guidelines on cost estimation of research …...the methodology has been discussed and tested with...

TRANSCRIPT

GUIDELINES ON COST ESTIMATION OF RESEARCH INFRASTRUCTURES

StR-ESFRI Study

GUIDELINES ON COST ESTIMATION OF RESEARCH INFRASTRUCTURES

StR-ESFRI Study

GUIDELINES ON COST ESTIMATION OF RESEARCH INFRASTRUCTURES

This publication was developed for StR-ESFRI – Support to Reinforce the European Strategy Forum on Research Infrastructures – by CSIL – the Centre of Industrial Studies.

The StR-ESFRI and StR-ESFRI2 Projects have received funding from the European Union’s Horizon 2020 Research & Innovation programme under grant agreements n° 654213 and n° 823711.

FOREWORDThe ESFRI Roadmap contains indicative figures on the on the set-up and operating costs of the Research Infrastructures, based on estimates provided by the ESFRI Projects and Landmarks. The previous methodology for collecting estimated cost data presented two significant challenges with results: cost categories were not uniformly represented by the RIs, and quoted values fluctuated inconsistently over time.

A discussion developed in the ESFRI Executive Board and in the ESFRI Forum on the need to elaborate a cost analysis for RIs that would be referenced to standard economic methods – e.g. adopting the discount cash-flow analysis for the full lifecycle of the RI, but with RI-specific figures that could be appropriate for the different kind of RIs and their funding schemes. The objective of the cost analysis is to give full transparent evidence of the required investment for the set-up and running resources for operation of the RIs, using state of the art financial units that are easily interpreted and communicated to the political and funding authorities. Adoption and use of the cost analysis will strengthen the reliability of the cost information reported in the ESFRI Roadmap updates, and will provide solid reference values for the monitoring activities of ESFRI on the Projects and on the periodic update of the Landmarks status of the operational RIs.

StR-ESFRI opened a public competition of professional consultants to commission a cost analysis study on RIs and the proposition of a user-guide for applying it to the specific case of ESFRI RIs. The contract was awarded to CSIL – the Centre of Industrial Studies – an independent research and consulting company, specialised in applied economic research, evaluation of public investment projects, infrastructure project appraisal, that already worked in the past on cost-benefit analysis of some Research Infrastructures like CERN and CNAO.

The results of this research are summarized in a CSIL document that was presented during the 68th ESFRI Forum Meeting on 27th-28th March 2019 in Liblice (CZ) and well received by the Forum. ESFRI will take note of the results of the CSIL report in developing its Roadmap methodology and guide for the next updates.

Here we present an extended version of the Guidelines on Cost Estimation of Research Infrastructures as a StR-ESFRI Study downloadable from the esfri.eu website. It is offered for reference to all RI managers and financial officers informing on an advanced cost analysis methodology.

Tableofcontents

1. Introduction.........................................................................................................................1

2. Themethodinanutshell......................................................................................................3

3. Generalprinciples................................................................................................................53.1 Identificationoftheunitofanalysis.........................................................................................53.2 Settingthetimehorizon...........................................................................................................83.3 Discountedcashflowmethod................................................................................................113.4 Currencyandprices................................................................................................................133.5 Incrementalapproachandcounterfactual..............................................................................14

4. Totalinvestmentcostsandresidualvalue..........................................................................154.1 Definition...............................................................................................................................154.2 Mainitems.............................................................................................................................15

4.2.1 Designandpreparation............................................................................................................................154.2.2 Constructionandstart-upcosts...............................................................................................................164.2.3 Replacementcosts...................................................................................................................................174.2.4 Majorupgrades........................................................................................................................................174.2.5 Decommissioningandend-of-lifecosts...................................................................................................17

4.3 Residualvalue........................................................................................................................174.4 Presentvalueoftotalinvestmentcosts..................................................................................18

5. Operatingcosts..................................................................................................................195.1 Definition...............................................................................................................................195.2 Mainitems.............................................................................................................................195.3 Presentvalueofoperatingcosts............................................................................................20

6. Annex:Casestudies...........................................................................................................216.1 Asingle-sitedRIinoperation.................................................................................................216.2 AdistributedRIinoperation..................................................................................................246.3 Anupgradeofanexistingsingle-sitedfacility.........................................................................276.4 AdistributedRIinoperation..................................................................................................30

Listoffiguresandtables

Figure1DistributedRI........................................................................................................................6

Figure2Aggregationandapportionment..........................................................................................7

Figure3CoststructuresofRIs............................................................................................................9

Figure4Actualizationanddiscounting............................................................................................13

Figure5Upgradescenariovs.BAUscenario....................................................................................27

Table1Investmentandoperatingcostsofasingle-sitedRI-EURmillion,nominalnotdiscounted..........................................................................................................................................................22

Table2InvestmentandoperatingcostsofadistributedRI-EURthousand,nominalnotdiscounted..........................................................................................................................................................25

Table3Investmentandoperatingcostofasingle-sitedRIwithamajorupgrade-EURthousand,nominalnotdiscounted...................................................................................................................28

Table4Investmentandoperatingcosts-DistributedRIwithwave-likecoststructure-EURmillion,nominalnotdiscounted...................................................................................................................31

Abbreviationlist

BAU Businessasusual

EOSC EuropeanOpenScienceCloud

ESFRI EuropeanStrategyForumonResearchInfrastructures

FAIR Findable,accessible,interoperableandre-usable(data)

IPRs IntellectualPropertyRights

NPV NetPresentValue

RI ResearchInfrastructure

VAT ValueAddedTax

1

1. IntroductionThese guidelines are developed in the framework of the StR-ESFRI project (Support to

ReinforcetheEuropeanStrategyForumforResearchInfrastructures),toprovideaconceptualandmethodologicaltoolforcostestimationofResearchInfrastructures(RIs)included(orwillingtobe)intheESFRIRoadmap.ThereportprovidesaunifiedframeworktogatherdataconcerningcostsalonglifecycleofRIsinaharmonizedway.Itillustratesgeneralprinciplesandsuggeststechnicalsolutions when data seem not immediately available or difficult to estimate. It also takes intoaccount the specificities of different typologies of RIs, which are active in different researchdomainsandadoptdifferentaccountingsystems.

ThemainaudienceoftheseguidelinesisRIseniormanagerswhoareresponsibleforfinancialplanningandlong-termsustainabilityoftheRI;however,sometechnicalexpertisemaybeneededtoimplementthemethodology(e.g.headoffinance).

Thecommoncostaccountingmethodologypresentedintheseguidelinesisbasedonthebestinternationalpracticeinthefieldofinfrastructureprojectappraisal,allowingcomparabilityacrossdifferenttypesofRIs,countriesandscientificfieldsanditisinspiredbysolidprinciplesleadingtounivocallyinterpretableresults.

The main purpose of this document is to support ESFRI and the ESFRI-related ResearchInfrastructures(‘projects’and‘landmarks’) inprovidingevidence-basedfinancialperspectivesfortheirlifecyclephasesandmaintainingregularlyupdatedinformationfortheForum.

Adopting a common framework is essential not only for gathering data and supportingfundingdecisions,butalsotoallowupdateandverificationoftheinformation.ItcanalsobeusedbyRImanagersformorefarreachingexercisessuchasassessingthesocio-economicimpactoftheRIs1 (particularly with the use of cost-benefit analysis) or ensuring long-term financialsustainabilityand,ultimately,facilitatingthedialoguewithfundingagencies.

Ithastobenotedhoweverthat,inofferingapan-Europeanmethodologytoevaluatecostsofdesign, preparation, implementation and decommissioning of RIs across different legalframeworks,andregulatoryandaccountingstandards,theseguidelinesdonotaimatsubstitutingthe standard accounting rules in place in the different countries and under the different legalstatuses.

Themethodologyhasbeendiscussedand testedwith fourexistingRIsand their commentsandreactionsarereflectedinthefinalversionoftheguidelines.

Theguideisstructuredasfollows:thefirstchapterdescribesinanutshellthestepsandeasy-to-use rules to be followed for cost estimation; the following chapters instead provide amorecomprehensivedescriptionandexplanationsofthebasicprinciplesandthedifferentcostitemstobeconsidered.TheAnnex includesasetofexemplarytablesshowingthepossiblestructureandlevelofdisaggregationofdataandfinancialinformation.TheguideiscomplementedbyanExcelfileprovidingatemplateforthecostdatacollectionandcomputationofpresentvalues.

