hfs blueprint report - accenture.com · introduction to the 2016 hfs blueprint report: ... •...

TRANSCRIPT

The Services Research Company

Reetika JoshiResearch Director, Operations & Analytics [email protected]

HfS Blueprint Report

Mortgage As-a-ServiceExcerpt for Accenture

July 2016

ConfidentialandProprietary│Page1©2016HfSResearchLtd.ExcerptforAccenture

Table of Contents

TOPIC PAGE

ExecutiveSummary 2

MarketOverview 8

Journeyto MortgageAs-a-Service 16

ResearchMethodology 29

Service ProviderAnalysis 34

MarketDirectionandRecommendations 38

About theAuthor 46

ConfidentialandProprietary│Page2

Executive Summary

Proprietary│Page3©2016HfSResearchLtd.ExcerptforAccenture

Introduction to the 2016 HfS Blueprint Report: Mortgage As-a-Servicen The Mortgage As-a-Service Blueprint for 2016 is an analysis of the business process services and

outsourcing market for mortgage. This Blueprint builds on the Mortgage BPO Blueprint report wepublished in 2014, reviewing in more detail the market and service provider adoption of the EightIdeals of the As-a-Service Economy for redefining the value of sourcing engagements.

n This Blueprint covers market trends direction, as well as analysis of 11 service providers. Unlikeother quadrants and matrices, the HfS Blueprint identifies relevant differentials between serviceproviders across a number of facets under two main categories: innovation and execution.

n For this 2016 report, HfS has increased the attention paid to innovation criteria in particular andadopted the new 2016 Blueprint Grid layout to assess service providers. This Grid nowrecognizes up-and-coming service providers (High Potentials) that are scoring higher oninnovation criteria than on execution criteria as the providers invest and collaborate with clientsand in services that move to a more business outcome-focused, flexible, and talent- andtechnology-enabled mortgage operations.

n The Grid includes a new grouping for established, high-execution service providers (ExecutionPowerhouses) that have maintained effective delivery operations but need to innovatecapabilities and offerings further. That is in addition to the existing rankings for highest overallperformance (Winner’s Circle) and a strong combination of innovation and executionperformance (High Performers).

Proprietary│Page4©2016HfSResearchLtd.ExcerptforAccenture

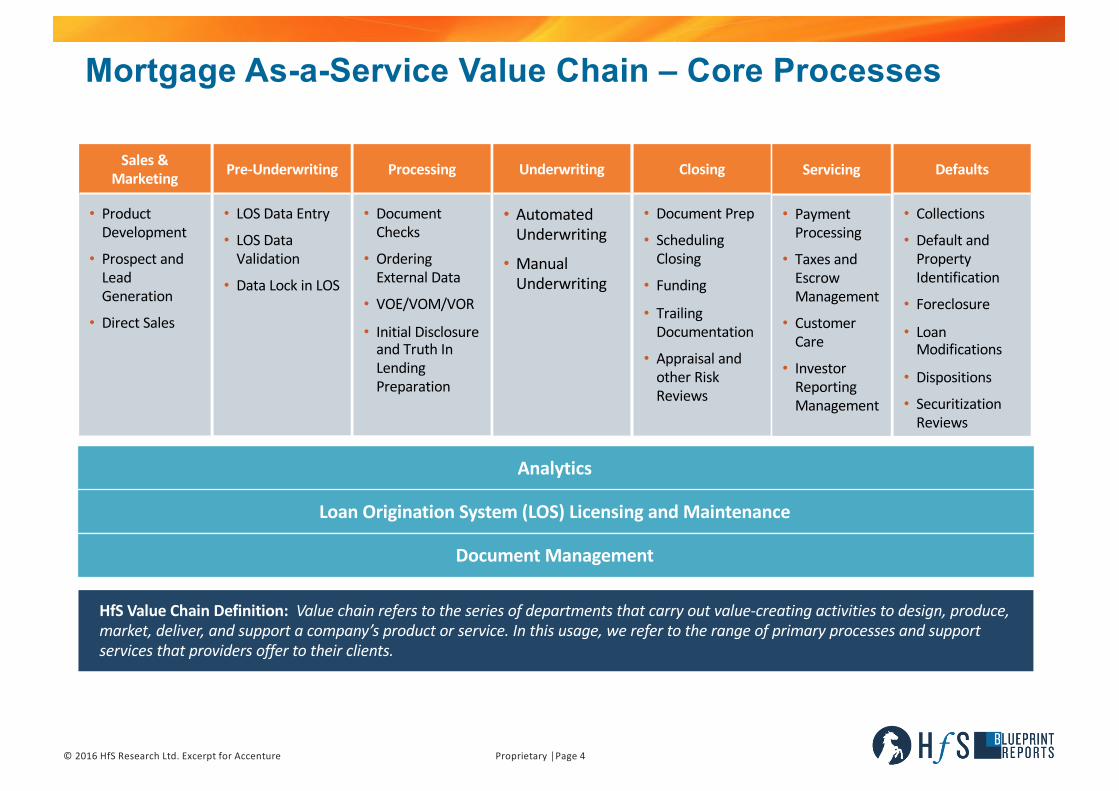

Sales&Marketing

• ProductDevelopment

• ProspectandLeadGeneration

• DirectSales

Pre-Underwriting

• LOSDataEntry

• LOSDataValidation

• DataLockinLOS

Processing

• DocumentChecks

• OrderingExternalData

• VOE/VOM/VOR

• InitialDisclosureandTruthInLendingPreparation

Underwriting

• AutomatedUnderwriting

• ManualUnderwriting

Closing

• DocumentPrep

• SchedulingClosing

• Funding

• TrailingDocumentation

• AppraisalandotherRiskReviews

Servicing

• PaymentProcessing

• TaxesandEscrowManagement

• CustomerCare

• InvestorReportingManagement

Defaults

• Collections

• DefaultandPropertyIdentification

• Foreclosure

• LoanModifications

• Dispositions

• SecuritizationReviews

Analytics

LoanOriginationSystem(LOS)LicensingandMaintenance

DocumentManagement

Mortgage As-a-Service Value Chain – Core Processes

HfSValueChainDefinition:Valuechainreferstotheseriesofdepartmentsthatcarryoutvalue-creatingactivitiestodesign,produce,market,deliver,andsupportacompany’sproductorservice.Inthisusage,werefertotherangeofprimaryprocessesandsupportservicesthatprovidersoffertotheirclients.

Proprietary│Page5©2016HfSResearchLtd.ExcerptforAccenture

Executive Summaryn AnIndustryRecognizingtheNeedforChange:Weseeamarkeddepartureinthemarket

dialogue,awayfromlaborarbitrageandmanual“liftandshift”processes,andtowardsusingacombinationoftechnologyplatforms,analyticalinsights,automation,digitizationandotheracceleratorstoredesignprocessesanddrivemorevalueinsourcingengagements.Severallendersinourresearchdescribedtheirmortgageprocessesascomplex,brokenandinneedofhelptocompetewithnon-traditionallendersandfastercycletimes.Saidone,“Ourindustryneedstogothroughmassivebusinessprocessreengineeringefforts…somanylendersdon’thaveprocessesdocumentedstill,weneedtostartthere,findwaystoimprovecycletimesandcreatebetterexperiencesforborrowers.”

n RegulationIsDrivingNewAreasofDemand:TheConsumerFinancialProtectionBureauintheU.S.iscontinuingtorolloutregulatoryreformforfinancialinstitutions,suchasitsOctober2015HomeMortgageDisclosuresActamendmentstodictatehowlendersmaintain,report,andpubliclydiscloseinformationaboutmortgages.• Leadingtechnologyandserviceprovidersarestartingtoproactivelymonitortheseindustry

changesandisanareaclientsexpectmoreguidanceandrecommendationsfromthem,e.g.howthedisclosureswouldaffectLOSsystemsanddataflowstomaintaincompliance.

• Additionally,theauditandduediligencereportingbacktoCFPBisincreasinglygettingmorecomplicatedandfrequent,makingitchallengingforlenderstokeeppacewithassurance.Weseeservicesandacceleratorscomingfromserviceproviderstoaddressthisregulatorypressure.

• WealsoseemultipleserviceprovidersstarttousespeechanalyticsandotherIntelligentAutomationcapabilitiestosignificantlyimprovecompliancetestingduringcallmonitoringandQAactivitiesincallcenters.

Proprietary│Page6©2016HfSResearchLtd.ExcerptforAccenture

Executive Summary (contd.)

n Some Service Expansion Since 2014: The 2014 Mortgage BPO Blueprint found that serviceproviders had strengths in certain parts of the mortgage value chain, in particular, servicing andfulfilment in the refinance category, with limited interest in foreclosure-default management.• With greater purchase originations, we see the mortgage operations market become more

broad-based in the work sought from lenders.• Accordingly, service providers have grown both their technology and process capabilities in

originations and servicing in the last two years, with a couple that have foreclosure anddefault management work today.

• State licenses are required to have more of an end-to-end portfolio in originations, fromprocessing, underwriting to closing/post-closing. This is an area where a number of serviceproviders are trying to actively close gaps today. We expect the majority of providersfocused on this market to complete acquiring requisite licenses in the next year to meetclient demands.

