hfmweek - hfm globalhfm.global/digitaleditions/hfmw/reports/hfm_gibraltar_2016.pdf · hfmweek.com 3...

TRANSCRIPT

FEATURING Argon Financial // GFIA // Gibraltar Finance // Gibraltar Stock Exchange // Hassans // ISOLAS // Nexus Fund Administration

WEEKHFMS P E C I A L R E P O R T

FLEXIBILITY Adapting to the needs of the industry

COOPERATION Working to create a stronger jurisdiction

SKILL Availability of expertise and services

GIBRALTAR 2016

H F M W E E K . CO M 3

I N T R O D U C T I O N

Published by Pageant Media Ltd LONDONThird Floor, Thavies Inn House, 3-4 Holborn Circus, London, EC1N 2HAT +44 (0) 20 7832 6500

NEW YORK 200 Park Avenue South Suite 1603, NY 10003T +1 646 891 2110

REPORT EDITOR Mike Sheen T: +44 (0) 20 7832 6628 [email protected]

HFMWEEK HEAD OF CONTENT Paul McMillan T: +1 646 891 2118 [email protected]

HEAD OF PRODUCTION Claudia Honerjager

SUB-EDITORS Luke Tuchscherer, Mary Cooch, Alice Burton, Charlotte Romeyer

GROUP COMMERCIAL MANAGER Lucy Churchill T: +44 (0) 20 7832 6615 [email protected]

HEAD OF BUSINESS DEVELOPMENT AMERICAS Tara Nolan T: +1 (646) 891 [email protected]

PUBLISHING ACCOUNT MANAGERS Amy Reed T: +44 (0) 20 7832 6618 [email protected] Roper T: +44 (0) 20 7832 [email protected] Butroid +44 (0)207 832 6613 [email protected]

CONTENT SALES Tel: +44 (0) 20 7832 6511 [email protected]

CEO Charlie Kerr

HFMWeek is published weekly by

Pageant Media Ltd ISSN 1748-5894

Printed by The Manson Group

© 2015 all rights reserved. No part of

this publication may be reproduced

or used without the prior permission

from the publisher

ibraltar’s position as a European finance centre continues to evolve and develop as a true alternative within Europe. Jurisdictions across the world are now adapting or introducing legislation that seeks EU equivalence, attempting to secure EU access from a fund distribution or investment services perspective. Gibraltar is a fund and investment services domicile providing a European passporting solution and access within an EU compliant framework.

Changes to regulatory frameworks across multiple jurisdictions seeking equivalence are important, but ‘third country’ access to Europe in respect of AIFMD or MiFID II is far from clear. What the changes show is that there will continue to be less and less regulatory arbitrage between different jurisdictions and a narrowing gap between non-EU and EU jurisdictions in this respect.

Gibraltar offers a secure, safe and typically low-cost jurisdiction that keeps complying with the full weight of European regulation, which can enhance from the full range of benefits. Consider the A.M. Best country risk tier for Gibraltar, which provides a CRT rating of one and a better rating than many other international finance centres. This rating denotes the lowest possible level of economic, political and financial system risk.

Also consider Gibraltar’s OECD report on transparency and exchange of information where the city received the same largely-compliant rating as the UK. This is of course critical to Gibraltar’s future and being on the front foot in terms of compliance and international standards has been a strategic direction.

This means Gibraltar is able to offer a European, fully-compliant framework, within a VAT exempt territory and extremely competitive rates of individual and personal tax. This is backed by a pro-active and engaged regulator, which has also been heavily invested in over the last few years.

The Gibraltar Finance Centre also strongly supports and assists the Gibraltar Funds and Investments Association (GFIA) and the Gibraltar industry in its efforts to develop the city in this space. Recent trips to Singapore, Hong Kong and Geneva are beginning to bear fruit as managers start to plan for the long-term. Meanwhile Swiss managers begin to see the changes to their own asset management industry, placing the classic independent asset manager model under regulatory pressures for the first time. These managers are not necessarily able to secure access to the EU under third country provisions provided by MiFID II, which will introduce additional requirements before they are able to offer their services in Europe. Gibraltar offers a tried and tested solution, which is likely to be faster and cheaper to establish and operate.

Similarly, in an AIFMD context Gibraltar can act not only as a domicile for the AIFM and the AIF, but is also one of the few smaller jurisdictions that has a selection of AIFM depositaries based within the jurisdiction to service such AIFs. Something that will become a requirement from 2017.

Gibraltar continues to offer a very strong value proposition and, as an association, GFIA continues to evolve and support the growth of the industry.

Joey GarciaChairman, Gibraltar Funds & Investments Association, for and on behalf of the GFIA Executive: James Lasry, Moe Cohen, Johann Olivera, Benjy Cuby, Carlos Martins, Jay Gomez, Jordan Ramagge.

GG I B R A L T A R 2 0 1 6

4 H F M W E E K . CO M

G I B R A L T A R 2 0 1 6 C O N T E N T S

PRIME BROKERAGE

PRIME BROKER REPRICING PRESENTS OPPORTUNITIES FOR SMALLER PROVIDERSSimon Brown, CEO of Argon Financial, talks to HFMWeek about the impact of prime broker repricing and what Gibraltar has to offer the industry

LEGAL

BUILDING A PASSPORTABLE EUROPEAN FUNDJames Lasry of Hassans talks to HFMWeek about the realities of marketing hedge funds in Europe and how marketing needs affect your choice of jurisdiction

FINANCIAL SERVICES

MAINTAINING A STRONG JURISDICTIONPhilip Canessa, senior executive at Gibraltar Finance, talks to HFMWeek about how Gibraltar supports its hedge fund industry

FINANCIAL SERVICES

A SOLUTIONS-DRIVEN JURISDICTION Jonathan Garcia, senior associate at ISOLAS, explains how Gibraltar’s fund industry is serviced with flexibility and competence

FINANCIAL SERVICES

EU ACCESSIBILITY: EXCHANGE TRADED INSTRUMENTSPhilip Young, marketing director of GSX Limited, explains the variety and versatility the Gibraltar Stock Exchange can offer

ACCOUNTING

CONTINUED GROWTHMoe Cohen, CEO of Benady Cohen & Co Group, Chartered Accountants including Nexus Fund Administration, talks to HFMWeek about the growth of Gibraltar’s fund industry and what the jurisdiction has to offer funds

06

08

11

14

17

20

In recent years, the fund industry in Gibraltar has seen rapid and impressive growth. Gibraltar is now a serious option for individuals and companies considering where to base investment funds.

Hassans has been at the forefront of this development and in 2004 became the first firm in Gibraltar to set up a funds practice, quickly establishing itself as the “go to” firm.

Hassans is ranked as the sole leader for Investment Funds by Legal 500 and EMEA

describe the department as a “Rolls-Royce investment funds practice...led by James Lasry, a leading investment funds lawyer with first-class knowledge of the local and wider market”. (EMEA 2014 Edition)

Hassans is fundamental to any fund being

set-up in Gibraltar whether Private, EIFs,

Non- UCITS Retail Funds, UCITS Funds or

Protected Cell Companies.

Hassans - 75 years in Gibraltar.

TAX PLANNING • CORPORATE & COMMERCIAL • FINANCIAL SERVICES • FUNDS • LITIGATION • PROPERTY • TRUSTS

International Lawyers

When it comes to funds...

...Hassans leads the way

www.gibraltarlaw.com 57/63 Line Wall Road, PO Box 199, Gibraltar. +350 200 79000 • +350 200 71966 • [email protected]

6 H F M W E E K . CO M

G I B R A L T A R 2 0 1 6

HFMWeek (HFM): Th ere is a growing trend of prime broker repricing occurring at the moment and costs are increasing as a result. What do you see at the main cause of this trend?Simon Brown (SB): Undoubtedly, the primary cause of this trend of prime broker repricing is the Basel III regu-latory framework on bank capital adequacy, stress testing and mar-ket liquidity risk. Th is framework contains a set of buff ers, capital and liquidity ratios, which have ef-fectively made it more expensive for the banks to conduct prime brokerage business; typically pro-viding fi nancing, custody, securi-ties lending, capital introduction, trading systems and access to markets. Th e key reason for the implementation of these require-ments and ultimately the scenario that many smaller funds and other corporates are now facing, is the type of bank trading that occurred up to 2008/09, which in turn was a catalyst to the systemic collapse and banking crisis.

