guide to international financial reporting …/media/site/r2-docs/guide to...canadian series...

TRANSCRIPT

Canadian SerieS

FINANCIAL REPORTING

Guide to International FinancialReporting Standards in Canada

IAS 16 Property, Plant and EquipmentIrene Wiecek, FCPA, FCA

Martha Dunlop, FCPA, FCA

Jane Bowen, FCPA, FCA

primary editor: Alex Fisher, CPA, CA

June 2013

Canadian SerieS

Guide to International Financial Reporting Standards in Canada

IAS 16 Property, Plant and EquipmentIrene Wiecek, FCPA, FCA

Martha Dunlop, FCPA, FCA

Jane Bowen, FCPA, FCA

primary editor: Alex Fisher, CPA, CA

June 2013

iiiIAS 16 Property, Plant and Equipment

June 2013

Table of ContentsPreface 1

Research Resources 4

Notice to Readers 4

Introduction to IAS 16 5

Standards Update 6

IASB 6

Methods of Depreciation and Amortization 6

Bearer Biological Assets 6

Annual Improvements 7

IFRIC 7

Key Standards Referred to in This Publication 8

IAS 16 Definitions 9

Overview of Key Requirements 10

Analysis of Relevant Issues 12

Scope 12

Recognition of Initial and Subsequent Costs 14

Items Acquired for Safety or Environmental Reasons 14

Spare Parts, Standby Equipment and Servicing Equipment 15

Subsequent Costs 15

Measurement at Recognition 17

Costs of a Self-Constructed Asset 18

Borrowing Costs 19

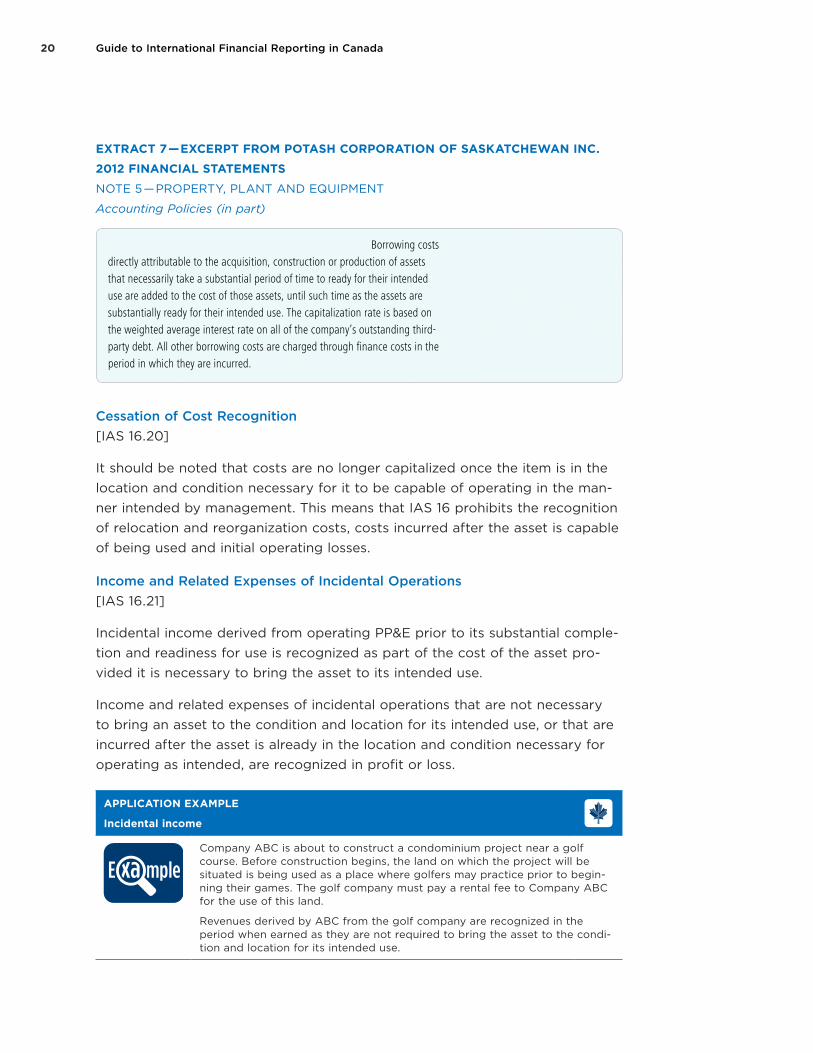

Cessation of Cost Recognition 20

Income and Related Expenses of Incidental Operations 20

Assets Acquired Using Government Grants 21

Assets Held under a Finance Lease 21

Non-Monetary Transactions 21

Transfers of Assets from Customers [IFRIC 18] 22

Subsequent Measurement 24

Cost Model 24

Revaluation Model 24

iv Guide to International Financial Reporting in Canada

Costs of Dismantling, Removal and Site Restoration (Decommissioning Costs) and Changes to These Costs 31

