handset industry 2013 outlook

TRANSCRIPT

DISCLOSURE APPENDIX CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, INFORMATION ON TRADE ALERTS, ANALYST MODEL PORTFOLIOS AND THE STATUS OF NON-U.S ANALYSTS. FOR OTHER IMPORTANT DISCLOSURES, visit www.credit-suisse.com/researchdisclosures or call +1 (877) 291-2683 US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION™

Client-Driven Solutions, Insights, and Access

07 January 2013

Americas/United States

Equity Research

Telecommunications Equipment / MARKET WEIGHT

Handset Industry 2013 Outlook INDUSTRY PRIMER

Bigger market, Apple and Samsung win

■ Market size underestimated for both smartphones/handsets. Our bottom-up analysis suggests that the market underestimates the size of low-end ‘white-label’ smartphones, which causes us to restate our 2012/2013 volume estimates for the smartphone market higher by 6%/15% and 3%/4% for overall handsets. We also raise our smartphone volume estimates by 20-25% long term and now estimate 1.43bn/1.74bn smartphones to be shipped in 2015/2017. We believe that the growth of ‘white-label’ smartphone market specifically poses a threat for vendors like Nokia, RIMM, LG and possibly Samsung, given their exposure to feature phones and low-end smartphone segments.

■ Raising LT smartphone units to 1.74bn – a barbell develops for price points. We believe that the addressable market for smartphones is 4.95bn longer term, resulting in effective penetration of only 24% currently given our estimate of 1.2bn smartphone users by end of 2012. We expect effective smartphone penetration to rise to ~80% long term driving smartphone volumes of 1.43bn/1.74bn units by 2015/2017 (26%/19% CAGR over this period). By price point, we continue to see the high-end of the smartphone market rising to unprecedented levels increasing from 190mn units in 2011 to 300/400mn units in 2012/2013 (>40% of smartphone volumes), but equally see the low-end (<$200 ASP) to rise from 19% of smartphone volumes in 2012 to 25%/43% by 2013/2015 mainly driven by MediaTek and Spreadtrum ecosystem.

■ CS smartphone vendor scorecard – Apple and Samsung lead. We continue to rely on our proprietary smartphone vendor scorecard which is based on nine metrics (software, services, cloud, product, brand, distribution, compute convergence, IPR and chipset efficiency), which we think drive success in smartphones. We conclude that secular share gainers will be Samsung, Apple and Huawei, while other vendors will struggle to make returns.

■ Apple – compute advantage gives it a sustainable edge, reiterate OP. Increasingly, success in smartphones will be impacted by success in PCs and tablets. The ability to compete across all segments will be driven by software, services and hardware offerings across device types, with success in one area driving increased demand in the other. In this new paradigm of the compute market, Apple remains best positioned. Even with its current price point, we expect Apple’s smartphone share to rise from 19% in 2012 to 20% in 2013, driven by expanding distribution and an innovation advantage.

■ Nokia – a challenging turnaround. With limited differentiation for Windows Phone 8, strong competition and slow portfolio roll out, we see Nokia’s smartphone share falling further from 5% to 2% in 2013. In addition, accelerating growth in low-end Android presents further cannibalization risks to its Mobile Phone business. All of this means that cash burn will remain high, and we see net cash excl. NSN dropping from €2.6bn in 2012 to €0.8bn by the end of 2013.

■ RIMM – is there room for BB10? Despite excitement around upcoming new portfolio announcements, we believe it is too late with too little differentiation for BB10 to create material traction in the smartphone market. Consequently, we keep our Neutral rating.

Research Analysts

Kulbinder Garcha

212 325 4795

Achal Sultania

44 20 7883 6884

Talal Khan, CFA

212 325 8603

Matthew Cabral

212 538 6260

Ray Bao

212 325 1227

Asian Research Analysts

Randy Abrams, CFA

886 2 2715 6366

Keon Han

822 3707 3740

Pauline Chen

886 2 2715 6323

Yan Taw Boon

852 2101 7039

Thompson Wu

886 2 2715 6386

07 January 2013

Handset Industry 2013 Outlook 2

Executive summary The smartphone market has continued to defy expectations in recent years; indeed, we

note that a combination of fast innovation at the high end and lower cost handsets have

made the smartphone market mainstream, systematically cannibalizing several consumer

electronics (CE) products. In fact, we estimate that smartphones will account for nearly

35% of CE spend globally in 2012. At the same time, while smartphone growth is indeed

strong, the spoils are not being equally shared. So where to now? In this note, our

extensive review of the smartphone market arrives at three main conclusions. First, the

emergence of a robust white-label market is developing in smartphone so much so that

most market observers are underestimating the actual size of the smartphone market.

Second, we see continued and unprecedented growth in the high end of smartphone

market, i.e., at above $400 ASP. Finally, in terms of winners and losers, we believe Apple

and Samsung will remain truly dominant and the rest of the industry will struggle to be

even at breakeven levels in terms of handset profitability.

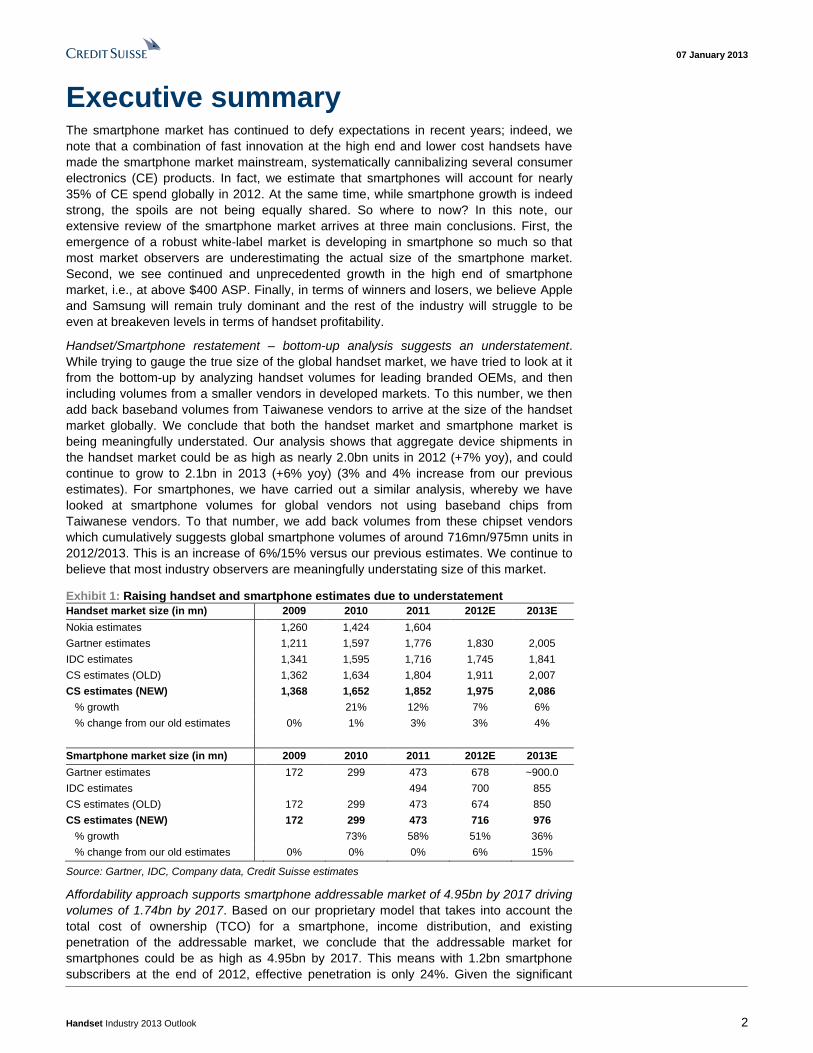

Handset/Smartphone restatement – bottom-up analysis suggests an understatement.

While trying to gauge the true size of the global handset market, we have tried to look at it

from the bottom-up by analyzing handset volumes for leading branded OEMs, and then

including volumes from a smaller vendors in developed markets. To this number, we then

add back baseband volumes from Taiwanese vendors to arrive at the size of the handset

market globally. We conclude that both the handset market and smartphone market is

being meaningfully understated. Our analysis shows that aggregate device shipments in

the handset market could be as high as nearly 2.0bn units in 2012 (+7% yoy), and could

continue to grow to 2.1bn in 2013 (+6% yoy) (3% and 4% increase from our previous

estimates). For smartphones, we have carried out a similar analysis, whereby we have

looked at smartphone volumes for global vendors not using baseband chips from

Taiwanese vendors. To that number, we add back volumes from these chipset vendors

which cumulatively suggests global smartphone volumes of around 716mn/975mn units in

2012/2013. This is an increase of 6%/15% versus our previous estimates. We continue to

believe that most industry observers are meaningfully understating size of this market.

Exhibit 1: Raising handset and smartphone estimates due to understatement

Handset market size (in mn) 2009 2010 2011 2012E 2013E

Nokia estimates 1,260 1,424 1,604

Gartner estimates 1,211 1,597 1,776 1,830 2,005

IDC estimates 1,341 1,595 1,716 1,745 1,841

CS estimates (OLD) 1,362 1,634 1,804 1,911 2,007

CS estimates (NEW) 1,368 1,652 1,852 1,975 2,086

% growth 21% 12% 7% 6%

% change from our old estimates 0% 1% 3% 3% 4%

Smartphone market size (in mn) 2009 2010 2011 2012E 2013E

Gartner estimates 172 299 473 678 ~900.0

IDC estimates 494 700 855

CS estimates (OLD) 172 299 473 674 850

CS estimates (NEW) 172 299 473 716 976

% growth 73% 58% 51% 36%

% change from our old estimates 0% 0% 0% 6% 15%

Source: Gartner, IDC, Company data, Credit Suisse estimates

Affordability approach supports smartphone addressable market of 4.95bn by 2017 driving

volumes of 1.74bn by 2017. Based on our proprietary model that takes into account the

total cost of ownership (TCO) for a smartphone, income distribution, and existing

penetration of the addressable market, we conclude that the addressable market for

smartphones could be as high as 4.95bn by 2017. This means with 1.2bn smartphone

subscribers at the end of 2012, effective penetration is only 24%. Given the significant

07 January 2013

Handset Industry 2013 Outlook 3

increase in smartphones being available at sub-$100, we see this rising to around 80%

long term, reaching 3.9bn users, i.e. 79% of the 4.95bn addressable market. In turn, even

assuming a moderate decline in replacement rates, smartphone volumes will grow to

1.74bn by 2017, almost 2.5x from levels in 2012, and seeing a CAGR of 19% over the

next five years.

