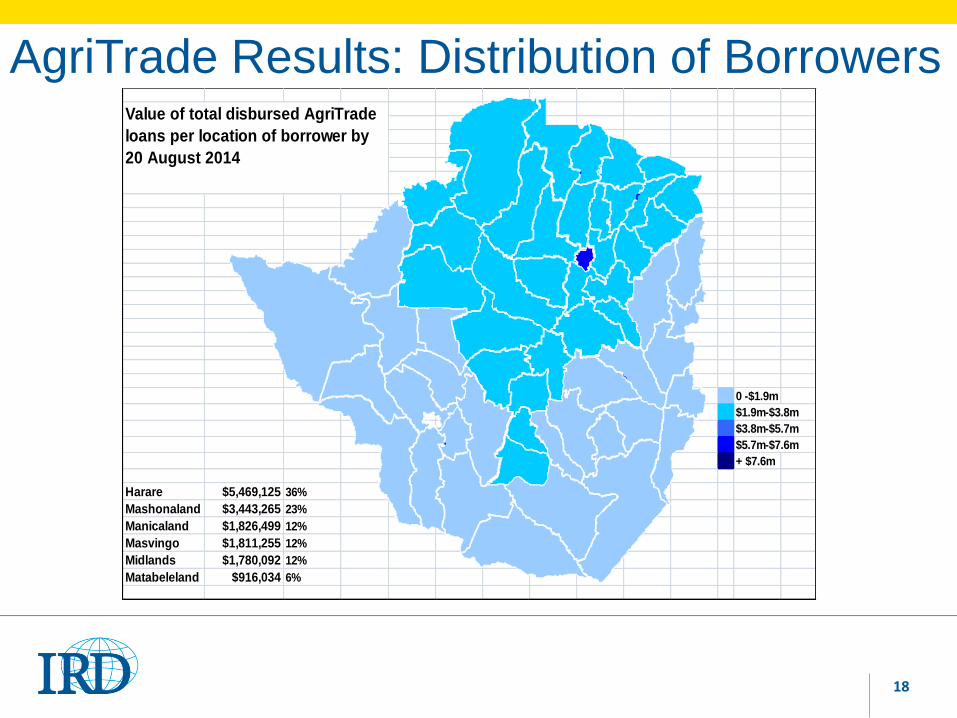

AgriTrade Results: Distribution of Borrowers

0 -$1.9m

$1.9m-$3.8m

$3.8m-$5.7m

$5.7m-$7.6m

+ $7.6m

Harare $5,469,125 36%

Mashonaland $3,443,265 23%

Manicaland $1,826,499 12%

Masvingo $1,811,255 12%

Midlands $1,780,092 12%

Matabeleland $916,034 6%

Value of total disbursed AgriTrade

loans per location of borrower by

20 August 2014

19

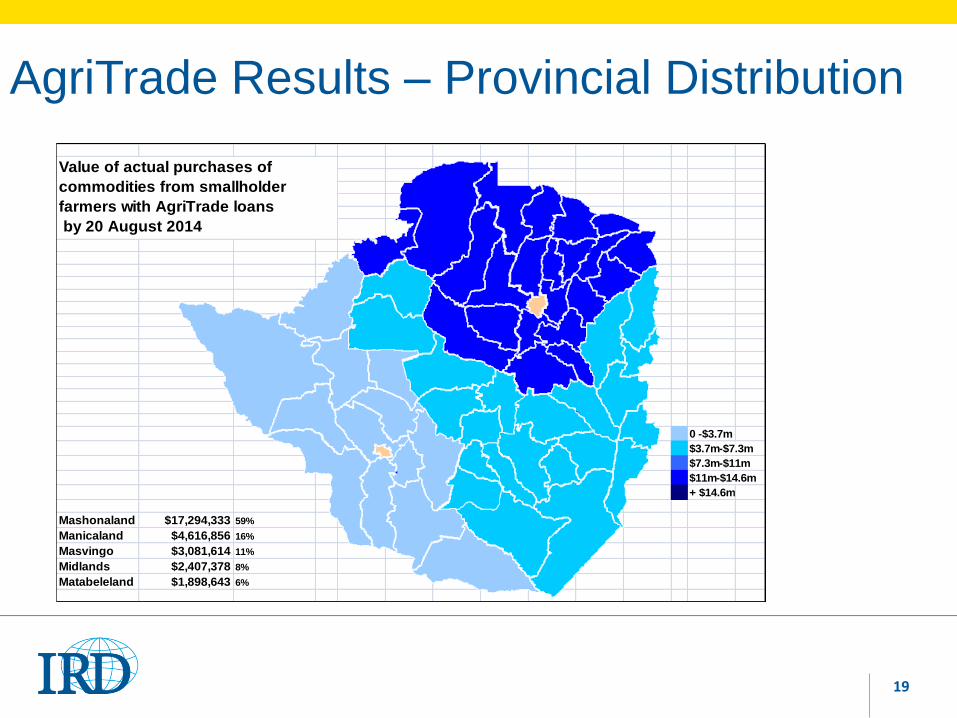

AgriTrade Results – Provincial Distribution

0 -$3.7m

$3.7m-$7.3m

$7.3m-$11m

$11m-$14.6m

+ $14.6m

Mashonaland $17,294,333 59%

Manicaland $4,616,856 16%

Masvingo $3,081,614 11%

Midlands $2,407,378 8%

Matabeleland $1,898,643 6%

Value of actual purchases of

commodities from smallholder

