horizontally integrated or vertically divided? · horizontally integrated or vertically divided? a...

TRANSCRIPT

Horizontally integrated orvertically divided?

A comparison of outsourcing strategies atEricsson and Nokia

”Outsourcing is one of the most misunderstood concepts in use today”Jorma Ollila

Working paperOctober 2002

Lars Bengtsson and Christian Berggren

2 (22)

PREFACE

In this report we try to compare the outsourcing strategies of Nokia and Ericsson, delimited tothe production of radio base stations. The results from a preliminary version of this reportrendered a great interest in media during summer year 2002. The results and implicationshave, however, in several cases been over-interpreted and even misinterpreted. We thus feelimpelled to elucidate the ambition and status of the report.

This is a working paper which aims at illustrating various choices and discuss theirconsequences, in order to elaborate questions for our further research. A follow-up study, inwhich we analyse current outsourcing strategies is in progress. The analysis in this report isdelimited to one business area within Nokia and Ericsson, namely the radio base stationbusiness. The description of other business areas mainly serves as a background to thecomparison.

The working paper mostly deals with the situation and planned activities as they appearedduring early spring year 2002. During late spring and summer of 2002, the market situationhas dramatically changed for the telecom companies. In order to conclude this report, we havechosen not to include the efforts made to deal with these new conditions.

The descriptions and analysis are based on the picture given by the interviewees and thematerial we have had access to. We cannot exclude that there are alternative andcomplementary images of the companies. The rapid changes within the companies have alsoled to a situation in which the strategies are expressed and interpreted differently in variousparts of the organisations. The overall strategies of the corporations have not been available tous. We have thus not analysed the relations between our descriptions and these overallstrategies.

Despite these limitations we believe that the questions, decisions and consequencesconcerning costs and competence, which are elaborated in the report, are of general interest.We hope that the analysis may provide a valuable contribution to the discussion onoutsourcing and its effects, which is a topical question in many companies.

Gävle in October 2002

Lars Bengtsson Christian Berggren

University of Gävle University of Linköping

3 (22)

CONTENTS

PREFACE .................................................................................................................................2

1 BACKGROUND....................................................................................................................5

1.1 THE FUTURE OF MANUFACTURING: A COMMODITY OR A STRATEGIC COMPETENCE?..........51.2 OUTSOURCING IN THE TELECOM INDUSTRY – ONLY ONE WAY FORWARD? .........................61.3 PURPOSE OF THE REPORT....................................................................................................7

2 NOKIA AND OUTSOURCING...........................................................................................9

3 ERICSSON AND OUTSOURCING..................................................................................11

4 LEARNING FROM NOKIA OR ERICSSON? COMPARING TWO

OUTSOURCING STRATEGIES .........................................................................................14

4.1 TWO ALTERNATIVE STRATEGIES FOR OUTSOURCING ........................................................144.2 RISKS AND COSTS. AN ANALYSIS OF JUSTIFICATIONS AND OUTCOMES. ............................154.3 INDUSTRIALIZE WITHOUT VOLUME PRODUCTION? THE PROBLEM OF CORE COMPETENCE 184.4 LEARNING FROM NOKIA OR ERICSSON? ...........................................................................19

REFERENCES .......................................................................................................................21

4 (22)

5 (22)

1 BACKGROUND

1.1 The future of manufacturing: A commodity or a strategic competence?During recent years there has been a strong trend within Swedish industry towardsoutsourcing of manufacturing and resources supporting manufacturing. An indication is thedecreasing level of value-added within the engineering industry, from 31% in 1990 down to25% in 1998 (VI 1999).

This outsourcing trend signifies a changing view on the significance of manufacturing. Quitea few companies have begun to view manufacturing as an undifferentiated standard activity(e.g. Arnold 2002), a ”commodity” which easily can be sourced from external market actorsin the new “network economy”. A representative case of this attitude could be found inHarvard Business Review 2000: ”Does Manufacturing Matter? The short answer is: notmuch. And that´s a good thing” (Ramaswamy & Rowthorn 2000).

In the research on production and outsourcing, however, several authors have pointed to theproblems of large-scale outsourcing. The outsourcing decisions are often justified by costconsiderations, but paradoxically it has turned out to be quite difficult to sort out the actualcost effects of outsourcing decisions, not only in the long-term, which is always difficult, butalso the short-term outcomes. The costs, ex post, of manufacturing at contract manufacturers,are often different from the quoted price, ex ante. Various transaction expenses, such as thecosts of transferring products, equipment and knowledge from the customer firm to thecontract manufacturer are left out of the analyses, and so are the costs and potentials ofvarious production learning curves, etc.

Against the ”manufacturing-as-commodity”-perspective, a perspective on manufacturing as astrategic competence within technology-based firms has been formulated (e.g. Brown et al2000; Pfeffer & Sutton 2000). Whereas the outsourcing trend tends to downgrade the value ofmanufacturing knowledge and process engineering skills, this perspective points to the needof investing in advanced manufacturing processes and competence development. From thisview follows the importance of making the strategic role of manufacturing visible inside andoutside the firm. Otherwise valuable resources might be lost as a result of short-term financialconsiderations. Since outsourcing tends to be an irreversible process, these resources might beimpossible to recover. If the role of manufacturing competencies remains neglected and”invisible”, there could be an increasing gap between actual productivity in the down-gradedproduction departments and the productivity increases which might result from a commitmentto invest in strategic production development.

This potential productivity gap has motivated a new research project on the consequences ofoutsourcing for renewal and learning capabilities in technology-based firms (Bengtsson2001). A key question concerns the role – if any – of manufacturing for the long-termcompetitive positions of the studied firms. According to the project proposal, there is a needfor an elaboration of the future-oriented and company-unique capabilities, which are or couldbe realized in advanced manufacturing operations. In previous studies five categories of suchpotentially strategic competencies have been singled out (Berggren & Bengtsson 2000;Bengtsson & Berggren 2001):

6 (22)

• Operational skills in achieving high levels of quality, productivity, flexibility and deliveryprecision. The links between these capabilities and the competitiveness of innovative firmshave been demonstrated in several studies.

• Competence in logistics and sourcing. Manufacturing skills constitute an important basisboth for evaluation of suppliers and knowledge exchange with the suppliers.

• Competence in design for manufacture, experiences of participation in cross-functionaldevelopment and in analyzing and communicating manufacturing consequences of designdecisions.

• Competence in industrialization (process engineering and production ramp-up). The abilityto achieve a rapid ramp-up from try-out runs of new products to high volume production ina short period of time is of increasing importance for competition in global industries. Thiscompetence is based on several production-related capabilities, such as process planning,industrial engineering and materials management, test development and prototypefabrication. A systematical development of product-process flexibility in the productionsystem is a key condition for achieving such a competence in industrialization.

• Competence in environmental management. The experience of structured quality andenvironmental management efforts in well-run manufacturing units could serve as a modelfor company-wide environmental management systems, including management of supplieractivities.

As long as the potential and actual capabilities of manufacturing are not visible, notunderstood and not appreciated at corporate levels, it is difficult to evaluate the possiblecontributions of a firm´s production operation to the future competitiveness of the firm. In thissituation efforts to estimate the merits and demerits of outsourcing remain elusive. Infinancially hard times firms are tempted to find “silver bullet-solutions”, by for exampleselling off manufacturing divisions, to get rid of visible costs tracked by stock marketanalysts. In these circumstances it is particularly important to understand the full costs ofoutsourcing, and the potential role of manufacturing competencies for effective productdevelopment, supply strategies and product industrialization in the future.

