history of corporate governance by m.h.m.faizer. enterprise governance corporate governance business...

TRANSCRIPT

History of Corporate Governance

by

M.H.M.Faizer

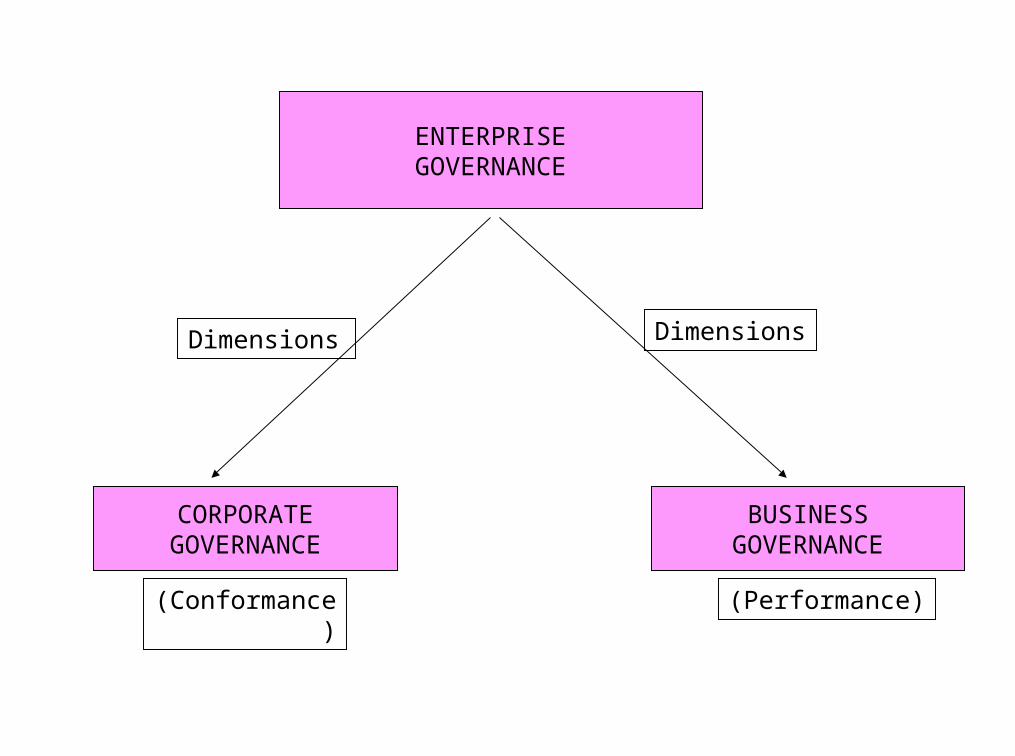

ENTERPRISEGOVERNANCE

CORPORATEGOVERNANCE

BUSINESSGOVERNANCE

The two dimensions need to be in balance !

Dimensions Dimensions

(Conformance) (Performance)

Enterprise Governance

Defined as the set of responsibilities & practices exercised by the board & executive management with the goal of providing strategic decision, ensuring that objectives are achieved, ascertaining that risks are managed appropriately and verifying that organizations resources are used responsibly.

