high-tech services to companies in the city: therise of the modern economy in brazil

TRANSCRIPT

High-tech services to companies in the city: therise of the modern economy in Brazil

Ana Maria Bonomi Barufi

NEREUS – University of São Paulo, Brazil

Smart People in Smart Cities

Banská Bystrica

August 28-30, 2016

Industry-Space: the dynamics of industrial development

• R1: agriculture share in GDP is high

• R2: urbanization requires industrial development, as well as services for final consumption

• R3: breaking the middle income trap –diversification in the demand from families for services, and industrial development demands new types of services – increase industrial density, decreases manufacture/GDP, increase in commercial services/GDP.

• R4: more advanced industrial development –increased industrial density and more commercial services, while industry/GDP decreases even more. Industry invests on innovations in the service sector (IoT, big data, cloud computing, etc.) - Helper et al. (2012)

Industrial share in GPD (%) – D1

Ind

ust

rial

Den

sity

–D

2

Co

mm

ercial se

rvices share in

GD

P –

D3

R1 R2

R3R4

Source: Arbache (2012)

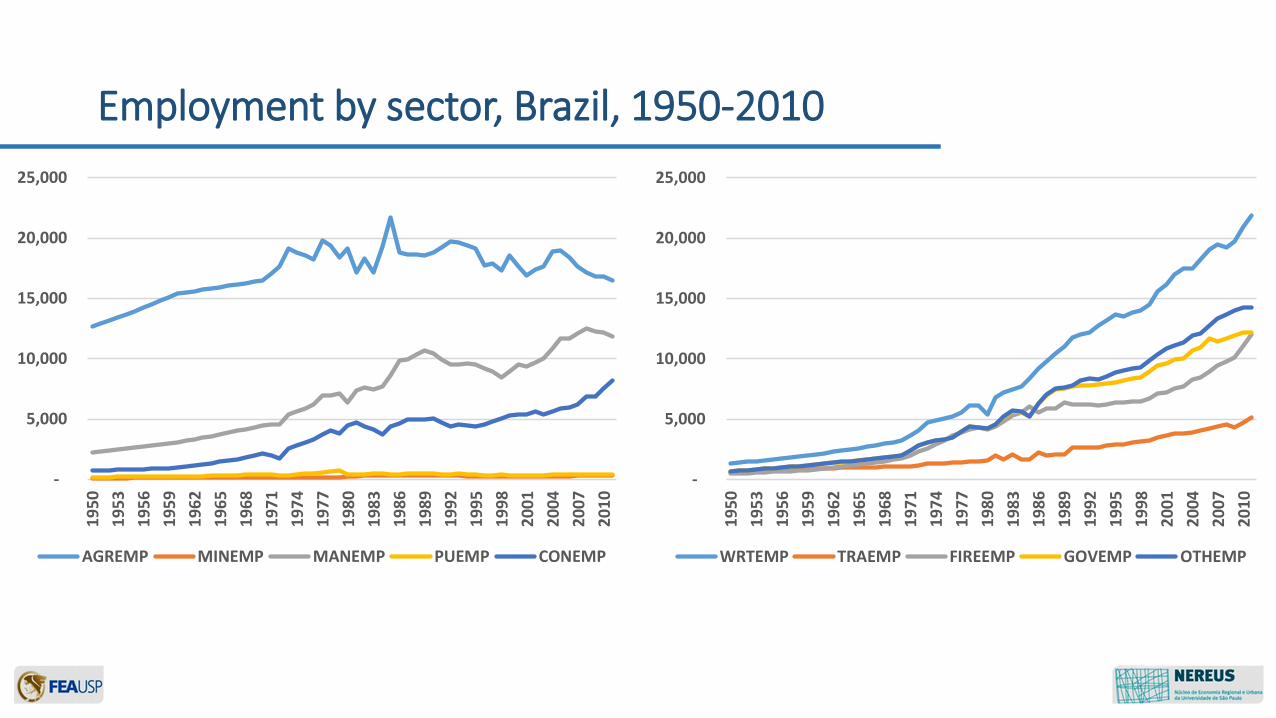

Employment by sector, Brazil, 1950-2010

-

5,000

10,000

15,000

20,000

25,000

19

50

19

53

19

56

19

59

19

62

19

65

19

68

19

71

19

74

19

77

19

80

19

83

19

86

19

89

19

92

19

95

19

98

20

01

20

04

20

07

20

10

WRTEMP TRAEMP FIREEMP GOVEMP OTHEMP

-

5,000

10,000

15,000

20,000

25,000

19

50

19

53

19

56

19

59

19

62

19

65

19

68

19

71

19

74

19

77

19

80

19

83

19

86

19

89

19

92

19

95

19

98

20

01

20

04

20

07

20

10

AGREMP MINEMP MANEMP PUEMP CONEMP

% Employment by sector, Brazil, 1950-2010

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

19

50

19

53

19

56

19

59

19

62

19

65

19

68

19

71

19

74

19

77

19

80

19

83

19

86

19

89

19

92

19

95

19

98

20

01

20

04

20

07

20

10

s_AGREMP s_MINEMP s_MANEMP s_PUEMP s_CONEMP

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

19

50

19

53

19

56

19

59

19

62

19

65

19

68

19

71

19

74

19

77

19

80

19

83

19

86

19

89

19

92

19

95

19

98

20

01

20

04

20

07

20

10

s_WRTEMP s_TRAEMP s_FIREEMP s_GOVEMP s_OTHEMP

• Services may reduce costs and/or add value to manufacturing

• Services in Brazil have one of the highest shares in the economy in the developing world – close to developed economies, but with a different composition