Exhibit 2: We estimate smartphone market to be 716mn/976mn units in 2012/2013, growing to 1.74bn by 2017

Global Handset Volumes 2008 2009 2010 2011 2012E 2013E 2014E 2015E 2016E 2017E CAGR ‘12-‘17

Basic Phones 407 432 530 593 612 615 607 607 591 548 -2.2%

Feature Phones 761 763 823 787 646 495 324 177 107 49 -40.3%

Smartphones 139 172 299 473 716 976 1,219 1,425 1,577 1,737 19.4%

Total (in mn) 1,307 1,368 1,652 1,852 1,975 2,086 2,149 2,209 2,275 2,334 3.4%

Global Handset Volume Mix

Basic Phones 31% 32% 32% 32% 31% 30% 28% 28% 26% 24% NM

Feature Phones 58% 56% 50% 42% 33% 24% 15% 8% 5% 2% NM

Smartphones 11% 13% 18% 26% 36% 47% 57% 65% 69% 74% NM

Total (in %) 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% NM

Source: Gartner, Company data, Credit Suisse estimates

A barbell develops in the smartphone market as the mid-end shrinks. We believe that the

smartphone market at $400+ ASP will grow over 4x in volume terms over 2010 to 2013

reaching nearly 400mn units by 2013, before seeing some moderation in growth. This

combined with our view around volume growth in <$200 ASP market (driven by white-label

vendors in China/India) means that smartphone volumes in the $200 to $400 ASP range

will only grow from ~300mn units in 2012 to ~400mn units by 2015. Specifically, we see

this low-end market (<$200 ASP) being enabled by a plethora of low-end launches (our

portfolio database shows 74 low-end smartphone models out of 425 models we tracked

from branded vendors) as well as low cost chipset efforts from MediaTek, Spreadtrum and

also Qualcomm. For the mid-end segment, we expect it to decline from 40% of total

smartphone volumes in 2012 to ~25% by 2015. This continued shift towards high-end now

combined with move towards low-end means that a number of branded OEMs including

RIM, Nokia, LG, Sony Mobile may continue to struggle given stiff competition in the high-

end from Apple and Samsung driven by better smartphone offering, and then aggressive

pricing from white-label vendors in the low-end.

LTE at an inflection point. We expect rapid growth in LTE devices to be driven by the

confluence of several factors, including the launch on an LTE iPhone, increasing handset

availability (we note that there are some 75 LTE smartphones available in the market out

of a total of 425 smartphones from branded OEMs). Further, we see Samsung’s robust

growth in the high-end segment as another significant driver of LTE device uptake. Further,

this is being supported by expanding LTE network coverage as Korea and Japan were

seen as early adopters of LTE, but carriers’ network rollout plans in the US and China

point to a rapid expansion of LTE network coverage over the next 2-3 years.

The importance of compute. Historically we would argue that handset, PC and other CE

devices were largely independent purchases by a consumer or corporation to fulfill a

specific need. However, the growth of smartphones has now evolved to a degree whereby

consumers and corporations demand access to their key digital content across multiple

devices. In this context, smartphone success also needs to take into account the ability of

the entire platform. Looked at from a hardware perspective, success in smartphones will

be determined by the ability to simultaneously execute in the PCs and tablet market, and

perhaps the TV market as well in the long term. In this new world, success will no longer

be judged by category unit share alone, whether it be in smartphones, mobile phones,

tablets or PCs, but in the combined compute segment.

The importance of value share. While Android continues to enjoy its dominance in the

smartphone market and indeed with a market share of 70-75% in unit terms, this cannot

07 January 2013

Handset Industry 2013 Outlook 4

be simply ignored. However, we do equally believe that scale also should be reflected by

value share, and further due to the significant volume growth we expect in the low-end

smartphone segment, this issue will be further exacerbated. Looking at value share in the

smartphone market, we see Apple and Samsung to remain #1 and #2 vendor in terms of

value share as we see Others category (non-branded OEMs) to account for 28% of

volume share in 2013 but still less than 15% value share.

Exhibit 3: Apple and Samsung to remain leaders in the smartphone market

Smartphone unit share (%) 2010A 2011A 2012E 2013E Smartphone value share (%) 2010A 2011A 2012E 2013E

Apple 16% 19% 19% 20% Apple 30% 36% 38% 40%

Samsung 9% 19% 29% 32% Samsung 8% 17% 27% 31%

Nokia 34% 18% 5% 2% Nokia 21% 10% 3% 1%

HTC 8% 9% 5% 5% HTC 10% 9% 4% 4%

Motorola 5% 4% 3% 2% Motorola 5% 4% 3% 1%

Sony 3% 4% 3% 2% Sony 4% 4% 3% 2%

Huawei 0% 3% 4% 5% Huawei 0% 2% 2% 2%

Research in Motion 17% 11% 5% 3% Research in Motion 16% 10% 3% 2%

LG 2% 4% 4% 4% LG 1% 3% 3% 2%

Others 6% 9% 24% 28% Others 5% 6% 13% 14%

Total 100% 100% 100% 100% Total 100% 100% 100% 100%

Source: Company data, Credit Suisse estimates

Apple – compute advantage gives competitive edge

Specifically in smartphones, we see Apple as continuing to gain share with its smartphone

share rising to 20% in 2013 up from 19% in 2012 driven by several factors:

Ranking first on our scorecard. Even 5 years after the first iPhone launch, Apple continues

to rank above peers, specifically when looking at our proprietary scorecard which takes in

to account 9 key factors ranging from software and services to brand and distribution,

Apple ranks #1, which is a reflection of the underlying strengths of the business. We

currently assume Apple will be able to consolidate its smartphone market share to 20% in

2013, up from 19% in 2012.

Expanding carrier distribution can drive an extra 75mn units per year. We specifically see

an opportunity for Apple to grow units through expanded carrier distribution. In fact, as

Apple scales its distribution, we estimate that the next 50 largest carriers could increase

iPhone units by around 75mn annually, compared to 138mn units we assume for 2012.

Compute advantage gives the competitive edge. Perhaps the biggest advantage for Apple

is being driven by the company’s ability to compete in the compute market, i.e.,

smartphones, tables and PC like no other vendor. Add to this, the broad range of “i-

Services” that are built well beyond iTunes, to include the Apps Store, iAd services, iBooks

and iCloud, the company allows consumers to seamlessly access content across multiple

devices. The issue is that when considered in the context of the entire compute market in

volume terms Apple has a ~18% share, which will rise given its exposure to the relatively

faster growing smartphone and tablet end markets towards 22% longer term. However,

this is unlikely to be dominant. Should Apple want to maximize this, we retain our view that

the company may want to consider launching a lower end iPhone.

Valuation. With solid product cycles in the back half of 2012 and shares trading on a P/E

of 8.8x our CY13 EPS, Apple remains inexpensive in the context of 30% bottom-line

growth and $128 of net cash per share.

Nokia – still a challenging turnaround

For Nokia, we retain our below consensus EPS estimates of €(0.28)/€(0.24), in particular

the company continues to face material challenges in turning the business around over the

07 January 2013

Handset Industry 2013 Outlook 5

next 12 months. This, combined with our concerns around cash burn, leads us to reiterate

our Underperform rating.

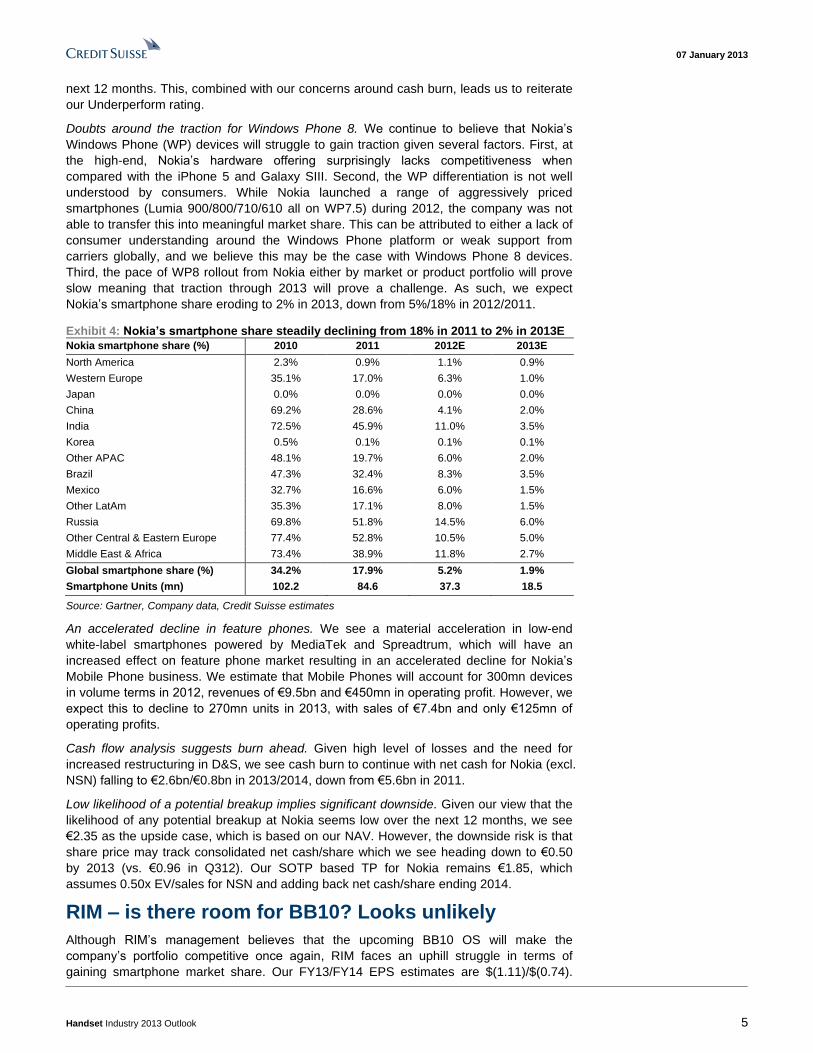

Doubts around the traction for Windows Phone 8. We continue to believe that Nokia’s

Windows Phone (WP) devices will struggle to gain traction given several factors. First, at

the high-end, Nokia’s hardware offering surprisingly lacks competitiveness when

compared with the iPhone 5 and Galaxy SIII. Second, the WP differentiation is not well

understood by consumers. While Nokia launched a range of aggressively priced

smartphones (Lumia 900/800/710/610 all on WP7.5) during 2012, the company was not

able to transfer this into meaningful market share. This can be attributed to either a lack of

consumer understanding around the Windows Phone platform or weak support from

carriers globally, and we believe this may be the case with Windows Phone 8 devices.