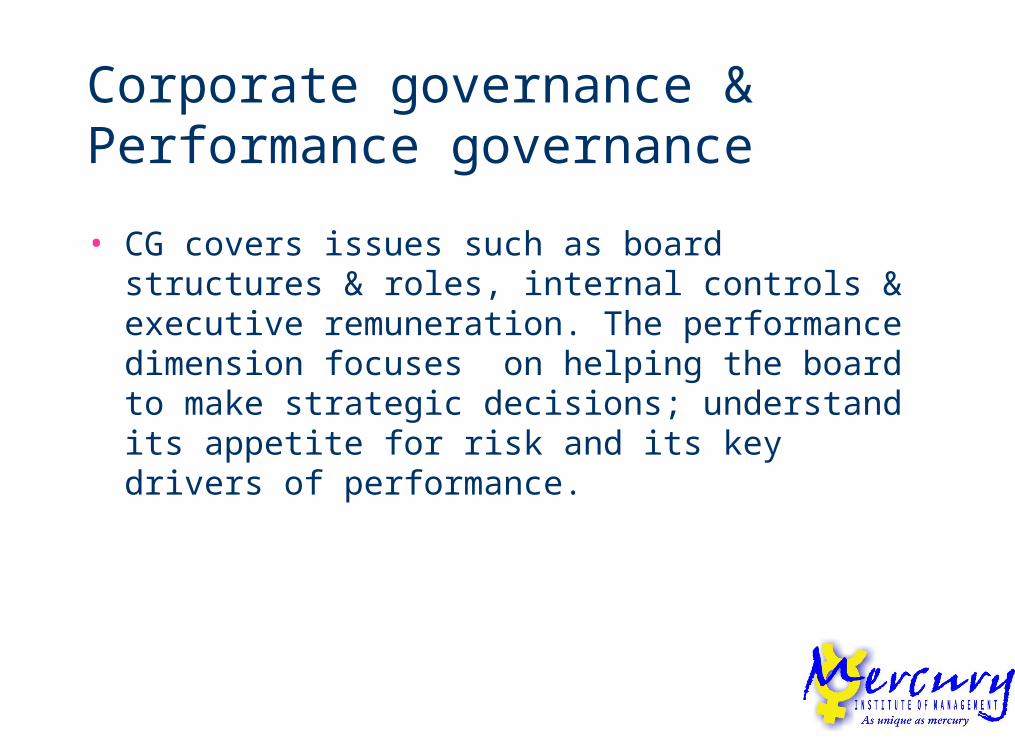

Corporate governance & Performance governance

• CG covers issues such as board structures & roles, internal controls & executive remuneration. The performance dimension focuses on helping the board to make strategic decisions; understand its appetite for risk and its key drivers of performance.

• Corporate Governance is necessary but not sufficient for success. Bad governance can ruin a company but cannot on its own ensure success hence the need for enterprise governance.

Treadway & COSO (USA)

• Issued a report on fraudulent financial reporting in 1987 which confirmed the role & status of Audit committees (a listing requirement) with a majority of non executive directors

• Frame work for internal controls

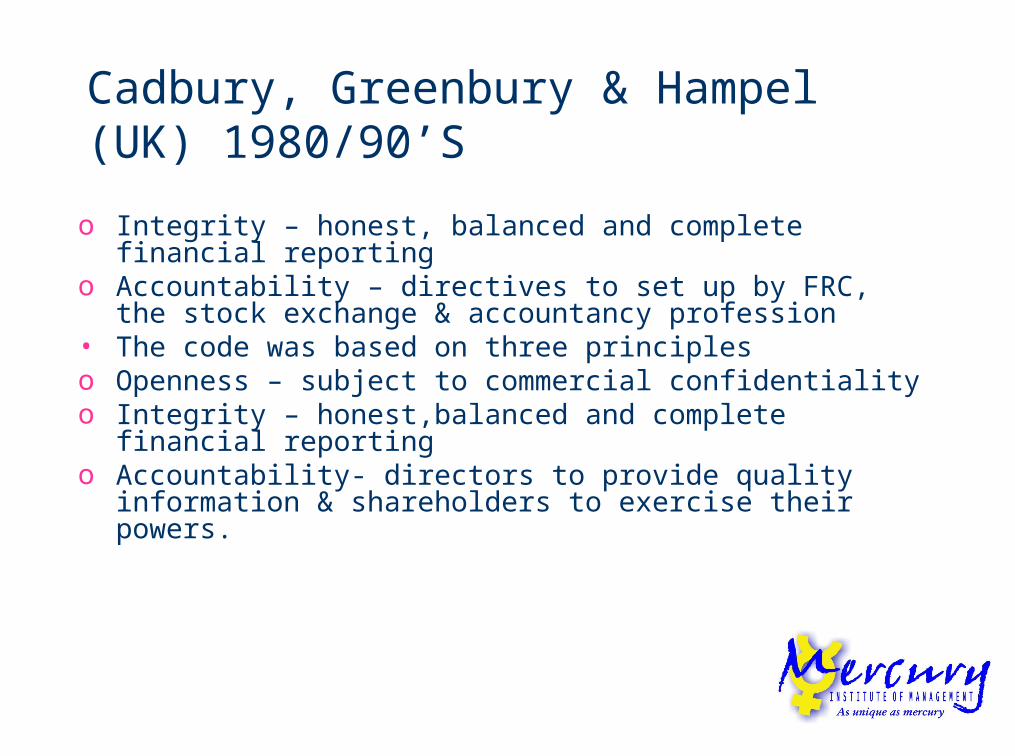

Cadbury, Greenbury & Hampel (UK) 1980/90’S

o Integrity – honest, balanced and complete financial reporting

o Accountability – directives to set up by FRC, the stock exchange & accountancy profession

• The code was based on three principleso Openness – subject to commercial confidentialityo Integrity – honest,balanced and complete financial

reportingo Accountability- directors to provide quality information &

shareholders to exercise their powers.

