hkfrs 7 financial instruments: disclosures - hong kong institute of

TRANSCRIPT

Financial Instruments:

Disclosures

Hong Kong Financial Reporting Standard 7

HKFRS 7 Revised December 2016September 2018

Effective for annual periods beginning on or after 1 January 2007

FINANCIAL INSTRUMENTS: DISCLOSURES

© Copyright 2 HKFRS 7 (September 2018)

COPYRIGHT

© Copyright 2018 Hong Kong Institute of Certified Public Accountants

This Hong Kong Financial Reporting Standard contains IFRS Foundation copyright material. Reproduction within Hong Kong in unaltered form (retaining this notice) is permitted for personal and non-commercial use subject to the inclusion of an acknowledgment of the source. Requests and inquiries concerning reproduction and rights for commercial purposes within Hong Kong should be addressed to the Director, Finance and Operation, Hong Kong Institute of Certified Public Accountants, 37/F., Wu Chung House, 213 Queen's Road East, Wanchai, Hong Kong. All rights in this material outside of Hong Kong are reserved by IFRS Foundation. Reproduction of Hong Kong Financial Reporting Standards outside of Hong Kong in unaltered form (retaining this notice) is permitted for personal and non-commercial use only. Further information and requests for authorisation to reproduce for commercial purposes outside Hong Kong should be addressed to the IFRS Foundation at www.ifrs.org.

Further details of the copyright notice form IFRS Foundation is available at http://app1.hkicpa.org.hk/ebook/copyright-notice.pdf

© Copyright 3 HKFRS 7 (September 2018)

CONTENTS

from paragraph

INTRODUCTION IN1

HONG KONG FINANCIAL REPORTING STANDARD 7 FINANCIAL INSTRUMENTS: DISCLOSURES

OBJECTIVE 1

SCOPE 3

CLASSES OF FINANCIAL INSTRUMENTS AND LEVEL OF DISCLOSURE

6

SIGNIFICANCE OF FINANCIAL INSTRUMENTS FOR FINANCIAL POSITION AND PERFORMANCE

7

Statement of financial position 8

Categories of financial assets and financial liabilities 8

Financial assets or financial liabilities at fair value through profit or loss

9

Reclassification 12

Offsetting financial assets and financial liabilities 13A

Collateral 14

Allowance account for credit losses 16

Compound financial instruments with multiple embedded derivatives

17

Defaults and breaches 18

Statement of comprehensive income 20

Items of income, expense, gains or losses 20

Other disclosures 21

Accounting policies 21

Hedge accounting 22

Fair value 25

NATURE AND EXTENT OF RISKS ARISING FROM FINANCIAL INSTRUMENTS

31

Qualitative disclosures 33

Quantitative disclosures 34

Credit risk 36

Financial assets that are either past due or impaired 37

Collateral and other credit enhancements obtained 38

Liquidity risk 39

Market risk 40

Sensitivity analysis 40

Other market risk disclosures 42

© Copyright 4 HKFRS 7 (September 2018)

TRANSFERS OF FINANCIAL ASSETS 42A

Transferred financial assets that are not derecognised in their entirety

42D

Transferred financial assets that are derecognised in their entirety

42E

Supplementary information 42H

INITIAL APPLICATION OF IFRS 9

EFFECTIVE DATE AND TRANSITION

42I

43

WITHDRAWAL OF HKAS 30 45

APPENDICES

A Defined terms

B Application guidance

C Amendments to other HKFRSs

BASIS FOR CONCLUSIONS

Amendments to Basis for Conclusions on other IFRSs

IMPLEMENTATION GUIDANCE

Amendments to guidance on other IFRSs

Hong Kong Financial Reporting Standard 7 Financial Instruments: Disclosures (HKFRS 7) is set out in paragraphs 1-45 and Appendices A-DC. All the paragraphs have equal authority. Paragraphs in bold type state the main principles. Terms defined in Appendix A are in italics the first time they appear in the Standard. Definitions of other terms are given in the Glossary for Hong Kong Financial Reporting Standards. HKFRS 7 should be read in the context of its objective and the Basis for Conclusions, the Preface to Hong Kong Financial Reporting Standards and the Conceptual Framework for Financial Reporting. HKAS 8 Accounting Policies, Changes in Accounting Estimates and Errors provides a basis for selecting and applying accounting policies in the absence of explicit guidance.

© Copyright 5 HKFRS 7 (September 2018)

Introduction Reasons for issuing the HKFRS

IN1 In recent years, the techniques used by entities for measuring and managing

exposure to risks arising from financial instruments have evolved and new risk management concepts and approaches have gained acceptance. In addition, many public and private sector initiatives have proposed improvements to the disclosure framework for risks arising from financial instruments.

IN2 The Hong Kong Institute of Certified Public Accountants (Institute) believes that users

of financial statements need information about an entity’s exposure to risks and how those risks are managed. Such information can influence a user’s assessment of the financial position and financial performance of an entity or of the amount, timing and uncertainty of its future cash flows. Greater transparency regarding those risks allows users to make more informed judgements about risk and return.

IN3 Consequently, the Institute agreed that there was a need to revise and enhance the

disclosures in HKAS 30 Disclosures in the Financial Statements of Banks and Similar Financial Institutions and HKAS 32 Financial Instruments: Disclosure and Presentation. As part of this revision, the Institute removed duplicative disclosures and simplified the disclosures about concentrations of risk, credit risk, liquidity risk and market risk in HKAS 32.

Main features of the HKFRS

IN4 HKFRS 7 applies to all risks arising from all financial instruments, except those

instruments listed in paragraph 3. The HKFRS applies to all entities, including entities that have few financial instruments (eg a manufacturer whose only financial instruments are accounts receivable and accounts payable) and those that have many financial instruments (eg a financial institution most of whose assets and liabilities are financial instruments). However, the extent of disclosure required depends on the extent of the entity’s use of financial instruments and of its exposure to risk.

IN5 The HKFRS requires disclosure of:

(a) the significance of financial instruments for an entity’s financial position and performance. These disclosures incorporate many of the requirements previously in HKAS 32.

(b) qualitative and quantitative information about exposure to risks arising from

financial instruments, including specified minimum disclosures about credit risk, liquidity risk and market risk. The qualitative disclosures describe management’s objectives, policies and processes for managing those risks. The quantitative disclosures provide information about the extent to which the entity is exposed to risk, based on information provided internally to the entity’s key management personnel. Together, these disclosures provide an overview of the entity’s use of financial instruments and the exposures to risks they create.

IN5A Amendments to the HKFRS, issued in March 2009, require enhanced disclosures

about fair value measurements and liquidity risk. These have been made to address application issues and provide useful information to users.

IN5B Disclosures—Transfers of Financial Assets (Amendments to HKFRS 7), issued in

October 2010, amended the required disclosures to help users of financial statements evaluate the risk exposures relating to transfers of financial assets and the effect of those risks on an entity’s financial position.

© Copyright 6 HKFRS 7 (September 2018)

IN5C In June 2011 the HKICPA relocated the disclosures about fair value measurements to HKFRS 13 Fair Value Measurement.

IN6 The HKFRS includes in Appendix B mandatory application guidance that explains how

to apply the requirements in the HKFRS. The HKFRS is accompanied by non-mandatory Implementation Guidance that describes how an entity might provide the disclosures required by the HKFRS.

IN7 The HKFRS supersedes HKAS 30 and the disclosure requirements of HKAS 32. The

presentation requirements of HKAS 32 remain unchanged. IN8 The HKFRS is effective for annual periods beginning on or after 1 January 2007.

Earlier application is encouraged. IN9 Disclosures—Offsetting Financial Assets and Financial Liabilities (Amendments to

HKFRS 7), issued in December 2011, amended the required disclosures to include information that will enable users of an entity’s financial statements to evaluate the effect or potential effect of netting arrangements, including rights of set-off associated with the entity’s recognised financial assets and recognised financial liabilities, on the entity’s financial position.