1Themethodologypresentedhereisinlinewiththe‘GuidetoCostBenefitAnalysisofInvestmentProjects’(lastrelease2014)adoptedbytheEuropeanCommission,DGRegionalandUrbanPolicies,formajorinfrastructureprojects,includingRIs.ThisisareferencealsoadoptedbytheEuropeanInvestmentBankandacceptedbytheEuropeanCourtofAuditorsandbyotherinternationaldevelopmentbanks.

2

3

2. ThemethodinanutshellCostsofResearchInfrastructures(RIs) includeamountsthathavetobepaid(cashoutflows)

or resources that have to be employed (in-kind contribution) for the design, preparation,construction or set up, operation, maintenance, upgrade and decommissioning of a RI. Thestandardrulestobefollowedforcostestimation,whicharepresentedinmoredetailsinthenextchapters,arethefollowing:

1. Define the unit of analysis. A careful delimitation of the unit of analysis may requireapportionment and aggregations of cost items, for examplewhen the infrastructureworkswithacomplexoffacilitiesmanagedbydifferentlegalentitiesorwhentheyaredistributed.RIsdonotalwayscoincidewiththecostsofthehostingorganisation(s).

2. Adoptalongtimehorizon.ThetimespanforcostestimationmustreflecttheentirelifecycleoftheRI.Costsmustbereportedforeachyearofthetimehorizon.

3. Fix the start date. The time horizon starts the yearwhen the first resources are deployed(cash or in-kind) for the design and preparation phase of the RI. Re-use of components ofexistingfacilitiesare‘sunk’costsandshouldnotbeincluded.

4. Fixthebaseyear.Thebaseyearisthepoint-in-timewhenthecostestimationismadeanditdoesnotnecessarily coincidewith the startdate.Pastand future costs shouldbe intendedwithrespecttothebaseyear.

5. Costs should be expressed in real terms.Pricesmust be constant at the base year: futurecostsmust be forecasted according to realistic assumptions and should be net of inflationwhilepastcosts,usuallyreported in financialstatements,mustbeconverted intobaseyearvaluebyapplyingtheinflationindex.

6. Only cash outflows are reported. The cost accounting must follow a cash flow method.Depreciation,reservesandotheraccountingitemsthatareusuallyreportedinbalancesheetsmustnotbeincluded.Sourcesoffinancingcanbeusedtoidentifycostitemsbutshallnotbemixedoraddedtothem.

7. In-kind contribution must be included by calculating their corresponding market price oractualproductioncosts.

8. CostsmustbeexpressedinEuro.TheofficialexchangerateofthebaseyearmustbeusedtoconvertforeigncurrenciesinEuro.

9. Costs must distinguish between investment costs and operating costs. Investment costsinclude: design and preparation; construction and start-up; replacement costs; majorupgrades; decommissioning. Operating costs include: rent of building or equipment;personnel; ordinary maintenance and repair; utilities and consumables; management andadministration,etc.

10. Totalcostsmustbecalculatedatpresentvalue.Futurecostsmustbediscountedwhilepastcostsmustbecapitalised(inadditiontoinflated,asexplainedatpoint5)withanappropriatediscountfactor.

4

Thestepsareillustratedinthefollowingdiagram,whilemorecomprehensiveexplanationsanddiscussionsoftherulestobefollowedareprovidedinthefollowingsections.

5

3. GeneralprinciplesBeforeillustratingthespecificrulesforcostaccounting,thischapterillustratessomegeneral

principles that shouldguide thecostingexercise.Theyaremeant toclarify theoverall rationaleandapproachofthecostestimates.

3.1 Identificationoftheunitofanalysis

Projectidentificationconsistsofthedefinitionoftheunitofanalysisandofitsprecisebordersingeographical, legal, functionaland timing terms. It is the first step fora soundcostestimate.Such exercise is not always as straightforward as it may appear at a first glance. The unit ofanalysis must indeed include all cost components that are necessary to achieve the scientificmissionoftheRI;thismeansthatitcanincludeacomplexofdifferentfacilitieslocatedindifferentplacesandmanagedbydifferentorganisations.

RIsareoftenmanagedthroughinternationalcollaborationsinvolvingmanylegalentities.Anindividual scientificprojectcanrequireacomplexof facilitiesandexperiments.Forexample,anaccelerator without a detector cannot deliver any experimental data and the same if only thedetector isconsidered.Suchfacilitiescanberunbydifferent legalbodieswithseparate juridical(and accounting) arrangements. In this case, the definition of the unit of analysis requires thecarefulaggregationandapportionmentofseveralitemswhichmaybeunderdifferentcontractualarrangements.Thisentailsgatheringdatafromthefinancialstatementsofalltheentitiesinvolvedsothatsomeharmonisationmaybeneededbeforeaggregatingcostitems.

FordistributedRIs,consistingofanetworkofhub(s)(e.g.coordinatingsecretariat)andnodeslocatedindifferentlocations/countriesandindifferent(oftenalreadyexisting)infrastructures,therelevant cost items include those incurredby thehub togetherwith those incurredbynationalnodes,aslongasallthosecomponentsand/orprojectsarenecessarytomaketheRIachievingitsmission. The costs of the RI are the sum of the costs of each component, disregarding itsgeographical location. As nodes and/or hubsmay be located within existing facilities that alsoperform research activities unrelated to the distributed RI, only cost items attributable to thedistributedone,includingsharesoftimemachineorpersonnelcosts,mustbeincludedinthecostestimation.

The cost estimationmust include all thematerial and immaterial components which are functionallyconnected to the attainment of the RIs mission. The elements so identified should consist of a self-sufficientunitofanalysis.

6

DETERMININGTHETOTALCOSTSOFDISTRIBUTEDRIs

AdistributedRI is «anetworkofdistributed resources»2 and consistsof aCentralHub (i.e. coordinationsecretariat) and interlinked National Nodes, which can be further coordinating local nodes. A firstimportant distinction is betweendistributedRIs (which, according to the ESFRI roadmap, need – amongother requirements – to be identified by a unique name, legal status3, and governance structure) and acoordinatedresearchnetwork,whichisinsteadthecollaborationoffullyindependentresearchperformingorganizations.

Figure1DistributedRI

Whereas theproblemsof apportionmentandaggregationarise forbothdistributedRIs and coordinatedresearchnetworks, the specificityof the former is that resources (in full or inpart) are coordinatedandmanagedbytheCentralHub.Thisaddsalayerofcomplexity,whichrequiresdistinguishing:

-Thecostsofcentralhubforresearchactivitiesand/orserviceprovision(ifany);-Thecostsofcentralhubforcoordination;-Thecostofnationalnodesforthecoordinationoflocalentities;-Thecostsofnational/localnodesforresearchactivitiesand/orserviceprovision.

Thelackofmandatoryrequirementsforthenodestosharefinancialdatawiththehubrequireswillingness,resourcesandstrongcoordinationtoperformareliablecostingexercise.Insomecases,whenthenumberof sub-entities is too high and the exercise to gather all the data would be too time-consuming,approximation should bemade atmore aggregate level, basedon the available sources.Whenonly thecostsofthecentralhubareavailable,thisshouldbemadeclear.

2Source:https://ec.europa.eu/research/infrastructures/index.cfm?pg=about3Itisworthnotingthattherequirementofthelegalstatusisnotuniversallyrequired,seeforexampleOECD(2014),InternationalDistributedResearchInfrastructure:IssuesandOptions,availableherehttps://ec.europa.eu/research/infrastructures/index.cfm?pg=about

7

AnindividualRIcanmanageaportfolioofdifferentfacilitiesandresearchprojects,eachofthemwithitsownobjective(s).Ifthecostestimationrelatestoasingleexperimentalfacilitybeingpartofalargercomplex,thecoststhataresharedwithotherexperimentsarenotentirelywithinthe scope of the cost estimation and therefore should be carefully apportioned to theinfrastructureunderexamination.Inotherwords,ifdifferentfacilitiesarehostedinthesamesite,withsomefunctionalinterrelations–e.g.,energycosts,administrativecosts,datacentres–coststhatarecommontoallthefacilitiesmustbeapportionedtothedifferententitiesaccordingtotherateoftheiractualuseandfollowingtransparentcriteria.