Cadbury (contd)• Report on financial reporting & accountability of

corporate governance• Responsibility of Executive & Non Executive

directors• Case for Audit committees• Principal responsibilities of Executive & Non

Executive Directors• Links between shareholders, board & auditors

Greenbury (Jan 1995)

• Initiative of CBI (Confederation of British industry)

• Emphasis on determining directors pay• Role of Non Executive Directors

Hampel (Nov.1995)

• Initiative of FRC, Stock Exchange, the CBI & CCAB

• Review Cadbury & propose amendments• Review greenbury & propose amendments• Review role of directors• Address the roles of shareholders & auditors in

the CG• The committee produced a “ Combined Code”

Combined Code

• Directors • Directors remuneration• Accountability & Audit• Relations with shareholders

Directors

• Balance of Executive & Non Executive Directors• Clear division of responsibilities between

Chairman & CEO• Appointments be formal, rigorous & transparent• The Board evaluate its own performance on an

annual basis• Re- election at regular intervals

Directors’ Remuneration

• Remuneration necessary to recruit & retain directors

• Significant portion of Executive Directors’ pay should be performance related

• Policy on remuneration to be clear & transparent

• No director should be involved in determining his/her remuneration

Accountability & Audit

• Board is responsible for presenting a balanced and understandable assessment of the company’s financial position & prospects

• Board is responsible to maintain a sound system of internal controls to safeguard company’s assets & S/H investments

• Financial reporting

• Relationship with external auditors

Benefits of Corporate Governance

• Reduces risk – it provides a mechanism to review risk. It helps to reduce the risk of fraud

• Stimulates performance – it institutes clear accountability & effective links between performance & rewards.

• Improves access to capital markets- corporate governance is seen as protecting shareholders rights.

• Enhances the marketability of goods & services – it creates confidence among the shareholders, customers & suppliers, etc…

• Improves leadership – appointments of NED’S - wider pool of knowledge

• Demonstrating transparency & social accountability

Corporate governance in South Asia

Bangladesh

• Market Capitalization USD 3.8 Billion (6.8% of GDP )

• 277 Securities listed in DSE• 198 Securities listed in CSE• 49 Banks & 28 Non Banking Institutions• 44 State owned enterprises

(60 Privatized )

Bangladesh contd…..

• Awareness was low (2002) but now…..• Legal framework : company’s Act 1994• SEC Act 1993

Corporate Governance Initiatives• Bangladesh Bank directives• National Taskforce on corporate governance• Code of corporate governance• SEC guidelines• Role of World Bank & Asian Development Bank• In 2002, Bangladesh Enterprise Institute

examined the current state of corporate governance & practices in South Asia(OECD Principles of Corporate governance as benchmark )

