heat exchanger(final project) by hussain

TRANSCRIPT

2012Report on financial viability for installation of new heat exchanger in rfo (reduced fuel oil) at delayed coking unit of guwahati refinery

Presented By : Hussain Mustafa Azad

MBA 3rd Semester.

Jawarharlal Nehru School Of Management Studies.

Assam University

Indian oil Corporation LtdGuwahati Refinery Noonmati.

TABLE OF CONTENTS

SL. NO. PARTICULARS PAGE NO.

PREFACE 5

ACKNOWLEDGEMENT 6

STUDENT DECLARATION 7

EXECUTIVE SUMMARY 8

1.1IOCL

Brief introduction of IOCL,Guwahati Refinery 9

Aims & Objectives 12-13

Indian Oil Corporate History 14-15

Vision,Mission,Objectives & Obligation 16-19

Board Of Directors 20-21

Organistion Structure 22-23

Business Chart of IOCL 24

Divisions 25-30

Major Petroleum products 32-33

Performance Review 34-36

SWOT analysis 37-38

1.2Under IOCL, GUWAHATI REFINERY

Classification Of Capital Budget 39-45

Finance Department 46-49

A report by-Hussain Mustafa Azad,JNSMS Page 2

Function of Finance Department 50-57

Achievement of Finance Department 58-59

Development Report 2010-11 60-61

Implementation Of ERP-SAP 62-65

1.3Project Analysis

Project Finance under IOCL 66

Project Evaluation under IOCL 67

Capital Projects in IOCL 68

Clean Development Mechanism under IOCL 69

Name Of The Proposal & Desciption 70

Cost Estimate 72

Justification of the Proposal 72

Advantage 73

Technical Feasibility 73

Impact of Proposal on Manpower 74

Operating & Maintance Cost 74

Economies 75

Completion Schedule 77

Project Selection Criteria 79-82

Calculation 83-91

Conclusion 93

Bibliography 94

A report by-Hussain Mustafa Azad,JNSMS Page 3

PREFACE

In today’s era of globalization and competition, coping up with

technological advancement, which is undergoing evolution at a very fast

A report by-Hussain Mustafa Azad,JNSMS Page 4

rate, holds the key to the survival and growth of any organization. Installing

technology, well-equipped facilities or going for modification in the existing

ones are the means to attain better performance efficiency and hence

further the value addition.

Indian Oil, the largest commercial enterprise of India (by sales turnover)

is India’s sole representative in Fortunes prestigious listing of world’s 500

largest corporations, ranked 105th for the year 2009. To maintain strategic

edge in the market place, Indian Oil has given importance to capital

budgeting because capital investment decisions often represent the most

important decisions taken by an organization, and they are extremely

important, they sometimes also pose difficulties.

A company in practice should take all care in selecting a method or

methods of investment evaluation. The criterion selected should be a true

measure of the investment’s profitability (in terms of cash flows), and it

should lead to the net increase in the company’s wealth (that is, its benefits

should exceed its cost adjusted for time value and risk). It should also be

seen that the evaluation criteria do not discriminate between the investment

proposals. They should be capable of ranking projects correctly in terms of

profitability. The NPV method is theoretically the most desirable criterion as

it is a true measure of profitability; it generally ranks projects correctly and is

consistent with the wealth maximization criterion.

ACKNOWLEDGEMENT

A report by-Hussain Mustafa Azad,JNSMS Page 5

This training part of MBA programme taught me a lot to understand the

key of success in the organization. One of them is teamwork. Teamwork is

ability to work together towards a common vision. It is a fuel that allows

common people to attain results. Therefore, I would like to thank all

management team of Indian Oil Corporation Limited who help me to

achieve this result.

I would hereby like to extend my gratitude to the following people

without whose cooperation and help at every stage, successful completion of

the project would not have been possible.

It is my privilege to express my deep gratitude to Mr. G.K.Arora (CFM

at IOCL) who gave me such a great opportunity & infrastructure to do this

project and also for his kind cooperation & help throughout the project.

I would like to express my profound gratitude & a sincere thanks to Mr.

Ritesh Agarwal (ACO, Main Account), Mr. Abhishekh Maurya (ACO)

and Mr. Sushil Shil for their valuable time & educative guidance. Their

constant support, innovative ideas & practical approach helped me to make

the project more objective.

I would like to use this opportunity to thank my institution guide Mrs.

Lurai Rongmai(Assistant Professor,JNSMS) for her constant guide and

support.

Last but not the least, I would like to thank all others who directly or

indirectly helped me in this regard.

A report by-Hussain Mustafa Azad,JNSMS Page 6

STUDENT DECLARATION

I hereby declare that the project report entitled, “Report on Financial viability for installation of New Heat Exchanger in RFO (Reduced Fuel Oil) at Delayed Coking Unit of Guwahati Refinery” as per requirement of the MASTER OF BUSINESS ADMINISTRATION AT ASSAM UNIVERSITY is my original work prepared on individual effort based on the data provided by the Finance Department and Technical Service Department of Guwahati Refinery.

Place HUSSAIN MUSTAFA

AZAD

Date: MBA

3rd Semester

Jawarharlal Nehru School Of

Management Studies.

A report by-Hussain Mustafa Azad,JNSMS Page 7

A report by-Hussain Mustafa Azad,JNSMS Page 8

EXECUTIVE SUMMARY

Project Title: To provide a brief overview of the organization and working of

Guwahati Refinery and determine the financial viability for installation of the New

Heat Exchanger In RFO (Reduced Fuel Oil) for Heat Recovery at Delayed Coking

of Guwahati Refinery.

Organization: Guwahati Refinery, Indian Oil Corporation Limited.

Organizational Guide: Mr Ritesh Agarwala (ACO, MAIN ACCOUNT)

Institution Guide: Mrs. Lurai Rongmai(Assistant Professor,JNSMS)

Duration of the project: 17th May to 30th July, 2012.

Objective of the study: To study the functioning of the different sections of the Finance Department of Guwahati Refinery and to determine the financial viability for installation of Heat Exchanger in RFO of Guwahati Refinery as an initiative towards CDM (Clean Development Mechanism) Projects.

Research Methodology: The Research carried out is a Descriptive study including mostly the secondary data. The data are analyzed using the various Capital Budgeting techniques. The data has been collected from the Finance and the Projects Department of Guwahati Refinery.

A report by-Hussain Mustafa Azad,JNSMS Page 9

INTRODUCTION

Brief introduction: GUWAHATI REFINERY:

The Guwahati Refinery in North East India -- the first Public Sector refinery of the country -- was commissioned in 1962 with a capacity of 0.75 MMTPA which was subsequently increased to 1.0 MMTPA through debottlenecking projects. The refinery processes only indigenous crude oil from the Assam oil fields. With its main secondary unit, a coking unit, it produces middle distillates from heavy ends and supplies petroleum products to North-Eastern India, and surplus products onward to Siliguri in West Bengal in 2003. Hydrotreater Unit for improving the quality of diesel has been commissioned in 2002. In 2003, the refinery installed an Indmax Unit, a novel technology developed by Indianoil's R&D Centre for upgrading heavy ends into LPG, Motor Spirit and Diesel oil.

Beginning of Petroleum Refining in India

• In 1881, Assam Railway & Trading co. began laying of tracks in Assam They used elephants in place of cranes.

• One day, one of the elephants wandered away, to come back with its feet smeared by slimy oil. Backtracking led to the discovery of oil in Borbhil, near present day Digboi

• A Canadian driller, Willey Leove shouted at native boys, “Dig boy dig”. Oil was struck and the name ‘Digboi’ stuck.

• Digboi became the birth place of India’s oil industry.

A report by-Hussain Mustafa Azad,JNSMS Page 10

• In 1890s, crude oil distillated at Margherita, 16 km away from Digboi, in cast iron pans, called ‘Stills’.

• Digboi Refinery of Assam Oil Company (AOC) was commissioned at its present location in 1901 with 500 Barrels per day capacity.

• AOC nationalized and its Refining and Marketing functions merged with IOC in October, 1981.

• Digboi refinery is the oldest running refinery in the world.

In 1890s Crude Oil used to be distilled in DIGBOI in Cast Iron pans – called ‘Stills’. Bottom portion of one such still of 9 feet diameter is still kept at Digboi Refinery.

Indian Oil Corporation Limited:

Date of Incorporation: 1st September 1964.

Type of Company:

Government Company under Section 617 of the Companies Act, 1956.

Administrative Minister:

Ministry of Petroleum & Natural Gas, Government of India.

Share Capital:

i)Authorized: Rs.6000.00croresii) Subscribed, issued & paid-up: Rs.2427.95 crores.

A report by-Hussain Mustafa Azad,JNSMS Page 11

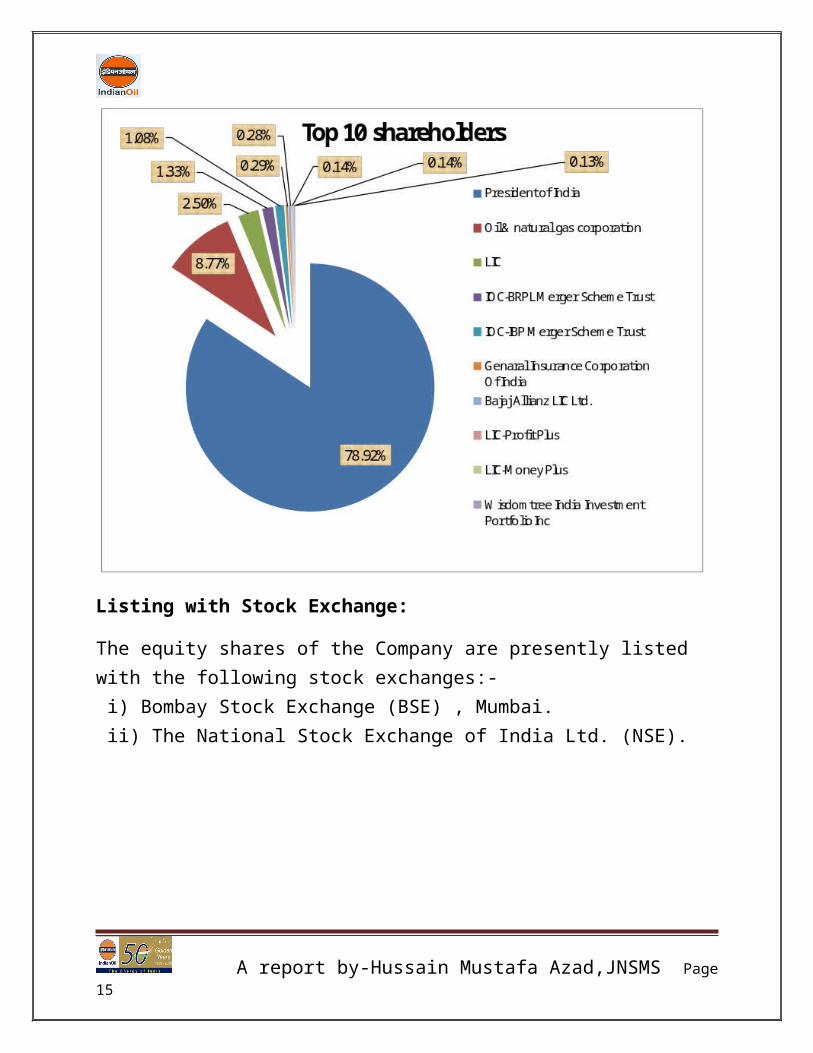

Share Holding Pattern as on 31 st March 2011:

Listing with Stock Exchange:

The equity shares of the Company are presently listed with the following stock exchanges:- i) Bombay Stock Exchange (BSE) , Mumbai. ii) The National Stock Exchange of India Ltd. (NSE).

A report by-Hussain Mustafa Azad,JNSMS Page 12

AIMS AND OBJECTIVES

Any project work exposes the research scholar to the ground realities prevailing in the particular industry and thereby enables to carry out a meaningful realistic analysis.

The objectives of the project are as follows:-

• To provide a glimpse of Indian Oil Corporation Limited and of Guwahati

Refinery.