It is important to remember that the banking crisis was not just a capital issue, it was a liquidity is-sue as well. As a result liquidity has become the focus for regulators, particularly those in Europe, in an eff ort to ensure that a systemic crisis will not occur again. Balance sheet effi ciency is now a main fo-cus for the banking industry with this focus precipitating in the large prime brokers becoming more selective in who they seek and keep as their clients.

In response to the framework of Basel III, the banks have been reviewing all client accounts to evaluate whether they can justify the return on equity (RoE) from those accounts. Repricing has been just one of the choices for increasing RoE. Some banks have also introduced minimum monthly fees for clients, or even both monthly fees and repricing.

And in many cases an increasing trend has emerged of prime brokers kindly asking funds and other corporates to look for alternative prime broker relationships.

Th is problem is tough enough if you are already a client of one of the larger prime brokers. New applicants are of-ten asked to jump through many more hoops before their

application is considered, with minimum balance sheet require-ments of more than $20m not un-common.

HFM: Do you think fund man-agers will begin to look to alter-native providers in an eff ort to lower costs?SB: Large bank prime brokers may fi nd themselves in a situation where they can no longer justify providing prime broker services to smaller funds. As a result, the mar-ket has opened up for smaller prime brokers (mini prime or prime of prime), who may not be burdened by legacy technologies/systems and high fi xed costs, with many boutique operators choosing a vari-able cost operational model. Th ese mini prime operators can therefore onboard the smaller clients as they do not have the high fi xed costs or the extent of capital and leverage constraints that the larger ‘bank’ prime brokers may have.

Th ere is no doubt that if exist-ing large prime brokers have been making noises about account re-views to their clients, these funds

and other corporates have been looking for alternative options for execution, lending, sett lement and custody. Th ere are also instances where medium-sized funds are coming under pressure from their prime brokers and this pressure is unlikely to subside in the near future, given the increased level and cost associated with the regulatory en-vironment and reporting requirements.

Gone are the days where banks would do their upmost

IN RESPONSE TO THE FRAMEWORK OF BASEL

III, THE BANKS HAVE BEEN REVIEWING ALL CLIENT

ACCOUNTS TO EVALUATE WHETHER THEY CAN

JUSTIFY THE RETURN ON EQUITY (RoE) FROM THOSE ACCOUNTS. REPRICING HAS

BEEN JUST ONE OFTHE CHOICES FOR INCREASING RoE

”

SIMON BROWN, CEO OF ARGON FINANCIAL, TALKS TO HFMWEEK ABOUT THE IMPACTOF PRIME BROKER REPRICING AND WHAT GIBRALTAR HAS TO OFFER THE INDUSTRY

PRIME BROKER REPRICING PRESENTS OPPORTUNITIESFOR SMALLER PROVIDERS

Simon Brown is CEO of Argon Financial. His career in the financial markets has spanned almost three decades. He worked for 12 years as a derivative trading specialist in London followed by 17 years building trading and agency businesses servicing institutional, corporate, hedge fund and high-net-worth clients. Simon founded one of the first institutional electronic derivative broking businesses and has been CEO of Argon Financial for eight years.

P R I M E B R O K E R A G E

H F M W E E K . CO M 7

to onboard any size fund to increase their client account quota in the hope that those applicants would grow to be-come large hedge funds.

HFM: How are smaller prime brokers able to provide their services to funds at a lower cost than larger firms?SB: All large ‘bank’ prime brokers are subject to all of the new capital and liquidity ratios imple-mented under the Basel III framework. Liquidity constraints for these large banks result is less capi-tal being available for their clients. However, there are some smaller tier one operators (investment firms) who have the permissions and capability to offer small-to medium-sized funds and brokers execution, clearing, lending and custody services, without the burden of the cost-base and liquidity constraints that the larger prime brokers are sub-ject to.

These mini prime brokers are therefore filling an important gap in the prime broker market, provid-ing key execution and custody services to the small funds and corporates who would otherwise be un-able to operate in these markets.

HFM: Do the large prime brokers welcome volume aggregators such as Argon Financial?SB: Absolutely. Even though the larger prime bro-kers may be unable to onboard and/or facilitate services for many funds and other corporates, they are still able to benefit from the volume when ag-gregated by a mini prime broker. In this instance the mini prime aggregator incurs the cost of on-boarding and administration of multiple small clients, while still facing the prime broker as one corporate omnibus account.

Among other roles, Argon Financial is one such mini prime broker. It has an extensive network of relationships with many of the large bank prime brokers. As a smaller firm, without some of the constraints

the larger banks have, it is able to onboard and service these funds and other corporates. That is not to say mini primes do not conduct similar KYC onboarding processes as the banks, but they may not have the extent of bureaucracy and administrative processes that the banks have, and are there-fore able to process applications more efficiently.

As long as mini prime brokers are able to fill the gap providing prime broker services to the small- to medium-sized funds and brokers, which may oth-erwise fail to reach the bar set by the larger prime brokers, the fund industry can continue to grow. However, without the participation of mini prime brokers, new entrants to the market may struggle to find adequate execution and settlement services by which to operate.

HFM: Why is Gibraltar an attractive jurisdic-tion for the hedge fund industry?SB: Argon Financial was founded and incorporat-ed in Gibraltar, simply because Gibraltar is a great place to do business. Gibraltar offers a robust regu-latory structure governed by the Financial Services Commission, with passporting capabilities into the rest of Europe. The Financial Services Commis-sion is structured to regulate investment firms (like Argon Financial), banks and funds, among others; with the Experience Investor Fund (EIF) structure seeing strong growth since its inception.

The Gibraltar funds industry also benefits from the recently set up Gibraltar Stock Exchange where funds can be publicly listed, regardless of size. If a fund wants an EU listing the GSX provides the platform for them to do so.

Gibraltar’s finance centre offers a well-regulated, transparent and internationally cooperative juris-diction. Although Gibraltar is relatively small, it is able to punch above its weight as a centre for finan-cial services and does an excellent job of providing

services to firms operating within its shores.

AS LONG AS MINI PRIME BROKERS ARE ABLE TO FILL THE GAP PROVIDING PRIME BROKER SERVICES TO THE SMALL- TO MEDIUM-SIZED

FUNDS AND BROKERS, WHICH MAY OTHERWISE FAIL TO REACH THE BAR

SET BY THE LARGER PRIME BROKERS, THE FUND

INDUSTRY CAN CONTINUE TO GROW

”

8 H F M W E E K . CO M

G I B R A L T A R 2 0 1 6

HFMWeek (HFM): What are the key challenges faced by hedge funds marketing themselves in Europe?James Lasry ( JL): AIFMD has fundamentally changed the way in which hedge funds are marketed in Europe. In the past, in order to be able to promote a fund to European investors you had to rely on questionable doctrines such as reverse solicitation. Th ese days, regimes have changed. Th is means that you must rely on national private-place-ment issues, which are now standardised among Euro-pean jurisdictions. Alternatively you must have a way of marketing funds throughout Europe. Th is is something that AIFMD can off er by way of the European Marketing Passport.

At AIFMD’s inception, the industry started looking at doctrines such as reverse solicitation. Th e industry has moved on in this respect. Th e dis-cussion that occurs now is primar-ily around national private-place-ment regimes.

Some thought is being given to using the marketing passport of AIFMD. But in my view, not enough thought is being given in this regard. Th is is because the perception has been that compli-ance with AIFMD doesn’t bring a lot of value to investors, but brings a lot of cost and regulatory bur-den. However, there are two big surprises with AIFMD: First, com-pliance is not nearly as diffi cult as was feared. Second, the national private-placement regimes have ac-tually been tightened, in many in-stances, well in advance of the 2018 deadline imposed by the directive. So with these regimes, by and large, being diffi cult to comply with (with the notable exception of the UK), it would stand to reason that managers that wish to market into the EU should consider a passportable vehicle.

HFM: Which of the European jurisdictions should one use in order to have a passportable fund?JL: Most of the industry has been used to jurisdictions like the Cayman Islands. It would stand to reason, therefore, that rather than going to jurisdictions that have very diff er-ent regulatory philosophies, funds should operate in juris-

dictions that are as close to Cayman in terms of its regula-tory structure as possible, while still being in the context of the EU.

