guide to public retirement systems in texas · guide to public retirement systems in texas. ... and...

TRANSCRIPT

State Pension Review Board 84th Legislature February 2015

GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS

PAGE INTENTIONALLY LEFT BLANK

State Pension Review Board

Anumeha (Anu)

Interim Executive Director

Paul A. Braden, Chair Position: Pension Law Term Expiration: January 31, 2015 Hometown: Dallas J. Robert Massengale, Vice Chair Position: Retired Member Term Expiration: January 31, 2017 Hometown: Lubbock Keith W. Brainard Position: Pension Administration Term Expiration: January 31, 2019 Hometown: Georgetown Andrew W. Cable Position: Active Member Term Expiration: January 31, 2019 Hometown: Wimberley

Leslie Greco-Pool Position: Securities & Investment Term Expiration: January 31, 2015 Hometown: Euless Robert M. May Position: Actuary Term Expiration: January 31, 2019 Hometown: Austin Wayne R. Roberts Position: Governmental Finance Term Expiration: January 31, 2015 Hometown: Austin

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

PAGE INTENTIONALLY LEFT BLANK

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

February 12, 2015

Honorable Members of the 84th Texas Legislature

Ladies and Gentlemen:

The State Pension Review Board (PRB) is pleased to present its Guide to Public Retirement Systems in Texas, February 2015. This publication provides general and comparative information on Texas public retirement systems, including current data in the following areas: financial, actuarial, benefits, membership, and governance.

The Guide specifically focuses on the 93 actuarially-funded defined benefit systems and is divided into three major sections. The first section contains summaries of the statewide and municipal retirement systems governed by state statute. The second section provides trends and key financial, actuarial, benefit, and governance data for retirement systems. The third section provides a summary of significant pension-related legislation passed in recent legislative sessions, benefit information for the pay-as-you-go volunteer firefighter and defined contribution retirement systems, a glossary of pension terminology, and a directory of all 331 systems registered with the PRB.

The PRB would like to thank the retirement systems for their assistance in preparing this report. We look forward to working with all interested parties during the 84th Legislative Session and hope that this report will serve as a reference point for any possible pension bills considered during this session.

The PRB is honored to serve the State of Texas and is firmly committed to its mission to help ensure that Texas public retirement systems are properly managed and actuarially sound.

Sincerely,

Anumeha Interim Executive Director

TABLE OF CONTENTS Introductory Section About the State Pension Review Board

PRB Guidelines for Actuarial Soundness

Summary of Statutorily Governed Public Retirement Systems in Texas Employees Retirement System of Texas .................................................................................................................................................................... 2

Judicial Retirement System of Texas Plan One .......................................................................................................................................................... 3

Judicial Retirement System of Texas Plan Two .......................................................................................................................................................... 3

Law Enforcement and Custodial Officer Supplemental Retirement Fund ................................................................................................................. 4

Teacher Retirement System of Texas ........................................................................................................................................................................ 5

Optional Retirement Program ................................................................................................................................................................................... 6

Texas County & District Retirement System .............................................................................................................................................................. 7

Texas Emergency Services Retirement System .......................................................................................................................................................... 8

Texas Municipal Retirement System .......................................................................................................................................................................... 9

City of Austin Employees’ Retirement System ......................................................................................................................................................... 10

Austin Fire Fighters Relief & Retirement Fund ........................................................................................................................................................ 11

Austin Police Retirement System ............................................................................................................................................................................. 12

Dallas Police & Fire Pension System ........................................................................................................................................................................ 13

El Paso Firemen & Policemen’s Pension Fund ......................................................................................................................................................... 14

Fort Worth Employees’ Retirement Fund ................................................................................................................................................................ 15

Galveston Employees’ Retirement Plan for Police ................................................................................................................................................... 16

Houston Firefighters’ Relief & Retirement Fund ..................................................................................................................................................... 17

Houston Municipal Employees Pension System ...................................................................................................................................................... 18

Houston Police Officer’s Pension System ................................................................................................................................................................ 19

San Antonio Fire & Police Pension Fund .................................................................................................................................................................. 20

TABLE OF CONTENTS

Texas Local Fire Fighters Retirement Act ................................................................................................................................................................. 21

Plans Governed by Chapter 810 of the Texas Government Code ........................................................................................................................... 22

Financial Section Financial Summary ................................................................................................................................................................................................... 24 Financial Summary – Investment Returns ............................................................................................................................................................... 25 Financial Summary – Key Data ................................................................................................................................................................................. 33 Asset Summary for Statewide and Municipal Public Retirement Systems .............................................................................................................. 38

Actuarial Section Actuarial Summary ................................................................................................................................................................................................... 46 Actuarial Assumptions and Methods for State and Local Retirement Systems ...................................................................................................... 54

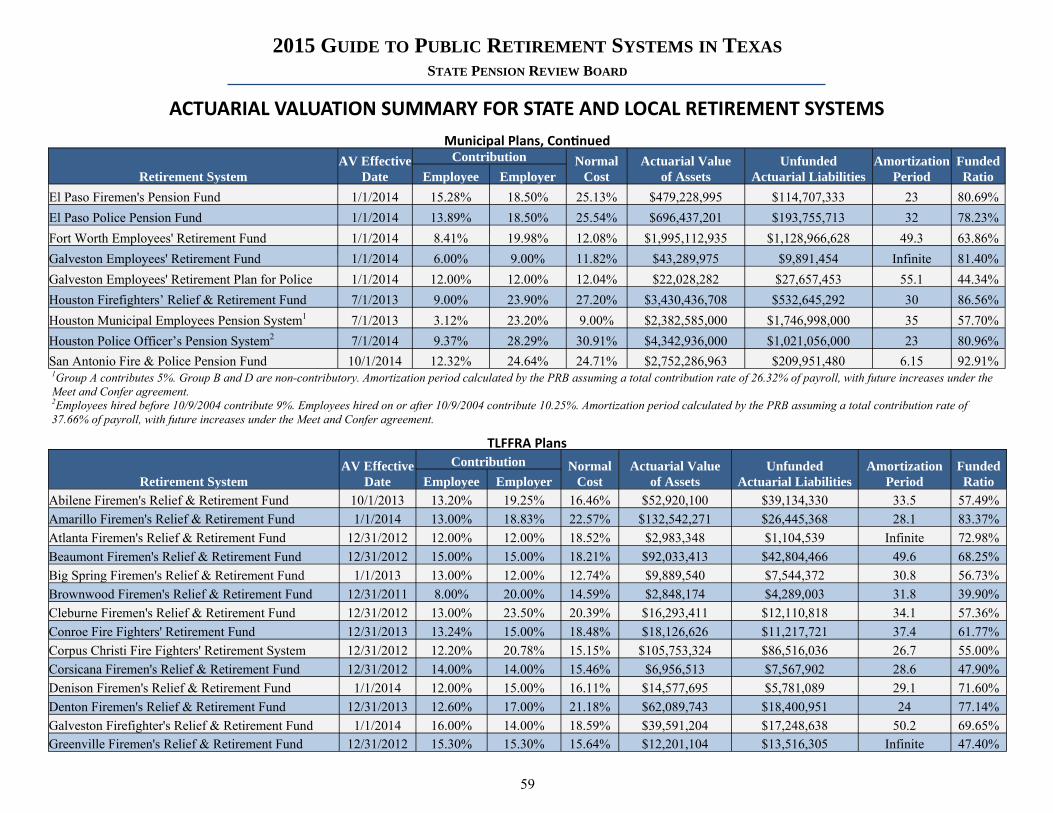

Actuarial Valuation Summary for State and Local Retirement Systems .................................................................................................................. 58

Membership Summary for Actuarially Funded Retirement Systems ...................................................................................................................... 62

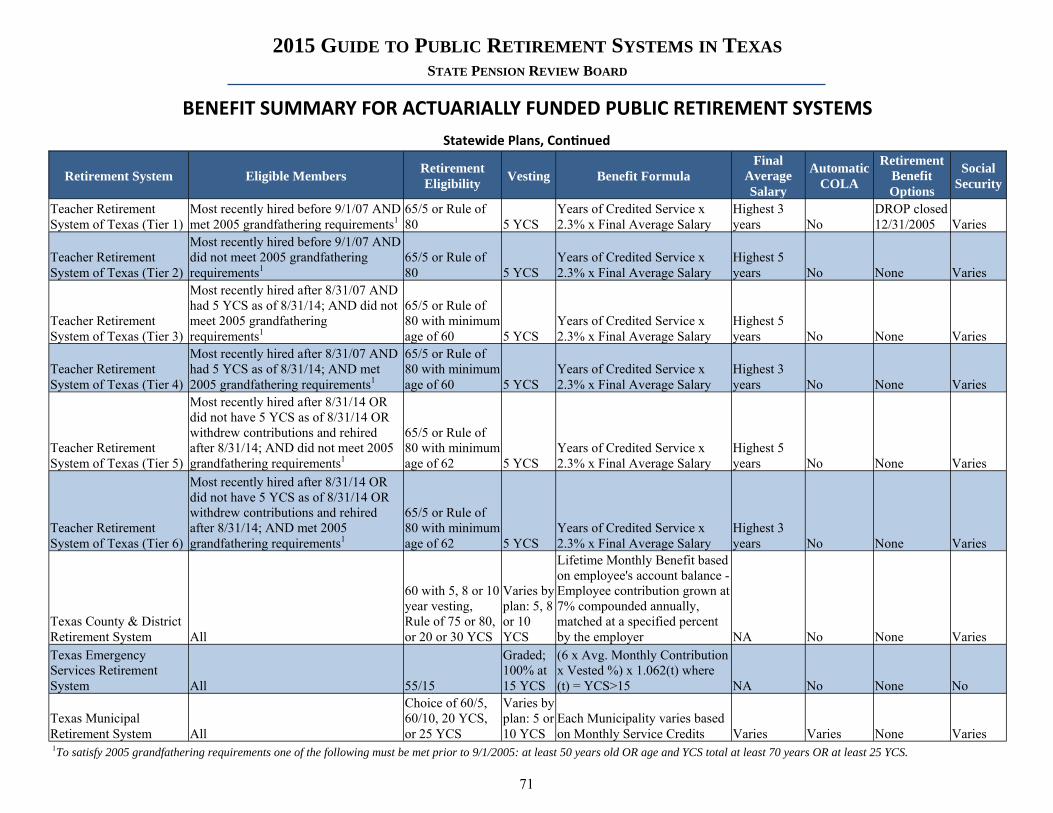

Benefits Section Benefits Summary .................................................................................................................................................................................................... 67 Benefit Summary for Actuarially Funded Public Retirement Systems ..................................................................................................................... 70

Governance Section

Governance Summary .............................................................................................................................................................................................. 88

Vernon’s Texas Revised Civil Statutes and Government Code ................................................................................................................................ 91

Contribution and Benefit Decision‐Making for Texas Public Retirement Systems .................................................................................................. 92

Statewide and Municipal Public Pension Board Composition ............................................................................................................................... 100

Appendices

A. Legislation Relating to Public Retirement Systems Adopted by the 81st, 82nd, and 83rd Legislature ................................................................ 105

B. Defined Contribution Plans – Benefit Summary ................................................................................................................................................ 123

