homeowners description -2015 5/2015 ho - 5 standard coverage descriptions - section ii personal...

TRANSCRIPT

FMIC 5/2015 HO - 0

HOMEOWNERS PROGRAM

RULES/UNDERWRITING GUIDELINES Page Standard Amounts of Coverage HO - 1 Perils Insured Against HO - 1 Eligible List HO - 2 Consideration List - Submit Non-Bound HO - 2 Prohibited List - Do Not Submit HO - 2 Description of Coverage HO - 3 Special Limits of Liability HO - 3 Coverage E – Additional Coverages HO - 4 Personal Liability HO - 5 Farmette HO - 5 Optional Coverages – Section I – Property HO – 6 & 7 Optional Coverages – Section II – Liability HO - 7 DESCRIPTION OF RULES & RATES OF HOMEOWNERS PROGRAMS Homeowner Miscellaneous Rates HO - 7RA Homeowner Rate Formulas HO - 7RB Class A – 75 Homeowner Rules HO - 8 Class A – 75 Homeowner Rates HO - 8R Class A – 50 Homeowner Rules HO - 9 Class A – 50 Homeowner Rates HO - 9R Class B – 50 Homeowner Rules HO - 10 Class B – 50 Homeowner Rates HO - 10R Class C – 50 Homeowner Rules HO - 11 Class C – 50 Homeowner Rates HO - 11R Homeowner Contents Rules HO - 12 Homeowner Contents Rates HO - 12R

This page is left blank for future use.

FMIC 5/2015 HO - 1

HOMEOWNERS DESCRIPTION HOMEOWNERS POLICY STANDARD AMOUNTS OF COVERAGE – SE CTION 1 Coverage Homeowners Tenant – (HO-4) A - Dwelling Amount of Insurance NA B - Other Structures 10% of Coverage A NA C - Personal Property 75% of Coverage A Amount of Ins. on Class A-75 50% of Coverage A on Class A-50, B & C D - Loss of Use 20% of Coverage A 20% of Cov. C (HO4) L - Personal Liability Various Limits Available M - Medical Payments Various Limits Available PERILS INSURED AGAINST Group 1 - Basic Perils . Fire or Lightning . Removal . Windstorm or Hail . Explosion . Riot and Civil Commotion . Aircraft . Vehicles . Vandalism & Malicious Mischief . Smoke Group 2 - Broad Forms Perils . Theft . Sudden and Accidental Tearing Apart of Heating Systems . Freezing of a Plumbing, Heating or Air Conditioning System . Falling Objects . Weight of Ice, Snow or Sleet . Collapse . Breakage of Glass . Sudden and Accidental Damage from Artificially Generated Electrical Current . Accidental Discharge or Overflow of Water or Steam Group 3 - Other Perils Other Perils covers property described in Coverage A and B against other risks of physical loss, with certain exceptions.

FMIC 5/2015 HO - 2

HOMEOWNERS UNDERWRITING GUIDELINES ELIGIBLE LIST The Insured may be: . Owner/Occupant of a one to three family dwelling . Tenant of an apartment, dwelling, condominium. CONSIDERATION LIST - Submit Non-Bound The following risk may not be bound by the Agent. Submit to the Company for Underwriting approval: . Premises with questionable unsafe characteristics. . Premises with visible trash and debris that can be removed or cleaned. . Vacant dwellings with future occupancy contemplated. . Unfenced or inadequately fenced swimming pools. . Open pits or stone quarries on the insured location. . Three losses in five years. . Homes being remodeled or with unrepaired damage. . Homes without continuous masonry foundation. . Home Day Care Operations with four or more children. . More than four rental units for any one Insured. PROHIBITED LIST - Do Not Submit The following risks are PROHIBITED: . Commercial risks. . Insureds with known vicious animals. . Rental dwellings containing more than three family units. . Homes heated primarily with woodburning appliances. . Homes without interior plumbing. . Breeding, raising and selling of dogs on the premises. . Insureds with known claim frequency (more than three losses in five years). . Homes with more than two mortgagees. . Homes with more than two roomers or boarders. . Horse stables and training operations. . Insured that has a bankruptcy or under bankruptcy proceedings. . Log Homes. . Insured that has been convicted of a felony. See liability section of manual for the list of those not eligible for Personal Injury coverage.