When you consider common law, the prevalence of the English language, ultimate appeal to the Privy Council and a regulatory philosophy similar to that of the Cayman Is-lands that allows you to launch a fund before you receive regulatory approval, Gibraltar checks all of these boxes. Gibraltar is the closest jurisdiction to the Cayman Islands, in terms of regulatory experience, that one is likely to get within the context of the EU. It also of course provides the ability to passport throughout the EU.

Th e industry is probably insuffi ciently aware of the speed-to-market capabilities of launching inherent in the process of launching a fund in Gibraltar. For example, in

Gibraltar you can establish your funds in as long as it takes to draft the documentation and open the various bank and brokerage ac-counts. You are then able to launch the fund aft er just 20 days of notifi -cation from the regulator. Th is fund will be passportable throughout the EU. In contrast, in other jurisdic-tions you would have to potentially wait signifi cant periods of time for that fund to become authorised in its own right, which is in addition to authorisation of AIFMD itself, before you can begin trading with that fund. My estimation is that this process would take six weeks at the very least, and potentially several months to complete in other Euro-pean jurisdictions.

Furthermore, the costs in Gi-braltar are signifi cantly lower than

in other European jurisdictions. It is possible to set up a fund with much lower AuM than would be viable in these jurisdictions.

HFM: What is Hassans role in helping its clients over-come the challenges associated with marketing a fund in Europe?JL: First of all, we help by identifying the client’s invest-ment and marketing needs. We advise clients on the most appropriate regulatory regime for them to meet those needs.

GIBRALTAR IS THE CLOSEST JURISDICTION TO THE CAYMAN ISLANDS, IN

TERMS OF REGULATORY EXPERIENCE, THAT ONE IS LIKELY TO GET WITHIN THE

CONTEXT OF THE EU

”

JAMES LASRY OF HASSANS TALKS TO HFMWEEK ABOUT THE REALITIES OF MARKETING HEDGE FUNDS IN EUROPE AND HOW MARKETING NEEDS AFFECT YOUR CHOICE OF JURISDICTION

BUILDING A PASSPORTABLE EUROPEAN FUND

James Lasry is head of funds at Hassans Law Firm. He has been instrumental in setting up many of Gibraltar’s funds, including the first Experienced Investor Fund (EIF) and Protected Cell Company (PCC) Fund and advises the govern-ment of Gibraltar on funds legislation.

L E G A L

H F M W E E K . CO M 9

HFM: What role has Hassans played in advis-ing the Gibraltar government on new laws?JL: Just over 10 years ago, my colleagues proposed the Experienced Investor Fund (EIF) legislation to the government. This proposition was reviewed by the Finance Centre, the regulator and the govern-ment. In what is a tribute to the open-mindedness of this small jurisdiction, this legislation became law within 12 months of the original proposition. In legislative terms, this is just about the speed of light.

This is possible because of the close relationship that exists between the government, the regulator and the industry in Gibraltar. In fact, the industry since then has become much more galvanised. This can be seen through the work of the Gibraltar Funds & Investments Association. This three-part relationship has become that much stronger as a result, which allows for innovation and prudent regulation.

HFM: How do you expect the hedge fund industry to develop in the years ahead with regard to AIFMD?JL: The industry has found it difficult to get to grips with

AIFMD because it is such a fundamental change in the way funds are managed. Hedge funds and private equity funds are now obligated to create or employ an AIFMD manager, which in many ways is analogous to a Ucits. This is not necessarily ful-filling an investment manager role that it used to before the directive. Because of this, much of the industry seem to be clinging to the old ways of structuring funds and using the same jurisdictions as they used to before the directive.

I think that with time the industry will become more comfortable with both the requirements and advantages presented by AIFMD with regard to passporting rights. This is particularly relevant in the respect of the narrowing and closure of private-placement regimes, as well as the possible opening up of passporting to third jurisdictions. I think the AIFMD will become the norm for marketing into Europe. It has taken time, but the industry will

adapt. When it does, jurisdictions like Gibraltar that offer very competitive solutions as a result of not ‘gold-plating’ the directive, will become a much more prevalent and pop-ular fund jurisdiction.

WITH TIME THE INDUSTRY WILL BECOME MORE

COMFORTABLE WITH BOTH THE REQUIREMENTS AND ADVANTAGES PRESENTED

BY AIFMD WITH REGARD TO PASSPORTING RIGHTS

”

F I N A N C I A L S E R V I C E S

H F M W E E K . CO M 11

G I B R A L T A R 2 0 1 6

HFMWeek (HFM): How has Gibraltar’s hedge fund industry developed over the past decade?Philip Canessa (PC): We introduced the Experienced Investor Funds (EIFs) regime in 2005 and since its intro-duction it has been the main driver of growth of our fund industry. The EIF has proved to be an excellent vehicle for the establishment of hedge funds. This has become more significant since the introduction of the AIFMD, as EIFs may be operated as a compliant Alternative Invest-ment Fund under AIFMD.

Our EIF is a very flexible and attractive vehicle with a number of key advantages such as a pre-launch ap-proval process, competitive start-up costs, it can be self-managed and it is tax neutral.

Our regulator, the Gibraltar Financial Services Commission, currently have around 200 regis-tered EIFs, including sub-funds with investment strategies, which include securities, mixed strategies, fund-of-funds, real estate and private equity among others.

MAINTAINING A STRONG JURISDICTION

PHILIP CANESSA, SENIOR EXECUTIVE AT GIBRALTAR FINANCE, TALKS TO HFMWEEK ABOUT HOW GIBRALTAR SUPPORTS ITS HEDGE FUND INDUSTRY

F I N A N C I A L S E R V I C E S

1 2 H F M W E E K . CO M

G I B R A L T A R 2 0 1 6

HFM: What does Gibraltar ensure are effi cient and appropriate regulatory framework?PC: We have a forward-looking and eff ective regulator that treats the fi rms it authorises and supervises in the same manner as the private sector fi rms treat their clients.

Th is means being fast and responsive. Th ere are many jurisdictions in Europe, let alone outside Europe, where the regulator is able to deal with the applications at what-ever pace it wishes and is not accountable to anyone.

We do not believe that this should be the case. We have invested heavily and worked very hard with our regulator to ensure that it is delivering speed to market. Th at is of fundamental importance in fi nancial services in today’s world.

What we expect from our regu-lator is a fast, responsive and effi -cient service to license fi rms, not just in the application process but in the general regulatory approach and environment.

As a small jurisdiction we all work together; the regulator, the government and the industry pro-fessional to achieve this aim. HFM: What are the tax advan-tages of operating a fund in Gi-braltar?PC: If we talk about the EIF, which is the fund vehicle for hedge funds, these funds are tax neutral. Th is means that the EIF itself does not pay tax.

Th e tax advantages, however, can also be enjoyed by the regulated AIFM or investment manager and by cer-tain individuals working for the regulated fi rm. Th e cor-porate tax rate chargeable on taxable profi ts of the fi rm is 10% and the eff ective rate of income tax for individuals is 25%.

Th ere is a scheme, the high executive possessing spe-

cialist skills (HEPSS) scheme, for individuals who have skills or experience that are not available in Gibraltar, and deemed necessary to promote and sustain economic ac-tivity of particular economic value to Gibraltar.

Th ese individuals must also have approved residential accommodation in Gibraltar. Th e HEPSS could be the CEO or chief investment offi cer of a hedge fund man-agement fi rm and, under this scheme, the individual’s personal tax would be capped at approximately £30,000, providing the individual’s earnings are in excess of

£120,000 p.a.

HFM: How important is Gibral-tar’s position as an EU domicile in appealing to hedge funds?PC: Th is is extremely important and more so following the trans-position and introduction of the AIFMD. Gibraltar is within the European Union and can there-fore passport its fi nancial services throughout the EU.

As an example, a non-EU man-ager wanting to market their ser-vices or raise capital within the EU, could set up in Gibraltar and pass-port its services from the Gibraltar fi rm to the rest of the EU.

Th is advantage obviously does not apply solely to non-EU manag-ers. A start-up manager from the UK could also use Gibraltar to set up and take advantage of the costs and effi ciencies associated with a small jurisdiction, but having

all the benefi ts of a familiar legal and regulatory system within a high quality infrastructure and a good quality of life.

