heathrow airport’s cost of capital a report on behalf of...

TRANSCRIPT

- 1 -

Heathrow Airport’s

Cost of Capital

A report on behalf of Heathrow

Public Version

February 2013

Europe Economics is registered in England No. 3477100. Registered offices at Chancery House, 53-64 Chancery Lane, London WC2A 1QU.

Whilst every effort has been made to ensure the accuracy of the information/material contained in this report, Europe Economics assumes no

responsibility for and gives no guarantees, undertakings or warranties concerning the accuracy, completeness or up to date nature of the

information/analysis provided in the report and does not accept any liability whatsoever arising from any errors or omissions © Europe Economics.

All rights reserved. Except for the quotation of short passages for the purpose of criticism or review, no part may be used or reproduced without

permission.

Contents

1 Introduction .................................................................................................................................................................... 1

1.1 Estimate of Heathrow’s Cost of Capital ......................................................................................................... 1

1.2 Structure of Report .............................................................................................................................................. 1

2 Methodological Issues .................................................................................................................................................. 3

2.1 The CAPM Framework and other Cross-checks ......................................................................................... 3

2.2 Lack of Direct Market Data ............................................................................................................................... 5

2.3 Choice of the Relevant Capital Market ........................................................................................................... 7

2.4 The Impact of the Financial Crisis ..................................................................................................................... 7

2.5 Time Period ............................................................................................................................................................ 8

2.6 Gearing .................................................................................................................................................................... 9

2.7 Assumed Debt Beta ........................................................................................................................................... 10

2.8 Assumed Tax Rate .............................................................................................................................................. 11

3 Total Market Returns ................................................................................................................................................. 12

3.1 The Relationship between Market Returns and Macroeconomic Conditions ..................................... 12

3.2 The Sustainable Growth Rate (and hence Risk-Free Rate) is Likely to Increase during the Price

Control Period ................................................................................................................................................................. 18

3.3 Why the Sustainable Growth Rate is Likely to Increase ........................................................................... 21

3.4 The Equity Risk Premium .................................................................................................................................. 26

3.5 Conclusion on Total Market Returns ............................................................................................................ 32

3.6 Skewness and Non-Diversifiable Skewness in Total Market Returns .................................................... 33

3.7 Appendix: Technical Details Underpinning the Model .............................................................................. 34

4 Debt Premium ............................................................................................................................................................. 40

4.1 Introduction ......................................................................................................................................................... 40

4.2 Bond Spread Analysis ......................................................................................................................................... 40

4.3 Issuance costs ...................................................................................................................................................... 46

4.4 CEPA’s debt premium estimate ...................................................................................................................... 47

4.5 Conclusion on Heathrow’s debt premium ................................................................................................... 49

5 Developments at Heathrow and in the Airport Sector Since 2007 ............................................................... 50

5.1 Introduction ......................................................................................................................................................... 50

5.2 Macroeconomic context ................................................................................................................................... 50

5.3 Changes in demand ............................................................................................................................................ 50

5.4 Regulatory context ............................................................................................................................................. 52

5.5 The Impact of Capacity Constraints and Regulation on Skewness......................................................... 52

6 Equity Beta .................................................................................................................................................................... 53

6.1 Comparator Data ............................................................................................................................................... 53

6.2 Fundamental Beta Analysis ............................................................................................................................... 59

6.3 Skewness Analysis ............................................................................................................................................... 64

6.4 CEPA’s estimate of Equity Beta ....................................................................................................................... 75

6.5 Overall Conclusion on Equity Beta ................................................................................................................ 78

7 Overall WACC ............................................................................................................................................................ 79

7.1 Overall WACC Estimate .................................................................................................................................. 79

7.2 CEPA’s estimate of the WACC ...................................................................................................................... 81

7.3 Aiming Up ............................................................................................................................................................. 82

7.4 Conclusion ............................................................................................................................................................ 83

Appendix: Approach to Calculating Betas ...................................................................................................................... 84

Introduction

- 1 -

1 Introduction

1.1 Estimate of Heathrow’s Cost of Capital

This report considers what cost of capital would be appropriate for Heathrow in the Q6 airports

price control. It has been commissioned by Heathrow Airport from Europe Economics, with a view

to ensuring that the cost of capital determined for Heathrow is no lower than is justified by market

and economic conditions and outlook.

In the Q5 control, the values for key parameters of the cost of capital determination, as proposed by

the Competition Commission and the CAA, were as shown in columns two and three of Table 1.1.

Column four contains the derivation of this report’s proposed minimum value of the WACC for Q6,

which we would currently expect to revise upwards in later phases.

Table 1.1: Overall WACC

Q5 determination

WACC estimate for Q6

from this report

Low High

Risk free rate (%)

2.5 2.5 2.0

Equity risk premium (%)

2.5 4.5 5.0

Debt Premium including

issuance cost (%) 1.05 1.05 2.6

Equity beta

0.91 1.15 1.3

Cost of equity

(post-tax) (%) 7.3 8.5

Tax rate* (%)

28 21

Cost of equity (pre-tax) (%)

10.2 10.8

Cost of debt (pre-tax) (%)

3.55 4.6

Gearing (%)

60 60

WACC (vanilla) (%)

WACC (pre-tax) (%)

6.2 7.1

The Q6 price control is, at the time of writing, expected to apply for the period April 2014 to March

2019. Even the commencement of this period is some distance away at the time of writing, in highly

volatile market conditions. We anticipate that our proposed values could be amended significantly

(probably upwards) between the time of this report and later submissions.

1.2 Structure of Report

Subsequent sections of this report proceed as follows:

Introduction

- 2 -

In Section 2 we set out a number of the key methodological issues arising in respect of Q6.

Section 3 considers Total Market Returns, including key generic parameters of the CAPM model

such as the risk-free rate and the equity risk premium. The central issue of this section is how

total market returns should be expected to evolve between the time of writing and the mid-point

of the Q6 price control period.

Section 4 considers Heathrow’s cost of debt, in particular noting the rise in debt premia since the

lows of 2005-7 (now commonly acknowledged to reflect market under-pricing of risk).

Section 5 considers developments in the airports sector since the time of the Q5 Competition

Commission advice and CAA determination.

Section 6 estimates equity beta from comparator and Heathrow data.

Section 7 draws together the analysis of previous sections into an estimate for the overall

WACC, and considers the appropriate methodology for aiming up.

Methodological Issues

- 3 -

2 Methodological Issues

These sections sets out the key methodological issues that we consider particularly relevant in the

context of the upcoming price review. These are:

The general framework to be used and additional cross-checks.

Issues related to the lack of direct market data.

The choice of the relevant capital market.

The impact of the financial crisis.

The relevant time period.

The assumed gearing.

2.1 The CAPM Framework and other Cross-checks

The standard way UK regulators assess the cost of capital is through the Weighted Average Cost of

Capital / Capital Asset Pricing Model (WACC-CAPM) approach. The relationship between the

CAPM and the WACC approach is discussed below.

2.1.1 The CAPM

The CAPM framework was developed in the 1960s, building on the portfolio analysis work of

Markowitz (1958), as a way to estimate the value of assets. The key feature of CAPM is that, given

its important assumptions concerning the efficiency of financial markets and that investors care only

about the mean and variance of returns, investment returns can be expressed as:

r = rf + MRP × βA [Eq. 2.1]

where r is the (expected) return on the asset, rf is the return that would be required for a perfectly

risk-free asset, MRP is the “market risk premium”, that is to say the excess return over the risk-free

rate that would be delivered by a notional perfectly diversified portfolio equivalent consisting of all

assets (“the whole market”), and βA is a measure of the correlation between movements in the value

of the asset of interest and in the value of assets as a whole. It is also called “beta” (or sometimes

the “asset beta”).