Depreciation 33

Component Accounting 34

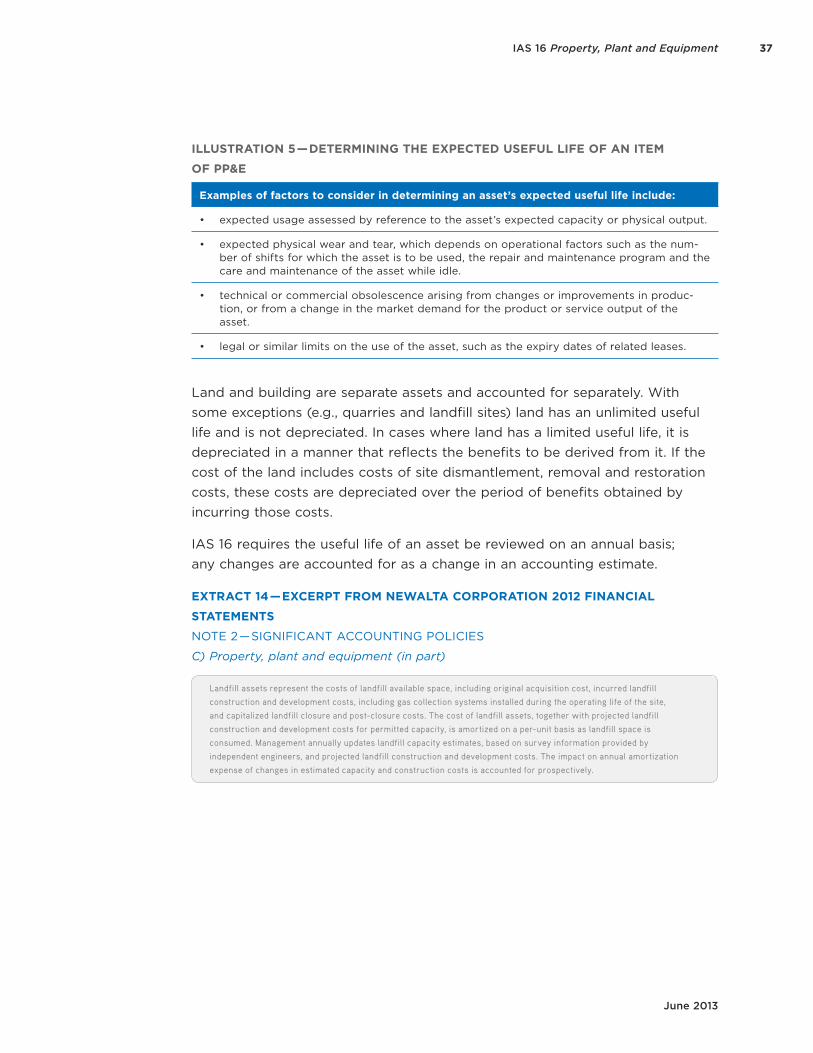

Residual Value 36

Useful Life 36

Depreciation Start Date 39

Depreciation End Date 40

Depreciation Method 40

Impairment and Compensation for Impairment 43

Compensation for Impairment 44

Derecognition of PP&E 44

Disclosure 46

Accounting Policy Choices 50

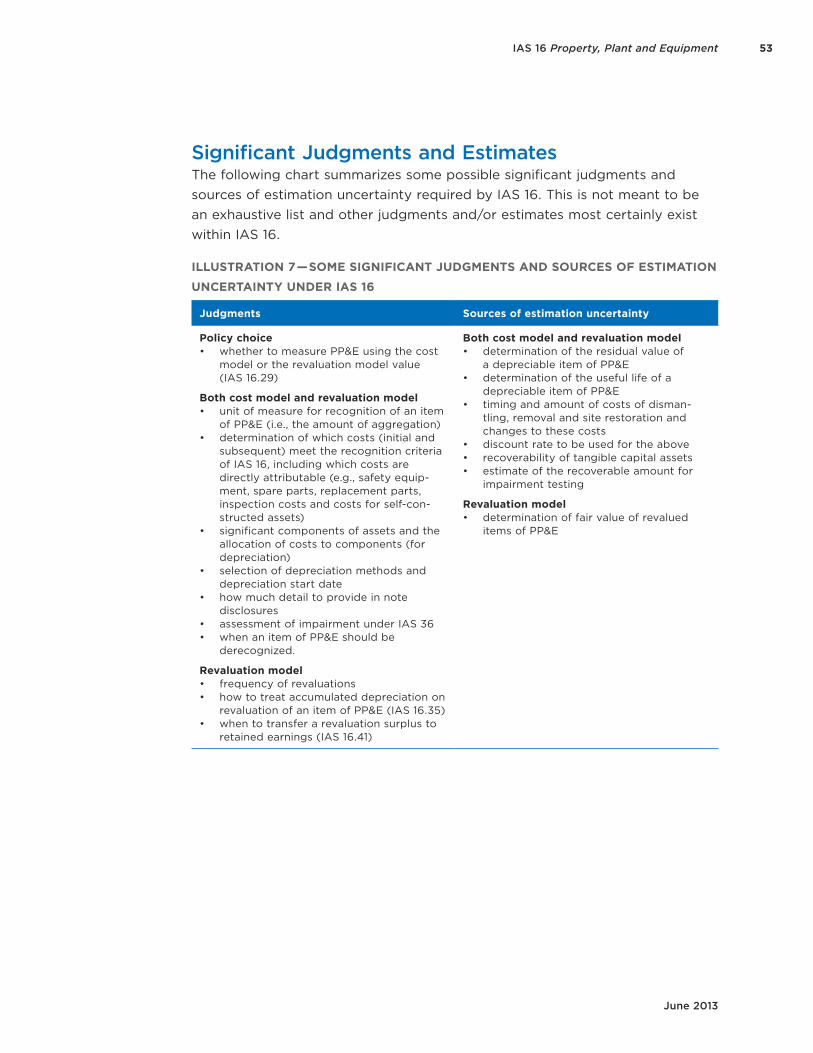

Significant Judgments and Estimates 53

Appendix A — Acronyms Used 55

List of ExtractsExtract 1 — Excerpt from The Brick Ltd. 2012 Financial StatementsNote 3 — Significant Accounting Policies 13

Extract 2 — Excerpt from Sherritt International Corporation 2012 Financial StatementsNote 2 — Summary of Significant Accounting Policies 15

Extract 3 — Excerpt from Air Canada 2012 Financial StatementsNote 2 — Basis of Presentation and Summary of Significant Accounting Policies 16

Extract 4 — Excerpt from Saskatchewan Transportation Company 2012 Financial StatementsNote 4 — Significant Accounting Policies 16

Extract 5 — Excerpt from Bombardier Inc. 2012 Financial StatementsNote 2 — Summary of Significant Accounting Policies 17

v

June 2013

Table of Contents

Extract 6 — Excerpt from Rogers Communications Inc. 2012 Financial StatementsNote 2 — Significant Accounting Policies 19

Extract 7 — Excerpt from Potash Corporation of Saskatchewan Inc. 2012 Financial StatementsNote 5 — Property, Plant and Equipment 20

Extract 8 — Excerpt from Cenovus Energy Inc. 2012 Financial StatementsNote 3 — Summary of Significant Accounting Policies 21

Extract 9 — Excerpt from the Great Canadian Gaming Corporation 2012 Financial StatementsNote 3 — Critical Accounting Estimates and Judgments 22

Extract 10 — Excerpt from The Brick Ltd. 2012 Financial StatementsNote 3 — Significant Accounting Policies 24

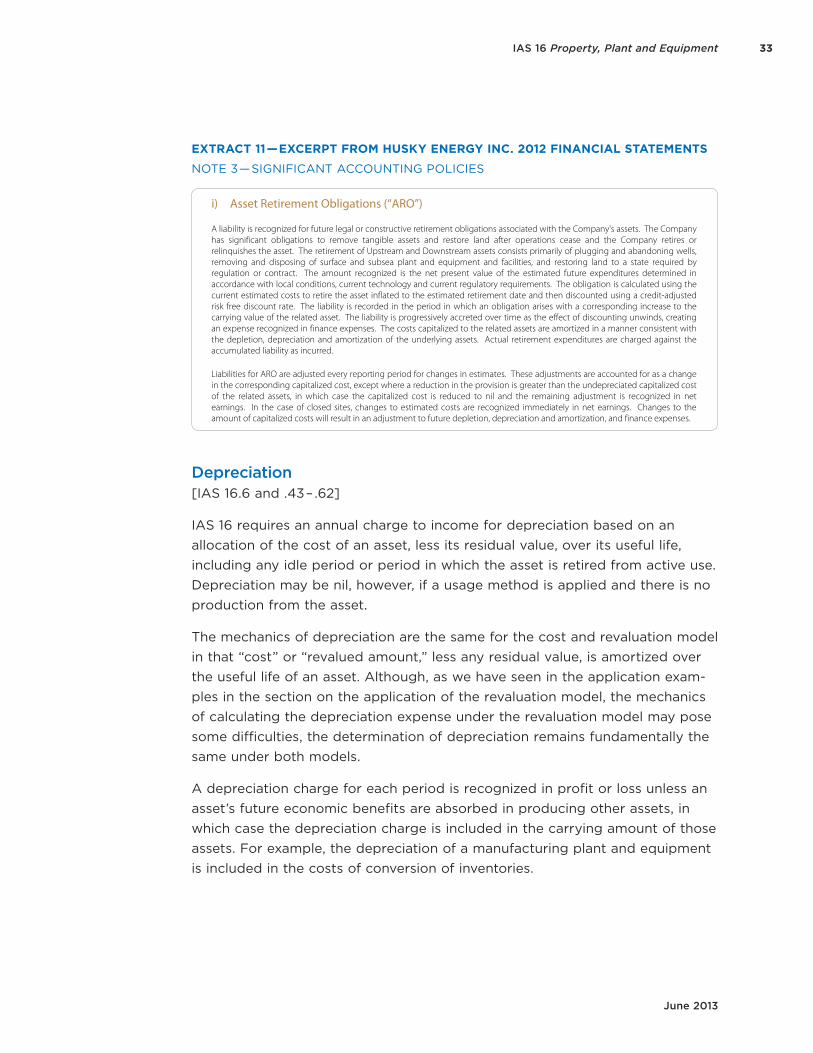

Extract 11 — Excerpt from Husky Energy Inc. 2012 Financial StatementsNote 3 — Significant Accounting Policies 33

Extract 12 — Excerpt from Air Canada 2012 Financial StatementsNote 2 — Basis of Presentation and Summary of Significant Accounting Policies 35

Extract 13 — Excerpt from Westjet Airlines Ltd. 2012 Financial StatementsNote 1 — Statement of Significant Accounting Policies 36

Extract 14 — Excerpt from Newalta Corporation 2012 Financial StatementsNote 2 — Significant Accounting Policies 37

Extract 15 — Excerpt from Sears Canada Inc. 2012 Financial StatementsNote 2 — Significant Accounting Policies 43

Extract 16 — Excerpt from Royal Bank of Canada 2012 Financial StatementsNote 2 — Summary of Significant Accounting Policies, Estimates and Judgments 43

Extract 17 — Excerpt from Shoppers Drug Mart Corporation 2012 Financial StatementsNote 3 — Significant Accounting Policies 45

Extract 18 — Excerpt from Telus Corporation 2012 Financial StatementsNote 15 — Property, Plant and Equipment 50

Extract 19 — Excerpt from Enerflex Ltd. 2012 Financial StatementsNote 4 — Significant Accounting Estimates and Judgments 54

vi Guide to International Financial Reporting in Canada

List of IllustrationsIllustration 1 — Included and Excluded Costs of PP&E 17

Illustration 2 — Application of the Revaluation Model 25

Illustration 3 — Recognition of Revaluation Changes 28

Illustration 4 — IFRIC 1 — Changes in Existing Decommissioning, Restoration and Similar Liabilities 32

Illustration 5 — Determining the Expected Useful Life of an Item of PP&E 37

Illustration 6 — Summary of Some IAS 16 Disclosure Requirements 46

Illustration 7 — Some Significant Judgments and Sources of Estimation Uncer-tainty Under IAS 16 53

1

June 2013

IAS 16 Property, Plant and Equipment

PrefaceThis publication is part of the Guide to International Financial Reporting Stan-dards in Canada series published by the Chartered Professional Accountants of Canada (CPA Canada) to support its members.

