henrique de campos meirelles brazilian-american chamber of commerce september 2010 addressing new...

TRANSCRIPT

Henrique de Campos Meirelles

Brazilian-American Chamber of Commerce

September 2010

Addressing New Basel Regulations, their Effects on Global Banking, and the

Impact on the Brazilian Financial System

2

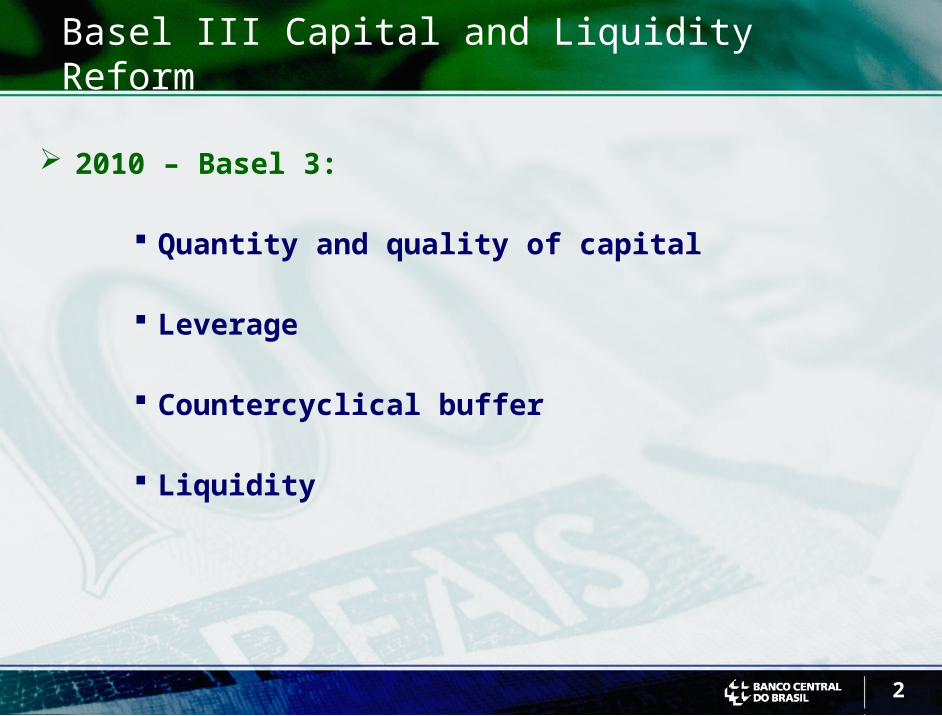

2010 – Basel 3:

Quantity and quality of capital

Leverage

Countercyclical buffer

Liquidity

Basel III Capital and Liquidity Reform

3

Conservation Buffer

- Common Equity (2.5%)

Minimum Requirement

- Capital (8%)

- Tier 1 Capital (6%)

- Common Equity (4.5%)

Countercyclical Buffer - Common Equity (0-2.5%)