2.1.2 The vanilla WACC and the capital structure

Utilities typically use a combination of debt and equity. Therefore, in the (vanilla) WACC

framework assets’ returns are decomposed into a cost of equity and a cost of debt, according to the

following formula:

r = (E/V) × re + (D/V) × rd [Eq. 2.2]

where V is the total value of the assets of the company, E is the value of the equity, D is the value of

the debt so V ≡ D + E (D/V is the proportion of the total value of the company accounted for by

debt and is often referred to as the company’s “leverage” or “gearing” — clearly, D/V + E/V = 1), re

Methodological Issues

- 4 -

is the (expected) return on equity and rd is the (expected) return on debt (note that this is not

identical to the coupon rate or yield on debt, since these do not embody probabilities of and losses

on default).

2.1.3 Equivalence between CAPM and WACC

The fundamental relationship between CAPM and WACC stems from the Modigliani-Miller (MM)

insight that the asset beta, and hence the vanilla WACC, will not change due to gearing, unless either

a) the debt tax shield has value or b) the market’s assessment of the systematic risk exposure of the

underlying cash flows has changed with gearing. Using the second Modigliani-Miller Theorem1, the

following equivalence between asset beta and vanilla WACC can be shown:

Table 2.1: Asset beta — vanilla WACC equivalence

Return via asset beta Return via vanilla WACC

MRPrr Af

DE r

ED

Dr

ED

Er

MRPED

D

ED

Err DEf .

)()( MRPrED

DMRPr

ED

Er DfEf

MRPED

DMRP

ED

Err DEf

MRPED

DMRP

ED

Err DEf

The above utilises the decomposition of the corporate debt premium into debt beta and market risk premium components

In Table 2.1 βe is a measure of the correlation between movements in the value of the company’s

equity and in the value of assets as a whole. Similarly, βd is a measure of the correlation between

movements in the value of the company’s debt and in the value of assets as a whole. Since returns

on equity and debt tend to move under different circumstances (e.g. when companies are not in

default debt returns differ little but equity returns may differ considerably, whilst when companies

are in default equity returns differ little (they are close to zero) whilst debt returns differ markedly

(depending on the scale of the default)), equity and debt betas are not typically the same.

2.1.4 Alternatives to CAPM

In some other price reviews, regulators have considered alternatives to CAPM, typically to act as

cross-checks on the main CAPM calculation. Some of the alternatives to CAPM that have been

considered in other contexts would not appear to be relevant for Heathrow at Q6. In particular:

The Fama French model is typically used to take account of small company effects, which would

not be relevant to Heathrow airport. Moreover, the use of the Fama and French approach has

been heavily criticised by the CC in the previous (Q5) review.

The Dividend Growth Model (DGM) can be used to estimate the cost of equity, but the CC has

noted that it is compatible with a very wide range estimate, thus limiting its practical usefulness.

Moreover, the CC was highly sceptical about the value of the DGM in the context of the Bristol

Water judgment, stating that they “regard the DGM evidence as consistent with a wide range of

figures for the cost of WaSCs’ equity”.2

1 The Modigliani-Miller theorem implies the following expression:

ED

D

ED

EDEA .

2 http://www.competition-commission.org.uk/rep_pub/reports/2010/fulltext/558_appendices.pdf

Methodological Issues

- 5 -

In the Q5 price control, the CAA noted the potential value, at least as a cross-check, of the third

moment CAPM model. The third moment CAPM addresses the possibility that investors have

preferences over the distribution of returns that go beyond mean and variance, in particular taking

account of skew. The potential usefulness of the third moment CAPM can be justified on the

following grounds:

The third moment CAPM represents a natural extension of the traditional CAPM framework (as

opposed to being a completely separate methodological approach).

The third moment CAPM has been mentioned by the CC as a potentially relevant cross-check

method for estimating the cost of capital in the airport sector, and it has not been the subject of

heavy criticism (as is the case for the DGM and Fama and French approaches).

Airports’ returns in general, and Heathrow’s returns in particular, are likely to be negatively

skewed (mainly due to the joint effects of capacity and regulatory constraints, a point which is

discussed in more detail below) which makes consideration of the results of the third moment

CAPM model particularly relevant.

Market to Asset Ratios (MARs) for listed companies are typically used as one source of evidence on

whether the regulated WACC is higher or lower than the true market WACC (although one needs

to bear in mind that other factors may also affect MARs). Regulators may also look at MARs

following draft determinations to see whether the overall price control package seems too harsh or

too generous.

2.2 Lack of Direct Market Data

The most significant methodological challenge in the upcoming price control review is the lack of

direct market data for Heathrow Airport Holdings. (In the Q5 review direct market data for

Heathrow was lacking, but market data for the then BAA group was available up until only a few

months before the CAA’s initial estimates were produced). We therefore list below potential

approaches to deal with this issue.

2.2.1 Use of comparators

When direct market data for the entity of interest is lacking it is common practice to infer the asset

beta of the entity of interest (Heathrow airport in this case) based on analysis of relevant

comparators for which market data is available. In the last price control review a number of

international airports, airline companies and UK utilities were used as comparators. We shall

discuss below which potential comparators are most relevant to use on this occasion.

Beta estimates can vary significantly across comparators, and not all comparators are equally

representative of Heathrow’s exposure to systematic risk. A degree of judgment is therefore

needed in deciding to which estimates more weight should be attached. A number of criteria can be

used to assist this process. For example, airports with significant similarities to Heathrow (e.g. in

passenger numbers, status as an international hub, full capacity utilisation etc.) could be considered

to be more representative than UK water companies. Nevertheless, inferring Heathrow’s asset beta

directly from comparators’ estimates alone can be problematic and would be necessarily subject to a

material degree of arbitrariness.

Methodological Issues

- 6 -

2.2.2 Changes since the last period in which direct market data was available

Another potential use of comparators is to assess changes occurring since the last price control

period. This approach does not attempt to assess a precise beta estimate for Heathrow, but rather

indicates the direction of a change (e.g. whether Heathrow’s asset beta has increased or decreased

since the Q5 price control). In the context of the third moment CAPM, a particular consideration

would be whether there is evidence that the skewness of returns to Heathrow has changed since

the time of the last price review.

2.2.3 Fundamental and accounting beta

Alongside the comparator beta analysis, another source of evidence on Heathrow’s asset and equity

betas would be the employment of account and fundamental beta methodologies.

Accounting betas are based on econometric analysis of accounting returns rather than stock market

returns, and hence can be calculated even for non-listed companies. In particular, it would be

possible to regress changes in accounting earnings for Heathrow airport against changes in earnings

for an equity index (such as the FTSE All Share).

However, there are various potential limitations with this approach. One is that firms do not publish

measured earnings on a daily basis, leading to regressions with fewer observations and limited

statistical power compared to those obtainable with daily market data. Another is that earnings are

often smoothed out and subject to accounting judgments, leading to potential mis-measurement of

accounting betas. Finally, accounting information on earnings reflect ex post achieved earnings,

whereas stock prices used in normal beta estimation reflect expectations of future earnings.

A more sophisticated variant of this approach is to calculate what are called “fundamental” betas.

This involves estimating a relationship between various fundamental characteristics of firms and their

betas, and then use the characteristics for Heathrow airport to estimate Heathrow’s beta.

However, it should be noted that a fundamental beta analysis will only imperfectly account for the

effects of systematic skewness, especially insofar as a company has skewness disproportionate to its

variance (as we shall argue Heathrow does).

2.2.4 Disaggregation of Ferrovial’s beta

The largest shareholder in Heathrow airport is Ferrovial, until recently with 33.65 per cent of its

equity. Heathrow is a material component of Ferrovial’s overall business. As at 20103:

the airport business accounted for approximately 23 per cent of Ferrovial’s total revenues, 50

per cent of Ferrovial’s earnings, and 50 per cent of Ferrovial’s total assets;

Heathrow was responsible for 70 per cent of the revenues and 75 per cent of earnings generated

by Ferrovial in its airport business segment, and hence 16 per cent of total revenues and 38 per

cent of earnings.

