hedging with forward/ futures contracts chap 22 & chap 24 1

TRANSCRIPT

HEDGING WITH FORWARD/ FUTURES CONTRACTS

Chap 22 & Chap 24

1

Lecture Outline

Purpose: Introduce Forwards & Futures contracts and show how they can be used to hedge.

Introduction to Forwards and Futures

Three types of prices: Forward/Future, Spot & Delivery

Payoff of Forward/Future contract

Hedging with Forwards/Futures Micro Hedge Macro Hedge

2

Forward/Future Contract a Primer

Forward & future contracts: are agreements, made at t=0, obligating parties to exchange some pre-specified amount of an asset at a pre-specified price some time in the future.

Example: http://www.cmegroup.comIf your company is a large coffee buyer (Starbucks) you may want to hedge against movements in the price of coffee – lock in a price today for the purchase of coffee in 1.5 years

Coffee Forward Prices

$1.87/lb

$2.75/lb

Contract payoff$0.88

The price that the coffee buyer can lock in at any time is the forward price

The price that the coffee buyer locks-in is the

delivery price

Just an agreement – no exchange of money

3

$2.75/lb

1.87/lb

-$0.88/lb $1.87/lb

Introduction to Forwards & Futures

4

Forward/Future Contract A Primer

Differences between Forwards and Futures

Forward contracts are custom Futures contracts are standard

2. Forwards settled at maturity

1. Trade on OTC dealer markets

3. More exposed to counterparty default risk

4. Almost always delivered

2. Futures are marked-to-market

1. Trade on exchanges

3. Exchange guarantees performance (there is much less counter party default risk)

4. Almost never delivered

Economic Hedgers Speculators

Who Trades in each market

Speculators or Hedgers?

Every day the change in the value of the forward contract is added or

subtracted from the investors account

5

6

Forward/ Future Price, Spot Price & Delivery Price

Prices You Need to Keep Straight

Spot Price (S0): Price of the underlying asset (coffee)

Forward/Futures Price (Ft): The current price at which you can enter a forward contract – varies over time!

Delivery Price: The transaction price specified in the contract. Equal to the forward/futures price when the contract is entered Remains constant over the life of the contract. (Locked-in)

ktTot krSF )()/1(

Ft = future price ; S0 = underlying spot price k = compounding periods per year; r = risk-free rate; (T-t) = number of years to delivery

7

S0 =Current Market Price of CoffeeCurrent Market Price of Ford StockCurrent Market Price of a 10-year Treasury

Note: this is for the special case where the underlying asset does not make payments for the life of the contract. That is, it does not work for coupon bonds dividend paying stocks …