Basel III Capital and Liquidity Reform

4

Basel III Capital and Liquidity Reform

Sources: BIS and Central Bank of Brazil

minimumrequirement

8%

current minimum

requirement11%

countercyclical buffer

current level In Brazil

conservation buffer

0

3

6

9

12

15

18

Basel Brazil

% o

f G

DP

5

Transition period reduces adjustment costs

In the long run, benefits outweight costs

Reform reduces the probability of financial crisis

Possible increase in the cost of financial intermediation

are more than offset by the economic benefits of

ensuring more financial stability

Basel III Economic Impact

6

Brazil in 2003

60% of total sovereign debt denominated in dollars

IMF debtor country

High public debt to GDP ratio: 60.6%

Policy rate at 25%

Rising inflation

High country risk premiums and sovereign debt rated as speculative grade

Unemployment rate at 12%

Minimum wage at US$ 60

7

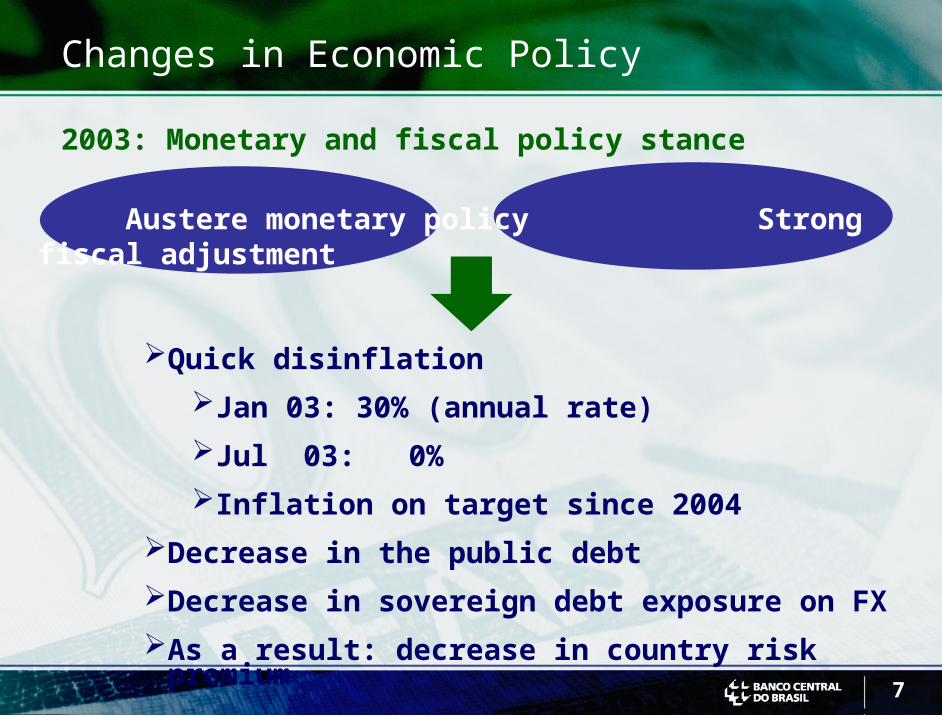

Quick disinflation

Jan 03: 30% (annual rate)

Jul 03: 0%

Inflation on target since 2004

Decrease in the public debt

Decrease in sovereign debt exposure on FX

As a result: decrease in country risk premium

Changes in Economic Policy

2003: Monetary and fiscal policy stance

Austere monetary policy Strong fiscal adjustment

8

Public Sector Net Debt%

of

GD

P

Sources: Central Bank of Brazil

60.6

54.9

50.648.2

47.045.1

42.7

38.4

42.840.6

30

35

40

45

50

55

60

Dec02

Dec03

Dec04

Dec05

Dec06

Dec07

Aug08

Dec08

Dec09

Dec10

marketconsensus

9

Floating Exchange Rate Regime and Build Up of International Reserves

Source: Central Bank of Brazil

international reserves allow for a safe fluctuation of the exchange rate Sep 21st