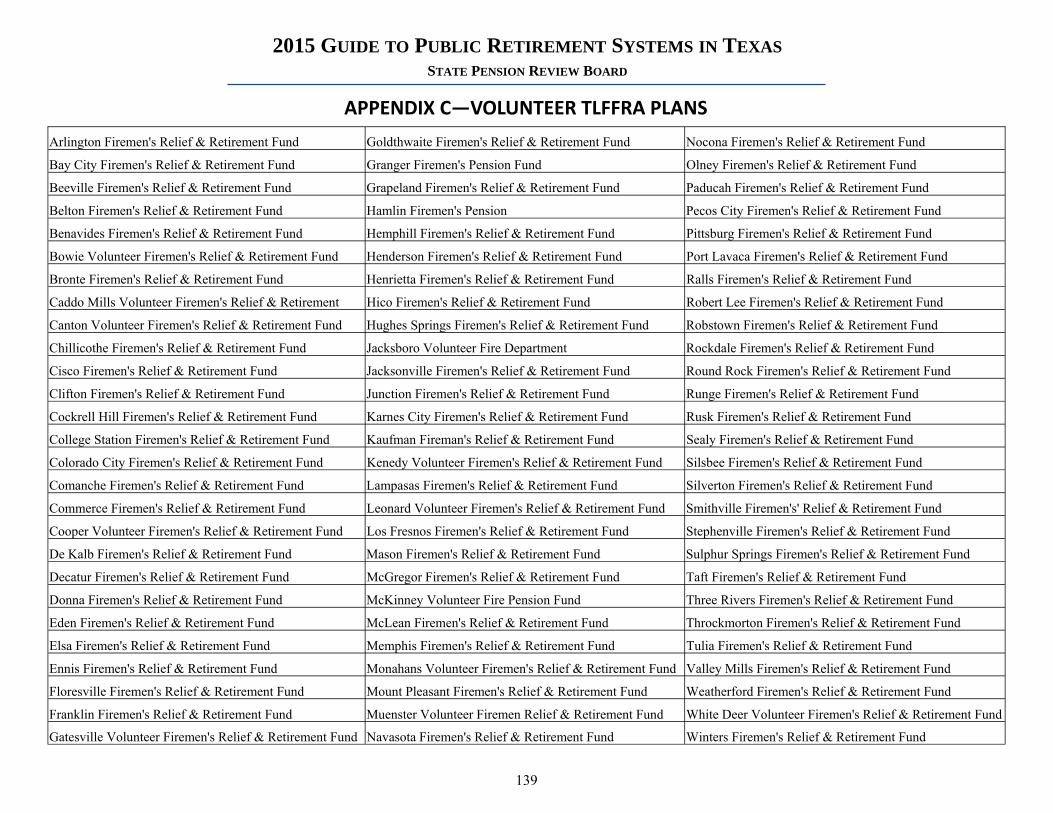

C. Volunteer TLFFRA Plans ..................................................................................................................................................................................... 137

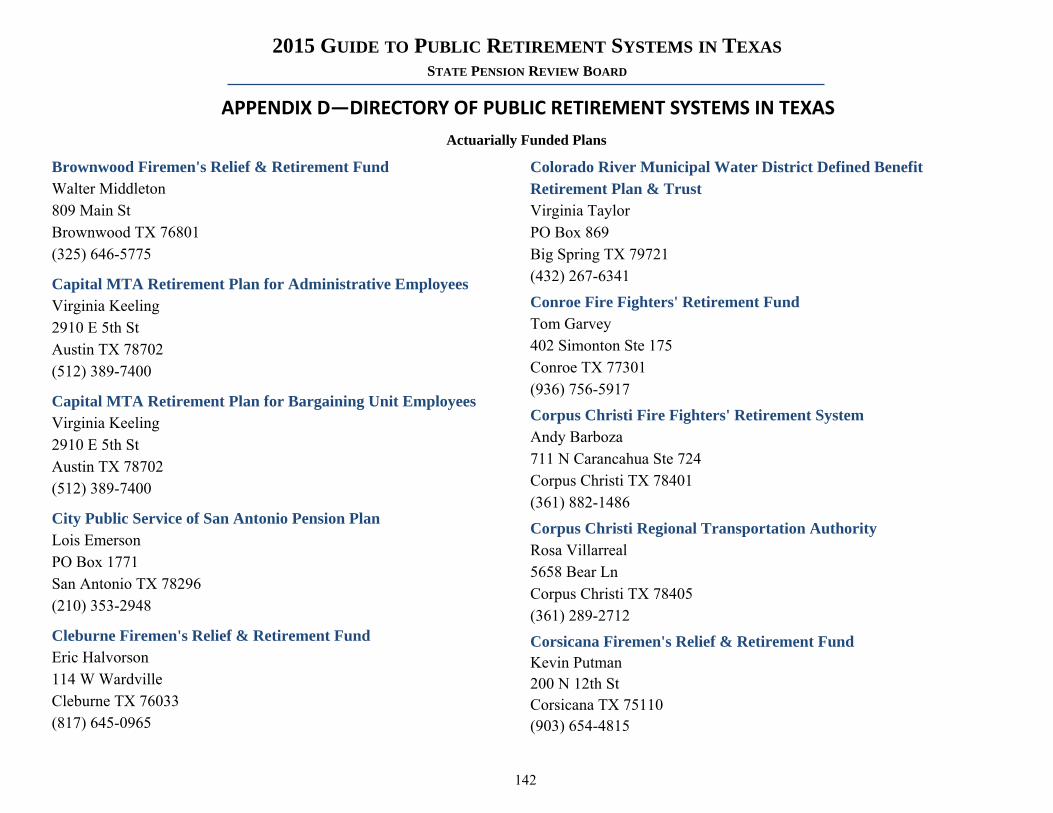

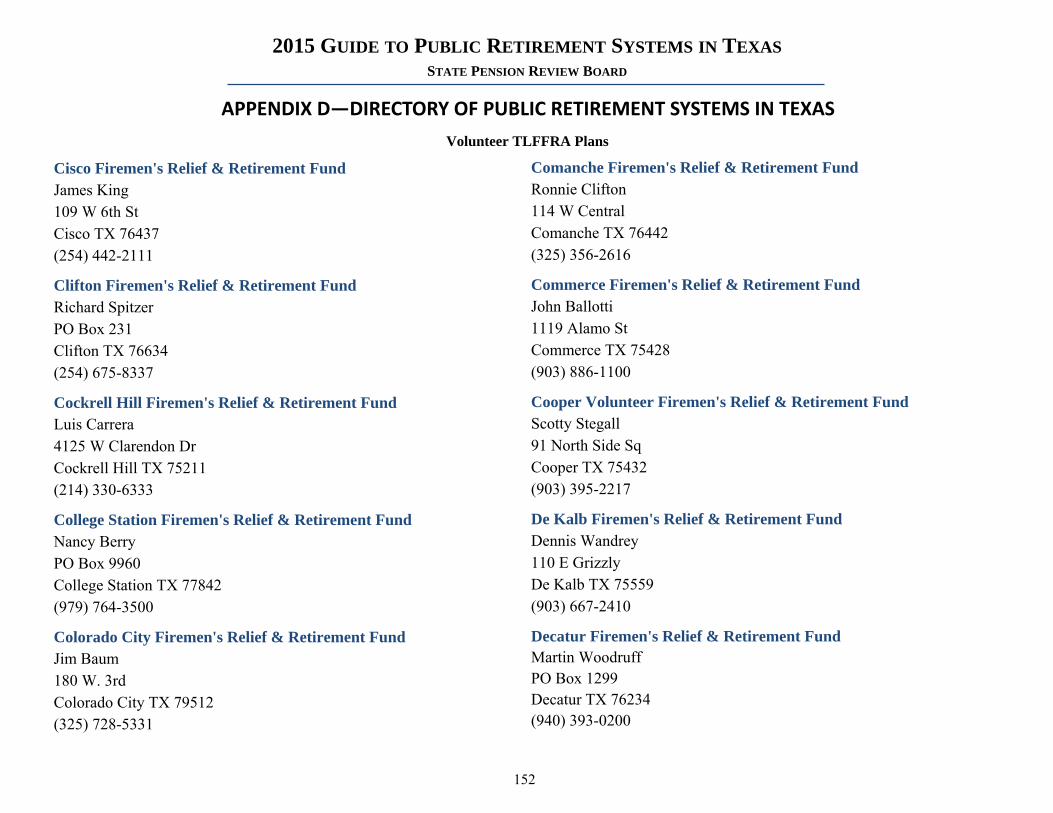

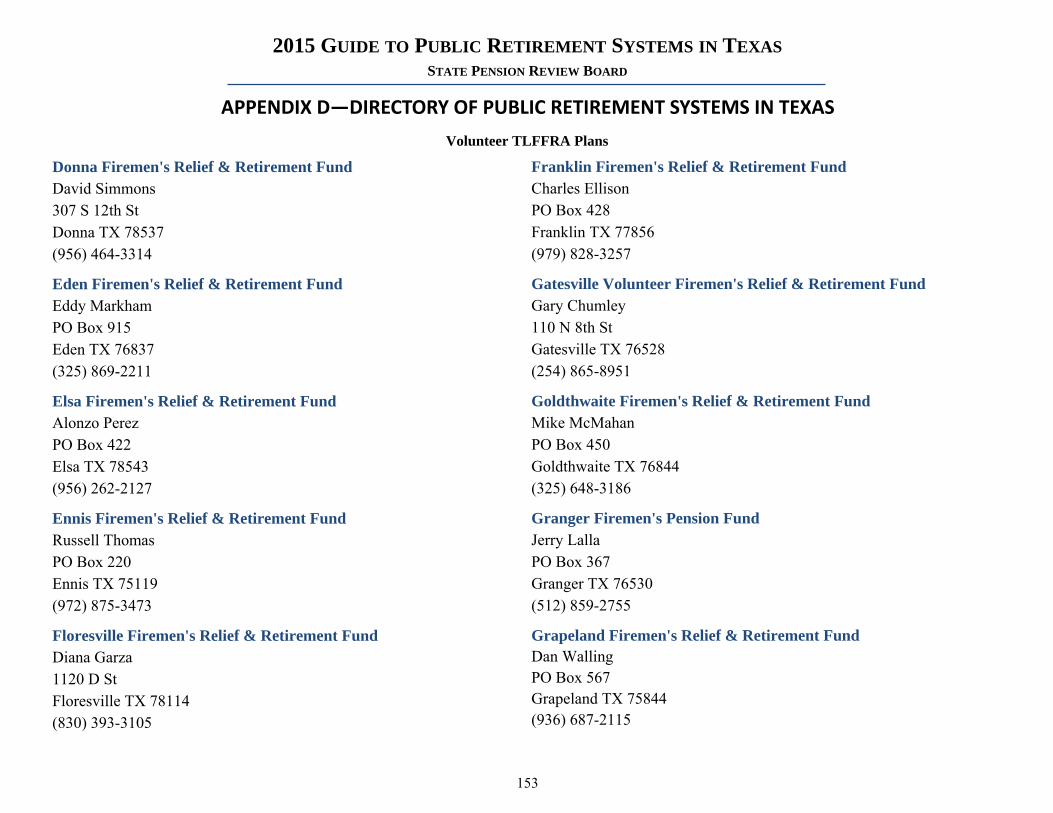

D. Directory of Public Retirement Systems in Texas .............................................................................................................................................. 140

E. Pension Terminology .......................................................................................................................................................................................... 176

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

The State Pension Review Board (PRB) was established in 1979 as the State’s oversight body for Texas public retirement systems at the state and local level. The PRB’s service population consists of the members, trustees, and administrators of 331 public retirement plans; state and local government officials; and the general public.

The PRB monitors the financial and actuarial soundness of 93 actuarially funded defined benefit public retirement systems in Texas, as well as their compliance with state law. As of December 2014, these retirement systems had approximately $238 billion in total net assets and nearly 2.4 million members. The agency also oversees 238 defined contribution and pay-as-you-go volunteer firefighter systems across the state. However, these retirement systems are only required to register with the PRB and submit plan description information.

Board Composition

The Board is composed of seven governor-appointed members, including: three persons who have experience in the fields of securities investment, pension administration, or pension law and are not members or retirees of a public retirement system; one active public retirement system member; one retired member of a public retirement system; one person who has experience in the field of governmental finance; and one member who is an actuary.

Primary Duties

The agency’s general duties as stated in §801.202 of the Texas Government Code are: (1) conduct a continuing review of public retirement systems, compile and compare information about benefits, creditable service, financing, and the administration of systems; (2) conduct intensive studies of potential or existing problems that threaten the actuarial soundness of or inhibit an equitable distribution of benefits in one or more public retirement systems; (3) provide information and technical assistance on pension planning to public retirement systems on request; and (4) recommend policies, practices, and legislation to public retirement systems and appropriate governmental entities. Additionally, the PRB is charged with developing and administering an educational training program for trustees and system administrators of Texas public retirement systems.

Actuarial Impact Statements

During legislative sessions, the agency is required to prepare and provide an actuarial impact statement that analyzes the economic or financial impact of a proposed pension bill on the retirement system affected by the bill. Changes to pension systems often create financial commitments that extend far into the future. By addressing the actuarial impact of certain proposed changes, the PRB provides the Legislature with information that assists in managing pension costs.