Spot Price

8

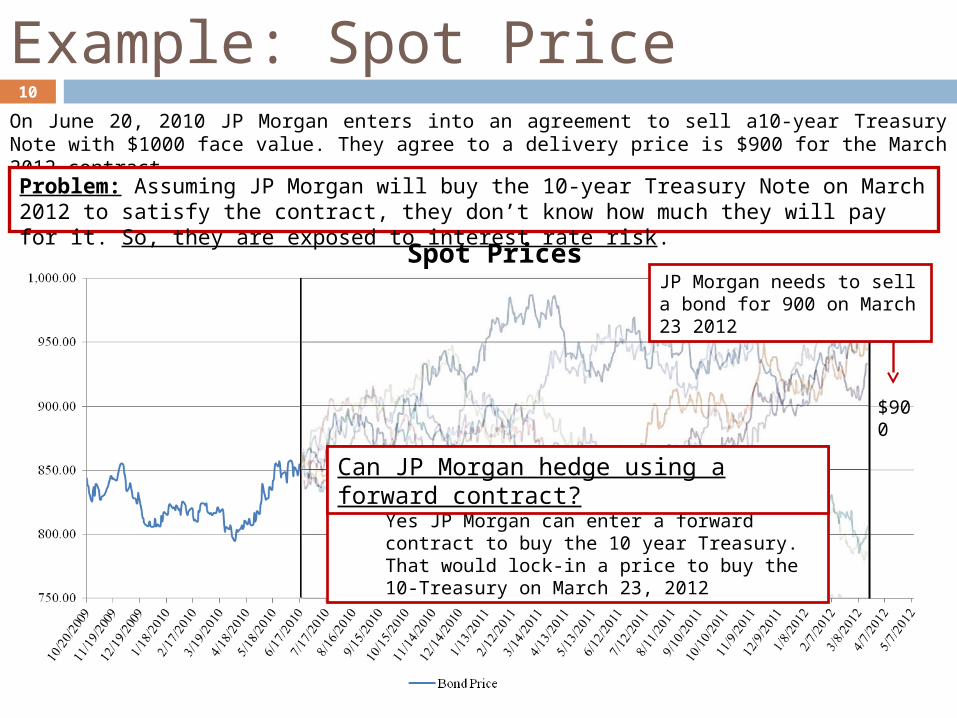

Example: Spot Price On June 20, 2010 JP Morgan enters into an agreement to sell a10-year Treasury note with $1000 face value. They agree to a delivery price is $900 for the March 2012 contract.

9

Price of 10-year Treasury

Bonds are expensive

Bonds are cheap

Un

certainty

On June 20, 2010 JP Morgan agrees to sell a Treasury Bond for $900 on March 23,

2012

On March 23, 2012 JP Morgan needs to deliver a 10-year Treasury Note

SetupIs JP Morgan exposed to risk?

Spot Prices

Problem: Assuming JP Morgan will buy the 10-year Treasury Note on March 2012 to satisfy the contract, they don’t know how much they will pay for it. So, they are exposed to interest rate risk.

Example: Spot Price On June 20, 2010 JP Morgan enters into an agreement to sell a10-year Treasury Note with $1000 face value. They agree to a delivery price is $900 for the March 2012 contract.

10

Can JP Morgan hedge using a forward contract?Yes JP Morgan can enter a forward contract to buy the 10 year Treasury. That would lock-in a price to buy the 10-Treasury on March 23, 2012

$900

Can JP Morgan hedge using a forward contract?

Spot Prices

Problem: Assuming JP Morgan will buy the 10-year Treasury Note on March 2012 to satisfy the contract, they don’t know how much they will pay for it. So, they are exposed to interest rate risk.

JP Morgan needs to sell a bond for 900 on March 23 2012

Example: Spot Price

Main Point:Spot prices vary through time which exposes banks/investors to risk (interest rate risk, price risk, FX risk … )

Forward/Futures contracts can be used to hedge that risk

How?