271.4

Aug 08205.1

0

50

100

150

200

250

Jan02

Jan03

Jan04

Jan05

Jan06

Jan07

Jan08

Jan09

Jan10

US

D b

illi

on

10

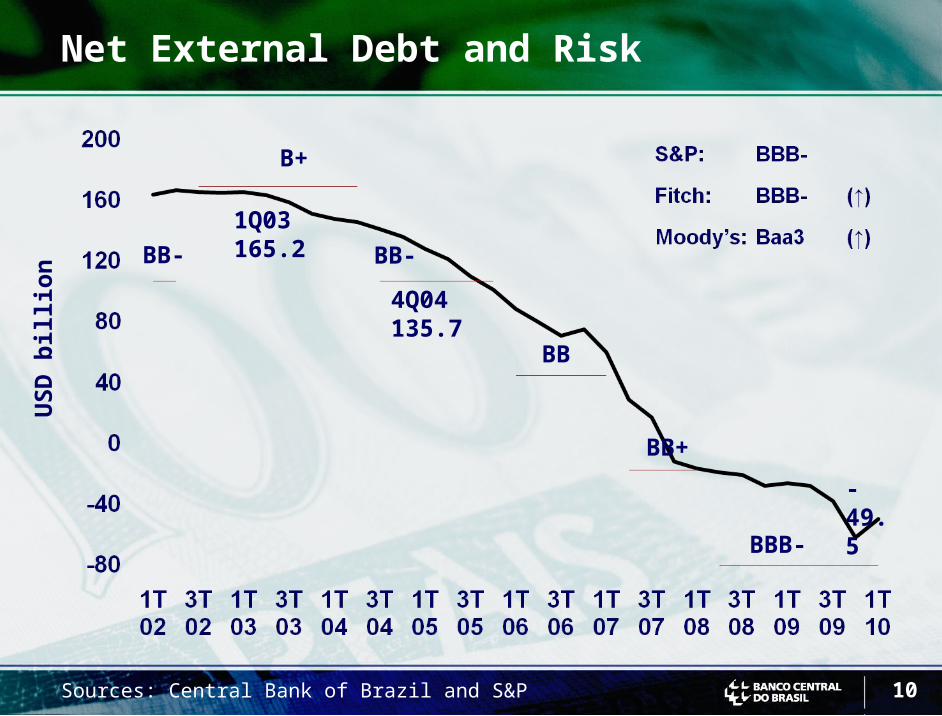

Net External Debt and RiskU

SD

bil

lio

n

1Q03165.2

4Q04135.7

-49.5

BBB-

BB+

BB

BB-

B+

BB-

Sources: Central Bank of Brazil and S&P

11

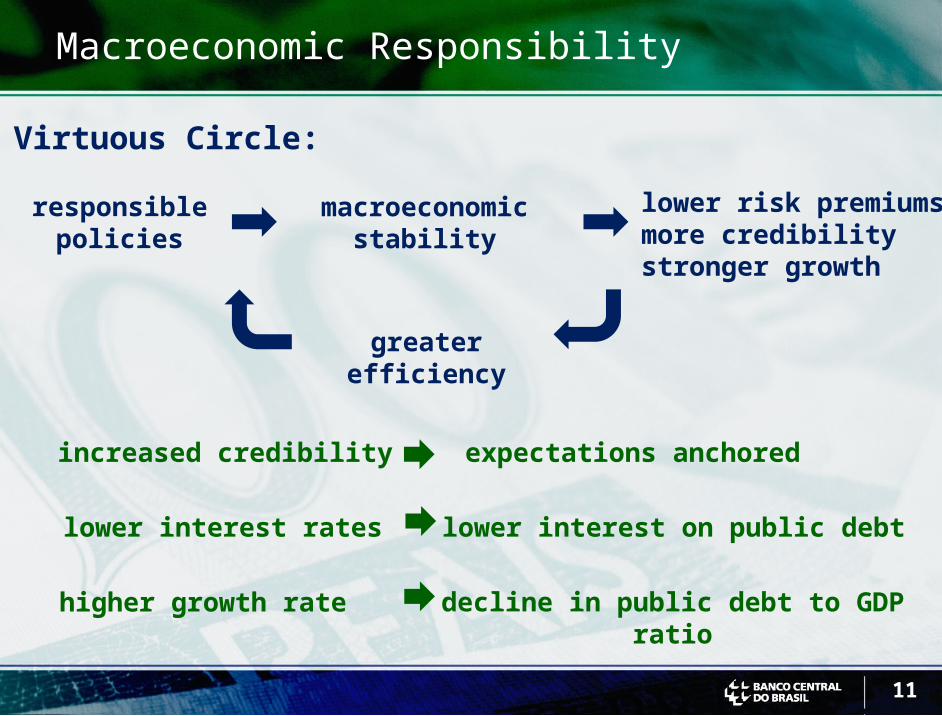

increased credibility expectations anchored

macroeconomicstability

responsiblepolicies

lower risk premiumsmore credibilitystronger growth

greater efficiency

lower interest rates lower interest on public debt

higher growth rate decline in public debt to GDPratio

Virtuous Circle:

Macroeconomic Responsibility

12

Macroeconomic Policy Framework

Macroeconomic fundamentals of inflation targeting, fiscal responsibility, exchange rate flexibility,

combined with

Adequate prudential policy and solid bank supervision,

resulted in

capacity to absorb internal and external shocks

macroeconomic and financial stability

sustainable growth

investment growth

credit and capital market development

13

100

290

480

670

860

1050

1240

1430

1620

1810

2000

90

100

110

120

130

140

150

160

170

1Q 00

1Q 01

1Q 02

1Q 03

1Q 04

1Q 05

1Q 06

1Q 07

1Q 08

1Q 09

3Q 10

investmentsGFCF (left)

country risk - Brasil t-2 (right)