• To understand and describe the functioning of each sections of the Finance

Department of Guwahati Refinery.

• To determine the financial viability for installation of Heat Exchanger in

RFO (reduced fuel oil) rundown circuit of Guwahati Refinery leading to

reduce the energy consumption.

LIMITATIONS

The limitations of this study are as follows:-

The scope of the study is limited to the vicinity of Guwahati Refinery.

Time taken to complete the project work is very limited.

The primary data collected are assumed to be correct.

RESEARCH METHODOLOGY

The data collection is carried out mainly through personal interviews as well

as through the literature review from the relevant policy manuals as well as from

the various daily reports made by the Finance Department.

A report by-Hussain Mustafa Azad,JNSMS Page 13

SOURCES OF DATA:

For collecting necessary data two sources have been used. They are

primary data & secondary data.

a) PRIMARY DATA:

Face to face discussion with the Finance Manager, Training Department

personnel, Technical Department, Environment control, Finance Department

Personnel and the employees of Guwahati Refinery (a unit of IOCL).

b) SECONDARY DATA :

1. Data provided from the finance dept. regarding Cost of Investment, Cost of

Capital and other related information.

2. Journals and magazines published by I.O.C. Ltd.

3. Library: records and manuals.

4. Annual Report 2010-2011

5. Also through Company websites i.e.

www.iocl.com

6. Data collected from the Technical Service Department.

DATA ANALYSIS: The Research carried out is a Descriptive study including

mostly the secondary data. The data are analyzed using the various Capital

Budgeting techniques.

A report by-Hussain Mustafa Azad,JNSMS Page 14

Indian Oil Corporation-“The Energy of India”

Indian Oil Corporation Ltd. (Indian Oil) was formed in 1964 through the merger of Indian Oil Company Ltd. (Est. 1959) and Indian Refineries Ltd. (Est. 1958).

It is currently India's largest company by sales. Indian Oil is also the highest ranked Indian company in the prestigious Fortune 'Global 500' listing, at 105th position. It is also the 20th largest petroleum company in the world. Indian Oil and its subsidiaries account for 46.9% petroleum products market share in the industry, 40.4% national refining capacity and 67% downstream sector pipelines capacity.

The Indian Oil Group of companies owns and operates 10 of India’s 20 refineries with a combined refining capacity of 60.2 million tones per annum. These include one of the subsidiary refinery i.e. Chennai Petroleum Corporation Ltd. (CPCL). The Company’s cross-country crude oil and product pipelines network spanning over 9,300 km meets the vital energy needs of the country.

The Indian Oil Corporation Ltd. operates pipelines and refines imported as well as indigenous crude oil and markets petroleum products.

To maintain its competitive edge and leadership status, Indian Oil has invested Rs. 43,250 crore (US $10. 65 billion) during the XI Plan period (2007-12) in integration and diversification projects, besides refining and pipeline capacity augmentation, product quality upgradation and expansion of marketing infrastructure.

Indian Oil operates the largest and the widest network of petrol & diesel stations in the country, numbering around 16,455. It reaches Indane cooking gas to the doorsteps to over 46.4 million households in 2,709 markets through a network of 4,996 Indane distributors

Indian Oil's ISO-9002 certified Aviation Service commands a 63% market share in aviation fuel business, meeting the fuel needs of domestic and international flag carriers, private airlines and the Indian Defense Services. Indian Oil also enjoys a

A report by-Hussain Mustafa Azad,JNSMS Page 15

dominant share of the bulk consumer business, railways, and state transport undertakings, industrial, agricultural and marine sectors.

Indian Oil's world class R&D Centre is perhaps Asia's finest. Besides pioneering work in lubricants formulation, refinery processes, pipeline transportation and alternative fuels such as bio-diesel, the Centre is also the nodal agency of the Indian hydrocarbon sector for ushering in Hydrogen fuel in the country. Indian Oil joined the league of global technology providers in 2006-07 with its in-house developed IndMax technology selected for the 4 MMTPA Fluidized Catalytic Cracking (FCC) unit at the Corporation’s upcoming 15 MMTPA refinery-cum-petrochemicals complex at Paradip in Orissa, as well as for the FCC unit coming up at BRPL.

A report by-Hussain Mustafa Azad,JNSMS Page 16

Functions & duties

Indian Oil Corporation Ltd. has been established to carry out the objectives specified in the Memorandum & Articles of Association of the Company. The main activities of Indian Oil are refining, transporting and marketing of petroleum products.

A report by-Hussain Mustafa Azad,JNSMS Page 17

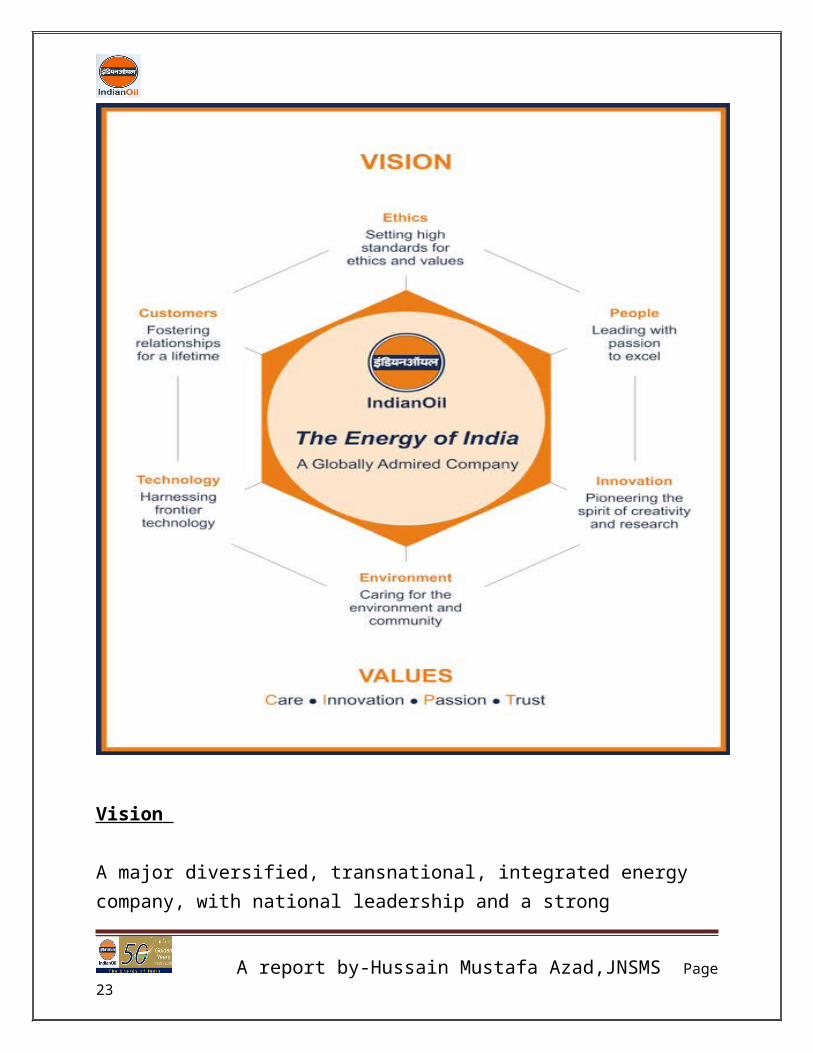

Vision

A major diversified, transnational, integrated energy company, with national leadership and a strong environment conscience, playing a national role in oil security & public distribution

Mission:

To achieve international standards of excellence in all aspects of energy and

diversified business with focus on customer delight through value of

products and services, and cost reduction.

To maximise creation of wealth, value and satisfaction for the stakeholders.

To attain leadership in developing, adopting and assimilating state-of- the-

art technology for competitive advantage.

To provide technology and services through sustained Research and

Development.

To foster a culture of participation and innovation for employee growth and

contribution.

To cultivate high standards of business ethics and Total Quality

Management for a strong corporate identity and brand equity.

To help enrich the quality of life of the community and preserve ecological

balance and heritage through a strong environment conscience.

Objectives:

To serve the national interests in oil and related sectors in accordance and

consistent with Government policies.

To ensure maintenance of continuous and smooth supplies of petroleum

products by way of crude oil refining, transportation and marketing activities

A report by-Hussain Mustafa Azad,JNSMS Page 18

and to provide appropriate assistance to consumers to conserve and use

petroleum products efficiently.

To enhance the country’s self-sufficiency in crude oil refining and build

expertise in laying of crude oil and petroleum product pipelines.

To further enhance marketing infrastructure and reseller network for

providing assured service to customers throughout the country.

To create a strong research & development base in refinery processes,

product formulations, pipeline transportation and alternative fuels with a

view to minimising/eliminating imports and to have next generation

products.

To optimise utilisation of refining capacity and maximise distillate yield and

gross refining margin.

To maximise utilisation of the existing facilities for improving efficiency

and increasing productivity.

To minimise fuel consumption and hydrocarbon loss in refineries and stock

loss in marketing operations to effect energy conservation.

To earn a reasonable rate of return on investment.

To avail of all viable opportunities, both national and global, arising out of

the Government of India’s policy of liberalisation and reforms.

To achieve higher growth through mergers, acquisitions, integration and

diversification by harnessing new business opportunities in oil exploration &

production, petrochemicals, natural gas and downstream opportunities

overseas.

To inculcate strong ‘core values’ among the employees and continuously

update skill sets for full exploitation of the new business opportunities.

A report by-Hussain Mustafa Azad,JNSMS Page 19

To develop operational synergies with subsidiaries and joint ventures and

continuously engage across the hydrocarbon value chain for the benefit of

society at large.

Obligations:

To provide prompt, courteous and efficient service and quality products at competitive prices:

1. Towards suppliers

To ensure prompt dealings with integrity, impartiality and courtesy and help promote ancillary industries.

2. Towards employees

To develop their capabilities and facilitate their advancement through

appropriate training and career planning.

To have fair dealings with recognised representatives of employees in

pursuance of healthy industrial relations practices and sound personnel

policies.

3. Towards community

To develop techno-economically viable and environment-friendly products.

To maintain the highest standards in respect of safety, environment

protection and occupational health at all production units.

4. Towards Defence Services

To maintain adequate supplies to Defence and other para-military services during normal as well as emergency situations.