When a bill with a potential cost effect on a retirement system is scheduled for committee hearing, the PRB obtains an actuarial analysis of the legislation from the actuary who represents the retirement system targeted by the bill. The analysis is reviewed by the PRB’s staff actuary, providing a “second opinion” on any costs associated with the bill. These two documents— the system’s actuarial analysis and the PRB’s actuarial review— are summarized in an actuarial impact statement prepared by staff and submitted to the Legislative Budget Board (LBB). The LBB publishes the final actuarial impact statement, which is attached to

ABOUT THE STATE PENSION REVIEW BOARD (PRB)

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

ABOUT THE STATE PENSION REVIEW BOARD the bill in committee and stays with the bill throughout the legislative process. If a bill is subsequently amended or substituted so that its actuarial effect is changed, another impact statement is usually prepared.

Financial Health Study of Texas Public Retirement Systems

In December 2014, the PRB published a study examining each Texas public retirement system’s ability to meet its long-term obligations. As required by H.B. 13 (83R), the study contains findings and the Board’s recommendations regarding how a public retirement system may mitigate its risk of not meeting its long-term obligations, as well as responses to the study received from public retirement systems. In conducting the study, the PRB reviewed financial, actuarial, demographic, and benefit information of Texas public retirement systems, including a statistical analysis of historical data to determine which factors have had the greatest impact on systems’ current ability to meet their long-term obligations. The study and a summary of the report can be found on the PRB website at http://www.prb.state.tx.us/.

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

Actuarial assumptions and methodologies are used to determine the proper funding policy for public pension plans. Actuaries include plan participant demographics, benefit obligations, and economic forecast assumptions to calculate the periodic contributions necessary to ensure the long-term financial viability of pension plans; and to estimate the impact that potential plan changes will have on their financial position.

To lend transparency to retirement systems’ actuarial processes and to establish minimum funding standards necessary to meet long-term obligations, the PRB created the Guidelines for Actuarial Soundness in 1984. Since the original adoption of the Guidelines, the PRB has reviewed and updated them as necessary, with the last revisions adopted on September 28th, 2011.

Under the current version of the Guidelines, an actuarially funded defined benefit public retirement system is considered actuarially sound if an actuary determines that it has sufficient money to pay the ongoing normal cost and amortize the unfunded liability over a period of no more than 40 years, preferably 15 to 25 years. This measure of actuarial soundness represents one of the five Guidelines, presented below.

1. The funding of a pension plan should reflect all plan obligations and assets.

2. The allocation of the normal cost portion of the contributions should be level or declining as a percent of payroll over all generation of taxpayers, and should be calculated under applicable actuarial standards.

3. Funding of the unfunded actuarial accrued liability should be level or declining as a percent of payroll over the amortization period.

4. Funding should be adequate to amortize the unfunded actuarial accrued liability over a period not to exceed 40 years, with 15-25 years being a more preferable target. Benefit increases should not be adopted if all plan changes being considered cause a material increase in the amortization period and if the resulting amortization period exceeds 25 years.

5. The choice of assumptions should be reasonable, and should comply with applicable actuarial standards.

PRB GUIDELINES FOR ACTUARIAL SOUNDNESS

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

SUMMARY OF STATUTORILY GOVERNED PUBLIC RETIREMENT SYSTEMS IN TEXAS

1

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

EMPLOYEES RETIREMENT SYSTEM OF TEXAS (ERS)

In November 1946, voters approved an amendment to the Texas Constitution to create a retirement fund for state employees. ERS was officially established by the Legislature in 1947. ERS is responsible for overseeing retirement benefits for elected state officials and state employees. Other programs administered by ERS include the Texas Employees Group Benefits Program (GBP), TexFlex and Texa$aver. In addition, ERS acts as the administrative and investment body for the Law Enforcement and Custodial Officers Supplemental Retirement Fund and the Judicial Retirement System, Plans I and II.

2

Link To: Financial | Actuarial | Benefits | Governance | Bill Summaries

Summary of Current Plan Data

Date of Valuation

Actuarial Accrued Liability

Actuarial Value of Assets

Unfunded Actuarial Accrued Liability Funded Ratio

Amortization Period (years)

Membership Contribution1

Active Annuitant Employee Employer

8/31/2014 $32,924,737,211 $25,431,922,496 $7,492,814,715 77.24% Infinite 134,162 95,840 6.90% 8.00%

Governing Statute Texas Constitution

Article XVI, Section 67 Government Code Title 8, Subtitle B Chapters 811-815

Executive Director Ann S. Bishop

Executive Director Designate

Porter Wilson

PO Box 13207 Austin, Texas 78711

(512) 867-7711

www.ers.state.tx.us

Name

Brian D. Ragland, Chair

Frederick E. Rowe, Jr., Vice Chair

Cydney C. Donnell

Yolanda “Yoly” Griego

I. Craig Hester

Doug Danzeiser

Position

Elected Member

Appointed By Speaker

Appointed by the Governor

Elected Member

Appointed by Chief Justice

Appointed by ERS Board

Term Expires

8/31/2017

8/31/2020

8/31/2018

8/31/2015

8/31/2016

8/31/2019

Employees Retirement System of Texas Board of Trustees

1Employer contribution represents state contribution at 7.50% and state agency contribution of 0.50%. Employee contribution is scheduled to increase to 7.20% for FY 2016 and 7.50% for all subsequent years.

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

JUDICIAL RETIREMENT SYSTEM OF TEXAS PLAN ONE (JRS I)

JRS I is a closed, pay-as-you-go retirement plan for state judges and justices who held office before September 1985. The administration of this plan was transferred to ERS in 1954. No trust fund exists for JRS I, and all benefits are paid by direct appropriation as they become due. To reduce the long-term liabilities associated with a pay-as-you-go retirement system, this plan was replaced by the actuarially funded Judicial Retirement System Plan II in 1985. Revisions in funding, benefits, service credit, and eligibility under JRS I require legislative action. (Government Code, Title 8, Subtitle B, Chapters 831-835)

JRS II is a retirement plan for state judges and justices who took office after August 31, 1985. This plan is also administered by ERS. All revisions in funding, benefits, membership eligibility, and creditable service under JRS II require legislative action.

JUDICIAL RETIREMENT SYSTEM OF TEXAS PLAN TWO (JRS II)

3

Link To: Financial | Actuarial | Benefits | Governance | Bill Summaries

Link To: Financial | Actuarial | Benefits | Governance | Bill Summaries

Summary of Current Plan Data

Date of Valuation

Actuarial Accrued Liability

Actuarial Value of Assets

Unfunded Actuarial Accrued Liability Funded Ratio

Amortization Period (years)

Membership Contribution1

Active Annuitant Employee Employer

8/31/2014 $386,286,372 $348,430,575 $37,855,797 90.20% Infinite 554 267 6.87% 15.66%

Governing Statute Government Code Title 8, Subtitle B Chapters 836-840

Executive Director Ann S. Bishop

Executive Director Designate

Porter Wilson

PO Box 13207 Austin, Texas 78711

(512) 867-7711

www.ers.state.tx.us

Name

Brian D. Ragland, Chair

Frederick E. Rowe, Jr., Vice Chair

Cydney C. Donnell

Yolanda “Yoly” Griego

I. Craig Hester

Doug Danzeiser

Position

Elected Member

Appointed By Speaker

Appointed by the Governor

Elected Member

Appointed by Chief Justice

Appointed by ERS Board

Term Expires

8/31/2017

8/31/2020

8/31/2018

8/31/2015

8/31/2016

8/31/2019

Employees Retirement System of Texas Board of Trustees

1Employee contributions may cease after 20 years or Rule of 70 with 12 years’ service on Appellate Court. The average employee contribution rate is 6.87%. Employee contribution is scheduled to increase to 7.20% for FY 2016 and 7.50% for all subsequent years.

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

LAW ENFORCEMENT AND CUSTODIAL OFFICER SUPPLEMENTAL RETIREMENT FUND (LECOSRF)

LECOSRF was created by the Texas Legislature in 1979. It is a supplemental plan to ERS, and is administered by ERS. Membership is limited to law enforcement officers who have been commissioned by the Department of Public Safety, Texas Alcoholic Beverage Commission, Parks and Wildlife Department, and those members whose commissions are recognized by the Commission on Law Enforcement Officer Standards and Education. Membership is also provided to custodial officers employed by the Texas Department of Criminal Justice, and certified by the department as having direct contact with inmates. The supplemental benefits are available to any employee who completes 20 years of service in an eligible position.

4

Summary of Current Plan Data

Date of Valuation

Actuarial Accrued Liability

Actuarial Value of Assets

Unfunded Actuarial Accrued Liability Funded Ratio

Amortization Period (years)

Membership Contribution

Active Annuitant Employee Employer1

8/31/2014 $1,206,769,921 $883,594,932 $323,174,989 73.22% Infinite 37,084 10,024 0.50% 1.70%

Link To: Financial | Actuarial | Benefits | Governance | Bill Summaries

Governing Statute Government Code Title 8, Subtitle B Chapters 811-815

Executive Director Ann S. Bishop

Executive Director Designate

Porter Wilson

PO Box 13207 Austin, Texas 78711

(512) 867-7711

www.ers.state.tx.us

Name

Brian D. Ragland, Chair

Frederick E. Rowe, Jr., Vice Chair

Cydney C. Donnell

Yolanda “Yoly” Griego

I. Craig Hester

Doug Danzeiser

Position

Elected Member

Appointed By Speaker

Appointed by the Governor

Elected Member

Appointed by Chief Justice

Appointed by ERS Board

Term Expires

8/31/2017

8/31/2020

8/31/2018

8/31/2015

8/31/2016

8/31/2019

Employees Retirement System of Texas Board of Trustees

1Employer contribution represents state contribution at 0.50% and court fee contributions equivalent to 1.20%. Rates are in addition to rates paid for ERS.

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

In November 1936, voters approved an amendment to the Texas Constitution to create a statewide teacher retirement system. TRS was officially established by the Legislature in 1937. TRS is the largest public retirement system in Texas, in both membership and assets. The system provides benefits to public school teachers, other public school employees, and higher education personnel who are not eligible for the Optional Retirement Program (ORP), or who choose not to belong to ORP. Revisions regarding benefits, contributions, and post-retirement adjustments require legislative action.

TEACHER RETIREMENT SYSTEM OF TEXAS (TRS) Link To: Financial | Actuarial | Benefits | Governance | Bill Summaries

5

Summary of Current Plan Data

Date of Valuation

Actuarial Accrued Liability

Actuarial Value of Assets

Unfunded Actuarial Accrued Liability Funded Ratio

Amortization Period (years)

Membership Contribution1

Active Annuitant Employee Employer

8/31/2014 $160,035,600,826 $128,397,777,855 $31,637,822,971 80.23% 29.8 873,214 363,182 6.70% 6.80%

Name

R. David Kelley, Chair

Nanette Sissney, Vice Chair

Todd Barth

T. Karen Charleston

Joe Colonnetta

David Corpus

Christopher Moss

Anita Palmer

Dolores Ramirez

Position

Appointed by the Governor

Active Public Education Position

Appointed by the Governor

Higher Education Position

Appointed by the Governor

Nominated by the State Board of Education

Nominated by the State Board of Education

Retiree

Active Public Education Position

Term Expires

8/31/2017

8/31/2015

8/31/2015

8/31/2017

8/31/2019

8/31/2019

8/31/2015

8/31/2017

8/31/2019

Governing Statutes Texas Constitution

Article XVI, Section 67 Government Code Title 8, Subtitle C Chapters 821-825

Executive Director Brian K. Guthrie

1000 Red River Street Austin, Texas 78701

(512) 542-6400

www.trs.state.tx.us

Teacher Retirement System of Texas Board of Trustees

1In FY 2015, school districts not participating in Social Security began contributing 1.50% of payroll. In combination with 6.80% from the state, estimated employer rate is expected to be 7.76% of payroll. Employee contribution is scheduled to increase to 7.20% for FY 2016 and 7.70% for all subsequent years.