The objective of this publication, IAS 16 Property, Plant and Equipment, is to help you understand IAS 16 and the IASB material that accompanies it. The publication begins with an introduction and standards update and then includes definitions, an overview chart, an analysis section, a section on accounting policies and one on significant judgments and estimates.

Every attempt has been made to use plain language and to avoid mere restatement of the IFRS standards although, where deemed necessary, specific wording from the standards is referred to.

This publication has been carefully prepared, but it necessarily contains infor-mation in summarized form and is, therefore, intended for general guidance only. It is not intended to be a substitute for detailed research or the exercise of professional judgment.

The overview section takes a high-level look at the key requirements of the standard in a chart format (the Overview chart). Specific “touchstone” refer-ences to IAS 16 are included in the Overview chart to help you navigate the standard. These are not meant to be comprehensive references, rather a

2 Guide to International Financial Reporting in Canada

starting point for your research. The Analysis section analyzes the more com-plex areas of the standard in more depth. Note that, where parts of the stan-dard are more straightforward, they are included in the Overview chart only as it is felt that this coverage is at a sufficient level.

Illustrations, examples and extracts have been used to explain a particular concept and/or provide insight into how the standard is applied. Financial statement note extracts have been selected to illustrate a particular point but do not necessarily represent best practices.

Several features have been included to enhance understanding as follows:

1. Illustrations, including the following:• charts• decision trees• summaries

These illustrations add value by summarizing, grouping, highlighting simi-larities/differences and working through decision processes in applying the standard.

2. Examples• IASB Illustrative Examples excerpts• IASB examples excerpted from the standard• other examples

These examples add value by showing how a particular part of the standard might be applied in a specific situation. Note that IAS 16 does not include any illustrative examples and therefore the examples included in this publi-cation are not authoritative.

3. Extracts from the IASB standards, including the following:• definitions• select quotes

Even though every attempt has been made to use plain language, in some cases, it has been important to use the specific wording in the standard to get a point across.

4. Extracts from financial statements — financial statements of prominent Canadian companies have been selected, including those that were recipi-ents of the CPA Canada Corporate Reporting Awards. The report on the Corporate Reporting Awards, including a list of winners, may be found at www.cpacanada.ca.

The extracts included illustrate a particular aspect. It may be useful to review the complete note, which may be found at www.sedar.com.

3IAS 16 Property, Plant and Equipment

June 2013

5. Non-IFRS Interpretations Committee insights — Items discussed but not taken to the IASB agenda, referred to as NIFRICs (Non-IFRICs), have been included because, in some cases, they provide insights into the standard setting decision processes.

6. IFRS Discussion Group (IDG) insights — references to IDG discussions. The IDG was established by the Canadian Accounting Standards Board (AcSB) in 2009. Its aim is to provide a public forum for the discussion of issues relating to IFRSs and to collect the views of Canadians experiencing issues in implementing IFRSs. These discussions are not meant to provide authori-tative guidance; however, they do help clarify issues and allow interested parties to learn how others are working through their financial reporting issues and applying judgment in the application of IFRSs. These have been drawn from the publically available reports of the IDG meetings. The IDG’s meetings are recorded and audio webcasts are archived on the AcSB website (www.frascanada.ca). Discussants include preparers, practitioners, regulators and users of financial statements.

7. References to other relevant CPA Canada material.

8. This publication is part of a series with various publication dates. The dates have been noted on each publication.

Where necessary, icons have been used throughout the publication to refer to many of these features so the reader can easily distinguish the sources of the information.

Insight

Application insights explain, discuss and/or debate a particular IFRS application issue.

Application insights include:• NIFRICs (Non-IFRICs)• IFRS Discussion Group reports

Viewpoints

Viewpoints refer to the Viewpoints: Applying IFRSs in the Min-ing Industry or the Viewpoints: Applying IFRSs in the Oil and Gas Industry — a series of papers that addresses specific IFRS application issues.

E xa mpleExamples illustrate how a particular part of an IFRS might be applied in a specific situation.

4 Guide to International Financial Reporting in Canada

Statistics Statistics on particular IFRS application practices highlight common practices and/or application approaches.

Resources Resources include references to other relevant CPA Canada material.

Research ResourcesCPA Canada has compiled various IFRS technical summaries, practical applica-tion guides and frequently-asked-question documents aimed at supporting the understanding and application of IFRSs. For more information on IFRSs visit our website.

Notice to ReadersThe Research, Guidance and Support Group of the Chartered Professional Accountants of Canada (CPA Canada) commissioned this publication as part of its continuing research program. The views and conclusions expressed in this publication are those of the authors. They have not been adopted, endorsed, approved or otherwise acted upon by a Board or Committee of CPA Canada or any Provincial Institute / Ordre. CPA Canada and the authors do not accept any responsibility or liability that might occur directly or indirectly as a conse-quence of the use, application or reliance on this material.

5IAS 16 Property, Plant and Equipment

June 2013

Introduction to IAS 16IAS 16 prescribes the accounting treatment for property, plant and equipment (PP&E) held for use in the production or supply of goods or services, for rental to others or for administrative purposes, that are expected to be used for more than one period. IAS 16 allows an accounting policy choice for PP&E: items may be carried at cost or at a revalued amount.

IAS 16 provides guidance on what may, and what may not, be considered PP&E, the recognition and measurement of initial and subsequent costs and the derecognition of an item of PP&E.

IAS 16 includes a Basis for Conclusions document that summarizes the Inter-national Accounting Standards Board’s (IASB) considerations and conclusions in the development of this standard. IAS 16 does not include any illustrative examples.

The costs to dismantle, remove and restore items of PP&E are included in the carrying amount of the asset. IFRIC 1 Changes in Existing Decommissioning, Restoration and Similar Liabilities, provides guidance on accounting for the effect of changes in the measurement of existing decommissioning liabilities and discusses the related impact on PP&E.

IFRIC 18 Transfers of Assets from Customers, applies to the accounting for transfers of items of PP&E by entities that receive such transfers from their customers. This IFRIC provides guidance on the recognition and measurement of such asset transfers.

This publication is based on the requirements of IFRS standards and inter-pretations for annual periods beginning January 1, 2013. Where appropriate, for illustration purposes, certain note-disclosure examples are presented from financial statements with annual periods ending before January 1, 2013.

This publication has not been updated since the publication date of June 2013. readers are cautioned that certain aspects of iFrSs may have changed since the publication date.

6 Guide to International Financial Reporting in Canada

Standards Update

IASB

Methods of Depreciation and AmortizationIn December 2012, the IASB issued an Exposure Draft (ED), Clarification of Acceptable Methods of Depreciation and Amortization (Proposed Amendments to IAS 16 and IAS 38), based on a submission from the IFRS Interpretations Committee. IAS 16.60 requires the depreciation method to reflect the pattern in which an asset’s future economic benefits are expected to be consumed. The proposed revisions are intended to clarify that revenue-based methods are not acceptable methods of depreciating or amortizing an item of PP&E or an intangible asset. This is because a revenue-based method reflects the eco-nomic benefits being generated from an asset rather than the expected pat-tern of consumption of the asset.

The proposed amendment also provides further guidance on the application of the diminishing balance method of depreciation. This proposed guidance clarifies that information about technical or commercial obsolescence of the output of the asset (product or service) is relevant for estimating the pattern of consumption of future economic benefits and the useful life of the asset. As an example, the ED notes that an expected future reduction in the unit selling price of the output, as a result of technical or commercial obsolescence, could be an indication of the diminution of the future economic benefits of the asset.

The comment period on this ED closed April 2, 2013, and the expected com-pletion date is the fourth quarter of 2013.