SomeRIstakeadvantageoffacilities,land,orequipmentownedbyexistinginfrastructures.For the purpose of the costing exercise it is important to distinguish whether the new facilityconstitutesanadditional, self-standingunitorwhether it is insteadanupgradeoranadditionalcomponentstillpartofthesamefacility.Moreprecisely,consideringthecomponentsownedbyanexistingfacility:

APPORTIONMENTANDAGGREGATION

Apportionment and aggregation usually go hand in hand. In RIs involving several legal entities andcollaborations, for instance, actual costs from the different legal entities’ accounts must first beapportionedandthenaggregatedinauniqueaccount.ThisisacommonsituationfordistributedRIs,butitalsoappliestosingle-sitedRIswhereitmayhappenthatamajorinstitutionincludesdifferentfacilitiesandexperimentswithseverallegalentitiesaspartoftherelatedinternationalcollaborations.Hence,indefiningtheunitofanalysis,itisimportant:

- for the institution hosting the facility/experiment, to distinguish the costs pertaining to the facilitywhich has to be costed from those pertaining to the more general functioning (e.g., institutionalactivities,outreach,etc.)ofthehostingRI(apportionment).

- fortheinternationalcollaborations,todistinguishthecostsrelevanttotheactivitiesoff-sitefromthecoststhatinsteadpertaintothegeneralfunctioningofthelegalentity(apportionment).

- to aggregate only the costs of the facility/experiments pertaining both to the hosting RI and theinternationalcollaborationsdulyapportioned.

Figure2Aggregationandapportionment

Differentiatingbetween“blue”and“brown”costsistheactofapportionment

Thesumof“brown”costsistheactofaggregation

8

- if they are simply a re-use of a spare component of a previous facility that could not havealternativeuse,theircostshouldbeconsideredas“sunk”4andshouldnotbeincludedinthecostcomputationofthenewRI.

- If they are a re-use of a spare component but some investments are required for minorimprovements of the inherited facilities/equipment, such additional costs should beconsideredaspartofthecost-estimationofthenewRI.

- Ifthefacility, landorequipmentisprovidedasin-kindcontribution,thentheircostispartofthe cost-estimation of the RI and their appropriate value shall be computed (see below onthis).

3.2 Settingthetimehorizon

The financial resources needed to set-up and run a RImay span a long period of time. Inaddition,thetypicalspendingprofileandcostdistribution,fordifferentcategoriesoftheRI,oftenshowspikesovertime(seefigurebelow).

4Asunkcostisacostthathasalreadybeenincurredandthuscannotberetrieved.Forthisreasontheyareirrelevantforfuturedecision-making.

Costestimatesmustberelatedtotheentirelifecycleoftheinfrastructure,whichmeansconsideringthecostsspanningtheentireperiodoftimeduringwhichthefacilityremainsuseful.Totalcostsincludebothinvestmentandoperatingcosts.

9

Figure3CoststructuresofRIs

A standard spending pattern shows a relatively large investment peak during design,preparationandconstruction,aramp-upphaseafterlaunchanduntilthefullcapacityisreached,thenaquasi-flat spendingperiodduringoperation; spendingpeaksagain ifmajorupgradesareplannedandduringdecommissioning5.Therearehoweverexceptions to this cost-structure. Forexample, RIs involved in taskswhich are performed cyclically (e.g., surveys) display awave-likecoststructure,wherepreparationandimplementationcostsareincurredateverycycle.Anotherexample isprovidedbythoseRIs, typicallydistributedfacilitiesand/orRIswhichrelyonexisting

5Theimpactofmajorupgradesonthelevelofoperatingcostsmaybedifferent:incaseofsignificantupscaling(e.g.increase in the scale or complexity of performed activities), operating costs may increase while in case oftechnologicalimprovementsleadingtoefficiencygainstheymayremainequalorevendecreaseaftertheupgrade.

10

infrastructures, whose set-up phase includes only minor investment costs as compared to theoperationalcosts.

ThecostsofaRIshouldbeconsideredthroughitsentirelifecycle.Itisthusimportanttotakeintoconsiderationareasonably longtimehorizon(theECGuide,2014suggests15-25yearsbutforsomeRIsa longertimehorizoncanalsobe justified).This is irrespectiveofthepoint intimewhenthecost-analysis isconducted(beitexante, in itinere,orexpost).Forthepurposeofthecosting exercise a long-term perspective, looking at the entire lifecycle of a RI, will allow todescribe and assess all the expected/generated costs, including those spreading far into thefuture. This will enable not to miss costs that may be important even if less immediatelyobservable (e.g. replacement costs) and to plan in advance the means to secure long-termfinancialsustainability.RIsmayproduceeffects(andfinancialconsequences)overlongperiodsoftime even beyond its life cycles – e.g., in presence of nuclear wastes requiring expensivedecommissioning costs for their disposal and long-lasting liability, or air/soil/water pollutionbringingremediationcosts.

Inorder to fixanappropriate timehorizontwoelementsarenecessary:a) identificationofthe‘startdate’andb)estimationoftheoverallrealisticdurationoftheRI.Aspertheformer,itshouldcoincidewiththeyearinwhichthefirstoutflowrelatedtotheRImaterializesorthefirstin-kind contribution is received. This is not always straightforward to identify because theconceptualphaseofaRIcanbelongandmayincludeaninitialperiodwhenthescientificmissionis still open to different options defined in a very broadway. As a general rule, the start dateshould be fixed when the first financial or in-kind allocation is made for activities of thepreparatoryphaseofthealreadywell-definedRI.Thereshouldbeevidenceofadetailed,technicalidentificationof the scope andnatureof research activities for considering the timehorizon tohavestarted.Tothisend,thediscussionwiththescientificstaffcanbekeytoidentifytheproperstartingpoint.

Once the start date is set, the entire life-cycle of the infrastructuremust be defined. Thisincludes the design, preparation, set-up and a sufficiently long operational phase, includingupgrades, if any, and final decommissioning. The technical and scientific staff can advise abouthowlongistheperiodinwhichthefacilityremainsreasonablyuseful.Insomecases,sincenotalldesign or feasibility studies lead to the implementation of a RI, some of these costs may beconsideredassunkcosts(moredetailsonthisin3.5).

Thebaseyearisthepoint-in-timewhenthecostestimationisperformed,i.e.theyearoftheESFRI Roadmap application. Depending on whether it is ex-ante (before or approximatelycoincidingwiththestartyear), initinere(justafterthesetupandlaunch),mid-term(aftersomeyearsofoperations)orex-post(aftermostoftheoperationshavealreadybeenperformed),costscanbeforecasts/projections,actual/observeddataoramixofthem.Theyshallbeaccountedforeachyearofthetimehorizon,accordingtothediscountedcashflowapproach,asdescribedinthenextsection.

11

3.3 Discountedcashflowmethod

Therecommendedcostaccountingruleisthecashflowmethod,whichrequiresconsideringonly actual cash inflows and outflows reported in themoment inwhich theymaterialise. Thissystem differs from the standard company accounting conventions and requires someadjustmentsifbalancesheetsandfinancialstatementsareusedassourcesofdata.Inparticular,accounting items that do not correspond to actual flows, such as for example depreciation orreserves,aredisregarded.Asageneral rule,allpricesshouldbeconsiderednetofValueAddedTax,unlessitisnotrecoverableandthusrepresentsanactualcashoutflow.Differencesmayarisefromonecountrytotheother.Forcostestimations,outflowsrepresenttheonlyrelevantsourceofdata(seeboxbelow).

SOURCESOFFINANCING

RI facilitiesare largelydependentonawide rangeofpublic financingsources.While sourcesoffinancing (such as grants, loans, or member fees) provide essential insights for assessing thefinancialsustainabilityofinvestment(whichrequiresthematchingbetweenfinancialin-flowsandoutflowsyear-by-year), itshouldbekept inmindthattheyare inflowsandhenceshouldnotbetakenintoconsiderationforthecostestimation.Theyarehoweveraproxyofthecostscoveredtroughcashcontributions.

Many RIs may rely on some forms of in-kind support. This can be related to the use ofdonated scientific equipment or the exploitation of time machine or personnel costs (this isparticularly true forpan-EuropeanRIs,which relyheavilyon in-kindcontributions fromnationalmembers). They can also refer to technical components or equipment supplied by one of thepartners(e.g.oneMemberStateasashareofitscontribution)andmadeavailablein-kindtotheRI.Sucharrangementscorrespondtotheuseofrealresourcesnotappearinginthebudgetarycostas a cash flow of the RI (but can appear in the budget of the donating/participating partnerinstitution).Theyarehoweverrelevantindicationofcostsand,asageneralrule,shouldbetakenintoaccountattheircurrentmarketprice,ifavailable.Whendealingwithinnovativeproductsforwhichnomarketpriceisavailable,itmaybepossibletodeterminelikelypricesbylookingattheprice of competing, perhaps less innovative, products, or to calculate the marginal cost ofproductionasaproxyformarketprice.