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

ORP is a 403(b) defined contribution plan that was created in 1967 as an alternative to TRS for full-time faculty, librarians, and certain administrators and professionals employed by Texas public institutions of higher education. ORP is administered by the Texas Higher Education Coordinating Board (THECB). Because their careers normally involve interstate mobility, it was determined that a more portable retirement option would substantially improve higher education institutions’ ability to compete for quality employees at the national level. Certain employees of the Texas Higher Education Coordinating Board and the Commissioner of Education are eligible to elect ORP in lieu of the Employees Retirement System. Eligible employees have up to 90 days to make a one-time irrevocable election of ORP. Each institution administers the plan for its employees, including authorization of companies to offer ORP accounts. Participants select a company and direct the allocation of their own investments. Benefits are a result of the amounts contributed and any net return on the investments selected by each participant. Contribution rates are set by the Legislature biennially. Institutions may supplement the state’s base rate up to a total employer contribution rate of 8.5%.

OPTIONAL RETIREMENT PROGRAM (ORP)

6

Governing Statute Government Code Title 8, Subtitle C

Chapter 830

Statewide Coordinator Toni Alexander

Texas Higher Education Coordinating Board

PO Box 12788 Austin, TX 78711 (512) 427-6101

www.thecb.state.tx.us/orp

Name

Harold W. Hahn, Chair

Robert “Bobby” Jenkins, Jr., Vice Chair

David D. Teuscher, M.D., Secretary

Dora G. Alcalá

Ambassador Sada Cumber

Christopher M. Huckabee

Jacob M. Monty

Janelle Shepard

John T. Steen, Jr.

Term Expires

9/31/2019

9/31/2017

9/31/2017

9/31/2015

9/31/2015

9/31/2019

9/31/2015

9/31/2017

9/31/2019

Texas Higher Education Coordinating Board

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

TEXAS COUNTY & DISTRICT RETIREMENT SYSTEM (TCDRS)

TCDRS was established in 1967 and provides retirement, disability and survivor benefits to 656 Texas counties and districts, including water, hospital, appraisal and emergency service districts. Although created by the Texas Legislature, TCDRS does not receive funding from the State of Texas. Each plan is funded independently by the county or district, its employees and investment earnings. Plan sponsors (participating counties and districts) are required to pay 100% of their required contribution every year. TCDRS is a savings-based plan where the benefit is based on how much a member has saved over the course of their career and employer matching at retirement.

7

Link To: Financial | Actuarial | Benefits | Governance | Bill Summaries

Summary of Current Plan Data

Date of Valuation

Actuarial Accrued Liability

Actuarial Value of Assets

Unfunded Actuarial Accrued Liability Funded Ratio

Amortization Period (years)

Membership Contribution1

Active Annuitant Employee Employer

12/31/2013 $24,514,806,684 $21,912,711,318 $2,602,095,366 89.39% 10.8 124,525 49,820 6.95% 12.20%

Governing Statute Government Code Title 8, Subtitle F Chapters 841-845

Executive Director Amy Bishop PO Box 2034

Austin, Texas 78768 (512) 328-8889

www.tcdrs.org

Name

Robert A. Eckels, Chair

H.C. “Chuck” Cazalas, Vice Chair

Jerry Bigham

Mary Louise Garcia

Deborah Hunt

Jan Kennady

Bridget McDowell

Kristeen Roe

Bob Willis

County

Harris

Nueces

Randall

Tarrant

Williamson

Comal

Taylor

Brazos

Polk

Term Expires

12/31/2019

12/31/2017

12/31/2015

12/31/2017

12/31/2015

12/31/2015

12/31/2019

12/31/2017

12/31/2019

Texas County & District Retirement System Board of Trustees

1The members' contribution rate is set by plan sponsor with a weighted average calculated by the PRB. Employer contribution also reflects weighted average.

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

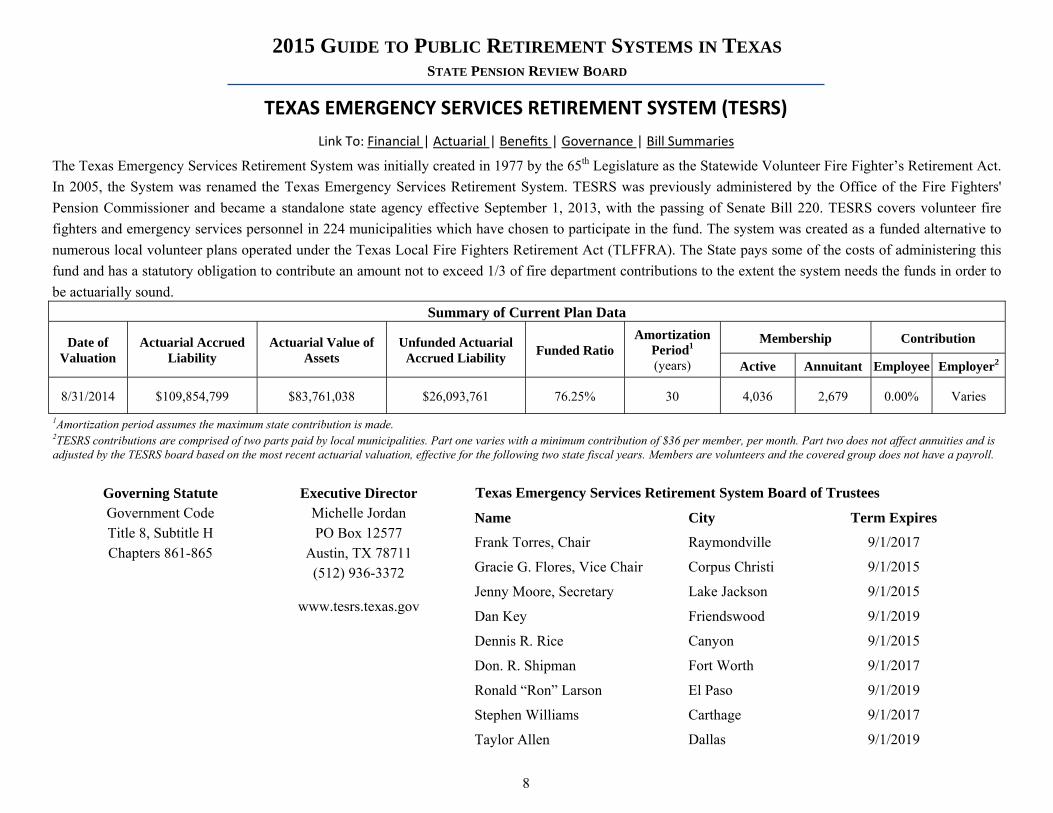

The Texas Emergency Services Retirement System was initially created in 1977 by the 65th Legislature as the Statewide Volunteer Fire Fighter’s Retirement Act. In 2005, the System was renamed the Texas Emergency Services Retirement System. TESRS was previously administered by the Office of the Fire Fighters' Pension Commissioner and became a standalone state agency effective September 1, 2013, with the passing of Senate Bill 220. TESRS covers volunteer fire fighters and emergency services personnel in 224 municipalities which have chosen to participate in the fund. The system was created as a funded alternative to numerous local volunteer plans operated under the Texas Local Fire Fighters Retirement Act (TLFFRA). The State pays some of the costs of administering this fund and has a statutory obligation to contribute an amount not to exceed 1/3 of fire department contributions to the extent the system needs the funds in order to be actuarially sound.

TEXAS EMERGENCY SERVICES RETIREMENT SYSTEM (TESRS)

8

Link To: Financial | Actuarial | Benefits | Governance | Bill Summaries

Summary of Current Plan Data

Date of Valuation

Actuarial Accrued Liability

Actuarial Value of Assets

Unfunded Actuarial Accrued Liability Funded Ratio

Amortization Period1 (years)

Membership Contribution

Active Annuitant Employee Employer2

8/31/2014 $109,854,799 $83,761,038 $26,093,761 76.25% 30 4,036 2,679 0.00% Varies

Governing Statute Government Code Title 8, Subtitle H Chapters 861-865

Executive Director Michelle Jordan PO Box 12577

Austin, TX 78711 (512) 936-3372

www.tesrs.texas.gov

Name

Frank Torres, Chair

Gracie G. Flores, Vice Chair

Jenny Moore, Secretary

Dan Key

Dennis R. Rice

Don. R. Shipman

Ronald “Ron” Larson

Stephen Williams

Taylor Allen

City

Raymondville

Corpus Christi

Lake Jackson

Friendswood

Canyon

Fort Worth

El Paso

Carthage

Dallas

Term Expires

9/1/2017

9/1/2015

9/1/2015

9/1/2019

9/1/2015

9/1/2017

9/1/2019

9/1/2017

9/1/2019

Texas Emergency Services Retirement System Board of Trustees

1Amortization period assumes the maximum state contribution is made. 2TESRS contributions are comprised of two parts paid by local municipalities. Part one varies with a minimum contribution of $36 per member, per month. Part two does not affect annuities and is adjusted by the TESRS board based on the most recent actuarial valuation, effective for the following two state fiscal years. Members are volunteers and the covered group does not have a payroll.

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

TEXAS MUNICIPAL RETIREMENT SYSTEM (TMRS)

The Texas Municipal Retirement System was established in 1947 and is an agent multiple-employer retirement system which provides retirement, disability and survivor benefits for employees of 844 municipalities in the State. Although created by the Texas Legislature, TMRS does not receive funding from the State of Texas. Municipalities that participate in TMRS have their own retirement plans within the general framework of the TMRS Act. Plan provisions may vary from city to city depending upon the options selected by each individual municipality. Revisions to available options require legislative action. Each plan in TMRS is funded independently by the municipalities, its employees and investment earnings.

9

Link To: Financial | Actuarial | Benefits | Governance | Bill Summaries

Summary of Current Plan Data

Date of Valuation

Actuarial Accrued Liability

Actuarial Value of Assets

Unfunded Actuarial Accrued Liability Funded Ratio

Amortization Period1 (years)

Membership Contribution2

Active Annuitant Employee Employer

12/31/2013 $25,320,767,136 $21,293,624,657 $4,027,142,479 84.10% 21.9 102,870 49,969 6.61% 13.25%

Governing Statute Government Code Title 8, Subtitle G Chapters 851-855

Executive Director David Gavia

PO Box 149153 Austin, Texas 78714

(512) 476-7577

www.tmrs.org

Name

Julie Oakley, Chair

Jim Parrish, Vice Chair

Roel “Roy” Rodriguez

James “Jim” Paul Jeffers

David Landis

Bill Philibert

City

Lakeway

Plano

McAllen

Nacogdoches

Perryton

Deer Park

Term Expires

2/1/2019

2/1/2017

2/1/2017

2/1/2015

2/1/2015

2/1/2019

Texas Municipal Retirement System Board of Trustees

1The amortization period is a weighted average of the member cities' amortization periods. 2The members' contribution rate is set by plan sponsor with a weighted average calculated by the PRB. Employer contribution also reflects weighted average.

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

CITY OF AUSTIN EMPLOYEES’ RETIREMENT SYSTEM (COAERS)

The City of Austin Employees' Retirement System was initially established in 1941 by city ordinance. In 1991, the 72nd Legislature enacted Article 6243n, Vernon’s Texas Civil Statutes, establishing the system in statute. COAERS is a single employer contributory defined benefit pension plan providing retirement, disability, and death benefit programs for regular full-time employees of the City of Austin working 30 or more hours per week and their beneficiaries. COAERS does not provide benefits for the mayor, members of the City Council, or commissioned civil service police officers and firefighters.

10

Link To: Financial | Actuarial | Benefits | Governance | Bill Summaries

Summary of Current Plan Data

Date of Valuation

Actuarial Accrued Liability

Actuarial Value of Assets

Unfunded Actuarial Accrued Liability Funded Ratio

Amortization Period (years)

Membership Contribution

Active Annuitant Employee Employer

12/31/2013 $2,909,917,750 $2,047,929,504 $861,988,246 70.38% 26 8,592 5,120 8.00% 18.00%

Governing Statute Vernon’s Texas Civil Statutes

Article 6243n

Executive Director Christopher Hanson

418 E Highland Mall Blvd Austin, TX 78752

(512) 458-2551

www.coaers.org

Name

Sam Jones, Chair

Jim Williams, Vice Chair

Leslie Pool

Ed Van Eenoo

Elizabeth S. Gonzales

Russ Sartain

Reagan David

Francine Gertz

Julia Robbins

Chris Noak

Anthony B. Ross, Sr.