Third, the pace of WP8 rollout from Nokia either by market or product portfolio will prove

slow meaning that traction through 2013 will prove a challenge. As such, we expect

Nokia’s smartphone share eroding to 2% in 2013, down from 5%/18% in 2012/2011.

Exhibit 4: Nokia’s smartphone share steadily declining from 18% in 2011 to 2% in 2013E

Nokia smartphone share (%) 2010 2011 2012E 2013E

North America 2.3% 0.9% 1.1% 0.9%

Western Europe 35.1% 17.0% 6.3% 1.0%

Japan 0.0% 0.0% 0.0% 0.0%

China 69.2% 28.6% 4.1% 2.0%

India 72.5% 45.9% 11.0% 3.5%

Korea 0.5% 0.1% 0.1% 0.1%

Other APAC 48.1% 19.7% 6.0% 2.0%

Brazil 47.3% 32.4% 8.3% 3.5%

Mexico 32.7% 16.6% 6.0% 1.5%

Other LatAm 35.3% 17.1% 8.0% 1.5%

Russia 69.8% 51.8% 14.5% 6.0%

Other Central & Eastern Europe 77.4% 52.8% 10.5% 5.0%

Middle East & Africa 73.4% 38.9% 11.8% 2.7%

Global smartphone share (%) 34.2% 17.9% 5.2% 1.9%

Smartphone Units (mn) 102.2 84.6 37.3 18.5

Source: Gartner, Company data, Credit Suisse estimates

An accelerated decline in feature phones. We see a material acceleration in low-end

white-label smartphones powered by MediaTek and Spreadtrum, which will have an

increased effect on feature phone market resulting in an accelerated decline for Nokia’s

Mobile Phone business. We estimate that Mobile Phones will account for 300mn devices

in volume terms in 2012, revenues of €9.5bn and €450mn in operating profit. However, we

expect this to decline to 270mn units in 2013, with sales of €7.4bn and only €125mn of

operating profits.

Cash flow analysis suggests burn ahead. Given high level of losses and the need for

increased restructuring in D&S, we see cash burn to continue with net cash for Nokia (excl.

NSN) falling to €2.6bn/€0.8bn in 2013/2014, down from €5.6bn in 2011.

Low likelihood of a potential breakup implies significant downside. Given our view that the

likelihood of any potential breakup at Nokia seems low over the next 12 months, we see

€2.35 as the upside case, which is based on our NAV. However, the downside risk is that

share price may track consolidated net cash/share which we see heading down to €0.50

by 2013 (vs. €0.96 in Q312). Our SOTP based TP for Nokia remains €1.85, which

assumes 0.50x EV/sales for NSN and adding back net cash/share ending 2014.

RIM – is there room for BB10? Looks unlikely

Although RIM’s management believes that the upcoming BB10 OS will make the

company’s portfolio competitive once again, RIM faces an uphill struggle in terms of

gaining smartphone market share. Our FY13/FY14 EPS estimates are $(1.11)/$(0.74).

07 January 2013

Handset Industry 2013 Outlook 6

Although we retain our Neutral rating given the risk of a takeout at some point, both

fundamentals and NAV analysis suggest downside risks.

Launch of first two BB10 smartphones to be announced in January 2013. After having

seen multiple delays in launch of BB10 platform, RIM has announced that it will officially

launch its new BB10 OS as well as unveil its first two BB10 smartphones in an event on

January 30, 2013. So we have yet to see the specifications of the actual device. However,

in order to develop an ecosystem around its new BB10 OS, RIM has already issued

developers its BB10 Dev Alpha smartphone, although this is not the final product. While

we acknowledge that the new OS shows marked improvement vs. previous versions, we

still believe that it faces fierce competition from existing platforms such as Android and iOS,

given most of the features offered by new BB10 is already being offered by rivals, which

also benefit from presence of a strong ecosystem around their platforms.

A high price point could be detrimental to adoption. We believe that one of the reasons for

the delay in launching BB10 devices could have been RIM’s dependence on Qualcomm’s

Snapdragon 8960 processor, which has seen constraints during 2012 due to 28nm

capacity shortage. What this also may imply that the new BB10 smartphones could be

highly spec’d devices targeting at a high price point. We simply do not believe much of a

share opportunity exists in the high end of the market, given the success seen by Apple

and Samsung in that segment of the market.

Running out of the services revenue stream. One of the benefits that RIM had in the past

was that its strong Services revenue stream had been more or less stable so far over the

last few quarters. However, we believe that visibility of the services revenue stream is

rapidly deteriorating given BB10 monetization of the NOC, ongoing carrier renegotiation

and declining subscribers. This means that service revenue should fall, and we note the

recent quarter marks the first time management has discussed its expectation that some

of the base may generate no service revenue. We assume services revenue of

$3.9bn/$3.3bn in FY13/14, down 4%/16% y/y, further compounding issues around

profitability. In turn, this would expose the company’s high level of hardware losses which

we estimate could be as high as $3.5bn/$2.7bn in FY13/FY14.

NAV of $3.1bn (or $5.9/share). A combination of the late arrival of BB10 devices, as well

as a fiercely competitive environment, hinders RIM’s ability to turnaround its handset

business and estimate its global smartphone share declining to 3% in 2013 (vs. 5% in

2012). A break up is possible, however, we question the quality of the underlying IPR and

also believe that converting its existing NOC for other OS platforms may require a high

level of effort for minimal functionality improvement. Our NAV estimate for RIM is about

$3.1bn, and requires the acquirer to take over the company and shut down its hardware

business. At current levels, RIM does not offer meaningful upside and selling the company

will prove to be a challenge, although the appointment of bankers, the relatively small size

of a transaction, and ongoing positive FCF results in us maintaining our Neutral rating and

$11 TP (based on applying 0.3x EV/sales multiple to our FY14 estimate).

Lenovo – eyes on #1 spot in China smartphones

On Dec 28, 2012, CS raised its estimates and target price of Lenovo (covered by

Thompson Wu), and reiterated an Outperform rating. CS analyst Thompson Wu cited

positive smartphone demand in China, and improving momentum at Lenovo through

select country expansion, thus raising estimates. This is driven by his view that Lenovo

has the tools to build a profitable smartphone business long-term in China/Asia-Pac, and a

sound strategy to do so. Thompson Wu expects Lenovo to ship 25mn/38mn smartphones

in FY13/FY14, up from ~4mn in FY12. Of these, we expect the company to ship 94%/84%

respectively of its overall shipments in China. These estimates would imply Lenovo’s

China smartphone market share reaches around 10% in CY12/CY13.

Gain a strong China foothold. We expect China to account for around 30% of global

smartphone market by 2015 in volume terms. China happens to be Lenovo’s core market

07 January 2013

Handset Industry 2013 Outlook 7

generating 44%/67% of revenues/op profits YTD FY13. Lenovo can leverage its China PC

position (33% PC share YTD ‘12), localized manufacturing, PC supply chain advantages

(i.e. distribution), a popular China brand, and operational experience in the region as a

stepping stone for its smartphone business.

Selective country expansion. Lenovo is not initially building a global smartphone business.

Instead, Lenovo is focused on China and expanding into select Asia-Pac/Eastern

European countries with a large and fast growing smartphone market opportunity. In the

Dec 2012 quarter, Lenovo has entered into India (#1 in PC share), Indonesia (#3),

Philippines (#2), and Russia (#3). These are countries in which it also has top three PC

market and infrastructure investments we believe it can leverage such as distribution and

marketing. Lenovo plans to double its countries-addressed in FY14 to 10, from 5 in FY13.

Expand and strength operator relationships, leverage China distribution advantage.

Operator support is needed to deepen its penetration in China, expand into new countries,

and enter the high-end smartphone market. This latter is a market we expect Lenovo will

attack in FY14, and Lenovo will compete with other smartphone vendors (i.e.

Apple/Samsung) for subsidies and marketing dollars. According to Lenovo, roughly half of

China smartphones are sold through open-channels, which can yield 3x better gross

margins vs. operator channels. To date, more than 70% of Lenovo’s smartphones sold

have been through operators. Indeed, Lenovo will eventually leverage its China

distribution advantage once it achieves a certain level of scale, and having developed its

operator relationships. In China currently, it is deliberately choosing to distribute its popular

smartphones through operators, rather than use its own distribution, in efforts to build a

longer-lasting operator relationship. It is working with China Unicom, China Mobile, and

China Telecom and looks to balance distribution amongst the three operators in FY14.