11

12

Forward/Future Price

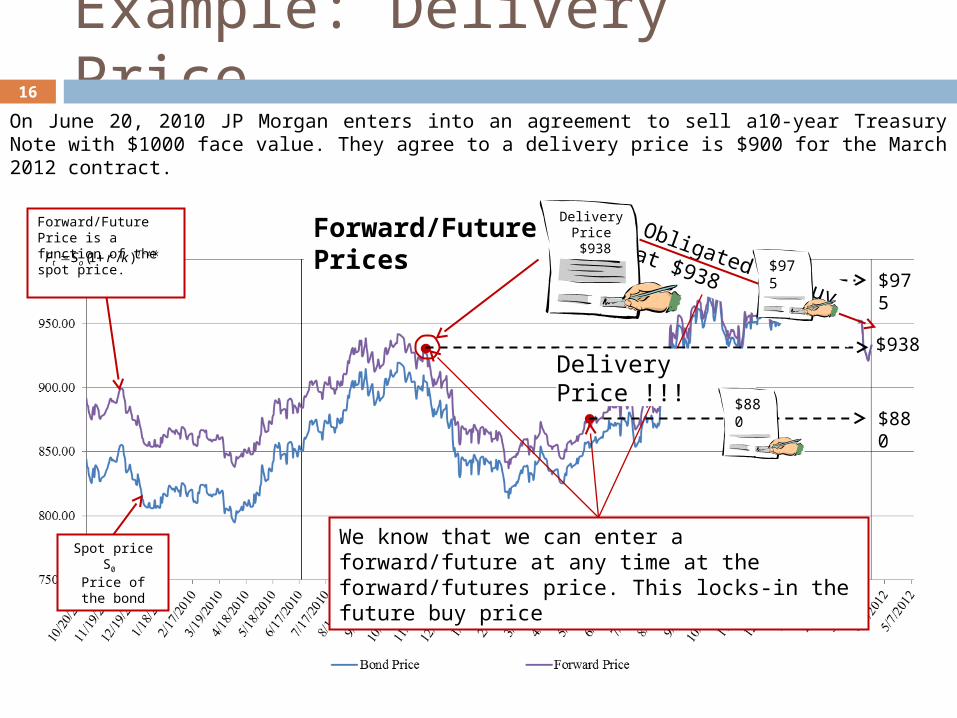

Example: Forward/Futures Prices On June 20, 2010 JP Morgan enters into an agreement to sell a10-year Treasury Note with $1000 face value. They agree to a delivery price is $900 for the March 2012 contract.

13

Spot price S0 Price of the bond

Forward/Future Price is a function of the spot price.ktT

ot krSF )()/1(

Forward/Future & Spot Prices

At any point in time I can enter a forward/futures contract at the forward/futures price

Example: Forward/Futures Price

Main Point:The Forward/Futures price is a function of the spot price and varies through time.

At any point in time you can enter a forward/futures at the current forward/futures price

14

15

Delivery Price

Example: Delivery PriceOn June 20, 2010 JP Morgan enters into an agreement to sell a10-year Treasury Note with $1000 face value. They agree to a delivery price is $900 for the March 2012 contract.

16

Spot price S0 Price of the bond

Forward/Future Price is a function of the spot price.

ktTot krSF )()/1(

Forward/Future & Spot Prices

We know that we can enter a forward/future at any time at the forward/futures price. This locks-in the future buy price

$938

$880

$975

Obligated to buy at $938

Delivery Price $938

Delivery Price !!!

$880

$975

Example: Delivery Price

Main Point:The delivery price is specified in the contract. Once you enter the contract the delivery price does not change.

This is the price you agree to buy or sell at in the future

17

Hedging with a ForwardBasic Idea

18

Example: Bring it all togetherOn June 20, 2010 JP Morgan enters into an agreement to sell a 10-year Treasury note with $1000 face value. They agree to a delivery price is $900 for the March 23, 2012 contract.

19

Spot price S0 Price of the bond

Forward/Future Price is a function of the spot price.

ktTot krSF )()/1(

Forward/Future & Spot Prices

Agreed to sell T-note for $900

Enter forward contract to buy a T-Note at the delivery price

-$890$900

$10$890

20

Forward/Futures Payoff

Payoff of a forward/futures contract

21

Payoff – Refers to the cash flow that occurs at maturity for a contract with cash settlement.

Example: Forward/Future Payoff

JP Morgan entered a forward contract to buy a Treasury Note on March 23, 2012 with a delivery price of $890. They have locked-in a buy price. The question is: what happens at maturity?

22

Forward/Future Price(March 2012 contract)

ktTot krSF )()/1(

Forward/Future & Spot Prices

$933

Payoff

ONLY CONSIDER THE FORWARD TO BUY AT $890:

- $890Delivery Price

If the contract is financial (cash) settled, what does JP Morgan receive at maturity?

1. Buy at the delivery price2. Immediately sell in the market at the

current spot price (also the forward price)

$43

Example: Forward/Future Payoff

JP Morgan entered a forward contract to buy a Treasury Note on March 23, 2012 with a delivery price of $890. They have locked-in a buy price. The question is: what happens at maturity?

23

- $890

Forward/Future Price(March 2012 contract)

ktTot krSF )()/1(

Forward/Future & Spot Prices

$933

Payoff

ONLY CONSIDER THE FORWARD TO BUY AT $890:

Delivery Price

$43

$43

Example: Forward/Future Payoff 24

Take Away•The payoff of the forward/futures contract is difference between the price of the underlying asset (bond) at maturity and the delivery price that was locked in the on the contract

Payoff = (S – FD) - long positionPayoff = (FD – S) - short position

Question: Will the Forward/Future contract payoff always be positive?