Bearer Biological AssetsThe IASB has a limited-scope project to amend IAS 41 to address bearer bio-logical assets (e.g., grapevines, dairy cows, etc.). These assets are accounted for under IAS 41 at fair value less costs to sell based on the principle that the transformation of bearer biological assets is best reflected by fair value mea-surement. The counter argument is that mature bearer biological assets are not going through biological transformation and, as such, are similar to manufac-turing assets and should be accounted for under IAS 16.

This project will focus on measurement of bearer biological assets that are plants. This ED was issued on June 26, 2013, and was available for comment until October 28, 2013.

7IAS 16 Property, Plant and Equipment

June 2013

Annual Improvements

2010 — 2012 cycle (ED issued May 2012)The IASB proposes an amendment to IAS 16 to address concerns about the computation of accumulated depreciation at the date of a revaluation of PP&E for entities that apply the revaluation method to account for PP&E. The con-cern stems from differing practices in computing accumulated depreciation for a revalued item where the residual value, the useful life or the depreciation method is re-estimated before a revaluation.

When an item of PP&E is revalued, IAS 16 currently allows entities a choice to (1) restate accumulated depreciation proportionately with the change in the gross carrying amount of the asset, or (2) eliminate accumulated depreciation against the gross carrying amount of the asset. A problem arises with the use of method (1) if the residual value, useful life or depreciation method is re-estimated before a revaluation adjustment. In these situations, the restatement of accumulated depreciation proportionately would not result in the carrying amount of the asset being equal to the revalued asset amount less the reval-ued accumulated depreciation. The proposed amendment to IAS 16 (and IAS 38) would state that the accumulated depreciation is computed as the differ-ence between the gross and net carrying amounts. The proposed amendment would also clarify that the determination of accumulated depreciation does not depend on the selection of the valuation technique.

A similar amendment is proposed in IAS 38 for intangible assets measured using the revaluation model.

It is expected that this amendment will be approved and issued in the fourth quarter of 2013 and will be effective for annual periods beginning on or after January 1, 2014, with early adoption permitted.

IFRICThe Interpretations Committee received a request to address an issue related to contractual arrangements within the scope of IFRIC 12, Service Concession Arrangements. This request is to clarify in what circumstances contractual pay-ments made by an operator under a service concession arrangement should:1. be included in the measurement of an asset and liability at the start of the

concession; or2. be accounted for as executory in nature (i.e., be recognized as expenses as

incurred over the term of the concession arrangement).

8 Guide to International Financial Reporting in Canada

At the January 2013 meeting, the Interpretations Committee tentatively decided to recommend that the IASB amend IAS 16 to require the adjustments of the carrying amount of a financial liability, other than those adjustments for finance costs not eligible for capitalization in accordance with IAS 23, be recognized as corresponding adjustments to the cost of the asset to the extent that IAS 16 or IAS 38 requires them. The Interpretations Committee also decided to propose amendments to IFRIC 12.

Key Standards Referred to in This PublicationThe following is a list of standards mentioned in this publication. Names of the standards have been included for the sake of clarity. The standards have been separated into two groups for purposes of this list — primary and secondary. The primary standards are the main standards that deal with the topic under discussion (in this publication — property, plant and equipment). The secondary standards are those referred to in this publication but not discussed in depth.

Primary standards:

IAS 16 Property, Plant and EquipmentIFRIC 1 Changes in Existing Decommissioning, Restoration and Similar LiabilitiesIFRIC 18 Transfers of Assets from Customers

Secondary standards:

IFRS 2 Share-based PaymentsIFRS 5 Non-current Assets Held for Sale and Discontinued OperationsIFRS 6 Exploration for and Evaluation of Mineral ResourcesIFRS 13 Fair Value MeasurementIAS 1 Presentation of Financial StatementsIAS 2 InventoriesIAS 8 Accounting Policies, Changes in Estimates and ErrorsIAS 12 Income TaxesIAS 17 LeasesIAS 18 RevenueIAS 20 Accounting for Government Grants and Disclosure of Government AssistanceIAS 23 Borrowing CostsIAS 36 Impairment of AssetsIAS 37 Provisions, Contingent Liabilities and Contingent AssetsIAS 38 Intangible AssetsIAS 40 Investment PropertyIAS 41 AgricultureIFRIC 12 Service Concession Arrangements

9IAS 16 Property, Plant and Equipment

June 2013

Subsequently, only the standard number will be referenced, not the name (e.g., IAS 36).

IAS 16 Definitions[IAS 16.6]

These definitions were taken directly from IAS 16.

Carrying amount Carrying amount is the amount at which an asset is recognized after deducting any accumulated depreciation and accumulated impair-ment losses.

Cost Cost is the amount of cash or cash equivalents paid or the fair value of the other consideration given to acquire an asset at the time of its acquisition or construction or, where applicable, the amount attributed to that asset when initially recognized in accordance with the specific requirements of other IFRSs (e.g., IFRS 2 Share-based Payment).

Depreciable amount Depreciable amount is the cost of an asset or other amount substi-tuted for cost less its residual value.

Depreciation Depreciation is the systematic allocation of the depreciable amount of an asset over its useful life.

Entity-specific value Entity-specific value is the present value of the cash flows an entity expects to arise from the continuing use of an asset and from its disposal at the end of its useful life or expects to incur when settling a liability.

Fair value Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between mar-ket participants at the measurement date. (See IFRS 13 Fair Value Measurement.)

Impairment loss An impairment loss is the amount by which the carrying amount of an asset exceeds its recoverable amount.

Property, plant and equipment

Property, plant and equipment are tangible items that:1. are held for use in the production or supply of goods or services,

for rental to others or for administrative purposes; and2. are expected to be used during more than one period.

Recoverable amount Recoverable amount is the higher of an asset’s fair value less costs to sell and its value in use (VIU).

Residual amount The residual value of an asset is the estimated amount that an entity would currently obtain from disposal of the asset, after deducting the estimated costs of disposal, if the asset were already of the age and in the condition expected at the end of its useful life.

Useful life Useful life is:1. the period over which an asset is expected to be available for use

by an entity; or2. the number of production or similar units expected to be obtained

from the asset by an entity.

10 Guide to International Financial Reporting in Canada

Overview of Key RequirementsThe following chart provides a high-level overview of the key requirements of IAS 16 and accompanying IASB support materials. The intent is not to repeat the standard but to walk the reader through the main requirements in the standard and identify the areas where detailed guidance is given and where complexity in application exists. Areas of greater complexity will be covered in more detail under the Analysis section of this publication.

As mentioned in the Preface, specific “touchstone” references to IAS 16 have been inserted to help the reader navigate the standard. The referencing is not meant to be all-inclusive but rather to give a starting point for further research in the standard itself.

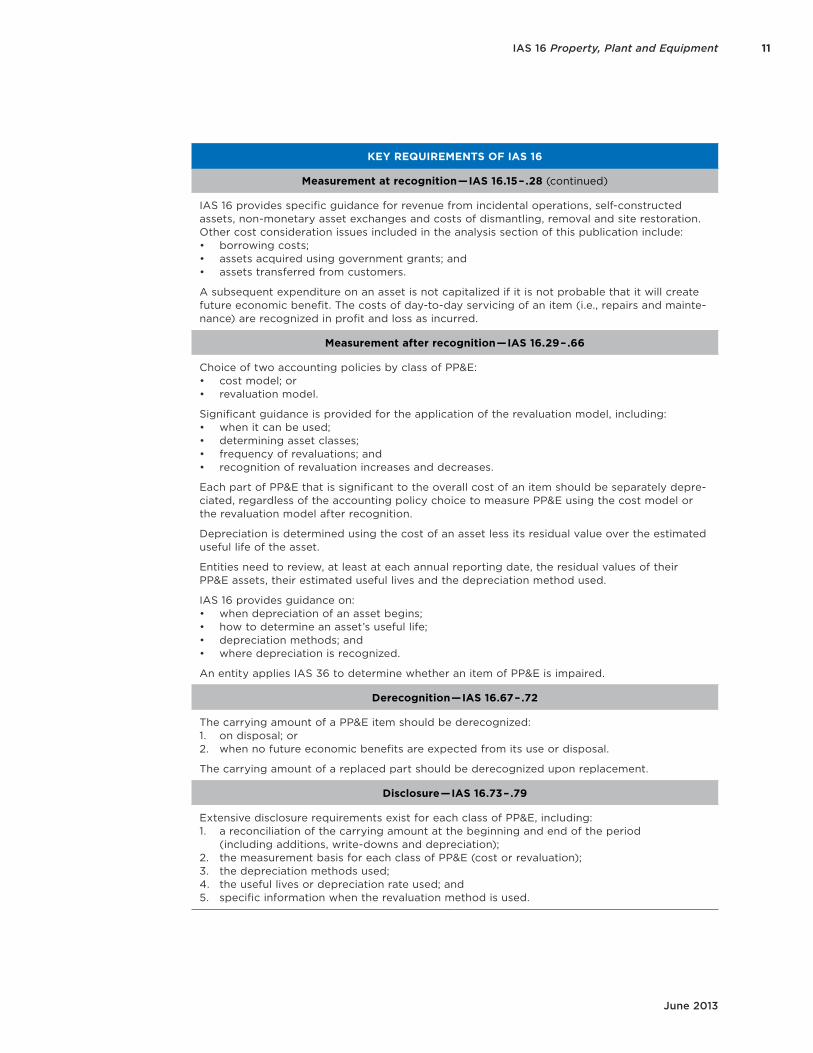

KeY reQUireMenTS OF iaS 16

Scope — iaS 16.2 – .5

Assets Included within the Scope of IAS 16• PP&E, including assets that are carried