FMIC 5/2015 HO - 3

STANDARD COVERAGE DESCRIPTIONS - SECTION I Coverage A - Dwellings Covers Dwelling on insured location, including attached structures. Coverage B - Other Structures Provides coverage for other structures on the residence premises set apart from the dwelling by a clear space. This does not include structures used for business, farming, or rented to others. Coverage C - Personal Property Covers personal property owned or used by an Insured. The limit of liability for personal property usually located at an insured’s residence, other than the residence location is 10% of the limit of liability for Coverage C, or $1,000 whichever is greater. Students occupying an apartment, rooming house or dormitory room are considered to be temporarily away from the insured location. Coverage for personal property is limited to 10% of the Personal Property coverage of the parent's policy. (This applies if the student is still a member of the parents' household. Some restrictions apply to theft.) Special Limits of Liability $200 Money, Bank Notes, Bullion, Gold, Silver, etc. $1,000 Securities, Accounts, Deeds, Passport, Stamps, etc. $1,000 Watercraft including their trailers, furnishings, equipment and outboard motors. $1,000 On Trailers not used with watercraft. $1,000 On Gravemarkers $1,000 For loss by theft of Jewelry, Watches, Precious & Semi-Precious Stones, Furs, etc $2,000 For loss by theft of Firearms. $2,500 For loss by theft of Silverware, Silver & Gold Plated Ware, etc. $2,500 On Business Property on Insured location. $250 On Business Property off Insured location. $500 Recreational Motor Vehicles. $500 Dismounted Camper Bodies. $200 Detached Tires. $1000 On devices/accessories used to transmit sound or picture which could be connected to a motor vehicle, etc., while in or on the vehicle etc. Coverage D – Additional Living Expense Covers reasonable increase in living expense necessary to maintain the Insured's normal standard of living while the Insured lives elsewhere following a covered loss, until the residence location is repaired or replaced, or the Insured permanently relocates.

FMIC 5/2015 HO - 4

STANDARD COVERAGE DESCRIPTIONS - SECTION I Coverage E - Additional Coverages Refer to the policy for specific coverage availability. a. Trees, Shrubs, Plants and Lawns Covers up to 5% of Coverage A - Dwelling not to exceed $1,500 for damaged trees, shrubs, plants or lawns, caused by specific perils as outlined in the policy. Up to $300 will be paid on any one item. Items grown for business or farming purposes are excluded. Coverage is limited to 250 feet of the Insured dwelling. b. Debris Removal

Provides an additional 5% of the Limit of Liability (up to $5000) per occurrence for debris removal. We also pay a reasonable expense not to exceed $200.00 for the removal of trees from the residence location felled by wind. See policy for restrictions and limitations on certain items.

c. Credit Card, Forgery, etc. (Applicable only if we provide coverage under Coverage C, Personal Property). Covers up to $1,000 per occurrence for the legal obligation of an Insured to pay because of theft or unauthorized use of any credit card or fund transfer card issued to an Insured. No deductible applies. d. Fire Department Service Covers up to $500 per occurrence for Insured's liability under a contract or agreement when a Fire Department is called to protect the insured property from perils insured against. No deductible applies. e. Refrigerated Products Covers up to $500 for loss or damage to insured contents (Coverage C) of a freezer or refrigerated unit on the insured location. The loss or damage caused by change in temperature must result from: Interruption of electrical service by utility company, mechanical or electrical breakdown of the refrigeration system or accidental interruption of electrical service. No deductible applies. f. Reasonable Repairs Covers necessary repairs made solely to protect covered property from further damage following an insured loss.

FMIC 5/2015 HO - 5

STANDARD COVERAGE DESCRIPTIONS - SECTION II

PERSONAL LIABILITY Liability coverage is provided by Rockford Mutual Insurance Co. Personal Liability Basic Coverage includes: . Bodily Injury & Property Damage . Medical Payments . Damage to Property of Others Various limits are available for Comprehensive Personal Liability and Medical Payment, see the liability section of the manual.

FARMETTE FARMETTE ENDORSEMENT With the popularity of the homeowner purchasing small acreages in the country including parcels of land with farm buildings, it is important that you, as Agent, have the opportunity to remain competitive and yet maintain the proper Company underwriting approach. Many rural homeowners are raising livestock for their own consumption, planting large vegetable gardens, and own a few pieces of farm equipment which are not used in a farming operation. The ownership of horses is also popular. As a result of the above, it is important that you, as Agent, be aware of the following underwriting practice that will be fair to both the Insured and Company. Dwellings that are not used in connection with a farming operation may qualify for a Home Protector Policy. Any outbuilding originally constructed for farming purposes must be insured as a farm outbuilding using applicable rates from the farm section of the Agent's Manual. These buildings are not to be insured under the Auxiliary Private Structure coverage. Since maintenance and utility value of these outbuildings tend to be limited or very low, caution should be given to either declining coverage or accepting only at a Class C or D rate. Blanket Farm Personal Property is not acceptable. Use Scheduled Farm Personal Property classification for any livestock or equipment. Farmette liability is to be added when there is minimal farm exposure. If insured is involved in a farming operation, coverage must be on a farm policy. See liability section of manual or contact Forreston Mutual's home office for clarification.

.