Valuation. Lenovo’s operational leverage is a key focal point for investors next year. We

forecast its corporate operating will rise to 2.6% in FY14E (vs. 2.3% in FY13E) and for

earnings to grow ~28% (CS/Consensus of US$0.74/$0.69) driven by scaling benefits in

both its PC and MIDH business. Lenovo is trading at 13.2x our FY14E EPS (7.5x ex-cash).

Asian beneficiaries across the ecosystem

Based on bottom up analysis of smartphone chipsets for Asian built smartphones

(excluding Korean handset vendors), our Asian semiconductor analyst, Randy Abrams,

believes that has shown a ramp from 68mn units in 2011 to 244mn units in 2012. He

projects these units expanding to 816mn units in 2015, offering growth of 83% in 2013,

40% in 2014, and 31% in 2015, a substantial unit opportunity for several suppliers to

provide revenue growth even in the face of price competition. He also expects Mediatek to

lead the market, ramping from 110mn units in 2012 to 220mn in 2013 and 370mn units by

2015, with Spreadtrum achieving similar 25% share to feature phones as it expands from

31mn units in 2012 to 199mn units by 2015. The upstart is RDA which is taking material

share in feature phones and will sample its EDGE chipset from this quarter for 2H13

volumes. He expects Qualcomm to be the most material overseas competitor, with Marvell

only having high-end TD traction and Broadcom still needing to demonstrate inroads.

Looking at the beneficiaries across the smartphone ecosystem in Taiwan, Randy Abrams

notes his preference to own the space through the manufacturers benefiting from unit

growth (TSMC, ASE), IC design companies at reasonable valuations (Spreadtrum and

RDA – note Mediatek is restricted), and Asian devices gaining share (ZTE and Lenovo).

Within foundry, he downgrades UMC from Outperform to Neutral with same NT$14 target

(0.85x P/B) (reduced mobile leverage as Texas Instruments exits and Mediatek shifts to

28nm) and upgrades SMIC (turnaround and China smartphone and tablet leverage) and

raises his TP from HK$0.41 (0.7x P/B) to HK$0.57 (1x P/B). For details, please refer his

detailed note on China smartphone sector titled ‘Global handset forecast lifted by

emerging market demand’ also published concurrently.

07 January 2013

Handset Industry 2013 Outlook 8

Restating & raising smartphones Before even considering projection of smartphone volumes, it is essential to have the

correct historic estimates. The issue facing the handset industry in recent years has been

the size of the white-label market, and our analysis suggests both the handset and

smartphone markets at least in volume terms are being meaningfully understated. Next

when it comes to forecasting, most of the long-term forecasts for smartphone volumes are

based on an estimate of smartphones increasing as a percentage of the overall mobile

handset market. However, given that smartphones continue to be significantly more

expensive than a low-end phone, we continue to believe that any long-term forecast has to

be based on linking the income distribution and total cost of ownership to device

affordability. As such, we have again refreshed our proprietary analysis to look at the

smartphone market from an affordability perspective while taking in to account the total

cost of ownership (TCO) or ASP of a smartphone which is often overlooked. The

conclusion is that when we factor in the rising availability of lower end smartphones, we

see an increase in the total number of people globally who can afford to buy a

smartphone, either with a monthly data plan, or at times even without it especially in some

of the developing markets like China and India.

Raising and restating the market size as both handsets and smartphones are being

underestimated. A lingering issue for the global handset market over recent years, which

has often been debated, is the actual size of the market in volume terms. In fact, we note

there is a wide spread of handset estimates that currently exist for 2011/2012, as shown in

Exhibit 5. The key issue which causes such a diversion remains around the treatment of

the white-label and/or grey market handsets (we define this as either legitimate or

illegitimate handsets which are being sold by non-tier I global brands). By conducting a

bottom-up volume exercise, both the handset and smartphone markets are already

meaningfully higher than most analysts believe.

Exhibit 5: We see a wide range of estimates for the size of global handset market

Handset market size (in mn) 2009 2010 2011 2012E 2013E

Nokia estimates 1,260 1,424 1,604

Gartner estimates 1,211 1,597 1,776 1,830 2,005

IDC estimates 1,341 1,595 1,716 1,745 1,841

CS estimates (OLD) 1,362 1,634 1,804 1,911 2,007

CS estimates (NEW) 1,368 1,652 1,852 1,975 2,086

Source: Gartner, IDC, Company data, Credit Suisse estimates

Handset units – bottom-up analysis suggests volumes of 2bn for global handset market in

2012, but slowing growth ahead. While trying to gauge the true size of the global handset

market, we have tried to look at it from a bottom-up angle by analyzing handset volumes

for leading branded OEMs, and then including volumes from a bunch of smaller vendors in

developed markets (both of which do not use baseband chips from Taiwanese vendors).

To this, we add baseband volume numbers from MediaTek, Spreadtrum and RDA Micro in

Taiwan, and our analysis shows that aggregate device shipments in the handset market

could be as high as nearly 2bn units in 2012 (+5% yoy), and could continue to grow to

2.1bn in 2013 (+7% yoy). Beyond this, with the market being 72% penetrated in terms of

unique subscribers, and as this rises to 85% by 2017, it results in a significant slowdown in

the number of new mobile subscribers buying handsets. Simultaneously, we do not

assume any pick up in handset replacement rates (we have it constant at around 27% of

previous year’s subscriber base), which drives our view that volume growth for the global

handset market may stall to only around 3% beyond 2013.

Smartphone volumes – emergence of the white-label market. Similar to handsets, we have

done a similar bottom-up analysis for smartphone vendors to estimate the true size of the

global smartphone market. Our analysis here shows that the level of understatement in

smartphone volumes could be material especially as Taiwanese chipset vendors continue

07 January 2013

Handset Industry 2013 Outlook 9

to ramp their smartphone chip volumes in 2H12 and 2013. We now estimate that volumes

in the smartphone market could be 716mn/976mn units in 2012/2013, which are around

6%/15% higher than our earlier estimates. Note these estimates are also significantly

higher than estimates from other market research firms or analysts. For example, IDC

estimates 855mn smartphones to be shipped in 2013, while that number for Gartner is

around 900mn, as shown in Exhibit 6.

Exhibit 6: Our smartphone estimates are significantly higher than Gartner and IDC

Smartphone market size (in mn) Q112 Q212 Q312 Q412E 2011 2012E 2013E

Gartner estimates 147.0 153.7 169.2 207.6 472.9 677.5 ~900.0

IDC estimates 144.9 153.9 179.7 221.1 494.4 699.6 854.6

CS estimates (OLD) 147.0 153.7 169.0 204.1 472.9 673.8 850.2

CS estimates (NEW) 151.5 160.9 181.4 222.4 472.9 716.3 975.5

Source: Gartner, IDC, Company data, Credit Suisse estimates

Affordability/TCO approach supports LT addressable market of 4.95bn for smartphones...

To project long term market for smartphones, we continue to rely upon our proprietary

model that takes into account the total cost of ownership (TCO) for a smartphone, income

distribution, and existing penetration of the addressable market. We conclude that the

addressable market for smartphones could be as high as 4.95bn by the end of 2015. We

define TCO as the upfront cost that a consumer pays for a smartphone (subsidised or

unsubsidized depending on the region) combined with the annual service cost for a basic

voice and data plan associated with that device where relevant. Our smartphone model

suggests that by 2015/2017, the global smartphone subscriber base will rise from 1.2bn at

the end of 2012 to reach 2.8bn/3.9bn, i.e. nearly 60%/80% of the 4.95bn addressable

market.

….driving annual smartphone shipments to 1.74bn units by 2017. Based on this long-term

estimate of an addressable market of 4.95bn and that by the end of 2012, there will be

1.2bn smartphone subscribers, effective penetration for smartphones could rise from 24%

in 2012 to nearly 60%/80% by 2015/2017. This will drive smartphone volumes from 716mn

in 2012 to 1.43bn/1.74bn in 2015/2017, implying a CAGR of 26%/19% over this period.

Our 2012/2013/2014 volume estimates of 716mn/976mn/1.22bn (implying 51%/36%/25%

yoy growth) are 6%/15%/21% higher than our earlier projections. With significant

improvements in availability of lower end smartphones, this drives our smartphone volume

estimate of 1.74bn units by 2017.

07 January 2013

Handset Industry 2013 Outlook 10

Handset market to be 2.09bn/2.15bn units in 2013/14

A lingering issue for the global handset market over recent years, which has often been

debated, is the actual size of the market in volume terms. In fact, we note the wide spread

of handset estimates that currently exist for 2011/2012. The key issue which causes such

a diversion remains around the treatment of the white-label, or grey market handsets (we

define this as either legitimate or illegitimate handsets which are being sold by non-tier I

global brands). By conducting a bottom-up volume exercise, both the handset and

smartphone markets are already meaningfully higher than most analysts believe. As a

result, we are raising our 2012/2013/2014 handset estimates by 3%/4%/2% to

1.98bn/2.09bn/2.15bn respectively as shown in Exhibit 7. Similarly, the smartphone

market is materially higher than expected and we are raising our volume estimates here by

6%/15%/21% to 716mn/976mn/1.22bn units for 2012/2013/2014 respectively. Specifically,

our analysis takes in to account a bottom-up analysis for all vendors for both handset and

smartphone markets.