APPORTIONMENTOFIN-KINDCONTRIBUTIONS

In-kind contributions may happen in many forms and for a variety of items. It is worthdistinguishing the case of variable in-kind costs (e.g., contribution of personnel, access toequipmentof services) from fixed in-kindcosts (e.g.,hosting,building,overheadcosts). For thelatter case, where the “burden” of the in-kind contribution can be considered uniformlydistributed,itispossibletocalculateafixedrateofapportionmentasashareofthevariablecostsoftheRI.

Caremustbepaidwhenaggregatingcostsoccurringindifferentyears.Costsoccurringinoneyearcannotsimplybeaddedtocostsoccurringinanotheryear,withtheexceptionperhapsaverydistantyearinthelifespanoftheRI.Thisisbecause1€todayhasmorevaluethan1€tomorrow,foravarietyofreasons including inflation,riskaversionandopportunitycostofcapital.Forthis

Toallowconsistencyandcomparability incostestimates,aharmonizedsystemofaccountsandpricesshallbeadoptedfortheentiretimehorizon.

12

reason,totalcostsmustbeexpressedinpresentvalue6.Past/futurecostsmustbetranslatedintopresent values by means of an appropriate capitalisation/discount rate: each future cash flowshouldbediscountedbyanappropriatefinancialdiscountfactorandeachpastcashflowshouldbecapitalised7.Inprinciplethetwodiscount/capitalisationratesmaydifferastheyrepresenttwodifferent opportunity costs (prospective and retrospective). The adopted rates must be in realterms(seenextsectiononthepricesystem).

6Presentvalue(PV)isthecurrentvalueofafuturesumofmoneyorstreamofcashflowsgivenaspecifieddiscountfactor.7ThesuggestedvaluebytheEuropeanCommissionformajorinfrastructuralprojectsco-fundedwithEuropeanStructuralandInvestmentFundsis4%inrealterms,seeArticle19(Discountingofcashflows)ofCommissionDelegatedRegulation(EU)No480/2014).Theadoptionofadifferentdiscountrateshouldbejustified.

CAPITALISATIONANDDISCOUNTING

Inordertotranslatefuturecostsintopresentvaluestheyshouldbediscountedbyanappropriaterate (actualization). The opposite applies to past costs which are capitalized. To this and, anappropriatediscountfactorwouldbe:

a" =1

(1 + '))

where*isthetime;'isthediscountrate;a"isthediscountfactor.

Theactualizationoffuturecostscanbedonebymultiplyingthetotalcostsinagivenyearbytheidentifieddiscountfactor:

PV =FV)1 + i "

WherePVisthepresentvalue(atthebaseyear)ofthefutureestimatedamountFV).Thehigheris thediscount rate', the lower thepresentvalueof the futureamount.ThePVofa streamofcashflowsisthuscalculatedasthesumofallthepresentvalues:

PV =FV)1 + i "

0

)12

Thecapitalisationofpastcostsisdoneintheoppositeway,consideringthefollowingcoefficient:

a" = 1 + i "

whichdeterminesthefollowingformulafordeterminingthepresentvaluePVofpastcostsPC:

PV = PC) 1 + i "

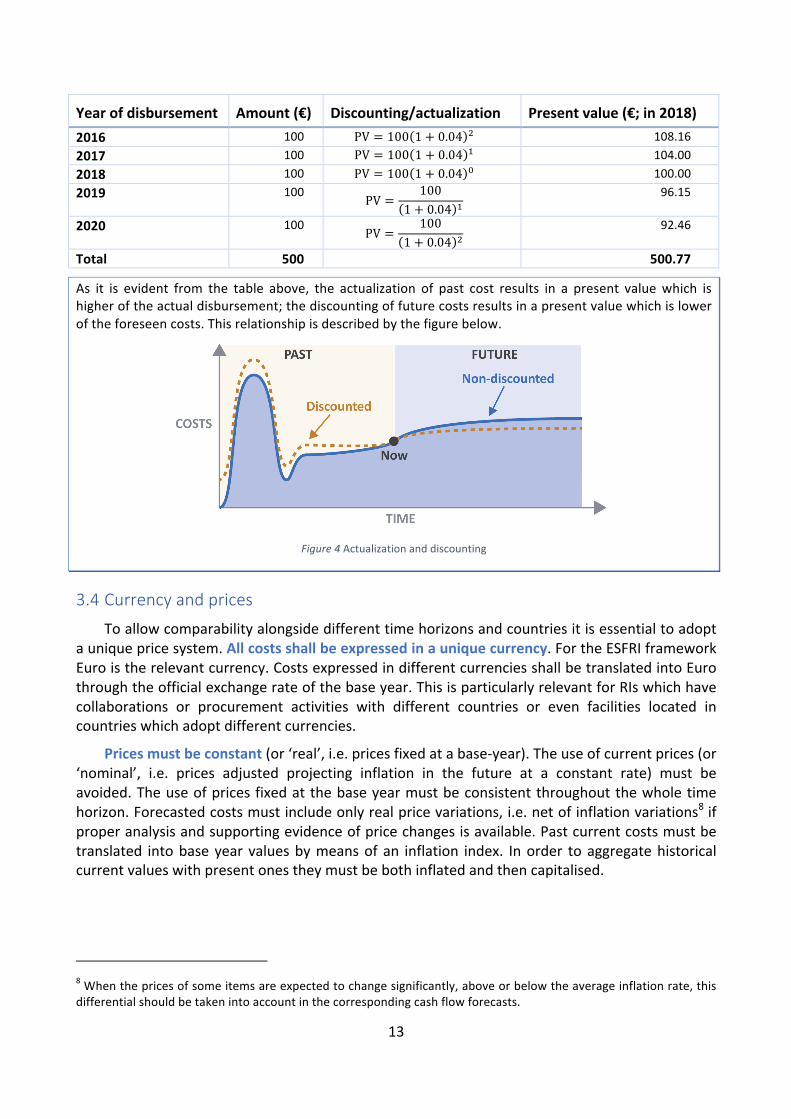

IfweconsiderthecaseofaRIinfrastructureoverashorttimehorizonof5years(2016-2020)withthe total spending per year being € 100, the point-in-time of the analysis being 2018 (i.e. theprojectisinthemiddleofitslifecycleandtheanalysisisinitinere),thenthecapitalisationofpastcostsanddiscountingoffutureonesisdepictedinthetablebelow.

13

3.4 CurrencyandpricesToallowcomparabilityalongsidedifferenttimehorizonsandcountriesitisessentialtoadopt

auniquepricesystem.Allcostsshallbeexpressedinauniquecurrency.FortheESFRIframeworkEuroistherelevantcurrency.CostsexpressedindifferentcurrenciesshallbetranslatedintoEurothroughtheofficialexchangerateofthebaseyear.ThisisparticularlyrelevantforRIswhichhavecollaborations or procurement activities with different countries or even facilities located incountrieswhichadoptdifferentcurrencies.

Pricesmustbeconstant(or‘real’,i.e.pricesfixedatabase-year).Theuseofcurrentprices(or‘nominal’, i.e. prices adjusted projecting inflation in the future at a constant rate) must beavoided.Theuseofpricesfixedatthebaseyearmustbeconsistentthroughoutthewholetimehorizon.Forecastedcostsmustincludeonlyrealpricevariations,i.e.netofinflationvariations8ifproperanalysisandsupportingevidenceofpricechangesisavailable.Pastcurrentcostsmustbetranslated intobaseyearvaluesbymeansofan inflation index. Inorder toaggregatehistoricalcurrentvalueswithpresentonestheymustbebothinflatedandthencapitalised.

8Whenthepricesofsomeitemsareexpectedtochangesignificantly,aboveorbelowtheaverageinflationrate,thisdifferentialshouldbetakenintoaccountinthecorrespondingcashflowforecasts.

Yearofdisbursement Amount(€) Discounting/actualization Presentvalue(€;in2018)2016 100 PV = 100 1 + 0.04 7 108.162017 100 PV = 100 1 + 0.04 8 104.002018 100 PV = 100 1 + 0.04 2 100.002019 100 PV =

1001 + 0.04 8

96.15

2020 100 PV =100

1 + 0.04 792.46

Total 500 500.77

As it is evident from the table above, the actualization of past cost results in a present valuewhich ishigheroftheactualdisbursement;thediscountingoffuturecostsresultsinapresentvaluewhichisloweroftheforeseencosts.Thisrelationshipisdescribedbythefigurebelow.