at revalued amounts• PP&E used to develop or maintain the

assets shown as excluded from the scope of IAS 16

• measurement of investment property (IAS 40) accounted for using the cost model

• finance leases from the lessee perspective (other than the recognition criteria, which are included in IAS 17)

Assets Excluded from the Scope of IAS 16• PP&E, classified as held for sale (IFRS 5)• PP&E where another standard requires or

permits a different accounting treatment (e.g., investment property (IAS 40))

• intangible assets (IAS 38)• biological assets related to agricultural

activity (e.g., vines used to grow grapes (IAS 41))

• recognition and measurement of explora-tion and evaluation assets (IFRS 6)

• mineral rights and mineral reserves (e.g., oil and natural gas)

recognition — iaS 16.7 – .14

General recognition criteria:1. must be probable that an item of PP&E’s future economic benefits will flow to the entity;

and2. the item of PP&E’s cost can be measured reliably.

Items acquired for safety and environmental reasons, certain spare parts, standby equipment, servicing equipment and major inspection costs are recognized as they enable an entity to obtain future economic benefits from other assets.

Measurement at recognition — iaS 16.15 – .28

An entity considers the IAS 16 recognition criteria for all PP&E costs at the time they are incurred. These costs include costs incurred initially to acquire or construct an item of PP&E and costs incurred subsequently to add to or replace part of PP&E.

An item of PP&E should be recognized at cost, which is the amount of cash or cash equiva-lents paid, or the fair value of other consideration given, to acquire an asset at the time of its acquisition or construction.

There are specific elements to consider when assessing what contributes to the cost of an item of PP&E, particularly when such an item is self-constructed rather than acquired. IAS 16 provides guidance as to what cost elements should be included and those that should be excluded from the cost determination.

11IAS 16 Property, Plant and Equipment

June 2013

KeY reQUireMenTS OF iaS 16

Measurement at recognition — iaS 16.15 – .28 (continued)

IAS 16 provides specific guidance for revenue from incidental operations, self-constructed assets, non-monetary asset exchanges and costs of dismantling, removal and site restoration. Other cost consideration issues included in the analysis section of this publication include:• borrowing costs;• assets acquired using government grants; and• assets transferred from customers.

A subsequent expenditure on an asset is not capitalized if it is not probable that it will create future economic benefit. The costs of day-to-day servicing of an item (i.e., repairs and mainte-nance) are recognized in profit and loss as incurred.

Measurement after recognition — iaS 16.29 – .66

Choice of two accounting policies by class of PP&E:• cost model; or• revaluation model.

Significant guidance is provided for the application of the revaluation model, including:• when it can be used;• determining asset classes;• frequency of revaluations; and• recognition of revaluation increases and decreases.

Each part of PP&E that is significant to the overall cost of an item should be separately depre-ciated, regardless of the accounting policy choice to measure PP&E using the cost model or the revaluation model after recognition.

Depreciation is determined using the cost of an asset less its residual value over the estimated useful life of the asset.

Entities need to review, at least at each annual reporting date, the residual values of their PP&E assets, their estimated useful lives and the depreciation method used.

IAS 16 provides guidance on:• when depreciation of an asset begins;• how to determine an asset’s useful life;• depreciation methods; and• where depreciation is recognized.

An entity applies IAS 36 to determine whether an item of PP&E is impaired.

derecognition — iaS 16.67 – .72

The carrying amount of a PP&E item should be derecognized:1. on disposal; or2. when no future economic benefits are expected from its use or disposal.

The carrying amount of a replaced part should be derecognized upon replacement.

disclosure — iaS 16.73 – .79

Extensive disclosure requirements exist for each class of PP&E, including:1. a reconciliation of the carrying amount at the beginning and end of the period

(including additions, write-downs and depreciation);2. the measurement basis for each class of PP&E (cost or revaluation);3. the depreciation methods used;4. the useful lives or depreciation rate used; and5. specific information when the revaluation method is used.

12 Guide to International Financial Reporting in Canada

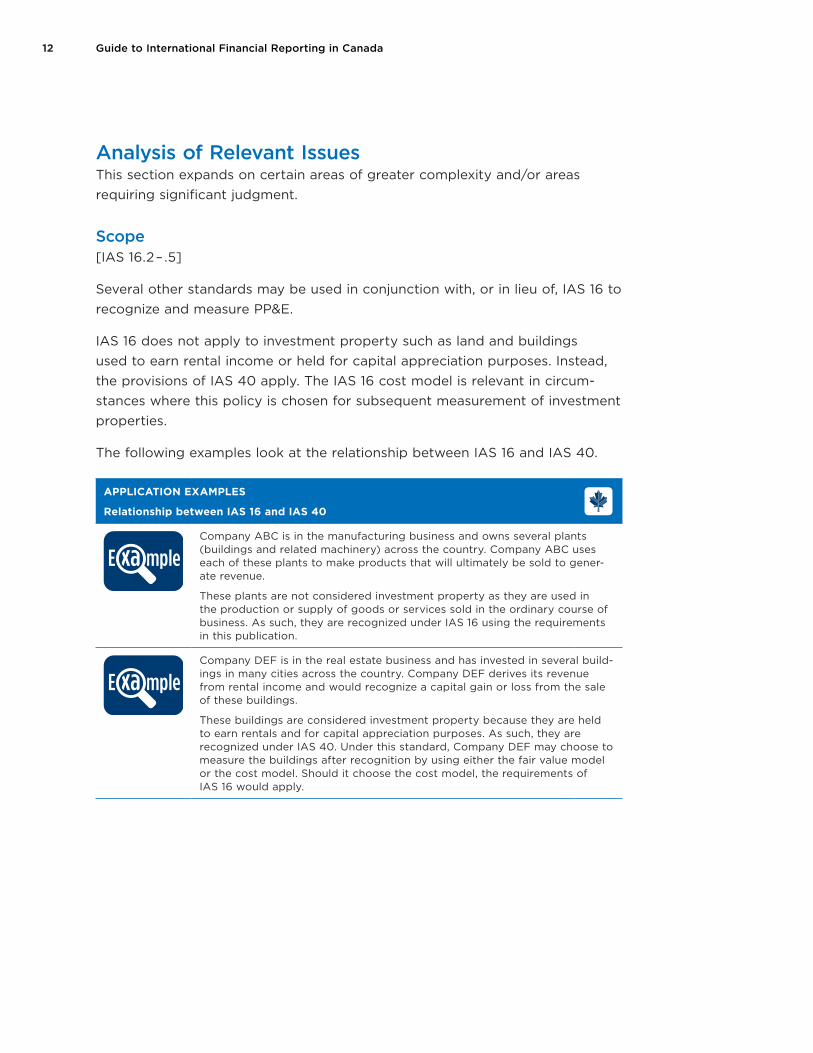

Analysis of Relevant IssuesThis section expands on certain areas of greater complexity and/or areas requiring significant judgment.

Scope[IAS 16.2 – .5]

Several other standards may be used in conjunction with, or in lieu of, IAS 16 to recognize and measure PP&E.

IAS 16 does not apply to investment property such as land and buildings used to earn rental income or held for capital appreciation purposes. Instead, the provisions of IAS 40 apply. The IAS 16 cost model is relevant in circum-stances where this policy is chosen for subsequent measurement of investment properties.