1995

= 1

00

bas

is p

oin

ts

Investments x Country Risk

2Q 10

Sources: IBGE and JPMorgan

14

Credit – Outstanding Balances

25.7

46.2

5

10

15

20

25

30

35

40

45

50

0

200

400

600

800

1,000

1,200

1,400

1,600

Jan02

Jan03

Jan04

Jan05

Jan06

Jan07

Jan08

Jan09

Aug10

R$

bil

lio

n

% o

f G

DP

consistent growth throughout the period

Source: Central Bank of Brazil

15Source: CVM (Brazilian Securities Comission) *12 months to August

Capital market – primary issues

0

20

40

60

80

100

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010*

Stocks Commercial papers Others

R$

bil

lio

n

16

Net Foreign Direct Investment

market consensus*

US

D b

illi

on

2007-09 35.2

2002-0615.7

0

10

20

30

40

50

02 03 04 05 06 07 08 09 10 11 12 13 14

2010-1437.8

Source: Central Bank of Brazil (market consensus) *17/9/2010

17

0 20 40 60 80 100

Spain

Peru

South Africa

Chile

Japan

Canada

Malaysia

Australia

France

Poland

Tailand

Vietnan

Indonesia

German

United Kingdom

Mexico

Russia

United States

Brazil

India

China

3rd preferred host economy for FDI for the 2010-12 period

Source: UNCTAD

18

as a percentage of the gross external liabilities

Brazilian External Liabilities

2001 2010*

FDI37%

Stocks (domestic and foreign)

31.3%

Fixed income18.6%

FDI32.8%

Stocks (domestic and foreign)