Position

Retiree Elected Member

Active Elected Member

City Council Member

City Manager Designee

Council Appointed Citizen

Council Appointed Citizen

Board Appointed Citizen

Active Elected

Active Elected

Active Elected

Retiree Elected

Term Expires

12/31/2016

12/31/2017

N/A

N/A

12/31/2016

12/31/2017

12/31/2017

12/31/2015

12/31/2015

12/31/2017

12/31/2018

City of Austin Employees’ Retirement System Board of Trustees

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

AUSTIN FIRE FIGHTERS RELIEF & RETIREMENT FUND

The Austin Fire Fighters Relief and Retirement Fund was initially created in 1937 by an Act of the 45th Legislature under the Texas Local Fire Fighters Retirement Act (Article 6243e, Vernon’s Texas Civil Statutes). In 1975, the 64th Legislature enacted Article 6243e-1, establishing the Fund independently in statute. The Fund is a single employer contributory defined benefit pension plan that provides retirement, disability, death and survivor benefits to firefighters employed by the City of Austin and their beneficiaries.

11

Link To: Financial | Actuarial | Benefits | Governance | Bill Summaries

Summary of Current Plan Data

Date of Valuation

Actuarial Accrued Liability

Actuarial Value of Assets

Unfunded Actuarial Accrued Liability Funded Ratio

Amortization Period (years)

Membership Contribution

Active Annuitant Employee1 Employer

12/31/2013 $808,771,153 $742,073,494 $66,697,659 91.75% 10.51 1,074 627 17.70% 22.05%

Governing Statute Vernon’s Texas Civil Statutes

Article 6243e.1

Administrator William E. Stefka

4101 Parkstone Heights Dr Suite 270

Austin, TX 78746 (512) 454-9567

www.afrs.org

Name

Stephen Adler, Chair

Keith Johnson, Vice Chair

Art Alfaro, Treasurer

Jeremy Burke

James R. Fedro

Position

Mayor

Fund Member

City Treasurer

Fund Member

Fund Member

Term Expires

N/A

12/31/2017

N/A

12/31/2016

12/31/2015

Austin Fire Fighters Relief & Retirement Fund Board of Trustees

1Employee contribution increased from 17.2% to 17.7% on 10/1/2014 and is scheduled to increase to 18.20% on 10/1/2015 and 18.70% on 10/1/2016 for all subsequent fiscal years.

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

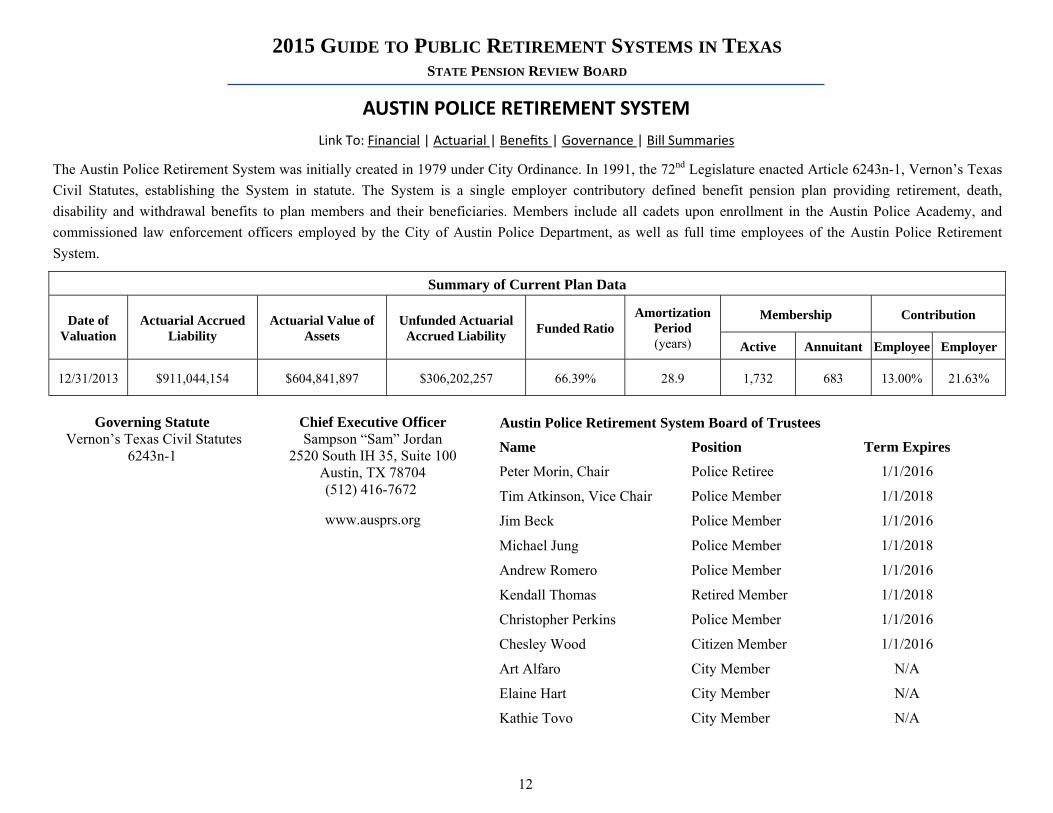

AUSTIN POLICE RETIREMENT SYSTEM

The Austin Police Retirement System was initially created in 1979 under City Ordinance. In 1991, the 72nd Legislature enacted Article 6243n-1, Vernon’s Texas Civil Statutes, establishing the System in statute. The System is a single employer contributory defined benefit pension plan providing retirement, death, disability and withdrawal benefits to plan members and their beneficiaries. Members include all cadets upon enrollment in the Austin Police Academy, and commissioned law enforcement officers employed by the City of Austin Police Department, as well as full time employees of the Austin Police Retirement System.

12

Link To: Financial | Actuarial | Benefits | Governance | Bill Summaries

Summary of Current Plan Data

Date of Valuation

Actuarial Accrued Liability

Actuarial Value of Assets

Unfunded Actuarial Accrued Liability Funded Ratio

Amortization Period (years)

Membership Contribution

Active Annuitant Employee Employer

12/31/2013 $911,044,154 $604,841,897 $306,202,257 66.39% 28.9 1,732 683 13.00% 21.63%

Governing Statute Vernon’s Texas Civil Statutes

6243n-1

Chief Executive Officer Sampson “Sam” Jordan

2520 South IH 35, Suite 100 Austin, TX 78704 (512) 416-7672

www.ausprs.org

Name

Peter Morin, Chair

Tim Atkinson, Vice Chair

Jim Beck

Michael Jung

Andrew Romero

Kendall Thomas

Christopher Perkins

Chesley Wood

Art Alfaro

Elaine Hart

Kathie Tovo

Position

Police Retiree

Police Member

Police Member

Police Member

Police Member

Retired Member

Police Member

Citizen Member

City Member

City Member

City Member

Term Expires

1/1/2016

1/1/2018

1/1/2016

1/1/2018

1/1/2016

1/1/2018

1/1/2016

1/1/2016

N/A

N/A

N/A

Austin Police Retirement System Board of Trustees

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

DALLAS POLICE & FIRE PENSION SYSTEM

The Dallas Police & Fire Pension System was initially created in 1916 under city ordinance. In 1933, the 43rd Legislature enacted 6243a, Vernon’s Texas Civil Statutes, establishing the System in statute. The System was restated and continued in 1989 by an Act of the 71st Legislature under Article 6243a-1. The System is a single employer contributory defined benefit plan providing retirement, survivor, and disability benefits to the uniformed public safety employees of the City of Dallas and their beneficiaries.

13

Link To: Financial | Actuarial | Benefits | Governance | Bill Summaries

Summary of Current Plan Data

Date of Valuation

Actuarial Accrued Liability

Actuarial Value of Assets

Unfunded Actuarial Accrued Liability Funded Ratio

Amortization Period (years)

Membership Contribution

Active Annuitant Employee Employer

1/1/2014 $5,129,195,887 $3,877,321,261 $1,251,874,626 75.59% 26 5,397 3,890 8.50% 27.50%

Governing Statute Vernon’s Texas Civil Statutes

Article 6243a-1

Interim Administrator Donald C. Rohan

4100 Harry Hines Blvd Suite 100

Dallas, TX 75219 (214) 638-3863

www.dpfp.org

Name George J. Tomasovic, Chair Dan Wojcik, Vice Chair Rick Salinas, Deputy Vice Chair Tennell Atkins Gerald “Jerry” Brown Samuel L. Friar Scott Griggs Ken Haben Philip T. Kingston Lee Kleinman John M. Mays Joe Schutz

Position Active Fire-Rescue Active Police Active Fire-Rescue City Council Retired Fire-Rescue Active Fire-Rescue City Council Active Police City Council City Council Retired Police Active Police

Term Expires

5/31/2015 5/31/2015 5/31/2015 6/22/2015 5/31/2017 5/31/2017 6/22/2015 5/31/2017 6/22/2015 6/22/2015 5/31/2017 5/31/2015

Dallas Police & Fire Pension System Board of Trustees

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

EL PASO FIREMEN & POLICEMEN’S PENSION FUND

The El Paso Firemen & Policemen’s Pension Fund was initially created in 1920. In 1933, the 43rd Legislature enacted Article 6243b, Vernon’s Texas Civil Statutes, establishing the Fund in statute. The Fund is a single employer contributory defined benefit plan, providing retirement, disability and death benefits to uniformed public safety employees of the City of El Paso and their beneficiaries. The Fund is comprised of two divisions, a Policemen’s Fund and a Firemen’s Fund, both managed by a common Board of Trustees and administrative staff.

14

Summary of Current Plan Data Firemen

Date of Valuation

Actuarial Accrued Liability

Actuarial Value of Assets

Unfunded Actuarial Accrued Liability Funded Ratio Amortization

Period (years) Membership Contribution

Active Annuitant Employee Employer

1/1/2014 $593,936,328 $479,228,995 $114,707,333 80.69% 23 871 644 15.28% 18.50%

Policemen

1/1/2014 $890,192,914 $696,437,201 $193,755,713 78.23% 32 1,052 853 13.89% 18.50%

Link To: Financial | Actuarial | Benefits | Governance | Bill Summaries

Governing Statute Vernon’s Texas Civil Statutes

Article 6243b

Executive Director Robert J. Stanton

Chase Tower 201 E Main, Suite 1616

El Paso, TX 79901 (915) 771-8111

www.elpasofireandpolice.org

Name Tyler Grossman, Chair Jerry Villanueva, Vice Chair Jeffrey Cotham Ricci J. Carson John C. Schneider Paul Thompson Robert D. Tollen, Ph.D. Carmen Arrieta-Candelaria Terri Garcia Presi Ortega Judy Balmer

Position Active Police Active Fire Active Police Active Fire Active Police Active Fire Mayoral Appointee Mayoral Appointee City Manager Appointee Mayoral Appointee City Manager Appointee

Term Expires

7/2017 7/2017 7/2015 7/2015 7/2018 7/2017 7/2015 7/2017 9/2015 9/2015 9/2017

El Paso Firemen & Policemen’s Pension Fund Board of Trustees

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

FORT WORTH EMPLOYEES’ RETIREMENT FUND

The Fort Worth Employees' Retirement Fund was initially created in 1945 by city ordinance. In 2007, the 80th Legislature enacted Article 6243i, Vernon’s Civil Statues, establishing the Fund independently in statute. The Fort Worth Employees’ Retirement Fund is a multi-employer cost sharing defined benefit pension plan covering all regular employees, police officers and firefighters employed full time by the City of Fort Worth (“City Plan”), as well as all employees of the Fort Worth Employees’ Retirement Plan (“Staff Plan”). The two plans are commingled for investment purposes and are both administered by the Retirement Fund’s Board of Directors; each plan has its own separate actuarial valuation completed each year and its own funded status.