HFM: How else is Gibraltar able to support funds in-dustry?PC: Th e funds industry is supported by high quality ser-vice providers. We have banks, which are licensed deposi-taries as required under the AIFMD and 10 licensed fund administrators.

HFM: How do you expect Gibraltar’s fund industry to develop in the decade ahead?PC: We are very confi dent our funds industry will de-velop in a very positive way in the decade ahead. We have been very active in raising the profi le of our jurisdiction and in informing professionals in diff erent geographical areas about our funds regime.

As part of this strategy, for example, we visited Singa-pore and Hong Kong in July of this year, where we hosted events, together with a delegation of fi nancial services professionals from Gibraltar, and explained the benefi ts of using Gibraltar and what it has to off er.

We are also focusing our business development pro-gramme in London and Switzerland, our traditional tar-get locations, and are certain that this will develop suc-cessfully for us.

THE FUNDS INDUSTRY IS SUPPORTED BY

HIGH QUALITY SERVICE PROVIDERS. WE HAVE BANKS, WHICH ARE

LICENSED DEPOSITARIES AS REQUIRED UNDER THE AIFMD AND 10 LICENSED FUND ADMINISTRATORS

”

Philip Canessa joined Gibraltar Finance as senior finance centre executive, focusing on the development of the funds and asset management sectors, in which he has more than 30 years of experience. He was managing director of an investment firm for 11 years and also served as a board director in different jurisdictions.

EVERY WEEK YOU WILL RECEIVE More exclusive stories than any other hedge fund publication All the latest searches and investment news Exclusive data on launches and performance Investment strategy analysis Topical comment from leading industry figures

Exclusive research surveys Regulatory developments People on the move

As a subscriber, you will also receive full registration to www.hfmweek.com, where you can access:

Daily updated performance data Exclusive research Daily news alerts Industry events information Service directory listings and much more...

vF O R M O R E I N F O R M A T I O N P L E A S E C O N T A C TThe Membership Team at +44 (0)207 832 6511 OR email membership@hfmweek .com O R V I S I T H F M W E E K . C O M F O R D E T A I L S

THE BEST READ IN THE HEDGE FUND INDUSTRY

SUBSCRIBE TO

www.hfmweek .com

THE DEADLINE FOR imple-

menting controversial parts of

Mifid II could be delayed beyond

January 2017 as Esma prepares

to water down the proposed ban

on dealing commissions to pay

for research, HFMWeek under-

stands.

The directive, first f loated in

2010, includes an overhaul of

managers’ commission arrange-

ments, transaction reporting

and recording requirements.

It is understood the European

Commission is considering a

delay as commission propos-

als have been caught up in

political wrangling. The UK’s

Investment Association wants a

one-year delay.

Under Esma’s proposed

advice, commission sharing

agreements (CSAs) would not

be acceptable and managers

would need to pay for research

directly or through a ring-

fenced account.

An HFMWeek poll shows

76% of managers support a

delay to the directive, with 17%

wanting to go ahead as planned

and 7% believing delays should

only come if there are major

changes.

“There is clearly a lot of appe-

tite for it to be delayed,” said Nick

Colston, partner at Simmons

and Simmons. “The latest

rumour is that parts of the imple-

mentation could be delayed with

most brought in by

January 2017.”

Managers back implementation

postponement

BY SAM DALE

03

COMMENT THE CHANGING WORLD OF HEDGE FUND ADMIN

14

Mifid II delay likely

as Esma considers

softening rules

THIRD POINT

RULING SPARKS

CALLS FOR REFORM

MANAGERS WANT “OUTDATED

RULES” CHANGED ANALYSIS 21

LAUNCHES 10

EX-HIGHBRIDGE AND BLUE RIDGE PROS PREP L/S EQUITY FUND

Jim Glynn and Nicholas Danaher to start Domando by year-end

LAUNCHES 03

DAVIDE SERRA’S ALGEBRIS EXPANDS PRODUCT RANGE

Financials specialist opens global diversifi ed Ucits

REGULATION 09

MORE CTAS AND CPOS MUST JOIN NFA AFTER CFTC RULING

Regulator to force swaps-only funds to join association

HFMWeek research highlights the

large numbers of ex-regulators who

have walked through the revolving

door to work for hedge funds

ANALYS IS 16

The long and the short of it

ISSUE 393 24 Sep 2015

THE REGULATORS

GOING HEDGE

FUND NATIVE

r indd 1

22/09/2015 17

www.hfmweek .com

BREVAN HOWARD HAS

raised nearly $500m for its spe-

cialist Argentine fund that invests

in a mixture of equities and

bonds, HFMWeek understands.

The $27bn Jersey-based

firm launched the vehicle last

December, according to SEC fil-

ings, with the open-ended fund

invested in a mixture of sover-

eign debt and equities, according

to reports at the time. The fund, which is understood

to have $448m in AuM, is run by

portfolio manager Ben Melkman,

a partner who has been with the

firm since 2009. Prior to this he

worked as a director in Morgan

Stanley’s fixed income division

and an analyst at Deutsche Bank.

There are currently 12

Argentina-focused hedge funds,

according to figures from Pre-

qin, with a total of $878m of

assets, plus a number of other

hedge funds with exposure to

the country as part of emerging

market strategies. A number of Argentina-

focused hedge funds have

launched in the past year as

firms bet on an improving eco-

nomic climate. Presidential

elections take place next month

and experts suggest the nation

will resolve its differences with

holdout creditors who did not

accept the terms of previous

debt restructurings and have

been pushing for a full payout on their bonds.

Fund one of a number looking to take advantage of

opportunities in the region BY BENJAMIN JAGLOM

03

COMMENT HOW EU REGULATION IS CHANGING SERVICE PROVIDER RELATIONSHIPS 14

Brevan Howard’s Argentina fund

assets near $500m

LONDON KEEPS CALLINGHFMWEEK SPEAKS TO

DELOITTE’S CHRIS FARKAS ANALYSIS 16

LAUNCHES 11

EX-ABYDOS COO PREPS GLOBAL MACRO FUND

Paul Brunsden founds Ironwall Capital Management

LAUNCHES 05

CF PARTNERS HIRES CIO AHEAD OF EVENT-DRIVEN LAUNCH

Fund structure moves from RS Platou Asset Management

TAX 07

HEDGE FUNDS BACK EC ACTION ON WITHHOLDING TAX RELIEF

Cross-border lending hurdles to be removed, leaked plan suggests

HFMWeek looks at the new recording

requirements ushered in by Mifi d II

and why some hedge fund fi rms

remain unprepared

ANALYS IS 19

The long and the short of it

ISSUE 394 1 Oct 2015

GET READY FOR A

REVOLUTION

001_003_HFM394_cover.indd 1

29/09/2015 17:01

www.hfmweek .com

A FORMER ZIFF Brothers sec-

tor head is planning to launch a

long/short equity hedge fund,

HFMWeek has learned.

Will Cook registered Stam-

ford, Connecticut-based Sunri-

ver Management with the SEC

in June this year and plans to

launch by year-end, HFMWeek

understands. Cook has lined up

former JAT Capital Management

CFO Justin Morgan to take on

the same role at Sunriver, regula-

tory filings indicate.

HFMWeek understands a

number of other staff could also

join Sunriver from an affiliated

family office.

Through a Cayman master/

feeder structure, Sunriver will

run a fundamental equities strat-

egy, buying “high-quality compa-

nies” that are temporarily marked

down but can outperform as mar-

ket concern fades, and shorting

“lower quality companies” that

have long-term business issues

overlooked by the market.

The strategy will invest pri-

marily in publicly traded US

equities, but may also trade in

common or preferred stocks,

sovereign and corporate debt,

bonds, convertibles, derivatives

or commodities.

Cook spent over 10 years

working for Ziff Brothers Invest-

ments, the Ziff family’s internal,

multi-billion-dollar hedge fund,

which closed down at

the end of 2013.