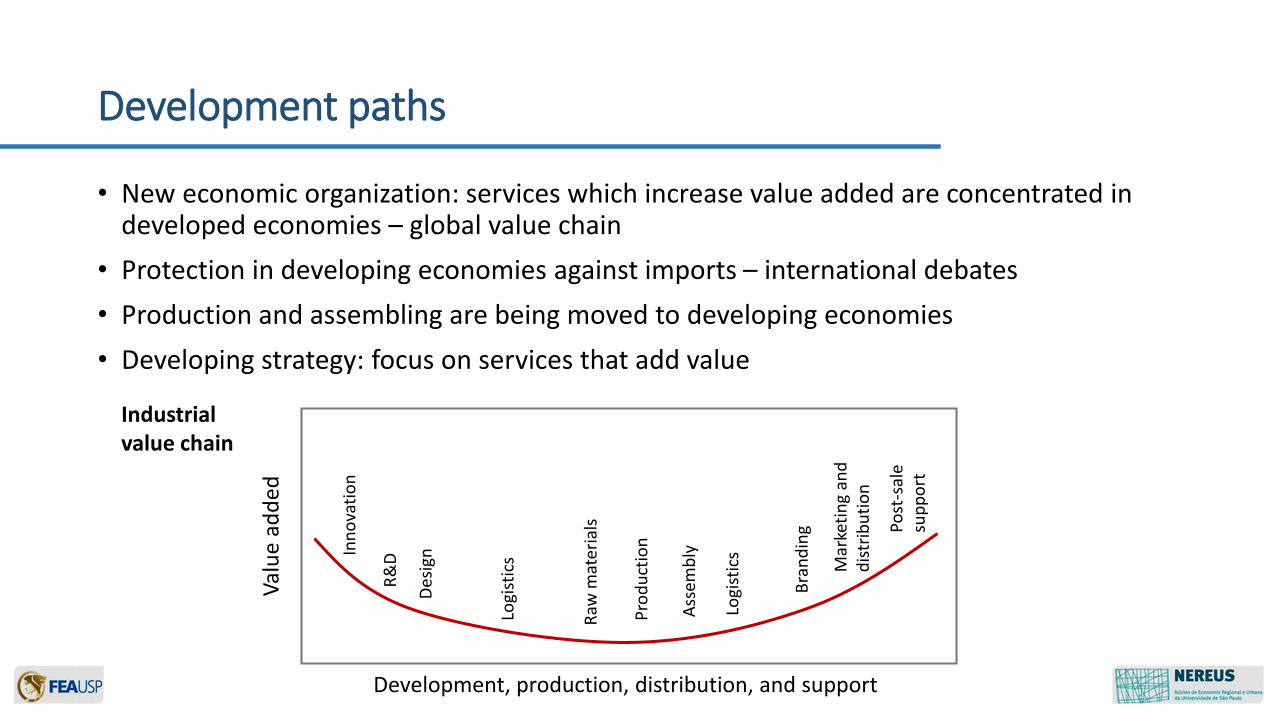

Development paths

• New economic organization: services which increase value added are concentrated in developed economies – global value chain

• Protection in developing economies against imports – international debates

• Production and assembling are being moved to developing economies

• Developing strategy: focus on services that add value

Development paths

Inn

ova

tio

n

Development, production, distribution, and support

Val

ue

add

ed

R&

D

Des

ign

Logi

stic

s

Raw

mat

eria

ls

Pro

du

ctio

n

Ass

emb

ly

Logi

stic

s

Bra

nd

ing

Mar

keti

ng

and

d

istr

ibu

tio

n

Post

-sal

e su

pp

ort

Industrial value chain

• Opportunity-motivated entrepreneurship tends to flourish in urban regions with high levels of economic growth and diversity of economic activities (Bosma and Sternberg, 2014)

• High growth firms tend to be favoured by different factors than firms in general (Li et al., 2015)

• ICT firms co-locate and benefit from knowledge spillovers (Lasch et al., 2011)

Empirical Literature

Data

• RAIS database• Demographic Census• REGIC areas

• Main variables• Industry mix firm growth• Urbanization• Education• Unemployment• Density• Sector composition• RegionLong time lags to avoid endogeneity (still may be an issue)

Sectors: • IT• information services• management consultancy• arquitecture and engineering• R&D• marketing• other professional activities

