hayley moynihan food & agribusiness research and advisory rabobank 8 july 2013 winning through...

TRANSCRIPT

Hayley MoynihanFood & Agribusiness Research and AdvisoryRabobank

8 July 2013

Winning through the supply chain

Red Meat Sector Conference

2

3

Looking in the mirror

Supply chain dynamics

Looking forward

4

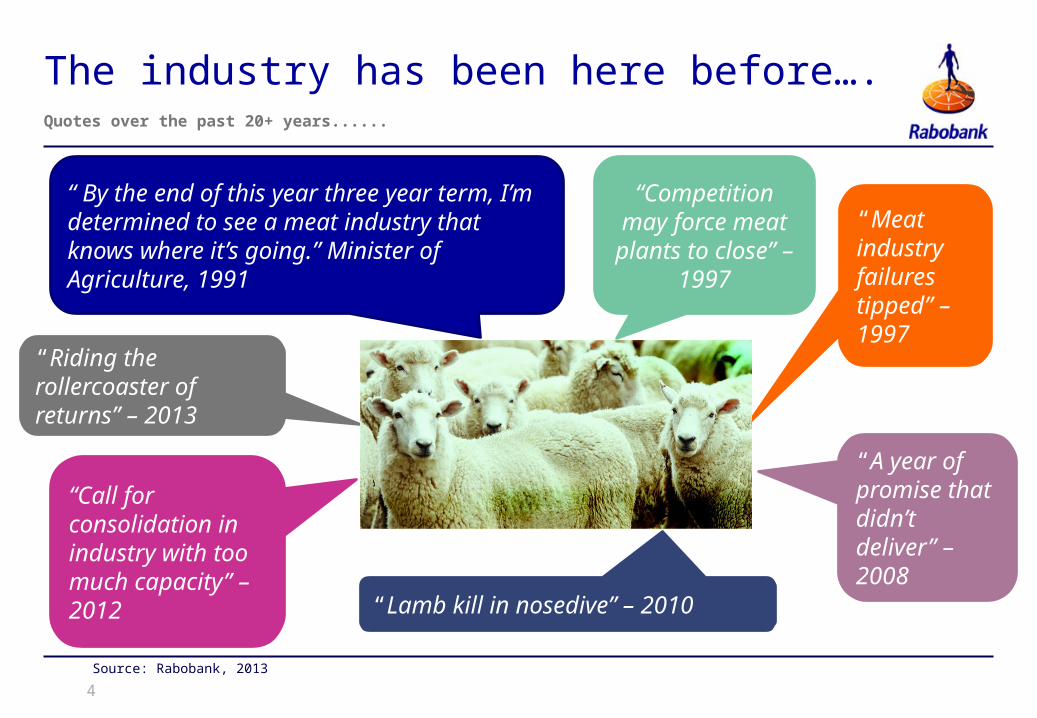

The industry has been here before….

Source: Rabobank, 2013

Quotes over the past 20+ years......

“ By the end of this year three year term, I’m determined to see a meat industry that knows where it’s going.” Minister of Agriculture, 1991

“Competition may force

meat plants to close” – 1997

“Meat industry failures tipped” – 1997

“A year of promise that didn’t deliver” – 2008

“Lamb kill in nosedive” – 2010

“Call for consolidation in industry with too much capacity” – 2012

“Riding the rollercoaster of returns” – 2013

5

Sheep flock has been in a constant decline

Source: Beef and Lamb NZ, Rabobank, 2013

Likely to get below 30 million head for the first time in over 50 years……19

7219

7319

7419

7519

7619

7719

7819

7919

8019

8119

8219

8319

8419

8519

8619

8719

8819

8919

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

12

25

30

35

40

45

50

55

60

65

70

75

Flock numbers

million h

ead

Over 30 years 35 million head less (down 50%), but processing capacity not adjusted to the same extent