When a regulated entity is a material part of a broader non-regulated business, regulators

sometimes choose to infer the beta for the regulated entity by disaggregating the beta for the overall

entity. This is, for example, the approach that has been taken by Ofcom to the regulation of BT.

However, such exercises are most normally conducted when the target entity (in this case

Heathrow) constitutes a majority of the total business. A 16 per cent share in revenues / 38 per

3 These figures were sourced from Ferrovial’s annual accounts (January-December 2010)

Methodological Issues

- 7 -

cent in earnings, though significant, is unlikely to be sufficient for such an exercise to constitute the

main data basis for a regulatory decision.

2.3 Choice of the Relevant Capital Market

Past regulatory decisions concerning utilities in the UK have adopted the UK as the relevant capital

market. For instance, beta analyses based on European and world market indices have been used

mainly as cross-checks but have never represented the centrepiece of the analysis. Obviously an

airport has, intrinsic to its business, a straightforwardly international dimension that is of a

completely different order from any international dimension in, say, a water company. Furthermore,

as we understand it, the typical investor relevant to Heathrow operates mainly in developed western

economies.

It might therefore be appropriate to place more weight, at least for some parts of the estimation

exercise, on European and US figures as opposed to UK figures. Alternatively, even if the UK

market continued to be the main source of data, a greater weight might be placed upon international

data than would be the case for UK utilities.

2.4 The Impact of the Financial Crisis

The financial crisis had a significant impact on cost of capital parameters. There have been a number

of key regulatory decisions regarding the cost of capital since 2008, including Ofwat (2009), Ofcom

(2009, 2011), Ofgem (2011) and the Competition Commission’s judgement on the Bristol Water

case (2010). Based on these judgments, the following trends can be noted:

Increase in Equity Risk Premium (ERP) — periods of high market turbulence are associated with

an increased perceived risk of equity investments and, as a result, investors tend to require

higher premiums. ERP regulatory judgements have tended to rise, from typical figures of around

2.50 - 4.50 per cent in 2008 (as per the Q5 Competition Commission recommendation). During

the height of the credit crisis, figures above 5 per cent were used (e.g. 5.25 per cent for

Electricity Distribution in 2009, 5.4 per cent for Water in 2009). Some recent figures have fallen

back to around 5 per cent (e.g. 4.0-5.0 per cent in the Bristol Water judgement, and 5.0 per cent

in Ofcom’s OpenReach judgement of 2011), though in its final proposals for electricity and gas

transmission and gas transmission in 2012, Ofgem proposed an ERP of 5.25 per cent

Decrease in risk-free rate — as the economic conditions deteriorate market expectations about

the economy’s sustainable growth are revised downward and the risk-free rate falls. In fact, risk-

free rate judgements have tended to fall over time, from figures such as the CAA’s Q5 judgement

of 2.50 per cent in 2008, to the 1-2 per cent range of the Competition Commission’s 2010

Bristol Water judgement and the 1.4 per cent figure in the Ofcom OpenReach judgement of

2011. In its final proposals for electricity and gas transmission and gas transmission in 2012,

Ofgem proposed a risk-free rate of 2.0 per cent.

Increase in debt premium — Bond spreads rose sharply during the financial crisis, but have since

come down — though without falling back to their pre-crisis lows. A crucial issue is what view

to take about where bond spreads are likely to settle during the forthcoming price control

period. For instance, it is arguably not appropriate to assume that spreads will end up around the

level seen immediately prior to the financial crisis, since it can be argued that risk was being

under-priced during this period.

Methodological Issues

- 8 -

Other potential impacts — In addition to the impacts illustrated above, which can be viewed —

to a certain extent — as being transitory, an interesting issue is whether the behaviour of

financial markets during the recent global recession has changed the shape of the distribution of

expected investment returns. The recent global recession might demonstrate that perceived

downside risk in some sectors is now greater than previously thought, tending to balance out

returns that were previously perceived as skewed upwards. For example, perhaps in the

regulated sector some investors previously thought that the worst that regulated entities might

do would be to secure their cost of capital, but that there was potential for them to outperform

regulatory assumptions and so gain on the upside; whereas now it is better understood that

there is genuine downside risk. Or alternatively, some stakeholder might argue that for many

assets, there were previously fairly balanced returns but there is now seen to be downside tail

risk, skewing distributions.

Assuming one does proceed with a UK-based WACC analysis, another issue is the relevance of

“crisis” analysis of the cost of capital to the current review. The Q5 determination was undertaken

at the beginnings of the credit crisis. Determinations by regulators since then have had to take

account of the financial crisis and market turbulence. This has had implications for inferring the cost

of capital from historic or contemporaneous data. A key is question is therefore: is the crisis over

or will it be over by the time of the next price control period?

For the purposes of the main estimates reported here we shall assume that by the time the Q6 price

control commences, the acute phase of the crisis will be over. However, this is clearly a question

that is material and should be kept under close review. Alongside our main estimates, we report in

specific sections below the implications for key affected parameters if the crisis were to persist.

However, our overall estimates in this document do not assume a crisis scenario.

2.5 Time Period

The Q6 price control is, at the time of writing, expected to apply for the period April 2014 to March

2019. The precise appropriate weightings, across the price control period, for cost of capital

purposes might reflect a number of complex factors, such as the scheduling of the capital

programme for Q6, that are not available to us at the time of writing. We shall assume, for our

purposes here, that the desired exercise is to estimate what the cost of capital for Heathrow will be

at the mid-point of the price control period — roughly at the turn of the year 2016/17 or, more

strictly, October 2016.

As we write, in the first half of 2012, October 2016 is clearly some distance away, and much could

happen. Very often in finance, the values of contemporaneous forwards-looking variables constitute

the best-estimate of future variables — even, sometimes, quite distant variables. Even when market

data allow us to infer implied estimates for how views about forwards-looking variables will change

in the future, relatively modest differences in the implied future values and the actual current value

are often best explained in terms of factors such as liquidity, uncertainty, and transactions costs.

In current and recent very extreme market conditions, however, (i) it seems much less likely than

usual that current forwards-looking estimates provide a best-estimate of circumstances more than

four years ahead — fundamental analysis of economic conditions and outlook might provide us with

strong reasons to believe that conditions in more than four years’ time will be very different from

those today; and (ii) as we shall see below, implied estimates, drawn from current market data, for

how views about forwards-looking variables will change in the future involve changes far greater in

magnitude than those normally attributed to liquidity, uncertainty or transactions costs.

Methodological Issues

- 9 -

There are thus strong reasons to believe that key elements of the cost of capital in more than four

years’ time could be different from that indicated by market data today.

2.6 Gearing

The gearing assumed for Heathrow in the Q5 price control was 60 per cent. For Q5, Heathrow’s

notional gearing was determined at 60 per cent. In our August 2012 report we took as given the

assumption that Heathrow’s notional gearing would be 60 per cent in Q6, also. We consider what

are the implications of recent trends in gearing for the continued appropriateness of this 60 per cent

assumption. The most widely-quoted analysis of UK non-financial sector indebtedness is that from

the McKinsey Global Institute. In the chart below we provide evidence from the latest available

report at the time of writing (the January 2012 report4).

Figure 2.1: McKinsey Global Institute January 2012

Source: McKinsey Global Institute

We see first that in the period leading up to the Q5 determination non-financial sector indebtedness

rose, relative to GDP, as indeed it had been rising for much of the previous two decades. However,

whilst aggregate UK indebtedness has increased since the time of the Q5 determination in 2008,

driven particularly by increases in bank and government debt, the non-financial corporate sector has

been deleveraging, down from 122 per cent of GDP to 109 per cent.