© Copyright 7 HKFRS 7 (September 2018)

Hong Kong Financial Reporting Standard 7 Financial Instruments: Disclosures Objective 1 The objective of this HKFRS is to require entities to provide disclosures in their

financial statements that enable users to evaluate:

(a) the significance of financial instruments for the entity’s financial position and performance; and

(b) the nature and extent of risks arising from financial instruments to which the

entity is exposed during the period and at the end of the reporting period, and how the entity manages those risks.

2 The principles in this HKFRS complement the principles for recognising, measuring

and presenting financial assets and financial liabilities in HKAS 32 Financial Instruments: Presentation and HKAS 39 HKFRS 9 Financial Instruments: Recognition and Measurement.

Scope 3 This HKFRS shall be applied by all entities to all types of financial instruments, except:

(a) those interests in subsidiaries, associates or joint ventures that are accounted for in accordance with HKFRS 10 Consolidated Financial Statements, HKAS 27 Separate Financial Statements or HKAS 28 Investments in Associates and Joint Ventures. However, in some cases, HKFRS 10, HKAS 27 or HKAS 28 require or permit an entity to account for an interest in a subsidiary, associate or joint venture using HKAS 39HKFRS 9; in those cases, entities shall apply the requirements of this HKFRS and, for those measured at fair value, the requirements of HKFRS 13 Fair Value Measurement. Entities shall also apply this HKFRS to all derivatives linked to interests in subsidiaries, associates or joint ventures unless the derivative meets the definition of an equity instrument in HKAS 32.

(b) employers’ rights and obligations arising from employee benefit plans, to

which HKAS 19 Employee Benefits applies. (c)

[deleted]

(d) insurance contracts as defined in HKFRS 4 Insurance Contracts. However,

this HKFRS applies to derivatives that are embedded in insurance contracts if HKAS 39HKFRS 9 requires the entity to account for them separately. Moreover, an issuer shall apply this HKFRS to financial guarantee contracts if the issuer applies HKAS 39HKFRS 9 in recognising and measuring the contracts, but shall apply HKFRS 4 if the issuer elects, in accordance with paragraph 4(d) of HKFRS 4, to apply HKFRS 4 in recognising and measuring them.

(e) financial instruments, contracts and obligations under share-based payment

transactions to which HKFRS 2 Share-based Payment applies, except that this HKFRS applies to contracts within the scope of paragraphs 5-7 of HKAS 39 HKFRS 9.

(f) instruments that are required to be classified as equity instruments in

accordance with paragraphs 16A and 16B or paragraphs 16C and 16D of HKAS 32.

© Copyright 8 HKFRS 7 (September 2018)

4 This HKFRS applies to recognised and unrecognised financial instruments. Recognised financial instruments include financial assets and financial liabilities that are within the scope of HKAS 39HKFRS 9. Unrecognised financial instruments include some financial instruments that, although outside the scope of HKAS 39 HKFRS 9, are within the scope of this HKFRS (such as some loan commitments).

5 This HKFRS applies to contracts to buy or sell a non-financial item that are within the

scope of HKAS 39 (see paragraphs 5-7 of HKAS 39)HKFRS 9. 5A The credit risk disclosure requirements in paragraph 35A-35N apply to those rights

that HKFRS 15 Revenue from Contracts with Customers specifies are accounted for in accordance with HKFRS 9 for the purposes of recognising impairment gains or losses. Any reference to financial assets or financial instruments in these paragraphs shall include those rights unless otherwise specified.

Classes of financial instruments and level of disclosure

6 When this HKFRS requires disclosures by class of financial instrument, an entity shall

group financial instruments into classes that are appropriate to the nature of the information disclosed and that take into account the characteristics of those financial instruments. An entity shall provide sufficient information to permit reconciliation to the line items presented in the statement of financial position.

Significance of financial instruments for financial position and performance

7 An entity shall disclose information that enables users of its financial statements to evaluate the significance of financial instruments for its financial position and performance.

Statement of financial position Categories of financial assets and financial liabilities

8 The carrying amounts of each of the following categories, as defined in HKAS 39specified in HKFRS 9, shall be disclosed either in the statement of financial position or in the notes:

(a) financial assets measured at fair value through profit or loss, showing

separately (i) those designated as such upon initial recognition or subsequently in accordance with paragraph 6.7.1 of HKFRS 9 and (ii) those classified as held for trading in accordance with HKAS 39; mandatorily measured at fair value through profit or loss in accordance with HKFRS 9.

(b)-(d) held-to-maturity investments; [deleted]

(c) loans and receivables; (d) available-for-sale financial assets;

(e) financial liabilities at fair value through profit or loss, showing separately (i) those designated as such upon initial recognition or subsequently in accordance with paragraph 6.7.1 of HKFRS 9 and (ii) those classified asthat meet the definition of held for trading in accordance with HKAS 39; andHKFRS 9.

(f) financial liabilities assets measured at amortised cost. (g) financial liabilities measured at amortised cost.

© Copyright 9 HKFRS 7 (September 2018)

(h) financial assets measured at fair value through other comprehensive income,

showing separately (i) financial assets that are measured at fair value through other comprehensive income in accordance with paragraph 4.1.2A of HKFRS 9; and (ii) investments in equity instruments designated as such upon initial recognition in accordance with paragraph 5.7.5 of HKFRS 9.

Financial assets or financial liabilities at fair value through profit or loss

9 If the entity has designated a loan or receivableas measured at fair value through profit or loss a financial asset (or group of loans or receivables financial assets) as at fair value through profit or loss that would otherwise be measured at fair value through other comprehensive income or amortised cost, it shall disclose:

(a) the maximum exposure to credit risk (see paragraph 36(a)) of the loan or

receivable financial asset (or group of loans or receivables financial assets) at the end of the reporting period.

(b) the amount by which any related credit derivatives or similar instruments

mitigate that maximum exposure to credit risk (see paragraph 36(b)). (c) the amount of change, during the period and cumulatively, in the fair value of

the loan or receivable financial asset (or group of loans or receivables financial assets) that is attributable to changes in the credit risk of the financial asset determined either:

(i) as the amount of change in its fair value that is not attributable to

changes in market conditions that give rise to market risk; or (ii) using an alternative method the entity believes more faithfully

represents the amount of change in its fair value that is attributable to changes in the credit risk of the asset.

Changes in market conditions that give rise to market risk include changes in an observed (benchmark) interest rate, commodity price, foreign exchange rate or index of prices or rates.

(d) the amount of the change in the fair value of any related credit derivatives or

similar instruments that has occurred during the period and cumulatively since the loan or receivable financial asset was designated.

10 If the entity has designated a financial liability as at fair value through profit or loss in

accordance with paragraph 9 of HKAS 39 4.2.2 of HKFRS 9 and is required to present the effects of changes in that liability's credit risk in other comprehensive income (see paragraph 5.7.7 of HKFRS 9), it shall disclose:

(a) the amount of change, during the period and cumulatively, in the fair value of

the financial liability that is attributable to changes in the credit risk of that liability determined either:(see paragraphs B5.7.13-B5.7.20 of HKFRS 9 for guidance on determining the effects of changes in a liability's credit risk).

(i) as the amount of change in its fair value that is not attributable to

changes in market conditions that give rise to market risk (see Appendix B, paragraph B4); or

(ii) using an alternative method the entity believes more faithfully

represents the amount of change in its fair value that is attributable to changes in the credit risk of the liability.

(b) the difference between the financial liability’s carrying amount and the amount

the entity would be contractually required to pay at maturity to the holder of the obligation.

© Copyright 10 HKFRS 7 (September 2018)

(c) any transfers of the cumulative gain or loss within equity during the period

including the reason for such transfers. (d) if a liability is derecognised during the period, the amount (if any) presented in

other comprehensive income that was realised at derecognition. 10A If an entity has designated a financial liability as at fair value through profit or loss in

accordance with paragraph 4.2.2 of HKFRS 9 and is required to present all changes in the fair value of that liability (including the effects of changes in the credit risk of the liability) in profit or loss (see paragraphs 5.7.7 and 5.7.8 of HKFRS 9), it shall disclose:

(a) the amount of change, during the period and cumulatively, in the fair value of

the financial liability that is attributable to changes in the credit risk of that liability (see paragraphs B5.7.13-B5.7.20 of HKFRS 9 for guidance on determining the effects of changes in a liability's credit risk); and

(b) the difference between the financial liability's carrying amount and the amount the entity would be contractually required to pay at maturity to the holder of the obligation.