Figure4Actualizationanddiscounting

14

3.5 Incrementalapproachandcounterfactual

Costsestimationneedtoconsideranappropriatecounterfactual,i.e.whatwouldhavebeenthe costs in the absence of the project. The computation of the incremental costs is thusperformedbysubtractingthecostsofthecounterfactualscenariofromthecostsoftheRI.

In the case of a newly established RI, i.e. with no pre-existing scientific service orinfrastructure, the without-the-project scenario is onewith no operations and the incrementalscenarioisrelativelyeasytocalculatesinceitcoincideswiththecostsoftheRIitself.However,incaseofinvestmentsaimedatimprovingorexpandinganalreadyexistingRI,thecounterfactualisrepresented by the costs of maintaining the service or infrastructure at a level that it is stilloperable(BusinessAsUsual–BAU)orevensmalladaptationinvestmentsthatwereprogrammedto take place anyway (do-minimum). Incremental costs are then the difference between thescenariowithandthatwithouttheproject.This impliesthatcostsavingstranslates intopositivecashflows.

As mentioned, not all the feasibility, design and preparation studies lead to theimplementation of the potential RI considered. Hence, in some cases the BAU scenario shallincludealsothedesignandpreparationphaseoftheabortedRI,atleastpartially,as"sunkcosts".

ThechoicebetweenBAUordo-minimumascounterfactualshouldbemadeonacasebycasebasis. In case of uncertainties, the BAU scenario shall be adopted as a rule of thumb. If do-minimum is usedas counterfactual, this scenario shouldbeboth feasible and credible, andnotcauseundueandunrealisticadditionalbenefitsorcosts.Forsomedistributedinfrastructurestheestablishment of the RI may include only the setting up of the network. In this case the BAUscenariowouldcoincidewiththeproject(s)continuingtooperateinanuncoordinatedway.

INFLATION

ThetablebelowshowstheinflationratesandfactorsforcostsconsideringthetimeseriesofinflationratefortheUnitedKingdom(Source:IMF):

The inflation factor is calculatedbydividingby100 the inflation rate; for the calculationof the inflationadjustmentfactor,oneshouldsetat1theinflationadjustmentofthepoint-in-timeyearandcalculatetheadjustmentfactorbackwardaccordingtotheformula

IAF";8 = IAF" 1 + IF";8

whereIAFistheInflationAdjustmentFactorandIFistheInflationfactor.

Thisinflationfactorconcursthentotheestimationofthepresentvalue.Forexample,ifacostof€100isincurred in 1995, the computation of the present value of this cost will require adjusting this value forinflationbymultiplyingitbyafactorof1.58(seetableabove).

Costsmustalwaysbeaccounted foraccording toan incrementalapproach,which requires toconsiderthecostsoccurringfortheset-upandimplementationoftheRInetofthosethatwouldoccurinanycaseinabsenceoftheRI(the‘withouttheRI’,orcounterfactual,scenario).

15

4. Totalinvestmentcostsandresidualvalue

4.1 Definition

Total investment costs include initial investment costs (thoseoccurringat thebeginningofthe lifecycle for the design, set-up and start of the infrastructure) and replacement costs(occurringduringthereferenceperiodtoreplaceshort-lifemachineryand/orequipment).Insomecasestheycanalsoincludecostsformajorupgrading(asubstantialchangeoftechnicalapproachwhich cannotbe considered routinemaintenance) anddecommissioning costs (when therearedangerousmaterialsorwastetobedisposedofaftertheshutdownofthefacility).

Informationoninvestmentcostsareusuallycontainedinthefeasibilitystudy(iftheanalysisisperformed fromanex-ante perspective) or in the financial statement (ex-post) and thedata toconsiderarethecashorin-kinddeploymentencounteredinthesingleaccountingperiods(years)inordertomakeavailablethevarioustypesofassetsortheequivalentmarketvaluefor in-kindcontributionsnotreportedasfinancialflows.

A residual value of the fixed investments must be included within the investment costsaccount for the end-year. The residual value reflects the capacity of the remaining servicepotentialoffixedassetswhoseeconomiclifeisnotyetcompletelyexhausted.

4.2 Mainitems

Even if the cost types are project-specific, the data can be usually aggregated into somemacro-items,whichwillbeanalysedinthefollowingsections:

• Designandpreparation(aspartofinitialinvestmentcosts,includingtestingandstart-up)• Constructionandstart-up,including:

o Physical(e.g.,landacquisition,installations,constructions)andnon-physical(e.g.,IPRs,cloud,other informationtechnologies)assets,usually themajorcomponentof initialinvestmentcosts;

o Personnel;o Start-upcosts(e.g.training,licences,etc.);

• Replacementcosts;• Majorupgrades;• Decommissioningandend-of-lifecosts.

4.2.1 Designandpreparation

Design and preparation costs are all the in-kind and cash expenditures needed for theconceptualdesignandfeasibilitystudyofthe infrastructure.Theyalso includethecostsforthepreparatoryphaseofaRI,includingpossibleinterim-phaseafterthepreparatoryproject.

The main items included in this cost category are scientific, technical and managerialpersonnelcosts;networkingactivities;joint-researchactivitiesandtrans-nationalcooperation.In-

Investment costs are related to the acquisition of durable tangible and intangible assets. They areincurred inviewofeffects thatmaterialize ina financialyear(s)different fromthat inwhichtheytookplace.

16

kindcontributions in thisphasecanbemainly in the formof in-kindscontributionofpersonnelcosts.

Since not all design and preparation studies lead to the implementation of the project, insomecasesthesecanbeconsideredassunkcosts–atleastpartially.Moreover,inthecaseofnewfacilities developed in the same location of previous infrastructures and experiments,which tosomeextenttakeadvantageoftheexistingassets,itisimportantnottoincludethecostsincurredbefore the start of thedesignperiod, such as costs for feasibility studies undertakenwhen themissionof theRIhadnotbeenclearlydefinedyet,orconstructioncostsalreadysustainedforaprevious project. These, as mentioned, are often sunk costs and must be excluded from theinvestmentcosts.

4.2.2 Constructionandstart-upcosts

Constructions costs relate to the set up and launch from a physical, institutional, legal,organisationalandmanagerialpointofviewoftheinfrastructure.Themainitemsarepresentedinthefollowingsections.

4.2.2.1 Physicalandnon-physicalassets

Assets can be physical or non-physical. The former usually include all assets such as landacquisition,buildings,civilworks,machineriesandequipment.Physicalassetsusuallyrepresentasignificant share of investment costs of non-virtual major infrastructures. Non-physical assetsinclude virtual assets (such as IT platforms, clouds, virtual information technologies and databanks)andotherintangibles(suchasintellectualproperty,patentsandlicences).

Assetscanbeprovidedalsointheformofin-kindcontributions,whentheydonotcorrespondto any cash outflow corresponded directly by the RI. In-kind contributions may refer to bothphysical assets (such as a magnet, machinery, etc.) and non-physical assets (such as virtualcomponents).Inthecaseofmulti-sitedordistributedRIs,whichhavemorethanonephysicalsite,itiskeytoproperlyaggregatethecostitems.Inparticular,thecostsrelatedtothenationalhubsornodesmustbecalculatedasperquotaofparticipationinthedistributedRI.

4.2.2.2 Personnel

Cost of the personnel involved in all the construction and set-up phase not related to theroutine operations of the RI – should be included in the investment costs. They can includescientific,technical,administrativeandmanagerialpersonnelcosts.

Personnel may be provided also as in-kind contributions: they should be included in theanalysis at theequivalent labour cost coveredby thepartner institution and including salaries,fringebenefits,andsocialsecuritycontributionsofpersonnelengaged.InthecaseofdistributedRIs,whenthepersonnelmaybeinvolvedindifferentactivitiesalsonotrelatedtothedistributedRI, it is important to include only the share of his/her work-time actually dedicated to theconsideredRIasdocumented in timesheetsor similar internal records.Thesamemayapply forthe administrative personnel in the hosting organisation which do not fully coincide with thefacilityunderassessmentbuthostsaportfolioofdifferentfacilities.Inthiscase,thetimeshouldthusbedulyapportioneddistinguishingtheamountthatshouldbechargedtotheRI.

17

4.2.2.3 Consumables,utilitiesandothercosts

Theyincludeallthecostsincurredduringtheinitialphasetoset-upthefacilitywhicharenotincludedinthepreviouscategories.Theycanincludetheuseofenergy,waterorwastedisposal,travelandothercostfornetworkingandjoinresearchactivitiesandsoon.

4.2.2.4 Start-upcosts

They include all costs related to the launch of operations, including training costs andacquisitionoflicencesandpatents.