Will Cook teams with former JAT

Capital CFO to set up Sunriver

Management

BY JASMIN LEITNER

03

COMMENT THE IMPACT OF BREXIT ON THE UK HEDGE FUND SECTOR

14

Ex-Ziff Bros sector

head to launch l/s

equity fund

SEC TURNS UP

CYBER-SECURITY

HEATTHE REGULATOR GETS

SERIOUS ON TECH CRIME

ANALYSIS 21

LAUNCHES 11

QVT SPINOUT PORTSEA EYES DECEMBER TAKE-OFF

Firm led by de Weck and Spoljaric expects $50m day-one capital

UCITS 07

AMUNDI EYES UCITS PLATFORM START DATE IN 2016

Private banking clients push for fund vehicle

LAUNCHES 10

EX-DAIWA CHIEF ECONOMIST PREPS DEEPWATER

China-focused fund receives seeding from Westpac subsidiary

HFMWeek takes a look at the biggest

prospects for next year from funds

registered in the last 12 months

ANALYS IS 16

The long and the short of it

ISSUE 395 8 Oct 2015

06/10/2015

www.hfmweek .com

T WO R E L AT ION A L INVESTORS principals are

planning to launch an activ-ist hedge fund early next year, HFMWeek understands.John Sullivan and Jay Winship

have set up San Diego-based ActionView Capital and are aim-

ing to launch the ActionView Capital Fund I early next year,

a marketing document seen by HFMWeek indicates.$6bn Relational started

winding down last year after co-founder Ralph Whitworth

had to step back on account of health issues, with some reports

indicating at the time that exec-

utives may launch a new fund using Relational’s name.

The fund, which is likely to have onshore and offshore ver-

sions, will seek “to generate excess performance by proac-

tively engaging management teams, board members and

other constituencies to accom-plish positive change intended

to increase shareholder value”, the document said.ActionView Capital Fund I

will take a three- to five-year horizon to invest in a concen-

trated portfolio of underper-forming or out-of-favour com-

panies with strong cash f lows from sound core businesses.

The strategy will focus on mid-cap companies and take

between eight and 15 positions, starting

John Sullivan and Jay Winship to lead new San Diego-based

venture BY JASMIN LEITNER

03

COMMENT NAVIGATING THE COMPLEX MAZE OF RESPONSIBLE INVESTING14

Relational duo set to launch activist hedge fund

UNUSUAL FUNDEXPENSESINVESTOR CONCERN OVER HFMWEEK/CONVERGENCE RESEARCH

ANALYSIS 19

LAUNCHES 11

ACADIAN PREPS SYSTEMATIC LONG/SHORT EQUITY FUND

Boston manager to launch strategy after $50m commitment

SEEDING 05

NEW TAGES CAPITAL CEO UNVEILS SEEDING PLANS

Over $600m will be put to work next year says Jamie Kermisch

INVESTMENT 07

DYAL CAPITAL ACQUIRES STAKE IN CHENAVARI

London manager is latest to sell equity to private equity fund

Despite the hedge fund-bashing headlines, experts say the policies of

Republican frontrunners would be a boon for the sector

ANALYS IS 16

The long and the short of it

ISSUE 396 15 Oct 2015

DON’T BELIEVE THE POLITICAL HYPE

001_003_HFM396_News.indd 1

1 4 H F M W E E K . CO M

G I B R A L T A R 2 0 1 6

Gibraltar’s burgeoning fi nancial services sector dates back to 1967, when provi-sions for a special tax regime for interna-tional business were made. Th e industry has made great strides since those early days, transitioning into an “onshore” Eu-

ropean fi nancial services centre, with numerous benefi ts for funds and managers.

Gibraltar’s vantage point over the Western Mediter-ranean, known as the meeting place of continents, and its subtropical climate, are not the only factors att racting fund and fund managers to the British territory. Gibraltar’s regulator, the Financial Services Commission (FSC), has a strong history of delivering eff ective regulation that is modern and effi cient, operating to defi ned standards. Th e FSC, with the full support of the government of Gibraltar, is implementing a strategic plan with the objective of oper-ating in a professional and proportionate manner. Th e FSC is concentrating on the issues that matt er most, working to respond in shorter timescales and minimising the bur-den and cost of compliance, while delivering these changes with “business as usual” delivery. Th e FSC provides clear process and set timeframes for approval of applications and has recently established service standards shorter than that stated in legislation. Th is will further streamline the application and regulatory processes for ap-plicants.

UNIQUE PROPOSITION IN THE EUService-driven culture and the ju-risdiction’s approach to speed to market, has seen the number of licensed funds and managers grow. Th e Experienced Investor Fund (EIF) has been popular and de-spite regulatory challenges expe-rienced worldwide, Gibraltar con-tinues to have the facility to launch an EIF and notify (rather than ap-ply to) the FSC post-launch. Th is reduces any regulatory down-time, which makes this a unique propo-sition within the EU. Th e EIF also off ers a free choice of management style; a self-managed fund provides an alternative to third party management.

Gibraltar has a territorial corporate tax regime, which only taxes profi ts that are derived from a Gibraltar source.

Irrespective, managers licensed and regulated under Gi-braltar law are taxed in Gibraltar on their profi ts. Th e standard rate of company tax is 10%. Funds are generally structured to be tax-neutral. Th is can be achieved in two possible ways:• Th e fi rst is by obtaining a certifi cate from the commis-

sioner of income tax for an exemption on tax on invest-ment income to be granted. Under this certifi cate the fund is not subject to corporate tax on invested income.

• Th e other option is to elect to be taxed under Gibral-tar’s corporate tax regime, which is unlikely to result in tax liabilities unless the fund is investing in physical as-sets located in Gibraltar.

EMPLOYEE BENEFITSIncentives also exist for employees of fund managers. Th ose who meet certain criteria can avail themselves of the High Executive Possessing Specialist Skills (HEPSS) sta-tus and will only be taxed on the fi rst £120,000 of earned income, which at the current rate of income tax caps their tax at around £30,000. Gibraltar does not tax investment income, there is no capital gains tax, no wealth tax, no inheritance tax and the territory is excluded from the re-quirement to levy VAT, despite being in the EU. Territories

such as Malta, Dublin and Luxem-bourg for example, all levy VAT.

Th rough tax information ex-change agreements being entered into by the government, Gibraltar’s full integration in the EU and com-pliance with EU fi nancial services regulation, money laundering and co-operation rules, the territory has ended all distinction between “onshore” and “off shore” busi-ness. In October 2015, the Global Forum of the OECD on transpar-ency and exchange of informa-tion for tax purposes published the Phase Two peer review report on Gibraltar, rating it as ‘Largely Compliant’ overall with regard to the exchange of tax information in practice. AM Best rating agency has given Gibraltar a top score in

all three areas of evaluation: very low political risk, very low economic risk and very low fi nancial system risk. Th e chief minister of Gibraltar also recently announced that it would be the fi rst EU jurisdiction to have a central

SERVICE-DRIVEN CULTURE AND THE JURISDICTION’S APPROACH TO SPEED TO MARKET, HAS SEEN THE NUMBER OF LICENSED

FUNDS AND MANAGERS GROW

”

JONATHAN GARCIA, SENIOR ASSOCIATE AT ISOLAS, EXPLAINS HOW GIBRALTAR’S FUND INDUSTRY IS SERVICED WITH FLEXIBILITY AND COMPETENCE

A SOLUTIONS-DRIVEN JURISDICTION

Jonathan Garcia is a senior associate within the Funds and Investment Services Team at ISOLAS. He advises on a wide array of fund structures and solutions and is also routinely involved in assisting investment firms to become authorised in Gibraltar. He is ranked as an ‘up and coming’ practitioner in Chambers Global 2015, having attracted praise for his work on structuring of investment funds.

F I N A N C I A L S E R V I C E S

H F M W E E K . CO M 15

register of beneficial ownership of companies, which will be in place before the end of the year.

AIFMD COMPLIANCEAs an EU territory, Gibraltar is fully compliant with the AIFMD. While the directive has created many challenges for managers, its arrival has drawn attention to the posi-tive changes it will have for Gibraltar’s funds industry. In the transposition of the AIFMD to national law, EU countries were permitted to decide how to address the various derogations inherent in the AIFMD.