1.2 Outsourcing in the telecom industry – only one way forward?Within the telecom industry, most cases of outsourcing imply that production activities aretransferred to American contract manufacturers, who in the next round relocate theseactivities to low-wage locations. The far-reaching outsourcing process at Ericsson is well-known. But how is the situation at Nokia? There is an abundance of articles comparing thestyling and performance of the two companies´ various mobile phones, whereas studieslooking into the manufacturing and production ramp up strategies of the two Nordic firms arein short supply. In Sweden it has sometimes been argued that outsourcing represents thefuture of the industry, and in this sense Ericsson represents a more ”advanced” case, whichsoon will be followed by Nokia. This understanding is well received in the EMS community.However, this deterministic perspective of only one way to organize manufacturing in hightech industries is misleading. Maybe Nokia is not at all a ”latecomer” in the outsourcinggame, but represents a qualitatively different strategy, and a harbinger of future reorientation,beyond the current fads and fashions.

7 (22)

The CEO of Nokia, Jorma Ollila emphasize that outsourcing, or relocation to low cost sitesdoes not solve any problem by itself. In an interview in Swedish Dagens Nyheter (02-01-25)he argues: ”Outsourcing is one of the most misunderstood concepts in use today. The realchallenge is to get all the parts of the business, the entire network to function in an efficientway.”

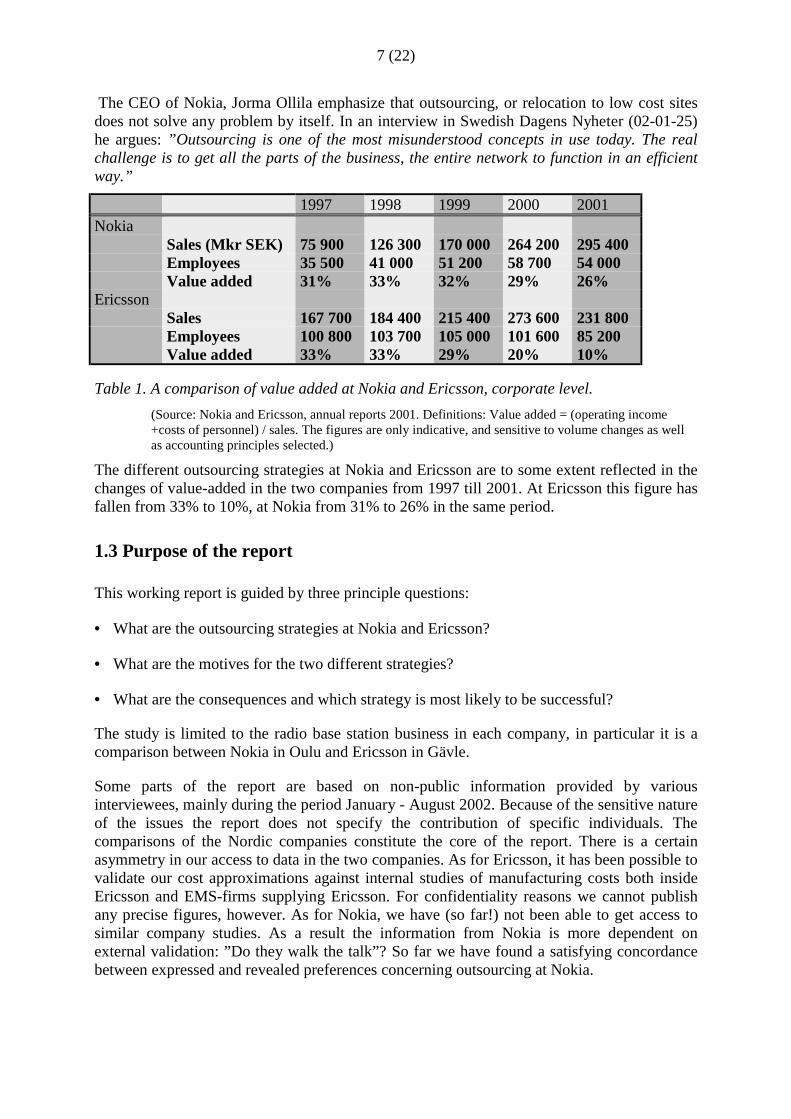

1997 1998 1999 2000 2001Nokia

Sales (Mkr SEK) 75 900 126 300 170 000 264 200 295 400Employees 35 500 41 000 51 200 58 700 54 000Value added 31% 33% 32% 29% 26%

EricssonSales 167 700 184 400 215 400 273 600 231 800Employees 100 800 103 700 105 000 101 600 85 200Value added 33% 33% 29% 20% 10%

Table 1. A comparison of value added at Nokia and Ericsson, corporate level.(Source: Nokia and Ericsson, annual reports 2001. Definitions: Value added = (operating income+costs of personnel) / sales. The figures are only indicative, and sensitive to volume changes as wellas accounting principles selected.)

The different outsourcing strategies at Nokia and Ericsson are to some extent reflected in thechanges of value-added in the two companies from 1997 till 2001. At Ericsson this figure hasfallen from 33% to 10%, at Nokia from 31% to 26% in the same period.

1.3 Purpose of the report

This working report is guided by three principle questions:

• What are the outsourcing strategies at Nokia and Ericsson?

• What are the motives for the two different strategies?

• What are the consequences and which strategy is most likely to be successful?

The study is limited to the radio base station business in each company, in particular it is acomparison between Nokia in Oulu and Ericsson in Gävle.

Some parts of the report are based on non-public information provided by variousinterviewees, mainly during the period January - August 2002. Because of the sensitive natureof the issues the report does not specify the contribution of specific individuals. Thecomparisons of the Nordic companies constitute the core of the report. There is a certainasymmetry in our access to data in the two companies. As for Ericsson, it has been possible tovalidate our cost approximations against internal studies of manufacturing costs both insideEricsson and EMS-firms supplying Ericsson. For confidentiality reasons we cannot publishany precise figures, however. As for Nokia, we have (so far!) not been able to get access tosimilar company studies. As a result the information from Nokia is more dependent onexternal validation: ”Do they walk the talk”? So far we have found a satisfying concordancebetween expressed and revealed preferences concerning outsourcing at Nokia.

8 (22)

An extended version of this English report is available as a working paper in Swedish(Bengtsson & Berggren 2002).

9 (22)

2 NOKIA AND OUTSOURCING

Nokia consists of three global divisions: Nokia Networks, Nokia Mobile Phones and NokiaVentures (as of early 2002). The mandate of Nokia Networks is to develop, build and delivermobile and fixed networks and IP network infrastructure and related services. In 2001, NokiaNetworks represented approximately 24% of Nokia´s net sales. The division employed 22,000people and seven factories worldwide, four in Finland and three in China.

At Nokia Phones, manufacturing is viewed as a core competence: ”We consider our mobilephone manufacturing to be a core competency and competitive advantage.” (Nokia Form 20-F, 2001: 34.) In contrast to other mobile phone providers, only a minor part, in 2001approximately 20%, of Nokia´s mobile phones are outsourced to external vendors.