Exhibit 7: Our bottom-up vendor analysis shows that global handset market could be close to 2bn units in 2012 Breakdown of global handset volumes including branded OEMs, and white-label and grey market vendors

Handset sell through (mn) 2008 2009 2010 2011 2012E 2013E

Samsung 199 236 281 315 408 459

Nokia 472 441 461 422 335 289

Apple 11 25 47 89 138 191

LG Electronics 103 122 114 86 56 67

HTC 7 11 25 43 32 44

Sony Ericsson / Sony Mobile 93 55 42 33 38 34

Motorola 107 58 39 40 32 29

Research In Motion 23 34 50 52 32 26

Kyocera / Sanyo 11 10 11 15 12 11

Pantech 5 4 9 10 10 9

Sharp 11 11 9 8 7 6

Panasonic Communications 7 5 5 4 4 4

Fujitsu 4 5 5 7 8 7

NEC / Casio / Hitachi 7 5 5 4 4 3

Top 14 vendors (mn) 1,060 1,023 1,101 1,127 1,115 1,179

% yoy growth 6% -4% 8% 2% -1% 6%

Other handsets, not based on Taiwanese chipset vendors

Other small Japanese vendors 5 2 1 2

Other branded non Taiwanese based vendors 16 11 6 6

Non Taiwanese based handsets (Other small vendors) 9 11 35 37

Total non Taiwanese based Other Vendors (mn) 29 24 42 46 48 46

% yoy growth -65% -19% 75% 10% 5% -5%

Handset market excl Taiwanese based volumes (mn) 1,090 1,046 1,143 1,173 1,163 1,224

% yoy growth 0% -4% 9% 3% -1% 5%

MediaTek baseband shipments 234 355 500 540 508 621

MStar baseband shipments 10 49 76

SpreadTrum baseband shipments 21 23 89 199 266 298

RDA baseband shipments 0 10 83 124

Total Taiwanese baseband shipments 255 378 599 798 932 1,042

Discount factor for obsolescence and multiple chips -15% -15% -15% -15% -15% -15%

MediaTek / Spreadtrum / MStar based handsets (mn) 217 322 510 679 793 886

MediaTek / Spreadtrum / MStar market share (%) 17% 24% 31% 37% 41% 42%

Total handset market (mn) (based on vendor analysis) 1,307 1,368 1,652 1,852 1,956 2,110

% yoy growth (sell in) 8% 5% 21% 12% 6% 8%

Current CS estimates (sell-in as per CS handset model) 1,307 1,368 1,652 1,852 1,975 2,086

% yoy growth (sell in) 8% 5% 21% 12% 7% 6%

Market estimates, as per Nokia (mn) 1,213 1,260 1,424 1,604

% difference between Nokia and CS estimates -7% -8% -14% -13%

Market estimates, as per Gartner (mn) 1,222 1,211 1,597 1,776 1,830 2,005

% difference between Gartner and CS estimates -7% -11% -3% -4% -7% -4%

Our bottom-up analysis shows handset volumes could be close to 2bn units in 2012 1) Slight decline in unit growth for top vendors in

2012. Our bottom-up analysis of handset vendor unitsindicate that the top 14 vendors (not using Taiwanesechipset vendors) may ship 1.1bn units in 2012, implying1% decline in volumes.

2) Taiwanese chipset vendors could ship nearly

950mn baseband units in 2012.

MediaTek to ship over 500mn baseband units.

MediaTek’s volumes continue to show stronggrowth, and we expect it to ship over 500mn/600mn baseband chipsets in 2012/2013 afterregistering 7% yoy growth in 2011.

Spreadtrum also expected to ship ~265mn

units in 2012. With Spreadtrum also likely to shiparound 265mn baseband units in 2012 and nearly300mn in 2013, we believe this momentum fromTaiwan based chipset vendor has continued into2012.

RDA – another Asian entrant in basebands.

Similar to MediaTek and Spreadtrum, RDA is alsoexpected to ship over 80mn baseband units in2012, and around 125mn in 2013. Combiningthese three vendors, we get to a total of930mn/1.04bn baseband units for 2012/2013.

Assuming 15% discount rate. To account forissues like inventory build, obsolescence and useof multiple chips, we have assumed 15% discountrate for Taiwanese baseband volumes. Even then,this shows that these vendors have captured over40% volume share in the handset market.

3) Bottom-up analysis shows that global handset

units can be 2bn in 2012. Our bottom-up analysisshows that the handset market in 2012 may be close to2bn units, which implies mid-single digit yoy volumegrowth, followed by 2.1bn units in 2013 (higher thanestimates from other sources).

1

2

3

Source: Company data, Gartner, Credit Suisse estimates

Our bottom-up analysis suggests volumes of ~2bn for global handset market in 2012.

While trying to gauge the true size of the global handset market, we have tried to look at it

from a bottom-up angle by analyzing handset volumes for leading branded OEMs, and

then including volumes from a bunch of smaller vendors in developed markets (both of

which do not use baseband chips from Taiwanese vendors). To this number, we then add

back baseband volumes from Taiwanese vendors to arrive at the size of the handset

market globally. As detailed in Exhibit 7, our analysis shows that aggregate device

shipments in the handset market could be as high as nearly 2bn units in 2012 (+6% yoy),

and could continue to grow to 2.1bn in 2013 (+8% yoy).

0

7 J

an

ua

ry 2

01

3

Ha

nd

se

t Ind

us

try 2

01

3 O

utlo

ok

1

1

Exhibit 8: We estimate global handset volumes to continue to show 6% growth in 2013 before slowing down to 3% in outer years Detailed assumptions around global handset demand

Global handset summary 2010 2011 2012E 2013E 2014E 2015E 2016E 2017E CAGR 12-17E

Population ('000) 6,509,465 6,600,011 6,692,091 6,786,667 6,883,658 6,983,051 7,084,974 7,189,471

Change (%) 1.4% 1.4% 1.4% 1.4% 1.4% 1.4% 1.5% 1.5%

GDP ($ bn) 57,230 58,880 60,297 61,960 64,051 66,393 68,872 71,480 3.5%

Change (%) 4.2% 2.9% 2.4% 2.8% 3.4% 3.7% 3.7% 3.8%

Factory ASP ($) 135 147 159 168 167 163 154 146 -1.7%

Change (%) 1% 9% 8% 6% -1% -3% -5% -5%

Mobile Subscriptions ('000) (*1) 5,157,390 5,746,901 6,225,776 6,638,735 6,999,144 7,331,280 7,670,007 8,006,611 5.2%

Change (%) 14.7% 11.4% 8.3% 6.6% 5.4% 4.7% 4.6% 4.4%

Reported penetration (%) 79.2% 87.1% 93.0% 97.8% 101.7% 105.0% 108.3% 111.4%

Unique Mobile Subscribers ('000) (*2) 3,965,363 4,424,247 4,799,394 5,111,788 5,384,068 5,632,304 5,883,394 6,130,982 5.0%

Change (%) 15.1% 11.6% 8.5% 6.5% 5.3% 4.6% 4.5% 4.2%

Real penetration (%) 60.9% 67.0% 71.7% 75.3% 78.2% 80.7% 83.0% 85.3%

Subscription / Subscriber ratio 1.30 1.30 1.30 1.30 1.30 1.30 1.30 1.31

Handsets for new subscriptions ('000) 546,369 505,224 417,057 357,489 312,163 285,595 290,486 287,997 -7.1%

Change (%) 2% -8% -17% -14% -13% -9% 2% -1%

% of handset market 34% 28% 21% 17% 15% 13% 13% 12%

Replacement Market ('000) 1,070,572 1,313,680 1,537,935 1,709,216 1,824,367 1,917,535 1,971,678 2,034,948 5.8%

Change (%) 27% 23% 17% 11% 7% 5% 3% 3%

% of handset market 66% 72% 79% 83% 85% 87% 87% 88%

Replacement units as % of

previous year subscription base 23.8% 25.5% 26.8% 27.5% 27.5% 27.4% 26.9% 26.5%

Sell-through handset shipments ('000) 1,616,941 1,818,904 1,954,992 2,066,705 2,136,529 2,203,130 2,262,165 2,322,945 3.5%

Unit Growth (%) 17% 12% 7% 6% 3% 3% 3% 3%

Sell-through handset revenues ($ mn) 218,152 267,781 310,844 347,206 357,142 359,068 348,412 338,990 1.7%

Revenue Growth (%) 18% 23% 16% 12% 3% 1% -3% -3%

Weeks of inventory 8.3 8.3 8.2 8.3 8.3 8.2 8.3 8.3

Mobile Handset Inventory units ('000) 256,926 290,325 310,118 329,083 341,845 347,417 359,989 371,001

Inventory Build / (Depletion) ('000) 35,407 33,399 19,793 18,965 12,762 5,572 12,572 11,012

Sell-in Mobile handset shipments ('000) 1,652,349 1,852,303 1,974,785 2,085,670 2,149,291 2,208,702 2,274,737 2,333,957 3.4%

Unit Growth (%) 21% 12% 7% 6% 3% 3% 3% 3%

Sell-in handset revenues ($ mn) 222,929 272,698 313,991 350,393 359,276 359,976 350,348 340,597 1.6%

Revenue Growth (%) 21% 22% 15% 12% 3% 0% -3% -3%

*1) Mobile subscriptions - this is the reported subscriber base and includes double counting of subscribers due to factors like Inertia, Multiple Devices and SIM-swapping

*2) Unique Mobile subscribers - this is the true subscriber base and excludes the impact of any double counting of same subscriber

1

1) Real penetration to reach 85% by 2017. Due to high ratio of subscription/subscriber, we estimate that the true global subs base at the end of 2012 to be4.8bn vs. the reported 6.2bn, implying true penetration level of 72%. Going forward, we expect this penetration number to rise to 85% by 2017 leading to6.1bn true subscribers.

2) Handset volume growth of 7%/6% in 2012/2013. We estimate the overall handset market to be 1.98bn/2.09bn for 2012/2013, up 7%/6% respectivelydue to strong growth in the smartphone market. Beyond that, we expect volume growth to remain around 3% as we reach towards saturation levels.

2

Source: Gartner, Credit Suisse estimates

07 January 2013

Handset Industry 2013 Outlook 12

Taiwan baseband vendors continue to gain share. For chipset vendors in Taiwan, we have

looked at baseband volumes for MediaTek (which acquired MStar recently), SpreadTrum

and RDA (all 3 companies covered by our analyst Randy Abrams). Cumulatively, these

vendors continue to see strong volume growth and may ship around 930mn baseband

chipsets in 2012 (up 17% yoy) and 1.04bn units in 2013 (up 12% yoy). Even assuming a

15% discount to their volumes to take into account impact from inventory build,

obsolescence and use of multiple chips, this implies that handsets using these chips may

account for over 40% of global handset shipments in 2012 (up from ~30% in 2010).