Some countries decided to gold-plate the AIFMD, taking the opportunity to include addi-tional provisions not covered by it, into local law. Implementation differences range from differences in regulation covering managers managing assets be-low the AIFMD’s de minimis threshold (i.e. €100m [$114.5m] for open-ended funds and €500m [$572m] for closed-ended funds without leverage), to depositary rules for out-of-scope funds, delega-tion rules, remuneration rules and the application of private placement laws. Gibraltar’s implementation approach has been to retain as much flexibility as the AIFMD provides for.

The EIF continues to form the basis for the regu-latory regime underlying an AIFMD-compliant fund. Gibraltar has also retained its EIF regime for those funds whose managers are out of scope of AIFMD, while allowing these managers to opt-in to AIFMD should they wish to. For those managers out of the scope of AIFMD, Gibraltar’s private placement re-gime, which was introduced at the end of 2014, means that Gibraltar funds and their managers would be allowed to

private place in territories that have introduced an equiva-lent regime.

Gibraltar can offer one of a number of solutions to many of the non-EU managers who are now facing a new era of financial services regulation, which although largely equivalent to EU standards, does not guarantee access to the European market. This will be even more impor-tant, given that the European Securities and Markets Au-

thority (Esma) has announced that it will delay publishing its advice on the application of the European marketing passport under AIFMD to non-EU managers and funds, and its opinion on the functioning of the passport for EU AIFMs and national private placement regimes until the fourth quarter of 2016. A Mifid or AIFM licence from Gibraltar would have the same effect as an equivalent licence from Luxembourg, London or Frankfurt but at a fraction of the cost.

OFFERING SOLUTIONSThe Gibraltar establishment options are varied. One possibility is that of using an investment management platform or incubator who is able to meet ongoing operational requirements, provide the support functions and resources that will be required for the substance requirements to be met and provide the operational and staff support that is required. This could work as an equivalent to full set-up and provide a shorter term solution for

managers who may not be able to take the full cost of com-pliance with AIFMD as a standalone manager. Gibraltar has the framework and service providers in place to offer these solutions.

GIBRALTAR’S IMPLEMENTATION

APPROACH HAS BEEN TO RETAIN AS MUCH

FLEXIBILITY AS THE AIFMD PROVIDES FOR

”

F I N A N C I A L S E R V I C E S

H F M W E E K . CO M 17

G I B R A L T A R 2 0 1 6

The Gibraltar Stock Exchange (GSX) opened in November 2014. GSX is an EU regulated market operating under FSC license and rec-ognised by the European Securities and Mar-kets Authority (ESMA).

GSX off ers access and solutions for the fund management industry, targeting asset managers who had not previously considered a listing on an EU exchange because of cost and complexity. GSX also has a stream-lined listing process across all product lines that is fast to market and commercially att ractive compared to its peers.

LISTING YOUR FUND ON GSX: THE FIRST STEP TO RAISING VISIBILITY IN THE EUA fund listing on GSX raises EU visibility and comple-ments distribution capability. Many institutions have in-vestment restrictions on non-listed securities. For inves-tors, a listed status shows a fund has met the standards of an EU exchange. GSX’s website off ers transparency, displaying regular fund data and reporting information.

AIFMD AND ACCESSING THE EUROPEAN MARKETRecent studies show non-EU managers are ignoring EU-based investors in order to avoid complying with AIFMD. Managers prefer to avoid the extra compliance costs, the risks that occur due to regulatory uncertainty and lack of guidance surrounding the directive.

Compliance rates for non-EU managers are low. Only 15% of US hedge fund managers and a quarter of fi rms across Asia and rest of world are currently compliant with AIFMD. Th e costs of compliance are higher than expected and 40% of fi rms with less than $100m AuM have made the strategic decision not to market a fund within the EU.

GSX off ers an alternative, fast to market, fl exible and economic solution for fund managers who want to include the EU as part of their growth strategy.

SECURITISATION AND EXCHANGE TRADED INSTRUMENTSTh e concept of securitisation, though not new, can be

applied innovatively to the asset management industry. By securitising alternative investments (without any restric-tion on asset classes) and issuing securities (debt), whose repayment value is linked to such alternative investments, it is then possible to list these securities on an EU regulated market such as GSX.

Exchange Traded Instruments (ETIs or asset-backed se-curities) listed on GSX, with approved prospectuses, qualify for EU passporting rights

SECURITISATION IN PRACTICETh e structure works as follows:

Asset Manager

Hedge Fund

Special Investment Vehicle

Securitisation Company

Exchange Trading Instruments

EU Professional Investor

Gibraltar Stock Exchange

Promote

PHILIP YOUNG, MARKETING DIRECTOR OF GSX LIMITED, EXPLAINS THE VARIETY AND VERSATILITY THE GIBRALTAR STOCK EXCHANGE CAN OFFER

EU ACCESSIBILITY: EXCHANGE TRADED INSTRUMENTS

Philip Young, marketing director, has over 26 years’ investment industry experience. He began his career in investment banking before moving to investment management where he spent five years with a start-up hedge fund and, latterly, five years with a principal emerging market private equity firm. Philip is a CFA Charterholder.

F I N A N C I A L S E R V I C E S

1 8 H F M W E E K . CO M

G I B R A L T A R 2 0 1 6

A special investment vehicle (SIV) is set up as a limited li-ability company, which then opens an account with a finan-cial institution and the asset manager makes an allocation of assets to be held within the SIV.

The Securitisation Cell Company (SCC) now issues an ETI unit that is a pass-through instrument of the invest-ments held within the SIV.

The ETI is therefore linked to and backed by the SIV and this passes through all the performance risks of the SIV to the investor of the ETI units.

Setting up an SCC in an EU jurisdiction that can issue these innovative financial instruments is critically impor-tant. It is vital such jurisdictions have an appropriate secu-ritisation act and SCC legislation.

These SCCs act as issuer for these ETIs and the proceeds of each of these issurances can be allocated to a segregated account of the SCC.

It is also important no creditor of the company has access to these assets even in the event of bankruptcy or in-solvency procedures.

BENEFITS OF EXCHANGE TRADED INSTRUMENTS• The Speed to Market: a securitisation transac-

tion can be structured and listed on GSX, with-in a few weeks.

• Unrestricted Choice of Asset Class: ETIs have no restrictions on the asset classes, any alterna-tive investments are eligible for a securitisation transaction.

• EU Promotion: ETIs listed on GSX are Ucits el-igible assets issued with an approved prospectus suitable for a public offering in the EU.

• Flexibility: ETIs have considerable flexibility and are created as a bespoke product. They may be designed with the components required by the client, for instance specified lock-in periods, weekly, monthly or quarterly subscription/re-demption periods, distributions, variable profit-related interest components. Sharia compliant Islamic Finance ETI products are also available.

• Licensed asset managers from third countries such as Hong Kong, Singapore, the US, and Switzerland are also able to act as the investment man-ager in such securitisation transactions.

• Regulation: ETIs issued by SCCs under ECB regula-tion 24/2009/ECB are not AIFs and are regulated by the Securitisation Act in the EU domicile of incorpora-tion.

MARKETING OPPORTUNITIESWith interest from all over the world to establish securiti-sation structures, ETIs have enormous potential to provide non-EU managers with passport and promotion rights throughout the EU.

The listing of ETIs on GSX with an approved prospectus ensures suitability for a public offering to professional inves-tors throughout Europe.

Professional investors, through their usual broker rela-tionship, can consequently purchase ETIs in a simple and price transparent way.

ETIs are always feeders into the underlying assets and have no derivative or leverage embedded.

EXPANDED CUSTOMER BASE UCITS ELIGIBILITYThe Ucits eligible assets regulation clearly states that securi-ties listed on an EU regulated market are eligible assets for a Ucits fund even if they are collateralised by and/or linked to otherwise non-eligible assets. ETIs can make your fund eligible for Ucits portfolios.

PRACTICAL EXAMPLESETIs can be used to test demand within the EU and directly gauge professional interest.

It will be possible for asset managers to work with GSX listing agents to securitise alternative assets, structure an ETI and list the instrument on GSX in order to access Eu-ropean investors.

A small non-EU asset manager may wish to gauge inves-tor interest within the EU by first launching an ETI. Such solutions can be provided at a fraction of the cost of tradi-tional compliance and in smaller issue sizes (€3-5m, for ex-

ample) perhaps not sustainable within a traditional fund structure.