Question: Can you calculate the payoff on a forward/future prior to maturity?

25

Hedging with Forward/Futures Contracts

Hedging 26

1.Find the hedging position long or short forward

2.Find the number of contracts

3.Show that the position is hedged

Long & Short Positions27

Underlying Asset: Long: you own the asset Short: you owe the asset

Forward Contract Long: you have agreed to buy the asset in the future at a pre- specified price (locked-in a price to buy)

Short: you have agreed to sell the asset in the future at a pre- specified price (locked-in a price to sell)

Example:Stock → If you are long the stock you own it

Example:Stock → If you are short the stock you have borrowed # shares from a dealer and sold them. So, you owe # shares back to the dealer

1. Finding the Hedging Position28

Investors

• Investors have some obligation that exposes them to risk (price fluctuations) ie. their position in the underlying asset (Long or Short).

• They want to offset this exposure this exposure by taking the opposite position in the forward contract. This locks in a payment in the future

T-Bill

Underlying

Basic Idea1. Find the position in the underlying asset2. Take the opposite position in the futures

3. LONG vs. SHORT – underlying• LONG: Better off (happy) when the price

goes up • SHORT: Better off (happy) when the price

goes down

1. Finding the Hedging Position29

Investors

Hedged Position

T-Bill

Underlying

Future Time Period Current Time (t=0)

Are you long or short the T-Bill?

Short

Do go long or short the forward?

Long

Underlying Position

Forward/Futures Position

1. Finding the Hedging Position30

Investors

Hedged Position

T-Bill

Underlying

Future Time Period Current Time (t=0)

Short

Long

Underlying Position

Forward/Futures Position

The object of hedging is to eliminate risk – ie. lock in a future value. That value does not have to be the same as

the present value!!!!!

1. Finding the Hedging Position31

Investors

Hedged Position

T-Bill

Underlying

Future Time Period Current Time (t=0)

Short

Long

Underlying Position

Forward/Futures Position

Goldman Sachs wants to hedge $5M of corporate bonds on its balance sheet.

1. Finding the Hedging Position32

Investors

Hedged Position

T-Bill

Underlying

Future Time Period Current Time (t=0)

Short

Long

Underlying Position

Forward/Futures Position

Goldman Sachs agrees to deliver $5M of corporate bonds in six months – payment on delivery?

1. Finding the Hedging Position33

Investors

Hedged Position

Underlying

Future Time Period Current Time (t=0)

Short

Long

Underlying Position

Forward/Futures Position

Exxon will deliver 5M barrels of oil in 6 months for $55/barrel.

1. Finding the Hedging Position34

Investors

Hedged Position

Underlying

Future Time Period Current Time (t=0)

Short

Long

Underlying Position

Forward/Futures Position

A corn farmer will sell 50M bushels of corn at market price in 3 months.

1. Finding the Hedging Position35

These 3 questions can help determine the hedging position:

1. Does the hedging party own or owe the underlying asset? Answer: own. Then they are long the underlying and need to take a short

position in the forward contract to hedge Answer: owe. Then they are short the underlying and need to take a long

position in the forward contract to hedge

2. Does the hedging party want to lock in a price to buy or sell in the future? Answer: lock-in a price to buy. Then they need to go long the forward Answer: lock-in a price to sell. Then they need to go short the forward

1. Finding the Hedging Position36

These 3 questions can help determine the hedging position:

3. Is the hedging party happy if the price of the underlying asset increases or decreases? Answer: Increases. Then the hedging party is long the underlying asset

and needs to take a short position in the forward contract Answer: Decreases. Then the hedging party is short the underlying and

needs to take a long position in the forward contract

2. Find the number of contracts37

Forward contract: These are custom contracts. The hedging party can specify the exact

notional amount. Therefore, only one contract is needed.