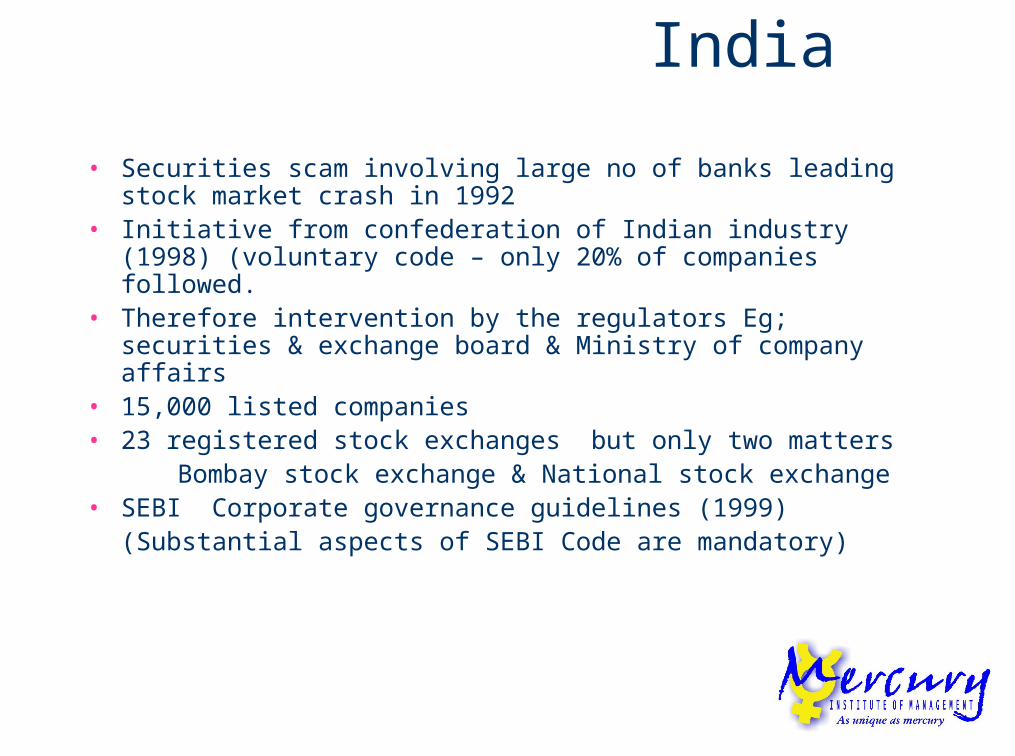

India • Securities scam involving large no of banks leading stock

market crash in 1992• Initiative from confederation of Indian industry (1998)

(voluntary code – only 20% of companies followed.• Therefore intervention by the regulators Eg; securities &

exchange board & Ministry of company affairs• 15,000 listed companies• 23 registered stock exchanges but only two matters Bombay stock exchange & National stock exchange • SEBI Corporate governance guidelines (1999)

(Substantial aspects of SEBI Code are mandatory)

Sri Lanka• Numerous company failures specially finance

companies in late 1980’s & 1990’s• Taskforce set up in 1992 by ICA followed by a

committee in 1996• Code of best practice on CG – 1997 by ICA• Setting up of the SL Accounting & Auditing

Standards (ICL) Act No 15 of 1995• SEC – to develop standards of financial

reporting

Sri Lanka Contd….

• 1997 – Initiated by Institute of Chartered Accountants together with

• Colombo Stock Exchange• Securities Exchange Commission• Ceylon Chamber of Commerce• Institute of Directors of Sri Lanka • ( voluntary best practice code)• Listed companies, unit trusts, fund management

companies, finance companies, Banks, insurance companies were expected to adopt the code.

• ( Primarily based on Cadbury Report)

Sri Lanka Contd…

• Areas Covered1) Effectiveness of the board2) The Chairman3) Non – Executive Directors4) Professional Advice5) Directors’ Training6) Directors Responsibilities for Financial

Statements7) Compliance Report8) Internal Controls9) Committee structure for Board

Sri Lanka Contd….

• Code of best practice on Audit Committees (2002)

Initiated by ICL A separate code covering Audit committees was

introduced Based on the combined code (UK)

Sri Lanka Contd…

• Areas Covered1) Effectiveness of the board2) The Chairman3) Non – Executive Directors4) Professional Advice5) Directors’ Training6) Directors Responsibilities for Financial

Statements7) Compliance Report8) Internal Controls9) Committee structure for Board

Sri Lanka Contd….

• Code of best practice on Audit Committees (2002)

Initiated by ICL A separate code covering Audit committees was

introduced Based on the combined code (UK)

SL Contd…• Revision of Corporate Governance Code 1997

• In 2003

• Applicability to all companies under companies Act

• Functions of the board – revisited• Disclosure of major transactions• Introduced performance evaluation

Sri Lanka contd

• Guidelines for listed companies(Audit or Audit Committees)

In 2004 Deals mostly with external Auditor related

issues(Qualification & appointment, power,

Remuneration, Rotations, conflict of interest). Audit committees, Financial reporting

requirements

Further Revision (code of best practice) In 2006 To include latest developments of the

combined code (UK) & NYSE listed co. manual, Singapore, Malaysia, India etc..

Specific new inclusions:I. Code of ethics for directors & senior

managersII. Specific board related DisclosuresIII. Audit committee aspects are strengthenedIV. Director Independence criteria is specified

Major Corporate Collapses

UK : The Maxwell publishing group BCCI Marconi USA : Enron

World Com Tyco

Germany : Berliner Bank Babcok

Australia : OneTel Ansett Airlines

Lessons of Experience

Lesson i : Corporate Governance cannot be introduced in isolation from a range of other reforms. Nor can these reforms achieve all their objectives without CG initiatives

Lesson ii : The need to monitor the trends in different sectors of the market so as to try & avoid a “perfect storm”

Lesson iii : need for range of players to improve CG.

Lesson iv : a degree of “stick” may be needed with “carrots” of increased investment & performance

Lesson v : critical importance of company & contract

laws & efficacy of the legal system.