11 The entity shall also disclose:

(a) a detailed description of the methods used to comply with the requirements in paragraphs 9(c) and ,10(a) and 10A(a) and paragraph 5.7.7(a) of HKFRS 9, including an explanation of why the method is appropriate.

(b) if the entity believes that the disclosure it has given, either in the statement of

financial position or in the notes, to comply with the requirements in paragraph 9(c) or, 10(a) or 10A(a) or paragraph 5.7.7(a) of HKFRS 9 does not faithfully represent the change in the fair value of the financial asset or financial liability attributable to changes in its credit risk, the reasons for reaching this conclusion and the factors it believes are relevant.

(c) a detailed description of the methodology or methodologies used to determine

whether presenting the effects of changes in a liability's credit risk in other comprehensive income would create or enlarge an accounting mismatch in profit or loss (see paragraphs 5.7.7 and 5.7.8 of HKFRS 9). If an entity is required to present the effects of changes in a liability's credit risk in profit or loss (see paragraphs 5.7.8 of HKFRS 9), the disclosure must include a detailed description of the economic relationship described in paragraph B5.7.6 of HKFRS 9.

Investments in equity instruments designated at fair value through other

comprehensive income 11A If an entity has designated investments in equity instruments to be measured at fair

value through other comprehensive income, as permitted by paragraph 5.7.5 of HKFRS 9, it shall disclose:

(a) which investments in equity instruments have been designated to be

measured at fair value through other comprehensive income. (b) the reasons for using this presentation alternative. (c) the fair value of each such investment at the end of the reporting period. (d) dividends recognised during the period, showing separately those related to

investments derecognised during the reporting period and those related to investments held at the end of the reporting period.

(e) any transfers of the cumulative gain or loss within equity during the period

including the reason for such transfers.

© Copyright 11 HKFRS 7 (September 2018)

11B If an entity derecognised investments in equity instruments measured at fair value

through other comprehensive income during the reporting period, it shall disclose: (a) the reasons for disposing of the investments. (b) the fair value of the investments at the date of derecognition. (c) the cumulative gain or loss on disposal.

Reclassification

12-12A [Deleted]If the entity has reclassified a financial asset (in accordance with paragraphs 51-54 of HKAS 39) as one measured:

(a) at cost or amortised cost, rather than fair value; or

(b) at fair value, rather than at cost or amortised cost,

it shall disclose the amount reclassified into and out of each category and the reason for that reclassification.

12A If the entity has reclassified a financial asset out of the fair value through profit or loss category in accordance with paragraph 50B or 50D of HKAS 39 or out of the available-for-sale category in accordance with paragraph 50E of HKAS 39, it shall disclose:

(a) the amount reclassified into and out of each category; (b) for each reporting period until derecognition, the carrying amounts and fair

values of all financial assets that have been reclassified in the current and previous reporting periods;

(c) if a financial asset was reclassified in accordance with paragraph 50B, the rare

situation, and the facts and circumstances indicating that the situation was rare;

(d) for the reporting period when the financial asset was reclassified, the fair value

gain or loss on the financial asset recognised in profit or loss or other comprehensive income in that reporting period and in the previous reporting period;

(e) for each reporting period following the reclassification (including the reporting

period in which the financial asset was reclassified) until derecognition of the financial asset, the fair value gain or loss that would have been recognised in profit or loss or other comprehensive income if the financial asset had not been reclassified, and the gain, loss, income and expense recognised in profit or loss; and

(f) the effective interest rate and estimated amounts of cash flows the entity

expects to recover, as at the date of reclassification of the financial asset.

12B An entity shall disclose if, in the current or previous reporting periods, it has reclassified any financial assets in accordance with paragraph 4.4.1 of HKFRS 9. For each such event, an entity shall disclose:

(a) the date of reclassification. (b) a detailed explanation of the change in business model and a qualitative

description of its effect on the entity's financial statements.

© Copyright 12 HKFRS 7 (September 2018)

(c) the amount reclassified into and out of each category.

12C For each reporting period following reclassification until derecognition, an entity shall disclose for assets reclassified out of the fair value through profit or loss category so that they are measured at amortised cost or fair value through other comprehensive income in accordance with paragraph 4.4.1 of HKFRS 9:

(a) the effective interest rate determined on the date of reclassification; and (b) the interest revenue recognised.

12D If, since its last annual reporting date, an entity has reclassified financial assets out of

the fair value through other comprehensive income category so that they are measured at amortised cost or out of the fair value through profit or loss category so that they are measured at amortised cost or fair value through other comprehensive income it shall disclose:

(a) the fair value of the financial assets at the end of the reporting period; and (b) the fair value gain or loss that would have been recognised in profit or loss or

other comprehensive income during the reporting period if the financial assets had not been reclassified.

13 [Deleted]

Offsetting financial assets and financial liabilities 13A The disclosures in paragraphs 13B–13E supplement the other disclosure

requirements of this HKFRS and are required for all recognised financial instruments that are set off in accordance with paragraph 42 of HKAS 32. These disclosures also apply to recognised financial instruments that are subject to an enforceable master netting arrangement or similar agreement, irrespective of whether they are set off in accordance with paragraph 42 of HKAS 32.

13B An entity shall disclose information to enable users of its financial statements to

evaluate the effect or potential effect of netting arrangements on the entity’s financial position. This includes the effect or potential effect of rights of set-off associated with the entity’s recognised financial assets and recognised financial liabilities that are within the scope of paragraph 13A.

13C To meet the objective in paragraph 13B, an entity shall disclose, at the end of the

reporting period, the following quantitative information separately for recognised financial assets and recognised financial liabilities that are within the scope of paragraph 13A:

(a) the gross amounts of those recognised financial assets and recognised

financial liabilities; (b) the amounts that are set off in accordance with the criteria in paragraph 42 of

HKAS 32 when determining the net amounts presented in the statement of financial position;

(c) the net amounts presented in the statement of financial position; (d) the amounts subject to an enforceable master netting arrangement or similar

agreement that are not otherwise included in paragraph 13C(b), including: (i) amounts related to recognised financial instruments that do not meet

some or all of the offsetting criteria in paragraph 42 of HKAS 32; and

© Copyright 13 HKFRS 7 (September 2018)

(ii) amounts related to financial collateral (including cash collateral); and

(e) the net amount after deducting the amounts in (d) from the amounts in (c)

above. The information required by this paragraph shall be presented in a tabular format, separately for financial assets and financial liabilities, unless another format is more appropriate.

13D The total amount disclosed in accordance with paragraph 13C(d) for an instrument

shall be limited to the amount in paragraph 13C(c) for that instrument. 13E An entity shall include a description in the disclosures of the rights of set-off

associated with the entity’s recognised financial assets and recognised financial liabilities subject to enforceable master netting arrangements and similar agreements that are disclosed in accordance with paragraph 13C(d), including the nature of those rights.

13F If the information required by paragraphs 13B–13E is disclosed in more than one note

to the financial statements, an entity shall cross-refer between those notes. Collateral

14 An entity shall disclose:

(a) the carrying amount of financial assets it has pledged as collateral for liabilities or contingent liabilities, including amounts that have been reclassified in accordance with paragraph 37(a) of HKAS 393.2.23(a) of HKFRS 9; and

(b) the terms and conditions relating to its pledge.

15 When an entity holds collateral (of financial or non-financial assets) and is permitted to

sell or repledge the collateral in the absence of default by the owner of the collateral, it shall disclose:

(a) the fair value of the collateral held; (b) the fair value of any such collateral sold or repledged, and whether the entity

has an obligation to return it; and (c) the terms and conditions associated with its use of the collateral.