Futures contracts: These are standard contracts with a standard notional amount. To find the number of contracts you must divide the total notional by

the standard contract notional Example: Goldman wants to hedge 10-year Treasury bonds with $5M

face value with a CME contract. The standard contract size is $100,000

contractsN 50000,100

000,000,5

3. Show that the position is hedged 38

Show that no matter what the price of the underlying asset is in the future the hedged portfolio has locked-in a payoff

Underlying position

Forward Payoff

t = 0 t = 6 months

Hedged portfolio

Scenario 1 price Scenario 2 price

Value an asset Value an asset Value an asset

Payoff on Forward/Futures

Payoff on Forward/Futures

Payoff on Forward/Futures

Sum to get hedged payoff

Sum to get hedged payoff

Sum to get hedged payoff

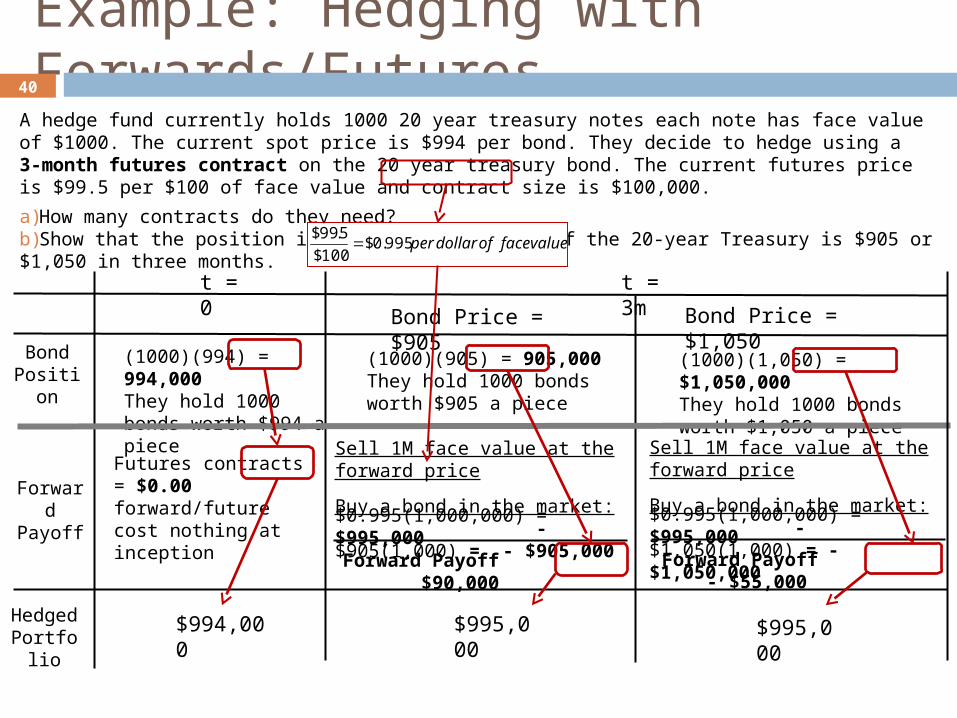

Example: Hedging with Forwards/FuturesA hedge fund currently holds 1000 20 year treasury notes each note has face value of $1000. The current spot price is $994 per bond. They decide to hedge using a 3-month futures contract on the 20 year treasury bond. The current futures price is $99.5 per $100 of face value and contract size is $100,000.

a)How many contracts do they need?b)Show that the position is hedged if the price of the 20-year Treasury is $905 or $1,050 in three months.

39

Step #1: What contract position do they need to hedge their exposure?They own the bonds. So, they are long the underlying. To hedge, they need to take a short position in the forward contract

Step #2: How many contracts do they need to short?

000,000,1$)000,1)($ 000,1( bondsValueFaceTotal

contractsContractsofNumber 10000,100

000,000,1$

Total face value held by the hedge fund

Once you know the number of contracts to long or short you have enough information to set up the hedge. What we do in the last step is show that the hedge works

Example: Hedging with Forwards/FuturesA hedge fund currently holds 1000 20 year treasury notes each note has face value of $1000. The current spot price is $994 per bond. They decide to hedge using a 3-month futures contract on the 20 year treasury bond. The current futures price is $99.5 per $100 of face value and contract size is $100,000.

a)How many contracts do they need?b)Show that the position is hedged if the price of the 20-year Treasury is $905 or $1,050 in three months.