• Residential markets continue to be the mainstay of most mortgage operations workoutsourced today. There are a couple of service providers (Accenture, Wipro) that have thedeep domain capabilities to venture into commercial real estate and other areas ofconsumer lending.

Proprietary│Page7©2016HfSResearchLtd.ExcerptforAccenture

n As-a-Service Winners are service providers that have thestrongest vision for As-a-Service delivery in the mortgageindustry, and are driving collaborative engagements withclients to bring the vision to life. They are makingsignificant investments in future capabilities inautomation, technology and borrower experiencemanagement to continue to increase the value over time:

• Accenture, Cognizant, TCS, Wipron The High Performers have high execution capabilities, are

growing their client bases as a result of investments infuture capabilities and innovation. These serviceproviders have the pieces in place for As-a-Servicedelivery, and need to focus on consistently bringing thesecapabilities to clients and scaling up with broad, multi-client solutions:

• Genpact, Infosys, ISGN/Firstsource, SutherlandGlobal Services, WNS

n The Execution Powerhouses are strong in operationalexcellence with ubiquitous technology platforms in theirrespective markets, and need to focus on value chainexpansion and innovation in their services stack:

• Unisys, Xerox

AS-A-SERVICEECONOMY

Useofoperatingmodels,enablingtechnologiesandtalenttodrivebusinessoutcomesthroughoutsourcing.Thefocusisonwhatmatterstotheendconsumer.

HfSusestheword“economy”todescribethenextphaseofoutsourcingasanewwayofengagingandmanagingresourcestodeliverservices.

The8IdealsoftheAs-a-ServiceEconomy:1. Write OffLegacy2. DesignThinking3. IntelligentEngagement4. BrokersofCapability5. IntelligentAutomation6. AccessibleandActionableData7. Holistic Security8. Plug-and-PlayDigitalServices

Source:BewareoftheSmoke:YourPlatformIsBurningbyHfSResearch,2015

State of the Mortgage As-a-Service Market

ConfidentialandProprietary│Page8

Market Overview

Proprietary│Page9©2016HfSResearchLtd.ExcerptforAccenture

The Mortgage Industry Is Staring At Significant Transformationn Regulationandhomebuyersaresteadilyshiftingtheentiremortgageindustrytowardsbeing

moredigitallyenabled.AnexampleofthechangecanbefoundwithBillEmerson,CEOofQuickenLoans,steppinginlatelastyear asthe2016ChairmanoftheMortgageBankersAssociation.Quickenisheraldedasoneofthedisruptiveforcesinthemortgagecompetitivelandscapethatisdrivingthenextwaveofmortgagebuying.Whataretheydoingdifferently?Reorientinginteractionsaroundborrowers—arevolutionaryconceptforanindustrysteepedintradition,usedtosettingthetermsforallpartiesintheloanlifecycleincludingborrowers.

n Newgenerationsofmillennialhomebuyersaswellasoldertechnologically-savvyborrowersinterpretthatreorientationasenabling“digital,”likeningittootherexperiencestheyalreadyenjoyintheirconsumerlives.E-mortgage/e-closinghasexistedasaconceptforawhile,butithasmostlybeenlimitedtoamovetodigitizationandonlineformsfrompaperbaseddocumentationandreviews.

n Thismovetopaperlessdeliveryisstillanongoingeffort,especiallyasregulationforcesmoredisclosuresandinformationintothehandsofpotentialhomebuyers.Butfundamentally,theborrowerexperiencehasremainedstatic.Inbecomingdigitallydriven,lendershavealongwaytogointhinkingaboute-mortgagebeyonddigitization,andborrowerexperiencesthatarebuiltonnewengagementstrategies,especiallyasthemarketshiftstomorepurchaseoriginations.

Proprietary│Page10©2016HfSResearchLtd.ExcerptforAccenture

This Creates An Opportunity For Service Providers To Help Lenders Create Competitive Advantagesn Borrowersareincreasinglylookingforthreekeybenefitsintheirinteractionswithagents,

brokers,andlenders:• Simplification intheprocesses,handoffsandinteractions• Transparency intheloantermsandcosts,applicationprogress• Control indocumentandinformationexchanges,decisionmaking

n Thisdoesn’timplythatallmortgageactivitywilltransitiontodigitalinthenearfuture.Tothecontrary,theinfrequentandcomplexnatureofhomebuyingoftendemands‘hightouch’customerserviceandadvocacy,especiallyforfirst-timehomebuyers.

n Eveninthesecases,however,theuseofdigitaltechnologycangreatlyhelp,inbothfacilitatinginteractionsandincreatingoperationalefficienciesattheback-endtospeedupapplicationsandfreeuploanofficers’time.Emersonhasstated thatthemoreefficientandeffectivetheback-officeisbyusingtechnology,thebetteralenderwilldointhemarketplace.

Proprietary│Page11©2016HfSResearchLtd.ExcerptforAccenture

This Creates An Opportunity For Service Providers To Help Lenders Create Competitive Advantages, Continuedn Thisimpactstheserviceproviderlandscapethatrunsmortgageoperations,asfinancial

institutionsconsider:• StrategiesandoperationsInorigination,servicingandforeclosure-defaultmanagement

thatfocusonborrowerexperience• Removingcostacrosstheboardbutespeciallyinorigination• Scalinginternalcapacitiestonewmarketvolumesandsourcingforvolatility• Addressingbrokenorinefficientprocessesespeciallywithautomation• Replacingexistingloan/servicingplatformsorfindingenablingtechnologiestosolvefor

gaps• Lookingfordeeperinsightsontheiroperationsandtheirportfolios

Proprietary│Page12©2016HfSResearchLtd.ExcerptforAccenture

30 Year Rates Continue Downward– and Are At A 3 Year Low Currently

8.05%

6.97%6.54%

5.83%5.94%

5.87%6.41% 6.34%

6.03%

5.04%4.69%4.45%

3.66%3.98%

4.34%3.85%3.60%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Average30YearMortgageRates(%),UnitedStates2000-2016

Source:FreddieMac.2016dataisforMay2016,allothersareannualaveragerates

Proprietary│Page13©2016HfSResearchLtd.ExcerptforAccenture

$-

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

1Q2011

2Q2011

3Q2011

4Q2011

1Q2012

2Q2012

3Q2012

4Q2012

1Q2013

2Q2013

3Q2013

4Q2013

1Q2014

2Q2014

3Q2014

4Q2014

1Q2015

2Q2015

3Q2015

4Q2015

The Rising Costs of Mortgage Origination Are Draining ProfitabilityNetCosttoOriginateANewMortgage($)

Source:MortgageBankersAssociation,The“netcosttooriginate”includesallproductionoperatingexpensesandcommissionsminusallfeeincome

Proprietary│Page14©2016HfSResearchLtd.ExcerptforAccenture

$1,399

$1,140

$731 $664$530 $505

$587$734 $760

$881$973 $1,011

$1,326

$1,166

$777

$1,331

$1,168

$931

$1,456

$1,111

$503

$749 $690

$372

$-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016e 2017e

Purchase Refinance

However, The Mix Is Changing: Purchase Originations Are Steadily Eclipsing RefinanceMortgageOriginationEstimates($Billions),One- tofour-familyhomes

Source:MortgageBankersAssociation

Proprietary│Page15©2016HfSResearchLtd.ExcerptforAccenture

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

2006-07-01

2006-12-01

2007-05-01

2007-10-01

2008-03-01

2008-08-01

2009-01-01

2009-06-01

2009-11-01

2010-04-01

2010-09-01

2011-02-01

2011-07-01

2011-12-01

2012-05-01

2012-10-01

2013-03-01

2013-08-01

2014-01-01

2014-06-01

2014-11-01

2015-04-01

2015-09-01

Delinquency Rates Are Steadily Dropping Due To The Rebounding EconomyDelinquencyRateonLoansSecuredbyRealEstate,Top100Banks

Source:FederalReserveBankofStLouis

Journey to Mortgage As-a-Service

©2016HfSResearchLtd.ExcerptforAccenture

TOOLS/INFRASTRUCTURE GOVERNANCE

Welcome to the As-a-Service EconomyHfSusestheword“economy”toemphasizethattheemergingnextphaseofoutsourcingisamoreflexible,outcomefocusedwayofengagingandmanagingresourcestodeliverservices.OperatingintheAs-a-ServiceEconomymeansarchitectinguseofincreasinglymatureoperatingmodels,enablingtechnologiesandtalenttodrivetargetedbusinessoutcomes.Thefocusisonvaluetotheconsumer.