FMIC 5/2015 HO - 6

OPTIONAL COVERAGES: SECTION I - PROPERTY COVERAGE B - AUXILIARY PRIVATE STRUCTURES Auxiliary Private Structures coverage is intended for structures which serve the dwelling, including garages, utility buildings, dog houses, etc. Any building which was originally constructed for farming purposes should not be an A.P.S. Those type buildings should be insured as farm outbuildings using applicable rates from the farm section of the Agent's Manual. . For increased A.P.S. limits - rate the amount of increased insurance per $100. COVERAGE C - PERSONAL PROPERTY Increased limit: . When the limit of liability for Coverage C is increased, the additional premium per $100 shall be used. Reduction in Limit: Not allowed. Replacement Cost - Loss Settlement 4 . Personal property may be extended to include replacement cost coverage. The rate is 10% of the base premium (after discounts). Antiques, fine arts, statuary and other similar articles are not eligible for the coverage. COVERAGE D - ADDITIONAL LIVING EXPENSE Increased Limit: The amount of insurance for A.L.E. may be increased. Use the rate per $100. REFRIGERATED PRODUCTS The Home Protector and Tenant programs automatically provide $500 coverage for Refrigerated Products. An additional amount may be purchased using the Refrigerated Products rate. SUMP PUMP FAILURE OR WATER BACKUP OF SEWERS OR DRAINS (FMIC 99-001) Sump Pump failure or water backup of sewers or drains provides coverage for direct loss to the property described caused by water which backs up through sewers or drains, or water which enters into and overflows from within a sump pump or sump pump well. This coverage does not apply: a. If the loss is caused by the negligence of any Insured. b. If the loss occurs or is in progress: (1) Five days after the effective date of this coverage, if added at the inception date or renewal date of this policy. Coverage is available in increments of $1000. A flat $250 deductible per occurrence will apply. This coverage is not available for dwellings that have had problems with this type of damage in the past unless action has been taken to eliminate the problem.

FMIC 5/2015 HO - 7

IDENTITY FRAUD EXPENSE (FMIC-010) This optional endorsement can be purchased to provide $5,000.00 coverage for an insured’s expense arising out of an occurrence of identity fraud. EQUIPMENT BREAKDOWN COVERAGE (FMIC-011) This optional endorsement can be purchased to add coverage for physical damage to specified types of covered property that occurs as a result of an equipment breakdown accident. MINE SUBSIDENCE & EARTHQUAKE Refer to the sections in this manual for rates and underwriting guidelines.

OPTIONAL COVERAGES SECTION II - LIABILITY The following optional coverages are offered by Rockford Mutual and can be attached to Forreston Mutual policies. See the "Farm and Personal Liability" section of the Manual for underwriting rules and rates. a. ADDITIONAL INSURED (RMIC 99-7001, RMIC 99-7002, & RMIC 99-7003) b. ADDITIONAL RESIDENCE OCCUPIED BY INSURED c. RENTAL DWELLINGS (RMIC 99-414 & DL 24 11) d. DWELLING PREMISES OLT (RMIC 99-414 & DL 24 11) e. PERSONAL INJURY (RMIC 99-8077) f. INCIDENTAL BUSINESS PURSUITS (99-420) g. HOME DAY CARE, ONE TO THREE CHILDREN (RMIC 99-192) h. WATERBED LEAKAGE LEGAL LIABILITY (RMIC 99-416) i. FARMETTE LIABILITY (RMIC 99-411) j. FARMS RENTED TO OTHERS (RMIC 99-406) k. RECREATIONAL UNITS (RMIC 99-8022 Watercraft Owners Endorsement) (RMIC 99-8023 Recreational Vehicles Owners Endorsement)

Forreston Mutual Insurance Co. Homeowner Miscellaneous Rates Effective 5/2015

Policy Fee $40Minimum Premium Per Policy $50

Personal Property Replacement Cost 10% of the base premium (after discounts)

Unscheduled Personal Property - Additional 13¢ per $100 of insurance

Auxiliary Private Structures - Additional 40¢ per $100 of insurance(Not Farm)

Additional Living Expense 30¢ per $100 of insurance

Fire Department Service Charge - Additional $1.00 per $100 of insurance

Refrigerated Products - Additional $1.00 per $100 of insurance

Sump Pump Failure/Backup of Sewers or Drains $20.00 per $1000 coverage with flat $250 deductible.

Identity Fraud Expense $5,000.00 Coverage $12.00 Flat Premium

Builders Risk 70% of Class B Rental Rate

Earthquake See Earthquake section of this manual

Mine Subsidence See Mine Subsidence section of this manual

Boat Docks Class C Outbuilding Rate

A replacement cost estimator is to be completed on all dwellings. For rating purposes, a maximum of 50% depreciation will be taken on Class B&C. If insured for less than that amounta $35.00 surcharge will apply.

HO-7RA

Forreston Mutual Insurance Co. HOMEOWNER RATES Effective 5/2015

Use these town rates to calculate premiums for coverage amounts not shown on the premium pages.

THESE ARE BASE RATES FOR $500 DEDUCTIBLE. OTHER DEDUCTIBLES ARE SUBJECT TO DEDUCTIBLE FACTOR SHOWN BELOW.

Policy Type

Special 100 $100,000 + .2690 + 5.21 .2716 + 6.89 .3488 + 5.99 .1422 + 5.82Class A-75 $ 70,000 + .2259 + 0.00 .2509 + 0.00 .2928 + 5.32 .1785 + 6.36Class A -50 Repair $ 60,000 + .2591 + 0.00 .2877 + 0.00 .3667 + 9.93 .2640 + 7.15Class B - 50 $ 40,000 To 49,999 .2301 + 0.00 .2558 + 0.00 .3196 + 3.97 .2679 + 7.56

$ 50,000 To 69,999 .2301 + 0.00 .2558 + 0.00 .3196 + 2.99 .2679 + 7.56$ 70,000 + .2301 + 0.00 .2558 + 0.00 .3196 + 0.00 .2679 + 7.56