4.2.3 Replacementcosts

Replacement costs correspond to the capital expenditure required to replace those assetswhoseeconomiclifetimeisshorterthanthereferenceperiod.Theeconomiclifetimeisdifferentfor various investment assets (buildings, machinery and equipment, etc.). In order to keep afacility in operation, each assetmust be replaced at the appropriate timeand the replacementcosts,whenforeseensincethestart,mustbeincludedintheinvestmentcosts.

4.2.4 Majorupgrades

Extraordinarymaintenanceandmajorupgradesareinvestmentscostwhichoccurduringtheoperational phase and are related to themodernization and expansionof the facility. They areinterventionswhichmodifytheperformanceinastructuralwayandproduceeffectsbeyondthefinancialyear(s)inwhichtheytakeplace.

Asageneralrule,theyshouldbeincludedintheanalysisintheyeartheyareplannedtooccuronly (i) if they are pertinent to the initial investment project and (ii) if they were alreadyscheduledintheex-antephase.Ifoneorbothconditionsarenotmet,theseinvestmentsshouldbeanalysedinseparatestudies.

The timingprofileofmajorupgradesmayvarydependingon thespecificRI.Suchupgradesareoftenplannedwellinadvance,inanticipationofnewtechnologieswhichwerenotavailableatthetimeoftheinitialdesignbutwereavailableatthestart-upoftheproject.

Itisimportanttodecidesincethebeginningwhetheranupgradeispartofthelife-cycleoftheRIorwhetherinsteaditconstitutesaself-standingproject.

4.2.5 Decommissioningandend-of-lifecosts

End-of-lifecostsrelatetoanydecommissioningcostsand/orenvironmentalmitigationcoststhat may be necessary at the end of the time horizon to dismantle the whole or individualcomponentsofthefixedassets.Majoritemsareusuallythecostsofdismantling,disposalandlandreclamation. In case of nuclear wastes, these costs can be particularly high (up to absorbingcompletelytheresidualvalue)andproducelong-standingfinancialresponsibility.

4.3 ResidualvalueThe residual value reflects the capacity of the remaining service potential of fixed assets

whoseeconomic life isnot yet completelyexhausted. Itmustbe included for theend-yearandwithanegativesign,sinceitisaninflow.Itwillbezeroornegligibleifatimehorizonequaltotheeconomiclifetimeoftheassethasbeenselectedorifdecommissioncostsareparticularlyhigh.Itistheonlyinflowitemofthetotalinvestmentcosts.

18

4.4 Presentvalueoftotalinvestmentcosts

Total investment costsmust be calculated along the entire time horizon as the discountedsumofthefinancialflowsofalltheinvestmentcostitemsfortheentiretimehorizon,regardlessthesourcesoffinancing.Inanex-anteperspective,thepresentvalueoftotalinvestmentcostsisthusasfollows:

<= = >?(8@A)?

0)12 + B?

(8@A)?+ CB?

(8@A)?+ DE?

(8@A)?+ >B?

(8@A)?− CG?

(8@A)?

whereNisthenumberofyearsofthetimehorizon,Dtisthedesignandpreparationcostsattimet,Ctistheconstructionandstart-upcostsattimet,RCtarethereplacementcostsatthetimet,MUtarethemajorupgradescostsattimet,DCtisthedecommissioningcostsattimet,RVtistheresidualvalueattimetandiistheselecteddiscountrate.

Similarly,inanex-postperspective,thepresentvalueoftotalinvestmentcostsis:

<= = H)(1 + ')) + I)(1 + ')) + JI)(1 + ')) + KL)(1 + ')) + HI)(1 + ')) − J=)(1 + '))0

)12

whereiistheselectedcapitalisationrate.

Inaninitinereperspective,bothdiscountedfuturecostsandcapitalisedpastcostsshouldbesummed.

19

5. Operatingcosts

5.1 Definition

In an ex-ante perspective, cost forecasts can be based on historic unit costs. In an ex-postperspective they can be retrieved from financial statements and balance sheets provided thenecessaryadjustmentstoadheretothecashflowmethod.

Operating costs canbedistinguishedbetween fixed (for a given capacity, they donot varywith the volume of good/service provided) and variable (they depend on the volume). Cost offinancing (i.e. interestpayments) followadifferent courseandmustnotbe includedwithin theoperatingcosts(buttheyshouldbeaccountedforinananalysisoffinancialsustainability).

Although it is always possible to compute the average annual operating costs, it should benotedthatoperatingcoststendtoberelativelyconstantwhentheRI isrunningat fullcapacity,but in the start-up and launchphase, before arriving at full capacity, there is a rampupphasewhichcanlastsomeyears(seeFigure3).Hence,assumingcoststobeconstantacrosstheentirelifetimeofRIisnotaccurateandcanfailtoprovideusefulinformation.Measuressuchasthenetpresentvalueprovidemuchmoreinsights,comparedtotheannualaverage,fortheaimsofcostestimation.

5.2 Mainitems

Although the actual composition is project-specific, typical operating costs include: rent ofbuildings or sheds, rental ofmachinery; personnel; ordinarymaintenance and repair of assets;utilities (consumption of rawmaterials, fuel, energy) and consumables; users support, servicespurchased from third parties. Other operating costs may include: environmental protectionmeasures, generalmanagement, administration and quality control costs, royalties paid for theuseofpatentedproductsorprocesses,promotionalcampaignsandotheroutreachexpenditures.Obviously,theweightofthesecostitemsisdifferentacrossvariousscientificdomainsandtypeofinfrastructures. As already mentioned, in line with the cash flow method items such asdepreciation, customarilyused in standardaccounting, shall notbe included for thepurposeofcostestimations.

AcostbookisalistofunitcostsforthemaincostitemsoftheRI(e.g.,costoftheaccessforoneday,unit costofadministrative/scientific/managerialpersonnel,etc.). It isusuallyproducedduringthepreparatoryphaseofinfrastructureandcanbeusedtoforecasttheoperatingcosts.

Personnel costs are usually distinguished by functions (research, administration, technicaloperation, etc.) and by category. As mentioned, if personnel contribution is provided in-kindcontributionstheyshouldbeincludedintheanalysisattheequivalentlabourcost, includingthevalueofsalaries,fringebenefit,andsocialsecuritycontributions.Apportionmentisneededincaseofdistributedfacilities,asalreadydiscussedforinvestmentcosts.

Trainingexpensesshouldalsobetakenintoaccount,asthoserelatedtothedevelopmentofscientific, technical and management skills and capabilities which are essential also for thesustainabilityoftheRI.

Operatingcostsincludealldisbursements(bothin-kindoroutflows)neededtooperateandmaintaintheneworupgradedfacility.

20

Equipment,materialsand labourcostsnecessary for cleaningandmaintaining thebuildingsandthefacilitiesingoodcondition,includingexpendituretofixbrokenpartsandreplacementofspare parts are included as repair and ordinarymaintenance costs. Asmentioned above, theyincludereplacementcostsoffixedassetifself-financedbytheprojectrevenues.

Utilitiesandsupportservicesinclude:fuel/diesel,electricity,gas,waterandrecycledwaste,aswellasotherspecificservices.Anestimateofutilitiesconsumption isessential for identifyingtheexistingsourcesofsupplyandanyexistingorpotentialbottlenecksorshortagesifrequestingeitherinternalorexternaladditionalsupplies.

Consumablesincluderawmaterials,basemetals,(semi)processedmaterialsandcomponents,packagingmaterials,containers, labmaterials,etc. Thetransportcostsfromsourceofsupplytothefacilityshallalsobeconsidered.

Users support refers to the cost-per-user related to the assistance to the users whenaccessing the facility (either physically or virtually). It has implications on the technical andscientific infrastructure, the timeof theadministrative, technicalandscientificpersonnel that isdedicated to each user (users office, referees, technical assessment of feasibility, specific user-demandedconsumables).Itmayalsoincludecostsrelatedtotheuseofguesthouseandcanteenfortheusers(tobeoperatedalsoonweek-endsandholidays)andpossiblecontributionstowardstravelofusersincaseoflackofexternalfunds.TheseitemscanvarysignificantlyacrossdifferenttypesofRIsbut,inanycase,theyrepresentactualcoststobereported.

Data Management, FAIR compliance, EOSC compliance result in significant costs for theimplementationofmetadataandmaintenanceofrepositoriesopentothereferenceusersand/ortothewiderpublicwhichmightexploit the interoperability.Suchcostsmay include:diskspace,computing power, networks, electric energy, specialised personnel (e.g., data stewards or datascientists);thesecostsareusuallyheavilydependentuponthenumberofusers.