farmers with AgriTrade loans

by 20 August 2014

20

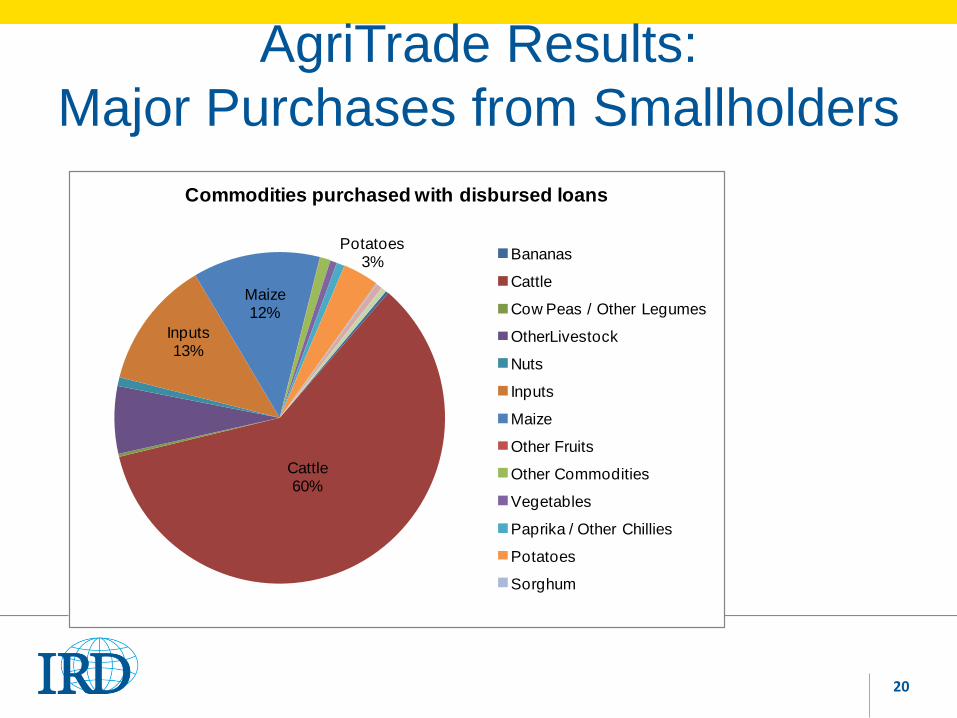

AgriTrade Results:

Major Purchases from Smallholders

Cattle60%

Inputs13%

Maize12%

Potatoes3%

Commodities purchased with disbursed loans

Bananas

Cattle

Cow Peas / Other Legumes

OtherLivestock

Nuts

Inputs

Maize

Other Fruits

Other Commodities

Vegetables

Paprika / Other Chillies

Potatoes

Sorghum

21

AGRITRADE DIRECT LENDING TO SMALLHOLDER HORTICULTURAL FARMERS

Scalable Experiences for horticulture from

- TWO programs – TWO approaches

A. DAIRYFIN FACILITY: MK/LOL/ZADF: USAID

B. ZIMAIED AGRITRADE Direct Lending Initiatives

22

DAIRYFIN – Revolving Credit Facility 1. Partners:Investors USAID & MK. NGO Partners:IRD/Land’O Lakes/ZADF