I.THEOPTIMUMOPERATINGMODEL

Outsourcing|SharedServicesGBS|BPaaS/SaaS/IaaS|Crowdsourcing

II.EMPOWERINGTALENTTOMAKEITALL

POSSIBLECapabilitiesoverSkills|

DefiningOutcomes|Creativity|DataScience

IV.TECHNOLOGYTOAUGMENTKNOWLEDGELABOR

Digitization&RoboticAutomation|Analytics|Mobility|SocialMedia|CognitiveComputing

III.ABURNINGPLATFORMFORCHANGE

GlobalizationofLabor|High-growthEmergingMarkets|

DisruptiveBusinessModels|Consumerization

AS-A-SERVICEECONOMY

Agility|CollaborationOne-to-Many|OutcomeFocus

Plug-and-PlayServices

Proprietary│Page18©2016HfSResearchLtd.ExcerptforAccenture

FixedAssetsLeveragedAssets

2DesignThinking

3BrokersofCapability

1WriteOffLegacy

4CollaborativeEngagement

7HolisticSecurity

5IntelligentAutomation

6Accessible&Actionable

Data

8Plug-and-PlayDigitalServices

SOLUTIONIdeals

LEGACYECONOMY

AS-A-SERVICEECONOMYCHANGEMGMT

Ideals

§ MovingintotheAs-a-ServiceEconomymeanschangingthenatureandfocusofengagementamongenterprisebuyers,serviceproviders,andadvisors

§ “As-a-Service”unleashespeopletalenttodrivenewvaluethroughsmartercombinationsoftalentandtechnologyfocusedonbusinessresultsbeyondcostreduction

Journey to the As-a-Service Economy

Proprietary│Page19©2016HfSResearchLtd.ExcerptforAccenture

Mortgage is at the Start of the Journey, Adopting the Ideals of the As-a-Service Economy

IDEAL AS-A-SERVICEIDEALDEFINITION

NONEXISTENT

INITIAL EXPANSIVE EXTENSIVE ALLPERVASIVE

WriteOffLegacyUsingplatformbasedsolutions,DevOps,andAPIecosystemsformoreagile,lessexceptionorientedsystemsandprocesses 2016

DesignThinkingUnderstandingthebusinesscontexttoreimagineprocessesalignedwithmeetingclientneeds 2016

Brokers ofCapability

Orientinggovernance tosourceexpertisefromallavailablesources,bothinternallyandexternally,toaddresscapabilitygaps 2016

CollaborativeEngagement

Ensuring relationshipsarecontractedtodrivesustainedexpertiseanddefinedoutcomes 2016

IntelligentAutomation

Using ofautomationandcognitivecomputingtoblendanalytics,talent,andtechnology 2016

Accessible&ActionableData

Applyinganalyticsmodels,techniquesandinsightsfrombigdata,real-time 2016

HolisticSecurityProactivelymanagingdigitaldataacrossservicechainofpeople,systems&processes 2016

Plug andPlayDigitalBusinessServices

Plugginginto“readytogo”business-outcomefocused, people/process/technologysolutionswithsecuritymeasures 2016

Proprietary│Page20©2016HfSResearchLtd.ExcerptforAccenture

How As-a-Service Is Taking Shape in Mortgage: Writing Off Legacy

Legacytechnologyinvestments thatlimitagilityandcreate exceptionsaddressedby

addinginternalandexternalFTEs

Usingplatform-basedsolutions,DevOps,andAPIecosystemsformoreagile,less-exception-orientedsystems

§ Writing off legacy for mortgage clients is not about technology replacements alone, although that landscape isdiverse and changing. Many lenders are at the point of sunsetting legacy systems including AS/400 to opt formore agile systems. This is coupled with a number of home grown applications and standard platforms such asBlack Knight that lenders have to maintain and upgrade, all towards adapting to the changing businessenvironment. It is in this “contextualizing” where service providers are starting to help mortgage clients writeoff legacy—by bringing an understanding of the industry’s challenges and opportunities that lie at theintersection of business and technology. We are starting to see examples of lenders that are partnering withservice providers on both process transformation and new technology adoption programs, where a fewproviders have developed capabilities to address risk mitigation during change, whether that is a legacy systemsunset and migration to a new loan origination system, regulatory change, employee retraining or creating thespace for experimenting with new technology solutions in a collaborative manner.

Examples:§ Cognizant has a multidisciplinary practice called Cognizant Digital Works which is charged with helping clients

manage ongoing innovations to become digital businesses. Digital labs has developed an e-mortgage solutionthat streamlines the loan application process for borrowers by making them available on a mobile app.

§ TCS helped a leading bank from Canada that wanted to improve its pull through rates, auto decision rates andturnaround time. TCS achieved this by defining the future state model for the client, operationalizing theprocess modification and implementation in the LoS, and the criteria for routing deals to credit support andimplementation. In addition to these goals, the initiative also improved end client experience, and enhancedthe credit knowledge within the origination phase.

Proprietary│Page21©2016HfSResearchLtd.ExcerptforAccenture

How As-a-Service Is Taking Shape in Mortgage: Design Thinking

Resolvingproblemsbylookingfirstattheprocessasthesourceofthesolution

Understandingthebusinesscontexttoreimagineprocessesalignedwithmeetingclientneeds

§ HfS believes that Design Thinking, when applied effectively, provides a continuous method to discover, define,rethink and address business problems. It offers service providers and buyers a new way to engage as partnersto define and achieve common goals and outcomes, tapping into the resources of both parties and beyond.With mortgage, we see only a couple of service providers making progress with this approach in order toredefine their relationships with banking and mortgage clients and the work and value they deliver. On theflipside, the majority of mortgage clients in our research were yet to fully understand the potential of usingdesign thinking with their service provider, making this a nascent concept for this market as of today. We expectthe service providers leading the charge on design thinking in mortgage to help more clients in this industrywrite off legacy in the next few years.

Examples:§ Sutherland has the most impactful example of using design thinking to redesign mortgage operations. Its

“mortgage process of the future” was developed after using design thinking for a client’s origination process.Sutherland found 90% inefficiencies across 600 origination components, in areas such as borrower interactions,document capturing, and handoffs between different parties. By redesigning processes around the borrower,the service provider reduced redundancies to the point of guaranteeing a 22 day cycle time for 90% of loans,including the sales process, fulfilment and other components. It is now exploring similar implementations withother mortgage clients.

Proprietary│Page22©2016HfSResearchLtd.ExcerptforAccenture

How As-a-Service Is Taking Shape in Mortgage: Brokers of Capability

Focusinggovernanceandoperationsstaffonmanagingtotheletterofthecontractandthedecimalpointsofservicelevels

Orientinggovernancetosourceexpertisefromallavailablesources,bothinternallyandexternally,toaddresscapabilitygaps

§ Being a broker of capability is about articulating a business problem or opportunity, the desired outcomes, andthen coordinating and facilitating across internal and external entities to reach those results. This is an evolvingrole with a handful of mortgage clients HfS spoke to during this research, where they are focusing on and takingaccountability to close capability gaps with the help of internal groups and service providers. In one case, aLending Operations Director described how closely integrated he wanted his operational environment to be,and as a result he works directly with his service provider’s offshore team instead of account managers,involving the team in management meetings, setting strategic and operational priorities across the enterprise.Service providers as well are expanding their range of partnerships, especially with technology vendors, to beable to bring true process transformation.

Examples:§ An Accenture’s client described how Accenture is working with them to solve a business challenge, which is the

high cost for data extraction and indexing because of a technology vendor that the client works with. Accenturebrought resources onsite from across its global locations to help the client evaluate different ways to embedautomation and drive down cost in the loan lifecycle. The client mentioned that Accenture is helping them lookat alternate technology vendors and the internal/external teams are “learning together.”

§ Sutherland has helped steer one of its largest mortgage clients in fulfilment away from a task-orientedgovernance model. The service provider had 25 SLAs that micromanaged borrower contacting. The two partiesrestructured business contracts that are now based on metrics such as—revenues, number of loans closed, pullthrough rates, cost, engagement experience as measured by NPS, etc. and the quality of the files from abusiness regulatory perspective.

Proprietary│Page23©2016HfSResearchLtd.ExcerptforAccenture

How As-a-Service Is Taking Shape in Mortgage: Collaborative Engagement

§ At the core of the As-a-Service Economy—linking the solution ideals to the change management ideals thatmake a solution effective over the long term—is collaborative engagement. Service providers and buyers thatare able to foster a “partnership” culture over time have the best chances to drive sustained value bycontracting for outcomes. Instead of a rigid and directive, arms-length, SLA-focused environment, both partiesare viewed as equals, with two way feedback, collaboration and accountability for success and innovation in theengagement. We see a few examples of this type of progressive sourcing in the mortgage space.

Examples:§ “Do we have a collaborative engagement? Absolutely!” remarked one of Wipro’s mortgage clients. He described

that even though the engagement with Wipro is new, they have developed a strong collaborative environment,with learning opportunities on both sides. As the client got up to speed, they appreciated Wipro’s accountmanager and the team’s way of engaging and collaborating openly—identifying areas for training or calibration,running analytics and reporting for more clarity, and pushing back on new ideas based on industry experience.

§ Genpact has been proactively suggesting a shift to outcome driven contracts and is starting to see some successwith this around full loan to closing transactions. As a result, the service provider has one of the highestgainsharing revenues for this industry vertical. One of its clients, a mortgage registry utility, commends Genpactfor its trusted relationship, where it provides valuable feedback to make process improvements up the chain.