5.3 PresentvalueofoperatingcostsSimilartoinvestmentcosts,operatingcostsmustbecalculatedalongtheentiretimehorizon

by reporting the total value of disbursement or in-kind contribution for each year of the timehorizonandforeachof themaincost items.Valueswillbeequal tozeroduringthedesignandconstructioncosts, then rampingupafter theopeningand startofoperationand finallyalmostconstantduringthefullcapacityphase.Thepresentvalueoftotaloperatingcostsiscalculatedasthesumofthediscountedandcapitalisedfinancialflowsofallthecostitemsfortheentiretimehorizon.

21

6. Annex:CasestudiesThecases included in thisannexareexamplesofdifferent typologiesofRIsandcoststructures.Theyaremeanttoprovidesuggestionsonhowtopresentthecostsandovercomingsomeofthemostcommonchallenges.ThecasestudiesareinspiredbyrealRIsbut,forobviousconfidentialityreasons, do not reflect their actual costs. They are however realistic examples reflecting – inproportion, evolution, apportionment and aggregation – reasonable estimates for the typologyandcoststructureconsidered.

ThecasesfollowthestructureoftheexceltemplateannexedtothepresentGuide.

Allcasesstartwithsettingthekey-parametersofaRI:

• Country:forthepropercomputationoftheappropriateinflationrate.• Baseyear,startdateandtimehorizon:forthesubsequentcomputationofdiscount

and/oractualization.• Capitalisationanddiscountrates:setalways,inthesecasestudies,attheratesof5%and

4%.Deviationsfromtheseparametersshouldbejustified.• Scaleandcurrencyshouldalsobemadeexplicit.

After setting the key-parameters, both investment and operating costs are presented. In thesecases,theexcerptsofthetablesalwaysrefertototalasdiscountedtotal.Finally,acostoverviewispresented.

6.1 Asingle-sitedRIinoperationThecasepresentedherecanbethoughtasastandardcasewithlowlevelofcomplexity.Itisthecaseofasingle-sitedRIinoperation.Thekeyparametersaresetasfollows:

The investment costs include all the relevant costs along the entire life-cycle: from design andconstruction, the foreseenupdate anddecommissioning. Theoperating costs followa standardstructure,witha ramp-upphase followedbya stabilisationofpricesanda little increaseat thetimeoftheforeseenmajorupgrade.

22

Table1Investmen

tand

ope

ratin

gcostso

fasingle-site

dRI-EU

Rmillion,nom

inalnotdisc

ounted

To

t.(disc

ounted

,EU

R20

18)

2006

20

07

2008

20

09

2010

20

11

2012

20

13-201

620

17

2018

20

19-202

520

26

Desig

nan

dpreparation

17.92

1.30

1.50

2.15

3.00

2.00

Physicalassets

13.01

1.00

1.20

1.50

2.00

1.50

Non

-physic

alassets

6.50

0.50

0.60

0.75

1.00

0.75

Person

nel

14.97

0.80

1.20

1.40

2.00

1.70

1.00

1.20

Majorupg

rade

4.62

2.00

2.50

Decommiss

ioning

2.19

3.00

Initialin

vestmen

tcosts

59.22

3.60

4.50

5.80

8.00

5.95

3.00

3.70

3.00

Replacem

entcosts

1.53

0.3

0.5

0.1

Totalinv

estm

entcosts

60.75

3.60

4.50

5.80

8.00

5.95

0.3

3.50

3.70

0.1

3.00

Resid

ualvalue

4.38

-6

Person

nel

27.11

1.20

1.40

1.60

1.90

1.90

1.90

0.90

Training

6.75

0.20

0.30

0.40

0.50

0.50

0.50

0.20

Utilities

5.41

0.20

0.25

0.30

0.40

0.40

0.40

0.20

Consum

ables

5.41

0.20

0.25

0.30

0.40

0.40

0.40

0.20

Usersup

port

8.77

0.10

0.30

0.50

0.70

0.70

0.70

0.30

Datam

anag

ement

0.81

0.05

0.05

0.05

0.05

0.05

0.05

0.05

Totalo

peratin

gcosts

54.25

1.95

2.55

3.15

3.95

3.95

3.95

1.85

23

Anoverviewoftotalcostsisprovidedbelow:

EUR Millionatbaseyear(2018)

Totaloperatingcosts,discountedYearlyoperatingcostsinthelastyearoftimehorizon

Totalinvestmentcosts,discountedResidualvalue,notdiscountedResidualvalue,discountedTotaloperatingcosts,notdiscounted

1.85

6.004.38

Totalinvestmentcosts,notdiscounted60.75

54.4854.25

42.32

24

6.2 AdistributedRIinoperationThis is the case of a distributedRI, including both national nodes and local sub-nodes. The keyparametersaresetasfollows:

Investment and operating costs can be presented aggregated per central hub and nationalnode(s). Investment costs are incurred up to 2013; from 2014 there are only operating costs.Operatingcostsincreaseuntiltheystabilizeaftertheramp-upphase.

25

Table2Investmen

tand

ope

ratin

gcostso

fadistrib

uted

RI-EUR

thou

sand

,nom

inalnotdisc

ounted

To

t.(disc

ounted

,EU

R20

18)

2007

20

08-

2011

20

12

2013

20

14

2015

20

16

2017

20

18

2019

…

2047

Centralhub

18

,455

12

8

1,78

2

1,78

2

1,78

2

Non-ph

ysica

lasset

5,68

4

80

540

540

540

Desig

n

1,70

5

24

162

162

162

In-kind

11,066

24

1,08

0

1,08

0

1,08

0

….

Node

Cou

ntry1

1,72

4

62

120

120

240

Node

coun

try2

743

33

55

55

90

Totalinvestm

entcosts

20,923

22

3

1,95

72,11

2

2,13

4

Resid

ualvalue

-1,500

Centralhub

18

6,23

5

1,00

1

2,00

92,92

2

4,46

19,55

3

9,70

7

9,70

7

9,70

7

Node

Cou

ntry1

144,33

2

775

1,55

7

2,26

4

3,45

7

7,40

37,52

2

7,52

2

7,52

2

Node

coun

try2

59’537

32

064

2

934

1,42

6

3,05

4

3,10

3

3,10

3

3,10

3

Totalope

ratin

gcosts

390,10

3

2,09

7

4,20

8

6,12

1

9,34

4

20,011

20

,333

20

,333

20

,333

26

Anoverviewofthetotalcostsisprovidedbelow:

EUR thousandatbaseyear(2018)

Totaloperatingcosts,discountedYearlyoperatingcostsinthelastyearoftimehorizon

Totalinvestmentcosts,discountedResidualvalue,notdiscountedResidualvalue,discountedTotaloperatingcosts,notdiscounted

20,333

1,500481

Totalinvestmentcosts,notdiscounted

390,103

14,38120,923

632,144

27

6.3 Anupgradeofanexistingsingle-sitedfacilityThis is the caseof a single-sitedRI; the case consideredhere concernsamajorupgradeof aRIexisting for over 50 years. Thismeans that the scope of the costing exercise is not the RI as awhole but the incremental scenario of the upgrade as compared to a business as usual (BAU)scenario.Themainchallengeshereconcerntheidentificationofaproperunitofanalysisandtherelatedtimehorizon. Indeterminingtheproperunitofanalysisapportionmentexercisesshouldbepossiblymade:forestimatingthecostofupgradeitwillbenecessarytoidentifyandapportiontherelatedcostsfrombalancesheetswhicharerelatedtotheentireRI.Itisinsteadessentialtoconsider only those costs which correspond to the incremental scenario with respect to thecounterfactual,i.e.,thebusinessasusual.Themainchallengeisthusto“isolate”theincremental,asshowedinthefigurebelow.

Figure5Upgradescenariovs.BAUscenario

Ofcoursethishasalsoaninfluenceonthetimehorizon;forinstance,inthecaseconsidered,eveniftheRIwasfoundedinthe1960sthebaseyearshouldrelatetotheupgrade–hence,itissetatyear 2000. It is not always straightforward to identify the correct base year as it is likely thatdifferent upgrading optionswere taken into considerations at differentmoments. Design costsshouldbeconsideredsunkcosts if theyarebornealso for thoseupgradeswhichare finallynotimplemented.

Thefollowingtablecontainsthekey-parametersasidentifiedperthecaseconsidered.