Slowing volume growth in the long term. One of the key observations we would make here

is that the global handset market will be around 72% penetrated in our view, as we

approach around 4.8bn unique mobile subscribers by the end of 2012, out of a population

base of 6.7bn. We estimate that penetration number will rise to 85% by 2017 (Exhibit 8),

which means that there will be a significant slowdown in the number of new mobile

subscribers buying handsets for the first time. Also in our estimates, we do not assume

any pick up in handset replacement rates (we have it constant at around 27% of previous

year’s subscriber base), which drives our view that volume growth beyond 2013 may stall

to only around 3% for the global handset market.

Smartphone volumes now also being restated higher

Similar to the handset market, we carried out bottom-up analysis for smartphone vendors

to estimate the true size of the global smartphone market. Our analysis here shows that

the level of understatement in smartphone volumes could be material especially as

Taiwanese chipset vendors continue to ramp their smartphone chip volumes in 2H12 and

2013. In summary as we detail in Exhibit 9, we estimate that volumes in the smartphone

market could be 716mn/976mn units in 2012/2013, which are around 6%/15% higher than

our earlier estimates. Further, these estimates are also significantly higher than estimates

from other market research firms or analysts. For example, IDC expects the smartphone

market to be 700mn/855mn units in 2012/2013.

Bottom-up vendor analysis shows market size could be >1bn units in 2013. We have done

an analysis similar to the overall handset market, whereby we have looked at smartphone

volumes for global vendors not using baseband chips from Taiwanese vendors. To that

number, we add back volumes from Taiwan chipset vendors, which cumulatively suggests

global smartphone volumes of around 735mn/1.05bn units in 2012/2013.

Growth in the tier I branded OEM category driven by Samsung and Apple. Although

smartphone volumes at some of the branded OEMs remain under pressure (Nokia, RIMM

and HTC), volume growth within this category to remain robust as we estimate 24%/29%

unit growth in 2012/2013 driven by Samsung and Apple.

Taiwanese vendors could ship close to 335mn smartphone basebands in 2013. The

reason for volume numbers to be restated is because of significant volume ramp for

smartphone basebands at chipset vendors in Taiwan. In fact, we estimate that MediaTek

and Spreadtrum together (both covered by Credit Suisse analyst Randy Abrams) shipped

only 10mn smartphone basebands in 2011, but that number will rise to nearly

150mn/335mn units in 2012/2013 (Exhibit 9). Even assuming 15% discount to these

volumes, we estimate that smartphones powered by these chips will account for some

17%/30% of global smartphone volumes in 2012/2013.

Significant understatement of smartphone market by analysts and market research firms.

All of this means that there may be a significant level of understatement in the volume

estimates for the smartphone market. As a result, we have had to restate/increase our

global volume numbers for the smartphone market in 2012/2013 by 6%/15%. This is

something, which could also happen to estimates from other sources including market

research firms like Gartner and IDC. For example, IDC expects the smartphone market to

be 700mn/855mn units in 2012/2013, but these number could again prove low based on

our analysis.

0

7 J

an

ua

ry 2

01

3

Ha

nd

se

t Ind

us

try 2

01

3 O

utlo

ok

1

3

Exhibit 9: Bottom-up vendor analysis suggests global smartphone volumes could be around 730mn/1.05bn units in 2012/2013 Breakdown of global smartphone volumes including branded OEMs, and white-label and grey market vendors

Q112 Q212 Q312 Q412E 2011 2012E 2013E

Top 8 vendors (not using Taiwan chip vendors)

Samsung 40.6 45.6 55.1 62.6 88.3 203.9 315.3

Apple 33.1 28.9 23.6 49.8 89.3 135.4 190.7

Nokia 13.3 11.7 7.2 5.1 84.6 37.3 18.5

HTC 7.7 9.3 8.4 7.0 43.0 32.4 44.0

Research In Motion 9.9 8.0 8.9 6.7 51.5 33.6 25.9

LG Electronics 5.0 5.8 7.0 8.3 19.0 26.0 35.0

Sony Ericsson / Sony Mobile 5.4 5.3 6.6 6.1 19.6 23.5 17.5

Motorola Mobility / Google 4.7 4.6 5.1 5.1 17.4 19.5 15.0

Sub-total of top 8 vendors (not using Taiwan chip vendors) (A) 119.8 119.3 121.9 150.6 412.7 511.6 661.9

Japan / Korea vendors

Sub-total of top Japan / Korea vendors (B) 6.2 5.2 6.6 6.6 16.9 24.6 27.1

Other vendors (using both Taiwan and international chip vendors)

ZTE 4.5 6.3 7.7 9.0 10.5 27.5 38.0

Huawei 5.3 5.4 7.8 9.0 15.6 27.5 35.0

Lenovo 2.4 4.4 7.0 11.2 1.7 25.0 38.0

Other key Chinese vendors 4.9 9.4 13.1 14.4 6.2 41.7 48.0

Remaining vendors 3.8 3.7 5.2 5.7 9.2 18.4 21.2

Sub-total of top China smartphone vendors (C) 21.0 29.2 40.7 49.3 43.3 140.2 180.2

Taiwan chipset vendors

MediaTek 10.0 20.5 38.3 47.0 10.0 115.8 243.4

SpreadTrum 0.1 1.6 11.0 18.0 0.2 30.8 91.5

Sub-total of Taiwan smartphone chip vendors 10.1 22.1 49.3 65.0 10.2 146.5 334.8

Assuming 15% discount 15% 15% 15% 15% 15% 15% 15%

Sub-total of Taiwan smartphone chip vendors (assuming 15% discount) (D) 8.6 18.8 41.9 55.3 8.7 124.6 284.6

Other vendors' volumes using Taiwan chip vendors

ZTE 0.2 0.9 1.1 1.3 0.5 3.7 11.4

Taiwan chip share at ZTE (%) 5% 15% 15% 15% 5% 13% 30%

Huawei 0.3 0.8 1.2 1.3 0.6 3.6 10.5

Taiwan chip share at Huawei (%) 5% 15% 15% 15% 4% 13% 30%

Lenovo 1.0 2.0 4.2 6.7 0.4 13.9 20.9

Taiwan chip share at Lenovo (%) 40% 45% 60% 60% 24% 55% 55%

Others 5.7 9.1 15.5 17.1 7.2 47.4 58.8

Taiwan chip share at Others (%) 65% 70% 85% 85% 47% 79% 85%

Smartphones based on Taiwan chip vendors (E) 7.2 12.8 22.1 26.5 8.7 68.6 101.6

Total smartphone market (mn) (A + B + C + D - E) 148.5 159.6 189.0 235.2 472.9 732.4 1,052.2

Smartphone volumes - CS published estimates (mn) 151.5 160.9 181.4 222.4 472.9 716.3 975.5

Smartphone volumes - Gartner estimates (mn) 147.0 153.7 169.2 207.6 472.9 677.5 ~900.0

Smartphone volumes - IDC estimates (mn) 144.9 153.9 179.7 221.1 494.4 699.6 854.6

Smartphone volumes - CS OLD estimates (mn) 147.0 153.7 169.0 217.1 472.9 673.8 850.2

1) Continued smartphone growth

at tier I vendors led by

Samsung and Apple. Withrobust volume growth at bothSamsung and Apple, we believesmartphone units at tier I brandedOEMs will continue to grow ataround 25% per annum in2012/2013.

2) Smartphone baseband units

from Taiwan to more than

double in 2013. We believe thatMediaTek and Spreadtrumtogether will ship over 325mnbaseband units for smartphonesin 2013, around 2.3x unit growthvs. 2012. This will drive significantvolume growth at the low-end ofthe smartphone marketparticularly led by white-label andgrey market vendors. Evenassuming 15% discount to theirvolumes, we estimatesmartphones powered by thesechips will grow from 125mn unitsin 2012 to 285mn in 2013.

3) Bottom-up analysis shows

volumes could be over 1bn in

2013. Our analysis suggests thatglobal smartphone volumes couldbe as high as 730mn units in2012 and 1.05bn in 2013. Wehave taken a conservative viewand estimate 716mn/975mnunits, which are 6%/15% higherthan our previous estimates, andalso higher than estimates frommarket research firms.

2

1

3

Source: Company data, Gartner, IDC, Credit Suisse estimates

07 January 2013

Handset Industry 2013 Outlook 14

Forecasting smartphones based on TCO

We continue to believe that any forecast of the smartphone market needs to have at its

core the affordability and total cost of ownership (TCO) of smartphones. Given subsidies in

developed markets, handsets are primarily bundled with a service package which tends to

mask the true cost of the device. While we acknowledge that aggressive promotions can

have a significant impact on the volume ramp-up of a given product, we still believe that

the TCO remains crucial for the penetration of the overall market. To arrive at our TCO

estimates, we have made several important assumptions, as are detailed in Exhibit 12.

■ Smartphone ASPs of close to $45 in most emerging markets by 2017. In a number of

emerging market countries like India and China, we already have low end

smartphones selling at around $70. This number will decline to around $45 by 2017

driven by improvement in chipset efficiency and decline in component pricing. In

developed markets, given the pricing for smartphones is still much higher compared to

emerging markets, we have assumed around $100 of cumulative ASP decline for a

typical lower end device over the next 5 years.

■ Normal levels of ARPU decline. We have assumed annual ARPU pressure of 6% in all

markets (except for NA where we have assumed 10%) to take into account pricing

pressure at mobile operators.

■ Including only device cost in TCO calculation in some of the developing markets.