6

Viability within the sector falling

Source: Rabobank, 2013

Particularly in relation to dairy

Mar

-09

Jun-

09

Sep-

09

Dec-0

9

Mar

-10

Jun-

10

Sep-

10

Dec-1

0

Mar

-11

Jun-

11

Sep-

11

Dec-1

1

Mar

-12

Jun-

12

Sep-

12

Dec-1

2

Mar

-13

Jun-

13

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

Dairy Sheep/Beef

Ea

sil

y v

iab

le a

nd

Via

ble

min

us

Just

via

ble

an

d U

nvia

ble

7

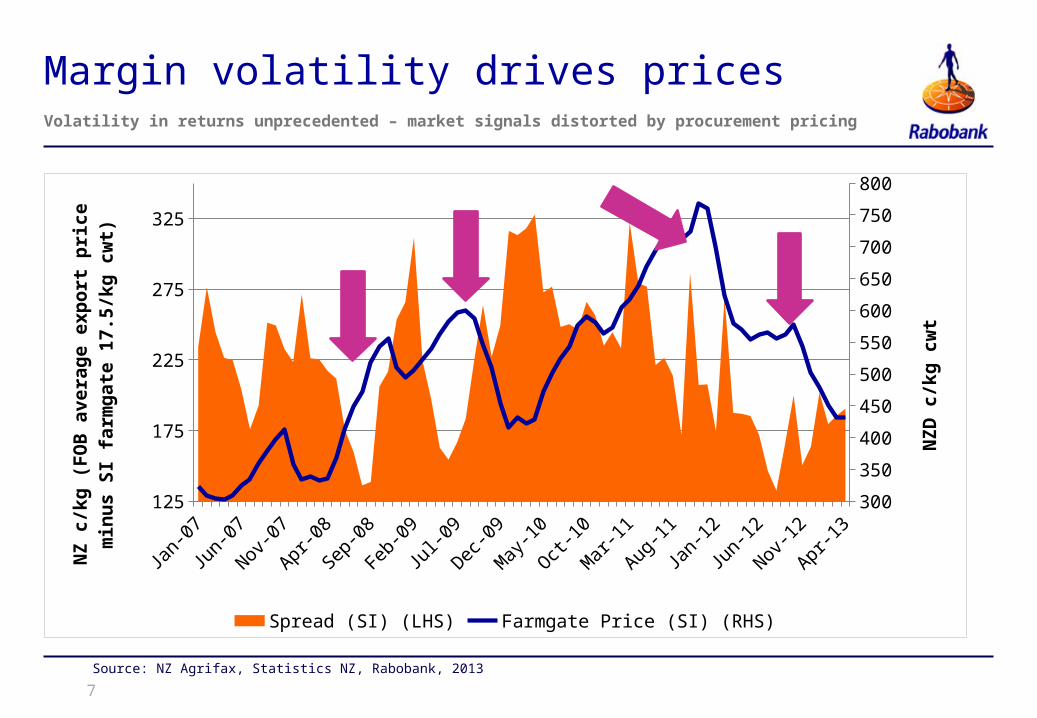

Margin volatility drives prices

Source: NZ Agrifax, Statistics NZ, Rabobank, 2013

Volatility in returns unprecedented – market signals distorted by procurement pricing

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13125

175

225

275

325

300

350

400

450

500

550

600

650

700

750

800

Spread (SI) (LHS) Farmgate Price (SI) (RHS)

NZ

c/k

g (

FO

B a

ve

rag

e e

xp

ort

p

rice

min

us S

I fa

rmg

ate

17

.5/k

g

cw

t)

NZ

D c

/kg

cw

t

8

Pressuring margins for processors too

Source: Annual reports, 2013

Small or negative margins across the supply chain

2008 2009 2010 2011 2012

-4%

-2%

0%

2%

4%

6%

8%

EB

IT/o

pe

rati

ng

pro

fit

ma

rgin

9

Déjà vu – supply chain tough to manageLooking in the mirror

Supply chain dynamics

Looking forward

10

Global food and agri markets have changed

Source: Rabobank, 2013

Red meat sector needs to evolve too, with greater coordination

11

The ultimate dilemma for both parties

Source: Rabobank, 2013

Which risks can you afford to live with and which can be managed?

Sellers’ dilemma

Buyers’ dilemma

12

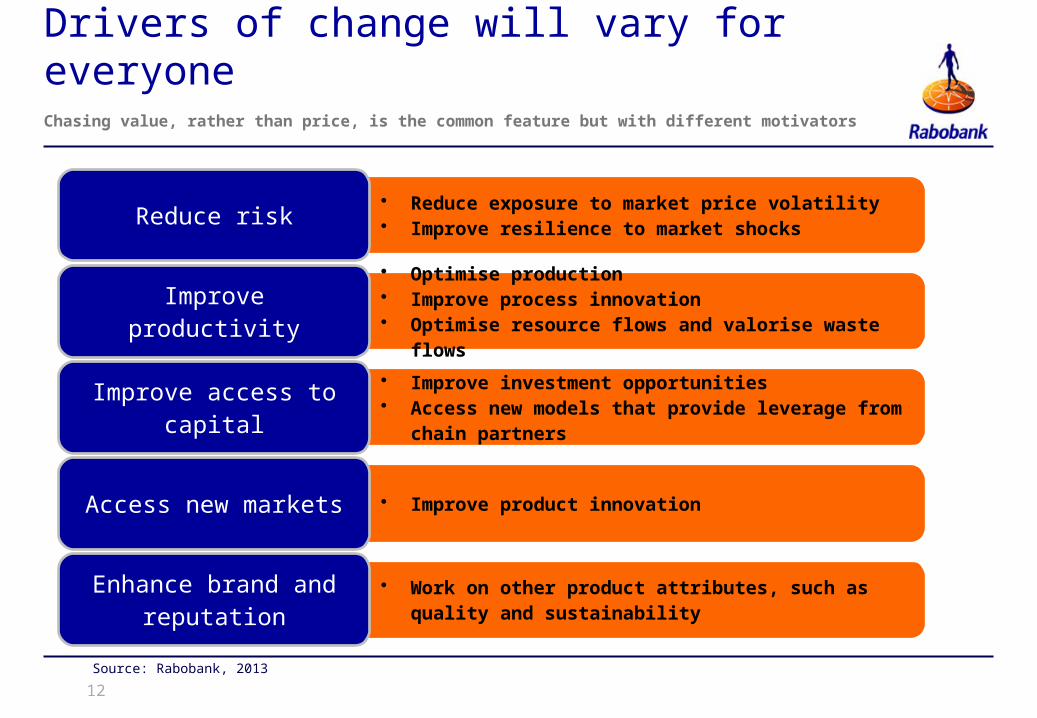

Drivers of change will vary for everyone

Source: Rabobank, 2013

Chasing value, rather than price, is the common feature but with different motivators