15

Link To: Financial | Actuarial | Benefits | Governance | Bill Summaries

Summary of Current Plan Data

Date of Valuation

Actuarial Accrued Liability

Actuarial Value of Assets

Unfunded Actuarial Accrued Liability Funded Ratio

Amortization Period (years)

Membership Contribution

Active Annuitant Employee Employer

1/1/2014 $3,124,079,563 $1,995,112,935 $1,128,966,628 63.86% 49.3 6,199 3,820 8.41% 19.98%

Governing Statute Vernon’s Texas Civil Statutes

Article 6243i

Executive Director/Chief Investment Officer

Joelle Mevi 3801 Hulen St, Suite 101

Fort Worth, TX 76107 (817) 632-8900

www.fwretirement.org

Name Billy Samuel, Chair Benita Harper, Vice Chair Matt Anderson Todd Cox Betty J. Tanner Lance Usrey Marsha Anderson Jesús Payán Jarod D. Cox Jason Brown Bill Crawford Cindy Brewington Aaron Bovos

Position Retired Police Active General Employee Active Police Active Fire Active General Employee Retired Fire Retired General Employee Council Appointee Council Appointee Council Appointee Council Appointee Council Appointee Chief Financial Officer

Term Expires

8/31/2016 8/31/2015 8/31/2015 8/31/2016 8/31/2016 8/31/2015 8/31/2015 8/31/2016 8/31/2015 8/31/2016 8/31/2015 8/31/2016

N/A

Fort Worth Employees’ Retirement Fund Board of Trustees

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

GALVESTON EMPLOYEES’ RETIREMENT PLAN FOR POLICE

The Galveston Employees’ Retirement Plan for Police was initially created in 1980 by city ordinance. In 1997, the 75th Legislature enacted Article 6243p, Vernon’s Texas Civil Statutes, establishing the Plan independently in statute. City code provisions pertaining to the Plan were replaced with the language from Article 6243p in 1998. The Plan is a single-employer contributory defined benefit pension plan covering police officers employed full time by the City of Galveston that provides retirement, disability and death benefits to eligible members and their beneficiaries. Participation is mandatory for eligible employees hired on or after December 1, 1980; eligible employees hired prior to this date were given a onetime option of electing to participate as of December 1, 1980.

16

Link To: Financial | Actuarial | Benefits | Governance | Bill Summaries

Summary of Current Plan Data

Date of Valuation

Actuarial Accrued Liability

Actuarial Value of Assets

Unfunded Actuarial Accrued Liability Funded Ratio

Amortization Period (years)

Membership Contribution

Active Annuitant Employee Employer

1/1/2014 $49,685,735 $22,028,282 $27,657,453 44.34% 55.1 141 131 12.00% 12.00%

Governing Statute Vernon’s Texas Civil

Statutes Article 6243p

Administrator Jacque Vasquez 4415 Avenue S

Galveston, TX 77571 (409) 765-5274

Name Andre Mitchell Blake Patton John Kelso Larry Chambers Matthew Whiting Vandy Anderson Mike Loftin

Position Police Officer Police Officer Council Appointment Police Officer Police Officer Mayor Appointment Mike Loftin

Term Expires

12/31/2017 12/31/2015 12/31/2015 12/31/2017 12/31/2016 12/31/2015

N/A

Galveston Employees’ Retirement Plan for Police Board of Trustees

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

HOUSTON FIREFIGHTERS’ RELIEF & RETIREMENT FUND

The Houston Firefighters’ Relief and Retirement Fund was initially created in 1937 under the authority of the Texas Local Fire Fighters Retirement Act. In 1975, the 64th Legislature enacted Article 6243e.2, Vernon’s Texas Civil Statutes, establishing the Fund independently in statute. The Fund was recodified by the 75th Legislature in 1997 under Article 6243e.2(1), Vernon’s Texas Civil Statutes. The Fund is a single-employer contributory defined benefit pension plan covering firefighters employed by the City of Houston that provides retirement, disability and death benefits to eligible members and their beneficiaries. Prior to 1988, the City of Houston provided the staff and financing for the daily administration of the Fund; effective July 1, 1988, the Board of Trustees assumed full responsibility for Fund administration.

17

Link To: Financial | Actuarial | Benefits | Governance | Bill Summaries

Summary of Current Plan Data

Date of Valuation

Actuarial Accrued Liability

Actuarial Value of Assets

Unfunded Actuarial Accrued Liability Funded Ratio

Amortization Period (years)

Membership Contribution

Active Annuitant Employee Employer

7/1/2013 $3,963,082,000 $3,430,436,708 $532,645,292 86.56% 30 3,835 2,997 9.00% 23.90%

Governing Statute Vernon’s Texas Civil Statutes

Article 6243e.2(1)

Executive Director Ralph Marsh

4225 Interwood N Pkwy Houston, TX 77032

(281) 372-5100

www.hfrrf.org

Name Todd E. Clark, Chair Gary M. Vincent, Vice Chair Francis “Frank” Maher, Secretary Fred S. Robertson Craig T. Mason The Honorable Carroll G. Robinson Albertino “Al” Mays Stephen Ray Whitehead Gary W. Blackmon, Sr. David L. Keller, Jr.

Position Firefighter Firefighter Retired Firefighter Mayor’s Representative City Treasurer’s Designee Citizen Member Citizen Member Firefighter Firefighter Firefighter

Term Expires 12/31/2015 12/31/2016 12/31/2015

N/A N/A

12/31/2015 12/31/2016 12/31/2017 12/31/2017 12/31/2016

Houston Firefighters’ Relief & Retirement Fund Board of Trustees

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

HOUSTON MUNICIPAL EMPLOYEES PENSION SYSTEM (HMEPS)

The Houston Municipal Employees Pension System was created in 1943 by an act of the 48th Legislature, and codified under Article 6243g, Vernon's Texas Civil Statutes. The System was recodified by the 77th Texas Legislature in 2001 under Article 6243h, Vernon's Texas Civil Statutes. The System is a multiple-employer defined benefit pension plan and includes a contributory group (Group A) and two noncontributory groups (Group B and D). The System provides service retirement, disability retirement and death benefits for all full-time municipal employees, except police officers and fire fighters (other than certain police officers in the System as authorized by the Statute), elected city officials, full-time employees of the System, and eligible beneficiaries.

Governing Statute Vernon’s Texas Civil Statutes

Article 6243h

Executive Director Rhonda Smith

1201 Louisiana, Ste 900 Houston, TX 77002

(713) 595-0100

www.hmeps.org

18

Link To: Financial | Actuarial | Benefits | Governance | Bill Summaries

Summary of Current Plan Data

Date of Valuation

Actuarial Accrued Liability

Actuarial Value of Assets

Unfunded Actuarial Accrued Liability Funded Ratio

Amortization Period1 (years)

Membership Contribution2

Active Annuitant Employee Employer

7/1/2013 $4,129,583,000 $2,382,585,000 $1,746,998,000 57.70% 35 11,781 9,427 3.12% 23.20%

1Amortization period calculated by the PRB assuming a total contribution rate of 26.32% of payroll, with future increases under the Meet and Confer agreement. 2Group A contributes 5%, Groups B and D are non-contributory.

Name Sherry Mose, Chair Roy W. Sanchez, Vice Chair Lonnie Vara David L. Long Lenard Polk Asha Patnaik Barbara Chelette Richard Badger Craig T. Mason Adrian Patterson Edward J. Hamb II

Position Employee Trustee Employee Trustee Retiree Trustee Retiree Trustee Employee Trustee Employee Trustee Board Appointed Trustee City Council Appointee Mayoral Appointee City Council Appointee Controller Appointee

Term Expires 8/2018 8/2018 8/2016 8/2018 8/2016 8/2016 7/2017 7/2017 7/2017 7/2017 7/2017

Houston Municipal Employees Pension System Board of Trustees

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

The Houston Police Officer’s Pension System was created in 1947 by an act of the 50th Legislature, and is governed by Article 6243g-4, Vernon's Texas Civil Statutes. The System is a single employer contributory defined benefit pension plan covering police officers employed full time by the City of Houston that provides for service, disability and death benefits for eligible members and their beneficiaries. The system is governed by a board comprised of seven members and the board is responsible for the general administration, management, and operation of the pension system, including the direction of investments and oversight of the fund's assets.

HOUSTON POLICE OFFICER’S PENSION SYSTEM (HPOPS)

19

Link To: Financial | Actuarial | Benefits | Governance | Bill Summaries

Summary of Current Plan Data

Date of Valuation

Actuarial Accrued Liability

Actuarial Value of Assets

Unfunded Actuarial Accrued Liability Funded Ratio

Amortization Period1 (years)

Membership Contribution

Active Annuitant Employee2 Employer

7/1/2014 $5,363,992,000 $4,342,936,000 $1,021,056,000 80.96% 23 5,343 3,475 9.37% 28.29%

Governing Statute Vernon’s Texas

Civil Statutes Article 6243g-4

Executive Director John Lawson

602 Sawyer St, Suite 300 Houston, TX 77007

(713) 869-8734

www.hpops.org

Name Terry Bratton, Chair George Guerrero, Vice Chair J. Larry Doss, Secretary Dwayne Ready Joe Glezman Craig T. Mason Fletcher Thorne-Thomsen, Jr.

Position Police Member Police Member Retired Member Police Member Retired Member City Treasurer Mayor’s Representative

Term Expires

12/31/2016 12/31/2015 12/31/2015 12/31/2017 12/31/2017

N/A N/A

Houston Police Officer’s Pension System Board of Trustees

1Amortization period calculated by the PRB assuming a total contribution rate of 37.66% of payroll, with future increases under the Meet and Confer agreement. 2Employees hired before 10/9/2004 pay 9%. Employees hired on or after 10/9/2004 pay 10.25%.

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

SAN ANTONIO FIRE & POLICE PENSION FUND

The San Antonio Fire & Police Pension Fund was created in 1941 by an act of the 47th Legislature, and is governed by Article 6243o, Vernon’s Texas Civil Statutes. The Fund is a single employer contributory defined benefit retirement plan that provides comprehensive retirement, death and disability benefits for the City of San Antonio's police officers, fire fighters, retirees and their beneficiaries.

20

Link To: Financial | Actuarial | Benefits | Governance | Bill Summaries

Summary of Current Plan Data

Date of Valuation

Actuarial Accrued Liability

Actuarial Value of Assets

Unfunded Actuarial Accrued Liability Funded Ratio

Amortization Period (years)

Membership Contribution

Active Annuitant Employee Employer

10/1/2014 $2,962,238,443 $2,752,286,963 $209,951,480 92.91% 6.15 3,944 2,373 12.32% 24.64%

Governing Statute Vernon’s Texas Civil

Statutes Article 6243o

Executive Director Warren J. Schott

11603 W Coker Loop San Antonio, TX 78216

(210) 534-3262

www.safppf.org

Name Shawn Ury, Chair J.T. Trevino, Secretary Ray Lopez, Secretary Larry Reed Harry Griffith Jim Smith Dean R. Pearson Art A. Hall Rey Saldana

Position Active Police Trustee Active Fire Trustee Councilman Retired Fire Trustee Retired Police Trustee Active Police Trustee Active Fire Trustee Mayoral Designee Councilman

Term Expires 2017 2015 N/A 2017 2015 2015 2017 N/A N/A

San Antonio Fire & Police Pension Fund Board of Trustees

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

TEXAS LOCAL FIRE FIGHTERS RETIREMENT ACT (TLFFRA)

The Texas Local Fire Fighters Retirement Act was originally created in 1937 by the 45th Legislature and named the Firemen’s Relief and Retirement Fund. In 1989, the Act was restated under Article 6243e and renamed as the Texas Local Fire Fighters Retirement Act (TLFFRA). The Act allows for paid and part-paid fire departments and volunteer fire departments in participating cities to administer their own local retirement systems. The Act provides general guidelines for fund management, including some investment restrictions, but leaves administration, plan design, contributions, and specific investments to each system’s local board. Systems operating under TLFFRA are entirely locally funded and each have their own local boards of trustees governed by state statute. The following list includes paid and part-paid TLFFRA retirement systems:

Governing Statute Vernon’s Texas Civil Statutes

Article 6243e

Abilene Firemen’s Relief & Retirement Fund Amarillo Firemen’s Relief & Retirement Fund Atlanta Firemen’s Relief & Retirement Fund Beaumont Firemen’s Relief & Retirement Fund Big Spring Firemen’s Relief & Retirement Fund Brownwood Firemen’s Relief & Retirement Fund Cleburne Firemen’s Relief & Retirement Fund Conroe Firemen’s Relief & Retirement Fund Corpus Christi Fire Fighter’s Retirement Fund Corsicana Firemen’s Relief & Retirement Fund Denison Firemen’s Relief & Retirement Fund Denton Firemen’s Relief & Retirement Fund Galveston Firefighter’s Relief & Retirement Fund Greenville Firemen’s Relief & Retirement Fund Harlingen Firemen’s Relief & Retirement Fund