Evaluatingrelationshipsonbaselinesofcost,effort,andlabor

Ensuringrelationshipsarecontractedtodrivesustainedexpertiseandoutcomes

Proprietary│Page24©2016HfSResearchLtd.ExcerptforAccenture

How As-a-Service Is Taking Shape in Mortgage: Intelligent Automation

Operatingfragmentedprocessesacrossmultipletechnologieswithsignificant

manualinterventions

Usingautomationandcognitivecomputingtoblendanalytics,talent,andtechnology

§ Most mortgage clients in our research are at the start of their journey on what we call Intelligent Automation—using software and technology to do routine tasks, and enhancing it through machine learning and naturallanguage processing, and moving up the curve with artificial intelligence. Service providers on their part havebeen very active—with a few more proactive than others—to recommend the piloting and deployment of thirdparty and proprietary automation technologies. A client described one provider as being “very persistent intheir recommendations on automation”.

§ This gives us the sense that automation, with robotic process automation (RPA) at the outset, is seeing a slowertake-up in mortgage than other areas of the services industry. Several clients described their LOS and servicingplatforms and internal infrastructure as being difficult to envision automation use cases, with concerns aboutregulatory oversight and due diligence.

§ However, these legacy environments with clunky data exchanges and workarounds are prime candidates forRPA technology, which suggests the need for service providers to better describe and contextualize theircapabilities in this space along the lines of regulatory concerns.

§ Where providers don’t own the LOS’ and are remotely logging in, Intelligent Automation is the next bastion ofeffective operations. This explains the initial success that some providers have had with RPA – we expectgreater adoption as more industry examples develop.

Proprietary│Page25©2016HfSResearchLtd.ExcerptforAccenture

How As-a-Service Is Taking Shape in Mortgage: Intelligent Automation (continued)

Operatingfragmentedprocessesacrossmultipletechnologieswithsignificant

manualinterventions

Usingautomationandcognitivecomputingtoblendanalytics,talent,andtechnology

Examples:§ Cognizanthasanorganization-wideinitiativetobuildcross-businessunitautomationframeworksandmaturity

modelstospeedupinstitutionalizationandadoption,whichmortgageclientsarestartingtovalueastheyformtheirownautomationcommittees.CognizanthasusedRPA,OCRandotherautomationtechnologiesintheareasofclaims,documentindexing,QAforvoice,email,chatcorrespondence,documentrequests,payoffquotesgeneration,escrow/taxanalysis,check/wiresentries,extractionofdatafromdocumentsforQAandloansetup.

§ Accentureisveryactiveinautomation,andseveralclientsrateditasthefrontrunnerinbringingthemopportunitiestoembedautomationformoreintelligentmortgageoperations.Foramajorbank,Accentureisworkingthroughalistof25automationopportunities,andtheclientdescribedtheserviceproviderashelpingthemwriteoff/workaroundlegacy.Forthem,Accenturehasdeployedautomationinthecreditspace,automatedmanualreportingtasks,paymentapplicationsandisnowevaluatingthecreationofintuitive,user-friendlyservicingdashboardsontopoflegacyapplicationswithautomateddataextraction.

§ Infosyshasalreadydeployedautomationtoolswith3ofits7clients,withanintenttocreateacommoditizedRPAofferingwithintheyearforeachoftheotherclientstodeliversimilarresultsinareaslikeauto-decisioning,underwritingassistance,audits,andloanboarding.

§ Wipro’sHOLMES,acognitivecomputingbasedsolution,isbeingdeployedforvariousscenarioslikeKYCandhelpdeskautomationandtheserviceprovideriscurrentlybuildingusecasesformortgageloanorigination.

Proprietary│Page26©2016HfSResearchLtd.ExcerptforAccenture

How As-a-Service Is Taking Shape in Mortgage: Accessible and Actionable Data

Performingad-hocanalysisofunstructureddatawithlittleintegrationor

businesscontext

Applyinganalyticsmodels,techniques,andinsightsfrombigdata in real-time

§ The most effective analytics—analysis of data for insight that leads then to plan and action—starts withaggregated, cleansed, and standardized processes and data. We see great examples of service providercapability in creating and embedding analytical insights and data into different parts of the mortgage valuechain, understanding the key triggers/outcomes in the process. The key areas we see progress in mortgageanalytics are in predictive modeling for loan origination to help prioritize underwriter time and understandlikelihood to close, predictive loan default and delinquency modeling to determine propensity to default, andloan fraud detection to help the appraisal process. Other examples relate to call center efficiencies, portfolio,risk and regulatory compliance reporting and analytics, and managing and improving the data coming fromprocesses. Collecting and maintaining good quality data in the loan lifecycle is still a challenge for a lot oflenders, and is an area where service providers are stepping up with solutions in the areas such as Know YourCustomer (KYC).

Examples:§ WNS has extensive experience in advanced mortgage analytics, offered as a standalone service to clients. It is

now actively extending this team to its larger mortgage BPO engagements for data scrubbing, reporting andpredictive modeling to provide customer and business insights across the mortgage value chain. For example, itbuilds retention models to prevent borrower attrition where it manages this process for a mortgage client.

§ Genpact has analytics bundling in two major areas in mortgage BPO—underwriting and customer prescreeningand targeting. It also has a utility for KYC to help banking clients with due diligence and onboarding.

Proprietary│Page27©2016HfSResearchLtd.ExcerptforAccenture

How As-a-Service Is Taking Shape in Mortgage: Holistic Security

Respondingreactivelywithpost-eventfixes; little focusonend-to-endprocess

valuechains

Proactivelymanagingdigitaldataacrossaservicechainofpeople,systems, andprocesses

§ Holistic Security is the proactive management across internal and external people, process, and technology.Often the focus is on the systems, but in business process services and in sourcing engagements, people andprocess become a significant factor in managing and securing data. Banking and mortgage clients havetraditionally had very stringent data protection laws, but today with more regulatory and compliance audits ondata security, we see more activity in this area in the form of control reviews and frequent site audits. Whilemost service providers have their own standards and guidelines for data storage/archival/destruction/encryption, we believe the lack of a shared culture for holistic security by both buyers and service providers is amajor inhibitor for mortgage As-a-Service. Risk and compliance management continues to mature. However toderive the most powerful benefits of As-a-Service, including analytics, advanced RPA, cloud delivery, andcollaboration around data, buyers have to balance control measures within all parts of the loan lifecycle andinstead work with their service provider to find a model to continuously mitigate both data breach andrepertory risks in mortgage.

Examples:§ Genpacthasastructuredcontrollershipframework,multi-levelauditstructureandexperienceofundergoing

auditswithglobalregulatorybodies

§ Sutherland Global Services has experience as a registered mortgage bank, which gives its clients confidence forreporting & regulatory know-how, and execution in the origination process in particular.

Proprietary│Page28©2016HfSResearchLtd.ExcerptforAccenture

How As-a-Service Is Taking Shape in Mortgage: Plug-and-Play Business Services

Undertakingcomplexandoftenpainfultechnologytransitionstoreachasteady

state

Plugginginto“readytogo”businessoutcome-focused,people,process, andtechnologywithsecuritymeasures

§ The concept of delivering mortgage As-a-Service, using plug and play business services is still in its infancy. AnAs-a-Service solution that includes a single contract for people, process and technology for an end-to-endprocess, contracted to deliver outcomes, is well positioned for the majority of loans that lenders originate todayin residential mortgage. By defining and complying with a prescribed process, lenders would be able to reducetheir cost to originate, have more compliant loans, improved experience for borrowers and reduced buy-backrisk. Of utmost importance to IT, this would reduce the complexity of the client’s technology landscape,however it must be balanced with selecting a partner whose product vision aligns with the lender. The buildingblocks for such a proposition already exist with a few service providers, albeit with limited execution as oftoday. From our research, we are starting to see readiness from smaller banks to undertake POCs in this newmodel, which will take a few years to gain momentum on the back of these collective industry experiences.

Examples:§ AccentureCreditServices(ACS)isundertakingresearchtounderstandthecurrentstateofmortgage

operations,andclients’perceptionsofandoutlookonMortgageAs-a-Service,withaparticularfocusonhowitspointsolutions(outsourcing,LOSplatform,analytics)couldbeleveragedinanAs-a-Servicedeliverymodel.

§ WithitsCreditEdge platform,InfosyshascreatedanAs-a-Serviceoffering,deliveredinthecloudonamanagedserviceandoutcome-basedpricingmodel(perloan).ThisislivewithaleadingU.S.basedcommercialrealestateservicer,whereInfosysmanagesacommercialrealestateportfolio,deliveringafasterturnaroundtimeonloanboardingandimprovingoperationalefficiency.

§ Wipro,Genpact,XeroxandCognizanthavemadeinvestmentstobolstertheirAs-a-Serviceportfoliosonthebackofproprietarymortgageplatforms.

Research Methodology

Proprietary│Page30©2016HfSResearchLtd.ExcerptforAccenture

Research MethodologyDataSummaryn DatawascollectedinQ22016,coveringbuyers,

serviceproviders,andadvisors/influencersofmortgageoperations.