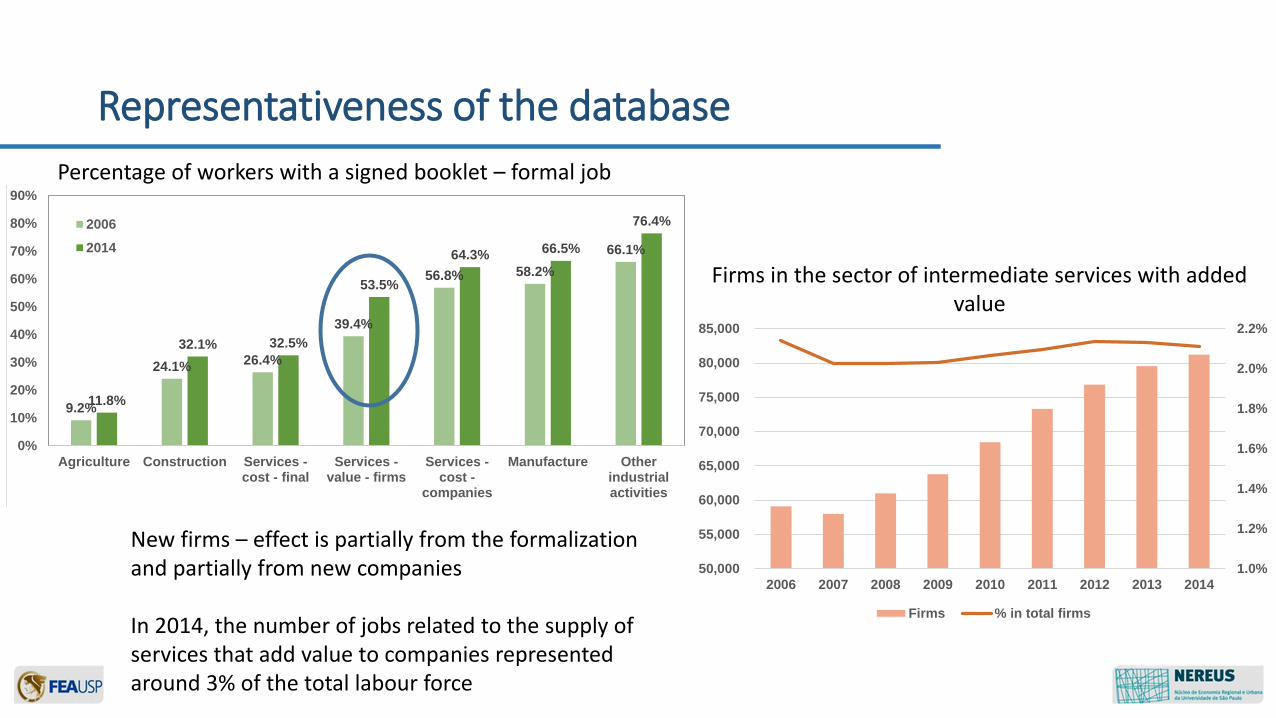

Representativeness of the database

9.2%

24.1%26.4%

39.4%

56.8% 58.2%

66.1%

11.8%

32.1% 32.5%

53.5%

64.3%66.5%

76.4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Agriculture Construction Services -cost - final

Services -value - firms

Services -cost -

companies

Manufacture Otherindustrialactivities

Título do Gráfico

2006

2014

Percentage of workers with a signed booklet – formal job

New firms – effect is partially from the formalization and partially from new companies

In 2014, the number of jobs related to the supply of services that add value to companies represented around 3% of the total labour force