2. Initial Capitalization:36 incalf cross-breed dairy heifers

- 50% MK contribution + 50% USAID Contribution

3. MK DairyFinance Facility Terms:

- 25% deposit, 24 months loan tenor, 13% APR

4. Collateral Security Requirements:

+ Cessation on insured dairy heifers purchased with DairyFin loan,

+ Smallholder group solidarity loan guarantees

+ Stop-order loan repayment agreement with milk processor 5. Performance:

+100% disbursed, 100% repayments,100% Loan Principal Recovery

+400% Return on Investment for USAID funds by end of Year1

23

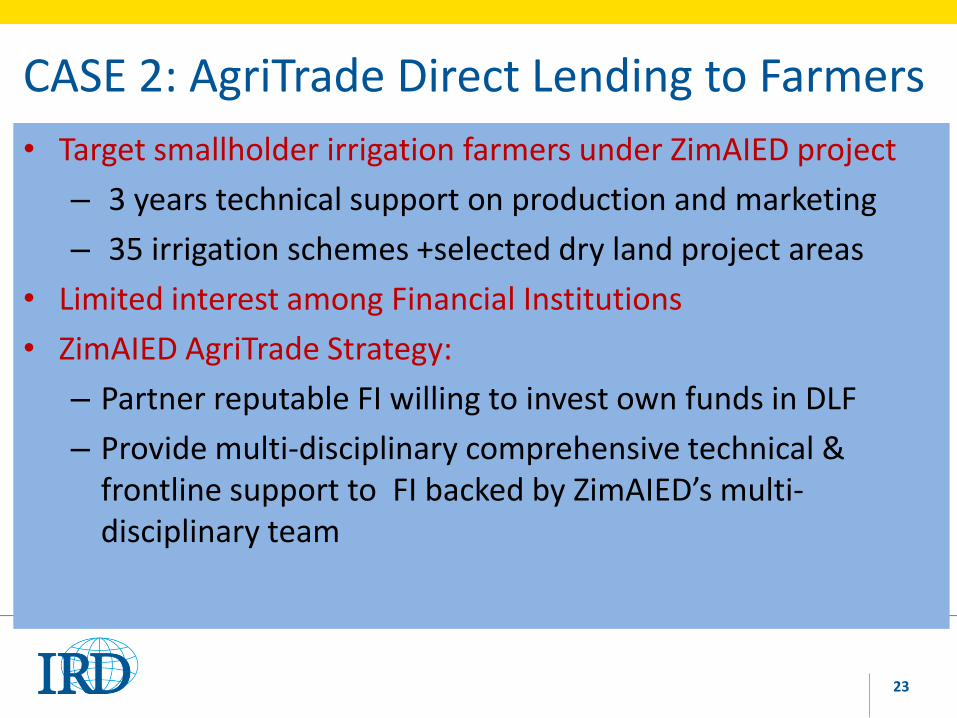

CASE 2: AgriTrade Direct Lending to Farmers

• Target smallholder irrigation farmers under ZimAIED project

– 3 years technical support on production and marketing

– 35 irrigation schemes +selected dry land project areas

• Limited interest among Financial Institutions

• ZimAIED AgriTrade Strategy:

– Partner reputable FI willing to invest own funds in DLF

– Provide multi-disciplinary comprehensive technical & frontline support to FI backed by ZimAIED’s multi-disciplinary team