EU AIFMs can also consider securitisation. An asset manager in London may wish to test a new trading strategy and bring a product offering to his client base. He may wish to limit the offering to €5-10m, a level at which may not be economically sustainable under a traditional fund model. The ETI route provides an ideal solution.

Ucits funds are not able to invest in alternative funds. Nonetheless, the eligible assets directive of the EU states that securities listed on a stock ex-change, linked to and backed by an asset that is non-eligible, will themselves be eligible for purchase by a Ucits funds.

A fund of funds established under Ucits regula-tions may wish to consider an investment in an open-ended real estate fund. While real estate funds themselves are alternative investments and ineligi-ble assets under the Ucits directive, by securitising the units of the real estate fund into an ETI and list-ing them on GSX, it becomes eligible.

A Ucits manager can buy the ETI units that are linked to and backed by real estate fund units and

consequently has the risk and reward profile of the underly-ing assets.

GSX’S NEW LISTING CODE LAUNCHIn Q4 2015, GSX will expand its offering of listing services to include the listing of ETIs. GSX will deliver a GSX List-ing Code for Debt, Derivatives, and Asset Backed Securities, which complies with the current applicable legislation in Gi-braltar for asset backed, debt and derivative securities.

CONCLUSIONGSX has identified a compelling business opportunity for Gibraltar to exploit its unique positioning and become a leading securitisation centre within the EU.

The successful introduction of ETIs and asset-backed se-curities will trigger the development of an alternative, mod-ern financial market for Gibraltar, which has a sound politi-cal, economic, and regulatory framework, with an attractive market and tax environment. ETIs have a bright future in Gibraltar.

GSX HAS IDENTIFIED A COMPELLING BUSINESS

OPPORTUNITY FOR GIBRALTAR TO EXPLOIT

ITS UNIQUE POSITIONING AND BECOME A LEADING SECURITISATION CENTRE

WITHIN THE EU

”

Why fly 10 hours when you can fly 2?

2 0 H F M W E E K . CO M

G I B R A L T A R 2 0 1 6

HFMWeek (HFM): What do you see as the most im-portant factors promoting growth in Gibraltar’s fund industry?Moe Cohen (MC): Gibraltar is the newest of a number of European jurisdictions that has grown signifi cantly over the last few years. It is very resilient, which has prov-en itself to also be very competitive in a number ways. In 2005, James Lasry, a prominent fund lawyer in Gibral-tar, and I went to the government and off ered the idea of a new industry – the fund industry. Th e government embraced this idea and within a year we had legislation in place, creating the foundation for what we now know as experienced investor funds. We had looked at a number of European and global jurisdictions and picked the best fund product for the European en-vironment. Th is is the origin of the experienced investor fund.

Th e main benefi ts of an experi-enced investor fund are:

• Fastest to market: As long as the fund has been approved by the licensed parties, including fund administrators, directors and lawyers, the fund can be-gin to trade within 10 days.

Th is is a big advantage com-mercially. If there is an oppor-tunity in private equity, securi-ties and instruments markets, time is of the essence. Being fast to market for a recognised fund is very important.

• Gibraltar’s regulator is very competent and internation-ally recognised for its ability to provide guidance on any issues throughout the life-time of a fund.

Th is also means that if you have any queries, you do not have to wait a long time to get them resolved. Th e accessibility of the regula-tor and the two-way relationship one is able to have with the latt er, are practically very advantageous.

• From a competitive pricing perspective: Gibraltar is in a very strong position. An example of how we – Nexus Fund Administration – have benefi ted in this respect, can be seen through a BVI/Cayman struc-

ture, which was being administered and audited in Dublin. We were able to change the administrator to Nexus while keeping the existing auditor, which was a Big Four Firm. We were able to reduce costs with regard to professional fees by approximately 40%. Th is gives you an indication of how Gibraltar pricing diff ers from other jurisdictions.

HFM: How is Gibraltar ensuring continued growth in its fund industry?MC: Gibraltar is a growing European fund jurisdiction building on its number of assets and industry players, continuing to command an excellent international repu-tation. Over the course of time we will see Gibraltar con-

tinuing to expand its position in the funds industry, particularly with the introduction of AIFMD.

A number of things are currently being done to ensure growth con-tinues in Gibraltar. First, we are ob-viously maintaining the advantages that I previously mentioned, which have enabled the industry to initial-ly grow exponentially.

Th ere is signifi cant marketing being undertaken by the Gibraltar government in conjunction with the industry. Th is has involved un-dertaking diff erent conferences in diff erent parts of the world, includ-ing conferences based in Gibraltar, where we have invited key players from the international market to come and hear about the benefi ts of the city. Th is has created quite a bit of att raction and truly helped to en-sure Gibraltar is always on the map.

Gibraltar has also effi ciently im-plemented the AIFMD legislation.

Gibraltar therefore off ers, where relevant, AIFMD solu-tions to a number of diff erent funds from a worldwide perspective. Th e fact Gibraltar has not ‘gold-plated’ the legislation and the rules are very similar to that of the UK, enables Gibraltar to become very competitive in the market in terms of legislation. It provides an avenue for AIFMD funds to set up in Gibraltar. In addition, the services available through the fund industry in Gibraltar,

MOE COHEN, CEO OF BENADY COHEN & CO GROUP, CHARTERED ACCOUNTANTS INCLUDING NEXUS FUND ADMINISTRATION, TALKS TO HFMWEEK ABOUT THE GROWTH OF GIBRALTAR’S FUND INDUSTRY AND WHAT THE JURISDICTION HAS TO OFFER FUNDS

CONTINUED GROWTH

GIBRALTAR IS A GROWING EUROPEAN FUND

JURISDICTION BUILDING ON ITS NUMBER OF

ASSETS AND INDUSTRY PLAYERS, CONTINUING TO COMMAND AN EXCELLENT

INTERNATIONAL REPUTATION

”

Moe Cohen is a founder and CEO of Benady Cohen & Co Group, Chartered Accountants, which includes Nexus Fund Administration Services. The group is also a member of Nexia International. Moe is a member of the executive board of GFIA and GSA and advised the Gibraltar government on the initial establishment of regulated funds in Gibraltar in 2004.

A C C O U N T I N G

H F M W E E K . CO M 21

with regard to AIFMD, ensure there can be contin-ued growth in this respect.

This general fund marketing as well as the ability to latch-on to the latest European legislation, will al-low Gibraltar to continue to successfully grow this industry.

HFM: What are the greatest challenges currently faced by your fund clients? How does Nexus Fund Administration help its clients to over-come these challenges? MC: Fund clients currently want a complete one-stop-shop solution. Therefore they want their pro-fessional service providers to be as well-informed as they can be on different aspects of their fund and its workings.

Benady Cohen & Co Group are chartered ac-countants and provide audit, tax advisory and fund administration services. We are not necessarily able to provide certain services to the same client, due to conflict of interest rules. However, when it comes to the audit of a fund we administer, we have the knowledge base to be able to prepare efficient

and effective audit files for the auditor in a pro-fessional manner. The audit can therefore go through the all process very smoothly.

Similarly, when we have Fatca considerations, we use the expertise of our tax department. We are able to provide funds with comprehensive services solution.

On the other hand, if we are undertaking the audit of funds as a result of our fund administra-tion knowledge, we are able to do so in a more effective way. The strong levels of experience across the different areas of our business adds value to the services we provide to clients.

We have recently obtained a private equity, AIFMD depository licence. In a sense, this is an extension of the audit work that we undertake for our fund clients and it encompasses some fund administration work that we do. We are also looking to obtain an AIFMD manager licence, which will also serve as an extension of our ex-pertise and serve to strengthen the services the Group provides to our current and future fund clients.

FUND CLIENTS CURRENTLY WANT A COMPLETE ONE-STOP-SHOP SOLUTION.