Allowance account for credit losses 16 When financial assets are impaired by credit losses and the entity records the

impairment in a separate account (eg an allowance account used to record individual impairments or a similar account used to record a collective impairment of assets) rather than directly reducing the carrying amount of the asset, it shall disclose a reconciliation of changes in that account during the period for each class of financial assets.[Deleted]

16A The carrying amount of financial assets measured at fair value through other

comprehensive income in accordance with paragraph 4.1.2A of HKFRS 9 is not reduced by a loss allowance and an entity shall not present the loss allowance separately in the statement of financial position as a reduction of the carrying amount of the financial asset. However, an entity shall disclose the loss allowance in the notes to the financial statements.

© Copyright 14 HKFRS 7 (September 2018)

Compound financial instruments with multiple embedded derivatives 17 If an entity has issued an instrument that contains both a liability and an equity

component (see paragraph 28 of HKAS 32) and the instrument has multiple embedded derivatives whose values are interdependent (such as a callable convertible debt instrument), it shall disclose the existence of those features.

Defaults and breaches 18 For loans payable recognised at the end of the reporting period, an entity shall

disclose:

(a) details of any defaults during the period of principal, interest, sinking fund, or redemption terms of those loans payable;

(b) the carrying amount of the loans payable in default at the end of the reporting

period; and (c) whether the default was remedied, or the terms of the loans payable were

renegotiated, before the financial statements were authorised for issue. 19 If, during the period, there were breaches of loan agreement terms other than those

described in paragraph 18, an entity shall disclose the same information as required by paragraph 18 if those breaches permitted the lender to demand accelerated repayment (unless the breaches were remedied, or the terms of the loan were renegotiated, on or before the end of the reporting period).

Statement of comprehensive income Items of income, expense, gains or losses

20 An entity shall disclose the following items of income, expense, gains or losses either in the statement of comprehensive income or in the notes:

(a) net gains or net losses on:

(i) financial assets or financial liabilities at fair value through profit or loss,

showing separately those on financial assets or financial liabilities designated as such upon initial recognition or subsequently in accordance with paragraph 6.7.1 of HKFRS 9, and those on financial assets or financial liabilities that are mandatorily measured at fair value through profit or loss in accordance with HKFRS 9 (eg financial liabilities that meet the definition of classified as held for trading in accordance with HKAS 39;HKFRS 9). For financial liabilities designated as at fair value through profit or loss, an entity shall show separately the amount of gain or loss recognised in other comprehensive income and the amount recognised in profit or loss.

(ii)-(iv) [deleted]available-for-sale financial assets, showing separately the

amount of gain or loss recognised in other comprehensive income during the period and the amount reclassified from equity to profit or loss for the period;

(iii) held-to-maturity investments; (iv) loans and receivables; and (v) financial liabilities measured at amortised cost;. (vi) financial assets measured at amortised cost. (vii) investments in equity instruments designated at fair value through

other comprehensive income in accordance with paragraph 5.7.5 of

© Copyright 15 HKFRS 7 (September 2018)

HKFRS 9. (viii) financial assets measured at fair value through other comprehensive

income in accordance with paragraph 4.1.2A of HKFRS 9, showing separately the amount of gain or loss recognised in other comprehensive income during the period and the amount reclassified upon derecognition from accumulated other comprehensive income to profit or loss for the period.

(b) total interest income revenue and total interest expense (calculated using the

effective interest method) for financial assets that are measured at amortised cost or that are measured at fair value through other comprehensive income in accordance with paragraph 4.1.2A of HKFRS 9 (showing these amounts separately); or financial liabilities that are not measured at fair value through profit or loss;.

(c) fee income and expense (other than amounts included in determining the

effective interest rate) arising from:

(i) financial assets orand financial liabilities that are not at fair value through profit or loss; and

(ii) trust and other fiduciary activities that result in the holding or investing

of assets on behalf of individuals, trusts, retirement benefit plans, and other institutions;.

(d) interest income on impaired financial assets accrued in accordance with

paragraph AG93 of HKAS 39; and[deleted] (e) the amount of any impairment loss for each class of financial asset.[deleted]

20A An entity shall disclose an analysis of the gain or loss recognised in the statement of

comprehensive income arising from the derecognition of financial assets measured at amortised cost, showing separately gains and losses arising from derecognition of those financial assets. This disclosure shall include the reasons for derecognising those financial assets.

Other disclosures

Accounting policies

21 In accordance with paragraph 117 of HKAS 1 Presentation of Financial Statements

(as revised 2007), an entity discloses its significant accounting policies comprising the measurement basis (or bases) used in preparing the financial statements and the other accounting policies used that are relevant to an understanding of the financial statements.

Hedge accounting

21A An entity shall apply the disclosure requirements in paragraphs 21B–24F for those risk exposures that an entity hedges and for which it elects to apply hedge accounting. Hedge accounting disclosures shall provide information about:

(a) an entity’s risk management strategy and how it is applied to manage risk; (b) how the entity’s hedging activities may affect the amount, timing and

uncertainty of its future cash flows; and

(c) the effect that hedge accounting has had on the entity’s statement of financial position, statement of comprehensive income and statement of changes in

© Copyright 16 HKFRS 7 (September 2018)

equity. 21B An entity shall present the required disclosures in a single note or separate section in

its financial statements. However, an entity need not duplicate information that is already presented elsewhere, provided that the information is incorporated by cross-reference from the financial statements to some other statement, such as a management commentary or risk report, that is available to users of the financial statements on the same terms as the financial statements and at the same time. Without the information incorporated by cross-reference, the financial statements are incomplete.

21C When paragraphs 22A–24F require the entity to separate by risk category the

information disclosed, the entity shall determine each risk category on the basis of the risk exposures an entity decides to hedge and for which hedge accounting is applied. An entity shall determine risk categories consistently for all hedge accounting disclosures.

21D To meet the objectives in paragraph 21A, an entity shall (except as otherwise

specified below) determine how much detail to disclose, how much emphasis to place on different aspects of the disclosure requirements, the appropriate level of aggregation or disaggregation, and whether users of financial statements need additional explanations to evaluate the quantitative information disclosed. However, an entity shall use the same level of aggregation or disaggregation it uses for disclosure requirements of related information in this HKFRS and HKFRS 13 Fair Value Measurement.

The risk management strategy

22 [Deleted]An entity shall disclose the following separately for each type of hedge described in HKAS 39 (ie fair value hedges, cash flow hedges, and hedges of net investments in foreign operations): (a) a description of each type of hedge; (b) a description of the financial instruments designated as hedging instruments

and their fair values at the end of the reporting period; and (c) the nature of the risks being hedged.

22A An entity shall explain its risk management strategy for each risk category of risk

exposures that it decides to hedge and for which hedge accounting is applied. This explanation should enable users of financial statements to evaluate (for example):

(a) how each risk arises. (b) how the entity manages each risk; this includes whether the entity hedges an

item in its entirety for all risks or hedges a risk component (or components) of an item and why.

(c) the extent of risk exposures that the entity manages.

22B To meet the requirements in paragraph 22A, the information should include (but is not

limited to) a description of:

(a) the hedging instruments that are used (and how they are used) to hedge risk exposures;

(b) how the entity determines the economic relationship between the hedged item

and the hedging instrument for the purpose of assessing hedge effectiveness; and

© Copyright 17 HKFRS 7 (September 2018)

(c) how the entity establishes the hedge ratio and what the sources of hedge ineffectiveness are.

22C When an entity designates a specific risk component as a hedged item (see paragraph

6.3.7 of HKFRS 9) it shall provide, in addition to the disclosures required by paragraphs 22A and 22B, qualitative or quantitative information about:

(a) how the entity determined the risk component that is designated as the

hedged item (including a description of the nature of the relationship between the risk component and the item as a whole); and

(b) how the risk component relates to the item in its entirety (for example, the

designated risk component historically covered on average 80 per cent of the changes in fair value of the item as a whole).