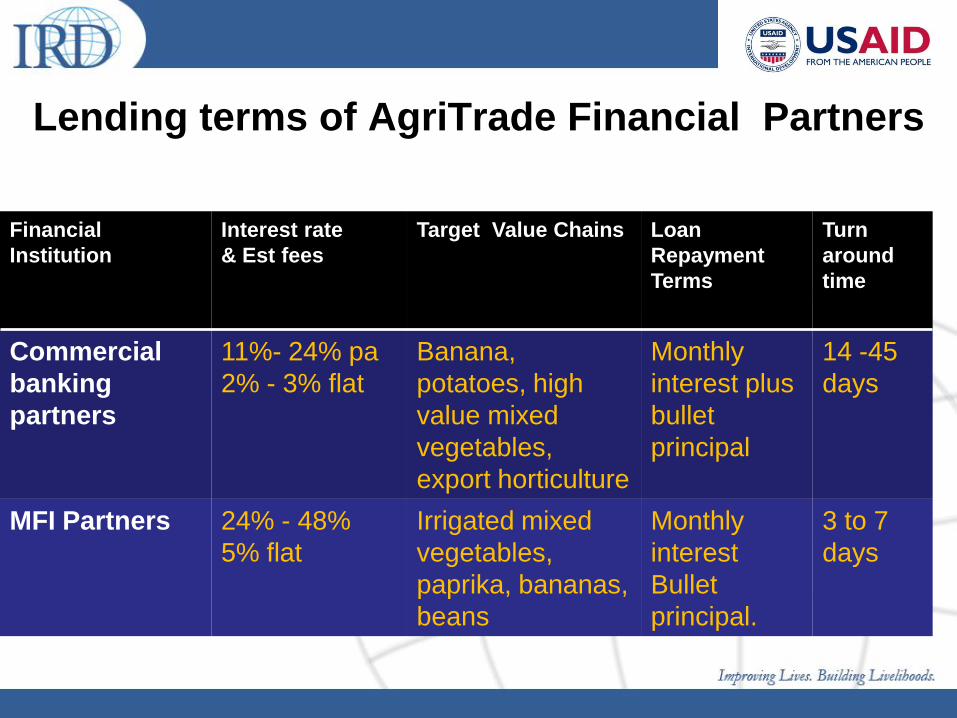

Lending terms of AgriTrade Financial Partners

Financial

Institution

Interest rate

& Est fees

Target Value Chains Loan

Repayment

Terms

Turn

around

time

Commercial

banking

partners

11%- 24% pa

2% - 3% flat

Banana,

potatoes, high

value mixed

vegetables,

export horticulture

Monthly

interest plus

bullet

principal

14 -45

days

MFI Partners 24% - 48%

5% flat

Irrigated mixed

vegetables,

paprika, bananas,

beans

Monthly

interest

Bullet

principal.

3 to 7

days

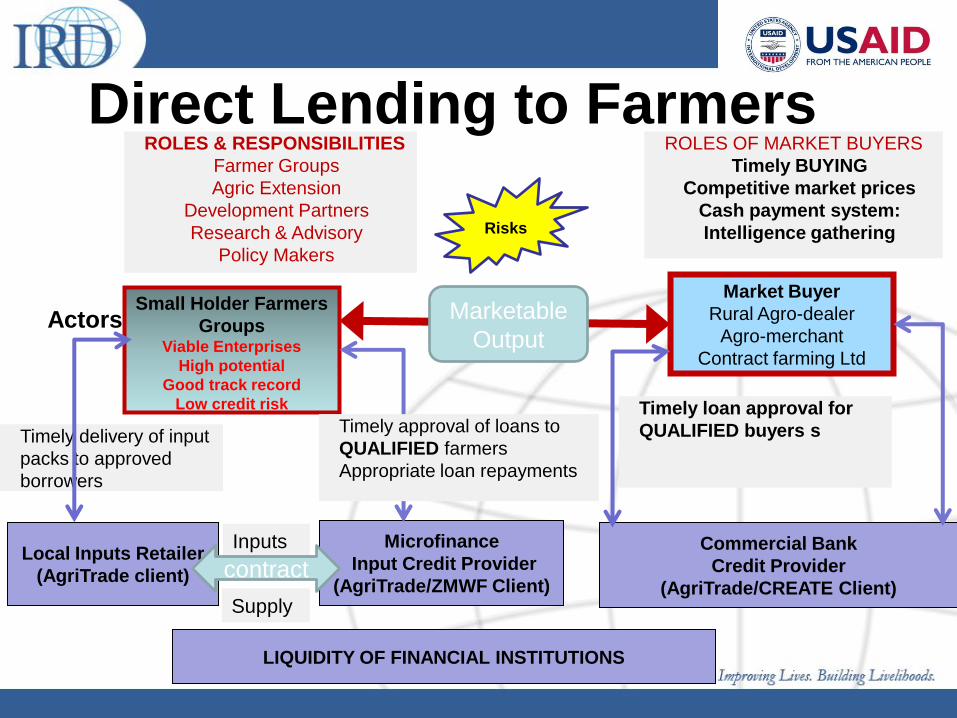

Direct Lending to Farmers

Small Holder Farmers

Groups Viable Enterprises

High potential

Good track record

Low credit risk

Market Buyer

Rural Agro-dealer

Agro-merchant

Contract farming Ltd

Local Inputs Retailer

(AgriTrade client)

ROLES & RESPONSIBILITIES

Farmer Groups

Agric Extension

Development Partners

Research & Advisory

Policy Makers

ROLES OF MARKET BUYERS

Timely BUYING

Competitive market prices

Cash payment system:

Intelligence gathering

Timely delivery of input

packs to approved

borrowers

Actors

Inputs Microfinance

Input Credit Provider

(AgriTrade/ZMWF Client)