A report by-Hussain Mustafa Azad,JNSMS Page 20

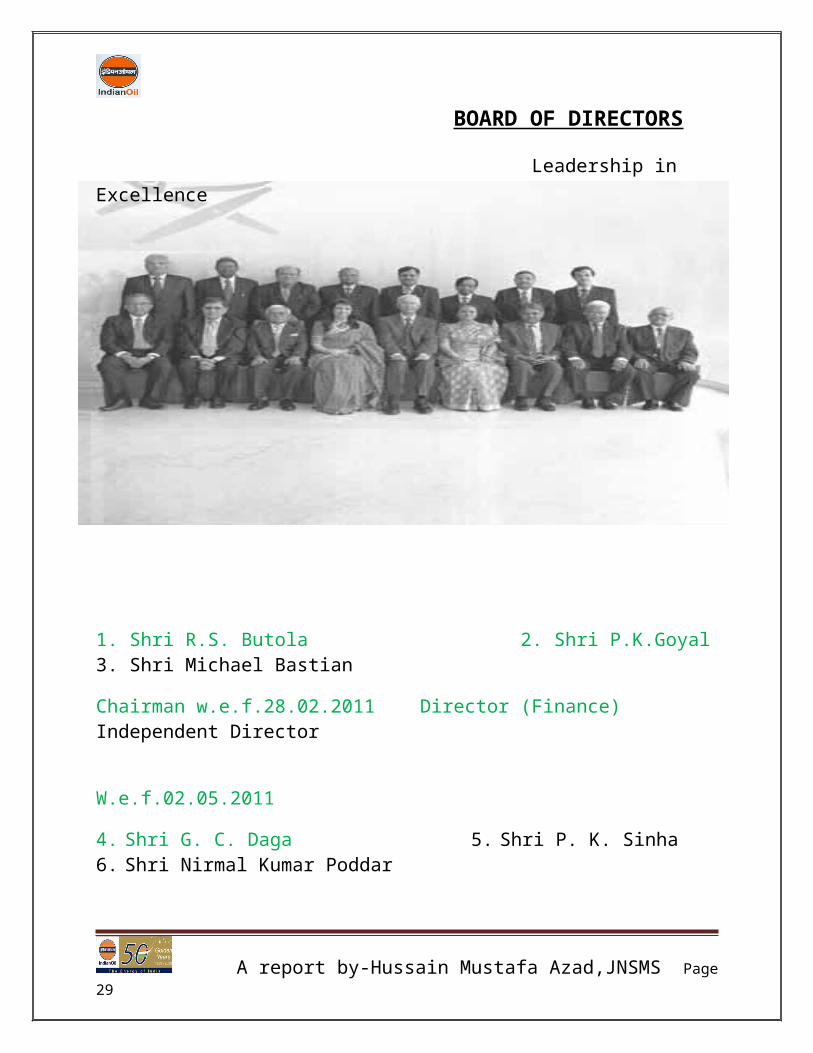

BOARD OF DIRECTORS

Leadership in Excellence

1. Shri R.S. Butola 2. Shri P.K.Goyal 3. Shri Michael Bastian

Chairman w.e.f.28.02.2011 Director (Finance) Independent Director

W.e.f.02.05.2011

4. Shri G. C. Daga 5. Shri P. K. Sinha 6. Shri Nirmal Kumar Poddar

Director (Marketing) Government Director Independent Director

7. Shri B. N. Bankapur 8. Shri Sudhir Bhargava 9. Dr. Sudhakar Rao

Director (Refineries) Government Director Independent Director w.e.f. 30.05.11 10. Shri K. K. Jha 11. Prof. (Dr.) Indira J. Parikh 12. Shri B. M. Bansal

Director (Pipelines) Independent Director Chairman & Director (P&BD)

A report by-Hussain Mustafa Azad,JNSMS Page 21

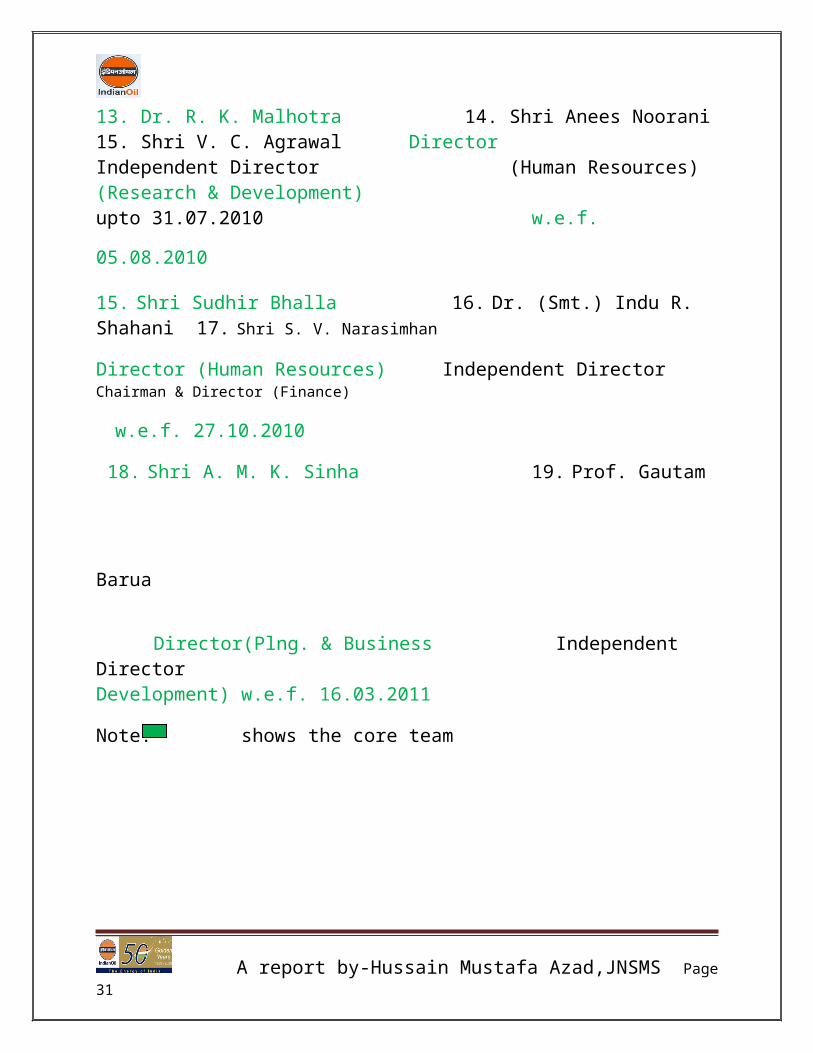

13. Dr. R. K. Malhotra 14. Shri Anees Noorani 15. Shri V. C. Agrawal Director Independent Director (Human Resources) (Research & Development) upto 31.07.2010

w.e.f. 05.08.2010 15. Shri Sudhir Bhalla 16. Dr. (Smt.) Indu R. Shahani 17. Shri S. V. Narasimhan

Director (Human Resources) Independent Director Chairman & Director (Finance)

w.e.f. 27.10.2010 18. Shri A. M. K. Sinha 19. Prof. Gautam Barua Director(Plng. & Business Independent DirectorDevelopment) w.e.f. 16.03.2011 Note: shows the core team

A report by-Hussain Mustafa Azad,JNSMS Page 22

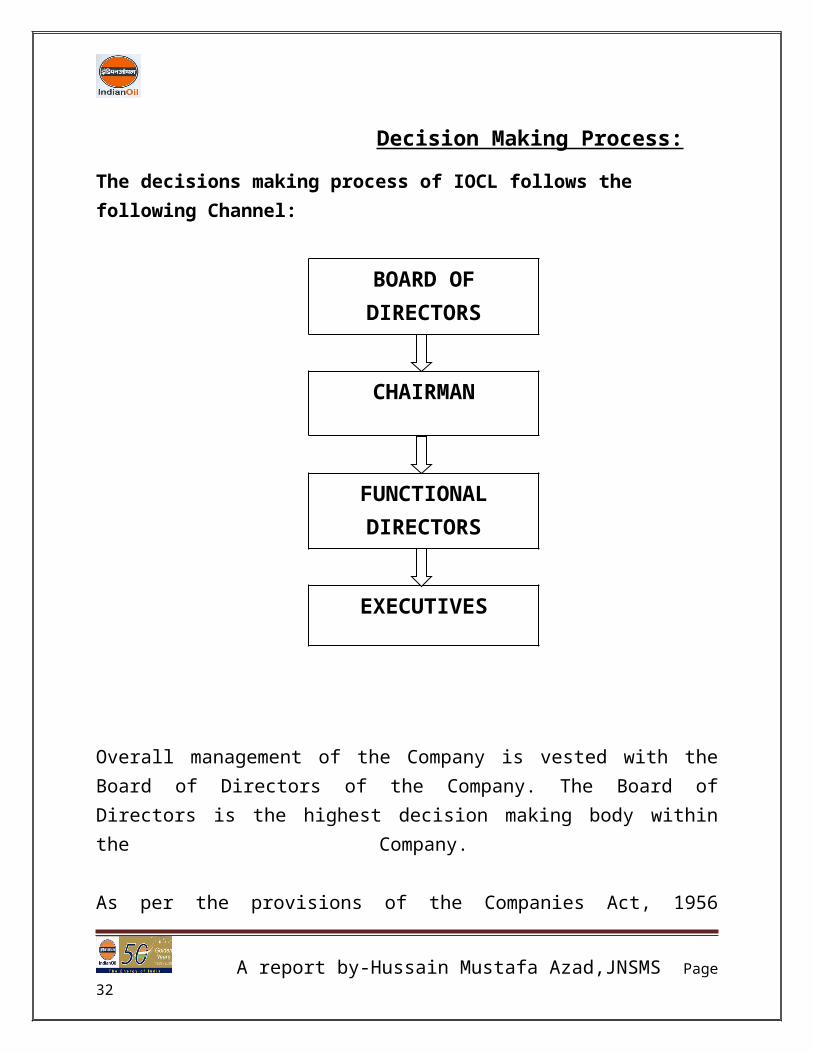

Decision Making Process:

The decisions making process of IOCL follows the following Channel:

Overall management of the Company is vested with the Board of Directors of the Company. The Board of Directors is the highest decision making body within the Company.

As per the provisions of the Companies Act, 1956 certain matters require the approval of the shareholders of the Company in General Meeting. The Board of Directors is accountable to the shareholders of the Company, which is the ultimate authority of a Company. Indian Oil being a Public Sector Enterprise (PSE) ,the Board of Directors of the Company is also accountable to Government of_India.

The day-to-day management of the Company is entrusted on the Chairman and the

A report by-Hussain Mustafa Azad,JNSMS Page 23

BOARD OF DIRECTORS

CHAIRMAN

FUNCTIONAL DIRECTORS

EXECUTIVES

Functional Directors and other Officers of the Company. The Board of Directors has delegated powers to the Chairman, Functional Directors, who have in turn delegated powers to the Executives of the Company through Delegation of Powers. The Chairman, Functional Directors and other officers exercise their decision-making powers as per this delegation of powers.

The Chairman, Functional Directors and other Executives are accountable to Board of Directors for proper discharge of their duties & responsibilities.

The powers, which are not delegated are exercised by the Board of Directors subject to the restrictions and provisions of the Companies Act, 1956.

A report by-Hussain Mustafa Azad,JNSMS Page 24

ORGANISATION SET-UP:

Refineries(including AOD’s Digboi Refinery)

Pipelines

Marketing (including AOD’s Marketing)

R&D

BOARD OF DIRECTORS

Divisional Set-up

Finance

Human Resource

Planning & Business Development

Corporate Set-up

Business Chart of IOCL

IOCL has its presence in all spheres of downstream operations.

A report by-Hussain Mustafa Azad,JNSMS Page 25

Major Division

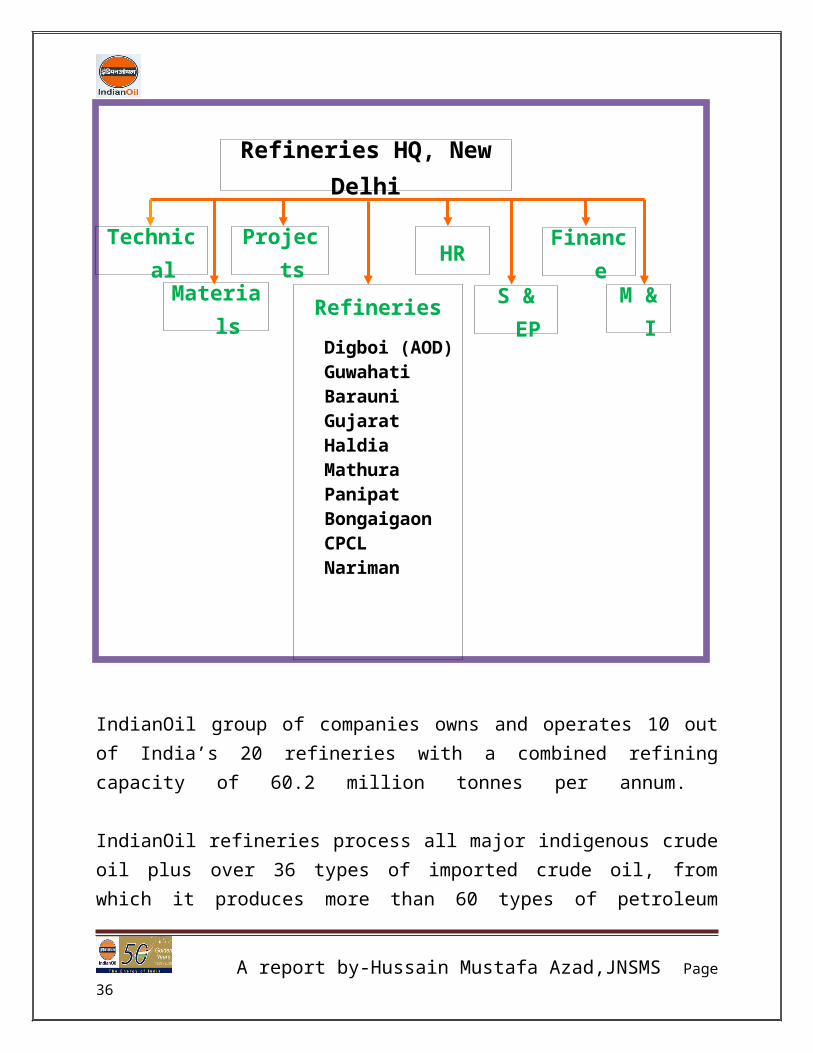

1. Refineries Division

IndianOil group of companies owns and operates 10 out of India’s 20 refineries with a combined refining capacity of 60.2 million tonnes per annum.