The amount, timing and uncertainty of future cash flows

23 [Deleted]For cash flow hedges, an entity shall disclose:

(a) the periods when the cash flows are expected to occur and when they are expected to affect profit or loss;

(b) a description of any forecast transaction for which hedge accounting had

previously been used, but which is no longer expected to occur; (c) the amount that was recognised in other comprehensive income during the

period; (d) the amount that was reclassified from equity to profit or loss for the period,

showing the amount included in each line item in the statement of comprehensive income; and

(e) the amount that was removed from equity during the period and included in

the initial cost or other carrying amount of a non-financial asset or non-financial liability whose acquisition or incurrence was a hedged highly probable forecast transaction.

23A Unless exempted by paragraph 23C, an entity shall disclose by risk category

quantitative information to allow users of its financial statements to evaluate the terms and conditions of hedging instruments and how they affect the amount, timing and uncertainty of future cash flows of the entity.

23B To meet the requirement in paragraph 23A, an entity shall provide a breakdown that

discloses:

(a) a profile of the timing of the nominal amount of the hedging instrument; and (b) if applicable, the average price or rate (for example strike or forward prices etc)

of the hedging instrument. 23C In situations in which an entity frequently resets (ie discontinues and restarts) hedging

relationships because both the hedging instrument and the hedged item frequently change (ie the entity uses a dynamic process in which both the exposure and the hedging instruments used to manage that exposure do not remain the same for long—such as in the example in paragraph B6.5.24(b) of HKFRS 9) the entity:

(a) is exempt from providing the disclosures required by paragraphs 23A and

23B. (b) shall disclose:

© Copyright 18 HKFRS 7 (September 2018)

(i) information about what the ultimate risk management strategy is in relation to those hedging relationships;

(ii) a description of how it reflects its risk management strategy by using

hedge accounting and designating those particular hedging relationships; and

(iii) an indication of how frequently the hedging relationships are

discontinued and restarted as part of the entity’s process in relation to those hedging relationships.

23D An entity shall disclose by risk category a description of the sources of hedge

ineffectiveness that are expected to affect the hedging relationship during its term. 23E If other sources of hedge ineffectiveness emerge in a hedging relationship, an entity

shall disclose those sources by risk category and explain the resulting hedge ineffectiveness.

23F For cash flow hedges, an entity shall disclose a description of any forecast transaction

for which hedge accounting had been used in the previous period, but which is no longer expected to occur.

The effects of hedge accounting on financial position and performance 24 [Deleted]An entity shall disclose separately:

(a) in fair value hedges, gains or losses:

(i) on the hedging instrument; and (ii) on the hedged item attributable to the hedged risk.

(b) the ineffectiveness recognised in profit or loss that arises from cash flow

hedges. (c) the ineffectiveness recognised in profit or loss that arises from hedges of net

investments in foreign operations. 24A An entity shall disclose, in a tabular format, the following amounts related to items

designated as hedging instruments separately by risk category for each type of hedge (fair value hedge, cash flow hedge or hedge of a net investment in a foreign operation):

(a) the carrying amount of the hedging instruments (financial assets separately

from financial liabilities); (b) the line item in the statement of financial position that includes the hedging

instrument; (c) the change in fair value of the hedging instrument used as the basis for

recognising hedge ineffectiveness for the period; and (d) the nominal amounts (including quantities such as tonnes or cubic metres) of

the hedging instruments. 24B An entity shall disclose, in a tabular format, the following amounts related to hedged

items separately by risk category for the types of hedges as follows:

(a) for fair value hedges:

© Copyright 19 HKFRS 7 (September 2018)

(i) the carrying amount of the hedged item recognised in the statement of financial position (presenting assets separately from liabilities);

(ii) the accumulated amount of fair value hedge adjustments on the

hedged item included in the carrying amount of the hedged item recognised in the statement of financial position (presenting assets separately from liabilities);

(iii) the line item in the statement of financial position that includes the

hedged item; (iv) the change in value of the hedged item used as the basis for

recognising hedge ineffectiveness for the period; and (v) the accumulated amount of fair value hedge adjustments remaining in

the statement of financial position for any hedged items that have ceased to be adjusted for hedging gains and losses in accordance with paragraph 6.5.10 of HKFRS 9.

(b) for cash flow hedges and hedges of a net investment in a foreign operation:

(i) the change in value of the hedged item used as the basis for

recognising hedge ineffectiveness for the period (ie for cash flow hedges the change in value used to determine the recognised hedge ineffectiveness in accordance with paragraph 6.5.11(c) of HKFRS 9);

(ii) the balances in the cash flow hedge reserve and the foreign currency

translation reserve for continuing hedges that are accounted for in accordance with paragraphs 6.5.11 and 6.5.13(a) of HKFRS 9; and

(iii) the balances remaining in the cash flow hedge reserve and the

foreign currency translation reserve from any hedging relationships for which hedge accounting is no longer applied.

24C An entity shall disclose, in a tabular format, the following amounts separately by risk

category for the types of hedges as follows:

(a) for fair value hedges:

(i) hedge ineffectiveness—ie the difference between the hedging gains or losses of the hedging instrument and the hedged item—recognised in profit or loss (or other comprehensive income for hedges of an equity instrument for which an entity has elected to present changes in fair value in other comprehensive income in accordance with paragraph 5.7.5 of HKFRS 9); and

(ii) the line item in the statement of comprehensive income that includes

the recognised hedge ineffectiveness.

(b) for cash flow hedges and hedges of a net investment in a foreign operation:

(i) hedging gains or losses of the reporting period that were recognised in other comprehensive income;

(ii) hedge ineffectiveness recognised in profit or loss; (iii) the line item in the statement of comprehensive income that includes

the recognised hedge ineffectiveness; (iv) the amount reclassified from the cash flow hedge reserve or the

© Copyright 20 HKFRS 7 (September 2018)

foreign currency translation reserve into profit or loss as a reclassification adjustment (see HKAS 1) (differentiating between amounts for which hedge accounting had previously been used, but for which the hedged future cash flows are no longer expected to occur, and amounts that have been transferred because the hedged item has affected profit or loss);

(v) the line item in the statement of comprehensive income that includes

the reclassification adjustment (see HKAS 1); and (vi) for hedges of net positions, the hedging gains or losses recognised in

a separate line item in the statement of comprehensive income (see paragraph 6.6.4 of HKFRS 9).

24D When the volume of hedging relationships to which the exemption in paragraph 23C

applies is unrepresentative of normal volumes during the period (ie the volume at the reporting date does not reflect the volumes during the period) an entity shall disclose that fact and the reason it believes the volumes are unrepresentative.

24E An entity shall provide a reconciliation of each component of equity and an analysis of

other comprehensive income in accordance with HKAS 1 that, taken together:

(a) differentiates, at a minimum, between the amounts that relate to the disclosures in paragraph 24C(b)(i) and (b)(iv) as well as the amounts accounted for in accordance with paragraph 6.5.11(d)(i) and (d)(iii) of HKFRS 9;

(b) differentiates between the amounts associated with the time value of options

that hedge transaction related hedged items and the amounts associated with the time value of options that hedge time-period related hedged items when an entity accounts for the time value of an option in accordance with paragraph 6.5.15 of HKFRS 9; and

(c) differentiates between the amounts associated with forward elements of

forward contracts and the foreign currency basis spreads of financial instruments that hedge transaction related hedged items, and the amounts associated with forward elements of forward contracts and the foreign currency basis spreads of financial instruments that hedge time-period related hedged items when an entity accounts for those amounts in accordance with paragraph 6.5.16 of HKFRS 9.

24F An entity shall disclose the information required in paragraph 24E separately by risk

category. This disaggregation by risk may be provided in the notes to the financial statements.

Option to designate a credit exposure as measured at fair value through profit or Loss

24G If an entity designated a financial instrument, or a proportion of it, as measured at fair

value through profit or loss because it uses a credit derivative to manage the credit risk of that financial instrument it shall disclose:

(a) for credit derivatives that have been used to manage the credit risk of financial

instruments designated as measured at fair value through profit or loss in accordance with paragraph 6.7.1 of HKFRS 9, a reconciliation of each of the nominal amount and the fair value at the beginning and at the end of the period;

(b) the gain or loss recognised in profit or loss on designation of a financial

instrument, or a proportion of it, as measured at fair value through profit or loss in accordance with paragraph 6.7.1 of HKFRS 9; and

© Copyright 21 HKFRS 7 (September 2018)

(c) on discontinuation of measuring a financial instrument, or a proportion of it, at

fair value through profit or loss, that financial instrument’s fair value that has become the new carrying amount in accordance with paragraph 6.7.4 of HKFRS 9 and the related nominal or principal amount (except for providing comparative information in accordance with HKAS 1, an entity does not need to continue this disclosure in subsequent periods).