1.0%

1.2%

1.4%

1.6%

1.8%

2.0%

2.2%

50,000

55,000

60,000

65,000

70,000

75,000

80,000

85,000

2006 2007 2008 2009 2010 2011 2012 2013 2014

Firms % in total firms

Firms in the sector of intermediate services with added value

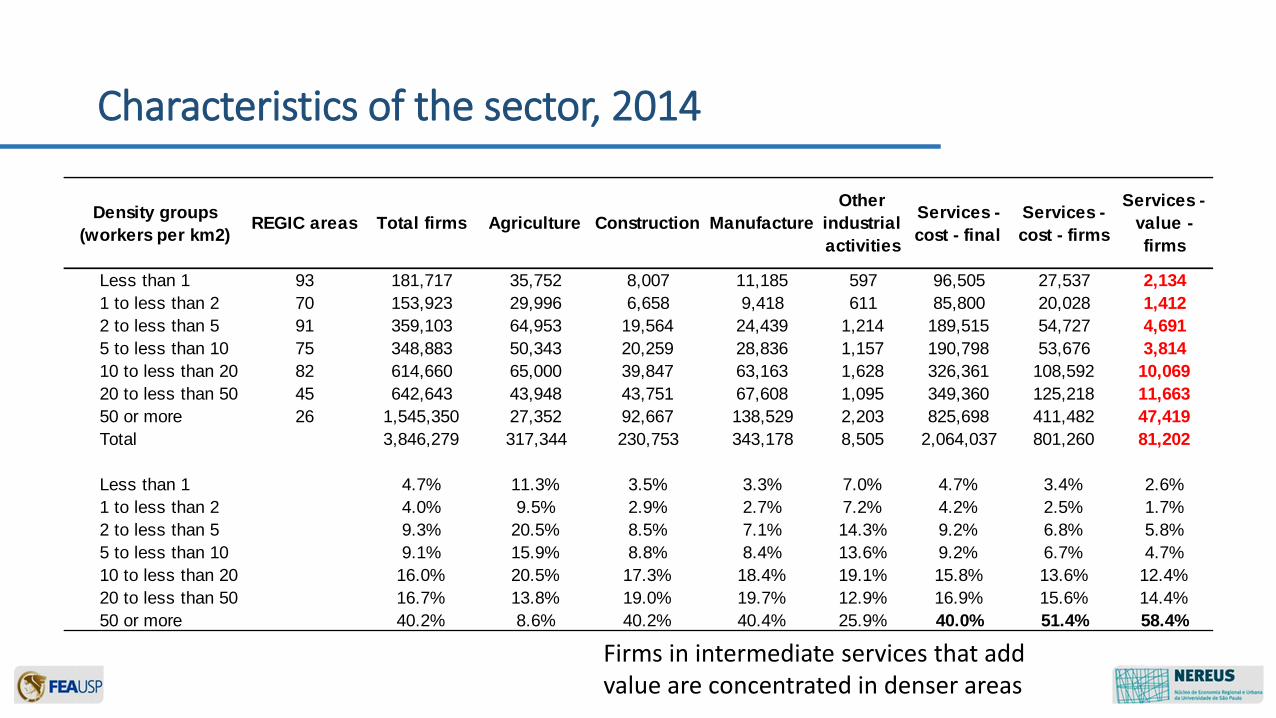

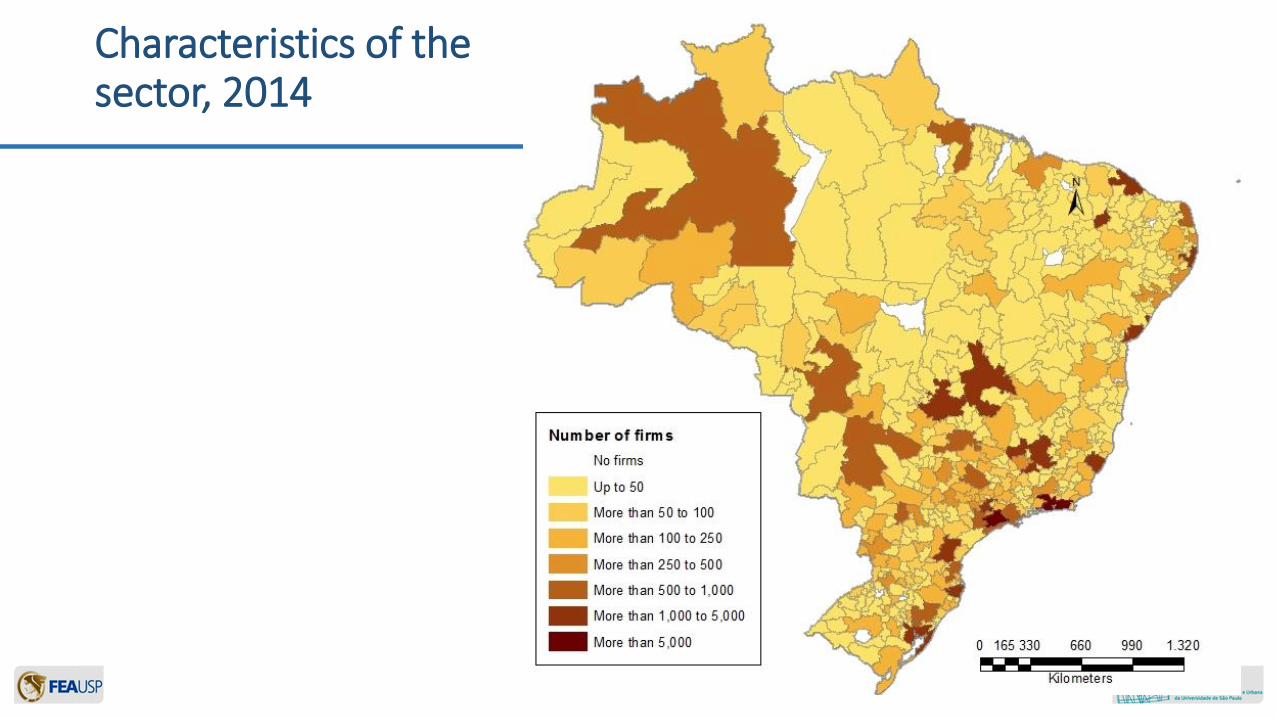

Characteristics of the sector, 2014

Firms in intermediate services that add value employ more educated workers

3.1%

5.3%

9.5%

14.5%

21.3%

25.3%

38.4%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0%

Agriculture

Construction

Manufacture

Services - cost - companies

Other industrial activities

Services - cost - final

Services - value - firms

% with bachelor

Characteristics of the sector, 2014

Firms in intermediate services that add value are concentrated in denser areas

Density groups

(workers per km2)REGIC areas Total firms Agriculture Construction Manufacture

Other

industrial

activities

Services -

cost - final

Services -

cost - firms

Services -

value -

firms

Less than 1 93 181,717 35,752 8,007 11,185 597 96,505 27,537 2,134

1 to less than 2 70 153,923 29,996 6,658 9,418 611 85,800 20,028 1,412

2 to less than 5 91 359,103 64,953 19,564 24,439 1,214 189,515 54,727 4,691