Given strong level of traction seen for low end smartphones (priced at around $70 to

$100) in a number of emerging market countries, we have adjusted the way we

calculate TCO for a smartphone. In these markets, we find that at the lower end of the

market, there is an increasing trend from consumers towards buying a low-end

smartphone on pre-paid plans (without any service plan included for voice and/or

data). This means that the TCO for a low-end smartphone user only includes the cost

of a device, which is around $70 in countries like China and India (as shown in Exhibit

10), and which we expect to fall to around $45 by 2017.

■ Smartphone affordability threshold in each region. Based on Exhibit 13, we arrive at

smartphone affordability threshold in each region by looking at mobile telecoms as a

percentage of GDP in each of the regions in 2011. As such, we have used a

smartphone affordability threshold level of 1.3% in Western Europe, 1.4% in North

America, 2.2% in Central/Eastern Europe, 2.3% in Asia-Pacific, 2.6% in Latin America

and 4.1% in Africa.

Based on these core assumptions, we conclude that 4.95bn people globally will be able to

afford a smartphone by 2017, which is around 2x compared to our estimated addressable

base of 2.4bn people in 2012. We discuss each of our assumptions in detail in the

following sections.

Smartphone TCO varies a lot by region. We analyzed the TCO for a low-end smartphone

by vendor and for around 15 countries as listed in Exhibit 10, and this demonstrates that

the ownership cost for smartphones falls in a wide range. We believe that this is owing to a

number of factors such as the stage of the smartphone market in terms of nascence,

competitive dynamics, and device positioning by vendor. We also note that our analysis is

based on the TCO at the lower end of the market, as this sub-segment of the overall

market will be key to driving adoption long term. In particular, we have looked at the lowest

consistent level of cost faced by a consumer by isolating comparable terminals and

reasonable levels of data usage. We note that the TCO varies significantly in subsidized

versus unsubsidized markets, with the cost ranging from as low as $70 for countries like

China and India (only the device cost given a number of users may use these devices on

pre-paid tariff plans to further lower their TCO) to as high as $720 in the US. This is

another trend in emerging markets which is likely to have a significant impact in terms of

further expanding the addressable market for smartphones.

07 January 2013

Handset Industry 2013 Outlook 15

Exhibit 10: TCO for a low-end smartphone – TCO composition varies significantly by region

69

70

146

158

0

0

0

0

69

1

6

128

0

1

0

0

0

0

250

311

368

374

312

388

466

451

632

720

0 100 200 300 400 500 600 700 800

India

China

Philippines

Brazil

UK

Spain

Australia

Mexico

Russia

France

Germany

Italy

Canada

United States

Low-end smartphone TCO in 2012 (US$)

Upfront Device ASP (US$)

One year Smartphone ARPU (US$)

ONLY DEVICE COST INCLUDED

BOTH DEVICE AND SERVICE COST INCLUDED

Source: Company data, Credit Suisse research

Forecasting the TCO long term. As shown in Exhibit 10, the two components of the

smartphone TCO are: i) the upfront cost of the terminal (device) to the consumer, and ii)

the annualized ARPU (voice and data) bundled with the device in markets where handset

subsidies exist. As can be seen in subsidized markets (such as Western Europe and North

America), this can be significantly different from unsubsidized markets such as Asia

Pacific.

Lower priced smartphones driven by BOM reductions. While we expect the smartphone

market to evolve with new features, at the lower end of the market, pricing will continue to

decline driven by BOM reductions. Here we would note that on a like-for-like basis,

component BOM can decline by around 10% per annum. Allowing for other fixed costs in

the total manufacturing expense and assuming some gross margin pressure at the

manufacturer level, we estimate that the ASP for low-end smartphones can continue to

decline to as low as around $45 by 2014 compared to around $70 currently. In subsidized

markets where the upfront cost for the terminal is already quite low given cost of the

device is bundled in the service plan, there will be around $100 of cumulative decline in

ASPs for a typical smartphone in developed markets over the next five years.

Expecting gradual ARPU declines. Forecasting ARPU declines is somewhat more

challenging given that each carrier tends to bundle data in a different way with a range of

voice minutes, texts and data. We note however, that at both the manufacturer and carrier

levels, there are several initiatives to bring down costs to the consumer over time. We

assume a moderate decline in the ARPU in the low-end smartphone market by 2015

based on an annualized ARPU reduction of 6% in all markets globally (except for the US

where we assume 10% decline given ARPU levels are significantly higher than other

regions).

Longer term TCO reduction to around $100 by 2017. As shown globally, by taking into

account the above assumptions for the low-end smartphone TCO (by region), we arrive at

07 January 2013

Handset Industry 2013 Outlook 16

the conclusion that the smartphone addressable market could reach 4.95bn units by 2017

in terms of affordability. We assume that at the very least, the reduction in the BOM will

pass straight on to the consumer and this implies that the TCO for a low-end smartphone

offering could reach as low as $103 longer term, a $90 decline or around 45% drop from

the current TCO of $194, which implies a CAGR decline of 12%. Geographically, we

continue to expect a variance in TCO, even in 2015 as shown in Exhibit 11.

Exhibit 11: TCO for a low-end smartphone device by 2015 in US$, unless otherwise stated

51

51

106

115

198

208

246

250

251

264

333

400

403

466

0 50 100 150 200 250 300 350 400 450 500

India

China

Philippines

Brazil

Spain

UK

Australia

Russia

Mexico

France

Germany

Canada

Italy

United States

TCO for a low-end smartphone by 2015 (US$)

ONLY DEVICE COST INCLUDED

BOTH DEVICE AND SERVICE COST INCLUDED

Source: Credit Suisse estimates

0

7 J

an

ua

ry 2

01

3

Ha

nd

se

t Ind

ustry

20

13

Outlo

ok

17

Exhibit 12: Smartphone TCO analysis – addressable market for smartphones can grow from around 2.4bn in 2012 to 4.95bn by 2017 driven by TCO declines Total cost of ownership in US$ and addressable population in millions

2012E 2015E 2017E% CAGR

(2012-2015)2012E 2015E 2017E 2012E 2015E 2017E

Additional

population

(2012 to 2017)

2012E 2015E 2017E

Developed countries

North America

United States 721 466 348 -13.5% 53 32 24 136 213 273 136 43% 66% 83%

Canada 632 400 295 -14.1% 50 27 20 18 30 33 15 53% 83% 90%

Western Europe

France 390 264 204 -12.2% 28 19 15 45 55 60 15 71% 86% 93%

Germany 503 333 264 -12.1% 36 25 19 54 69 74 20 66% 85% 91%

Italy 579 403 316 -11.4% 42 30 23 16 32 41 25 26% 51% 66%

Spain 311 198 147 -13.9% 22 15 11 30 40 43 13 66% 85% 91%

United Kingdom 250 208 184 -6.0% 18 15 14 51 55 59 8 81% 85% 90%

Rest of WE 363 277 217 -9.8% 26 20 16 67 81 88 21 67% 84% 90%

Other developed

Australia 368 246 188 -12.6% 19 11 8 21 24 24 3 91% 100% 100%

Hong Kong 363 242 185 -12.7% 19 10 8 6 7 7 1 81% 91% 95%

Japan 363 242 185 -12.7% 22 12 10 128 127 126 -2 100% 100% 100%

Singapore 363 242 185 -12.7% 19 10 8 5 5 6 1 86% 95% 100%

South Korea 363 242 185 -12.7% 19 10 8 36 46 49 13 71% 91% 95%

Taiwan 363 242 185 -12.7% 19 10 8 16 22 23 7 66% 91% 93%

Total Developed 457 322 253 -11.1% 31 21 17 628 805 905 277 63% 79% 88%

Emerging countries

China 70 51 46 -8.0% 3 2 2 948 1,236 1,248 300 70% 90% 90%

India 69 51 46 -8.0% 2 2 2 122 509 653 531 10% 40% 50%

Indonesia 69 51 46 -8.0% 3 2 2 98 204 236 138 40% 80% 90%

Brazil 158 115 94 -10.0% 6 4 3 118 121 164 46 60% 60% 80%

Pakistan 69 51 46 -8.0% 3 2 2 0 19 20 20 0% 10% 10%

Nigeria 69 51 46 -8.0% 2 1 1 33 71 113 80 20% 40% 60%

Bangladesh 69 51 46 -8.0% 3 2 2 0 15 16 16 0% 10% 10%

Russia 382 250 188 -13.2% 17 12 9 38 74 100 62 27% 53% 71%

Mexico 374 251 192 -12.5% 14 9 7 26 51 62 36 23% 43% 52%

Philippines 146 106 96 -8.0% 6 5 4 10 10 22 12 10% 10% 20%

Egypt 69 51 46 -8.0% 2 1 1 66 78 91 25 80% 90% 100%

Turkey 347 221 164 -13.9% 14 9 6 20 41 57 37 27% 53% 72%

Thailand 95 51 46 -13.6% 4 2 2 39 53 60 21 60% 80% 90%

Other emerging 136 105 92 -7.6% 5 4 3 619 1,010 1,200 581 39% 58% 65%

Total Developing 107 78 69 -8.3% 4 3 3 1,882 3,493 4,040 2,158 34% 59% 66%

Global Total 194 124 103 -12.0% 11 6 5 2,439 4,299 4,945 1,860 37% 62% 69%

% of Total population Income cutoff level,

US$ (000s) Addressable population, mn

Country

Total cost of ownership, $

(Smartphone and/or Service plan)

1

2

2

3

1) We expect the TCO for a

smartphone to decline by nearly

$90 or 45% over the next 5

years to $103 (from $194 in

2012). This decline will be driven

by a combination of lower end

smartphones and falling ARPU

levels.

2) Our affordability work shows that

an additional 275mn people will

be able to afford a smartphone in

developed markets, but more

importantly another 2.15bn in

developing markets by 2017.

The top three countries with the

largest absolute growth in

addressable population will be

India, China, Indonesia and US.

3) Around 4.95bn people will be

able to afford a smartphone

by 2017, which is around 2x the

current addressable population

base of 2.4bn globally.