Commercial Bank

Credit Provider

(AgriTrade/CREATE Client)

contract

Timely approval of loans to

QUALIFIED farmers

Appropriate loan repayments

LIQUIDITY OF FINANCIAL INSTITUTIONS

Timely loan approval for

QUALIFIED buyers s

Marketable

Output

Risks

Supply

26

$199,648

$281,576

$395,050

$445,878

$-

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

$450,000

$500,000

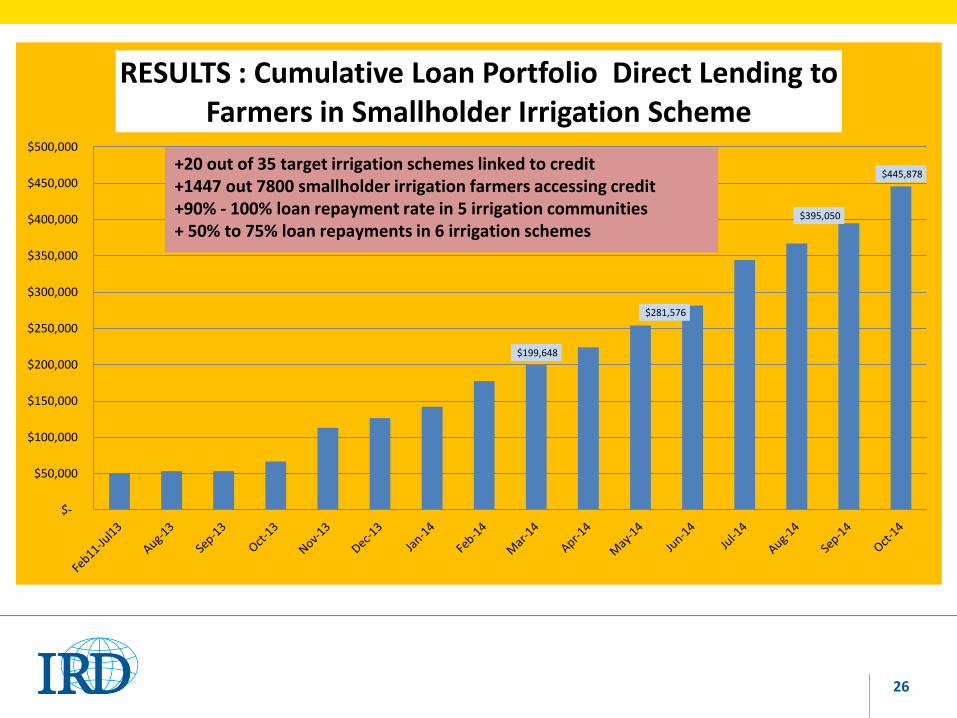

RESULTS : Cumulative Loan Portfolio Direct Lending to Farmers in Smallholder Irrigation Scheme

+20 out of 35 target irrigation schemes linked to credit +1447 out 7800 smallholder irrigation farmers accessing credit +90% - 100% loan repayment rate in 5 irrigation communities + 50% to 75% loan repayments in 6 irrigation schemes