IndianOil refineries process all major indigenous crude oil plus over 36 types of imported crude oil, from which it produces more than 60 types of petroleum products, ranging from light distillates, such as LPG, naphtha and motor spirit, to heavy ends, such as furnace oil and low sulphur heavy stock. The flexibility of

A report by-Hussain Mustafa Azad,JNSMS Page 26

Refineries

Digboi (AOD)GuwahatiBarauniGujaratHaldiaMathuraPanipatBongaigaonCPCLNariman

Refineries HQ, New Delhi

Projects

Materials M & I

Finance

S & EP

Technical HR

processing capability allows IndianOil to vary both its crude oil inputs and petroleum product outputs to achieve the company’s desired production mix. To meet the growing domestic demand for middle distillate products, such as HSD and superior kerosene oil, IndianOil has invested in secondary processing facilities to produce these higher value added products.

IndianOil refineries are fully equipped to meet the current environmental norms in relation to product specifications in the country and are being constantly modernized and upgraded to be able to meet all future environment regulatory requirements.

2. Pipelines:

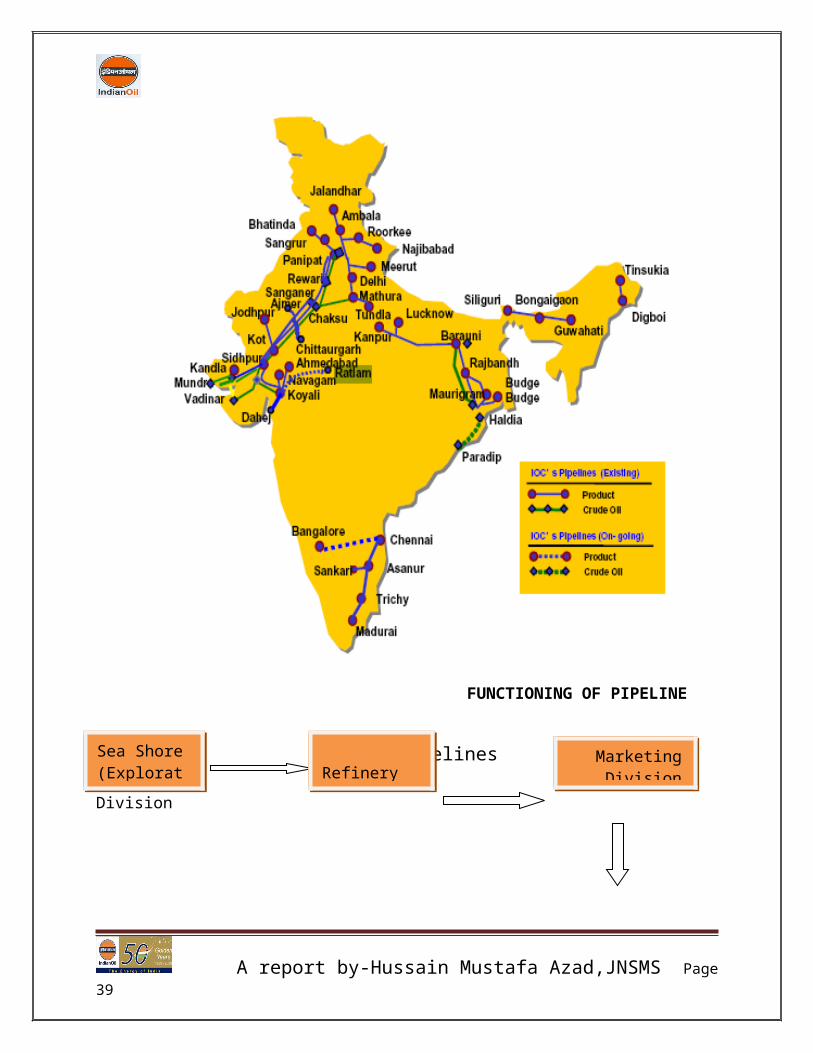

Indian Oil Corporation owns and operates the largest network of crude oil and

product pipelines in India. The total network of pipelines is more than 10,000 km

with a capacity of 71.61 million metric tonnes per annum as on March 2009.

IndianOil’s pipelines include 4366 kilometers of crude oil pipelines and 5964

kilometers of product pipelines.

The company’s pipelines are well positioned to supply petroleum products

from its refineries and India’s ports to high demand states in northwestern India.

Indian Oil Corporation owns and operates the largest network of crude oil and

product pipelines in India. The total network of pipelines is more than 10,000 km

with a capacity of 71.61 million metric tonnes per annum as on March 2009.

IndianOil’s pipelines include 4366 kilometers of crude oil pipelines and 5964

kilometers of product pipelines. The company’s pipelines are well positioned to

supply petroleum products from its refineries and India’s ports to high demand

states in northwestern India.

A report by-Hussain Mustafa Azad,JNSMS Page 27

FUNCTIONING OF PIPELINE

Pipelines Refinery PipelinesDivision

A report by-Hussain Mustafa Azad,JNSMS Page 28

Sea Shore(Exploration)

Refinery Division

Marketing Division

Finished products to clients

3. Marketing Division

Indian Oil and its subsidiaries account for 47% petroleum products market

share. The company distributes its products directly to bulk customers and to retail

customers via a network of retail outlets and dealers/distributors.

The company’s overall distribution network encompasses over 35,000 sales

points incorporating its own franchise as well as independent outlets, consumer

pumps, distributors etc. the substantial majority of which are governed by

dealership agreements. Products are transported to the distribution points by

pipeline, ship tanker, rail tankers and road tanker trucks.

4. Research and Development

A report by-Hussain Mustafa Azad,JNSMS Page 29

Marketing HO, Mumbai

Regional ServicesNorth/East/West/South

State Offices

AOD International Marketing &

Overseas Subsidiaries

R&D Centre, Faridabad

Fuels &

Emission

Petrochem

& BiotechLube

Technology

Refining

Technology

Process DevelopmentProduct DevelopmentTransportation

StudiesProjects

Others

Established in 1972 for the development of lube as well as refining process

technologies, the IndianOil R&D Centre at Faridabad has completed over 35 years

of glorious service to the nation. It is one of its kind in Asia and has grown into a

major technological development center of international repute in the down stream

areas of lubricants, pipelines and refining processes.

Developing more than 2500 formulations over the years, it has successfully

perfected the state-of-the-art lube formulation technology meeting latest national

A report by-Hussain Mustafa Azad,JNSMS Page 30

and international specifications with approvals from major original equipment

manufacturers. IndianOil markets around 800 grades of lubricants under the brand

name "SERVO" based on its own R&D technology and is one among the six

worldwide technology holders of marine oil technology. It has extensive laboratory

and pilot plant facilities to successfully pursue projects in lube, refining and

pipeline areas making it a unique technology centre.

Its rich reservoir of highly qualified/ specialized scientific and technical

manpower has elevated this centre to global status. Having an effective IPR

portfolio of 195 patents including 48 US patents, the vibrant and innovative

research at the Centre has led to many technological innovations, some of which

have received prestigious national and international awards. INDMAX, i-Max,

OiliVorous-S, INDETreat/INDESweet are few of them. Being the nodal agency of

the hydrocarbon sector for implementation of the Hydrogen energy programmes in

the country, the Centre has taken up a pilot project for developing infrastructure for

fuelling neat hydrogen as well as H2-CNG blended fuel and is currently in the

process of setting up a Hydrogen-CNG dispensing station at COCO retail outlet in

Delhi. The Centre has also taken the lead in the development and

commercialisation of biodiesel.

Indian Oil Refineries: Installed Capacities

S.NO. NAME OF THE COMPANY

LOCATION OF REFINERY

CAPACITY

A report by-Hussain Mustafa Azad,JNSMS Page 31

(MMTPA)

1. IOCL GUWAHATI 1.00

2. IOCL BARAUNI 6.00

3. IOCL KOYALI 13.70

4. IOCL HALDIA 6.00

5. IOCL MATHURA 8.00

6. IOCL DIGBOI 0.65

7. IOCL PANIPAT 12.00

8. IOCL BRPL 2.35

9. IOCL *CPCL 09.50

10 IOCL *NARIMAN 1.0

TOTAL 6O.2

NOTE:

1. MMTPA – Million Metric Tonne Per Annum.

2. * Subsidiary of IOCL.

3. Indian Oil group of companies owns and operates 10 out of India’s 20

refineries with a combined refining capacity of 60.2(49.70-own capacity and

10.50-capacity of the subsidiary refineries) million metric tonnes per annum.

4. Another refinery is being set up on the East Coast at Paradip (Orissa) with a

capacity of 15.00 million metric tonnes per annum.

Major Products of a Refinery:

A report by-Hussain Mustafa Azad,JNSMS Page 32

Lightest

Heaviest

Liquified Petroleum Gas (LPG)NaphthaMotor Spirit (MS)/ Petrol/ GasolineAviation Turbine Fuel (ATF)Superior Kerosene Oil (SKO)High Speed Diesel (HSD)Light Diesel Oil (LDO)Furnace oil (FO)Heavy Petroleum Stock (HPS)Lube oilsRaw Petroleum Coke (RPC)Petroleum WaxBitumen/ Asphalt

Products of the Refineries of IOCL:

A report by-Hussain Mustafa Azad,JNSMS Page 33

A report by-Hussain Mustafa Azad,JNSMS Page 34

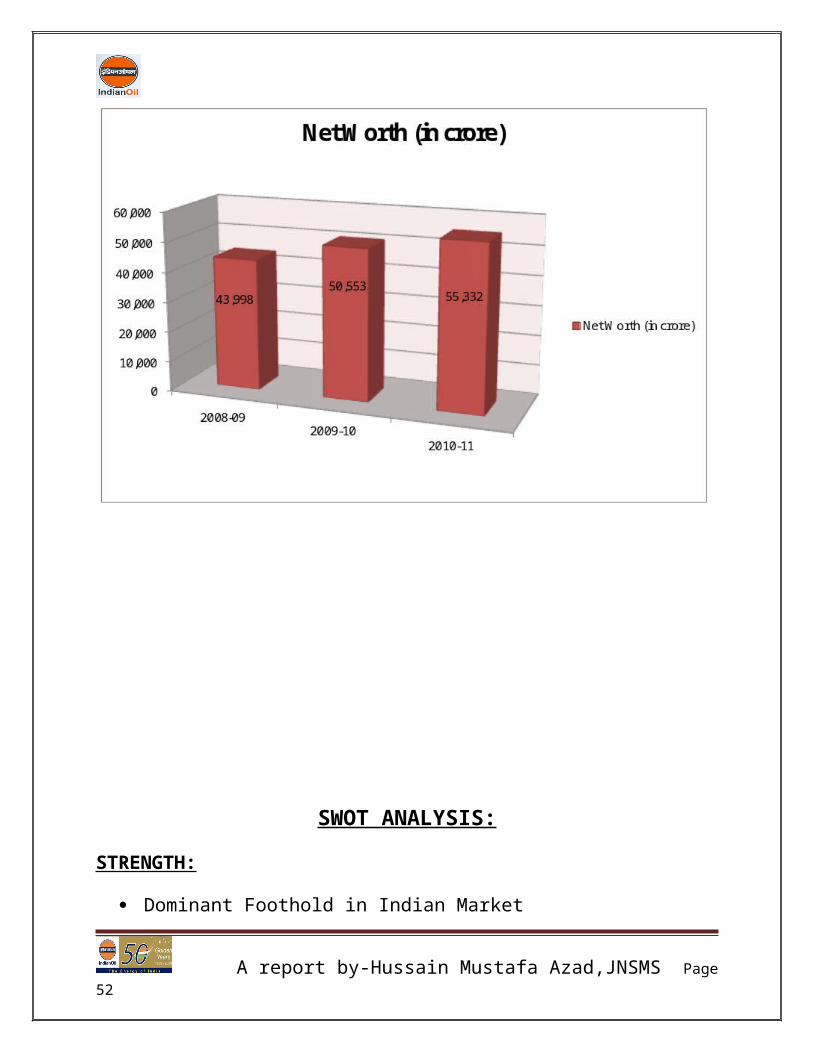

PERFORMANCE REVIEW

CHANGE IN AUTHORISED SHARE CAPITAL

During the year, the Authorised Share Capital of the Corporation was increased

from 2,500 crore to 6,000 crore with the approval of members by a Postal Ballot

Process to enable the Corporation to raise finance through the issuance of shares in

the future.