The production and supply structure of Nokia Networks is more complex, but the same basicconsiderations seem to apply also in this division. Both Nokia Phones and Networks havedeveloped long-standing partnerships with selected suppliers. These are evaluated on anumber of factors such as financial resources to increase production capacity, systems ofmanagement control, general technological skills and specific skills in quality systems,manufacturing, supply management, etc. On top of these hard issues, the attitudes, values,visions and goals of the potentials suppliers are evaluated (Ali-Yrkkö 2000).

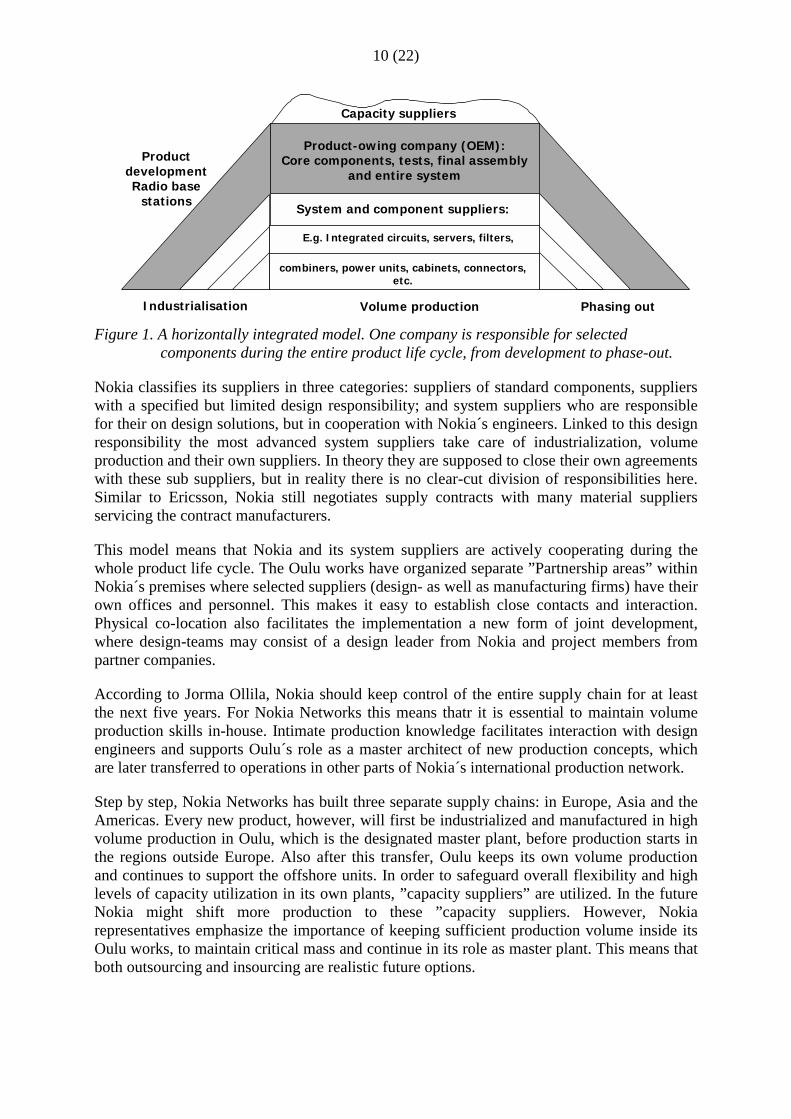

The main site of Nokia Networks´ radio base stations, both development and manufacturing,is located in Oulu, in northern Finland. In addition to research and global productdevelopment, the Oulu organization includes prototype fabrication and pilot plants,departments for product industrialization and high volume production of radio base stationsfor the European market. Close to the Nokia premises a good part of its suppliers are located(even though in a process of relocating to low wage sites). Previously, Nokia owned severalof these companies. Similar to Ericsson (but not to the Phone division) Nokia Networks hasdecreased its degree of vertical integration by selling off complete factories to contractmanufacturers. So far, however, the scale of this outsourcing is much more limited. Filterproduction has been transferred to Filtronics and in 2001, SCI acquired Nokia Networks´facilities, including personnel, for radio access products in Haukipudas, close to Oulu and thetransceiver (TRU) plant in Camberley, UK.

The sourcing strategy of Nokia Networks may be described as ”component oriented”. Thismeans that Nokia maintains strategic components and processes in-house, first and foremostTRU-manufacturing and the majority of final assembly and testing of complete radio basestations. By keeping volume manufacturing of the TRUs, the heart of the radio base station,in-house, Nokia Networks is well placed to prepare production of the next technologygeneration. Components, which are viewed as non-strategic, are sourced from selectedsuppliers, normally only one or a few for each component. This include for instance Nokia-specific integrated circuits and radio frequency components, servers and subassemblies suchas filters, combiners and power units, mechanical components (e.g. cabinets) and connectors.Some parts of the final assembly, including testing has been transferred to partner companies,but Nokia still tests random samples from these companies.

10 (22)

Volume production Phasing out

ProductdevelopmentRadio base

stations

Product-owing company (OEM):Core components, tests, final assembly

and entire system

Industrialisation

Capacity suppliers

System and component suppliers:

E.g. Integrated circuits, servers, filters,

combiners, power units, cabinets, connectors,etc.

Figure 1. A horizontally integrated model. One company is responsible for selectedcomponents during the entire product life cycle, from development to phase-out.

Nokia classifies its suppliers in three categories: suppliers of standard components, supplierswith a specified but limited design responsibility; and system suppliers who are responsiblefor their on design solutions, but in cooperation with Nokia´s engineers. Linked to this designresponsibility the most advanced system suppliers take care of industrialization, volumeproduction and their own suppliers. In theory they are supposed to close their own agreementswith these sub suppliers, but in reality there is no clear-cut division of responsibilities here.Similar to Ericsson, Nokia still negotiates supply contracts with many material suppliersservicing the contract manufacturers.

This model means that Nokia and its system suppliers are actively cooperating during thewhole product life cycle. The Oulu works have organized separate ”Partnership areas” withinNokia´s premises where selected suppliers (design- as well as manufacturing firms) have theirown offices and personnel. This makes it easy to establish close contacts and interaction.Physical co-location also facilitates the implementation a new form of joint development,where design-teams may consist of a design leader from Nokia and project members frompartner companies.

According to Jorma Ollila, Nokia should keep control of the entire supply chain for at leastthe next five years. For Nokia Networks this means thatr it is essential to maintain volumeproduction skills in-house. Intimate production knowledge facilitates interaction with designengineers and supports Oulu´s role as a master architect of new production concepts, whichare later transferred to operations in other parts of Nokia´s international production network.

Step by step, Nokia Networks has built three separate supply chains: in Europe, Asia and theAmericas. Every new product, however, will first be industrialized and manufactured in highvolume production in Oulu, which is the designated master plant, before production starts inthe regions outside Europe. Also after this transfer, Oulu keeps its own volume productionand continues to support the offshore units. In order to safeguard overall flexibility and highlevels of capacity utilization in its own plants, ”capacity suppliers” are utilized. In the futureNokia might shift more production to these ”capacity suppliers. However, Nokiarepresentatives emphasize the importance of keeping sufficient production volume inside itsOulu works, to maintain critical mass and continue in its role as master plant. This means thatboth outsourcing and insourcing are realistic future options.