The following examples look at the relationship between IAS 16 and IAS 40.

appliCaTiOn exaMpleS

relationship between iaS 16 and iaS 40

E xa mpleCompany ABC is in the manufacturing business and owns several plants (buildings and related machinery) across the country. Company ABC uses each of these plants to make products that will ultimately be sold to gener-ate revenue.

These plants are not considered investment property as they are used in the production or supply of goods or services sold in the ordinary course of business. As such, they are recognized under IAS 16 using the requirements in this publication.

E xa mpleCompany DEF is in the real estate business and has invested in several build-ings in many cities across the country. Company DEF derives its revenue from rental income and would recognize a capital gain or loss from the sale of these buildings.

These buildings are considered investment property because they are held to earn rentals and for capital appreciation purposes. As such, they are recognized under IAS 40. Under this standard, Company DEF may choose to measure the buildings after recognition by using either the fair value model or the cost model. Should it choose the cost model, the requirements of IAS 16 would apply.

13IAS 16 Property, Plant and Equipment

June 2013

exTraCT 1 — exCerpT FrOM The BriCK lTd. 2012 FinanCial STaTeMenTS

NOTE 3 — SIGNIFICANT ACCOUNTING POLICIES

3.9 Property, plant and equipment (in part)

The Brick Ltd. Notes to the Consolidated Financial Statements December 31, 2012 and December 31, 2011 (thousands of Canadian dollars except for share and per share amounts)

24

it is probable that there will be sufficient taxable profits against which to utilize the benefits of the temporary differences and they are expected to reverse in the foreseeable future.

The carrying amount of deferred tax assets is reviewed at the end of each reporting period and reduced to the extent that it is no longer probable that sufficient taxable profits will be available to allow all or part of the asset to be recovered.

Deferred tax assets and liabilities are measured at the tax rates that are expected to apply in the period in which the liability is settled or the asset realized, based on tax rates (and tax laws) that have been enacted or substantively enacted by the end of the reporting period. The measurement of deferred tax liabilities and assets reflects the tax consequences that would follow from the manner in which the Company expects, at the end of the reporting period, to recover or settle the carrying amount of its assets and liabilities.

Deferred tax assets and liabilities are offset when there is a legally enforceable right to set off income tax assets against income tax liabilities and when they relate to income taxes levied by the same taxation authority and the Company intends to settle its income tax assets and liabilities on a net basis.

3.9 Property, plant and equipment

3.9.1 Recognition and measurement Items of property, plant and equipment are carried at cost less accumulated depreciation and accumulated impairment losses.

Cost includes expenditures directly attributable to the acquisition of the asset and required to establish the asset in working condition given its intended use. Cost also includes expenditures for dismantling and removing items and restoring the site on which they were located, and borrowing costs on qualifying assets. Purchased software and costs directly related to the purchase and installation of such software are capitalized as a component of related equipment when the software is integral to its functionality. Software that is not considered integral to the functionality of equipment is classified as an intangible asset.

When parts of an item of property, plant and equipment have different useful lives, they are accounted for as separate items (major components) of property, plant and equipment.

Gains and losses on disposal of an item of property, plant and equipment are determined by comparing the proceeds from disposal with the carrying amount of property, plant and equipment and are recognized within other income (expense) on the consolidated statements of comprehensive income.

3.9.2 Reclassification to investment property Property, plant and equipment are used in the ordinary course of business in the production or supply of goods or services or for administrative purposes. Investment property is property held to earn rental revenue or for capital appreciation or both. When the use of a property changes from use in the business to investment property, the property’s cost and accumulated depreciation is reclassified from property, plant and equipment to investment property.

The following insight looks at accounting for the right to use land as to whether IAS 16, IAS 17 or IAS 38 applies.

appliCaTiOn inSighTS

purchase of right to use land

Source niFriC

Meeting date September 2012

Insight

The following insights were obtained from “IFRIC — items not taken onto the agenda” report.

issuereason for not adding to the iFriC agenda

In January 2012, the Interpreta-tions Committee received a request to clarify whether the purchase of a right to use land should be accounted for as a:• purchase of property, plant and

equipment;• purchase of an intangible asset;

or• lease of land.

In the fact pattern submitted, the laws and regulations in the juris-diction concerned do not permit entities to own freehold title to land. Instead, entities can purchase the right to exploit or build on land. According to the submitter, there is diversity in practice in the jurisdic-tion on how to account for a land right.

The Interpretations Committee iden-tified characteristics of a lease in the fact pattern considered, in accor-dance with the definition of a lease as defined in IAS 17. The Interpreta-tions Committee noted that a lease could be indefinite via extensions or renewals and, therefore, the exis-tence of an indefinite period does not prevent the ‘right to use’ from qualifying as a lease in accordance with IAS 17. The Interpretations Com-mittee also noted that the lessee has the option to renew the right and that the useful life for depreciation purposes might include renewal periods. Judgement will need to be applied in making the assessment of the appropriate length of the depre-ciation period.

The Interpretations Committee, not-withstanding the preceding observa-tions, noted that the particular fact pattern is specific to one jurisdiction. Consequently, the Interpretations Committee decided not to take this issue onto its agenda.

Details of the issues that have been considered by the IFRIC but not added to its agenda are available online at www.ifrs.org/.

14 Guide to International Financial Reporting in Canada

Recognition of Initial and Subsequent Costs[IAS 16.7 – .14]

IAS 16 does not specifically address what items constitute PP&E but provides general recognition guidance. The costs of an item of PP&E are capitalized only if:1. it is probable that future economic benefits from the item will flow to the

entity; and2. the cost can be reliably measured.

The recognition criteria are based on the IASB’s Conceptual Framework for Financial Reporting.

Judgment may be required to determine whether particular costs qualify for recognition as PP&E in certain circumstances, some of which are outlined in the following sub-sections.

Items Acquired for Safety or Environmental Reasons[IAS 16.11]

IAS 16 provides specific guidance for PP&E acquired for safety or environmen-tal reasons. A distinction is made for such PP&E because these assets generally do not have a direct impact on increasing the future economic benefits of any existing piece of PP&E. They may, however, allow an entity to obtain future economic benefits from its other assets in excess of what it might have derived had it not acquired the safety or environmental PP&E.

appliCaTiOn exaMple

items acquired for safety or environmental reasons

E xa mpleCompany ABC operates in the pharmaceutical industry. To run its plants it must abide by several environmental and chemical safety standards. To do so the company has hired several engineers to develop specific processes that will ensure compliance. It has also acquired specified quality control and monitoring equipment.

This equipment is not necessary for the production of goods and services, yet it is important for ensuring compliance with the environmental and chemical safety standards. The process development costs, as well as the equipment, are capitalized under IAS 16.

15IAS 16 Property, Plant and Equipment

June 2013

Spare Parts, Standby Equipment and Servicing Equipment[IAS 16.8]

Items such as spare parts, standby equipment and servicing equipment are recognized as PP&E when they meet the definition of PP&E. Otherwise, such items are classified as inventory.

exTraCT 2 — exCerpT FrOM SherriTT inTernaTiOnal COrpOraTiOn 2012

FinanCial STaTeMenTS

NOTE 2 — SUMMARy OF SIGNIFICANT ACCOUNTING POLICIES

2.8 Property, plant and equipment (in part)

Plant, equipment and land (in part)

Sherritt International Corporation 13

2.8 Property, plant and equipmentProperty, plant and equipment include capitalized development and pre-production expenditures that are recorded at cost less

accumulated depreciation and accumulated impairment losses. Cost includes expenditures that are directly attributable to the

acquisition of the asset. Also included in the cost of property, plant and equipment are borrowing costs on qualifying capital

projects. These are incurred while construction is in progress and before the commencement of commercial production. Once

construction of an asset is substantially complete and the asset is ready for its intended use, the costs are depreciated.

Plant, equipment and land

Plant, equipment and land includes assets under construction, equipment and processing, refining, power generation and other

manufacturing facilities.

The Corporation recognizes major long-term spare parts and standby equipment as plant, equipment and land when the parts

and equipment are significant and are expected to be used over a period greater than a year, or when the parts and equipment

can be used only in connection with an item of plant, equipment and land. Major inspections and overhauls required at regular

intervals over the useful life of an item of plant, equipment and land are recognized in the carrying amount of the related item if

the inspection or overhaul provides benefit exceeding one year.