DIVIDEND

The Board of Directors of your Corporation is pleased to recommend a dividend of

9.50 per equity share of 10/- each on the Paid-up Share Capital as against

13/- per share in the previous year due to lower profits. So far, your Corporation

has paid a cumulative dividend of 18,575 crore, excluding a dividend of 2,307

crore payable for the current year, subject to the approval by shareholders.

A report by-Hussain Mustafa Azad,JNSMS Page 35

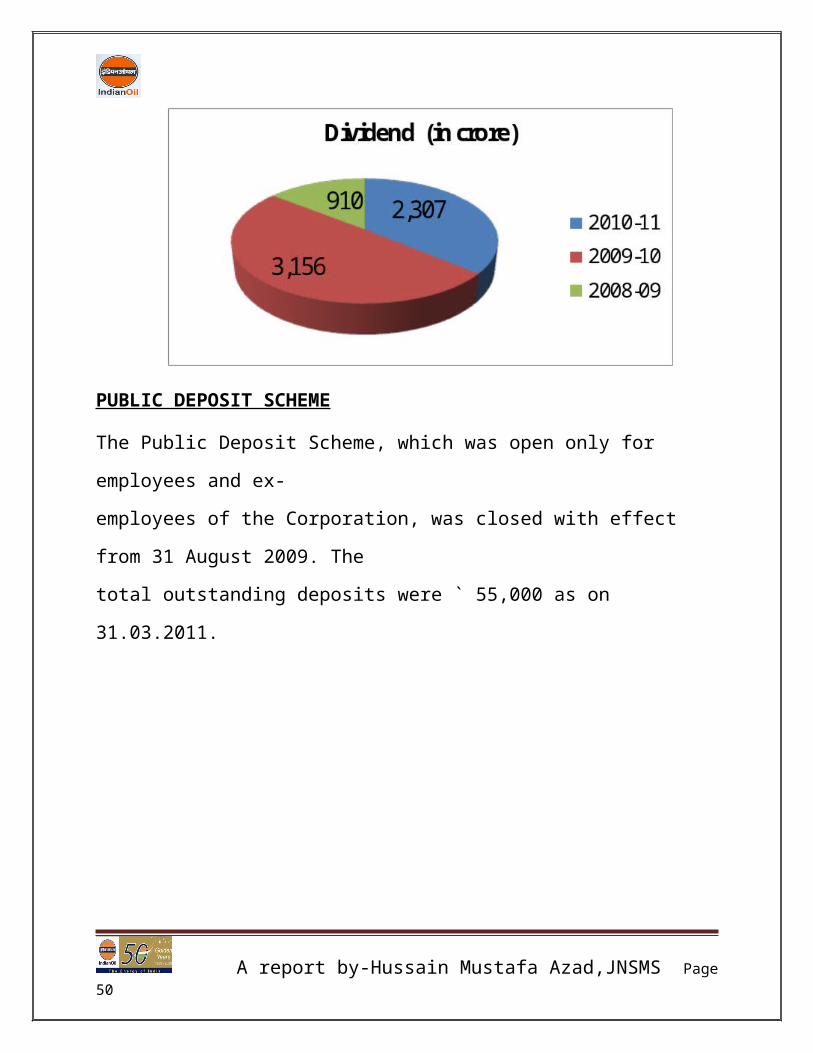

PUBLIC DEPOSIT SCHEME

The Public Deposit Scheme, which was open only for employees and ex-

employees of the Corporation, was closed with effect from 31 August 2009. The

total outstanding deposits were ` 55,000 as on 31.03.2011.

A report by-Hussain Mustafa Azad,JNSMS Page 36

CONTRIBUTION TO EXCHEQUER

Your Corporation has been making enormous contributions to the Exchequer in the

form of duties and taxes. During the year, 77,622 crore was paid to the Exchequer

as against 57,680 crore in the previous year. In the current year, 39,658 crore was

paid to the Central Exchequer and 37,964 crore to the States Exchequer.

A report by-Hussain Mustafa Azad,JNSMS Page 37

SWOT ANALYSIS:

STRENGTH:

Dominant Foothold in Indian Market

Prominent Producer and Supplier of LPG.

Robust Network.

IOCL has 10 Refineries under its Group having a combined.Throughput of

60 MMTPA which is the highest in India.

Vast Network of Petrol Pumps spread across all parts of India and IOC

occupies more than 60% of Market Share in Petroleum Products in India.

IOCL has downstream pipeline network of 10064 Km spread across India

which is 71.4% of Total Downstream Pipeline Network in India. Large

Network of Pipeline gives IOCL a competitive edge.

IOCL is the highest rank company in list of Global Fortune 500 companies.

Currently its stand at 116th position.

IOC has integrated ERP package i.e SAP spread all across India.

WEAKNESS:

Non Autonomy.

Most of IOCL Refineries are Inland Refineries which increases the cost of

Production.

Some of the Refineries Technology is old. They can only process Low

Sulphur Crude and efficiency is also low.

Low throughput of Individual Refineries increases the Fixed Cost of

Production and company is unable to take advantages of Economy of

Scale.

A report by-Hussain Mustafa Azad,JNSMS Page 38

Since IOCL is a Public Sector Undertaking there is high Government

Regulation.

OPPORTUNITY:

Diversification into Renewable Energy.

Positive Outlook for Natural Gas Business.

Strengthening Petrochemical Operation.

Increasing Demand for Petroleum Products.

Developing its own technology with emphasis on R & D units.

Company can integrate its core Business of Petroleum Products with

Exploration Activities.

Diversification oppurtunities are there in Gas Sector & Alternate Energy

Sectors such as Bio-Fuels and also in Power Sector.

THREATS:

Highly Competitive Market

Environmental Regulations.

Volatile Oil and Gas Prices.

Rising Capital Costs in the Refining Sector

Prices regulated by Govt. for Four Major Products. i.e HSD, MS, SKO &

LPG

Increasing International Crude Prices and Depleting Crude Oil Reserves.

Increasing Trend in Consumption of Gas & Nuclear Energy

Emergence of Private Player like Reliance/ESSAR with latest refining

technology having High Crude Throughput Installed Capacity and

locational advantages.

A report by-Hussain Mustafa Azad,JNSMS Page 39

CLASSIFICATION OF CAPITAL BUDGET

In IOCL, Guwahati Refinery capital budget is classified in 2 categories:

Plan schemes

Non- plan schemes viz. Additional Facilities (AF)

PLAN SCHEMES:

Plan schemes are those schemes which are required to be included in the annual

plan documents for submission to Government / Planning Commission for

approvals. These schemes ultimately form part of the government’s annual plan.

they are important from national point of view and involve substantial expenditure,

generally above 100 crores on items relating to capacity improvement of primary

or secondary units. While non-plan schemes generally cover capital investments on

additional facilities like buildings, off site, utilities, furniture, vehicles, etc.

They are generally developed in line with action plan drawn on Long Range Plan

(5 years) / Perspective plan (10-15 years) of the corporation. No expenditure on

plan schemes is incurred unless the scheme is included in the approved annual plan

document with a budget allocation for the year and also the scheme is approved by

competent authority as per the delegation of powers. The annual plan is required to

be submitted to the Government by mid September every year.

It is essential that the revised outlay for the current year and the outlay required for

the next year are assessed realistically in order to ensure that the total actual

expenditure would be close to the proposed outlay.

A report by-Hussain Mustafa Azad,JNSMS Page 40

NON- PLAN SCHEMES (AF):

The AF schemes encompasses wide spectrum of activities covering safety,

statutory requirements, technology up gradation, welfare, replacements/addition of

assets, operational necessities, etc. Individually AF schemes may be lower cost,

collectively they may account for significant portion of the total capital

expenditure. Therefore the handling of AF schemes with regard to their selection,

accurate cost estimates and timely completion assumes a great significance. The

schemes need to be judiciously implemented after detailed study of various

alternatives available.

PROCEDURE FOR APPROVAL OF AF (ADDITONAL FACILITES)

SCHEMES

All AF proposals shall be initiated and prepared by units in the ZBB decision-

making package. The AF proposals are required to be forwarded to Secretary,

Investment Review Committee, and HO for approval only after obtaining

concurrence of the local finance and endorsed by the Unit Head.

The proposals forwarded to HO for approval shall cover full details and

justifications. HO would examine the proposal and obtain the approval of the

competent authority. On approval, necessary provision will be made in the AF

budget.

PREPARATION OF AF PROPOSALS

A report by-Hussain Mustafa Azad,JNSMS Page 41

The units as per the prescribed format shall submit the AF proposals. While this is

the minimum requirement for submission of an AF proposal, additional/

supplementary date/ information needs to be added as required for a better

appreciation and evaluation of the proposal.

AF proposal shall contain the following information:

Name, objective and purpose

Background/ origin of the proposal

Generation/ evaluation of alternatives

Description of activities

Benefits / saving from the proposal

Project cost estimates

Completion schedule

Economics

NAME, OBJECTIVE AND PURPOSE

The name of the proposal should be brief but reflect the contents. The objective

and purpose of the proposal shall be stated clearly and unambiguously and it

should be ensured that the same are specific and not general nature.

BACKGROUND / ORIGIN OF THE PROPOSAL

Following points are of importance.

The circumstances leading to the preparation of the proposals should be

explained in detail. In case the proposal is prepared in pursuance of the

recommendations of a committee, working group, statutory bodies, ministry

etc., the mere mention of this does not constitute the background for

A report by-Hussain Mustafa Azad,JNSMS Page 42

propelling the case. The case must be presented in perspective, explaining

briefly the rationale behind particular recommendations. Full documentary

evidence must be presented in support wherever applicable.

In many cases, AF proposal are initiated to improve an existing operation by

removing constraints, updating technology, replacement/ addition of

equipments, process modifications, extension of an existing facility to new

areas etc. in all these cases, it is of prime importance that the proposal

includes a brief description of existing facilities/ operations . The

constraints/ limitations experienced with the existing facilities must be

discussed and efforts made in the past to overcome these problems etc.

should be sufficiently elaborated. Brief description of operation of facilities

in past vis-à-vis the need for proposed modification would help to appreciate

the problem.

GENERATION / EVALUATION OF ALTERNATIVES

Once the objective of the proposal is firmed and the evaluation of the existing

facilities have been completed the next logical step is the generation of alternatives

or options available for achieving the desired objectives.

The following 2 points are of importance in this regard:

All possible alternatives should be explored and listed. This may involve

different level of efforts and cost or different ways of performing the same

functions, activity or operation.

A report by-Hussain Mustafa Azad,JNSMS Page 43

Evaluation of alternatives must also be carried out in systematic manner.