Class C - 50 $ 20,000 + .4089 + 4.74 .4089 + 5.23 .4856 + 4.98 .3973 + 19.39Contents (Tenant HO) $ 10,000 + .2991 + 0.00 .3323 + 0.00 .4474 + 4.74 .1511 + 10.30

Ded. FactorCalculate the premium for $500 $ 0 2.16 POLICY FEE $40.00deductible using the rates above, then $ 100 1.73multiply by the appropriate factor to $ 250 1.31calculate the premium for other $ 500 1.00deductibles. $ 1,000 0.88

$ 2,000 0.80$ 3,000 0.72$ 5,000 0.68

Terr. FactorSee Page 13 in the General Section 20 1.00for a list of Territories by County 21 1.07

22 1.1023 1.1224 1.1625 1.25

FPC 1-5Fire

FPC 6-8

HO-7RB

Deductible Factors

Territory Factors

Base Rate Per $100 Coverage

Owner Occupied DwellingsCoverage Amount Fire

FPC 9-10WindFire

FMIC 5/2015 HO - 8

DESCRIPTION OF HOMEOWNER PROGRAMS/ELGIBILITY

CLASS A-75 HOMEOWNER

Perils Available Loss Settlement Types Available

Basic Perils Actual Cash Value Broad Form Perils 80% Replacement Cost Other Perils Standard Amounts Min. Amount of Ins. Max. Binding Authority of Coverage

$70,000 $300,000 HHG - 75% of Cov. A APS - 10% of Cov. A ALE - 20% of Cov. A Replacement on HHG is included at no additional charge.

Eligibility Requirements: Dwelling construction year 1975 or newer.

a. Dwelling and detached structures of superior character and excellent repair. Premises clean; free from weeds and trash. Continuous masonry or concrete foundation under all exterior walls, (porches excepted).

b. Residence must have an approved roof, central furnace, wiring and plumbing all 35 years of age or less, or updated within the last 35 years. Must meet local building codes and

building contractor inspection. Wood burning appliance must be UL approved.

c. Owner-occupied, one or two family permanent residence.

d. When insured for replacement cost the dwelling must be insured for 80% of the replacement value. When insured for actual cash value (ACV) the dwelling must be insured for a minimum of the ACV which can not be less than 60% of the replacement cost. Inflation factor will apply. Other Perils not available on ACV policy.

e. 100-amp electrical service, updated within the last 35 years.

f. Complete interior plumbing, being a permanent pipe system supplied by water from a continuous reliable source.

g. Smoke detector on each floor including basement.

h. Cost estimator and photographs (front & rear) submitted with application.

i. Modular homes not permitted.

j. Readily accessible to a fire truck.

Forreston Mutual Insurance Co. Town A-75 Homeowner Effective 5/2015

$1000 Deductible $2000 Deductible $3000 DeductibleAmount of FPC FPC FPC FPC FPC FPC FPC FPC FPCCoverage 1-5 6-8 9-10 1-5 6-8 9-10 1-5 6-8 9-10

70000 254 270 300 231 246 273 208 221 24571000 258 274 304 234 248 276 211 224 24972000 262 278 309 238 253 281 214 227 25373000 266 282 314 242 256 285 218 231 25774000 268 285 316 244 259 288 219 233 25975000 272 288 321 247 262 292 223 236 26376000 276 293 326 252 267 296 226 240 26677000 280 297 330 254 269 300 229 243 27078000 283 300 334 258 274 304 232 246 27379000 286 303 338 260 276 308 234 249 27780000 290 308 342 264 280 311 237 252 28082000 298 316 351 270 287 318 243 258 28684000 304 323 358 277 294 326 249 264 29386000 312 331 367 283 301 334 255 271 30088000 318 337 374 289 307 340 260 276 30690000 326 346 384 296 315 349 266 283 31495000 344 364 404 313 331 367 282 298 331

100000 362 384 425 329 349 386 296 314 348105000 380 402 446 345 365 405 311 329 365110000 397 422 467 360 383 424 325 345 381115000 416 441 488 378 401 444 340 361 399120000 432 459 508 394 418 463 354 376 416125000 450 478 528 409 434 480 368 391 432130000 468 496 549 425 451 499 383 406 449135000 485 515 570 442 469 519 398 422 467140000 503 534 590 458 486 537 412 437 483145000 522 553 611 474 503 556 427 453 501150000 539 572 633 490 520 575 441 468 517155000 557 591 653 506 537 593 456 484 534160000 575 610 674 523 555 613 470 499 551165000 593 629 694 539 572 631 486 515 568170000 611 649 716 555 590 650 499 530 585175000 629 667 737 571 606 669 514 546 603180000 647 687 757 588 624 688 529 561 619185000 665 705 778 604 641 708 544 577 637190000 682 724 799 620 659 727 558 592 654195000 700 742 819 636 674 744 573 607 670200000 717 761 839 652 692 763 586 622 687205000 734 779 860 668 709 783 601 638 704210000 752 799 881 684 727 801 615 653 720215000 771 817 902 701 743 820 631 669 738220000 788 837 922 717 761 838 645 684 754225000 806 856 943 732 778 857 660 701 772230000 825 875 965 750 796 877 674 715 789235000 842 894 985 766 813 895 689 732 806240000 860 913 1006 782 830 914 703 746 823245000 878 932 1027 797 847 933 718 763 841250000 896 951 1048 814 864 952 733 777 857255000 914 970 1069 831 882 972 748 794 874260000 931 988 1089 846 898 990 761 807 890