INCREM

ENTALSCEN

ARIO

28

Thetablebe

lowsh

owsthe

investmen

tcostsofa

majorupgrade

ofa

single-site

dRI.Itisw

orthnotingthatitisverylikelythatinth

efirstyearsth

eop

eratingcostsw

ouldberatherstable,beforetheup

gradeisfullyim

plem

ented,fo

llowingbyaru

mp-up

phaseand

thusastabilizatio

n.

Table3Investmen

tand

ope

ratin

gcostofa

single-site

dRIwith

am

ajorupgrade

-EUR

thou

sand

,nom

inalnotdisc

ounted

To

t.(disc

ounted

,EU

R20

18)

2000

20

01

2002

-202

120

22

2023

20

24

2025

20

26

2027

20

28-

2032

20

33

Desig

nan

dpreparation

2,31

9

172

237

Fixedassets

19,183

17

223

7…

900

800

ITassets

17,630

86

11

9…

2,70

02,40

0

Equipm

ent

51,726

17

223

7…

3,60

03,20

0

Person

nel

69,357

25

835

6…

900

800

IPRs

17,630

86

11

9…

900

800

Decommiss

ioning

22

,211

40

,000

Total

investmen

tcosts

200,05

7

946

946

…

9,00

0

8,00

0

40

,000

Consum

ables

992

10

0.0

100.0

100.0

100.0

115.5

127.1

139.8

97.9

Training

expenses

496

50

.0

50.0

50.0

50.0

57.8

63.5

69.9

48.9

Maintenan

ce

1,98

3

20

0.0

200.0

200.0

200.0

231.0

254.1

279.5

195.7

Administratio

n69

4

70

.0

70.0

70.0

70.0

80.9

88.9

97.8

68.5

Locatio

nrent

2,97

5

30

0.0

300.0

300.0

300.0

346.5

381.2

419.3

293.5

Person

nel

992

10

0.0

100.0

100.0

100.0

115.5

127.1

139.8

97.9

Totalo

peratin

gcosts

8,13

1

820

820

820

861

947

1,04

2

1,14

680

2

29

Asummarytablewithoverviewofinvestmentandoperatingcostsisprovidedbelow:

EUR thousandatbaseyear(2018)

200,057

11,8438,131

170,919

802

00

Totalinvestmentcosts,notdiscounted

Totaloperatingcosts,discountedYearlyoperatingcostsinthelastyearoftimehorizon

Totalinvestmentcosts,discountedResidualvalue,notdiscountedResidualvalue,discountedTotaloperatingcosts,notdiscounted

30

6.4 AdistributedRIinoperationThisisthecaseofadistributedRIinfrastructure,whosecentralhubisbasedinGermany.

TheparticularityofthisRIisthatitdoesnotfollowastandardcost-structurebutawave-likecoststructure (see Figure 3). One main challenge of this approach is to identify which are theinvestmentcostsandwhicharetheoperatingcosts.Indeed,differentlyfromwhathappenswithRIs with a standard cost-structure, the investment costs are incurred for each of the waves –hence,duringtheentirelife-cycleoftheRI.Inthisparticularcaseinvestmentandoperatingcostsspanoverthesametimehorizon.Inparticular,forthecaseconsideredhere,thephasesofdesign,preparation,andconstructionareconsideredtobepartoftheinvestmentcostsasreportedinthetablebelow.AnotherchallengeistheallocationofthecostsbetweenthecostsrelatedtothecoreoperationsoftheRI(thesurvey,inourcase),typicallycarriedoutbythenationalnodes,andthecostsrelatedtotheinternationalcoordination(bornebythecentralhub).

31

Table4Investmen

tand

ope

ratin

gcosts-Distrib

uted

RIw

ithwave-likecoststructure-E

URm

illion,nom

inalnotdisc

ounted

To

t.(disc

ounted

,EU

R20

18)

2002

20

03

2004

20

05

2006

20

07

2008

20

09-

2021

20

22

2023

Int.Co

ordina

tion

77.8

1.29

9

1.29

9

1.29

9

2.63

5

1.45

9

2.96

1

1.84

2

…

2.06

5

4.19

4

Desig

n65

.6

1.06

1

1.06

1

1.06

1

2.15

3

1.15

5

2.34

5

1.53

0

…

1.81

6

3.68

7

Preparation

5.3

0.11

9

0.11

9

0.11

9

0.24

1

0.15

2

0.30

8

0.15

6

…

0.08

2

0.16

7

Constructio

n6.8

0.11

9

0.11

9

0.11

9

0.24

1

0.15

2

0.30

8

0.15

6

…

0.16

7

0.34

0

Wav

es

130.0

0.85

5

0.85

5

0.85

5

1.73

6

0.61

8

1.25

5

0.64

6

…

6.22

0

12.629

Desig

n14

.0

0.21

4

0.21

4

0.21

4

0.43

5

0.28

4

0.57

7

0.28

8

…

0.40

6

0.82

5

Preparation

0.6

0.01

3

0.01

3

0.01

3

0.02

7

0.01

7

0.03

4

0.01

7

…

0.00

9

0.01

9

Constructio

n11

5.5

0.62

8

0.62

8

0.62

8

1.27

4

0.31

7

0.64

4

0.34

1

…

5.80

5

11.785

Totalinv

estm

entcosts

208.80

2.15

2.15

2.15

4.37

2.08

4.22

2.49

…

8.29

16

.82

Resid

ualvalue

1.03

1.2

Int.Co

ordina

tion

12.3

0.16

9

0.34

4

0.16

9

0.34

4

0.21

7

0.44

0

0.22

3

…

0.36

1

0.73

2

Waves

4.4

0.06

2

0.06

2

0.06

2

0.12

7

0.08

4

0.17

0

0.08

4

…

0.13

5

0.27

5

Totalo

peratin

gcosts

16.6

0.23

2

0.40

6

0.23

2

0.47

0

0.30

0

0.61

0

0.30

7

…

0.49

6

1.00

7

32

Thefinaltableshowsthemostrelevantsummaryinformationoftheanalysis.

EUR Millionatbaseyear(2018)

207.8

12.216.6

166.8

1.0

1.21.0

Totalinvestmentcosts,notdiscounted

Totaloperatingcosts,discountedYearlyoperatingcostsinthelastyearoftimehorizon

Totalinvestmentcosts,discountedResidualvalue,notdiscountedResidualvalue,discountedTotaloperatingcosts,notdiscounted

33

Glossary

Apportionment Thedivisionorsplitofresources(costsand/orpersonormachine-time)amongdifferent legalentitiesorprojectsaccordingtotheirproportionofactualuse.

Baseyear The point-in-time of the analysis, which serves as a base for financialcomputations.Itisthereferenceyearfortheanalysis,i.e.ex-ante,mid-term,ex-post.

Businessasusual Aninertialscenarioassumingnochangeintheoperation.

Capitalisation Theprocessofdetermining thepresent valueofpast flows (backwardperspective),adjustingforaproperfinancialcapitalisationrate.

Cashflow Theamountofmoneytransferredin-orout.

Currentprice Thecurrentprice,alsoknownasthenominalvalue,isthepriceatwhichgoodsandservicesaresold inthemarket.Differentlyfromrealprices,nominalpricesincludeinflation.

Constantprice Constantpricesareawayofmeasuringtherealvalueofagoodand/orservice. A year is chosen as the base year. For any subsequent ordifferentyear,thevalueofthegood/serviceismeasuredusingthepricelevelofthebaseyear,regardlessofvariationsintheinflationindex.

Counterfactual The scenario thatdescribeswhatwouldhappen in theabsenceof theproject/RI.

Deflating The action of changing current (nominal) prices into real (constant)pricesbyremovingtheeffectofpricechange.

Discountrate Theinterestrateusedtodiscountfuturecashvaluestodeterminetheirpresentvalue

Discounting The process of determining the present value of future cash flows(forwardperspective),adjustingforaproperdiscountrate

Do-minimum A scenario assuming only planned or committed minor futureinvestmentsneededtokeepunchangedthecurrentperformanceortoperformsmallimprovementoftheproject/RI.

In-kindcontribution Non-cash contribution provided by a legal entity (e.g. in terms ofpersonnel or machine time, supply of equipment, services, buildings,etc.)

Inflation Therateatwhichtheaveragepricelevelofabasketofselectedgoodsandservicesinaneconomyincreasesoveraperiodoftime.Itisaproxyoftheincreaseofthegeneral levelofprices.Realpricesareconvertedintocurrentonesbyaddinginflationtotheformer,andviceversa.

NetPresentValue The difference between the present value of inflows and the presentvaluesofoutflowsinagivenperiodoftime.

Presentvalue The capitalised or discounted value of a past or future cash flow at agivencapitalisationordiscountrate.