ParticipatingServiceProviders

This Report Is Based On:

n Tales from the Trenches: Interviews withbuyers who have evaluated serviceproviders and experienced their services.Some contacts were provided by serviceproviders, and others were interviewsconducted with HfS Executive Councilmembers and participants in ourextensive market research.

n Sell-Side Executive Briefings: Structureddiscussions with service providersregarding their vision, strategy, capability,and examples of innovation andexecution.

n Publicly Available Information: Thoughtleadership, investor analyst materials,website information, presentations givenby senior executives, industry events, etc.

Proprietary│Page31©2016HfSResearchLtd.ExcerptforAccenture

Sales&Marketing

• ProductDevelopment

• ProspectandLeadGeneration

• DirectSales

Pre-Underwriting

• LOSDataEntry

• LOSDataValidation

• DataLockinLOS

Processing

• DocumentChecks

• OrderingExternalData

• VOE/VOM/VOR

• InitialDisclosureandTruthInLendingPreparation

Underwriting

• AutomatedUnderwriting

• ManualUnderwriting

Closing

• DocumentPrep

• SchedulingClosing

• Funding

• TrailingDocumentation

• AppraisalandotherRiskReviews

Servicing

• PaymentProcessing

• TaxesandEscrowManagement

• CustomerCare

• InvestorReportingManagement

Defaults

• Collections• DefaultandPropertyIdentification

• Foreclosure• LoanModifications

• Dispositions• SecuritizationReviews

Analytics

LoanOriginationSystem(LOS)LicensingandMaintenance

DocumentManagement

Mortgage As-a-Service Value Chain – Core Processes

HfSValueChainDefinition:Valuechainreferstotheseriesofdepartmentsthatcarryoutvalue-creatingactivitiestodesign,produce,market,deliver,andsupportacompany’sproductorservice.Inthisusage,werefertotherangeofprimaryprocessesandsupportservicesthatprovidersoffertotheirclients.

Proprietary│Page32©2016HfSResearchLtd.ExcerptforAccenture

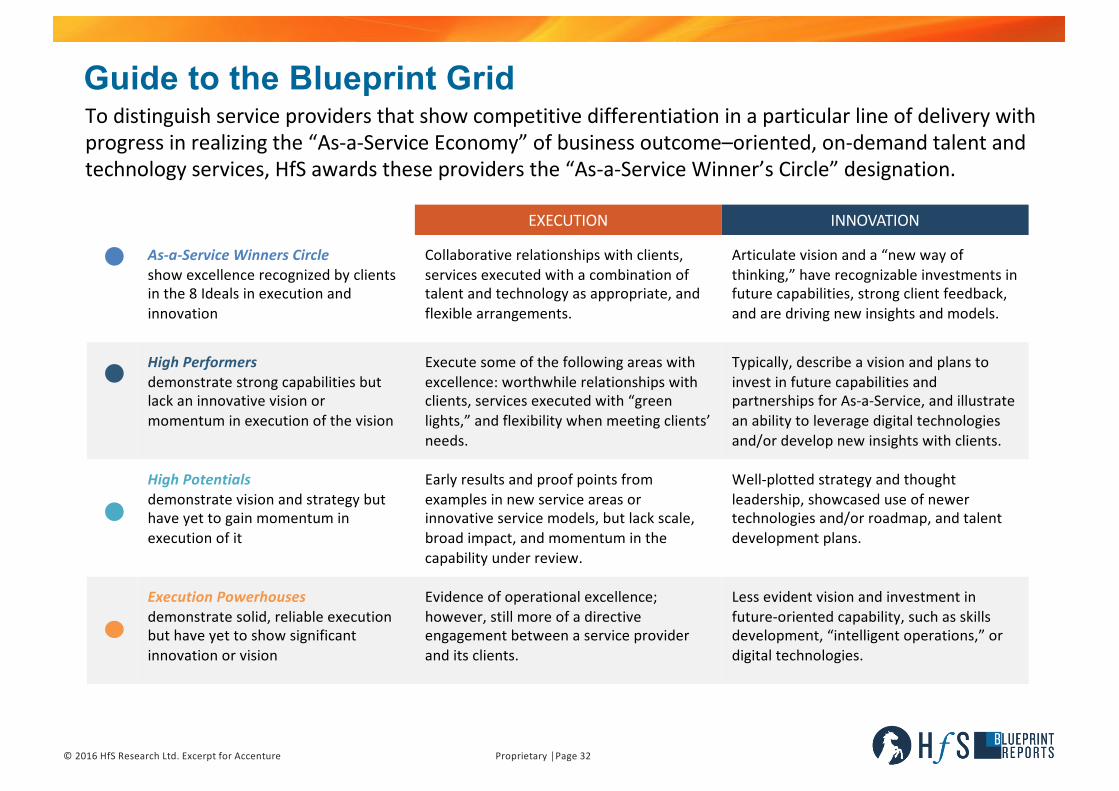

Todistinguishserviceprovidersthatshowcompetitivedifferentiationinaparticularlineofdeliverywithprogressinrealizingthe“As-a-ServiceEconomy”ofbusinessoutcome–oriented,on-demandtalentandtechnologyservices,HfSawardstheseprovidersthe“As-a-ServiceWinner’sCircle”designation.

Guide to the Blueprint Grid

EXECUTION INNOVATION

As-a-ServiceWinners Circleshowexcellencerecognizedbyclientsinthe8Idealsin executionandinnovation

Collaborativerelationshipswithclients,servicesexecutedwithacombinationoftalentandtechnology asappropriate,andflexiblearrangements.

Articulatevisionanda“newwayofthinking,”haverecognizableinvestmentsinfuturecapabilities,strongclientfeedback,and aredrivingnewinsights andmodels.

HighPerformersdemonstratestrongcapabilitiesbutlackaninnovativevisionormomentuminexecutionofthevision

Executesomeofthefollowingareaswithexcellence:worthwhilerelationshipswithclients,servicesexecutedwith“greenlights,”andflexibilitywhenmeetingclients’needs.

Typically, describeavisionandplanstoinvestinfuturecapabilitiesandpartnershipsforAs-a-Service,andillustratean abilitytoleveragedigitaltechnologiesand/ordevelop newinsightswithclients.

High Potentialsdemonstratevisionandstrategybuthaveyettogainmomentuminexecutionofit

Earlyresultsandproof pointsfromexamplesinnewserviceareasorinnovativeservicemodels,butlackscale,broadimpact,andmomentuminthecapabilityunderreview.

Well-plotted strategyandthoughtleadership,showcaseduseofnewertechnologiesand/orroadmap,andtalentdevelopmentplans.

ExecutionPowerhousesdemonstratesolid,reliableexecutionbuthaveyettoshowsignificantinnovationorvision

Evidence ofoperationalexcellence;however,stillmoreofadirectiveengagementbetweenaserviceprovideranditsclients.

Lessevidentvisionandinvestmentinfuture-orientedcapability,suchasskillsdevelopment,“intelligentoperations,”ordigitaltechnologies.

Proprietary│Page33©2016HfSResearchLtd.ExcerptforAccenture

HfS Blueprint Scoring Percentage Breakdown

ExecutionCriteria=100%

InnovationCriteria=100%

1. QualityofAccountManagementTeam 15%2.IntegrationofCustomerFeedbackandCollaborative ModelsofEngagement 10%3. FlexibilitytoDeliverPointandEndtoEndSolutions 10%4.ActualDeliveryofSolutions (Origination,Servicing,Foreclosure) 25%5.Experience DeliveringToTop50Lenders 10%6.Configurability ofSolutionsToMultipleGeographicLocations 5%7.AbilitytoAttract andRetainKeySkills 10%8. ModelForContinuousImprovement 5%9.EffectivenessofAnalyticsTeams onClientPerformance 5%10.Financial ReturnsforKeyClients 5%

1.VisionforMortgageAs-s-ServiceMarketEvolution 15%2.ApproachToHelpingClientsWriteOffLegacy 10%3.VisionForTheDeployment ofIntelligentAutomation 15%4.RoadmapforMOS(Internaland3rd Party)Usage 15%5.ConceptsforNewCommercialModelsforMortgageOperations 10%6.DeliveryofAccessibleandActionable DataAnalytics 20%7.SolutionsforHolisticSecurity inMortgageOperations 5%8.Response toRegulatoryRequirements 10%

Service Provider Analysis

Proprietary│Page35©2016HfSResearchLtd.ExcerptforAccenture

HfS Blueprint: Mortgage As-a-Service 2016INNOVA

TION

EXECUTION

ExcellentatInnovationandExecutionInvestinginInnovationtoChange

BuildingAllCapabilities ExecutionIsAheadofInnovation

AS-A-SERVICEWINNER’SCIRCLE

EXECUTIONPOWERHOUSES

HIGHPOTENTIALS

HIGHPERFORMERS

Accenture

Unisys

Cognizant

Genpact

ISGN/Firstsource

Infosys

WNS

TCSWipro

Xerox

Sutherland

Proprietary│Page36©2016HfSResearchLtd.ExcerptforAccenture

Major Service Provider Dynamics: HighlightsEXECUTION

• Quality of Account Management: Clients value serviceproviders that can foster good account managers – that arewilling to listen and understand unique client challenges, act astrue partners to the business and broker capabilities acrossinternal and external lines to deliver a solution. Accenture,Cognizant and TCS win in this regard, with their customer-centric account management practices.