Plant and equipment are depreciated using the straight-line method based on estimated useful lives, once the assets are available

for use. Plant and equipment may have components with different useful lives. Depreciation is calculated based on each

individual component’s useful life. New components are capitalized to the extent that they meet the recognition criteria of an

asset. The carrying amount of the replaced component is derecognized, and any gain/loss is included in net earnings (loss). If

the carrying amount of the replaced component is not known, it is estimated based on the cost of the new component less

estimated depreciation. The useful lives of the Corporation’s plant and equipment are as follows:

Buildings and refineries 5 to 40 years

Machinery and equipment 5 to 50 years

Office equipment 3 to 35 years

Fixtures and fittings 3 to 35 years

Assets under construction not depreciated during development period

Mining properties

Mining properties include acquisition costs and development costs related to mines in production, properties under development

and properties held for future development. Ongoing pre-development costs relating to properties held for future development

are expensed as incurred, including property carrying costs, drilling and other exploration costs. Once a project is determined to

be commercially viable, development costs are capitalized. Development costs incurred to access reserves at producing

properties and properties under development are capitalized and are depreciated on a unit-of-production basis over the life of

such reserves. Reserves are measured based on proven and probable reserves.

Oil and gas properties

Oil and gas properties include acquisition costs and development costs related to properties in production, under development

and held for future development. Ongoing pre-development costs relating to properties held for future development are

capitalized as incurred, including exploration costs. Development costs incurred to access reserves at producing properties and

properties under development are capitalized and are depreciated on a unit-of-production basis over the life of such reserves.

Reserves are measured based on proven and probable reserves.

Derecognition

An item of property, plant and equipment is derecognized upon disposal or when no future economic benefits are expected to

arise from the continued use of the asset. Any gain or loss arising on derecognition of the asset (calculated as the difference

between the net disposal proceeds and the carrying amount of the item) is included in net earnings (loss) in the period the item

is derecognized.

Capitalization of borrowing costs

Borrowing costs on funds directly attributable to finance the acquisition, construction or production of a qualifying asset are

capitalized until such time as substantially all the activities necessary to prepare the qualifying asset for its intended use or sale

are complete. A qualifying asset is one that takes a substantial period of time to prepare the asset for its intended use. Where

money borrowed specifically to finance a project is invested to earn interest income, the income generated is also capitalized to

reduce the total capitalized borrowing costs.

Subsequent Costs

Repairs and Maintenance[IAS 16.12]

IAS 16 applies the general recognition criteria to subsequent costs incurred to add to or service a previously recognized PP&E item. A subsequent expendi-ture on an asset is capitalized only when it is probable that it will create future economic benefit. The costs of day-to-day servicing of an item are described as being required for the repair and maintenance of an item of PP&E and these costs are recognized in profit and loss as incurred.

Replacement Parts[IAS 16.13]

Costs incurred subsequently in order to add to, replace part of, or service an item are capitalized if they meet the recognition criteria. In such cases, the standard requires an entity to derecognize the carrying amount of the part that has been replaced. This applies whether or not the replaced item has been separately identified and depreciated since acquisition. If the carrying amount of the replaced part cannot be identified, the cost of the replacement, suitably depreciated, can be used to estimate the carrying amount of the part being replaced and derecognized.

16 Guide to International Financial Reporting in Canada

exTraCT 3 — exCerpT FrOM air Canada 2012 FinanCial STaTeMenTS

NOTE 2 — BASIS OF PRESENTATION AND SUMMARy OF SIGNIFICANT ACCOUNTING

POLICIES

J) Maintenance and repairs (in part)

2012 Consolidated Financial Statements and Notes

10

H) EMPLOYEE PROFIT SHARING PLANS

The Corporation has employee profit sharing plans. Payments are calculated based on full calendar year results and an expense recorded throughout the year as a charge to Wages, salaries and benefits based on the estimated annual payment under the plan.

I) SHARE-BASED COMPENSATION PLANS

Certain employees of the Corporation participate in Air Canada’s Long-Term Incentive Plan, which provides for the grant of stock options and performance share units (“PSUs”), as further described in Note 14. PSUs are notional share units which are exchangeable, on a one-to-one basis, as determined by the Board of Directors based on factors such as the remaining number of shares authorized for issuance under the Long-Term Incentive Plan as described in Note 14, for Air Canada shares, or the cash equivalent. The options and PSUs granted contain both time and performance based vesting features as those further described in Note 14.

The fair value of stock options with a graded vesting schedule is determined based on different expected lives for the options that vest each year, as it would be if the award were viewed as several separate awards, each with a different vesting date, and it is accounted for over the respective vesting period taking into consideration forfeiture estimates. For a stock option award attributable to an employee who is eligible to retire at the grant date, the fair value of the stock option award is expensed on the grant date. For a stock option award attributable to an employee who will become eligible to retire during the vesting period, the fair value of the stock option award is recognized over the period from the grant date to the date the employee becomes eligible to retire. The Corporation recognizes compensation expense and a corresponding adjustment to Contributed surplus equal to the fair value of the equity instruments granted using the Black-Scholes option pricing model taking into consideration forfeiture estimates. Compensation expense is adjusted for subsequent changes in management’s estimate of the number of options that are expected to vest.

Grants of PSUs are accounted for as cash settled instruments as described in Note 14. Accordingly, the Corporation recognizes compensation expense at fair value on a straight line basis over the applicable vesting period, taking into consideration forfeiture estimates. Compensation expense is adjusted for subsequent changes in the fair value of the PSU and management’s current estimate of the number of PSUs that are expected to vest. The liability related to cash settled PSUs is recorded in Other long-term liabilities. Refer to Note 17 for a description of derivative instruments used by the Corporation to hedge the cash flow exposure to PSUs.

Air Canada also maintains an employee share purchase plan. Under this plan, contributions by the Corporation’s employees are matched to a specific percentage by the Corporation. Employees must remain with the Corporation until March 31 of the subsequent year for vesting of the Corporation’s contributions. These contributions are expensed in Wages, salaries, and benefits expense over the vesting period.

J) MAINTENANCE AND REPAIRS

Maintenance and repair costs for both leased and owned aircraft are charged to Aircraft maintenance as incurred, with the exception of maintenance and repair costs related to return conditions on aircraft under operating lease, which are accrued over the term of the lease, and major maintenance expenditures on owned and finance leased aircraft, which are capitalized as described below in Note 2T.

Maintenance and repair costs related to return conditions on aircraft leases are recorded over the term of the lease for the end of lease maintenance return condition obligations within the Corporation’s operating leases, offset by a prepaid maintenance asset to the extent of any related power-by-the-hour maintenance service agreements or any recoveries under aircraft subleasing arrangements. The provision is recorded within Maintenance provisions using a discount rate taking into account the specific risks of the liability over the remaining term of the lease. Interest accretion on the provision is recorded in Other non-operating expense. For aircraft under operating leases which are subleased to third parties, the expense relating to the provision is presented net on the income statement of the amount recognized for any reimbursement of maintenance cost which is the contractual obligation of the sublessee. The reimbursement is recognized when it is virtually certain that reimbursement will be received when the Corporation settles the obligation. Any changes in the maintenance cost estimate, discount rates, timing of settlement or difference in the actual maintenance cost incurred and the amount of the provision is recorded in Aircraft maintenance in the period.

T) Property and equipment (in part)

2012 Consolidated Financial Statements and Notes

13

at the average market price for the period and the difference between the number of shares and the number of shares assumed to be purchased are included in the calculation. The number of shares included with respect to performance-based employee share options and PSUs are treated as contingently issuable shares because their issue is contingent upon satisfying specified conditions in addition to the passage of time. If the specified conditions are met, then the number of shares included is also computed using the treasury stock method unless they are anti-dilutive.

P) CASH AND CASH EQUIVALENTS

Cash and cash equivalents include $218 pertaining to investments with original maturities of three months or less at December 31, 2012 ($356 as at December 31, 2011). Investments include bankers’ acceptances and bankers’ discount notes, which may be liquidated promptly and have original maturities of three months or less.

Q) SHORT-TERM INVESTMENTS

Short-term investments, comprised of bankers’ acceptances and bankers’ discount notes, have original maturities over three months, but not more than one year.

R) RESTRICTED CASH

The Corporation has recorded Restricted cash under Current assets representing funds held in trust by Air Canada Vacations in accordance with regulatory requirements governing advance ticket sales, as well as funds held in escrow accounts relating to Air Canada Vacations credit card booking transactions, recorded under Current liabilities, for certain travel related activities.