• Reduce exposure to market price volatility• Improve resilience to market shocksReduce risk

• Optimise production• Improve process innovation• Optimise resource flows and valorise waste

flows

Improve productivity

• Improve investment opportunities• Access new models that provide leverage from

chain partners

Improve access to capital

• Improve product innovationAccess new markets

• Work on other product attributes, such as quality and sustainability

Enhance brand and reputation

13

Example: UK dairy industryFocus on price may come at the expense of efficient supply chains

Over the last decade; production down 8%, farm numbers down 44% (10,000), average herd size doubled

Initial strategy to drive costs out of the business due to price pressure and industry shrinking

Processors have since consolidated, been acquired by multinational brand players and diversified their product range

New processing capacity and lower milk supply resulted in procurement competition heating up

“Voluntary code of best practice on contracts”

14

Example - MSA program Australia

Source: MLA’s NLRS Rabobank, 2013

Premiums obtained in all segments across the supply chain

18

0 - 2

20

kg

22

0 - 2

60

kg

26

0 - 2

80

kg

18

0 - 2

20

kg

22

0 - 2

60

kg

26

0 - 2

80

kg

0

10

20

30

40

50

60

MSA yearling cattle price differential 2012

NSWQLD

Heifers

c/k

g c

wt

Steers

• MSA is a beef and sheepmeat eating quality programme

• Designed to assure buying, eating and cooking quality for consumers

• Extensive research involving farm practices, processing, cuts, ageing periods and cooking methods

• MSA requires standards to be maintained from paddock to plate

15

Déjà vu – supply chain tough to manage

Adding value rather than chasing price

Looking in the mirror

Supply chain dynamics

Looking forward

16

Status quo + less scale = unsustainable

Source: Rabobank, 2013

But increases the necessity for addressing overcapacity - larger scale operators feel heat first

20

14

f

20

13

f

20

12

20

11

20

10

20

09

20

08

-

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

All other companies (excl Alliance, Affco & SFF)

AFFCO

Silver Fern Farms Limited

Alliance Group Lim-ited

* based on extrapolation of quota allocations in each year

17

Key considerations for the meat sector

Source: Rabobank, 2013

Which risks can you afford to live with and which can be managed?

Farmers’ dilemma

Processors’ dilemma

Need to manage efficiency, higher

prices and volatility

Need to secure share of limited

supply

How much margin or certainty to offer suppliers?

Will returns be better if I play the

open market?

Why commit to a processor?

Should I invest further capital in the supply chain?

18

A different path needs to be trodden carefullySupply chain behaviour needs to align with ambition

The red meat sector fundamentally has a positive market outlook BUT a shrinking industry is the greatest risk and reduces options

The status quo is not sustainable for all participants – efficiencies lost will hinder competitiveness

Change is needed – but must be based on greater value for consumers and a more efficient supply chain

Change also carries risks in execution; transactional costs and maintaining market share

Capital will be needed to support restructuring of the supply chain

Supply chain relationships and commitment will be key to extracting value

19

Déjà vu – supply chain tough to manage

Adding value rather than chasing price

Change is inevitable - scale needed for success

Looking in the mirror

Supply chain dynamics

Looking forward

20

Rabobank contact details

Rabobank International

Hayley MoynihanFood & Agribusiness Research and Advisory

t. +64 3 341 4218

DISCLAIMERThis document is issued by Rabobank New Zealand Limited incorporated in New Zealand (“Rabobank”). The information and opinions contained in this document have been compiled or arrived at from sources believed to be reliable, but no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. This document is for information purposes only and is not, and should not be construed as, an offer or a commitment by Rabobank or any of its affiliates to enter into a transaction. This information is not professional advice and has not been prepared to be used as the basis for, and should not be used as the basis for, any financial or strategic decisions. This information is general in nature only and does not take into account an individual’s personal circumstances. All opinions expressed in this document are subject to change without notice. Neither Rabobank, nor other legal entities in the group to which it belongs, accept any liability whatsoever for any direct, indirect, consequential or other loss or damage howsoever arising from any use of this document or its contents or otherwise arising in connection therewith. This document may not be reproduced, distributed or published, in whole or in part, for any purpose, except with the prior written consent of Rabobank. All copyrights, including those within the meaning of the Copyright Act 1968 (Cth), are reserved. New Zealand law shall apply. By accepting this document you agree to be bound by the foregoing restrictions. © Rabobank New Zealand Limited, Level 23 157 Lambton Quay, Wellington NI 6011 New Zealand, +64 4 819 2700

“The financial link in the global food chain”™

Food & Agribusiness Research and Advisory