While there cannot be a uniform approach for evaluation of alternatives,

some of factors to be considered are: cost-benefit analysis, repercussion on

other units/ operation, time schedule, availability of resources, down time

requirements in case of plant modifications, long – term implications,

conforming to corporate policies, legal and other statutory requirements, etc.

in any case, the proposal should clearly indicate the criteria and

considerations that led to the selection of the recommended alternative.

DESCRIPTION OF ACTIVITIES

Once the evaluation of alternatives and selection of the optimum scheme is

completed the proposal should be developed with sufficient detailing.

Some of the major considerations/ requirements at this stage are listed below:

BENEFITS /SAVING FROM THE PROPOSALS

The importance ability of the proposed scheme must be fully explored with

reference to area requirements vis-à-vis availability, extent of enabling jobs

required, execution feasibility (impact on running units, safety precautions

needed, etc.), shut down requirements, utility requirements/ availability,

hook up jobs, etc. these must also be documented as part of the proposal.

Efforts must be made to identify and examine the utility of redundant/-

unutilized materials available in the plant. This would help in cutting down

cost and time besides ensuring the use of idle equipment.

A report by-Hussain Mustafa Azad,JNSMS Page 44

The proposal should include only those activities/ facilities need for meeting

the objective. Each element/ activity included in the proposal must be

backed by adequate justification for its inclusion. It is always better not to

include an entirely unrelated activity/ facility in a proposal but rather make a

separate proposal with justification, etc. for the same.

In case the proposal envisages the introduction of new technology/ process/

equipments, it is desirable to gather reliable information on the performance

of similar process/ equipment elsewhere within the country or outside,

instead of relying entirely on the vendor’s claims.

An assessment of the additional manpower requirements for operating the

proposed facility should be made and included as a part of the proposal.

The methodology or execution of the project should be finalized at the

proposal stages itself. In case it is felt necessary to engage a consultant,

adequate justification for the same, job scope for consultant etc. must be

clearly mentioned in the proposal.

PROJECT COST ESTIMATES

Need for realistic cost estimates

The importance of making an accurate cost estimate4 cannot be over

stressed. It will have a direct bearing on the economic viability of the

scheme. While over-estimation may cause blockage of funds which

otherwise could be utilized profitability for some other purpose, under

estimation would necessitate repeated approvals for cost overruns and may

also affect the project completion schedules.

Basis

A report by-Hussain Mustafa Azad,JNSMS Page 45

It is essential that the basis adopted for cost estimation of all major

components be included. Generally, cost estimates for major equipments,

imported goods, proprietary items etc. shall be on the basis of current

budgetary quotations. Detailed work ups, copies of quotations etc, must be

enclosed with the proposal. The effort shall always be to base the cost

estimates on a sound basis.

Escalation

All cost estimates shall be as on the date of submission of the proposal and

the rate of escalation adopted for different cost estimates shall be indicated,

along with basis.

Foreign exchange requirements

The foreign exchange requirements are to be worked out separately and

shown. The need to import equipments /process etc. involving outgo of

Foreign exchange are to be critically reviewed, indigenous availability fully

explored and foreign exchange component of the proposal kept to the bare

minimum.

A report by-Hussain Mustafa Azad,JNSMS Page 46

FINANCE DEPERTMENT OF GUWAHATI REFINERY

FINANCIAL MISSIONS

1. To provide high quality financial staff support for decision-making and

control to all levels of management—corporate, divisional, unit and location

to enable the achievement of overall corporate objectives and goals.

2. To play a lead role in scanning the domestic and international financial

environment, the formulation and implementation of all financial policies

and plans for different time spans consistent with and conducive to the

business plans for expansion, diversification, productivity etc.

3. To interact pro-actively with the relevant Government agencies on pricing

and investment and with financial institutions, depositors and creditors, with

sensitivity and promptness, for mobilization and provision of funds for

uninterrupted operations and project execution at optimal costs.

4. To maintain, review and update of all relevant accounting records, systems

and procedures for discharging the fiduciary responsibilities and enabling

compliance with statutory obligations.

5. To inculcate financial awareness, cost benefit attitudes and system

orientation in the entire organization.

A report by-Hussain Mustafa Azad,JNSMS Page 47

6. To develop the human resources, systems and techniques of finance for

continuing innovation and contribution towards IOC corporate excellence.

FINANCIAL OBJECTIVES

1. To ensure adequate return on capital employed and maintain a reasonable

annual dividend on its equity capital.

2. To ensure maximum economy in expenditure.

3. To generate sufficient internal resources for financing partly/wholly

expenditure on new capital projects.

4. To develop long term corporate plans to provide adequate growth of the

activities of the Corporation.

5. To continue to make an effort in bringing reduction in the cost of production

of petroleum products by means of systematic cost control measures.

6. The endeavour to complete all planned projects within stipulated time and

within stipulated cost estimates.

FINANCIAL GOALS

1. To inculcate cost consciousness in user departments.

2. Development of Standard Refining costs at each unit level.

3. Proper implementation of budgetary control and submission of MIS in time.

4. To keep the level of inventories below the level fixed by the Board and

outstanding debts, loans & advances and claims at bare minimum.

5. Ensure payment on due date to various agencies.

A report by-Hussain Mustafa Azad,JNSMS Page 48

6. Monitor capital expenditure to ensure completion within stipulated time and

cost.

7. Optimize utilization of working capital.

8. Efficient management of Funds.

THE FUNCTIONS OF THE FINANCE DEPARTMENT INCLUDES:

Management of financial resources for meeting the Corporations

programmes of operations and capital expenditure including investment of

surplus fund, if any.

Ensuring uniform financial and accounting policies and procedures, to the

extent possible, in the Division.

Establish and maintain a system of financial scrutiny and internal checks and

render advice on financial matters including examination of feasibility

studies and detailed project reports.

Establishment and maintain an appropriate system of Budgetary Control and

Management Information System for different levels of the Management.

Carry out periodical/special studies with a view to control costs, reduce

expenditure, economy in administrative expenditure, and improve efficiency

to maximize profitability of the Corporation.

Maintain the financial accounts, cost accounts and other relevant books and

records in accordance with the various statutory and other requirements.

A report by-Hussain Mustafa Azad,JNSMS Page 49

FLOW OF FINANCE DEPARTMENT

(REFINERIES AND PIPELINES DIVISION)

DIRECTOR (R&P)

ED (FINANCE) HO

G.M. (FINANCE)

DGM (FINANCE)

A report by-Hussain Mustafa Azad,JNSMS Page 50

CFMs

SFMs

FMs

DFMs

SACOs

ACOs

THE FUNCTIONING OF DIFFERENT SECTIONS OF THE FINANCE DEPARTMENT AT GUWAHATI REFINERY:

1. MAIN ACCOUNTS:

The main accounts section is entrusted with the responsibility of the following:

1. Preparation of Balance sheet

2. Preparation of Tax Audit

3. Co-ordinator for all Audits i.e. Statutory, Government, CAG, Internal

Audit, etc.

4. Physical Asset verification.

5. Insurance of Assets and stocks.

6. Head Office Account Reconciliation.

7. Capitalization of Employee Assets.

A report by-Hussain Mustafa Azad,JNSMS Page 51

Cash budget is prepared in this section and the same is to be produced before HO.

All other section of finance department provides the information to the Main

Accounts for preparing list “B”. List “B” details include 20 items approximately.

Some of them are mentioned below.

Employment and Housing accommodation statistics.

Payment of sales tax, Excise duty, Entry tax and other tax and duties.

Loss on disposal/write-off of –

(a) Assets

(b) Stores and spares showing original cost, book value and

reason for disposal of each item under various categories.

Asset management is also controlled by this section. For assets management, they

prepare the master of assets, which includes name, cost centre and other details for

capitalization of assets. Further, receiving debit, credit notes and reconciliation of

the is also a part of this section.

2. PURCHASE ACCOUNT:

Generally this section deals with the payment of purchase items only. After

purchase, the material is delivered to the stores department. The Stores Department

makes Goods Receipt Note (GRN) and sends it to the purchase section. Here the

GRN is checked with the purchase order (PO) and payment is made through e-

banking.

The purchases section is responsible for:

1. Scrutiny of purchase proposals.

2. Deposit and advance payments to suppliers.

3. Passing of bill for supplies received.

A report by-Hussain Mustafa Azad,JNSMS Page 52

4. Pricing of goods receipts notes.

5. Accounting of cash purchases made by the materials department.

6. Arrangement for insurance of goods in transit.

7. Maintenance of books of accounts.

8. Sales tax matters/ VAT etc.

9. Payment for imported goods in the respective currency.

3. WORKS/PROJECTS:

The work section mainly deals with capitalization of CWIP (Capital Work In

Progress) and payment of running contracts. Its considers only plants

maintenance, roads, painting, welding, water etc. First and final payments are

made on the basis of work completion.

The works/project section is responsible for:

1. Payment of Bill.

2. Receipt/Release of EMD/SD.

3. Deductions/Deposits of various Statutory Deductions/Deposits like

TDS,WCT etc.

4. Creation of Assets Master.

5. Capitalization of Assets.

6. Accounting of post capitalization assets.

7. Issue of TDS certificate.

4. PAYROLL:

This section mainly deals with the payment to employees for their work. Rules for

pay and allowance are prescribed by head office from time to time. The eligibility

for special type of allowance such as special allowances, shift allowance etc. is

A report by-Hussain Mustafa Azad,JNSMS Page 53

determined by personnel department and intimations are sent to the finance

department giving the details of employees those who are eligible for such

allowance. Then the Pay Roll section functions accordingly.

Function dealing with this section can be broadly classified as:

1. Scrutiny & concurrence of proposals from personnel department.

2. Payment of salaries and allowances.

3. Advances payment to employees.

4. Deductions from pay bills.

5. Other welfare schemes including gratuity.

6. Personal claims and other payments.

7. Statutory and statistical requirements.

8. Deduction of Tax at Sources and filing ETDS.

This section also maintains the data of transfer and new recruitment of employees

and adds it to master information. If a person is transferred to another unit, the LPC

(last pay certificate) is required to be added into master information.

5. STORES AND CENVAT:

MODVAT stands for Modified Value Added Tax, which is now known as

CENVAT i.e. Central Value Added Tax. It is a scheme, which provides relief to

final manufacturers on the excise duty borne by the suppliers in respect of goods

manufactured by them. Under this scheme, a manufacturer can take credit of excise

duty paid on raw materials and components used by them. The normal excise duty

rate is 16%. However it depends upon the Tariff class under which the product is

classified.

The section dealing with accounting of stores have the following functions:

Passing and accounting of transportation bills.

A report by-Hussain Mustafa Azad,JNSMS Page 54

Accounting of receipts, issues, return and transfer of materials.

Accounting of imported materials for capital works and operations/

maintenance.

Stock verification.

Accounting for sale of surplus/scrap materials.

6. TA/LTC/MEDICAL:

This section maintains in-transfer and out-transfers accounting for claim settlement

and also handles the bill payment of official tour of employees. HO. The Claim of

Leave Travel Concession (LTC), Leave Fair Assistance(LFA) and the claim of the

foreign tours is controlled by this section. This section also deals with the payment

of medical related issues.

The main finctions of this section is:

1. Scrutiny and Payment of bills related to PRMS, Leave Fair Assistance

(LFA), Leave Travel Concession(LTC).

2. Bill payment of official tours of employees.

3. Scrutiny of orders and bill payment to Panel Doctors and Panel Hospital.

7. PRODUCTION ACCOUNTING:

This section maintains production accounts, including crude accounting, custom

duty payments, product bill accounts, bitumen drum accounts and stock valuation

accounts. Production Accounts Section keeps records of input in terms of crude oil

and output in terms of the company’s final products.

The basic functions of the production accounts are:

A report by-Hussain Mustafa Azad,JNSMS Page 55

1. Accounting of Crude oil quantity and value for the receipts, consumption

and stock.

2. Accounting of inter-divisional/ inter-unit transfer of products for ex-refinery

value and excise duty.