11 (22)

3 ERICSSON AND OUTSOURCING

Ten years ago, Ericsson was a vertically integrated company with significant and diversifiedproduction resources. The outsourcing process started in the mid 1990s, when ETX the fixednetwork division, suffering from increasingly difficult business conditions and falling demandstarted to outsource various simple components, such as cabinets and plastic details. A keyissue already at this time concerned Ericssons´s perception of its future core business and corecompetencies. The answer has been changing over time. Initially, Ericsson regarded mountedcircuit boards as part of its own manufacturing business. When the crisis at SwedishNorrköping surfaced, partly as a result of a failed project to develop a new SDH-switch(Synchronous Digital Hierarchy), the “core competence” line was redrawn and the in-houseproduction of advanced PCBs was put to an end. In this case it was no real outsourcingdecision, but rather a complete close down of the Norrköping plant, and the elimination of1800 jobs. In the wake of this crisis, the management of the fixed networks division revisedits entire production strategy. It was decided only to keep test platforms in-house, and tooutsource basically all other production. The first real outsourcing-case occurred inÖstersund, where complete AXE-switches were assembled. This plant and a French sisterplant was sold off to Solectron. The decision that was presented as an alternative to a plantclosure. The espoused rationale was that the American contract manufacturer would be able toimprove capacity utilization and reduce production costs by attracting other customers to theplant. This never materialized, however. As a consequence production efficiencies were neverimproved in the plant, and the justification of the outsourcing decision collapsed. Recently,Solectron has dismissed all employees in Östersund.

Within the Radio division, ERA, comprising systems as well as terminals (phones) there wasinitially an entirely different attitude towards outsourcing. As late as 1998, manufacturing andtesting were perceived as critical business competencies in this division, and actually plantswere transferred from ETX to ERA. This view was to change rapidly. Already in 2000, thesystems and networks business, still highly profitable, adopted the very outsourcing-strategyformulated at the ETX division and criticized by the radio people only two years earlier.According to this production strategy all volume production should be phased-out andtransferred to contract manufacturers. The centre for development and design of Ericsson´sradio base stations is located in Kista, whereas the main production site used to be Gävle,supported by the Kumla plant. Recently Ericsson had a base station plant in Visby, too. But in2000 as a result of the new outsourcing strategy, the Visby plant was sold out to Flextronics.Previous outsourcing decisions within ERA had been component-oriented, contracting outcomputer, signal cards and subassemblies like cabinets, cables and power supply units tocompanies such as Emerson, Flextronics and Sanmina. With the transfer of Visby, Flextronicsacquired sole responsibility for the complete TRU-production to the first generation GSM-systems (RBS 200) for the rest of its product life. And in the following year, the entire mobilephone production was suddenly transferred to Flextronics, who rapidly started to closefactories in Sweden and other high-cost countries and move production to low-wagelocations.

According to the new production strategy, the critical core competencies within Ericsson willbe product design, test development and industrialization of new products both strategiccomponents such as radio modules and of complete products such as radio base stations,including final assembly and testing. So far, the strategy has been implemented for two GSM-products, and will be fully implemented for all 3G products.

12 (22)

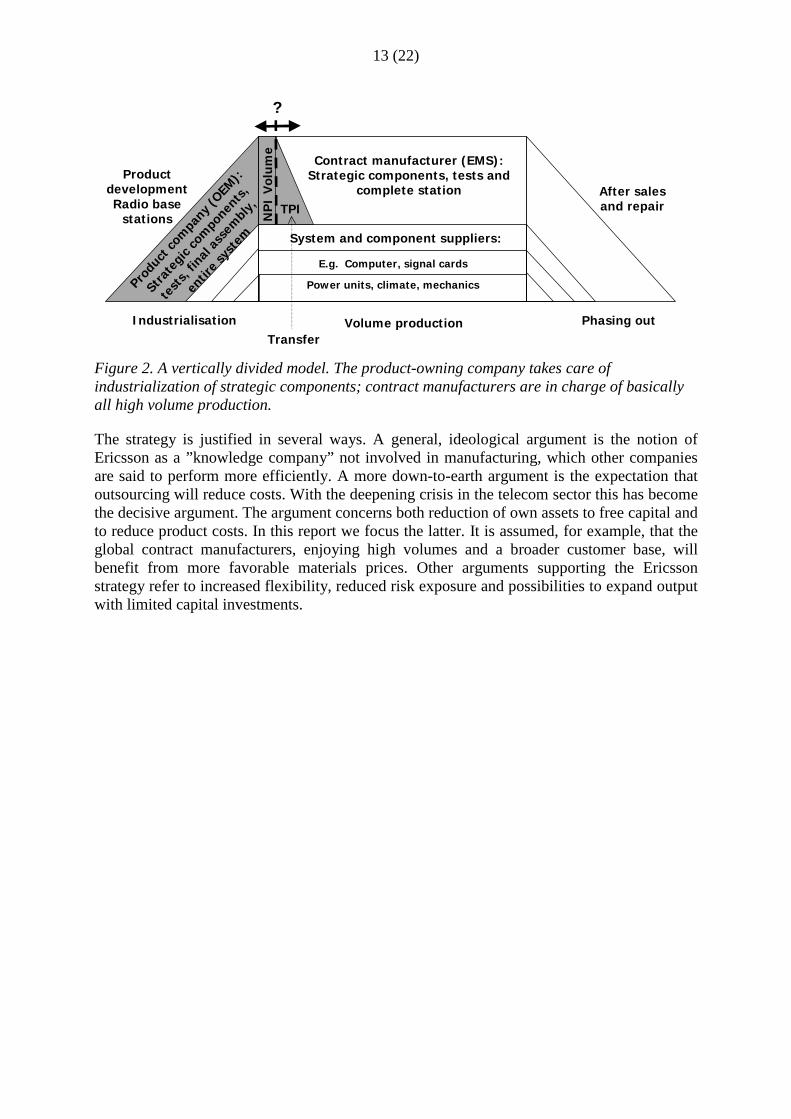

” Industrialization” refers to the process of preparing products for production (includingnecessary design modifications), the ramp-up of production from prototype fabrication andtry-out series to full industrial scale, and the design and fine-tuning of the supply chain fromorder to delivery and customer hand-over. Reduction of unit costs and lead-time are the over-riding goals of the industrialization process. The success is strongly dependent on achievingproduct and process stability. One key target is to increase process yield (i.e., to reduce theratio of products requiring rework after testing); another is to reduce through-put time byshortening the test time, which initially may be quite long (several hours).

When the process is regarded as stable, the baton is passed to the contract manufacturers, whowill now be responsible for volume production and the continued efforts to increase processyield and lower costs. Product and process stability are no unambiguous concepts, however.Within Ericsson, the cut-off point (final take over) between ERA and the contractmanufacturers normally equals a process yield of 60%. This is still far from efficient volumeproduction. If the yield is raised from 60% to 90%, production capacity will theoreticallyincrease by 50% and unit costs will drop 33%. This means that a lot of process improvementand to some extent also product modifications need to be carried out after this cut-off point isreached. Actual studies of changes in production costs at Ericsson plants as well as externalplants indicate strongly positive learning curves during several years. The lead-time needed toreach high yield levels decides when the new product can be produced profitably. In theEricsson strategy of 2000, contract manufacturers are responsible for this decisive process(and to some extent product) refinement.