4 http://www.mckinsey.com/insights/mgi/research/financial_markets/uneven_progress_on_the_path_to_growth

Methodological Issues

- 10 -

If the Q5 determination’s choice of a notional 60 per cent gearing reflected an assumption that the

trends of the previous two decades would be extended, such that 60 per cent gearing was

“forwards-looking”, then the natural assumption might be that the Q5 notional gearing of 60 per

cent was likely to have been too high — the trend of rising gearing did not continue. In that case it

might be natural to consider how much gearing should fall in Q6.

However, we note that the Q5 determination did not aspire fully to reflect then-recent trends of

increased leverage; neither did it anticipate further leverage rises. Notional gearing was raised,

recognising the increase in gearing associated with the January 2006 takeover, but not as far as actual

gearing. We observe that the Q4 notional gearing was 25 per cent so the increase to 60 per cent

already takes account of the gearing impact of the Ferrovial takeover.

This conscious decision to under-shoot those then-recent trends in infrastructure and utilities

leverage can be seen as having been vindicated by subsequent market developments. The question,

then, is not whether Q5 gearing trends have suggested that the Q5-determined gearing was errant

— quite the reverse is true. Rather, the question is whether recent trends imply there is a secure

basis for believing that Q6 gearing will be either materially higher or lower than that in Q5.

At this stage we see no such basis. There is expected to be significant deleveraging in the UK, but

this is expected to occur principally in the household and banking sectors. The non-financial

corporate sector has already deleveraged whilst leverage in the banking sector continued to rise. It

is possible that the non-financial corporate sector will deleverage further yet, in response to wider-

economy deleveraging. However, it is also possible that economic recovery will be associated with

an increased appetite for debt amongst non-financial corporates.

At this stage, we see no compelling reason to deviate from the 60 per cent notional gearing

assumption used in Q5, and would propose that analysis proceeds on that basis pending any basis for

a change.

2.7 Assumed Debt Beta

The debt beta assumed for Heathrow in the Q5 price control was 0.1. The reasons for choosing a

positive debt beta rather than the zero chosen in regulatory determinations up to that point

reflected the special circumstances of that review, as set out on p10 paragraph 3.4 of the “CAA’s price

control reference for Heathrow and Gatwick airports, 2008-2013 — Supporting Paper II” (March 2007)5,

namely:

Large step change in gearing;

Absence of observable equity data after the step change in gearing;

Relatively low equity beta before the change in gearing; and

Relatively high debt beta.

Since BAA/Heathrow Airport Holdings equity beta data has not been available since 2006, we

assume that the issue of there being a large step change in gearing shortly after the delisting of the

regulated entity’s equity does not arise in this review.

It was noted in the Q5 review, and has been noted in subsequent reviews such as Ofwat (2008-9)

and Ofgem (2010-11) that where these special factors do not arise the assumption of a zero debt

5 http://www.caa.co.uk/docs/5/ergdocs/ccref_sp2.pdf

Methodological Issues

- 11 -

beta is usually adequate for calculation purposes, as having a variable debt beta does not have a

material impact on the result. In these reviews debt betas of 0 or 0.1 were used.

In price reviews where use of a debt beta was investigated in more detail, as in Ofcom’s July 2011

WBA determination, its use was in specific response to particular methodological issues associated

with asset beta instability during 2009 under a variable gearing but non-variable debt beta estimation

model. Since we assume an invariant nominal gearing in this case, those gearing instability issues do

not arise here.

In the case of the methodologies discussed here, in addition to the above points, the implications of

a positive debt beta are not unambiguous, in that in some cases (e.g. when using Ferrovial data in our

fundamental beta analysis) the assumed notional Heathrow gearing (60 per cent) is below that of the

model (we “relever down” — in which case a higher debt beta would produce a higher asset beta),

whilst in other cases (e.g. when using comparator data from other airports such as Fraport) the

notional Heathrow gearing is higher (we “relever up”).

The lack of unambiguous directionality to the impact of debt beta undermines the case for using

non-zero estimates of it, given the intrinsic uncertainties in, and lack of a consensus method for, its

estimation. Calculating an elaborate debt beta on this occasion adds computational complexity and

estimation uncertainty without unambiguous significance for the final answer.

Bearing in mind the points above, for the purposes of this present report we assume that the

determined debt beta will be either 0 or 0.1.

2.8 Assumed Tax Rate

The tax rate assumed for Heathrow in the Q5 price control was the statutory tax rate of 28 per

cent. For the purposes of this present report we simply assume that the tax rate in Q6 will again be

the statutory tax rate. As per the most recent Treasury announcements, this will be 21 per cent.

Total Market Returns

- 12 -

3 Total Market Returns

In this section we shall argue the following points:

When the economy does better, total enterprise returns are greater (and vice versa).

This tends to mean that, when the economic outlook is better (i.e. the economy is expected to do

better in the future), required total market returns to capital also tend to be higher (and vice

versa).

Matters can, however, be somewhat complicated by the fact that total enterprise returns are

divided between returns to capital and returns to labour. Evidence suggests that labour may be

obtaining a diminishing share of total returns.

There is a relationship between the risk-free rate of return and the sustainable growth rate of the

economy, both in theory and in statistical evidence.

There is good reason to believe that, although the next few years may see quite low growth for

the UK economy (indeed, perhaps the economies of many developed countries), within the next

few years the medium-term outlook (the outlook beyond the next few years) may improve,

raising sustainable growth rates and associated with a rise in the risk-free rate.

When economic conditions are weak, the equity risk premium tends to be elevated. However,

the elevation in the equity risk premium is not always as great as the fall in the risk-free rate, so

total market returns often fall.

Conversely, when economic conditions improve, although the equity risk premium may fall back,

it should not be expected to fall back as much as the risk-free rate rises, so total market returns

should be expected to rise.

After a major economic and financial crisis, one might expect lasting impacts on risk appetites.

A major economic and financial crisis might also be associated with changes in (a) the degree of

skewness and kurtosis in returns; and (b) how much investors care about skewness and kurtosis

(e.g. the price of skewness).

3.1 The Relationship between Market Returns and Macroeconomic

Conditions

3.1.1 Impact of the economy on total returns to enterprise

When economic growth is higher, firms tend to have greater earnings. Demand is higher, so the

gross value added by businesses increases. Faster economic growth leads to greater total enterprise

returns.

So, if economic growth is expected to be higher in the future, there are expected to be greater

enterprise returns. Total enterprise returns are divided between labour and capital. If the split (the

ratio) can be taken as given (or indeed if returns to labour can be taken as fixed), then a rosier

economic outlook implies that returns to capital will be greater. If investors, responding to a rosier

economic outlook, did not demand higher returns, they would be conceding that labour would take

Total Market Returns

- 13 -

all the benefit from faster growth. Normally, however, capital demands its share of the expected

larger pie.

This is the straightforward case, but it is worth noting that there is no iron rule here. If there is a

change in the capital/labour split of returns, that could in principle reverse the overall effect or

enhance it. For example, poor economic times could coincide with a fall in the share of total returns

taken by labour, so that total returns to capital could rise even as total enterprise returns fell — in

which case our straightforward case effect would be reversed. As an alternative example, rosier

economic times could coincide with labour taking a lower share of total returns — so our

straightforward case effect would be enhanced.

As it happens, evidence suggests that labour has obtained a very stable share of total returns over

the past decade — employee compensation was 54.5 per cent of GDP in 2000 and 54.8 per cent of

GDP in 2010.6 The key change here occurred during the 1980s. In 1970 and 1980 employee

compensation was around 59 per cent of GDP, but by 1990 this had fallen to 55 per cent. Since

1990 the proportion has been very stable.