Irving Firemen’s Relief & Retirement Fund Killeen Firemen’s Relief & Retirement Fund Laredo Firefighter’s Retirement System Longview Firemen’s Relief & Retirement Fund Lubbock Fire Pension Fund Lufkin Firemen’s Relief & Retirement Fund Marshall Firemen’s Relief & Retirement Fund McAllen Firemen’s Relief & Retirement Fund Midland Firemen’s Relief & Retirement Fund Odessa Firemen’s Relief & Retirement Fund Orange Firemen’s Relief & Retirement Fund Paris Firefighter’s Relief & Retirement Fund Plainview Firemen’s Relief & Retirement Fund Port Arthur Firemen’s Relief & Retirement Fund San Angelo Firemen’s Relief & Retirement Fund

San Benito Firemen’s Pension Fund Sweetwater Firemen’s Relief & Retirement Fund Temple Firemen’s Relief & Retirement Fund Texarkana Firemen’s Relief & Retirement Fund Texas City Firemen’s Relief & Retirement Fund Travis County ESD #6 Firefighter’s Relief & Retirement Fund Tyler Firemen’s Relief & Retirement Fund University Park Firemen’s Relief & Retirement Fund Waxahachie Firemen’s Relief & Retirement Fund Weslaco Firemen’s Relief & Retirement Fund Wichita Falls Firemen’s Relief & Retirement Fund

21

Link To: Financial | Actuarial | Benefits | Governance | Bill Summaries

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

PLANS GOVERNED BY CHAPTER 810 OF THE TEXAS GOVERNMENT CODE

Arlington Employees Deferred Income Plan

Brazos River Authority Retirement Plan

Capital MTA Retirement Plan for Administrative Employees

Capital MTA Retirement Plan for Bargaining Unit Employees

City Public Service of San Antonio Pension Plan

Colorado River Municipal Water District Defined Benefit Retirement Plan & Trust

Corpus Christi Regional Transportation Authority

Cypress-Fairbanks ISD Pension Plan for Non-TRS Employees

Dallas County Hospital District Retirement Plan

Dallas/Fort Worth Airport Board DPS Retirement Plan

Dallas/Fort Worth Airport Board Retirement Plan

DART Employees’ Defined Benefit Retirement Plan & Trust

Galveston Wharves Pension Plan

Guadalupe-Blanco River Authority

Harris County Hospital District Pension Plan

Houston MTA Non-Union Pension Plan

Houston MTA Workers Union Pension Plan

Irving Supplemental Benefit Plan

Lower Colorado River Authority Retirement Plan

Nacogdoches County Hospital District Retirement Plan

Northeast Medical Center Hospital Retirement Plan

Northwest Texas Healthcare System Retirement Plan

Physicians Referral Service Retirement Benefit Plan

Plano Retirement Security Plan

Port of Houston Authority Retirement Plan

Refugio County Memorial Hospital District Retirement Plan

San Antonio Metropolitan Transit Retirement Plan

University Health System Pension Plan

22

Link To: Financial | Actuarial | Benefits | Governance | Bill Summaries

Chapter 810 of the Government Code was enacted in 1991 by the 72nd Legislature in response to two Attorney General opinions (JM-1068 and JM-1142) determining that several local retirement systems were established lacking appropriate legislative authority and were thus invalid under the Texas Constitution. Chapter 810 authorizes all those systems that had been established prior to the Attorney General opinions, and provides authority for subsequent local retirement systems to be established by local jurisdictions. Retirement systems established under Chapter 810 of the Government Code have the authority to determine plan provisions locally. The following list includes actuarially funded retirement systems enabled by Chapter 810:

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

FINANCIAL SECTION

23

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

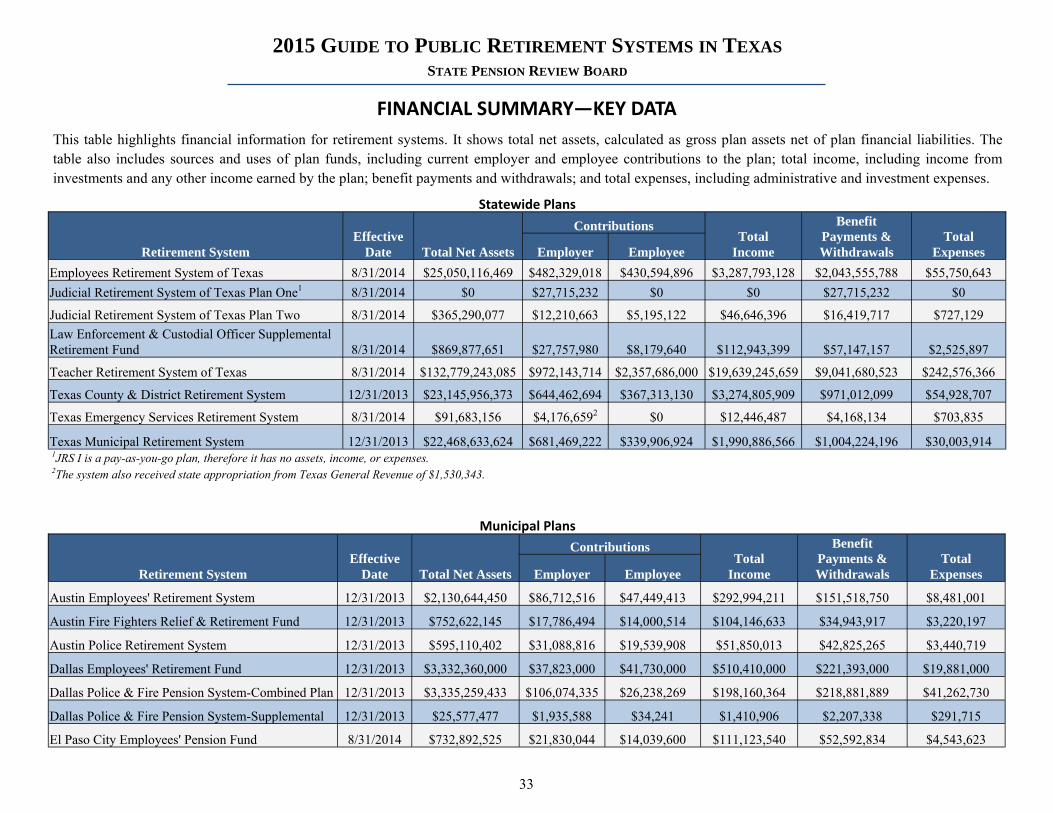

Public retirement systems have three main sources of funding: earnings and investments, employer contributions, and member contributions. It is the ratio of these funding sources relative to the benefits paid to plan participants and plan expenses that determines the long-term financial viability of a retirement system. Policymakers and retirement system sponsors generally set system contributions and benefits, however, for certain systems, the governing body of the retirement system and/or the employees can set system contributions and benefits. Earnings on investments are generated through management of assets held in trust by pension plans. This section will provide trends and plan-specific key financial data for retirement systems, including information relating to their investment performance and asset allocation.

Annual contributions plus investment earnings minus benefit payments and expenses equals the yearly change in total net assets of a plan. The following chart shows a time series of total net assets for Texas public retirement systems from 2003 to 2013. As the chart shows, overall, plans have made steady investment gains since 2009; the net assets reported for 2013 are significantly greater than the 2007 highs.

FINANCIAL SUMMARY

24

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

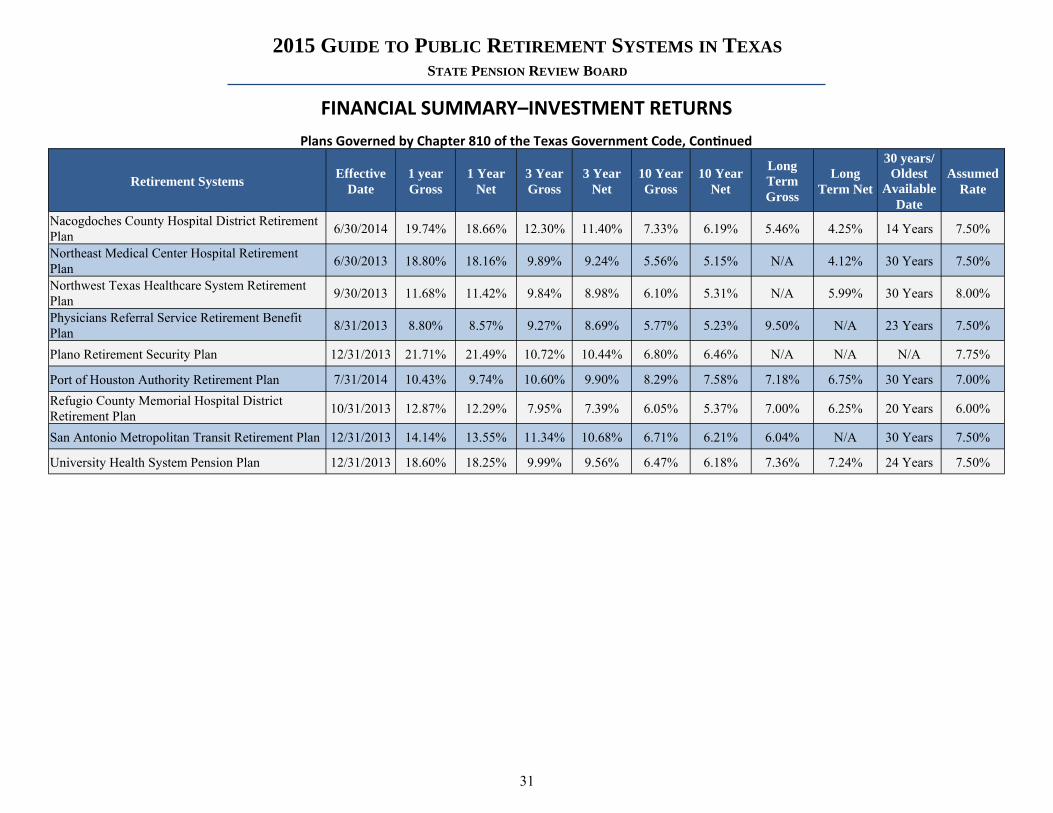

House Bill 13, passed by the 83rd Texas Legislature, added a new reporting requirement specifying that each retirement system must submit to the PRB the rolling gross and net investment returns for the most recent 1-year, 3-year, and 10-year period as well as the most recent 30-year period or since the plan’s inception, whichever is shorter. The PRB adopted a new form, PRB-1000 to facilitate this requirement and the data in the tables below were gathered from the systems submitting this form. Many systems were unable to provide thirty year numbers for various reasons and have instead provided return numbers from as far back as their records allow. Accordingly, the charts below reflect the return numbers provided to us by the retirement systems and include, either thirty year return numbers or the long term return numbers dating as far back as the system reported. The PRB did its own calculations to estimate the missing variables when enough information was available to do so. The PRB calculated the geometric mean of plan returns to form the three-year, ten-year, and long-term average and individual returns. Comparison of short-term investment return rates between plans may result in inaccurate conclusions due to the differences in plan fiscal year ending dates and methodologies used to calculate the annual returns. Additionally, any market volatility can result in plan investment returns that are greater or less than their long term averages. To ensure a more complete analysis, plan investment performance should be reviewed over longer time horizons. Long-term investment return analysis is consistent with pension funding policy, which is determined through forecasting of benefit liabilities over time periods incorporating the lives of plan participants. Average investment returns for all 93 actuarially funded Statewide, Municipal, TLFFRA, and Chapter 810 plans are shown in the table below. The table shows both the gross and net unweighted average investment returns over the one, three, and ten year periods through 2013. Analysis of the data shows that Texas public retirement systems have generated strong investment returns in recent years. As the table shows, the average investment return for Statewide, Municipal, TLFFRA, and Chapter 810 plans has exceeded eight percent for the one and three year period ending December 31, 2013. Overall, this strong investment return performance has helped retirement systems recover losses incurred during the 2008 market decline.

To determine whether actual investment returns met actuarial assumed rates of return over periods longer than ten years, the PRB included the following table.