Previously Gävle was a master plant for global radio base station production within Ericsson.The new strategy means that the most important mandate of Gävle and its 1,400 employees(May 2002) now is to be responsible for the industrialization process, in close cooperationwith the design departments in Kista. After several steps and iterations of product and processdevelopment, production ramp-up starts, and the plant focuses on reducing test times andincrease process yield. As noted above, the interface between industrialization and volumeproduction is by no means cast in concrete. Within Gävle there are strong arguments for anextended mandate, to run new products in high volumes during a short period of time, in orderto verify the process and safeguard its own competence (in the figure below this is called NPI-volume, i.e. volume production during New Product Introduction). An unresolved issue hereis the cost for investing in high-capacity production that will only be used for a strictly limitedperiod.

The Ericsson way of sourcing could be described as a vertically divided model. During theend phase of the industrialization process, the selection of contract manufacturers is finalized.A transfer project is set up to convey product and process knowledge and productiontechnology including the dedicated test systems to the selected EMS-company. The Ericssonmodel of industrialization and supplier cooperation is presented in Figure 2.

13 (22)

Volume production Phasing out

ProductdevelopmentRadio base

stations

Contract manufacturer (EMS):Strategic components, tests and

complete station

Industrialisation

Produ

ct co

mpa

ny (OEM

):

Stra

tegi

c com

ponen

ts,

test

s, fin

al as

sem

bly,

entir

e sys

tem

?

NP

I V

olu

me

TPI

Transfer

System and component suppliers:

Power units, climate, mechanics

E.g. Computer, signal cards

After salesand repair

Figure 2. A vertically divided model. The product-owning company takes care ofindustrialization of strategic components; contract manufacturers are in charge of basicallyall high volume production.

The strategy is justified in several ways. A general, ideological argument is the notion ofEricsson as a ”knowledge company” not involved in manufacturing, which other companiesare said to perform more efficiently. A more down-to-earth argument is the expectation thatoutsourcing will reduce costs. With the deepening crisis in the telecom sector this has becomethe decisive argument. The argument concerns both reduction of own assets to free capital andto reduce product costs. In this report we focus the latter. It is assumed, for example, that theglobal contract manufacturers, enjoying high volumes and a broader customer base, willbenefit from more favorable materials prices. Other arguments supporting the Ericssonstrategy refer to increased flexibility, reduced risk exposure and possibilities to expand outputwith limited capital investments.

14 (22)

4 LEARNING FROM NOKIA OR ERICSSON? COMPARING TWO

OUTSOURCING STRATEGIES

4.1 Two alternative strategies for outsourcingBoth Ericsson and Nokia are outsourcing production, citing the same general reasons: theneed to focus on core competencies and team up with global partners, to enhance flexibilityand reaction speed, etc. As noted above, however, there is a significant difference in thedegree of outsourcing and in the speed of change. De-integration of production operations hasproceeded much faster at Ericsson than at Nokia. Furthermore, there is a difference in theactual mode of outsourcing.

The different production networks that are formed as a result of idiosyncratic ways of teamingup with external manufacturing partners could be described in terms of configuration andcoordination (Shi & Gregory 1998). Configuration refers to the geographical structure andfocus of the various locations. Theoretically there are two types of configuration, productfocussed or process focused (Hayes & Schemmer 1978). Product focus means that eachproduction unit is responsible for a specific product or component. Process focus refers to anetwork divided according to process types and process steps. Coordination, the other keyconcept, refers to the modes of managing and controlling the various units in the network.

The sourcing strategy of Nokia Networks has resulted in a product-focused productionnetwork, akin to the component-based supply model common in the automotive industry(Corswant & Fredriksson 2002). Graphically, a horizontally sliced but vertically integratedmodel represents the product life cycle in this network (see Fig 1). A key aspect in the modelis the fact that Nokia maintains responsibility in-house for strategic components during theirentire life cycle: design and engineering, industrialization, volume production, after sales andphase out. Furthermore, Nokia Networks takes care of the final testing of key components,base station assembly and delivery. The responsibility for so-called non-strategic componentsis allocated to several different system suppliers. The model as a whole presupposes an activecollaboration between Nokia and its selected suppliers during the entire product life span.

The production network shaped by the sourcing strategy of Ericsson Radio is of a compositetype. In parts of the network there is a product focus. This involves the suppliers of non-corecomponents, such as Emerson (power supply) or SCI-Sanmina (cabinets). The new strategyimplemented since 2000, where volume production is transferred to contract manufacturers,had added a process-focused system of relations. As Figure 2 illustrates, this network can berepresented as a model, which is both horizontally sliced and vertically divided. In this model,outsourcing also encompasses production of strategic components, final assembly, test andinstallation. Most of the components, as well as the testing system and the product as a whole,are developed and industrialized by Ericsson, however. For the non-core components, systemsuppliers are responsible also for design (collaborating with Ericsson), and production. Inthese cases, the responsibility for industrialization is carried out mainly by the suppliers.

A key issue in both types of production network concerns coordination and management ofthe interfaces between components, both in the design and industrialization phases. How doNokia and Ericsson engineers collaborate with their counterparts at the system suppliers? Theambition of Nokia is to create cooperative interaction in its joint design areas at the Oulu

15 (22)

works. There is also an ambition to devise common IT-enabled development processes on aglobal level. So far this has not been accomplished (and maybe never will).

In the Ericsson network, the Swedish company retains responsibility for design andindustrialization of most components, but also strives to develop new forms of suppliercollaboration. As a result of its outsourcing of volume production, another interface issue isadded to its supply chain management. Both Nokia and Ericsson are coordinating theircomponent manufacturers, but on top of that Ericsson has to coordinate and integrate atechnologically highly complex process chain. The interface problem is aggravated by thedifferent orientation of Ericsson and its contract manufacturers. Product industrialization atEricsson is focused on design adaptation in order to improve manufacturability, not on theproduction process per se. As a result, the production systems formed at Ericsson may divergefrom the standardized processes at the contract manufacturers.

4.2 Risks and costs. An analysis of justifications and outcomes.

There are various motives behind outsourcing (The Outsourcing Institute 2001). Costconsiderations is a key factor driving outsourcing decisions. Neither Nokia nor Ericssonwould outsource production if they expected this would bring higher costs to the customer.Another motive is related to strategic focus, and the interpretation of future corecompetencies. A third factor concerns risk exposure and flexibility in the highly turbulenttelecom sector. According to Ericsson management, the EMS-companies can level theirproduction across several customers. By outsourcing production to these firms Ericsson willreduce the risk of being caught with over-capacity in a negative business cycle with fallingdemand.

The large contract manufacturers are not unconditionally flexible, however, but demandscompensation if real demand falls short of booked capacity. Alternatively Ericsson foots thebill for their production investments. The expressed intention at Ericsson is that contractmanufacturers should be able to increase their output with 30% within 2-4 weeks, oralternatively, to cease production (-100%) within the same time. The actual flexibility level asof today, and the price Ericsson has to pay for this flexibility is not disclosed.