If a period of elevated returns is relatively brief — for example, if it occurs only for a year or two in

the recovery phase from a recession — then although actual returns to capital may be higher, the

required rate of return will not. Over the lifetime of an investment, there will naturally be some

years in which actual rates of return are below the cost of capital and others in which actual rates of

return are higher. But overall, average expected rates of return will equal the cost of capital.

On the other hand, periods of slower or higher growth could be more sustained than this. In

economics, the “long-term” refers to the period over which there are no fixed costs — when all

investments must be renewed. A period of low or high growth sustained for a longer period than

the lifetime of investments is not merely cyclical in nature; it is structural, and should be expected to

affect not merely year-to-year actual returns but also the required rate of return on investment,

because if low / high growth is sustained and economy-wide, then it affects the opportunity cost of

investment; we can neither invest in something else nor can we simply wait a brief time and invest

under more favourable circumstances. Some of the higher returns effect will appear in the value of

assets, as opposed to the required rate of return on assets (e.g. assets will have lower prices when

outlooks are worse). But if the rate of growth in returns is systematically higher (i.e. returns are not

simply higher but grow at a faster rate each year), then required rates of return will be higher as well

as prices being higher.

Lastly, we observe that economic “shocks” affecting the sustainable growth rate can be both good

and bad in nature. There might be new technologies that raise the sustainable growth rate (e.g. by

stimulating more rapid innovation); there might be periods of sustained bad weather damaging

harvests (e.g. for a couple of decades).

Thus, if (as we shall argue below), within the next few years the long-term (i.e. longer than the

investment life) economic outlook will improve, we should expect total required rates of return to

capital to increase. To reiterate, note carefully: to deliver this result we are not required to argue

that economic conditions will improve over the next few years. Contemporaneous economic

conditions affect required returns only insofar as they provide evidence of expected future economic

conditions. Our case will thus not be that the economy should be expected to improve over the

next few years; rather, it will be that within the next few years the medium-term outlook will

6 Source National Statistics, UK Economic Accounts, Table A3: Gross domestic product: by category of

income

Total Market Returns

- 14 -

improve (in particular, for the average growth rate over the ten to twenty years from the

commencement of the price control period).

3.1.2 Relationship between the sustainable growth rate and the risk-free rate

It is common to think of the risk-free rate of return as an exogenous taste variable — if not actually

constant, then at least fixed by factors outside portfolio decision-making. We think of the risk-free

rate as a measure of impatience, of how much we would rather have things today than tomorrow.

However, though there is much in this, it is not quite the whole story. For the risk-free rate is not

simply the return any one individual would require to hold a risk-free asset. Rather, it is the return

that would be available in such an asset. As such, (a) it reflects collective tastes, rather than those of

any individual — the “taste” of the Market; and (b) it reflects an (albeit notional) equilibrium

condition.

In standard long-term economic growth models, such as the Ramsey-Cass-Koopmans model, a key

equilibrium condition is that (absent population growth) the sustainable growth rate of the economy

equals the risk-free rate.7 Indeed, in corporate finance theory the risk-free rate of return is

sometimes viewed as arising from the sustainable growth rate (i.e. causality runs from the sustainable

growth rate to the risk-free rate).

For our purposes here, we need not fully endorse either of these positions. Instead, we make the

more limited claim that one should expect changes in the risk-free rate to be correlated with

changes in the sustainable growth-rate.

We can make this thought more concrete by considering the likely relationship between the

sustainable growth-rate and our best proxy for the risk-free rate, namely yields on government

bonds. If, for example, yields on medium- to long-term government bonds are very low, we should

interpret that as an indicator that the sustainable growth rate of the economy is expected to be very

low. To see why, consider an investor that is willing to buy a government bond at a very low yield.

That investor is choosing to purchase that government bond in preference to, for example, shares

or bonds in any other business in the real economy. But that must indicate that expected returns

for the real assets of these other real economy businesses are expected to be low or very volatile.

Let us set aside the high volatility case for now, and focus on the case in which returns of these real

economy businesses are low. If returns to all real assets are low, over the medium- to long-term,

then the economy can only be expected to grow slowly over the medium- to long-term. But the

sustainable growth rate is simply the rate at which the economy can grow over the medium- to

long-term. So (setting aside issues of policy mistakes etc. that might eventually be rectified), when

government bond yields are very low, one plausible explanation is that the sustainable growth rate of

the economy is expected to be very low.

Consider the following graph.

7 Ramsey, F.P. (1928), "A mathematical theory of saving", Economic Journal, 38, 152, pp543–559. Cass, D.

(1965), “Optimum Growth in an Aggregative Model of Capital Accumulation”, Review of Economic Studies,

37 (3), pp233–240.

Total Market Returns

- 15 -

Figure 3.1: Comparison of normalised GDP series with quarterly growth (1985Q1 = 100)

Source: Europe Economics calculations

In this graph we compare the average quarterly yield on ten-year index-linked bonds (in blue) with

the actual average growth rate over the subsequent ten years (in red). To make the relationship

easier to see, we have “normalised” both series so that, as they begin in the first quarter of 1985, we

call them both 100. Because they look ahead ten years, the data in this graph ends at the beginning of

2001 (we’ll look ahead below). We can see that movements in the red graph mirror movements in

the blue graph fairly well, though not perfectly. (The correlation between the red and blue graphs is

0.49, which is certainly respectable.) If we believe that the introduction of inflation targeting in the

fourth quarter of 1992 can be treated as a game-changing event, we can compare the right-hand end

of the blue graph with the green graph instead – seeing that the mirroring becomes even better.

(The break-adjusted series has a correlation of 0.83, which is very high.) In Appendix B we confirm

that the series does indeed exhibit a statistically significant structural break in the fourth quarter of

1992.

0

20

40

60

80

100

120

140

160

Average annual quarter-on-quarter growth rate for forthcoming 10 years: 1965Q1 = 100

10-yr index-linked gilt rate 1965Q1 = 100

10-yr index-linked gilt rate 1965Q1 = 100; Series break 1992Q4

Total Market Returns

- 16 -

Figure 3.2: Scatter plot of GDP growth versus gilt rate (raw values)

Source: Europe Economics calculations

We focus on ten-year index-linked gilt yields and growth rates here. Five-year gilt yields can be

significantly affected by policy expectations — e.g. in a recession policy interest rates may be set low,

dragging down the five-year gilt yield. Since our data begins only in 1985, the use of twenty-year

values would make our dataset very short (just five years instead of fifteen). However, we

acknowledge that there is a compromise here. The actual growth rate could, in principle, deviate

materially from the underlying sustainable growth rate even over a ten-year horizon. For example,

one interpretation of our non-break-adjusted series could be that actual growth rates were below

sustainable growth rates during the 1980s but then above sustainable growth rates during the 1990s

(perhaps “catching up” on the “lost growth” of the 1980s). One implication of this reflection is that

it is not obvious, despite the higher correlation, that our break-adjusted series is really the better

series for correlating to ten-year-ahead growth rates.

3.1.3 Predictions of model

These caveats notwithstanding, the upshot of our analysis is that the close relationship that theory

predicts between the risk-free rate and the sustainable growth rate appears to be borne out in

practice. The sustainable growth rate of the economy appears to have been fairly stable from the

mid to late 1980s, risen somewhat in the early 1990s, and fallen fairly rapidly from the second

quarter of 1997 to below its late 1980s trough.