HO-8R

Fire + Wind Premium

FMIC 5/2015 HO - 9

DESCRIPTION OF HOMEOWNER PROGRAMS/ELIGIBILITY CLASS A-50 REPAIR HOMEOWNER Perils Available Loss Settlement Types Available Basic Perils Loss Settlement Clause 3 Special Repair/Replacement Cost Broad Form Perils With Commonly Used Building Material Standard Amounts Min. Amount of Ins. Max. Binding Authority of Coverage $60,000 $300,000 HHG - 50% of Cov. A APS - 10% of Cov. A ALE - 20% of Cov. A Replacement on HHG is included at no additional charge. Eligibility Requirements: a. Dwelling of good construction and in good repair. Premises clean; free from weeds and

trash. Continuous masonry or concrete foundation under all exterior walls, (porches excepted).

b. Residence must have an approved roof, furnace, wiring and plumbing all 35 years of age or less, or updated within the last 35 years. Must meet local building codes and building contractor inspection. Wood burning appliance must be UL approved. c. Owner-occupied, one to three family permanent residence. d. Insured for at least 50% of replacement cost. Inflation factor will apply.

e. 100-amp electrical service, updated within the last 35 years. f. Complete interior plumbing, being a permanent pipe system supplied by water from a continuous reliable source. g. Smoke detector on each floor including basement. h. Cost estimator and photographs (front & rear) submitted with application. i. Readily accessible to a fire truck.

Forreston Mutual Insurance Co. Town A-50 Repair Homeowner Effective 5/2015

$1000 Deductible $2000 Deductible $3000 DeductibleAmount of FPC FPC FPC FPC FPC FPC FPC FPC FPCCoverage 1-5 6-8 9-10 1-5 6-8 9-10 1-5 6-8 9-10

60000 282 298 348 257 271 317 232 245 28661000 287 302 354 260 274 321 235 247 28962000 292 307 359 266 279 327 239 251 29463000 295 311 364 268 283 331 242 255 29964000 301 317 371 274 288 337 247 259 30365000 306 323 376 277 293 341 250 264 30866000 309 326 381 282 297 347 253 267 31167000 315 332 387 286 301 352 257 271 31668000 320 337 393 291 307 357 262 276 32169000 324 341 397 294 310 361 265 279 32570000 328 346 404 299 315 368 268 283 33072000 338 355 414 308 324 377 277 291 33974000 348 366 426 316 332 387 284 299 34876000 356 376 437 324 341 397 292 308 35878000 365 384 447 332 349 407 298 314 36680000 374 394 459 340 358 416 306 323 37585000 398 420 487 362 382 444 325 343 39990000 421 444 515 382 403 468 344 362 42195000 443 467 542 403 424 492 363 383 444

100000 466 491 570 424 447 519 381 402 466105000 489 516 598 445 469 543 400 421 488110000 513 540 625 466 491 568 420 443 512115000 536 565 654 487 514 595 439 462 535120000 559 589 681 508 535 619 457 481 557125000 582 614 709 529 558 644 476 502 580130000 605 637 737 550 579 670 495 521 603135000 628 661 764 571 601 695 514 541 626140000 651 687 792 592 624 720 532 561 648145000 674 710 820 613 646 746 552 581 671150000 697 735 848 633 668 770 570 601 693155000 720 758 875 655 690 795 589 621 716160000 743 783 903 676 712 822 609 641 740165000 767 808 931 696 734 846 627 661 762170000 788 831 958 717 756 871 645 680 784175000 812 856 987 737 777 897 664 700 807180000 834 880 1014 759 800 922 683 720 829185000 858 904 1041 780 823 947 702 740 852190000 881 929 1070 801 845 973 720 760 875195000 903 953 1097 822 867 998 740 780 898200000 927 977 1125 842 888 1022 758 799 920205000 949 1001 1153 863 910 1048 777 820 944210000 974 1027 1181 885 933 1074 797 840 967215000 996 1051 1208 906 955 1098 815 860 989220000 1019 1074 1236 926 976 1124 833 879 1011225000 1042 1098 1264 947 999 1149 853 899 1034230000 1064 1123 1291 968 1021 1173 871 919 1056235000 1089 1148 1320 989 1043 1200 890 939 1080240000 1111 1171 1347 1011 1065 1225 910 959 1103245000 1135 1196 1375 1031 1087 1249 928 979 1125250000 1157 1220 1403 1052 1109 1276 947 998 1147

HO-9R

Fire + Wind Premium

FMIC 5/2015 HO - 10

DESCRIPTION OF HOMEOWNER PROGRAMS/ELIGIBILITY

CLASS B-50 HOMEOWNER Perils Available Loss Settlement Types Available Basic Perils Actual Cash Value Broad Form Perils 80% Replacement Cost Other Perils (45,000. Min. Cov.) Standard Amounts Min. Amount of Ins. Max. Binding Authority of Coverage $40,000 $300,000. HHG - 50% of Cov. A APS - 10% of Cov. A ALE - 20% of Cov. A Personal Property Replacement Cost charge is 10% of Base Rate. Eligibility Requirements: a. Dwelling of good construction and in good repair. Premises clean; free from weeds and

trash. Continuous masonry or concrete foundation under all exterior walls, (porches excepted).