• Ability to Attract and Retain Key Skills: Accenture, Genpact,WNS and Wipro received consistently positive feedback ontheir ability to attract and retain a broad range of mortgagetechnology, analytical and process professionals. In particular,their mortgage industry training and certifications programs inplace is industry leading.

• Flexibility In Catering to Different Client Needs: While a lot ofthe service providers focus on the top 50 lenders, regionalbanks, credit unions and mid-size or smaller lenders and sub-servicers present a different opportunity for those that canscale according to the needs of different clients. Infosys, WNS,Sutherland, Unisys, and ISGN/Firstsource scored particularlyhigh for their flexibility.

• Actual Delivery of Services: Service providers have experiencein servicing different parts of the loan lifecycle over the years.For example, Sutherland and ISGN/Firstsource’s originationcapabilities are comparatively strong versus their competitors.Meanwhile, TCS’ default management is industry leading, andAccenture and Cognizant have developed a more end-to-enddelivery capability.

INNOVATION

• Vision for Mortgage As-a-Service: Accenture, Cognizant,Genpact, ISGN/Firstsource and Infosys have developed a visionfor Mortgage As-a-Service and are at the forefront of exploringthis delivery model in the next few years, bringing togetherprocess and analytical talent and technology-based solutions.

• Introducing Intelligent Automation into Mortgage: Clients arecarefully evaluating their options with automation, and areincreasingly leaning on their trusted service providers to lead withexamples from other industries in how to go beyond macros andworkflow and into RPA and cognitive automation. Accenture,Infosys, and TCS have made the most progress inimplementations as of today.

• Delivery of Accessible and Actionable Data Analytics: Ourresearch highlighted client readiness for and expectations aroundproviding better analytics and reporting in mortgage operations,along with the fundamental need to collect and maintain goodquality data in the entire loan lifecycle.Wipro, Genpact,WNS andCognizant had the most compelling examples of embedded andAs-a-Service analytics services.

• Approach To Helping Clients Write Off Legacy: Service providersare approaching organizational change in different ways formortgage clients, resulting in a number of examples where we arestarting to see examples of lenders partnering with serviceproviders on process transformation as well as new technologyadoption programs. Accenture, Sutherland, Cognizant, TCS andWipro are making progress on helping their mortgage clientswrite off legacy toward delivering more intelligent operations.

Proprietary│Page37©2016HfSResearchLtd.ExcerptforAccenture

Accenture MortgageAs-a-Servicevisionarydrivingoperationallyexcellentengagementsbyleveragingleadingindustryassets

Winner’s Circle

RelevantAcquisitions/Partnerships KeyClients GlobalOperations ProprietaryTechnologies/Platforms

Acquisitions:• 2013,MortgageCadencewhich

bolsteredLOScapabilities• 2013, Vivere Brasil,amajoritystake

acquisitionwhichbringsAccentureCreditServicesintoBrazil.

• 2011,Zenta whichbroughtAccentureintotheMortgageServicesmarket

90majorMortgageOperationsclients,including:

• TopfiveU.S.financialinstitution• Top10U.S.mortgagebanker• Topfivemortgageservicer• Top30U.S.financialinstitution• Topfivecommercialbank

Headcount/Locations: Morethan375,000employeesworldwidewith3,500focusedonMortgageacross10locations:

• NorthAmerica:Charlotte,Dallas,NewYork,SanAntonio,Sacramento

• LatinAmerica: SaoPaulo• India: Bangalore,Chennai,Mumbai• ThePhilippines: Manila

• AccentureCreditServicesProprietaryTechnologyPlatform:LeveragingMortgageCadenceasaproprietaryLOSsystemforpipelinemanagementinloanlifecycle,includingstraight-throughprocessingandqualitycheckpoints

• PAR(Prioritization,Allocation,Routing):Analgorithmthatsystematicallyroutesandreassignsloansbasedonloancriteria,turn-timerequirementsandlicensing

• BPONavigatorforanalyticsandperformancemanagement• FirstPassYieldSystem(FPY) forcontinuousimprovements• PipelineAllocationManagement(PAM)foroptimizing

workloadallocation• Vivere (Brazil):Aconsumermortgageandconstruction-lending

contractprocessingplatform(originationandadministration)

Strengths Challenges

• Creating Industry Dialogue And Vision For Mortgage As-a-Service: AccentureOperations is exploring ways to move offerings towards As-a-Service. Accenture CreditServices (ACS) is undertaking research to understand the current state of mortgageoperations, and clients’ perceptions of and outlook on Mortgage As-a-Service, with aparticular focus on how its point solutions could be leveraged in an As-a-Servicedelivery model. HfS sees this as a strong indicator of Accenture progressing since thelast Blueprint on their vision – it is taking the lead to help clients write off legacytechnology and processes by first defining and articulating a vision for the marketspecifically, and understand its readiness and barriers to As-a-Service.

• Offering Diversity And Operational Excellence In Mortgage Operations: AccentureCredit Services is maintaining its best-in-class reputation among mortgage clients,particularly in origination and servicing processes. Its sizeable business in commercialmortgage is still unique with few competitors able to touch the complex nature ofwork involved. Clients give examples of how Accenture has been instrumental inredesigning their credit and operational processes, using automation as a key lever.

• Relationship Building To Deliver Value Beyond Cost: Following from the 2014Blueprint, Accenture is continuing its focus on creating strong account relationshipseven before the lenders become clients. Multiple clients commended the serviceprovider’s ability to customize deliverables and articulate clear governance structureswith considerable leadership involvement and engagement, stating that it is “an easycompany to do business with.”

• Shaping Market Dialogue On Software Vs. Platform BasedServices: As a market leader, Accenture will need to focus oncommunicating to the market how it intends to balancehaving a technology agnostic approach at ACS, and acquiringcompanies with platforms. Clients HfS spoke to had someexpectations around greater integration of its platform andservices, towards driving results. Accenture, like other serviceproviders in this industry, will need to balance these clientexpectations for platform based services, creating moretransparency around the ways in which business outcomesare delivered through different operating models.

• Expanding From Point Solutions To Get To As-a-Service:Accenture has what appears to be the best of a variety ofpoint solutions. A lot of its scale comes from large clients thathave engaged with the service provider on these pointsolutions, making it a challenge and an opportunity for it toturn them into As-a-Service clients in the future, leveragingits technology platform and operations support to deliveroutcomes. While this is an industry challenge in general, HfSexpects Accenture as a market leader to lead the change.

BlueprintLeadingHighlights

• ActualDeliveryOfServices• ExperienceDeliveringToTop50

Lenders• QualityofAccountManagement

Team• VisionforMortgageAs-s-Service

MarketEvolution• RoadmapforMOS(Internaland

3rd Party)Usage• IntegrationofCustomerFeedback

andCollaborative ModelsofEngagement

OfferingMaturity

Origination:75%

Servicing:~20%

Default:5%

ConfidentialandProprietary│Page38

Market Direction and Recommendations

Proprietary│Page39©2016HfSResearchLtd.ExcerptforAccenture

Where to Next for Mortgage As-a-Servicen Greater Alignment of Services Around MOS Platforms: Service providers like Wipro, Accenture and

Genpact that have made investments in acquiring MOS technology vendors have goals of providing abroader, end-to-end portfolio in mortgage, including people, process and technology. This is anindicator of a vision for providing Mortgage As-a-Service. However, most of the acquisitions madewere of independently branded software solutions, accompanied by their own branding legacies.Infosys took a different approach with its startup acquisition to create CreditEdge. In the next twoyears, we expect these service providers to further integrate these technology buys into theirportfolios and shape the thinking around Mortgage As-a-Service with more client implementations.

n Traction on Process Automation: It has taken a while for process automation to cautiously make itsway to the forefront of conversations in mortgage operations, due to its troubled “robosigning” past.We are now seeing greater understanding by both service providers and buyers to start thinkingpractically and implementing different kinds of automation technologies (RPA, intelligent OCR, etc.)across various parts of the mortgage services value chain. Today thus represents the early vanguardand the arrival of RPA in mortgage, leading us to believe that adoption will be fairly rapid over thenext 12-18 months.

n Digital Will Drive Disruption at the Top: Several of the big lenders that HfS interviewed are stillplaying the “wait and watch” game on digital disruption, in particular the strides made by fintechstartups and non-traditional banks in the mortgage industry. While “push button, get mortgage”might not be the path for all the Top 50 to go down, lenders are initiating more conversation andstrategy around how digital components can help them look at traditional operations differently. Thegoal for many will be to make borrower experiences more transparent, enabling more self-serviceand removing duplication in efforts and documentation. Service providers will have a big role to playin this, from a process reimagining perspective, as well as ultimately configuring the digitalcomponents that link these activities back to onboarding and origination platforms.