In the following graph, using the correlation between the break-adjusted series for the index-linked

gilt rate and the sustainable growth rate to model the sustainable growth rate, we assume the

Total Market Returns

- 17 -

sustainable growth rate was 2.5 per cent at the start of 1985 and that changes in the risk-free rate

and sustainable growth rates are proportionate to one another.8

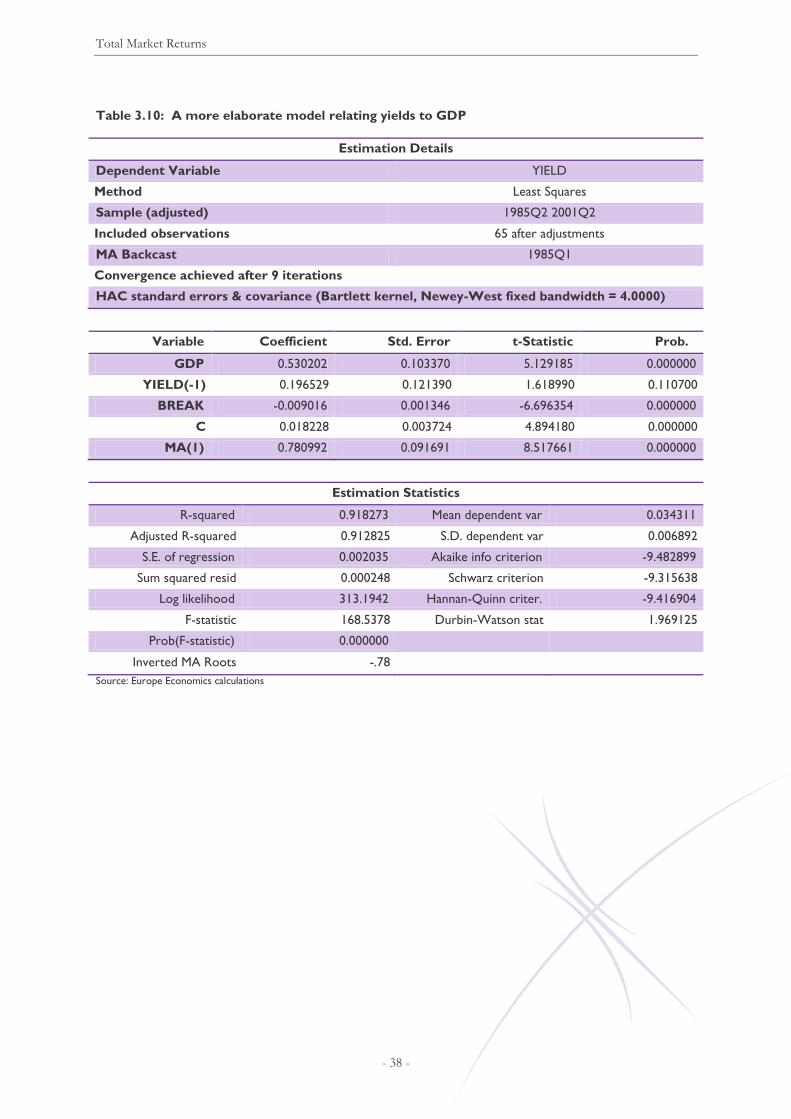

8 Our model, explains yields by a constant, the change in regime occurring in 1992Q3, and GDP, as set out in the

following table. A more elaborate version of the model (which confirms the presence of a statistically significant

correlation between yields and GDP) and additional statistical tests are provided in Appendix B to this section.

Estimation Details

Dependent Variable YIELD

Method Least Squares

Sample 1985Q1 2001Q2

Included observations 66

HAC standard errors & covariance (Bartlett kernel, Newey-West fixed bandwidth = 4.0000)

Variable Coefficient Standard Error t-Statistic Prob.

GDP 0.725478 0.095041 7.633279 0.000000

BREAK -0.01073 0.000983 -10.91737 0.000000

C 0.020568 0.002454 8.380193 0.000000

Estimation Statistics

R-squared 0.840297 Mean dependent var 0.034323

Adjusted R-squared 0.835227 S.D. dependent var 0.006840

S.E. of regression 0.002776 Akaike info criterion -8.890969

Sum squared resid 0.000486 Schwarz criterion -8.791439

Log likelihood 296.402 Hannan-Quinn criter. -8.85164

F-statistic 165.7408 Durbin-Watson stat 0.733382

Prob(F-statistic) 0.000000

Technically, this is a model of levels. In the model represented in Figure 3.3, we assume that the sustainable growth

rate in 1985Q1 is equal to the actual 10-year growth rate for the next ten years ahead (2.50 per cent, versus a value

of 2.0 generated by the model in the table). Changes in the level of yields from our model then constitute changes in

the level of yields from this 2.50 per cent startpoint. The effect is that the levels in the model represented in Figure

3.3 are around 0.5 per cent above those generated from the model in the table. For this reason the modelled

sustainable growth rate in Figure 3.3 is described as “Normalised”.

Total Market Returns

- 18 -

Figure 3.3: Modelled sustainable growth rate versus gilts yield

Source: Europe Economics calculations

So, according to our model, the sustainable growth rate peaked at about 4 per cent in the mid-

1990s, and had fallen to about 2 per cent by the end of 2000. The rate continues around 2 per cent

until 2002, when it starts falling again. There is a brief odd blip up in mid-2007, and then the spike in

late 2008 (which surely reflects a sudden rise in sovereign default risk – i.e. the model is breaking

down as the index-linked gilt yield is no longer nearly-risk-free). From the first quarter of 2009 we

also get a downward distortion, as quantitative easing is estimated by the Bank of England to take

perhaps 150 basis points off yields.

So we have some distortions from late 2008 that make it difficult to guess what happened next. In its

Bristol Water judgement, the Competition Commission proposes a range of 1-2 per cent for the

risk-free rate, implying, on our model, a sustainable growth rate of 1.35-2.07 per cent.

3.2 The Sustainable Growth Rate (and hence Risk-Free Rate) is Likely

to Increase during the Price Control Period

The government Office for Budget Responsibility estimates that the economy’s sustainable growth

rate is 0.5 per cent for 2012, and will rise to around 2.2 per cent (which would imply a risk-free rate

of 2.2 per cent) by 2016.9

We consider it plausible — indeed, likely — that the sustainable growth rate could return to these

levels during the next few years, perhaps even exceeding 2.2 per cent by the middle of the price

control period. That is not, of course, to say that we predict average economic growth might be

well above 2 per cent during the next few years or even over the 2010s as a whole — as we say, the

9 See, for example, Table 3.1 p42 Economic and Fiscal Outlook, December 2012, Office for Budget

Responsibility http://cdn.budgetresponsibility.independent.gov.uk/December-2012-Economic-and-fiscal-

outlook23423423.pdf. The OBR considers the long-term figure to be 2.3 per cent.

Total Market Returns

- 19 -

risk-free rate data imply an underlying growth rate averaging perhaps only around 1 per cent.10

Rather, we believe it plausible that, within the next few years, the average growth rate for the next

ten years or so after that point could be in the region of (or perhaps even higher than) the 2.2 per

cent the government proposes. We present this thought in a stylised way in the figure below. It

should be clear that if the actual growth-rate is low enough in 2013-17 or high enough in 2023-27,

then it is possible for the average growth rate of 2013-23 to be markedly below the average growth

rate of 2017-27.

Figure 3.4: Stylised representation of our contention concerning sustainable growth rates

3.2.1 Longer-term gilt rates imply a significant rise in ten-year yields by late 2016

The claim that the risk-free rate should be expected to increase over the next five years (to the mid-

point of the price control) is also supported by the term structure of bonds. The term structure of

yields on index-linked government bonds can be used to infer forward real yields. In particular, it is

possible to lock in the interest paid for borrowing and lending money in the future.

Given current interest rates it is possible to receive one pound at time t by investing the amount

, where t is the number of years from 0 to t and the annualised interest rate at time 0 for

borrowing over the period 0 to t. This can be financed by borrowing the amount over the

period from 0 to t+s.

The total amount of interest that is paid for borrowing one pound over the period t to t+s is

. This implies that at time 0 the forward interest rate for t to t+s equals

.

10 Of course, if there is an “output gap”, then in addition to the underlying trend rate of growth, the economy

might have the capacity to “catch up”, also, growing faster than its trend rate.