27

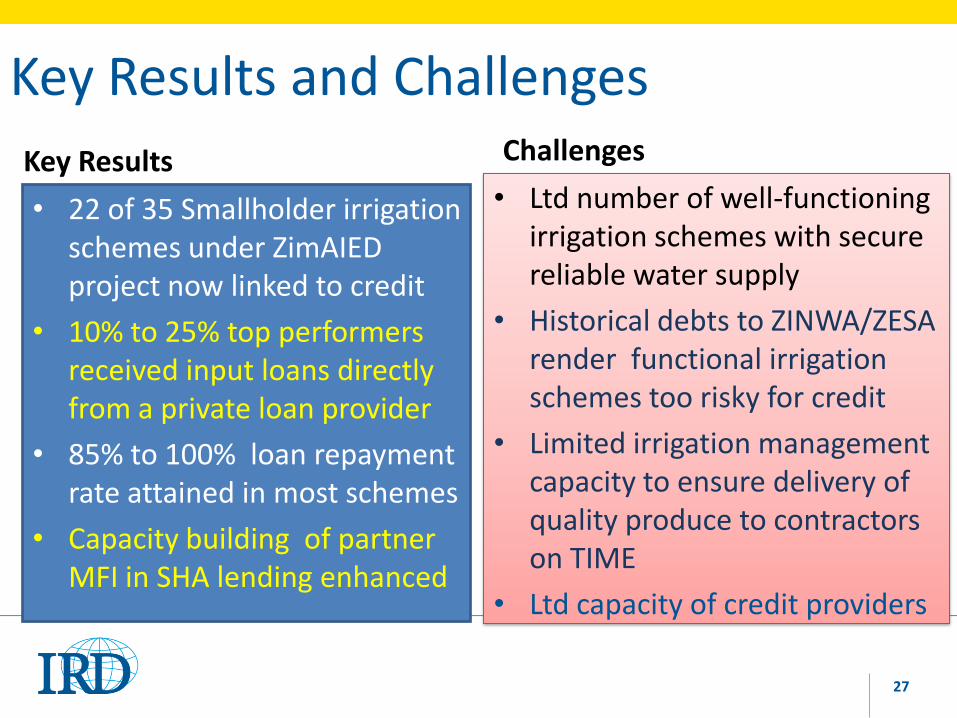

Key Results and Challenges

Key Results

• 22 of 35 Smallholder irrigation schemes under ZimAIED project now linked to credit

• 10% to 25% top performers received input loans directly from a private loan provider

• 85% to 100% loan repayment rate attained in most schemes

• Capacity building of partner MFI in SHA lending enhanced

Challenges

• Ltd number of well-functioning irrigation schemes with secure reliable water supply

• Historical debts to ZINWA/ZESA render functional irrigation schemes too risky for credit

• Limited irrigation management capacity to ensure delivery of quality produce to contractors on TIME

• Ltd capacity of credit providers

28

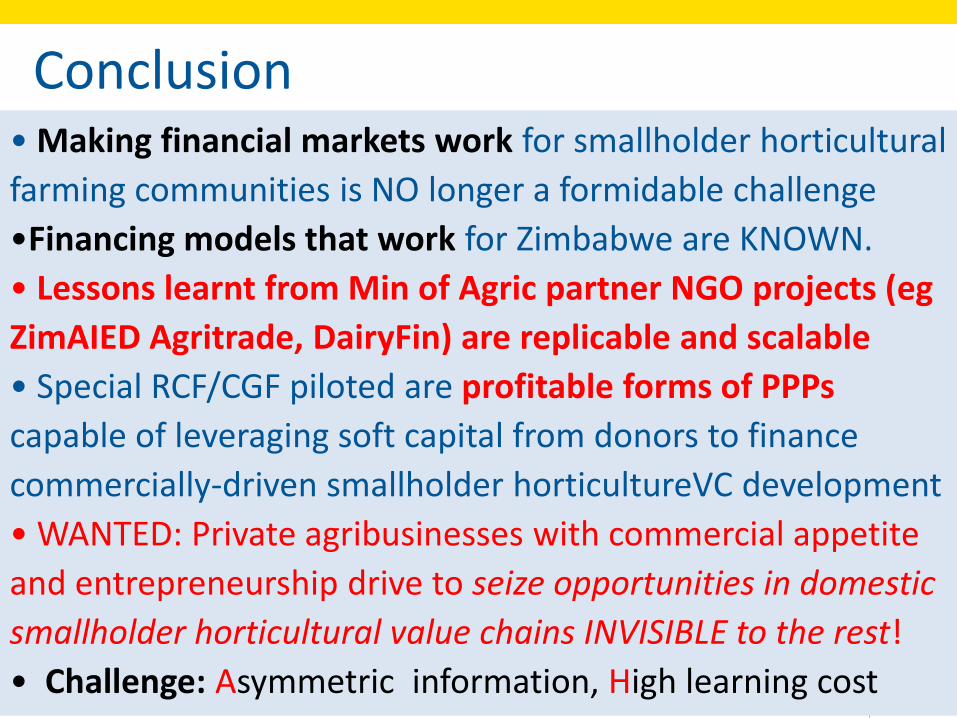

Conclusion • Making financial markets work for smallholder horticultural

farming communities is NO longer a formidable challenge

•Financing models that work for Zimbabwe are KNOWN.

• Lessons learnt from Min of Agric partner NGO projects (eg

ZimAIED Agritrade, DairyFin) are replicable and scalable

• Special RCF/CGF piloted are profitable forms of PPPs

capable of leveraging soft capital from donors to finance

commercially-driven smallholder horticultureVC development

• WANTED: Private agribusinesses with commercial appetite

and entrepreneurship drive to seize opportunities in domestic

smallholder horticultural value chains INVISIBLE to the rest!

• Challenge: Asymmetric information, High learning cost