3. Accounting of consumptions of own fuel/products.

4. Valuation of closing stocks i.e. Raw Material, ISD, Finished Goods

5. Preparation of Cost Sheet and Cost Audit Performa

6. Monitoring of Revenue Budget, Preparation of Revenue Budget.

7. Monthly Profitability.

8. Monitoring of STR MOU performance.

8. CASH / BANK:

This section mainly deals with making payments. No fixed limit is established by

the organization for making payments. The organization has special current

accounts with State Bank of India. These accounts are the sources of payments.

The balance at the end of the day, becomes nil by transferring the amount to the

head office. The employees of the organization are paid through cash up to

Rs.20000 and by cheque for over and above Rs. 20000. Salary to the employees is

paid through cheques.

Cash section shall be responsible for:

1. Receipts of cheques and bank drafts

2. Payment of cheques and bank drafts.

3. Handling of bank deposits/ withdrawls, custody of cash and transfer of

funds.

4. Preparation of BRS (Bank Reconciliation Statement)

A report by-Hussain Mustafa Azad,JNSMS Page 56

5. Safe custody of valuables and documents.

6. Preparation of bank reconciliation statement.

7. Maintenance of subsidiary cash credit account and special current account.

9. PROVIDENT FUND & ADVANCES:

The scheme of the provident fund is the same as in case of any government

undertaking i.e. 12% of the dearness allowance is kept aside for this purpose and

the company contributes the same amount. All the employees irrespective of their

position in the organization are entitled to 9.5% interest on provident fund. This

rule is applied uniformly to all the units and branches of the refineries division of

Indian Oil Corporation limited.

10. OIL ACCOUNT

Here are some basic functions of the oil accounting:

1. Accounting of crude oil receipts

2. Accounting of customs duty on crude oil.

3. Accounting of finished product receipts

4. Dispatch of products.

5. Excise procedure and accounting

6. Material balance & Production statistics.

7. Monthly Excise Duty Payment thorugh e-payment.

8. Loss/Gain calculation of finished product due to rise/decrease in

temperature.

11. CONCURRENCE SECTION

A report by-Hussain Mustafa Azad,JNSMS Page 57

The Financial Concurrence is objected towards protection of financial interests of

the Company in the decision making while ensuring financial propriety as a part of

internal control system. The internal control is exercised through the vetting and

concurrence by Finance department so that decision-making is as per policy

guidelines, rules, regulations, provision of budgets, etc. and it is not detrimental to

the financial interest of the Company.

The financial concurrence facilitates achievement of transparency in the decision

making which is subject to the scrutiny of various Government agencies like audit,

vigilance etc.

12. MISCELLANEOUS SECTION

The expense which cannot be accounted and beard by any other section is done by

this section.

The function of the Miscellaneous Section includes the following:

1. Accounting of cash imp rest and advances for company expenses for specific

reasons such as gift items for functions, urgent purchase etc.

2. Passing of bills of miscellaneous nature such as expenses of Auditor.

3. Miscellaneous recoveries from outsiders

4. Inter-sectional coordination.

5. Payment of Electricity Duty.

6. Payment for expenditure of Canteen and Training.

A report by-Hussain Mustafa Azad,JNSMS Page 58

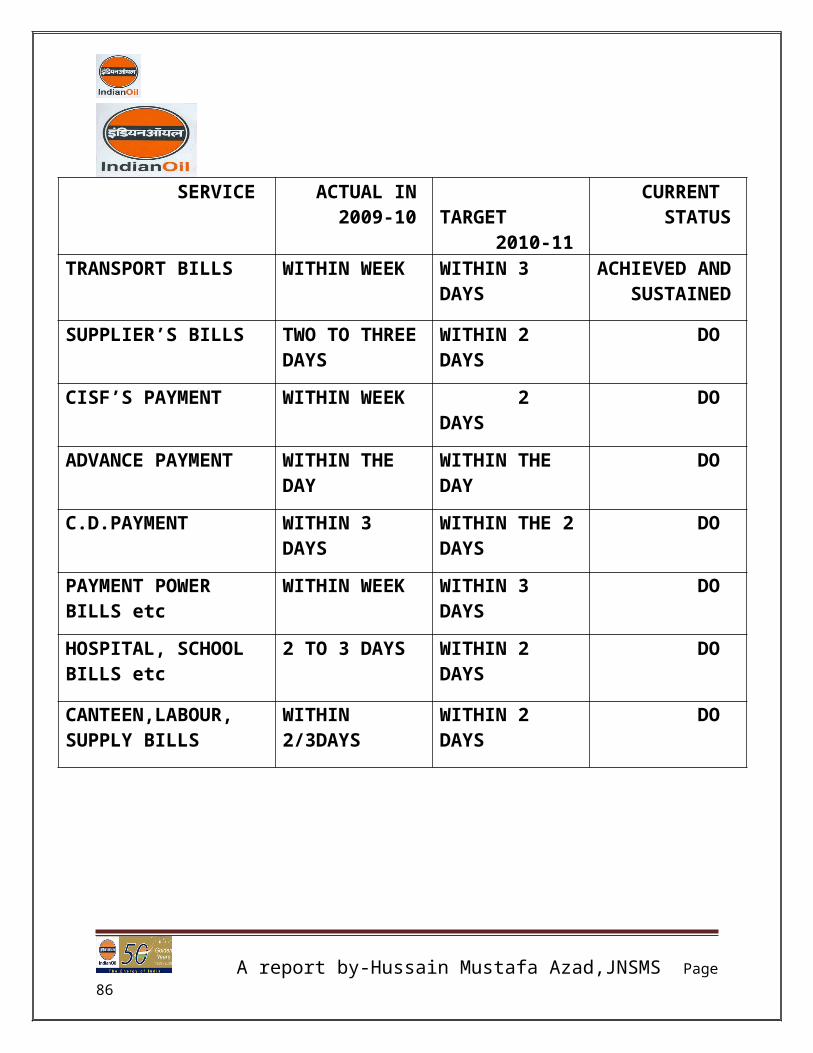

ACHIEVMENT OF FINANCE DEPARTMENT ATGUWAHATI REFINERY

INDIAN OIL CORPORATION LTD MIS.SECTION

SERVICE ACTUAL IN 2009-10

TARGET 2010-11

CURRENT STATUS

TRANSPORT BILLS WITHIN WEEK WITHIN 3 DAYS ACHIEVED AND SUSTAINED

SUPPLIER’S BILLS TWO TO THREE DAYS

WITHIN 2 DAYS DO

CISF’S PAYMENT WITHIN WEEK 2 DAYS DO

A report by-Hussain Mustafa Azad,JNSMS Page 59

ADVANCE PAYMENT WITHIN THE DAY

WITHIN THE DAY

DO

C.D.PAYMENT WITHIN 3 DAYS

WITHIN THE 2 DAYS

DO

PAYMENT POWER BILLS etc

WITHIN WEEK

WITHIN 3 DAYS

DO

HOSPITAL, SCHOOL BILLS etc

2 TO 3 DAYS WITHIN 2 DAYS

DO

CANTEEN,LABOUR, SUPPLY BILLS

WITHIN 2/3DAYS

WITHIN 2 DAYS

DO

A report by-Hussain Mustafa Azad,JNSMS Page 60

INDIAN OIL CORPORATION LTDGUWAHATI REFINARY

TA/LTC/MEDICAL

SERVICE ACTUAL IN 2009-10

TARGET2010-11

CURRENT STATUS

PAYMENT OF MEDICAL BILL/MEDICLA P.A

4 DAYS WITHIN 2 DAYS

ACHIEVED AND SUSTAINED

PAYMENT OF TA, LTC ect

4 DAYS WITHIN 2 DAYS

DO

PAYMENT OF PARTY’S BILL/PANNEL PHARMA etc

6 days WITHIN 2 DAYS

DO

PMRS PAYMENT WITHIN WEEK

WITHIN 2 DAYS

DO

A report by-Hussain Mustafa Azad,JNSMS Page 61

DEVELOPMENT REPORT 2010-11

FINANCE DEPARTMENT

#1. Utilisation of SAP

Tool developed and implemented for drawing fixed asset schedule along-

with Balance sheet through SAP

Designed and implemented new simplified procedure for accounting of fund

transfer from units through SAP thereby reducing work and improving

control.

#2.Account Review by Auditors

No comments received from CAG on balance sheet audit for 2009-10 annual

accounts of Refineries Division.

#3.Crude Oil Sales Agreement (COSA)

Crude Oil Sales Agreement (COSA) with ONGC,effective 1st April 2010 for

supply of indigenous crude Oil initiated in May 2010 & approved by Board.

#4. Banking & Insurance

E-payment target of 90% achieved

After review of the risk involved in crude oil transportation, risk coverage

has been extended by replacing the ICC-C policy with institute bulk oil

policy

A report by-Hussain Mustafa Azad,JNSMS Page 62

Reduction in package insurance policy rates to the extent of 19.24%

involving savings of around Rs 10 crores

#5 Trust Accounts

Merger of IBP& BRPL Trust with IOCL SABF Trust approved by the

respective Trusts. The merger activities have been completed.

Merger of BRPL Gratuity Trust with IOCL employees Gratuity Trust

completed.

#6 Custom & Excise

Custom Refund of RS86.33 crores has been received during calendar year.

Major demand on exempted values of clearances for products like SKO-

PDS,LPG-Domestic, LSHS/NAPTHA for end use as captive consumption

and by fertilizer industry involving Rs 1100 crores dropped at customs,

central Excise & service Tax Appellate Tribunal, Kolkata.

A report by-Hussain Mustafa Azad,JNSMS Page 63

IMPLEMENTATION OF ERP-SAP IN GUWAHATI REFINERY.

ERP-SAP has been implemented in Guwahati Refinery in 2002. This was the

fourth refinery to IOCL to go live in SAP after PRP, MR, JR in the year 2002.

All modules viz FICO, PM, MM, HR, PS implemented and all transactions are

done in SAP.

FEATURES OF ERP-SAP

Covers the entire value chain/ supply chain, from customer requirement to

fulfillment.

Covers all business dimensions of the organization, process, people, structure

and technology.

Oriented towards business process and not around function.

Covers all management levels of the organization.

Fully integrated with all functionality of the organization.

Built-in best practices available-strong enabler in improving business

performance.

Addresses all the enterprise requirements.

Flexible to accommodate future changes.

GENERAL ADVANTAGES

Reduced working capital requirements.

Improved customer service and quality.

A report by-Hussain Mustafa Azad,JNSMS Page 64

Reduced obsolescence.

Reduced cost.

Having accountability through out the organization.

Improved productivity and effectiveness.

MISCONCEPTIONS ABOUT SAP

ERP facilitates the decision-making and does not decide.

ERP provides comprehensive information to optimize but does not optimize

dynamically.

It automates and integrates transactions but does not target the cycle time

SPECIFIC ADVANTAGES FOR FINANCE

Each Refinery / Pipelines unit, each regional office and state office of marketing

division is a separate company under SAP. Inter company transactions involving

transfer of product, money and assets are taken care of by the system. There is no

need to generate control account advices, Debit/ credit notes between the division,

units, and regions and between units, regions vs. HOs.

No joint reconciliation meetings between divisions, regions, units and HOs.

Authorized executives of each company will have access to the inter-company

accounts of other companies. Hence, they can always compare and locate

differences, if any.

The new concept of fund center helps monitor online the revenue budget of each

company in respect of revenuer expenses (a commitment item as per SAP

terminology) at the time of release of payments. There is a warning message when

75% of the budget is exhausted. There is an error message in respect of

A report by-Hussain Mustafa Azad,JNSMS Page 65

controllable revenuer expenses when the budget is completely exhausted, and the

payment is not processed until supplementary budget is given to the fund center.

Whether the expanse is for current operation or for Assents under construction is

distinguished by capturing a cost center or internal order/ WBS respectively.

Various groups of vendors and customers have separate respective control

Accounts (reconciliation accounts, in SAP terminology) in the general ledger. No

one is allowed to post any transaction in these control (reconciliation) accounts;

therefore, the balances of each sub-ledger representing a group of vendors or

customers are always be equal to the respective control (reconciliation) accounts.