Forward Payoff

Futures contracts = $0.00 forward/future cost nothing at inception

Sell 1M face value at the forward price $0.995(1,000,000) = $995,000

Buy a bond in the market: -$905(1,000) = - $905,000

Bond Position

(1000)(994) = 994,000They hold 1000 bonds worth $994 a piece

(1000)(905) = 905,000They hold 1000 bonds worth $905 a piece

$994,000 $995,000

40

Bond Price = $905

t = 0 t = 3m

(1000)(1,050) = $1,050,000 They hold 1000 bonds worth $1,050 a piece

Bond Price = $1,050

Forward Payoff $90,000

$995,000

Sell 1M face value at the forward price $0.995(1,000,000) = $995,000

Buy a bond in the market: -$1,050(1,000) = - $1,050,000

Forward Payoff - $55,000

Hedged Portfolio

valuefaceofdollarper 995.0$100$

5.99$

$995,000$995,000$994,000Hedged Portfolio

Forward Payoff

Futures contracts = $0.00 forward/future cost nothing at inception

Bond Position

(1000)(994) = 994,000They hold 1000 bonds worth $994 a piece

(1000)(905) = 905,000They hold 1000 bonds worth $905 a piece

Bond Price = $905

(1000)(1,050) = $1,050,000 They hold 1000 bonds worth $1,050 a piece

Bond Price = $1,050

t = 0 t = 3m

Example: Hedging with Forwards/FuturesA hedge fund currently holds 1000 20 year treasury notes each note has face value of $1000. The current spot price is $994 per bond. They decide to hedge using a 3-month futures contract on the 20 year treasury bond. The current futures price is $99.5 per $100 of face value and contract size is $100,000.

a)How many contracts do they need?b)Show that the position is hedged if the price of the 20-year Treasury is $905 or $1,050 in three months.

Sell 1M face value at the forward price $0.995(1,000,000) = $995,000

Buy a bond in the market: -$905(1,000) = - $905,000

41

Forward Payoff $90,000

Sell 1M face value at the forward price $0.995(1,000,000) = $995,000

Buy a bond in the market: -$1,050(1,000) = - $1,050,000

Forward Payoff - $55,000

These are the transactions you would have to execute if the contract was physically settled – For financially, settled you just think through these transactions to get to the payoff

The company you work for is obligated to deliver 5,000 5-year zero coupon bonds in one year. Payment will be maid upon delivery. The current YTM for a 5-year zero is 12%. Each bond has face value of 1,000 Hedge your position using a one-year futures contract. Assume a standard contract size of 250,000 and the current future price is $64 per $100 of face value. Show that you are hedged if the YTM increases to 13% or decreases to 11% in one year. 42

Types of Hedging Strategies

1. Microhedge: The FI manager chooses to hedge the risk from a specific asset Example: An FI manager may believe that American auto manufactures are going to suffer

unexpected earnings losses in the near future causing their interest rates (financing cost) to increase. The manager shorts futures contracts on the Ford 5 ¼% 10 year bond which he currently holds

Managers will pick contracts where the underlying asset closely matches assets being hedged

2. Macrohedge: The FI uses futures contracts to hedge the risk of its entire portfolio (balance sheet). Example: using futures contracts to reduce the duration gap Managers hedging strategies must consider the duration of the entire portfolio because durations of

individual assets will cancel or multiply (“net out”)

3. Routine Hedging: The FI uses forward contracts to reduce the interest rate risk on its balance sheet to its lowest level

4. Selective Hedging: The FI chooses to bear some of the risk on its balance sheet by hedging only certain components of the balance sheet

43

Duration of a Forward Contract

Suppose you enter into a forward contract to purchase a 10 year treasury bond in 3 months. The duration of the treasury is currently 7.5 years. What is the duration of the forward contract?