Total Market Returns

- 20 -

At 30th November 2012, the real implied ten-year-ahead yield on indexed linked UK gilts was –0.7

per cent.11 But the implied yield for the ten years from November 2017 was 0.37 per cent — a rise

of more than one percentage point in the ten-year yield over the next five years. In the most recent

regulatory determination available at the time of writing — that of Ofcom — the risk-free rate was

determined at 1.4 per cent (despite the very low rates on contemporaneous ten-year gilt yields) for

a charge control applying in the period up to 31 March 2014.12 An implied rise of one percentage

point in yields, during the period February 2017-2027 versus the period November 2012-2022,

could be expected to imply a roughly equivalent rise in the risk-free rate.13

Figure 3.5: Implied Ten-Year Forward Yields at November 2012

Source: Europe Economics calculations based on Bank of England data

Some of this expected rise in yields may already be implicit in Ofcom’s determination of a risk-free

rate notably above contemporaneous ten-year yields. And it is also true that gilt yields are known

to have a term structure that is only imperfectly understood. However, we make the following

observations:

Though a positive slope to the yield curve is normal, on government bonds the standard rise

from around a 10 to a 20 years horizon is of the order of 10-20 basis points. The curve typically

flattens considerably after around eight years. In blue in the following figure we see the yield

curve for UK gilts for July 2003. Between 10 and 30 years there is a 32 basis points difference.

11 Source: Bank of England 12 http://stakeholders.ofcom.org.uk/binaries/consultations/823069/statement/statement.pdf 13 We note that Bank of England interventions via Quantitative Easing had the aim of lowering long term gilt

yields, implying that these interventions had the effect of flattening the curve. This raises the possibility that

the steepness of the curve shown in Figure 3.5 understates the underlying steepness.

Total Market Returns

- 21 -

Figure 3.6: Yield curves for July 2003 and July 2012

Source: yieldcurve.com

By contrast, in red in the figure we present the same curve for July 2012. We note that the rise

in yields across the curve is considerably more and over a longer timescale than can usually be

attributed to pure policy choice effects (e.g. decisions to keep interest rates low in the short

term to smooth out economic fluctuations such as recession). An above-100 basis point rise in

the 6 to 16 year phase (and indeed extended beyond that, even still rising materially to 30 years)

indicates a significant and unusual effect. It is possible that some element of this is a rise in

liquidity premia, but it seems very likely that the overwhelming majority of this effect reflects an

expectation that ten-year yields will be much higher by 2017 than those yields are today.

The common belief that index-linked gilt yields will, in due course, rise applies to longer-term

yields as well as to ten-year yields.

Though the Competition Commission has raised concerns about twenty-year yields in past

judgements, its view was that these were likely to be distorted downwards, not upwards.14

3.3 Why the Sustainable Growth Rate is Likely to Increase

We observe that a figure of 2.2 per cent for the sustainable growth rate would, on our models,

imply a risk-free rate of about 2.2 per cent — slightly above the top of the range recommended by

the Competition Commission in its Bristol Water judgement. Thus, one way of expressing our

claim is that although, recently, the risk-free rate may have lain around the middle of the CC’s

Bristol Water range (as reflected in, for example, the 2011 Ofcom judgement), there is reason to

believe that over the next few years it could rise towards (or even above) the top of that range, as

the sustainable growth rate of the economy rises.

14 See, for example, paragraph 70 in

http://www.competition-commission.org.uk/rep_pub/reports/2010/fulltext/558_appendices.pdf

Total Market Returns

- 22 -

Is it credible that the long-term sustainable growth rate might rise in the way implied by longer-term

gilt yields, perhaps reaching the 2.2 per cent claimed by the government or even, thereafter, rising

higher, perhaps to the 2.5 per cent or so that has been the UK’s longer-term historic average? We

point to six key factors that suggest it might be:

Reduced public spending / taxation relative to GDP

A reduction in the level of government debt relative to GDP

A reduction in corporate sector debt relative to GDP

A reduction in household debt relative to GDP, and an end to the financial crisis

Extension to the retirement age

An increase in the rate of productivity growth in the public sector

We shall now consider each of these cases in turn. We emphasize that in each case what we

propose is that a relevant factor has arisen in recent years that would tend to depress the rate of

overall economic growth for long enough to cover an entire investment cycle — and thus, in the

economist’s sense of “long term” affect the long-term sustainable growth rate — but that can

reasonably be expected (as indicated in both longer-term gilt yields and official economic forecasts)

to be at-least-partially reversed by the middle of the price control period, at least in terms of its

effects upon the growth rate for the ten years ahead from that point.

3.3.1 Reduced public spending relative to GDP

There is extensive academic empirical literature on the relationship between levels of public

spending, tax and GDP growth. Broadly stated, the conclusion of this literature is that at above

about 25 per cent of GDP, increasing public spending further reduces the long-term growth rate of

the economy (especially if such increases take the form of greater government consumption

expenditure, as opposed to investment expenditure or transfers).

We emphasize that it does not, of course, follow that it would be politically desirable only to spend

25 per cent of GDP. After all, the extra spending produces potentially socially desirable outputs,

such as ameliorating poverty, ill-health or poor education, enhancing social inclusion, enabling the

government to project military force around the world allowing the nation to diffuse its values and

fight injustice, and many other such things. Perhaps at some level of GDP spend, the reduction in

growth is of greater social cost than the social benefits of the extra spending (so then there would

be three zones — one in which additional spending enhanced growth, one in which spending

reduced growth but was still desirable because the trade-off was favourable, and a zone in which

further spending increases reduced growth and did not produce social benefits of greater value than

the cost of such growth reduction). In this report we make no comment on these essentially

political questions.

Instead, for our purposes here we focus on the well-established and long-established empirical

results concerning public spending, taxation and growth rates.

Regarding the impact of public spending, two particularly important recent studies are the following:

Afonso, A. & Furceri D. (January 2008), "Government size, composition, volatility, and economic

growth", European Central Bank working paper 849: “a percentage point increase in the share of total

revenue (total expenditure) would decrease output by 0.12 and 0.13 percentage points respectively for

the OECD and for the EU countries”

Total Market Returns

- 23 -

Mo, P.H. (2007), "Government expenditure and economic growth: the supply and demand sides", Fiscal

Studies 28 (4), pp497-522: “a 1 percentage point increase in the share of government consumption in

GDP reduces the equilibrium GDP growth rate by 0.216 percentage points”

The literature on the impacts of taxation gives similar results. The definitive study in that literature

was that of Leibfritz, W., Thornton, J. & Bibbee A., “Taxation and Economic Performance” OECD

Economics Department Working Papers 176 (1997). They find that a 10 percentage point increase

in the tax to GDP ratio reduces the growth rate by 0.5 – 2 percentage points — or equivalently that

each additional percentage point reduces the growth rate by 0.05-0.2 percentage points. (The more

recent Afonso & Furceri paper quoted above finds that a one percentage point increase in the share

of tax in GDP reduces growth by 0.12 percentage points.)

The practitioner rule of thumb here is that each additional percentage point rise in sustained levels

of public spending/tax should be expected to take 0.1-0.15 per cent off the growth rate of the

economy.

Total managed expenditure in the UK reached a trough of 36.3 per cent of GDP in financial year

1999/2000.15 This was the lowest figure recorded since straightforwardly comparable records began

in the early 1960s. It peaked at 47.6 per cent in 2009/10 — a rise of 11.3 percentage points over a

decade.