FINANCIAL SUMMARY—INVESTMENT RETURNS

25

Plan Type 1 Year Gross

1 Year Net

3 Year Gross

3 Year Net

10 Year Gross

10 Year Net

Statewide 12.52% 12.28% 10.00% 9.78% 7.25% 7.10% Municipal 13.07% 12.57% 8.92% 8.44% 7.71% 7.16% TLFFRA 14.86% 14.10% 9.10% 8.08% 7.12% 6.18% Chapter 810 14.49% 13.90% 9.56% 8.98% 6.70% 6.16% Total 14.25% 13.64% 9.28% 8.55% 7.13% 6.43%

Average Returns by Plan Type

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

Statewide Plans

Retirement Systems Effective Date

1 year Gross

1 Year Net

3 Year Gross

3 Year Net

10 Year Gross

10 Year Net

Long Term Gross

Long Term Net

30 years/Oldest

Available Date

Assumed Rate

Employees Retirement System 8/31/2013 10.07% 9.87% 10.28% 10.07% 7.12% 6.98% 8.52% N/A 30 Years 8.00%

Judicial Retirement System of Texas Plan Two1 8/31/2013 10.07% 9.87% 10.28% 10.07% 7.12% 6.98% 8.52% N/A 30 Years 8.00% Law Enforcement and Custodial Officer Supplemental Retirement Fund 8/31/2013 10.07% 9.87% 10.28% 10.07% 7.12% 6.98% 8.52% N/A 30 Years 8.00%

Teacher Retirement System 8/31/2013 9.15% 9.01% 10.76% 10.63% 7.25% 7.20% 10.02% 10.00% 30 Years 8.00%

Texas County & District Retirement System 12/31/2013 16.53% 16.39% 9.18% 9.03% 7.04% 6.90% 9.52% 9.46% 30 Years 8.00%

Texas Emergency Services Retirement System 8/31/2013 21.88% 21.29% 11.80% 11.31% 7.99% 7.55% 7.23% 6.91% 30 Years 7.75%

Texas Municipal Retirement System 12/31/2013 9.86% 9.65% 7.40% 7.26% 7.14% 7.09% 9.41% 9.39% 30 Years 7.00%

Municipal Plans

Retirement Systems Effective Date

1 year Gross

1 Year Net

3 Year Gross

3 Year Net

10 Year Gross

10 Year Net

Long Term Gross

Long Term Net

30 years/Oldest

Available Date

Assumed Rate

Austin Employees’ Retirement System 12/31/2013 15.98% 15.54% 9.38% 8.92% 7.73% 7.38% 9.95% 9.63% 30 Years 7.75%

Austin Fire Fighters Relief & Retirement Fund 12/31/2013 17.20% 16.90% 9.20% 8.70% 7.30% 6.90% 7.30% 7.00% 17 Years 7.75%

Austin Police Retirement System2 12/31/2013 9.58% 9.10% 5.71% 5.26% 6.64% 6.15% 9.92% 9.35% 30 Years 8.00%

Dallas Employees’ Retirement Fund 12/31/2013 N/A 16.93% N/A 10.47% N/A 7.96% N/A 9.64% 30 Years 8.25%

Dallas Police & Fire Pension System3 12/31/2013 5.10% 4.50% 4.50% 3.90% 6.30% 5.70% N/A 8.60% 30 Years 8.50%

El Paso City Employees’ Pension Fund 8/31/2013 14.18% 13.81% 10.54% 10.19% 7.90% 7.11% 8.93% N/A 30 Years 7.50%

El Paso Firemen’s Pension Fund 12/31/2013 17.86% 17.51% 9.21% 8.85% 8.35% 7.98% 9.27% 9.08% 30 Years 7.75%

El Paso Police Pension Fund 12/31/2013 17.86% 17.51% 9.21% 8.85% 8.35% 7.98% 9.27% 9.08% 30 Years 7.75%

Fort Worth Employees’ Retirement Fund 9/30/2013 10.97% 10.53% 7.73% 7.33% 6.46% 5.97% 9.34% 9.16% 30 Years 8.00%

Galveston Employees’ Retirement Fund 12/31/2013 16.72% 16.06% 9.71% 8.82% 7.25% 6.30% N/A 3.26% 15 Years 8.00%

FINANCIAL SUMMARY—INVESTMENT RETURNS

1JRS I is not included because it is a pay-as-you-go system.

26

2Returns calculated by the PRB using the Simple Dietz Method with multi-year returns calculated as an arithmetic average. 3Investments of the DPFPS’s Combined and Supplemental plans are commingled.

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

Retirement Systems Effective Date

1 year Gross

1 Year Net

3 Year Gross

3 Year Net

10 Year Gross

10 Year Net

Long Term Gross

Long Term Net

30 years/Oldest

Available Date

Assumed Rate

Galveston Employees’ Retirement Fund for Police 12/31/2013 16.26% 15.57% 8.96% 8.26% 6.11% 5.30% N/A N/A 10 Years 7.50%

Houston Firefighters’ Relief & Retirement Fund 6/30/2014 17.82% 17.52% 10.30% 10.03% 9.68% 9.34% 10.79% N/A 30 Years 8.50%

Houston Municipal Employees Pension System 6/30/2014 16.39% 15.97% 9.70% 9.30% 9.31% 8.96% 10.19% 9.72% 30 Years 8.50%

Houston Police Officer’s Pension System 6/30/2014 18.10% 17.40% 9.80% 9.30% 8.70% 8.20% 10.80% 10.30% 30 Years 8.00%

San Antonio Fire & Police Pension Fund 9/30/2014 9.54% 9.20% 11.60% 11.28% 6.67% 6.34% N/A 12.02% 30 Years 7.50%

Municipal Plans, Con nued

TLFFRA Plans

Retirement Systems Effective Date

1 year Gross 1 Year Net 3 Year

Gross 3 Year

Net 10 Year Gross

10 Year Net

Long Term Gross

Long Term Net

30 years/Oldest

Available Date

Assumed Rate

Abilene Firemen’s Relief & Retirement Fund 9/30/2013 10.02% 9.54% 8.44% 7.85% 7.15% 6.55% N/A 6.68% 20 Years 8.00%

Amarillo Firemen’s Relief & Retirement Fund 12/31/2013 24.66% 24.34% 12.82% 12.49% 8.45% 8.15% N/A 9.14% 19 Years 8.25%

Atlanta Firemen’s Relief & Retirement Fund 12/31/2013 16.02% 14.90% 9.35% 8.21% 7.36% 6.25% N/A 6.38% 19 Years 7.25%

Beaumont Firemen’s Relief & Retirement Fund 12/31/2013 12.66% 12.29% 8.17% 7.54% 6.30% 5.57% N/A 7.06% 19 Years 8.00%

Big Spring Firemen’s Relief & Retirement Fund 12/31/2013 15.40% 14.54% 9.28% 8.02% 7.88% 6.70% N/A 8.56% 19 Years 8.00%

Brownwood Firemen’s Relief & Retirement Fund 12/31/2013 16.06% 14.81% N/A 6.65% N/A 5.62% N/A 5.87% 19 Years 7.25%

Cleburne Firemen’s Relief & Retirement Fund 12/31/2013 17.72% 17.11% 9.36% 8.77% 5.90% 5.30% N/A 6.73% 19 Years 7.50%

Conroe Fire Fighters’ Retirement Fund 12/31/2013 13.74% 12.79% 6.86% 5.90% 4.98% 3.88% N/A 4.86% 19 Years 7.75%

Corpus Christi Fire Fighter’s Retirement System 12/31/2013 17.65% 17.18% 10.77% 10.21% 7.83% 7.23% N/A 8.18% 19 Years 8.00%

FINANCIAL SUMMARY—INVESTMENT RETURNS

27

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

Retirement Systems Effective Date

1 year Gross 1 Year Net 3 Year

Gross 3 Year

Net 10 Year Gross

10 Year Net

Long Term Gross

Long Term Net

30 years/Oldest

Available Date

Assumed Rate

Corsicana Firemen’s Relief & Retirement Fund 12/31/2013 15.07% 13.76% 8.36% 6.93% 6.62% 5.18% N/A 4.66% 19 Years 7.50%

Denison Firemen’s Relief & Retirement Fund 12/31/2013 21.40% 20.80% 11.03% 10.42% 7.32% 6.68% N/A 6.91% 19 Years 7.75%

Denton Firemen’s Relief & Retirement Fund 12/31/2013 15.69% 15.66% 9.95% 9.82% 7.34% 7.17% N/A 8.07% 19 Years 7.00%

Galveston Firefighter’s Relief & Retirement Fund 12/31/2013 15.00% 14.54% 8.92% 8.21% 6.28% 5.59% N/A 7.19% 19 Years 8.00%

Greenville Firemen’s Relief & Retirement Fund 12/31/2013 16.68% 15.85% 9.83% 8.99% 6.58% 5.90% N/A 7.14% 19 Years 8.25%

Harlingen Firemen’s Relief & Retirement Fund 12/31/2013 11.90% 11.20% 8.90% 8.20% 8.20% 7.40% 9.50% 8.70% 19 Years 8.00%

Irving Firemen’s Relief & Retirement Fund 12/31/2013 21.88% 21.06% 11.11% 10.35% 7.95% 7.21% N/A 6.50% 19 Years 8.25%

Killeen Firemen’s Relief & Retirement Fund 9/30/2013 5.67% 5.29% 5.72% 4.95% 6.52% 6.00% N/A 5.68% 18 Years 7.75%

Laredo Firefighters Retirement System 9/30/2013 12.37% 11.92% 8.69% 8.15% 6.56% 6.07% 5.46% 4.96% 19 Years 8.00%

Longview Firemen’s Relief & Retirement Fund 12/31/2013 10.65% 9.94% 7.36% 6.56% 6.59% 5.71% N/A 7.20% 19 Years 8.00%

Lubbock Fire Pension Fund 12/31/2013 18.94% 18.30% 9.78% 8.93% 7.63% 6.96% N/A 8.66% 19 Years 8.00%

Lufkin Firemen’s Relief & Retirement Fund 12/31/2013 15.60% 14.70% 9.40% 8.56% 8.07% 7.47% N/A N/A N/A 7.50%

Marshall Firemen’s Relief & Retirement Fund 12/31/2013 16.08% 15.14% 9.45% 8.52% 6.85% 5.98% N/A 6.52% 19 Years 7.75%

McAllen Firemen’s Relief & Retirement Fund 9/30/2013 12.26% 11.30% 9.33% 8.43% 7.62% 6.68% N/A 7.58% 18 Years 8.00%

Midland Firemen’s Relief & Retirement Fund 12/31/2013 15.20% 14.66% 8.12% 7.31% 7.04% 6.24% N/A 8.68% 19 Years 8.00%

Odessa Firemen’s Relief & Retirement Fund 12/31/2013 11.52% 11.00% N/A 5.70% N/A 5.34% N/A 8.02% 19 Years 8.25%

TLFFRA Plans, Con nued

FINANCIAL SUMMARY—INVESTMENT RETURNS

28

2015 GUIDE TO PUBLIC RETIREMENT SYSTEMS IN TEXAS STATE PENSION REVIEW BOARD

Retirement Systems Effective Date

1 year Gross 1 Year Net 3 Year

Gross 3 Year

Net 10 Year Gross

10 Year Net

Long Term Gross

Long Term Net

30 years/Oldest

Available Date

Assumed Rate

Orange Firemen’s Relief & Retirement Fund 12/31/2013 16.26% 15.07% 9.23% 7.96% 7.10% 5.87% N/A 7.01% 19 Years 8.00%

Paris Firefighters’ Relief & Retirement Fund 12/31/2013 3.28% 2.27% 4.65% 3.13% 5.49% 3.99% N/A 5.85% 19 Years 8.00%

Plainview Firemen’s Relief & Retirement Fund 12/31/2013 16.29% 15.14% 9.72% 8.49% 5.92% 4.61% N/A 5.38% 19 Years 7.75%

Port Arthur Firemen’s Relief & Retirement Fund 12/31/2013 16.31% 16.16% 9.22% 8.98% 6.64% 6.39% N/A 7.52% 19 Years 8.00%

San Angelo Firemen’s Relief & Retirement Fund 12/31/2013 17.89% 17.35% 9.95% 9.38% 7.64% 7.08% N/A 7.96% 19 Years 7.90%

San Benito Firemen’s Relief & Retirement Fund 12/31/2013 14.00% 12.66% 9.00% 6.28% 5.38% 3.73% N/A N/A N/A 7.00%