THEREFORE THEY WANT THEIR PROFESSIONAL

SERVICE PROVIDERS TO BE AS WELL INFORMED AS THEY CAN BE ON

DIFFERENT ASPECTS OF THEIR FUND AND ITS

WORKINGS

”

2 2 H F M W E E K . CO M

S E R V I C E D I R E C TO R YG I B R A L T A R 2 0 1 6

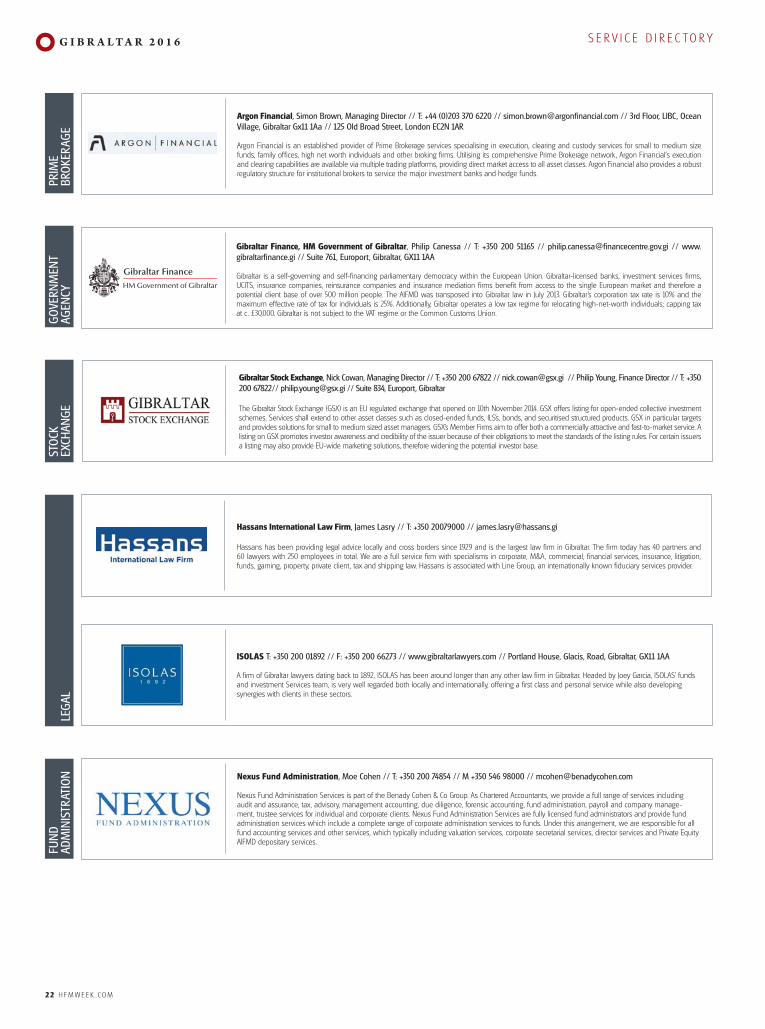

Nexus Fund Administration, Moe Cohen // T: +350 200 74854 // M +350 546 98000 // [email protected]

Nexus Fund Administration Services is part of the Benady Cohen & Co Group. As Chartered Accountants, we provide a full range of services including audit and assurance, tax, advisory, management accounting, due diligence, forensic accounting, fund administration, payroll and company manage-ment, trustee services for individual and corporate clients. Nexus Fund Administration Services are fully licensed fund administrators and provide fund administration services which include a complete range of corporate administration services to funds. Under this arrangement, we are responsible for all fund accounting services and other services, which typically including valuation services, corporate secretarial services, director services and Private Equity AIFMD depositary services.

ISOLAS T: +350 200 01892 // F: +350 200 66273 // www.gibraltarlawyers.com // Portland House, Glacis, Road, Gibraltar, GX11 1AA

A firm of Gibraltar lawyers dating back to 1892, ISOLAS has been around longer than any other law firm in Gibraltar. Headed by Joey Garcia, ISOLAS’ funds and investment Services team, is very well regarded both locally and internationally, offering a first class and personal service while also developing synergies with clients in these sectors.

PRIM

E BR

OKER

AGE

GOVE

RNM

ENT

AGEN

CYST

OCK

EXCH

ANGE

LEGA

L FU

ND

ADM

INIS

TRAT

ION

Gibraltar Finance, HM Government of Gibraltar, Philip Canessa // T: +350 200 51165 // [email protected] // www.gibraltarfinance.gi // Suite 761, Europort, Gibraltar, GX11 1AA

Gibraltar is a self-governing and self-financing parliamentary democracy within the European Union. Gibraltar-licensed banks, investment services firms, UCITS, insurance companies, reinsurance companies and insurance mediation firms benefit from access to the single European market and therefore a potential client base of over 500 million people. The AIFMD was transposed into Gibraltar law in July 2013. Gibraltar’s corporation tax rate is 10% and the maximum effective rate of tax for individuals is 25%. Additionally, Gibraltar operates a low tax regime for relocating high-net-worth individuals; capping tax at c. £30,000. Gibraltar is not subject to the VAT regime or the Common Customs Union.

Argon Financial, Simon Brown, Managing Director // T: +44 (0)203 370 6220 // [email protected] // 3rd Floor, LIBC, Ocean Village, Gibraltar Gx11 1Aa // 125 Old Broad Street, London EC2N 1AR

Argon Financial is an established provider of Prime Brokerage services specialising in execution, clearing and custody services for small to medium size funds, family offices, high net worth individuals and other broking firms. Utilising its comprehensive Prime Brokerage network, Argon Financial's execution and clearing capabilities are available via multiple trading platforms, providing direct market access to all asset classes. Argon Financial also provides a robust regulatory structure for institutional brokers to service the major investment banks and hedge funds.

Gibraltar Stock Exchange, Nick Cowan, Managing Director // T: +350 200 67822 // [email protected] // Philip Young, Finance Director // T: +350 200 67822// [email protected] // Suite 834, Europort, Gibraltar The Gibraltar Stock Exchange (GSX) is an EU regulated exchange that opened on 10th November 2014. GSX offers listing for open-ended collective investment schemes. Services shall extend to other asset classes such as closed-ended funds, ILS’s, bonds, and securitised structured products. GSX in particular targets and provides solutions for small to medium sized asset managers. GSX’s Member Firms aim to offer both a commercially attractive and fast-to-market service. A listing on GSX promotes investor awareness and credibility of the issuer because of their obligations to meet the standards of the listing rules. For certain issuers a listing may also provide EU-wide marketing solutions, therefore widening the potential investor base.

Hassans International Law Firm, James Lasry // T: +350 20079000 // [email protected]

Hassans has been providing legal advice locally and cross borders since 1929 and is the largest law firm in Gibraltar. The firm today has 40 partners and 60 lawyers with 250 employees in total. We are a full service firm with specialisms in corporate, M&A, commercial, financial services, insurance, litigation, funds, gaming, property, private client, tax and shipping law. Hassans is associated with Line Group, an internationally known fiduciary services provider.

GIBRALTAR: THE SPECIALIST FINANCIAL JURISDICTION OF CHOICE IN

THE EU

GFIA members include Funds, Fund Administrators, Stockbrokers, Investment Managers, Audit Firms, Law Firms,

For more information please contact GFIA Executive Coordinator by e-mail on

Established EU Jurisdictionfor a wide range of investment funds

Fully AIFMD compliant, with passportingright across the EU

Specialist European master feeder fundsolutions

Unique asset manager offering, combiningquality of life with fiscal and legislativestability

Professional and internationally recognized fund and investment expertise

Experienced Investor Funds (EIF)

An EIF is an authorised collective investment scheme exclusively for investment by experienced investors and is designed to invest in a wide range of traditional or alternative asset classes.

Gibraltar Finance is the growing success story in Europe for investment funds and investment managers. It offers robust fund legislation, a favourable fiscal regime, an EU framework, efficient regulation, the flexibility of a small jurisdiction and quality infrastructure.

As an EU domicile, Gibraltar Finance provides investors

thereby enabling passporting throughout the member states of the EU. Gibraltar also presents both political and economic

international standards and full employment rights for EU/EEA and Swiss citizens.

Asset Management

Management firms can establish themselves as a firm under

2006, or the Financial Services (Alternative Investment Fund

GATEWAY TO THE EUROPEAN UNION SINGLE MARKET

For more information visit the Gibraltar Finance website:

www.gibraltarfinance.gi

One of the attractions of Gibraltar as a fund domicile is that no regulatory approval is required before an EIF can begin to raise capital and commence its investment activities. An EIF may be launched based on a legal opinion that confirms that the EIF has met all legal and structural requirements for its operations, and provided that the fund’s documentation is submitted to the