Fair value

25 Except as set out in paragraph 29, for each class of financial assets and financial liabilities (see paragraph 6), an entity shall disclose the fair value of that class of assets and liabilities in a way that permits it to be compared with its carrying amount.

26 In disclosing fair values, an entity shall group financial assets and financial liabilities

into classes, but shall offset them only to the extent that their carrying amounts are offset in the statement of financial position.

27-27B [Deleted] 28 In some cases, an entity does not recognise a gain or loss on initial recognition of a

financial asset or financial liability because the fair value is neither evidenced by a quoted price in an active market for an identical asset or liability (ie a Level 1 input) nor based on a valuation technique that uses only data from observable markets (see paragraph AG76 of HKAS 39B5.1.2A of HKFRS 9). In such cases, the entity shall disclose by class of financial asset or financial liability.:

(a) its accounting policy for recognising in profit or loss the difference between the

fair value at initial recognition and the transaction price to reflect a change in factors (including time) that market participants would take into account when pricing the asset or liability (see paragraph AG76(b) of HKAS 39B5.1.2A(b) of HKFRS 9).

(b) the aggregate difference yet to be recognised in profit or loss at the beginning

and end of the period and a reconciliation of changes in the balance of this difference.

(c) why the entity concluded that the transaction price was not the best evidence

of fair value, including a description of the evidence that supports the fair value.

29 Disclosures of fair value are not required:

(a) when the carrying amount is a reasonable approximation of fair value, for example, for financial instruments such as short-term trade receivables and payables;

(b) for an investment in equity instruments that do not have a quoted market price

in an active market for an identical instrument (ie a Level 1 input), or derivatives linked to such equity instruments, that is measured at cost in accordance with HKAS 39 because its fair value cannot otherwise be measured reliably; or[deleted]

(c) for a contract containing a discretionary participation feature (as described in

HKFRS 4) if the fair value of that feature cannot be measured reliably. 30 In the cases described in paragraph 29(b) and (c), an entity shall disclose information

to help users of the financial statements make their own judgements about the extent of possible differences between the carrying amount of those financial assets or financial liabilities contracts and their fair value, including:

© Copyright 22 HKFRS 7 (September 2018)

(a) the fact that fair value information has not been disclosed for these

instruments because their fair value cannot be measured reliably; (b) a description of the financial instruments, their carrying amount, and an

explanation of why fair value cannot be measured reliably; (c) information about the market for the instruments; (d) information about whether and how the entity intends to dispose of the

financial instruments; and (e) if financial instruments whose fair value previously could not be reliably

measured are derecognised, that fact, their carrying amount at the time of derecognition, and the amount of gain or loss recognised.

Nature and extent of risks arising from financial instruments 31 An entity shall disclose information that enables users of its financial

statements to evaluate the nature and extent of risks arising from financial instruments to which the entity is exposed at the end of the reporting period.

32 The disclosures required by paragraphs 33-42 focus on the risks that arise from

financial instruments and how they have been managed. These risks typically include, but are not limited to, credit risk, liquidity risk and market risk.

32A Providing qualitative disclosures in the context of quantitative disclosures enables

users to link related disclosures and hence form an overall picture of the nature and extent of risks arising from financial instruments. The interaction between qualitative and quantitative disclosures contributes to disclosure of information in a way that better enables users to evaluate an entity’s exposure to risks.

Qualitative disclosures

33 For each type of risk arising from financial instruments, an entity shall disclose:

(a) the exposures to risk and how they arise; (b) its objectives, policies and processes for managing the risk and the methods

used to measure the risk; and (c) any changes in (a) or (b) from the previous period.

Quantitative disclosures

34 For each type of risk arising from financial instruments, an entity shall disclose:

(a) summary quantitative data about its exposure to that risk at the end of the reporting period. This disclosure shall be based on the information provided internally to key management personnel of the entity (as defined in HKAS 24 Related Party Disclosures), for example the entity’s board of directors or chief executive officer.

(b) the disclosures required by paragraphs 3635A-42, to the extent not provided

in accordance with (a). (c) concentrations of risk if not apparent from the disclosures made in accordance

with (a) and (b).

© Copyright 23 HKFRS 7 (September 2018)

35 If the quantitative data disclosed as at the end of the reporting period are unrepresentative of an entity’s exposure to risk during the period, an entity shall provide further information that is representative.

Credit risk

Scope and objectives

35A An entity shall apply the disclosure requirements in paragraphs 35F–35N to financial

instruments to which the impairment requirements in HKFRS 9 are applied. However:

(a) for trade receivables, contract assets and lease receivables, paragraph 35J(a) applies to those trade receivables, contract assets or lease receivables on which lifetime expected credit losses are recognised in accordance with paragraph 5.5.15 of HKFRS 9, if those financial assets are modified while more than 30 days past due; and

(b) paragraph 35K(b) does not apply to lease receivables.

35B The credit risk disclosures made in accordance with paragraphs 35F–35N shall enable

users of financial statements to understand the effect of credit risk on the amount, timing and uncertainty of future cash flows. To achieve this objective, credit risk disclosures shall provide:

(a) information about an entity’s credit risk management practices and how they

relate to the recognition and measurement of expected credit losses, including the methods, assumptions and information used to measure expected credit losses;

(b) quantitative and qualitative information that allows users of financial

statements to evaluate the amounts in the financial statements arising from expected credit losses, including changes in the amount of expected credit losses and the reasons for those changes; and

(c) information about an entity’s credit risk exposure (ie the credit risk inherent in

an entity’s financial assets and commitments to extend credit) including significant credit risk concentrations.

35C An entity need not duplicate information that is already presented elsewhere, provided

that the information is incorporated by cross-reference from the financial statements to other statements, such as a management commentary or risk report that is available to users of the financial statements on the same terms as the financial statements and at the same time. Without the information incorporated by cross-reference, the financial statements are incomplete.

35D To meet the objectives in paragraph 35B, an entity shall (except as otherwise

specified) consider how much detail to disclose, how much emphasis to place on different aspects of the disclosure requirements, the appropriate level of aggregation or disaggregation, and whether users of financial statements need additional explanations to evaluate the quantitative information disclosed.

35E If the disclosures provided in accordance with paragraphs 35F–35N are insufficient to meet the objectives in paragraph 35B, an entity shall disclose additional information that is necessary to meet those objectives.

The credit risk management practices

35F An entity shall explain its credit risk management practices and how they relate to the

recognition and measurement of expected credit losses. To meet this objective an entity shall disclose information that enables users of financial statements to understand and evaluate:

© Copyright 24 HKFRS 7 (September 2018)

(a) how an entity determined whether the credit risk of financial instruments has

increased significantly since initial recognition, including, if and how:

(i) financial instruments are considered to have low credit risk in accordance with paragraph 5.5.10 of HKFRS 9, including the classes of financial instruments to which it applies; and

(ii) the presumption in paragraph 5.5.11 of HKFRS 9, that there have

been significant increases in credit risk since initial recognition when financial assets are more than 30 days past due, has been rebutted;

(b) an entity’s definitions of default, including the reasons for selecting those

definitions;

(c) how the instruments were grouped if expected credit losses were measured on a collective basis;

(d) how an entity determined that financial assets are credit-impaired financial

assets; (e) an entity’s write-off policy, including the indicators that there is no reasonable

expectation of recovery and information about the policy for financial assets that are written-off but are still subject to enforcement activity; and

(f) how the requirements in paragraph 5.5.12 of HKFRS 9 for the modification of

contractual cash flows of financial assets have been applied, including how an entity:

(i) determines whether the credit risk on a financial asset that has been

modified while the loss allowance was measured at an amount equal to lifetime expected credit losses, has improved to the extent that the loss allowance reverts to being measured at an amount equal to 12-month expected credit losses in accordance with paragraph 5.5.5 of HKFRS 9; and

(ii) monitors the extent to which the loss allowance on financial assets

meeting the criteria in (i) is subsequently remeasured at an amount equal to lifetime expected credit losses in accordance with paragraph 5.5.3 of HKFRS 9.