Source: Company data, IMF, Credit Suisse estimates

07 January 2013

Handset Industry 2013 Outlook 18

Linking our TCO analysis to the addressable market

As we demonstrated and summarized in Exhibit 12, the TCO for a smartphone could fall

nearly 45% from the current level of $194 to $103 by 2017 as ASP and ARPU pressures

drive this trend. We now analyze effects due to income distribution and population by

region.

How much are consumers prepared to spend on smartphones? Once we have estimated

the cost of a smartphone to the consumer, the next issue is to calculate a sensible income

threshold level. While a smartphone is a desirable item, there is a limit to the income level

which the average consumer would be willing to spend on the combined hardware and

services. Here we have approached this analysis by looking at two separate metrics.

Exhibit 13: Mobile Telecoms as % GDP in 2011

1.4% 1.3%

2.6%

2.2%

4.2%

2.4% 2.3%

1.8%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

NorthAmerica

WesternEurope

Latin America EasternEurope

Africa Middle East Asia-Pacific(ex Japan)

Japan

Mo

bil

e T

ele

co

ms

as

% o

f G

DP

(2

011

)

1.9% - Avg. global

2.5% - Avg. developing countries

1.4% - Avg. developed countries

Source: Gartner, Credit Suisse estimates

■ Mobile spending to GDP ratio of around 1.9% globally. We see in Exhibit 13 that

globally, the amount of mobile spend varies by region, with consumers spending on

average some 1.9% of GDP on mobile telephony and services. Hence, we would

argue that the TCO of a smartphone should not represent more than this level of

income. If we believe, as shown in Exhibit 12, that the TCO of a smartphone will be

$103 globally on a longer term basis, then a user would need a minimum income level

of $5,200 to afford a smartphone assuming he/she spends the same proportion on

mobile telephony. This provides our key income cut off level for different regions and

can be used to determine the potential addressable market for smartphones.

■ In emerging markets, the level is higher at 2.5%. Given the 1.9% (global) and 1.4%

(developed markets) threshold levels, the higher 2.5% ratio for developing markets

shows the importance of data and communication for users in these markets; they are

prepared to spend a higher percentage of GDP on mobile telephony. As shown, we

believe that subscribers in some emerging markets like Africa are spending around

4.2% of GDP on mobile related services.

Income distribution data suggests addressable market of 4.95bn longer term. We conclude

that users are prepared to spend as much as 1.3% to 4.2% of their income on smartphone

purchases (depending on the geographic region) and we can apply these cut-off levels to

determine the minimum level of GDP per head needed to purchase a smartphone based

on the TCO for a low-end smartphone in that market. Over the longer term, we then use

07 January 2013

Handset Industry 2013 Outlook 19

this estimate of required income to compute the level of population that is addressable. As

shown in Exhibit 12, the addressable market for smartphones is around 4.95bn globally.

Smartphone units to grow nearly 2.5x by 2017

With an addressable market of some 4.95bn by 2017, we now turn our analysis to

quantifying the market opportunity in terms of units. We conclude, based on our

affordability, penetration, and replacement analysis that the smartphone subscriber base

longer term could be as high as 3.9bn by 2017 (around 80% penetration of the 4.95bn

addressable market) and that the smartphone segment is set for a period of robust volume

growth reaching volumes of 1.74bn by 2017, up from 716mn units in 2012 as shown in our

summary smartphone model in Exhibit 18.

Exhibit 14: Mobile voice saw penetration gains of 40pp over five years after reaching 30% Base year 1 is taken as the year when penetration in individual region reached near 10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

% s

ub

scri

ber

pen

etra

tio

n p

rog

ress

ion

on

ce p

enet

rati

on

rea

ches

10%

init

ially

Western Europe USA North America China India APAC CEE Africa Latin America Global Average

Mobile voice penetration

globally grew from 28% in

year 5 to 70% in year-10,

a 40pp absolute gain in 5

years.

Source: Gartner, Credit Suisse estimates

Penetration curves and the addressable market. We would note that effective smartphone

penetration (from affordability point of view) will be around 24% based on our estimate of

1.2bn smartphone subscribers at the end of 2012. The next step is to determine the

evolution of this penetration on a longer term basis. Here, a sensible approach is to take a

look at how the mobile voice market evolved. As shown in Exhibit 14, the voice market

followed a typical “S” curve for penetration, as it increased from 28% to 70% over a five-

year period, an increase of over 40 percentage points. Owing to the falling cost of

ownership, carrier push, and consumer pull, penetration gains will be higher in

smartphones than mobile voice. We estimate that smartphone effective penetration will

increase from 24% in 2012 to 79% by 2017 (Exhibit 15). This level of penetration would

imply smartphone subscribers of 3.9bn by 2017. In terms of sanity check, our estimates

imply that by 2017 smartphone penetration will reach i) 49% of the global mobile

subscriber base (Exhibit 16); ii) 54% of the global population; and iii) 74% of overall

handsets shipped.

07 January 2013

Handset Industry 2013 Outlook 20

Exhibit 15: Global smartphone penetration still low at 24% Effective smartphone penetration (based on affordability) over time

Exhibit 16: Smartphones account for 19% of mobile subs Smartphone subs base as percentage of mobile subscriptions

0%

20%

40%

60%

80%

100%

120%

NorthAmerica

WesternEurope

Japan APAC (exJapan)

CEE MEA Latam Global

2012E 2013E 2014E 2015E 2016E 2017E

Smar

tph

on

e p

ene

trat

ion

(as

% o

f ad

dre

ssab

lem

arke

t)

0%

20%

40%

60%

80%

100%

NorthAmerica

WesternEurope

Japan APAC (exJapan)

CEE MEA Latam Global

2012E 2013E 2014E 2015E 2016E 2017E

Sm

art

ph

on

esu

bs

as

% o

f to

tal

mo

bil

e s

ub

s b

ase

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Replacement rates will trend down but expecting only gradual declines. Given our view

that bulk of the volume growth in smartphone market going forward will be driven by

emerging markets, we acknowledge that replacement rates are likely to trend down.

However, with smartphones still operating at the higher-end of the market (vs. the overall

mobile industry), we assume that replacement rates in smartphones will continue to be

higher than overall handset market. As such, we assume an average replacement rate of

38% for the global smartphone market over 2013-2017, which remains above the global

replacement rate of 27% we forecast for the overall handset industry. Looking at our

regional replacement forecasts as demonstrated in Exhibit 17, we expect smartphone

replacement levels in North America to continue to remain highest amongst all regions

with an average of 55% in the long term.

Exhibit 17: Smartphone replacement rate by region Replacement rate measured as % of previous year’s smartphone subscriber base

Replacement rate (%) 2008 2009 2010 2011 2012E 2013E 2014E 2015E 2016E 2017E

NA 83% 69% 67% 64% 55% 55% 55% 55% 55% 55%

Latam 33% 33% 35% 36% 32% 32% 32% 32% 32% 32%

WE 43% 42% 44% 39% 40% 40% 40% 40% 40% 40%

APAC 29% 25% 26% 32% 35% 35% 36% 36% 35% 34%

Japan 44% 37% 37% 38% 38% 38% 34% 32% 29% 28%

MEA 37% 28% 32% 33% 34% 33% 33% 33% 33% 33%

CEE 33% 29% 34% 34% 36% 35% 34% 35% 35% 35%

Global 43% 39% 41% 41% 40% 39% 38% 38% 37% 36%

Source: Company data, Credit Suisse estimates

0

7 J

an

ua

ry 2

01

3

Ha

nd

se

t Ind

us

try 2

01

3 O

utlo

ok

21

Exhibit 18: We expect smartphone volumes to grow 36%/25% yoy in 2013/2014 driving CAGR unit growth of nearly 20% over 2012-2017 in millions, unless otherwise stated

Smartphone model summary 2008A 2009A 2010A 2011A 2012E 2013E 2014E 2015E 2016E 2017E CAGR 12-15 CAGR 12-17

Global mobile subscriptions (mn) 3,866 4,498 5,157 5,747 6,226 6,639 6,999 7,331 7,670 8,007 6% 5%

Global new subscriptions (mn) 616 632 660 590 479 413 360 332 339 337

Global mobile unit sell-in shipments (mn) 1,307 1,368 1,652 1,852 1,975 2,086 2,149 2,208 2,272 2,333 4% 3%

Global smartphone subscribers (mn) 242 321 490 763 1,178 1,693 2,267 2,841 3,373 3,892 34% 27%

as % of total mobile subscribers 6% 7% 9% 13% 19% 26% 32% 39% 44% 49%

Global smartphone addressable market (in mn by 2017) 4,945 4,945 4,945 4,945 4,945 4,945 4,945 4,945 4,945 4,945

Smartphone Effective Penetration (subs / addressable market) 5% 6% 10% 15% 24% 34% 46% 57% 68% 79%

Net smartphone adds (mn) 63 79 169 273 415 515 574 574 532 519 11% 5%

as % of total smartphone units 45% 46% 56% 58% 58% 53% 47% 40% 34% 30%

Replacements units (mn) 76 93 130 199 302 460 645 851 1,044 1,218 41% 32%

as % of last year's smartphone subs 43% 39% 41% 41% 40% 39% 38% 38% 37% 36%

as % of total smartphone units 55% 54% 44% 42% 42% 47% 53% 60% 66% 70%

Global smartphone units (mn) 139 172 299 473 716 976 1,219 1,425 1,577 1,737 26% 19%

% change yoy 14% 24% 73% 58% 51% 36% 25% 17% 11% 10%

as % of mobile shipments 11% 13% 18% 26% 36% 47% 57% 65% 69% 74%

Smartphone ASPs ($) 320 332 324 331 307 286 258 232 209 188 -9% -9%

% change yoy 4% -2% 2% -7% -7% -10% -10% -10% -10%

Global smartphone revenues ($ mn) 44,603 57,175 96,880 156,558 219,645 279,185 313,854 330,274 328,952 326,071 15% 8%

% change yoy 12% 28% 69% 62% 40% 27% 12% 5% 0% -1%