Had such a level of expenditure been maintained, with taxes raised to match it, the rate of GDP

growth could be expected to be reduced as a consequence. However, the government plans to

reduce spending back to 40.5 per cent by 2015/16 and 39.0 per cent in 2016/7. If, for the ten years

following that point, spending were maintained at around 40 per cent of GDP, the sustainable

growth rate could be expected to be materially higher than during the high-public-spending period of

2008/9-2014/15, which is projected to involve an average level of around 45 per cent of GDP. If we

assume that taxes would have to be set on average no more than three per cent below spending

(e.g. according to the Maastricht sustainability criteria), a five percentage point reduction in long-

term spending relative to GDP would imply around a five percentage point reduction in taxes. At

the Leibfritz et al. figure of 0.05-0.2 percentage points off growth for each percentage extra taxes, a

five percentage point reduction in long-term tax rates implies a 0.25-1 per cent rise in sustainable

growth rates.

To see whether a sustained cut in average long-term spending on this scale is plausible, we note that

public spending was 40.9 per cent of GDP in 2007 and the ten-year average was below 42 per cent

of GDP for every ten-year period commencing each year between 1985/6 and 2001/2. It thus seems

entirely plausible that public spending will be materially lower, relative to GDP, from 2017-on than

has been the case in recent years.

3.3.2 A reduction in the level of government debt relative to GDP

In their August 2011 Bank for International Settlements paper, Cecchetti et al.16 analyse the impact

of various forms of debt upon growth rates. Their conclusions are that, beyond a threshold level,

debt is damaging to growth. That threshold level in respect of government debt is around 85 per

cent of GDP.

15 Source: Public Finances Databank, March 2012 version: http://www.hm-

treasury.gov.uk/d/public_finances_databank.xls 16 Cecchetti, S.G., Mohanty, M.S. & Zampolli, F. (2011), “The real effects of debt”, prepared for the “Achieving

Maximum Long-Run Growth” symposium sponsored by the Federal Reserve Bank of Kansas City, Jackson

Hole, Wyoming, 25–27 August 2011 —

http://www.kc.frb.org/publicat/sympos/2011/2011.Cecchetti.paper.pdf

Total Market Returns

- 24 -

On UK government definitions, UK general government gross debt relative to GDP is projected to

peak at 97.4 per cent of GDP in 2015/16, falling to 94.4 per cent of GDP by 2017/18.17 This

compares with 37.0 per cent in 2001/2. The average from 1990/1 to 1999/2000 was 44.1 per cent.

The previous peak on straightforwardly comparable statistics was 64.2 per cent in 1976/7. On

Cecchetti et al.’s definitions, public sector debt rose from 42 per cent of GDP in 1990 to 54 per

cent in 2000 and 89 per cent in 2010.

Cecchetti et al. find that an additional ten percentage points of GDP of debt, above the threshold,

reduces annual trend growth by around 0.1 percentage points. Although the UK’s debt level will be

above the threshold, the government’s plans to reduce debt relative to GDP could take debt closer

towards the threshold level, mitigating its damaging effect and thereby increasing growth.

3.3.3 A reduction in corporate sector debt relative to GDP

On Cecchetti et al.’s figures, UK corporate sector debt rose from 93 per cent of GDP in 2000 to

126 per cent in 2010. The threshold level for corporate sector debt, above which it reduces trend

growth, is about 90 per cent of GDP. Each additional ten percentage points of debt above this level

reduces trend growth by around 0.05 per cent. So being 30 per cent above the threshold would be

expected to reduce trend growth by around 0.15 per cent.

The UK corporate sector has already materially deleveraged during the recession. It is natural to

expect further deleveraging over the next five years, as, relative to 2005-7, corporate debt spreads

have risen dramatically increasing the relative attractiveness of equity versus debt.

If corporate sector debt were to return to its 2000 level by around the middle of the price control

period, that could therefore be expected to add a further 0.15 percentage points to trend growth.

3.3.4 A reduction in household debt relative to GDP, and an end to the financial

crisis

Cecchetti et al. believe that there should be a similar threshold level for household debt, similar to

that applying for government and corporate sector debt. They state that their best guess as to this

level is around 85 per cent of GDP. However, it should be noted that in their statistical tests,

though 84 per cent was their models’ highest likelihood value for the threshold, the results were far

from statistically significant.

A related possibility, which Cecchetti et al. did not (directly) explore, is that household debt has its

effect upon growth primarily through increasing the likelihood of financial crises. Banking sector

crises have a huge effect in their model: each additional year of crisis takes 0.27 percentage points off

annual growth for the succeeding five years.

UK household debt rose from 75 per cent of GDP in 2000 to 106 per cent in 2010. However,

household debt in the UK has been falling back since its 2007 peak.18 Further falls by 2015/16 could

take it below growth-damaging levels, reducing the risk of further financial crises and reducing the

growth-depressing debt overhang.

17 Source: Public Finances Databank, December 2012 version: http://www.hm-

treasury.gov.uk/d/public_finances_databank.xls 18 Source: Household Indebtedness in the EU, Report prepared by Europe Economics for the European

Parliament’s CRIS committee, April 2010.

Total Market Returns

- 25 -

3.3.5 Extension to the retirement age

In the Cecchetti et al. model, a one standard deviation increase in the dependency ratio (the ratio of

the non-working to working population), or an increase of around 3.5 percentage points in that

ratio, is associated with a 0.6 percentage point reduction in future average annual growth.

Dependency ratios in the UK have been projected to rise significantly. The number of people of

state pensionable age was projected, by the government in 200919, to increase by 32 per cent from

11.8m in 2008 to 15.6m by 2033, whilst the number of working age is projected to rise by just 14

per cent from 38.1m to 43.3m.

Subsequently, the government has announced plans to accelerate rises in the state pension age —

reaching 66 in 2020 instead of between 2024 and 2026 as previously planned.20 It seems plausible

that announcements of further subsequent increases in pension ages will follow by 2015/16, reducing

peak dependency ratios from those currently projected.

3.3.6 An increase in the rate of productivity growth in the public sector

From 1998 to 2007 average annual public sector productivity growth was 0.3 per cent, whilst for the

private sector it was 2.3 per cent.21 It is perhaps natural that in a period in which public spending

rose rapidly, it was difficult to absorb large increases in spending whilst also increasing productivity.

With government consumption constituting around 22 per cent of GDP, if the value of outputs over

inputs grew 1 per cent more rapidly from 2015/16 onwards than in 1998-2007 — plausible given the

tighter spending growth, and the opportunity to catch up on private sector productivity growth as

the spending rises of 1998 to 2007 are finally adapted to — then that could add around 0.2 per cent

to GDP growth.

We observe because of the ways in which GDP is measured, increased productivity growth in the

public sector might not lead to rises in measured GDP growth on anything like this scale. However,

of course, gilt rates reflect the true underlying economic situation, not simply that measured.

3.3.7 Intermediate conclusion on the scope for a rise in the sustainable growth

rate

If all achieved together, the potential impacts we have described could be very large.

0.25-1 per cent for reductions in the long-term trend tax rate

A material impact from the reduction in government debt

0.15 per cent for the reduction in corporate indebtedness

An unclear amount for the reduction in household indebtedness

Some material amount for the reduction in the increase in dependency ratios

Perhaps 0.2 per cent for increased productivity growth in the public sector

All told, these values sum to more than 0.6-1.4 additional percentage points of average growth.

Perhaps it is ambitious to believe that the top end of this range could really be achieved in practice,

19 http://www.ons.gov.uk/ons/rel/npp/national-population-projections/2008-based-projections/statistical-

bulletin-october-2009.pdf 20 http://www.dwp.gov.uk/consultations/2010/spa-66-review.shtml 21 See Basset D., Cawston T., Haldenby A., and Parsons, L. (April 2010), Public sector productivity, Reform

Total Market Returns

- 26 -

and without any offsetting other factors reducing sustainable growth. Nonetheless, we contend that

the factors above do suggest that the government’s own projections could be credible by the middle

of the next price control period. That is to say, by the middle of the next price control period, it is

not totally unreasonable to believe that the sustainable growth rate for the UK economy could have

returned from the recent very low values implied by risk-free rates (perhaps as low as 1 per cent,