9.9%

Fixed income 30.9%

Others13.2%

Others26.4%

Source: Central Bank of Brazil*August

19

50

100

150

200

250

80 85 90 95 00 05 10

1980-8925.5

1990-9942.7

2000-09111.1

2010-14229.6*

Source: Central Bank of Brazil (market consensus) *17.9.2010

ExportsU

SD

bil

lio

n

14

20

Exports’ Diversification

Fonte: Banco Central * até Julho

%

9.9

21.4

23.7

27.8

9

12

15

18

21

24

27

30

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010*

USAEurope

Latin America

Asia

21

Price Stability and Real Payroll Growth

Source: Central Bank of Brazil

% c

han

ge

in 1

2 m

on

ths

Jan

03

= 1

00

95

100

105

110

115

120

125

130

135

-

2

4

6

8

10

12

14

16

18

Jan03

Jan04

Jan05

Jan06

Jan07

Jan08

Jan09

Jul10

IPCA

real payroll

stability generates increasing well-being

22

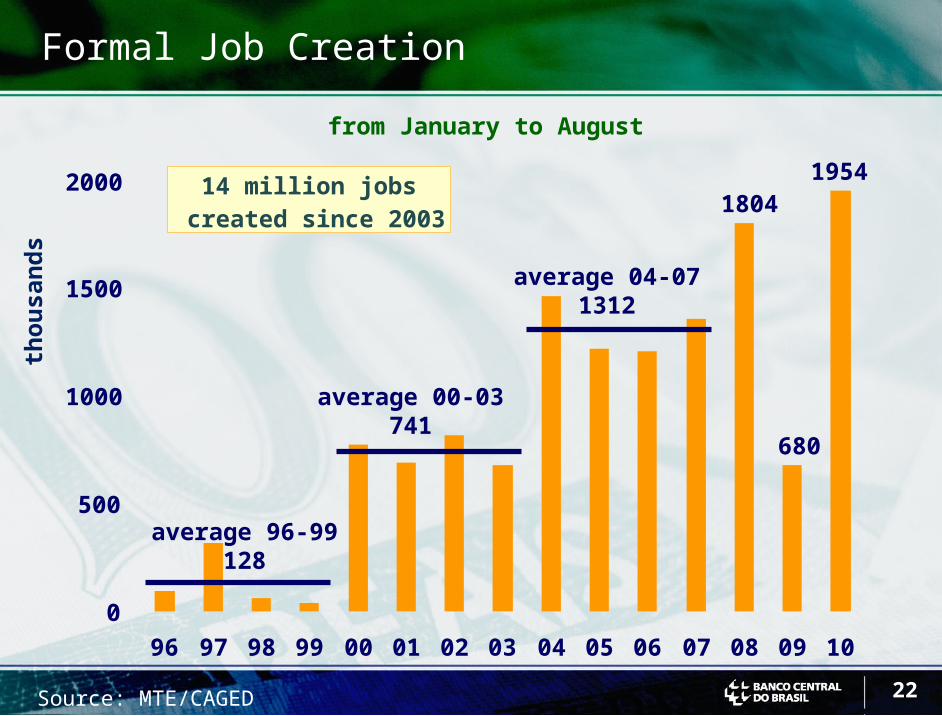

Formal Job Creation

Source: MTE/CAGED

1804

680

1954

average 96-99128

average 00-03741

average 04-071312

0

500

1000

1500

2000

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

14 million jobs created since 2003

from January to August

tho

usa

nd

s

23

Unemployment in Brazil

seasonally adjusted

Source: IBGE

6.737

8

9

10

11

12

13

Jan03

Jan04

Jan05

Jan06

Jan07

Jan08

Jan09

Ago10

%

24

relatively dynamic labor market

Source: Bloomberg

Unemployment Rate

25.320.3

18.316.4

13.613.3

11.811.4

1110.810.7

10.510

9.69.3

8.98.78.58.428.38.17.97.87.67.4

6.73

South AfricaSpain

LithuaniaCroaciaIreland

ColombiaGreecePoland

HungaryPortugal

IndiaTurkey

Euro zoneUnited States

FranceBelgium

VenezuelaFinland

ItalyChile

CanadaArgentina

United KingdomGermany

SwedenBrazil

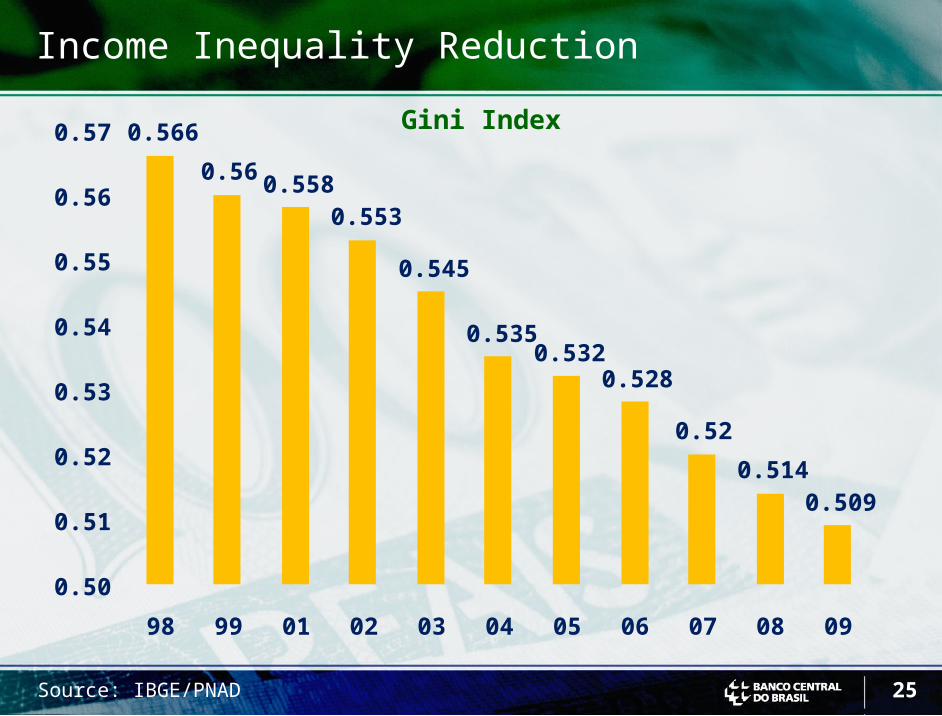

25

0.566

0.56 0.5580.553

0.545

0.5350.532

0.528

0.52

0.5140.509

0.50

0.51

0.52

0.53

0.54

0.55

0.56

0.57

98 99 01 02 03 04 05 06 07 08 09

Source: IBGE/PNAD

Gini Index

Income Inequality Reduction

26

From 2003 to 2009

35.7 million people have entered the middle class

20.5 million have crossed the poverty line upwards

2010-2014 forecast for the current trend

36.0 million more will enter the middle class

14.5 million more will come out of poverty

Family Grant Program (Bolsa Família): reduction of people

in extreme poverty from 12% to the 4% level

Middle Class Growth andPoverty Reduction

Source: FGV-CPS

27

Lower Level Income%

of

po

pu

lati

on

Source: CPS/FGV

28.1

25.4

22.8

19.318.3

16.015.3

10

15

20

25

30

2003 2004 2005 2006 2007 2008 2009

28

Social Mobility

4929 16

47

4440

6695

113

1320 31

0

50

100

150

200

2003 2009 2014*

A/B C D E

mil

lio

ns

of

peo

ple

+44.1% +19.0%

Source: Finance Ministry; * estimated

29Sources: FMI (WEO April 2010) and Central Bank of Brazil

2007 2008 2009 2010

GD

P r

eal

gro

wth

%

compared to other emerging markets

Performance Before and After the Crisis

5.7

3.6

-2.2 (*)