35G An entity shall explain the inputs, assumptions and estimation techniques used to

apply the requirements in Section 5.5 of HKFRS 9. For this purpose an entity shall disclose:

(a) the basis of inputs and assumptions and the estimation techniques used to:

(i) measure the 12-month and lifetime expected credit losses; (ii) determine whether the credit risk of financial instruments has

increased significantly since initial recognition; and

(iii) determine whether a financial asset is a credit-impaired financial asset.

(b) how forward-looking information has been incorporated into the determination of expected credit losses, including the use of macroeconomic information; and

(c) changes in the estimation techniques or significant assumptions made during

© Copyright 25 HKFRS 7 (September 2018)

the reporting period and the reasons for those changes.

Quantitative and qualitative information about amounts arising from expected credit losses

35H To explain the changes in the loss allowance and the reasons for those changes, an

entity shall provide, by class of financial instrument, a reconciliation from the opening balance to the closing balance of the loss allowance, in a table, showing separately the changes during the period for:

(a) the loss allowance measured at an amount equal to 12-month expected credit

losses; (b) the loss allowance measured at an amount equal to lifetime expected credit

losses for:

(i) financial instruments for which credit risk has increased significantly since initial recognition but that are not credit-impaired financial assets;

(ii) financial assets that are credit-impaired at the reporting date (but that

are not purchased or originated credit-impaired); and (iii) trade receivables, contract assets or lease receivables for which the

loss allowances are measured in accordance with paragraph 5.5.15 of HKFRS 9.

(c) financial assets that are purchased or originated credit-impaired. In addition to

the reconciliation, an entity shall disclose the total amount of undiscounted expected credit losses at initial recognition on financial assets initially recognised during the reporting period.

35I To enable users of financial statements to understand the changes in the loss

allowance disclosed in accordance with paragraph 35H, an entity shall provide an explanation of how significant changes in the gross carrying amount of financial instruments during the period contributed to changes in the loss allowance. The information shall be provided separately for financial instruments that represent the loss allowance as listed in paragraph 35H(a)–(c) and shall include relevant qualitative and quantitative information. Examples of changes in the gross carrying amount of financial instruments that contributed to the changes in the loss allowance may include:

(a) changes because of financial instruments originated or acquired during the

reporting period; (b) the modification of contractual cash flows on financial assets that do not result

in a derecognition of those financial assets in accordance with HKFRS 9; (c) changes because of financial instruments that were derecognised (including

those that were written-off) during the reporting period; and (d) changes arising from whether the loss allowance is measured at an amount

equal to 12-month or lifetime expected credit losses.

35J To enable users of financial statements to understand the nature and effect of modifications of contractual cash flows on financial assets that have not resulted in derecognition and the effect of such modifications on the measurement of expected credit losses, an entity shall disclose:

(a) the amortised cost before the modification and the net modification gain or

© Copyright 26 HKFRS 7 (September 2018)

loss recognised for financial assets for which the contractual cash flows have been modified during the reporting period while they had a loss allowance measured at an amount equal to lifetime expected credit losses; and

(b) the gross carrying amount at the end of the reporting period of financial assets

that have been modified since initial recognition at a time when the loss allowance was measured at an amount equal to lifetime expected credit losses and for which the loss allowance has changed during the reporting period to an amount equal to 12-month expected credit losses.

35K To enable users of financial statements to understand the effect of collateral and other

credit enhancements on the amounts arising from expected credit losses, an entity shall disclose by class of financial instrument:

(a) the amount that best represents its maximum exposure to credit risk at the

end of the reporting period without taking account of any collateral held or other credit enhancements (eg netting agreements that do not qualify for offset in accordance with HKAS 32).

(b) a narrative description of collateral held as security and other credit

enhancements, including:

(i) a description of the nature and quality of the collateral held; (ii) an explanation of any significant changes in the quality of that

collateral or credit enhancements as a result of deterioration or changes in the collateral policies of the entity during the reporting period; and

(iii) information about financial instruments for which an entity has not

recognised a loss allowance because of the collateral.

(c) quantitative information about the collateral held as security and other credit enhancements (for example, quantification of the extent to which collateral and other credit enhancements mitigate credit risk) for financial assets that are credit-impaired at the reporting date.

35L An entity shall disclose the contractual amount outstanding on financial assets that

were written off during the reporting period and are still subject to enforcement activity.

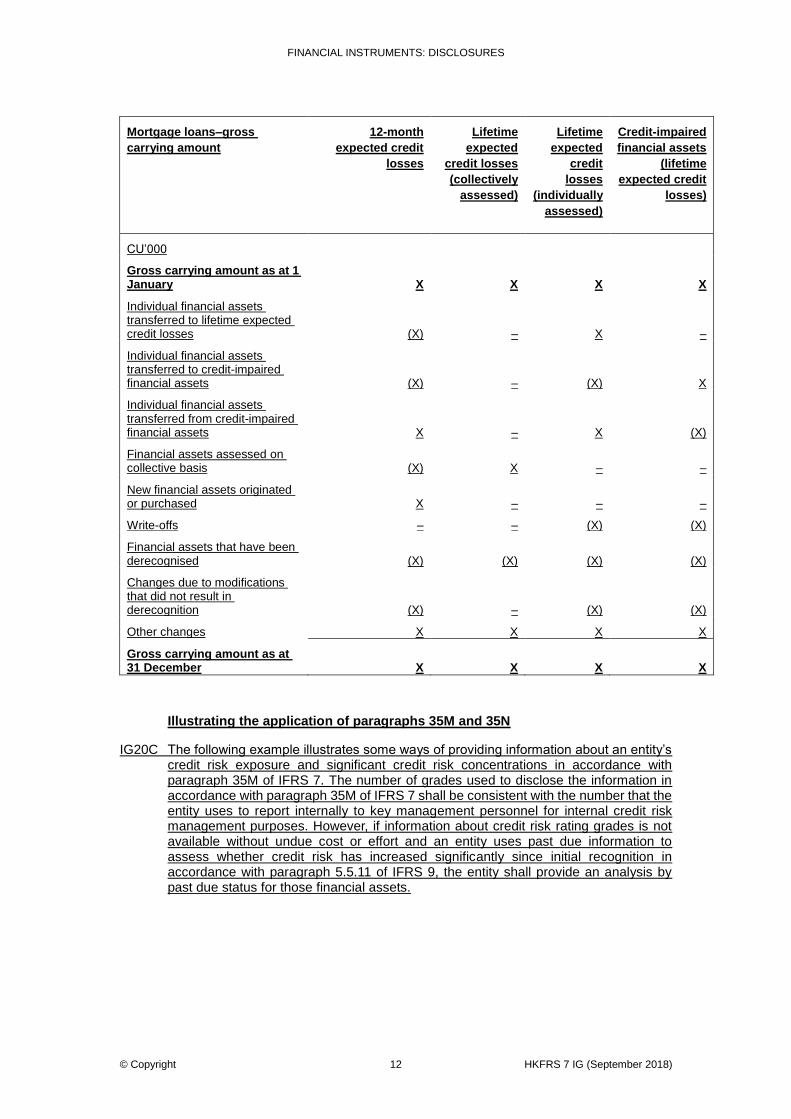

Credit risk exposure 35M To enable users of financial statements to assess an entity’s credit risk exposure and

understand its significant credit risk concentrations, an entity shall disclose, by credit risk rating grades, the gross carrying amount of financial assets and the exposure to credit risk on loan commitments and financial guarantee contracts. This information shall be provided separately for financial instruments:

(a) for which the loss allowance is measured at an amount equal to 12-month

expected credit losses; (b) for which the loss allowance is measured at an amount equal to lifetime

expected credit losses and that are:

(i) financial instruments for which credit risk has increased significantly since initial recognition but that are not credit-impaired financial assets;

(ii) financial assets that are credit-impaired at the reporting date (but that

are not purchased or originated credit-impaired); and (iii) trade receivables, contract assets or lease receivables for which the

© Copyright 27 HKFRS 7 (September 2018)

loss allowances are measured in accordance with paragraph 5.5.15 of HKFRS 9.