In general presentations such as the annual report Nokia, too, emphasizes that sourcing fromthird party suppliers increase flexibility and reaction speed (Nokia Form 20-F 2001: 34). Ininterviews, a considerable doubt is expressed if increased outsourcing really enhancesflexibility. Interviewed managers point out that almost all the EMS-firms are subject to thesame business cycle, which means that several of these companies, for example Solectron, isnow under heavy financial pressure. Another important consideration at Nokia is the risk ofbeing too dependent on international manufacturers whose strategies sometimes areunconvincing. One instance, mentioned by Nokia, is the tendency by several manufacturers,including Flextronics, to evolve into conglomerates. ”They now look similar to our structure10 years ago. What is their competitive advantage when they are manufacturing´everything´?”. At the end of the day, Nokia managers argue, the issue in risk management isnot outsourcing but forecasting, the capability to analyze future trends and adapt the capacitylevels accordingly. A possible objection to this reasoning is the question if reliable forecastingis possible in the deregulated telecom industry. It could be argued that the key question iswhich way of designing and controlling the production network yields the highest level of real(not to confuse with contractual) flexibility to the lowest cost. An investigation of thisimportant problem falls outside the scope of this report.

16 (22)

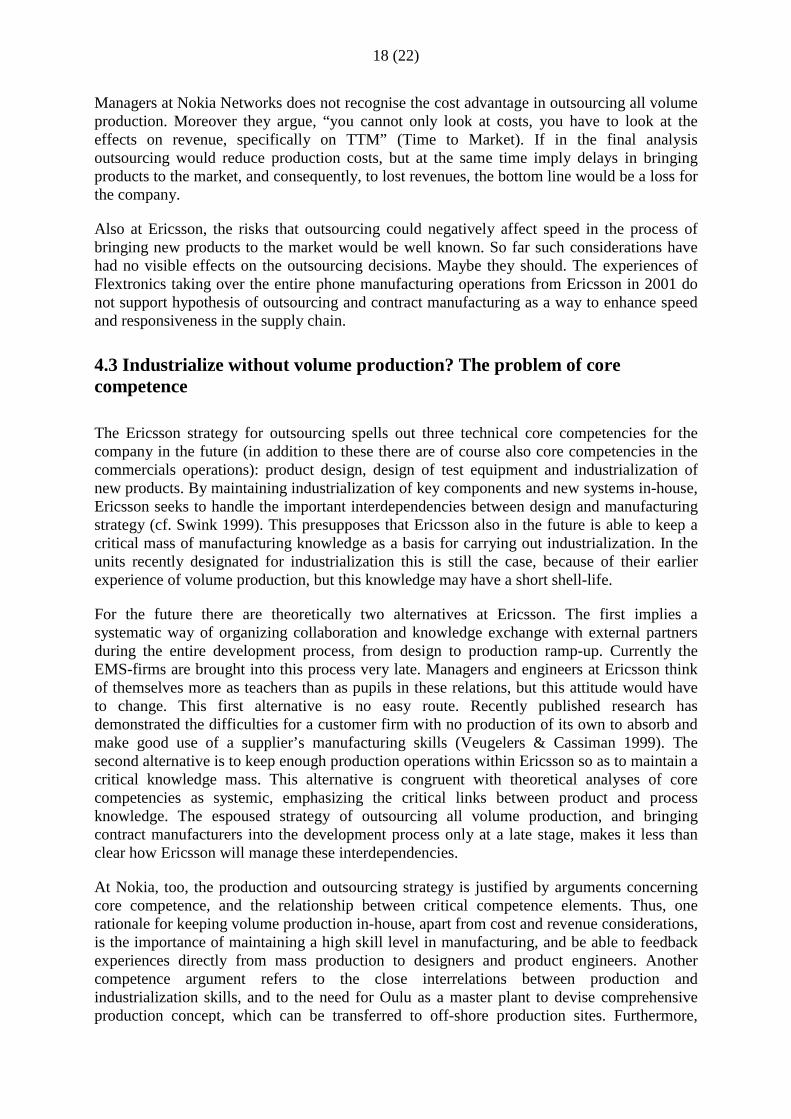

What is the possible cost advantage of outsourcing production? The opinions at Nokia andEricsson differ. Ex ante estimates demonstrating cost reductions are not difficult to find. It isharder to identify rigorous ex post analyses, which try to factor in all relevant parameters.Some follow up studies at Ericsson indicate cost savings, others zero or negative outcomes.The contract manufacturers regularly present positive figures. An ex post analysis at Ericssonof the transfer of a radio base product, which included the cost of the transfer process, yieldeda negative result. In the research literature too, it is a moot question if outsourcing reallyresults in cost savings, although many authors take this for granted, and several conflictingstudies have been presented. In this report it is not possible to present any precise figures.Instead we outline the main cost factors affecting the production of a radio base station andestimate their relative importance. The project related costs of industrialization and transfer tothird party suppliers are not included. Schematically the total unit cost could be divided intothe factors presented in Figure 3.

Profit

Value added

Standard material

Specific material

Figure 3. Schematically drawing of total unit cost

Purchased materials constitute the singularly most important cost factor, approximating70%-80% of total unit cost. It is often assumed that the large EMS-companies enjoy a costadvantage here. At a consolidated level the purchasing levels of Flextronics, for example, aremuch higher than those of Ericsson. Consequently, it is assumed that contract manufacturerswill benefit from lower component prices. This scale advantage is only relevant for a minorpart of the materials, however. The majority of all components are designed and specified bythe customer company (Nokia or Ericsson) for products. This means that the materials costsare already decided in the contracts which Nokia or Ericsson negotiate with these sub-suppliers. Thus, the purchasing discount enjoyed by contract manufacturers applies only to aminor part, approximately 20%-30%, of total materials costs. So even if the cost of standardmaterials could be lowered by 25%, which is a very optimistic assumption, total product costwould only be affected by 4-5 percentage points. By coordinating all its purchasing across thegroup, Nokia argues that they can reach very favorable agreements. The large Nokia Phonedivision supports Nokia Networks, and as a result ”nobody has better purchasing prices thanthe Nokia group”.

Ericsson expects the contract manufacturers to obtain advantageous price levels by relocatingto low cost countries and this is factored into its supply agreements. In this context it isimportant not to confuse economies of scale and economies of location. Relocation of TRU-manufacturing, for example, does not by itself reduce the price of purchased materials, which

17 (22)

is delivered from several different locations, (and also supply the original Ericsson plant). Itmight be argued that the international contract manufacturers could be in a stronger positionto entice their materials supplier to relocate and in this way build a more comprehensive baseof materials suppliers in low cost locations. The advantage of possible price reduction needsto be weighed against the potential loss of supply chain control as a result of the outsourcingprocess. Follow-up studies in 2002 comparing Ericsson plants and selected supplier sitesindicate that so far costs are approximately similar.

The costs of value-added are in the region of 20-25%. The principal components arepersonnel costs and capital costs for equipment and buildings. According to Nokia, theproduct-specific testing systems are the most expensive portion of the manufacturingequipment. The telecom manufacturer designs this equipment so the contract manufacturersenjoys no advantage of scale. Another production component is the SMD-lines (surfacemounting devices). This machinery commands the same prices worldwide, and low costcountries have no advantage. Contract manufacturers may achieve a higher capacityutilization by combining orders from several customers. Nokia´s strategy is to keep its ownhigh volume lines as busy as possible and shift excess order to its “capacity suppliers”.