Draw the cash flows of each investment assuming there are no payments made on the underlying during the life of the forward contract

The string of cash flows from the forward contract and the 10 year note are the same. Therefore, the duration of the futures contract is the same as the duration of the underlying asset

0.5 1 9 9.5 10

10 year Treasury

.5 1 9 9.5 10

Forward Contract on a10 year Treasury3 months

44

Hedging with Forwards (Macrohedge)

Object: immunize the balance sheet against changes in interest rates

Basic Idea: Construct a portfolio of futures contracts such that any gains/losses in equity capital on the balance sheet will be offset by gains/losses on the portfolio of futures (held off balance sheet)

Step #1 Calculate the potential gain or loss in equity capital

FE

R

RAkDDE LA

1

45

If interest rates change – how much will I gain or lose in equity capital

Hedging with Forwards (Macrohedge)

Step #2 Find the total forward position needed to hedge the change in equity

We know that DF = Dunderlying we can use this to find the total forward position

Note: we can use a forward on any asset as long as we know its duration

Set the change in equity equal to the negative change in the value of the forward position and solve for F

FE

Funderlying DD

46

What position (futures price × total face value) in the futures contract will offset the gain/loss in equity

S&P500 shares, bushels of corn, barrels of oil …

FR

RDE F

1

Macrohedge (continued)

Step #3 Find the Number of Contracts:

47

How many contracts do we need to enter (long/short) to get this position

Macrohedge (continued)

Step #3 Find the Number of Contracts:

F is the total position in the futures contracts but how many contracts do we need to buy to cover the position?

FFF PQNF

contract futuresin position total F

contracts futures ofNumber FNcoffee) of lbs (37,500contract futures one of Size FQ

lb)(per price Future FP

FFF PQ

FN

48

Total position in futures contracts(futures price × total face value)

Total position per contract

Example: Suppose a FI has assets and liabilities on its balance sheet with total values shown below. The duration of its assets and liabilities is 5 years and 3 years respectively. Management at the FI expects interest rates to increase from 10% to 11%. They hire you as a consultant to recommend a macrohedge.

Futures contract:A futures contract on a 20 year Treasury bond with 8% coupon and 100,000face value is available. The current futures price is $97 / $100 face value. Analysts have computed the duration of the bond to be 9.5 years

Assets Liabilities

A=$100 mill L = $90 mill

E = $10 mill

$100 mill $100 mill

Lecture Summary

What are Forward and Future contracts

Three types of prices: Spot Forward/Future Delivery

Payoffs of Forwards/Futures

Hedging with Forwards/Futures Micro Hedge Macro Hedge

50

Appendix

Valuing a forward/futures Forward/Futures Payoff Graphs Difficulties with Forward/Futures Hedging

Basis risk

51

Contract Value

52

Example: Forward/Future Value

On June 20, 2010, JP Morgan entered the forward contract to buy a 10-year Treasury with $1000 face value for $890 on March 23, 2012.

53

Spot price S0

Delivery Price

Forward/Future Price(March 2012 contract)

ktTot krSF )()/1(

ONLY CONSIDER THE FORWARD/FUTURE CONTRACT:

Forward/Future & Spot Prices

$941

For example: Oct 8, 2010

-$890

Sell

Buy$51

Locked–in a sure CF = $51

Because this is sure CF we can discount at the risk free rate

Value = PV(51) =$47.73

Example: Forward/Future Value54

ONLY CONSIDER THE FORWARD/FUTURE CONTRACT:

Take Away: The forward price will continue to change after you enter the forward

contract. This will cause the value of your contract to change over time.

At any point in time the value of the forward/futures contract is the present value of the difference between the delivery price and the price that you can close out your contract for.

On June 20, 2010, JP Morgan entered the forward contract to buy a 10-year Treasury with $1000 face value for $890 on March 23, 2012.