Proprietary│Page40©2016HfSResearchLtd.ExcerptforAccenture

Financial Institutions Have Ambitious 3 Yr Goals For Operational Maturity – With A Customer First StrategyWhichofyourbusinessfunctionsarethemostmatureintermsofintelligentoperationsnow?Wherewouldyoulikethemtobein3years?(Scale1-5,just4&5)

Source: “Intelligent Operations" Study, HfS Research 2016Sample: BFS Buyers = 67

18%

16%

11%

23%

46%

55%

61%

61%

NewProduct/ServiceDevelopment

Post-tradeProcessing/Back-office

Front-office

WealthManagement

Targetfor3years MaturityNow

Proprietary│Page41©2016HfSResearchLtd.ExcerptforAccenture

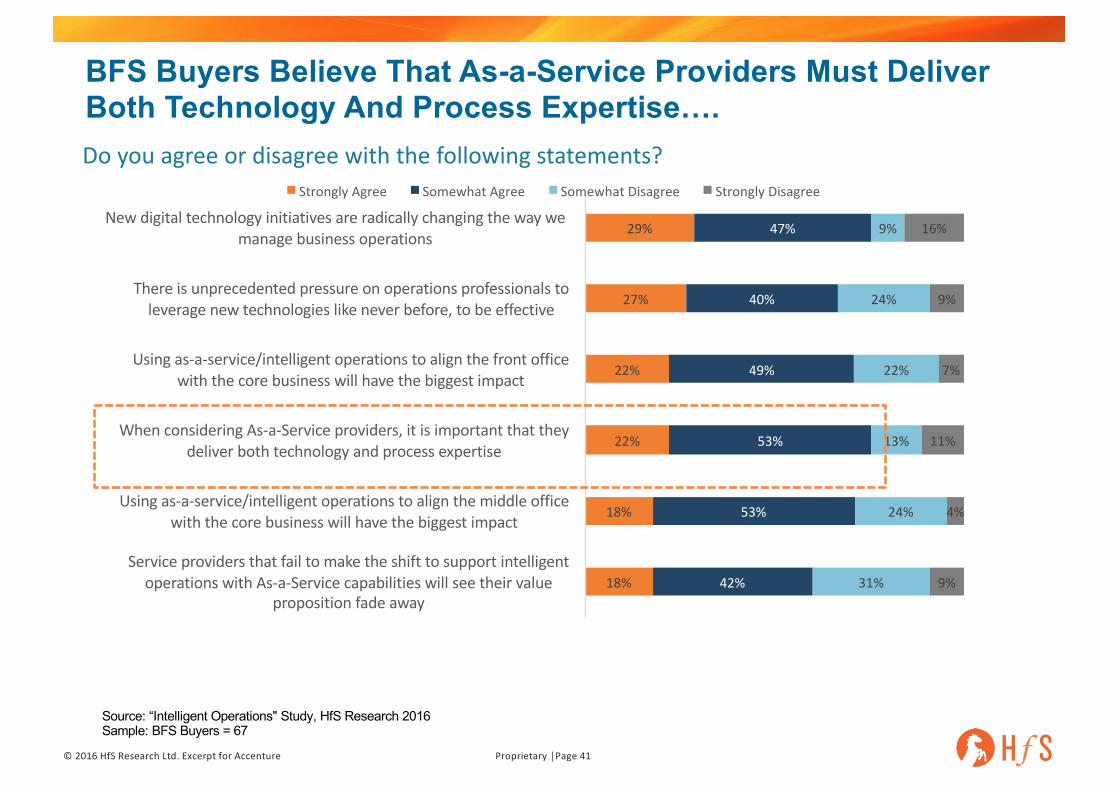

BFS Buyers Believe That As-a-Service Providers Must Deliver Both Technology And Process Expertise….Doyouagreeordisagreewiththefollowingstatements?

18%

18%

22%

22%

27%

29%

42%

53%

53%

49%

40%

47%

31%

24%

13%

22%

24%

9%

9%

4%

11%

7%

9%

16%

ServiceprovidersthatfailtomaketheshifttosupportintelligentoperationswithAs-a-Servicecapabilitieswillseetheirvalue

propositionfadeaway

Usingas-a-service/intelligentoperationstoalignthemiddleofficewiththecorebusinesswillhavethebiggestimpact

WhenconsideringAs-a-Serviceproviders,itisimportantthattheydeliverbothtechnologyandprocessexpertise

Usingas-a-service/intelligentoperationstoalignthefrontofficewiththecorebusinesswillhavethebiggestimpact

Thereisunprecedentedpressureonoperationsprofessionalstoleveragenewtechnologieslikeneverbefore,tobeeffective

Newdigitaltechnologyinitiativesareradicallychangingthewaywemanagebusinessoperations

StronglyAgree SomewhatAgree SomewhatDisagree StronglyDisagree

Source: “Intelligent Operations" Study, HfS Research 2016Sample: BFS Buyers = 67

Proprietary│Page42©2016HfSResearchLtd.ExcerptforAccenture

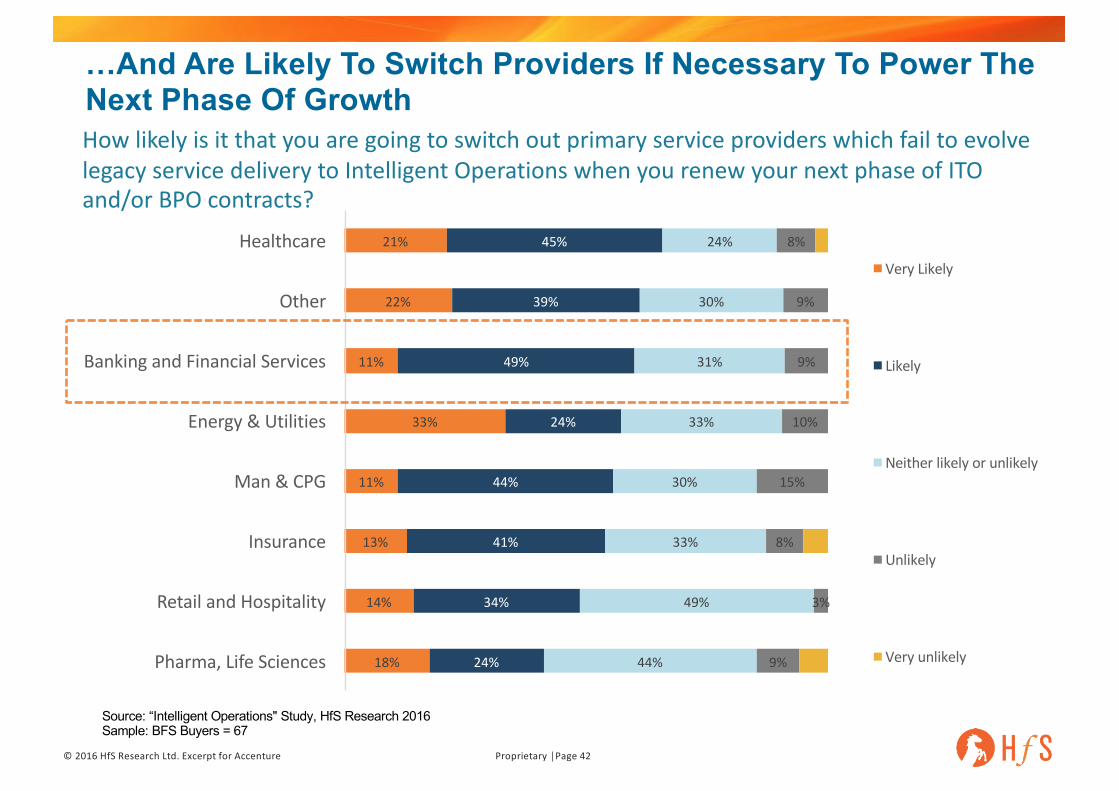

…And Are Likely To Switch Providers If Necessary To Power The Next Phase Of GrowthHowlikelyisitthatyouaregoingtoswitchoutprimaryserviceproviderswhichfailtoevolvelegacyservicedeliverytoIntelligentOperationswhenyourenewyournextphaseofITOand/orBPOcontracts?