4.3 (*)

6.1

5.2

-0.2

7.3 (**)

EME ex. Brazil,India and China

Brazil

30

GDP Growth

Sources: IBGE and Central Bank of Brazil

annual real growth rate

-0.2%

7.3%

-1

0

1

2

3

4

5

6

7

99 00 01 02 03 04 05 06 07 08 09 10

2.1%(1999-2002)

3.3%(2003-2005)

5.1%(2006-2008)

31

Agenda for the Future

Level of Domestic Saving

Quality of Public Expenditures

Investment Rate and Infra-Structure

Education

Review and Simplification of the Tax System

Legal Environment more favorable to Business

Incentive to Long Term Investment

32

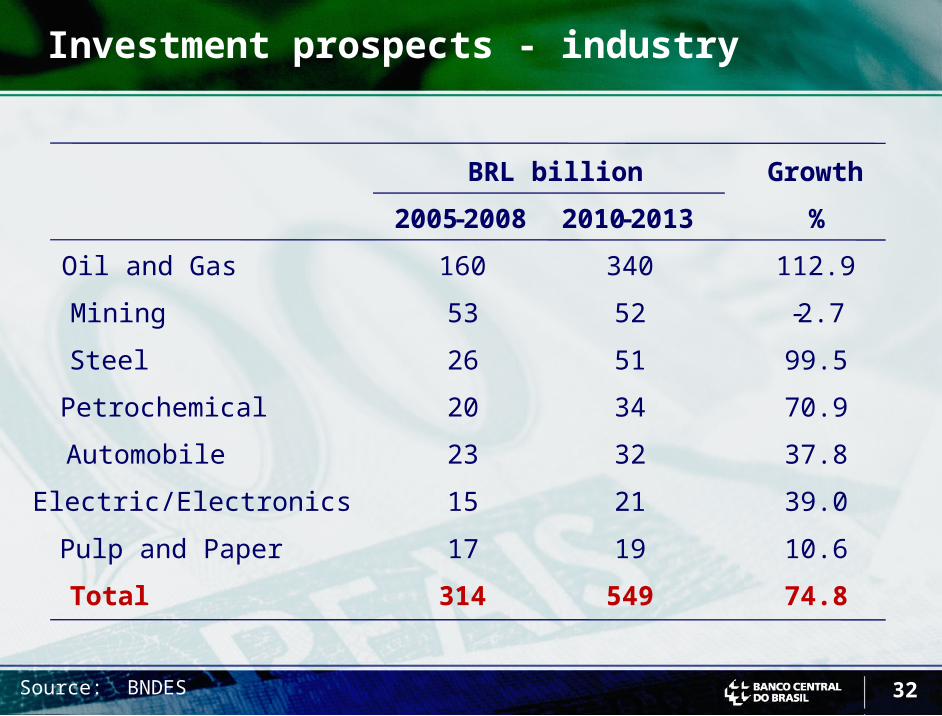

Investment prospects - industry

Source: BNDES

2005-2008 2010-2013 %

Oil and Gas 160 340 112.9

Mining 53 52 -2.7

Steel 26 51 99.5

Petrochemical 20 34 70.9

Automobile 23 32 37.8

Electric/Electronics 15 21 39.0

Pulp and Paper 17 19 10.6

Total 314 549 74.8

BRL billion Growth

33

Investment prospects - infrastructure

Source: BNDES

2005-2008 2010-2013 %

Electricity 67 98 45.2

Telecommunication 66 67 2.1

Sanitation 22 39 76.5

Railways 19 56 195.3

Highways 21 36 73.0

Ports 5 15 217.9

Total 199 310 55.6

BRL billion Growth

Henrique de Campos Meirelles

September 2010