b. Residence must have an approved roof, central furnace, wiring and plumbing. Must meet local building codes and building contractor inspection. Wood burning

appliance must be UL approved. c. Owner-occupied, one to three family permanent residence. d. When insured for replacement cost the dwelling must be insured for 80% of the

replacement value. When insured for actual cash value (ACV) the dwelling must be insured for a minimum of the ACV, which if less than 50% of the replacement cost a $35.00 surcharge will apply. Inflation factor will apply. Other Perils not available on ACV policy.

e. 100-amp electrical service updated within the last 40 years. f. Complete interior plumbing, being a permanent pipe system supplied by water from a continuous reliable source. g. Smoke detector on each floor including basement. h. Cost estimator and photographs (front & rear) submitted with application. i. Readily accessible to a fire truck.

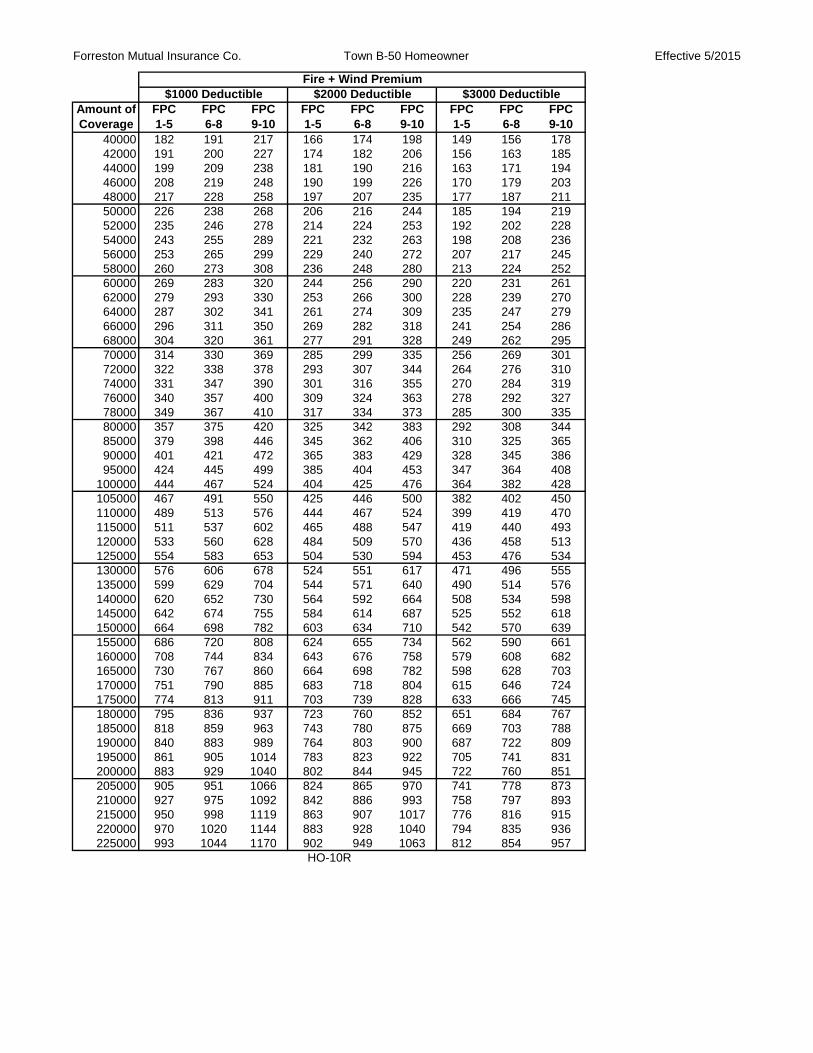

Forreston Mutual Insurance Co. Town B-50 Homeowner Effective 5/2015

$1000 Deductible $2000 Deductible $3000 DeductibleAmount of FPC FPC FPC FPC FPC FPC FPC FPC FPCCoverage 1-5 6-8 9-10 1-5 6-8 9-10 1-5 6-8 9-10

40000 182 191 217 166 174 198 149 156 17842000 191 200 227 174 182 206 156 163 18544000 199 209 238 181 190 216 163 171 19446000 208 219 248 190 199 226 170 179 20348000 217 228 258 197 207 235 177 187 21150000 226 238 268 206 216 244 185 194 21952000 235 246 278 214 224 253 192 202 22854000 243 255 289 221 232 263 198 208 23656000 253 265 299 229 240 272 207 217 24558000 260 273 308 236 248 280 213 224 25260000 269 283 320 244 256 290 220 231 26162000 279 293 330 253 266 300 228 239 27064000 287 302 341 261 274 309 235 247 27966000 296 311 350 269 282 318 241 254 28668000 304 320 361 277 291 328 249 262 29570000 314 330 369 285 299 335 256 269 30172000 322 338 378 293 307 344 264 276 31074000 331 347 390 301 316 355 270 284 31976000 340 357 400 309 324 363 278 292 32778000 349 367 410 317 334 373 285 300 33580000 357 375 420 325 342 383 292 308 34485000 379 398 446 345 362 406 310 325 36590000 401 421 472 365 383 429 328 345 38695000 424 445 499 385 404 453 347 364 408