5 to less than 10 75 348,883 50,343 20,259 28,836 1,157 190,798 53,676 3,814

10 to less than 20 82 614,660 65,000 39,847 63,163 1,628 326,361 108,592 10,069

20 to less than 50 45 642,643 43,948 43,751 67,608 1,095 349,360 125,218 11,663

50 or more 26 1,545,350 27,352 92,667 138,529 2,203 825,698 411,482 47,419

Total 3,846,279 317,344 230,753 343,178 8,505 2,064,037 801,260 81,202

Less than 1 4.7% 11.3% 3.5% 3.3% 7.0% 4.7% 3.4% 2.6%

1 to less than 2 4.0% 9.5% 2.9% 2.7% 7.2% 4.2% 2.5% 1.7%

2 to less than 5 9.3% 20.5% 8.5% 7.1% 14.3% 9.2% 6.8% 5.8%

5 to less than 10 9.1% 15.9% 8.8% 8.4% 13.6% 9.2% 6.7% 4.7%

10 to less than 20 16.0% 20.5% 17.3% 18.4% 19.1% 15.8% 13.6% 12.4%

20 to less than 50 16.7% 13.8% 19.0% 19.7% 12.9% 16.9% 15.6% 14.4%

50 or more 40.2% 8.6% 40.2% 40.4% 25.9% 40.0% 51.4% 58.4%

Characteristics of the sector, 2014

Characteristics of the sector, 2014

Firms in intermediate services that add value are concentrated in denser areas

Constant 0.288*** 0.623 5.985*** 0.598 -2.966** 2.127

Unemployment rate 2000 0.352 4.035** 3.606** 1.905 -4.256 -4.613

% Bachelor (25 or more) 2000 2.048*** 18.155*** 15.868*** 5.298*** 30.979*** 24.488***

% Urban population 2000 -0.183 0.656 0.665 -1.152** 3.290** 4.120**

% Firms of interm. services value added 2006 21.018*** 101.270*** 62.787*** 28.483*** 113.083*** 77.206***