18%

14%

13%

11%

33%

11%

22%

21%

24%

34%

41%

44%

24%

49%

39%

45%

44%

49%

33%

30%

33%

31%

30%

24%

9%

3%

8%

15%

10%

9%

9%

8%

Pharma,LifeSciences

RetailandHospitality

Insurance

Man&CPG

Energy&Utilities

BankingandFinancialServices

Other

HealthcareVeryLikely

Likely

Neitherlikelyorunlikely

Unlikely

Veryunlikely

Source: “Intelligent Operations" Study, HfS Research 2016Sample: BFS Buyers = 67

Proprietary│Page43©2016HfSResearchLtd.ExcerptforAccenture

Mortgage As-a-Service Will Start To Gain Traction In The Next Three Years, Through Collaborative Engagements

IDEAL AS-A-SERVICEIDEALDEFINITION

NONEXISTENT

INITIAL EXPANSIVE EXTENSIVE ALLPERVASIVE

WriteOffLegacyUsingplatformbasedsolutions,DevOps,andAPIecosystemsformoreagile,lessexceptionorientedsystemsandprocesses 2016 2019

DesignThinkingUnderstandingthebusinesscontexttoreimagineprocessesalignedwithmeetingclientneeds 2016 2019

Brokers ofCapability

Orientinggovernance tosourceexpertisefromallavailablesources,bothinternallyandexternally,toaddresscapabilitygaps 2016 2019

CollaborativeEngagement

Ensuring relationshipsarecontractedtodrivesustainedexpertiseanddefinedoutcomes 2016 2019

IntelligentAutomation

Using ofautomationandcognitivecomputingtoblendanalytics,talent,andtechnology 2016 2019

Accessible&ActionableData

Applyinganalyticsmodels,techniquesandinsightsfrombigdata,real-time 2016 2019

HolisticSecurityProactivelymanagingdigitaldataacrossservicechainofpeople,systems&processes 2016 2019

Plug andPlayDigitalBusinessServices

Plugginginto“readytogo”business-outcomefocused, people/process/technologysolutionswithsecuritymeasures 2016 2019

Proprietary│Page44©2016HfSResearchLtd.ExcerptforAccenture

2016-17 Recommendations: Enterprise Buyersn MobilizeInternallyandExternallytoDriveMortgageAs-a-Service:RealizingthevisionforMortgageAs-

a-Servicewillrequiremultiplepartieswithinthelendingorganizationtocometogetherandshareadesiredoutcomesothattheycanthencoordinatefornewwaysofworking.Thewholeprocessshouldcreateadifferentkindofexperienceforthecompany,andtherebyfortheborrowers.Thiswillrequiresharedservicesheadsandthird-partyserviceproviderstoplaykeyrolesaspartnersthathelplenderschipawayattheirtraditionalpractices,towardsanewborrowerparadigm—valuingsimplification,transparency,andcontrolinthepropertybuyingexperience.

n IdentifytheInnovativeProviders—andChallengeThemFurther:Mortgagelenderstypicallyworkwithmultipleserviceprovidersforvariousoutsourcedwork,sometimesinheritingcontractsfromacquiredentities,oroldermulti-towerdeals.Werecommendyouasanenterprisebuyertakethetimetodosomelitmustestingonwhoinyourserviceprovidermixisreallythinkingaboutchangingthetraditionallaborarbitragemodel,andwillingtoinvestinpartneringondevelopingandofferingyouabroadersetofchoicesforwhatsolutionsyouadoptandhowtheyinteractwithyourownretainedorganization.Inoneexample,weheardofamajormortgagelenderthatdidthisexercisespecificallyaroundautomation,andfoundoneserviceproviderthatreallycamethroughwithopportunitiesforrevenuecannibalizationandnewcommercialmodels—andanactionplanforthestaffaffected—andonethatsimplyputtogetheralistofquickfixesthatcouldhavebeenmadeyearsagowithalittleeffort.Followingfromthepreviouspoint,trustedservicepartnerswillplayakeyroleinthesuccessofrollingoutyourdigitalstrategy.

n FindWaystoBreakInternalDeadlockswiththeHelpofYourServiceProvider: “Theybringusmorestuffthanwecanhandlewithourslowpaceofchange”wasafrequentresponsetoourinterviewquestiontolendersonwhethertheirserviceprovidersareinnovative.Buyersinthisindustryareawareoftheirneedtorespondto“fintech”and“digitaldisruption.”However,internalbureaucracies,traditionandinertiaareholdingthemback.Thisisanareawhereserviceproviderscanhelptobreakdownsilos,andreorientconversationsandconcernsaroundthebusinessoutcomes.Designthinkingisarelevanttoolthatcanhelpyouworkwithyourserviceproviderinamannerthatfacilitateslong-termsuccess.

Proprietary│Page45©2016HfSResearchLtd.ExcerptforAccenture

2016-17 Recommendations: Service Providersn Focus on Flexible and Global Delivery Capabilities: One of the biggest business imperatives that lenders

outlined for the next two years was the responding quickly to the changing business environment. “How dowe continue to grow in volume and market share and blueprint, with more and more M&A and businessexpansion, without actually growing physical presence in North America? Rates will go up at some point,and we’ll still have to maintain our production levels – we will always need cheaper, better, faster.” Lendersstill look for that next level of flexibility in scale and speed to market with business processes, and severaloutlined the need for service providers to work on this aspect, along with adding more onshore andnearshore delivery capabilities.

n As-a-Service Platforms Must Further Address this Need for Flexibility: Service providers that haveproprietary technology platforms for this industry must have a clear understanding of their potentialclients’ needs around flexibility/agility, balanced with their appetite for writing off legacy. SaaS deliverymodels with variable, transaction-based prices, capable of scaling up and down will address businessflexibility. However, in a lot of cases, lenders might not be able to do a complete overhaul of legacy LOS’, orwant to select modular slivers of capability to augment existing processes. Service providers must continueto develop progressive product paths, tightly coupled with redesigning/improving services from applicationto post-closing. However, they will need to be able to work at the pace of this market on its slow march toAs-a-Service.

n Clients Value Industry Expertise—Continue Down the Industrialization Path: The most and the leastsatisfied mortgage clients in our research pointed to the caliber of talent at different levels within theirservice providers’ organizations. Several clients were in awe of the rigorous mortgage industry trainingthat leading service providers undertake, and the associated certifications and licensing associated thatthey have to maintain. These education and training opportunities are increasing the analytical, industry,and automation capability of each service provider, that can then further strengthened with appointingmore leadership roles around risk and compliance, and SMEs within mortgage. This investment will drivenew levels of value and deepen relationships with clients.

ConfidentialandProprietary│Page46

About the Author

Proprietary│Page47©2016HfSResearchLtd.ExcerptforAccenture

Overview• Tracksverticalizedtechnology-enabledoperationsininsuranceandretail• Tracksenterpriseanalyticsservicesandmarketinganddigitalcustomerexperiencemanagementservices

• ConductsBlueprintreportsacrossserviceareasinglobalsourcing

PreviousExperience• ProjectManagerinthesourcingresearchwingofthebusinessresearchandconsultingfirmValueNotes,encompassingarangeofresponsibilities,includingresearchproductdesignanddevelopmentfortheoutsourcingcommunity,managementofcustomresearchengagements,anddevelopmentofthoughtleadershipthroughtargetedcontentandcommunityinteraction

• NicheBPOandKPOcoverage,includinganalytics,medicaltranscription,marketresearch,ande-learning

• Bespokeengagements,includingin-depthcompetitiveintelligencestudies,marketandinvestmentopportunityassessments,demand-sidesurveys,andmarketingcommunicationoptimizationforoutsourcingbuyers,providers,consultants,andinvestors

Education• Bachelor’sinBusinessAdministration,SymbiosisInternationalUniversity,India• Master’sinMarketingManagementwithBetaGammaSigmahonors,AstonBusinessSchool,UK

Reetika JoshiResearchDirector,Operations&AnalyticsStrategiesHfSResearch:Cambridge,MA

[email protected]@joshireetika

Proprietary│Page48©2016HfSResearchLtd.ExcerptforAccenture

About HfS ResearchHfSResearch isTheServicesResearchCompany™—theleadinganalystauthorityandglobalcommunityforbusinessoperationsandITservices.Thefirmhelpsenterprisesvalidatetheirglobaloperatingmodelswithworld-classresearchandpeernetworking.

HfSResearchcoinedthetermTheAs-a-ServiceEconomy toillustratethechallengesandopportunitiesfacingenterprisesneedingtore-architecttheiroperationstothriveinanageofdigitaldisruption,whilegrapplingwithanincreasinglycomplexglobalbusinessenvironment.HfScreatedtheEightIdealsofBeingAs-a-Service asaguidingframeworktohelpservicebuyersandprovidersaddressthesechallengesandseizetheinitiative.

Withspecificfocusonthedigitizationofbusinessprocesses,intelligentautomationandoutsourcing,HfShasdeepindustryexpertiseinhealthcare,lifesciences,retail,manufacturing,energy, utilities,telecommunications andfinancialservices. HfSusesitsgroundbreakingBlueprintMethodology™toevaluatetheabilityofserviceandtechnologyproviderstoinnovateandexecutetheEightIdeals.

HfSfacilitatesathrivinganddynamicglobalcommunityofmorethan100,000activesubscribers,whichaddsrichnesstoitsresearch.Inaddition,HfSholdsseveralServiceLeadersSummits everyyear,bringingtogetherseniorservicebuyers,providersandtechnologysuppliersinanintimateforumtodevelopcollectiverecommendations—fortheindustryandadddepthtothefirm’sresearchpublicationsandanalystofferings.

Nowinits tenthyearofpublication,HfSResearch’sacclaimedblogHorsesforSources isthemostwidelyreadandtrusteddestinationforunfetteredcollectiveinsight,researchandopendebateaboutsourcingindustryissuesanddevelopments.HorsesforSourcesandtheHfSnetworkofsitesreceivemorethanamillionwebvisitsayear.

HfSwasnamed AnalystFirmoftheYearfor2016,alongsideGartnerandForrester,byleadinganalystobserverInfluencerRelations.