100000 444 467 524 404 425 476 364 382 428105000 467 491 550 425 446 500 382 402 450110000 489 513 576 444 467 524 399 419 470115000 511 537 602 465 488 547 419 440 493120000 533 560 628 484 509 570 436 458 513125000 554 583 653 504 530 594 453 476 534130000 576 606 678 524 551 617 471 496 555135000 599 629 704 544 571 640 490 514 576140000 620 652 730 564 592 664 508 534 598145000 642 674 755 584 614 687 525 552 618150000 664 698 782 603 634 710 542 570 639155000 686 720 808 624 655 734 562 590 661160000 708 744 834 643 676 758 579 608 682165000 730 767 860 664 698 782 598 628 703170000 751 790 885 683 718 804 615 646 724175000 774 813 911 703 739 828 633 666 745180000 795 836 937 723 760 852 651 684 767185000 818 859 963 743 780 875 669 703 788190000 840 883 989 764 803 900 687 722 809195000 861 905 1014 783 823 922 705 741 831200000 883 929 1040 802 844 945 722 760 851205000 905 951 1066 824 865 970 741 778 873210000 927 975 1092 842 886 993 758 797 893215000 950 998 1119 863 907 1017 776 816 915220000 970 1020 1144 883 928 1040 794 835 936225000 993 1044 1170 902 949 1063 812 854 957

HO-10R

Fire + Wind Premium

FMIC 5/2015 HO - 11

DESCRIPTION OF HOMEOWNER PROGRAMS/ELIGIBILITY

CLASS C-50 HOMEOWNER

Perils Available Loss Settlement Types Available

Basic Perils Actual Cash Value Broad Form Perils Standard Amounts Min. Amount of Ins Max. Binding Authority of Coverage

$20,000. $300,000. HHG - 50% of Cov. A APS - 10% of Cov. A ALE - 20% of Cov. A

Personal Property Replacement Cost charge is 10% of Base Rate.

Eligibility Requirements:

a. Dwelling fully utilized and in a good state of repair. Premises clean; free from weeds and trash. Continuous masonry or concrete foundation under all exterior walls, (porches excepted).

b. Residence must have an approved roof, heating system, electrical wiring of at least 60 amp service and plumbing. Wood burning appliances must be UL approved.

c. Owner-occupied, one to three family permanent residence.

d. Insured for at least minimum of actual cash value. If insured for less than 50% of replacement cost, a surcharge of $35.00 will apply. Inflation factor will apply.

e. Complete interior plumbing, being a permanent pipe system supplied by water from a continuous reliable source.

f. Smoke detector on each floor including basement.

g. Cost estimator and photographs (front & rear) submitted with application.

h. Readily accessible to a fire truck.

Forreston Mutual Insurance Co. Town C-50 Homeowner Effective 5/2015

$1000 Deductible $2000 Deductible $3000 DeductibleAmount of FPC FPC FPC FPC FPC FPC FPC FPC FPCCoverage 1-5 6-8 9-10 1-5 6-8 9-10 1-5 6-8 9-10

20000 164 164 177 149 149 161 134 134 14422000 178 178 193 162 162 176 145 145 15824000 192 192 208 174 174 190 157 157 17126000 206 207 223 187 188 203 169 170 18328000 220 221 239 200 201 218 180 180 19630000 234 235 255 213 213 232 191 192 20932000 249 249 270 227 227 246 204 204 22134000 263 263 286 238 238 259 215 215 23336000 277 277 301 252 252 274 226 226 24738000 291 292 317 264 265 288 237 238 25940000 305 306 332 276 277 301 249 250 27142000 319 320 348 290 291 316 261 261 28444000 334 334 364 303 303 330 273 273 29846000 348 348 379 316 316 344 284 284 30948000 362 363 394 329 330 358 296 296 32250000 376 377 410 341 342 372 307 308 33652000 390 391 425 355 355 387 319 320 34854000 405 405 441 368 368 401 331 331 36056000 419 419 457 381 381 416 342 342 37358000 433 433 473 394 394 430 354 354 38760000 447 448 487 406 407 443 366 367 39962000 461 462 503 419 420 458 378 378 41264000 475 476 519 432 433 472 389 389 42566000 490 490 534 446 446 486 401 401 43768000 504 504 550 458 458 500 413 413 45070000 518 518 566 471 471 514 425 425 46372000 531 532 580 483 484 528 435 436 47674000 545 546 595 496 496 541 446 447 48776000 560 560 611 510 510 556 459 459 50078000 575 575 628 522 522 570 470 470 51380000 589 589 643 536 536 584 482 482 52682000 603 604 659 548 549 598 493 494 53884000 617 618 674 560 561 612 505 505 55186000 631 632 690 574 575 627 516 517 56588000 646 646 705 587 587 641 529 529 57790000 660 660 721 600 600 656 540 540 58995000 695 696 759 632 633 691 569 570 622