Personnel costs are per definition lower in low cost countries, at least the labor costcomponent. Management costs are normally not lower, frequently the opposite is true. Inspecific cases (not referring to TRUs), Flextronics has offered to reduce labor costs by half bymoving from Sweden to Poland. The wage components when producing radio base station isinsignificant, however, normally lower than 10% of total unit cost. In an estimate of totaloutsourcing costs, this modest advantage needs to be balanced against the costs oftransferring knowledge, equipment and products to the contract manufacturers. Theconsultant firm Booz Allen Hamilton has estimated these costs to be in the range of 5%-10%of total product costs (Jackson et al., 2001); but arguably this level is highly dependent onactual production volumes.

Furthermore, some of the personnel costs consist of administration and services, not directlyinfluenced by outsourcing or location.

Finally, the contract manufacturers have to make their own profit on the outsourced products.

Taking all these factors together the cost advantages of outsourcing tend to be marginal atbest, calculated as the cost of the final product. Reduced prices for a minor part of materialspurchases, lower labor costs and maybe somewhat higher capacity utilization on the one hand,increased expenditures in terms of transfer costs, extended and more complicatedindustrialization and supplier margins on the other. For Ericsson an estimate by the authorsindicates a 5-10% reduction of total product cost, not including transfer costs, etc. Theestimate has been verified by cross-checking company internal studies. These studies havedemonstrated that the real costs of manufacturing at the EMS-firms tend to exceed contractedprices, when items such as capital costs paid for by Ericsson, general administrative expenses,etc. are corrected for. Follow-up studies have also pointed out that the calculations precedingthe outsourcing decisions tend to neglect the consequences for Ericsson units which continuemanufacturing some of the otherwise outsourced product. Because of reduced volume theseunits will suffer from a diseconomy of scale, and units costs will increase, sometimes so muchthat the entire justification of involving contract manufacturers falls apart. Generally, both theex ante and the ex post estimates performed by Ericsson and its consultants lack a dynamicperceptive, i.e. considerations of how and if learning effects and improvement potentials in itsown plants might offset the 5-10% cost difference in the static perspective.

18 (22)

Managers at Nokia Networks does not recognise the cost advantage in outsourcing all volumeproduction. Moreover they argue, “you cannot only look at costs, you have to look at theeffects on revenue, specifically on TTM” (Time to Market). If in the final analysisoutsourcing would reduce production costs, but at the same time imply delays in bringingproducts to the market, and consequently, to lost revenues, the bottom line would be a loss forthe company.

Also at Ericsson, the risks that outsourcing could negatively affect speed in the process ofbringing new products to the market would be well known. So far such considerations havehad no visible effects on the outsourcing decisions. Maybe they should. The experiences ofFlextronics taking over the entire phone manufacturing operations from Ericsson in 2001 donot support hypothesis of outsourcing and contract manufacturing as a way to enhance speedand responsiveness in the supply chain.

4.3 Industrialize without volume production? The problem of corecompetence

The Ericsson strategy for outsourcing spells out three technical core competencies for thecompany in the future (in addition to these there are of course also core competencies in thecommercials operations): product design, design of test equipment and industrialization ofnew products. By maintaining industrialization of key components and new systems in-house,Ericsson seeks to handle the important interdependencies between design and manufacturingstrategy (cf. Swink 1999). This presupposes that Ericsson also in the future is able to keep acritical mass of manufacturing knowledge as a basis for carrying out industrialization. In theunits recently designated for industrialization this is still the case, because of their earlierexperience of volume production, but this knowledge may have a short shell-life.

For the future there are theoretically two alternatives at Ericsson. The first implies asystematic way of organizing collaboration and knowledge exchange with external partnersduring the entire development process, from design to production ramp-up. Currently theEMS-firms are brought into this process very late. Managers and engineers at Ericsson thinkof themselves more as teachers than as pupils in these relations, but this attitude would haveto change. This first alternative is no easy route. Recently published research hasdemonstrated the difficulties for a customer firm with no production of its own to absorb andmake good use of a supplier’s manufacturing skills (Veugelers & Cassiman 1999). Thesecond alternative is to keep enough production operations within Ericsson so as to maintain acritical knowledge mass. This alternative is congruent with theoretical analyses of corecompetencies as systemic, emphasizing the critical links between product and processknowledge. The espoused strategy of outsourcing all volume production, and bringingcontract manufacturers into the development process only at a late stage, makes it less thanclear how Ericsson will manage these interdependencies.

At Nokia, too, the production and outsourcing strategy is justified by arguments concerningcore competence, and the relationship between critical competence elements. Thus, onerationale for keeping volume production in-house, apart from cost and revenue considerations,is the importance of maintaining a high skill level in manufacturing, and be able to feedbackexperiences directly from mass production to designers and product engineers. Anothercompetence argument refers to the close interrelations between production andindustrialization skills, and to the need for Oulu as a master plant to devise comprehensiveproduction concept, which can be transferred to off-shore production sites. Furthermore,

19 (22)

Nokia managers view advanced production knowledge as an important element in themanagement of the entire supply chain.

At the Ericsson industrialization unit in Gävle, there is an awareness of the importance ofmanufacturing knowledge. Said by a member of the management team: ”Today we still havethe knowledge and skills needed to set-up efficient, high-quality (volume) production.However, we don´t know how the outsourcing will affect our future industrialization skills.And maybe it will be hard to assess and select suppliers when we don’t have the relevantproduction skills in-house any more.”

To preserve and update a sufficient base of manufacturing knowledge, it is now proposed thatGävle continue volume production of each new product for a short period after the officialindustrialization process is concluded. (In figure 2 this is referred to by the acronym NPI-volume). Such ”NPI-volumes” could both act as capacity regulators and as a strategic sourceof production knowledge.

This solution, however, begs the question how to synchronize new production processes atEricsson and the corresponding processes at the contract manufacturers. The risk of a doubleindustrialization process is still very real. There is a potential conflict between an emphasis oninvesting in resources for maintaining in-company industrialization skills and an emphasis onexploiting the skills of the contract manufacturers in arranging standardized manufacturingprocesses. Given the outsourcing strategy the dilemma is: Should Ericsson let go of newproducts at an earlier stage in the industrialization process, and risk harming the informalknowledge exchange between product and process engineers needed to increase productionyield? Or would it be a better option invest more resources in the internal industrializationprocess, including some high volume production, but incur possibly substantial costs formaintaining knowledge and capacity and still not solve the problem of a “doubleindustrialization”?

4.4 Learning from Nokia or Ericsson?

Summing up, it could first be stated that both Nokia and Ericsson argue that out-sourcing andcooperation with third party suppliers are necessary, but secondly, that their specific strategiesdiffer in important aspects.

• Ericsson views far-reaching outsourcing and sell-off of production as a key measure toincrease flexibility and reduce risk exposure. At Nokia, it is argued that forecasting is moreimportant than outsourcing, citing Cisco as a “teaching case”. Cisco prided itself of being avirtual company with practically no manufacturing of its own. Nevertheless, when thetelecom boom ran out of juice in early 2000, the Californian corporation suddenly had towrite of 2 billion USD in inventories. “If there are excess stocks somewhere in the deliverychain it´s a question about uncompetitiveness of the whole chain”, is the Nokia argument.

• Expected cost reductions are the key driver for outsourcing decisions at Ericsson. If theseexpectations come true, and to what extent, is open to argument. Interviewed in early 2002,managers at Nokia Networks did not see any cost advantages by outsourcing moreproduction. Looking at the revenue side, it was pointed out that too much outsourcingcould result in product delays and lost sales.