Earlier since there was a time gap in communicating the frequent price changes to

supply locations, the invoices continue to be prepared at the old rates for some time

at some locations. This necessitates checking of all the invoices prepared at supply

locations with the rate masters maintained at the regional office. This job was

currently been done by the rate checking section of finance in the divisional

offices, which raised debit/credit loads on the customers. After SAP, there is no

need for rate checking because the price changes are made centrally for most of the

price elements. Hence, there is no need for subsequent rate checking of the

invoices.

After SAP, each of collection, withdrawal and current bank account has a separate

general ledger code. The user had to feed the bank statement in to the system and

the system is doing the bank reconciliation and is moving the matched transactions

to another account living the open unmatched items in the general ledger account

of that bank account. After SAP, with the help of cash management facility, it is

possible to view all the balances as per our books of all the bank accounts in the

desired manner. This will help in managing the overdraft facility in a more logical

manner.

A report by-Hussain Mustafa Azad,JNSMS Page 66

Since the system security is of utmost importance under SAP, user ID and

Password is strictly enforced. Under SAP a complete Audit trial is maintained in

the System. Therefore, the responsibility for any miss-happening is established as

per the user ID to perform the relevant transactions.

DEMERITS

ERP facilitates the decision making and does not decide.

ERP provides comprehensive information to optimize but does not optimize

dynamically.

It automates and integrates transactions but does not target the cycle time

A report by-Hussain Mustafa Azad,JNSMS Page 67

Project Analysis

Project finance under IOCL

A report by-Hussain Mustafa Azad,JNSMS Page 68

.

Project financing is a loan structure that relies primarily on the project's cash

flow for repayment, with the project's assets, rights, and interests held as secondary

security or collateral. Project finance is especially attractive to the private sector

A report by-Hussain Mustafa Azad,JNSMS Page 69

because they can fund major projects off balance sheet. Project financing involves

identifying the project, determining the feasibility of the project, identifying

sources of finance for the project, mitigating the risk and monitoring

implementation of the project. It is most commonly used in the mining,

transportation, telecommunication and public utility industries.

KEY PARAMETERS TO BE EVALUATED IN A PROJECT

The key parameters to be evaluated in a project are:

Risk Analysis

Demand Analysis

Project Cost Estimation

Revenue Analysis

Financial Analysis

Project Selection Criteria

Project Evaluation under IOCL

Project evaluation is a high level assessment of the project to see whether the

project is worthwhile to proceed and whether the project will fit in the strategic

planning of the whole organization. Project evaluation helps to decide which of the

several alternative projects has a better success rate, a higher turnover.

A report by-Hussain Mustafa Azad,JNSMS Page 70

Capital Projects in IOC are broadly divided

into:

· Core-sectors projects: The core divisions of IOCL are Refining,

Marketing, Pipelines and R&D, and the projects undertaken by these divisions

come under the Core-sector projects.

· Diversification projects: Projects undertaken by IOCL in fields other than

A report by-Hussain Mustafa Azad,JNSMS Page 71

its core divisions (e.g. Exploration &Production (E&P), Liquefied natural

gas (LNG), Petrochemicals and power etc.) come under diversification

Projects.

· Globalization projects: Core/ non- core sector projects which are

undertaken oversees come under globalization projects

· Merger / Acquisitions: The merger and acquisition of other organizations

by IOCL come under this head.

Clean Development Mechanism under IOCL

The Clean Development Mechanism (CDM) is one of the "flexibility"

mechanisms defined in the Kyoto Protocol (IPCC, 2007). It is defined in Article 12

of the Protocol, and is intended to meet two objectives: (1) to assist parties not

included in Annex I in achieving sustainable development and in contributing to

the ultimate objective of the United Nations Framework Convention on Climate

Change (UNFCCC), which is to prevent dangerous climate change; and (2) to

assist parties included in Annex I in achieving compliance with their quantified

emission limitation and reduction commitments (greenhouse gas (GHG) emission

caps). "Annex I" parties are those countries that are listed in Annex I of the treaty,

and are the industrialized countries.

The CDM allows industrialized countries to invest in emission reductions

wherever it is cheapest globally through renewable energy, energy efficiency, and

fuel switching. An industrialised country that wishes to get credits from a CDM

project must obtain the consent of the developing country hosting the project that

the project will contribute to sustainable development.

A report by-Hussain Mustafa Azad,JNSMS Page 72

Crediting mechanisms like the CDM could play three important roles in reducing the amount of (mitigating) future climate change:

Improve the cost-effectiveness of GHG mitigation policies in developed countries.

Help to reduce "leakage" (carbon leakage) of emissions from developed to developing countries.

Boost transfers of clean, less polluting technologies to developing countries.

NAME OF THE PROPOSAL:

Heat Recovery at Delayed Coking Unit by installing a new Heat Exchanger in RFO (Reduced Fuel Oil) rundown circuit.

1. BRIEF DESCRIPTION:

Delayed Coking Unit (DCU) of Guwahati Refinery was installed with

Rumanian Technology with a capacity of 0.33 MMTPA. Heat integration of the

unit was done by M/s Kinetic Technology of India (KTI) with installation of New

Charge Heater (03F101) and feed preheat exchanger trains. But, heat integration of

Reduced Fuel Oil (RFO) was not addressed during the said revamp. Opportunity

exists in RFO circuit to recover heat by integrating with generation of MPS in the

existing system. Further, Delayed Coking Unit of Guwahati Refinery has been

identified in Benchmarking Study conducted among all PSU refineries by M/s

A report by-Hussain Mustafa Azad,JNSMS Page 73

Shell Global Solutions at the request of MoP&NG. As per Benchmarking report

2008 , DCU is operating with higher Energy Index, which signifies that the unit

consumes more energy than theoretical/ benchmark energy figure of DCU of

similar capacity and has recommended to explore possibility of heat integration to

improve energy Index.

In light of above, this is a proposal to install a new exchanger in DCU to recover

additional heat from rundown stream. This recoverable heat energy, equivalent to

175 SRFT, is presently being rejected in Cooling Water System and thus being

wasted. The proposed exchanger is Reduced Fuel Oil (RFO) Vs Boiler Feed Water

(BFW) leading to increase in MP steam generation in Steam Generator section due

to increased BFW inlet temperature.

A report by-Hussain Mustafa Azad,JNSMS Page 74

2. COST ESTIMATE : Rs. 70.7 Lakhs- Price used are based on which year : 2008-09

- % of escalation amount : N/A

- % of custom duty : N/A

Budgetary cost estimate of exchanger contingency @ 10%. Datasheet of the proposed exchanger was sent to a Heat Exchanger vendor M/s Ozone Engineers, Kolkata. The party conducted the detailed thermal design of the heat exchanger and has submitted their budgetary offer for basic price of Rs. 9.58Lakhs for design, fabrication, testing ,commissioning and supply of the exchangers.

The total cost estimate including the additional expenses for piping, fittings, instruments and cost of execution works out to Rs.63.1Lakhs. Based on cost estimation of Engineering Services the total cost estimation of Heat Exchanger installation has worked out to be Rs 70.7 Lakhs .

3. JUSTIFICATION OF THE PROPOSAL

The envisaged energy saving potential of this process scheme is equivalent to 175 SRFT.. Considering SRF price of Rs. 18354/MT, similar to that of LSHS price of MoU 10-11, this translates in additional Gross Refinery Margin (GRM) of Rs.32.10 Lakhs/Annum.

With total investment cost of Rs. 70.7 lakhs, simple payback for the proposed AF project would be mere 2.85 years(without CDM) and 2.65 years ( with CDM). Reduction of 175 SRFT of fuel in boilers will lead to reduction of 567 MT of CO2 emission to the atmosphere translating to equivalent Carbon Emission Reduction

A report by-Hussain Mustafa Azad,JNSMS Page 75

(CER) of 567MT. This would provide an additional benefit of Rs. 2.55lakhs under CDM as it qualifies under technological barrier.

4. ADVANTAGES :

The increased heat recovery in the unit, due to installation of the new exchanger, would result in increased Medium Pressure generation from steam generator. This would reduce the energy consumption and hence the Energy Index of DCU.

The investment cost would be recovered in only 2.85 years and the installed heat exchanger would continue to yield recurring benefit.

ALTERNATIVE OPTION CONSIDERED, IF ANY: No.

CONSEQUENCE (ON PRODUCTION/ PROFIT/ EFFICIENCY ETC.,) IN CASE THE PROPOSAL IS NOT ACCEPTED:

i) LOSS OF PRODUCTION : No ii) LOSS OF PROFIT : Yesiii) LOSS OF EFFICIENCY : Yesiv) OTHERS (PLEASE SPECIFY) : Opportunity to maximize MPS

production ex DCU.

5. TECHNICAL FEASIBILITY :

a) EFFECT OF ENVIRONMENT, IF ANY : None b) TECHNICAL CONSTRAINTS, IF ANY : None

A report by-Hussain Mustafa Azad,JNSMS Page 76

6. IMPACT OF PROPOSAL OF MAN POWER :

a) WHETHER ADDITIONAL MANPOWER IS REQUIRED FOR RUNNING

THE FACILITY. IF YES, PLEASE FURNISH THE DETAILS IN THE FORM

OF AN ANNEXURE: No

b) IF ADDITIONAL MANPOWER IS REQUIRED, HOW THE SCHEME WILL

BE MANNED : No

c) WILL THE PROPOSAL RESULT IN SAVING MANPOWER FOR

DEVELOPMENT IN OTHER JOBS : No

7. OPERATIONING AND MAINTENANCE COST :

Power, Fuel & Utility cost : Nil

Salary & allowance : Nil

Repair & Maintenance cost : Rs. 0.9 Lakhs

(Considering 1.25% of Investment Cost)

Overheads & Insurance : Rs. 0.29 Lakhs

(Considering 0.4 % of Investment Cost)

Total Net Operating cost : Rs 1.19 Lakhs

8. REQUIREMENT OF ADDITIONAL WORKING CAPITAL, IF ANY : NIL(DETAILS TO BE ATTACHED)

A report by-Hussain Mustafa Azad,JNSMS Page 77

9. ECONOMICS:

a) PAY BACK PERIOD : 2.65 Years (With CDM)

2.3 Years (Without CDM)

b) INTERNAL RATE OF RETURN : 36.37% (With CDM)

33.72% (Without CDM)

c) ANY OTHER CRITERIA USED: ARR, NPV, PI, Discounted payback

period.

(Refer to below)

10.PHASING OF EXPENDITURE :

YEAR Rs.in Lakhs

2012 70.7 Lakh (100 % of total investment)

A report by-Hussain Mustafa Azad,JNSMS Page 78

11.CLASS OF PROPOSAL :

PRIORITY MARKS

STATUTORY REQUIREMENT [ X ] 20SAFETY ITEM [ X ] 20

ECONOMIC GROUNDS [ √ ] 18

OPERATIONAL NECESSITY [ √ ] 16 WELFARE / SOCIAL BENEFIT [ X ] 14

REPLACEMENT / ADD.OF ASSETS [ X ] 12

12. LEVEL OF DESIRABILITY : WEIGHTAGE

ESSENTIAL [ ] 5HIGHLY DESIRABLE [ ] 3

DESIRABLE [ ] 1.5

PRIORITY RANKING:

PRIORITY WEIGHTAGE TOTAL

MARKS MARKS

DEPT. UNIT HEAD [ 18 ] [ 3 ] [ 54 ]

UNIT ED / GM [ 18 ] [ 3 ] [ 54 ]

HEAD OFFICE [ ] [ ] [ ]

13.APPROVAL:In view of the foregoing condition, for additional heat recovery in DCU,it is

proposed to procure a new heat exchanger as per attached process datasheet,

information and install the same in the unit as per attached process scheme.

A report by-Hussain Mustafa Azad,JNSMS Page 79

14.COMPLETION SCHEDULE:

The project is estimated to be complete within 12 months from the date of

financial approval of the proposal. Chart for various activities envisaged for

completion and commissioning is attached below:

Benefit calculation for installation of RFO Exchanger at Delayed Coking Unit

A report by-Hussain Mustafa Azad,JNSMS Page 80