100000 731 731 799 665 665 727 598 598 654105000 767 768 838 697 698 762 627 628 686110000 801 801 875 729 729 796 656 656 716115000 837 837 914 761 761 831 685 685 748120000 872 872 953 793 794 867 713 714 780125000 908 908 993 826 826 903 744 744 813130000 944 945 1032 858 859 938 772 773 844135000 979 979 1071 891 891 974 801 801 876140000 1015 1016 1110 923 923 1009 830 831 908145000 1050 1050 1148 954 954 1043 859 859 938150000 1085 1086 1186 986 987 1078 888 889 971155000 1121 1121 1226 1019 1019 1114 917 917 1003160000 1156 1156 1264 1051 1051 1150 946 946 1035

HO-11R

Fire + Wind Premium

FMIC 5/2015 HO - 12

DESCRIPTION OF HOMEOWNER PROGRAMS/ELIGIBILITY TENANT PROTECTOR POLICY Standard Amounts Perils Available Loss Settlement Types Available of Coverage Basic Perils Actual Cash Value ALE - 20% of Cov. C Broad Form Perils Replacement Cost Contents Minimum Amounts of Insurance/Binding Authority: Minimum Maximum Policy Type Amount of Ins. Binding Tenant Homeowner $10,000 $75,000 Personal Property Replacement Cost charge is 10% of Base Rate. Eligibility Requirements: a. The Standard Tenant Homeowners policy provides coverage for tenants of apartments and rental dwellings. b. Under $10,000 coverage is available for landlords insuring contents in a rental dwelling.

Forreston Mutual Insurance Co. Homeowner Contents (Tenant HO) Effective 5/2015

$500 Deductible $1000 Deductible $2000 Deductible $3000 DeductibleAmount of FPC FPC FPC FPC FPC FPC FPC FPC FPC FPC FPC FPCCoverage 1-5 6-8 9-10 1-5 6-8 9-10 1-5 6-8 9-10 1-5 6-8 9-10

10000 55 58 74 48 51 65 44 46 59 40 42 5311000 60 64 81 53 57 72 48 52 65 43 46 5812000 64 68 86 57 60 76 51 54 68 46 49 6213000 69 73 93 60 64 81 55 58 74 50 53 6714000 73 78 98 64 68 86 59 63 79 52 56 7015000 78 83 105 69 73 92 62 66 84 56 60 7616000 82 87 110 72 77 97 65 69 88 59 62 7917000 87 92 117 77 81 103 70 74 94 63 66 8418000 91 97 122 81 86 108 73 78 98 66 70 8819000 96 102 129 84 89 113 77 81 103 69 73 9320000 101 107 135 89 94 119 81 86 108 73 78 9821000 105 112 141 92 99 124 84 90 113 75 80 10122000 110 117 147 97 103 130 88 93 117 80 85 10623000 114 121 153 101 107 135 91 97 122 82 87 11024000 119 127 159 104 111 140 96 102 128 86 92 11525000 123 131 165 108 115 145 98 104 132 89 95 11926000 128 136 171 113 120 150 102 109 137 92 98 12327000 132 141 177 116 124 156 106 113 142 95 102 12828000 137 146 183 121 129 161 109 116 146 98 105 13229000 141 150 188 125 132 166 113 120 150 102 108 13530000 146 156 195 128 137 171 117 125 156 105 112 14031000 150 160 200 132 141 176 120 128 160 108 115 14432000 155 165 207 136 145 182 124 132 165 111 118 14933000 159 170 212 140 150 187 127 136 170 114 122 15234000 164 175 219 145 154 193 132 140 176 118 126 15835000 168 179 224 147 157 197 134 143 179 121 129 16136000 173 185 231 152 163 203 138 148 185 125 133 16737000 177 189 236 156 166 208 142 151 189 128 137 17038000 182 194 243 160 171 214 145 155 194 131 140 17539000 186 199 248 164 175 219 149 159 198 134 144 17940000 191 204 255 168 179 224 153 163 204 137 147 18341000 195 208 260 171 183 228 156 167 208 141 150 18742000 200 214 267 176 188 235 160 171 213 144 154 19243000 204 218 272 180 192 239 163 174 218 147 157 19644000 209 223 279 184 196 246 168 179 224 150 160 20045000 213 228 284 188 201 250 170 182 227 153 164 20446000 218 233 291 191 205 256 174 186 233 157 168 21047000 222 237 296 195 208 260 178 190 237 160 170 21348000 227 243 302 200 214 266 181 194 241 164 175 21849000 231 247 308 203 217 271 185 197 246 166 177 22150000 236 252 314 208 222 277 189 202 251 170 182 22651000 240 256 320 212 226 282 192 205 256 173 185 23152000 245 262 326 215 230 287 196 209 261 176 189 23553000 249 266 332 219 234 292 199 213 266 179 192 23954000 254 271 338 224 239 297 204 217 271 183 195 24355000 258 276 344 227 243 303 206 220 275 186 199 24860000 280 300 374 247 264 329 224 240 299 202 216 27065000 303 325 405 267 286 356 242 260 324 218 234 29170000 325 349 434 286 307 382 260 279 347 234 252 31375000 348 373 464 306 328 408 278 298 371 250 268 334

HO-12R

Fire + Wind Premium