20 (22)

• The modes of outsourcing at the two Nordic companies differ significantly. Ericssonapplies a vertically divided model, where volume production in principle is to be carriedout by contract manufacturers. The Oulu way of outsourcing could be described as ahorizontally integrated model, where Nokia is still responsible for strategic componentsand the final product during its entire product life.

The introduction to this report referred to arguments popular among consultants and the EMS-firms that outsourcing represents the future of the industry. From this perspective Nokia isconstrued as a laggard compared to Ericsson. This report supports the opposite view that thereis no one best way of organizing development and production in turbulent high-techindustries. Nokia represents a healthy reminder that there is a different way of achieving bothcost efficiency and speed. The argument about forecasting as a key success factor is notentirely convincing, however. Rather, the strategic challenge is how to increase theresponsiveness and flexibility of the production system in its entirety without incurringuncompetitive costs.

Integrating production and development competencies is a long-term strategy at Nokia. Onekey aspect is the decision to maintain responsibility for design, production and logistics ofstrategic components and products in Oulu. This reduces the extent of organizationalinterfaces and simplifies product transfers after industrialization. But some difficult interfacesdo remain, for example in relation to the company´s capacity suppliers. At the same time,selected suppliers are made responsible for their parts including design for manufacturealready in the design phase. This implies a high dependency on suppliers and their input andpresupposes effective ways of coordination and control by the product owner. The Nokiastrategy furthermore does not preempt future production and supply decisions. By keepingvolume manufacturing in its own plants both insourcing and outsourcing are viable futureoptions.

During the 1990s, the Nordic area emerged as an internationally leading telecom region, onthe back of advanced user, operators and manufacturers. Cooperation and competitionbetween user-developers and manufacturer-developers, and between manufacturers played animportant role for achieving this outstanding position (Berggren & Laestadius 2002).Competition between Ericsson and Nokia has been cut-throat, but in strategic standardizationissues three has also been a productive cooperation. In this period of unprecedented crisis inthe international telecom industry, it might be an advantage for both companies if competitionin the market-place could be combined with more openness and exchange in themanufacturing area, to safeguard Nordic production competencies and a competitiveproduction base.

21 (22)

REFERENCES

Interviews

Anders Wennberg, Manager Sourcing, Ericsson Radio Systems, Gävle

Bo Westerberg, Vice President, Corporate Sourcing, Ericsson, Kista

Gunnar Herdin, Manager, NPI and TPI projects, Ericsson Radio Systems, Gävle

Hemmi Piirainen, General Manager, Manufacturing Partnering, Product Operations, Nokia

Networks, Oulu

Jan Hedlund, Swedish Metal Workers´ Union, Kista

Jyrki Ali-Yrkkö, ETLA, Helsinki

Kari Sairo, The Finnish Metal Workers' Union, Helsinki

Karin Swärd-Hertel, Manager Business Development, Ericsson Radio Systems, Gävle

Magnus Bergqvist, Manager Technology, Ericsson Radio Systems, Gävle

Raimo Lovio, Researcher, VTT Technical Research Centre of Finland

Mats Lundin, General Manager, RBS Supply, Ericsson Radio Systems, Kista

Pekka Pesonen, Senior Manager, Strategic Planning, Nokia Mobile Phones, Operations,Logistics and Sourcing

Risto Lehtilahti, Nokia Networks, Oulu

Tommy Nejderyd, Manager Main Planning, Ericsson Radio Systems, Gävle

Åke Svenmarck, The Swedish Association of Graduate Engineers (CF), Kista

Literature

Ali-Yrkkö, J et al. (2000). Nokia – a big company in a small country. Helsingfors: TaloustietoOy.

Ali-Yrkkö, J. (2001). Nokia´s Networks - gaining competitiveness from co-operation.Helsingfors: Taloustieto Oy.

Arnold, U. (2000). New dimensions of outsourcing: a combination of transaction costeconomics and the core competencies concept. European Journal of Purchasing &Supply Management, 6, 23-29

Bengtsson, L. & Berggren, C. (2002). Horisontellt kopplad eller vertikalt klippt? Tvåmotsatta strategier för outsourcing. En jämförelse av radiobasverksamheten inomNokia och Ericsson. Working paper. Gävle: Högskolan i Gävle.

Bengtsson, L. (2001). Outsourcing av produktion och dess betydelse för innovations- ochförnyelseförmågan. Projektbeskrivning till Vinnova. Gävle: Högskolan i Gävle.

Bengtsson, L & Berggren, C. (2001). Produktionens förändrade roll. Mager klickfunktioneller kunskapsfabrik? I Backlund, T et al. (red.). Lärdilemman. Lund: Studentlitteratur.

Bengtsson, L. Niss, C. Stjernstöm, S. & Westin, S. (2002). The Challenge of MaintainingNew Product Manufacturability when Outsourcing Volume Manufacturing. Paper to bepresented at CINet2002, Espoo, September.

22 (22)

Berggren, C. & Bengtsson, L. (2000). Kunskapsfabriken. Stockholm: SvenskaMetallindustriarbetarförbundet.

Berggren, C. and S. Laestadius. (2002). Co-development and Composite Clusters - theSecular Strength of Nordic Telecommunications. Accepted for publication by Industrialand Corporate Change, no. 5.

Brown, S., Lamming, R., Bessant, J. & Jones, P. (2000). Strategic Operations Management.Oxford: Butterworth-Heinemann.

Corswant, F. & Fredriksson, P. (2002). Sourcing trends in the car industry. A survey of carmanufacturers’ and suppliers’ strategies and relations. International Journal ofOperations & Production Management, Vol. 22, No. 7, pp. 741-758.

Ericsson. Annual report (2001) and Ericsson (2000), Form 20-F, access: www.ericsson.comHayes, R.H. & Schemmer, R.W. (1978). How Should You Organize Manufacturing. Harvard

Business Review, 56 (19), pp. 106-118.Häikiö, M. (2002). Nokia. The Inside Story. Financial Times. Prentice Hall.Jackson, T., Iloranta, K. & McKenzie, S. (2001). Profits of Perils? The Bottom Line on

Outsourcing. Booz Allen Hamilton. Inc.Nokia. Annual report (2000) and Nokia (2001), Form 20-F, access: www.nokia.comPfeffer, J. & Sutton, R.I. (2000). The Knowing-Doing Gap. Boston: Harvard Business School

Press.Ramaswamy, R. & Rowthorn, R. (2000). Does Manufacturing Matter? Harvard Business

Review, November–December, 32.Shi, Y. & Gregory, M. (1998). International manufacturing Networks – to develop global

competitive capabilities. Journal of Operations Management, 16 (2,3), pp. 195-214.Swink, M. (1999). Threats to new product manufacturability and the effects of development

team integration processes. Journal of Operations Management, 17, 691–709.The Outsourcing Institute. (2001). Executive Survey. The Outsourcing Institute´s Annual

Survey of Outsourcing End Users. http://www.outsourcing.com. Access 2001-02-09.Veugelers, R. & Cassiman, B. (1999). Make or buy in innovation strategies: evidence from

Belgian manufacturing firms. Research Policy, 28, p. 63-80.VI (1999). Nya industriella system. OH-material. Stockholm: Sveriges Verkstadsindustrier.