55

Payoff Graphs

Long & Short Positions56

Underlying Asset: Long: you own the asset Short: you owe the asset

Forward Contract Long: you have agreed to buy the asset in the future at a pre- specified price (locked-in a price to buy)

Short: you have agreed to sell the asset in the future at a pre- specified price (locked-in a price to sell)

Example:Stock → If you are long the stock you own it

Example:Stock → If you are short the stock you have borrowed # shares from a dealer and sold them. So, you owe # shares back to the dealer

Underlying Asset Long Payoff Graphs57

Spot Price

Payo

ff

All possible spot prices for the Treasury Bond

This gives u

s all the possib

le payoffs for one Treasury Bond

Example: suppose the price of a Treasury bond is $550

$550Spot Price

$550

If you sell one Treasury bond the Payoff is $550

Long One Treasury Bond Payoff For one share

Underlying Asset Short Payoff Graphs58

Payo

ff

Example: suppose the price of a Treasury bond is $425

$425

Spot Price

- $425You will have to pay

$425 to buy one Treasury bond

Short One Treasury Bond Payoff

Long Forward Payoff Graphs59

Even if the price of the bond is zero you have still agreed to pay $900 for it

If the price of the bond is $900, then you can buy it using the forward for $900 and sell it in the market for $900. payoff = 0

Long Treasury Bond Forward Payoff

If the price of the bond is $1,380, then you can buy it using the forward for $900 and sell it in the market for $1,380. payoff = 1,380-900 = 480

480

Payoff =500

If the price of the bond is $280, then you must buy it using the forward for $900 and sell it in the market for $280. payoff = 280-900 = -620

-620

Short Forward Payoff Graphs60

Short Treasury Bond Forward Payoff

If the price of the bond is $1,380, then you can buy it in the market for $1,380 and sell it at the delivery price of 900. payoff = 900-1,380 = -480

-480

Payoff = -480

If the price of the bond is $280, then you can buy it in the market for $280 and sell it using the forward for 900. payoff = 900 - 280 = 620

620

Payoff Graphs61

Underlying Asset:

Forward Contract:

Long Short

Long Short

Delivery Price

Difficulties Hedging withFutures Contracts

62

Difficulties with Futures Hedge

Basis Risk: the risk that the gains/losses on the forward position do not exactly match the gains/losses on the underlying economic position over time

Example: Suppose you are a farmer in the heartland of America Your crop of choice is white corn (you think it makes you stand out) You routinely use forward contracts to hedge against unexpected price

movements. You will have 5,000 bushels of corn to sell in September http://www.cmegroup.com

Forward contract You have entered into the September contract to sell 5000 bushels of yellow corn for

$6.78/bushel. (6.78 x 5000 = $33,900) The fact that the contract is on yellow corn dose not concern you because the prices have always

been very similar

63

Difficulties with hedging

In September there is a large shock to the demand for white corn in the global market. International producers divert excess supply to the US driving the price of white corn down to $5/bushel

Surprisingly, the price of yellow corn is unaffected and still sells for $6.50 / bushel

Calculate the unexpected gain or loss on your position With the forward contract you would have expected to be able to sell

white corn for $6.78/bushel but the actual sale price was $5

loss = $5.00(5,000)-$6.78(5,000) = -$8,900 But you have the futures contract:

Buy 5000 bushels of yellow corn in the market = - ($6.50/bushel)(5000) = - 32,500 Sell 5000 bushels of yellow corn using the forward = + ($6.78/bushel)(5000) = +33,900

The gains from the forward position do not

cover the economic losses

+1,400

64

Routine vs. Selective Hedging

Question: why would a manager choose to perform a selective hedge instead of a routine hedge?

Answer: In finance, there is always a risk vs. return tradeoff!As managers reduce the FI’s risk by hedging positions, they also decrease the expected return on their investments.This also reduces the expected return to shareholdersTherefore, routine hedging usually occurs when interest rates are extremely unpredictable

65

Lecture Summary

We talked about how banks can hedge some or all of their interest rate risk exposure using Forward/Futures contracts

Forwards/Futures Introduction Prices: Forward/Future, Spot, and Delivery Payoffs vs Value Payoff Graphs Microhedge with Forward/Future contracts Macrohedge with Forward/Futures contracts Basis Risk – difficulties with Forward/Future hedge

66