(c) that are purchased or originated credit-impaired financial assets.

35N For trade receivables, contract assets and lease receivables to which an entity applies

paragraph 5.5.15 of HKFRS 9, the information provided in accordance with paragraph 35M may be based on a provision matrix (see paragraph B5.5.35 of HKFRS 9).

36 For all financial instruments within the scope of this HKFRS, but to which the impairment requirements in HKFRS 9 are not applied, Aan entity shall disclose by class of financial instrument:

(a) the amount that best represents its maximum exposure to credit risk at the end of the reporting period without taking account of any collateral held or other credit enhancements (eg netting agreements that do not qualify for offset in accordance with HKAS 32); this disclosure is not required for financial instruments whose carrying amount best represents the maximum exposure to credit risk.

(b) a description of collateral held as security and of other credit enhancements, and their financial effect (eg a quantification of the extent to which collateral and other credit enhancements mitigate credit risk) in respect of the amount that best represents the maximum exposure to credit risk (whether disclosed in accordance with (a) or represented by the carrying amount of a financial instrument).

(c) information about the credit quality of financial assets that are neither past due

nor impaired.[deleted] (d) [deleted] Financial assets that are either past due or impaired

37 [Deleted]An entity shall disclose by class of financial asset:

(a) an analysis of the age of financial assets that are past due as at the end of the reporting period but not impaired; and

(b) an analysis of financial assets that are individually determined to be impaired

as at the end of the reporting period, including the factors the entity considered in determining that they are impaired.

(c) [deleted]

Collateral and other credit enhancements obtained 38 When an entity obtains financial or non-financial assets during the period by taking

possession of collateral it holds as security or calling on other credit enhancements (eg guarantees), and such assets meet the recognition criteria in other HKFRSs, an entity shall disclose for such assets held at the reporting date:

(a) the nature and carrying amount of the assets; and (b) when the assets are not readily convertible into cash, its policies for disposing

of such assets or for using them in its operations.

© Copyright 28 HKFRS 7 (September 2018)

Liquidity risk 39 An entity shall disclose:

(a) a maturity analysis for non-derivative financial liabilities (including issued financial guarantee contracts) that shows the remaining contractual maturities.

(b) a maturity analysis for derivative financial liabilities. The maturity analysis shall

include the remaining contractual maturities for those derivative financial liabilities for which contractual maturities are essential for an understanding of the timing of the cash flows (see paragraph B11B).

(c) a description of how it manages the liquidity risk inherent in (a) and (b).

Market risk

Sensitivity analysis

40 Unless an entity complies with paragraph 41, it shall disclose:

(a) a sensitivity analysis for each type of market risk to which the entity is exposed at the end of the reporting period, showing how profit or loss and equity would have been affected by changes in the relevant risk variable that were reasonably possible at that date;

(b) the methods and assumptions used in preparing the sensitivity analysis; and (c) changes from the previous period in the methods and assumptions used, and

the reasons for such changes. 41 If an entity prepares a sensitivity analysis, such as value-at-risk, that reflects

interdependencies between risk variables (eg interest rates and exchange rates) and uses it to manage financial risks, it may use that sensitivity analysis in place of the analysis specified in paragraph 40. The entity shall also disclose:

(a) an explanation of the method used in preparing such a sensitivity analysis,

and of the main parameters and assumptions underlying the data provided; and

(b) an explanation of the objective of the method used and of limitations that may

result in the information not fully reflecting the fair value of the assets and liabilities involved.

Other market risk disclosures

42 When the sensitivity analyses disclosed in accordance with paragraph 40 or 41 are

unrepresentative of a risk inherent in a financial instrument (for example because the year-end exposure does not reflect the exposure during the year), the entity shall disclose that fact and the reason it believes the sensitivity analyses are unrepresentative.

Transfers of financial assets 42A The disclosure requirements in paragraphs 42B–42H relating to transfers of financial

assets supplement the other disclosure requirements of this IFRS. An entity shall present the disclosures required by paragraphs 42B–42H in a single note in its financial statements. An entity shall provide the required disclosures for all transferred financial assets that are not derecognised and for any continuing involvement in a transferred asset, existing at the reporting date, irrespective of when the related transfer transaction occurred. For the purposes of applying the

© Copyright 29 HKFRS 7 (September 2018)

disclosure requirements in those paragraphs, an entity transfers all or a part of a financial asset (the transferred financial asset) if, and only if, it either:

(a) transfers the contractual rights to receive the cash flows of that financial asset;

or (b) retains the contractual rights to receive the cash flows of that financial asset,

but assumes a contractual obligation to pay the cash flows to one or more recipients in an arrangement.

42B An entity shall disclose information that enables users of its financial statements:

(a) to understand the relationship between transferred financial assets that are not derecognised in their entirety and the associated liabilities; and

(b) to evaluate the nature of, and risks associated with, the entity’s continuing

involvement in derecognised financial assets. 42C For the purposes of applying the disclosure requirements in paragraphs 42E–42H, an

entity has continuing involvement in a transferred financial asset if, as part of the transfer, the entity retains any of the contractual rights or obligations inherent in the transferred financial asset or obtains any new contractual rights or obligations relating to the transferred financial asset. For the purposes of applying the disclosure requirements in paragraphs 42E–42H, the following do not constitute continuing involvement:

(a) normal representations and warranties relating to fraudulent transfer and

concepts of reasonableness, good faith and fair dealings that could invalidate a transfer as a result of legal action;

(b) forward, option and other contracts to reacquire the transferred financial asset

for which the contract price (or exercise price) is the fair value of the transferred financial asset; or

(c) an arrangement whereby an entity retains the contractual rights to receive the

cash flows of a financial asset but assumes a contractual obligation to pay the cash flows to one or more entities and the conditions in paragraph 19(a)–(c) of HKAS 393.2.5(a)-(c) of HKFRS 9 are met.

Transferred financial assets that are not derecognised in their entirety

42D An entity may have transferred financial assets in such a way that part or all of the

transferred financial assets do not qualify for derecognition. To meet the objectives set out in paragraph 42B(a), the entity shall disclose at each reporting date for each class of transferred financial assets that are not derecognised in their entirety:

(a) the nature of the transferred assets. (b) the nature of the risks and rewards of ownership to which the entity is

exposed. (c) a description of the nature of the relationship between the transferred assets

and the associated liabilities, including restrictions arising from the transfer on the reporting entity’s use of the transferred assets.

(d) when the counterparty (counterparties) to the associated liabilities has (have)

recourse only to the transferred assets, a schedule that sets out the fair value of the transferred assets, the fair value of the associated liabilities and the net

© Copyright 30 HKFRS 7 (September 2018)

position (the difference between the fair value of the transferred assets and the associated liabilities).

(e) when the entity continues to recognise all of the transferred assets, the

carrying amounts of the transferred assets and the associated liabilities. (f) when the entity continues to recognise the assets to the extent of its continuing

involvement (see paragraphs 20(c)(ii) and 30 of HKAS 39paragraphs 3.2.6(c)(ii) and 3.2.16 of HKFRS 9), the total carrying amount of the original assets before the transfer, the carrying amount of the assets that the entity continues to recognise, and the carrying amount of the associated liabilities.

Transferred financial assets that are derecognised in their entirety

42E To meet the objectives set out in paragraph 42B(b), when an entity derecognises

transferred financial assets in their entirety (see paragraph 20(a) and (c)(i) of HKAS 393.2.6(a) and (c)(i) of HKFRS 9) but has continuing involvement in them, the entity shall disclose, as a minimum, for each type of continuing involvement at each reporting date:

(a) the carrying amount of the assets and liabilities that are recognised in the