% Firms in manufacturing 2006 0.187 2.728** 1.945* 0.884 2.979 1.659

% Firms in other services 2006 -0.004 -0.400 -0.522 0.032 3.832** 3.137**

Density (formal employment 2005)

Less than 1 (reference)

1 to less than 2 0.069** 0.397** 0.234*

2 to less than 5 0.067** 0.496*** 0.363***

5 to less than 10 0.138*** 0.611*** 0.382**

10 to less than 20 0.165*** 0.739*** 0.473** 0.000 0.000 0.000

20 to less than 50 0.268*** 0.575* 0.246 0.054 -0.577** -0.608**

50 or more 0.409*** 1.286*** 0.944*** 0.110 -0.622* -0.629*

Macro-region dummies Yes Yes Yes Yes Yes Yes

N 482 471 471 101 101 101

Adj R-squared 0.641 0.662 0.586 0.651 0.768 0.690

Only REGIC with density >= 10

LQ

services

value

added

Firms

value

added

All firms

LQ

services

value

added

Firms

value

added

All firmsPreliminary results

Results

• Many firms locate in state capitals

• Firms locate in places with originally better conditions for productivity

• Denser places

• Education and pre-existing firms attract them more

Future steps

• Narrow down to the firm level – relocation, new firms, employment growth

• Within the city – what are the additional impacts of this sector? Are there effects in productivity at the neighbourhood?

Thank you ;)