Restricted cash with maturities greater than one year from the balance sheet date is recorded in Deposits and other assets. This restricted cash relates to funds on deposit with various financial institutions as collateral for letters of credit and other items.

S) AIRCRAFT FUEL INVENTORY AND SPARE PARTS AND SUPPLIES INVENTORY

Inventories of aircraft fuel and spare parts, other than rotables, and supplies are measured at the lower of cost and net realizable value, with cost being determined using a weighted average formula.

The Corporation did not recognize any write-downs on inventories or reversals of any previous write-downs during the periods presented. Included in Aircraft maintenance is $43 related to spare parts and supplies consumed during the year (2011 – $39).

T) PROPERTY AND EQUIPMENT

Property and equipment is recognized using the cost model. Property under finance leases and the related obligation for future lease payments are initially recorded at an amount equal to the lesser of fair value of the property or equipment and the present value of those lease payments.

The Corporation allocates the amount initially recognized in respect of an item of property and equipment to its significant components and depreciates separately each component. Property and equipment are depreciated to estimated residual values based on the straight-line method over their estimated service lives. Aircraft and flight equipment are componentized into airframe, engine, and cabin interior equipment and modifications. Airframe and engines are depreciated over 20 to 25 years, with 10% to 20% estimated residual values. Cabin interior equipment and modifications are depreciated over the lesser of 5 years or the remaining useful life of the aircraft. Spare engines and related parts (“rotables”) are depreciated over the average remaining useful life of the fleet to which they relate with 10% to 20% estimated residual values. Cabin interior equipment and modifications to aircraft on operating leases are amortized over the term of the lease. Major maintenance of airframes and engines, including replacement spares and parts, labour costs and/or third party maintenance service costs, are capitalized and amortized over the average expected life between major maintenance events. Major maintenance events typically consist of more complex inspections and servicing of the aircraft. All maintenance of fleet assets provided under power-by-the-hour contracts are charged to operating expenses in the income statement as incurred, respectively. Buildings are depreciated on a straight-line basis over their useful lives not exceeding 50 years or the term of any related lease, whichever is less. Leasehold improvements are amortized over the lesser of the lease term or 5 years. Ground and other equipment is depreciated over 3 to 25 years.

exTraCT 4 — exCerpT FrOM SaSKaTChewan TranSpOrTaTiOn COMpanY 2012

FinanCial STaTeMenTS

NOTE 4 — SIGNIFICANT ACCOUNTING POLICIES

c. Property and equipment (in part)

c. Property and equipmentProperty and equipment are recorded at cost less accumulated depreciation and any provisions for impairment. Cost includes expenditure that is directly attributable to the acquisition of the asset. The cost of self-constructed assets includes materials, services, direct labour and directly attributable overheads.

The costs of maintenance, repairs, renewals or replacements which donot extend productive life are charged to operations as incurred. Thecosts of replacements and improvements which extend productive lifeare capitalized. The cost of replacing part of an item of property andequipment is recognized in the carrying amount of the item if it isprobable that the future economic benefits embodied within the partwill flow to the Company and its cost can be measured reliably. Thecarrying amount of the replaced part is derecognized. The costs ofthe day-to-day servicing of property and equipment are recognized intotal comprehensive loss as incurred.

When property and equipment are disposed of or retired, the related costs and accumulated depreciation are eliminated from the accounts. Any resulting gains or losses are reflected in the statement of comprehensive loss for the period.

d. Non-financial assets held for saleNon-financial assets are classified as held for sale if their carryingamount will be recovered principally through a sale transactionrather than through continuing use. This condition is regarded asmet only when the sale is highly probable and the asset is availablefor immediate sale in its present condition. Management must becommitted to the sale, which should be expected to qualify forrecognition as a completed sale within one year from the date ofclassification.

Non-financial assets classified as held for sale are measured at thelower of their previous carrying amount and fair value less costs tosell.

e. Operating grant revenueOperating grants from CIC are recognized as revenue when received.

f. Capital grant revenueCapital grants related to depreciable property are deferred as receivedand are recognized as revenue over the life of the asset. The

Company recognizes a portion of the capital grant as revenue eachyear equivalent to the amount of depreciation recognized on theassets acquired with the grant funds.

Capital grants related to the acquisition of land and related costs are recognized as a direct increase in retained earnings.

g. Depreciation of property and equipmentDepreciation is recorded on buildings, vehicles, and equipment, on the straight-line basis over the estimated productive life of each asset. Depreciation commences when the property and equipment is ready for its intended use. The estimated useful life of property and equipment is based on manufacturer’s guidance, past experience and future expectations regarding the potential for technical obsolescence. The estimated useful lives are reviewed annually and any changes are applied prospectively.

The estimated useful lives of the major classes of property and equipment are as follows:

Buildings 10 - 50 years Vehicles 5 -15 years Other equipment 3 - 10 years

h. Impairment of non-financial assetsAt each reporting date, the Company reviews the carrying amount ofits non-financial assets to determine whether there is any indicationthat those assets have suffered an impairment loss. If any suchindication exists, the recoverable amount of the asset is estimated inorder to determine the extent, if any, of the impairment loss.

The recoverable amount is the higher of fair value less costs to selland value in use. In assessing value in use, the estimated future cashflows are discounted to their present value using a discount rate thatreflects current market assessments of the time value of money andthe risks specific to the asset for which the estimates of future cashflows have not been adjusted.

If the recoverable amount of an asset is estimated to be less than itscarrying amount, the carrying amount of the asset is reduced to itsrecoverable amount. An impairment loss is recognized immediately inthe statement of comprehensive loss.

Notes to Financial Statements (continued)

55Saskatchewan Transportation Company 2012 Annual Report

Major Inspections[IAS 16.14]

To continue operating, certain items of PP&E may require major inspections (for example: aircrafts, ships, etc.). When such major inspections take place, the costs are recognized as a separate component, if the recognition criteria are satisfied and amortized over the period between scheduled inspections. Once a scheduled inspection has taken place, any remaining carrying amount of the cost of the previous inspection (i.e., the unamortized portion) must be derecognized and the new inspection cost capitalized.

17IAS 16 Property, Plant and Equipment

June 2013

exTraCT 5 — exCerpT FrOM BOMBardier inC. 2012 FinanCial STaTeMenTS

NOTE 2 — SUMMARy OF SIGNIFICANT ACCOUNTING POLICIES

Property, plant and equipment (in part)

142

unfunded benefit plans, the benefit obligation, after adjusting for the effects of unrecognized past service costs (credits), is included in retirement benefit liability. Other long-term employee benefits – The accounting method is similar to the method used for defined benefit plans, except that all actuarial gains and losses and past service costs are recognized immediately in income. Other long-term employee benefits are included in other liabilities. Property, plant and equipment PP&E are carried at cost less accumulated amortization and impairment losses. The cost of an item of PP&E includes its purchase price or manufacturing cost, borrowing costs as well as other costs incurred in bringing the asset to its present location and condition. If the cost of certain components of an item of PP&E is significant in relation to the total cost of the item, the total cost is allocated between the various components, which are then separately depreciated over the estimated useful lives of each respective component. The amortization of PP&E is computed on a straight-line basis over the following useful lives: Buildings 5 to 75 years Equipment 2 to 15 years Other 3 to 20 years The amortization method and useful lives are reviewed on a regular basis, at least annually, and changes are accounted for prospectively. The amortization expense and impairments are recorded in cost of sales, SG&A or R&D expenses based on the function of the underlying asset. Amortization of assets under construction begins when the asset is ready for its intended use. When a significant part is replaced or a major inspection or overhaul is performed, its cost is recognized in the carrying amount of the PP&E if the recognition criteria are satisfied, and the carrying amount of the replaced part or previous inspection or overhaul is derecognized. All other repair and maintenance costs are charged to income when incurred. Intangible assets Internally generated intangible assets include development costs (mostly aircraft prototype design and testing costs) and internally developed or modified application software. These costs are capitalized when certain criteria for deferral such as proven technical feasibility are met. The costs of internally generated intangible assets include the cost of materials, direct labour, manufacturing overheads and borrowing costs. Acquired intangible assets include the cost of development activities carried out by vendors for which the Corporation controls the underlying output of the usage of the technology, as well as the cost related to externally acquired licences, patents and trademarks. Intangible assets are recorded at cost less accumulated amortization and impairment losses and include goodwill, aerospace program tooling, as well as other intangible assets such as licenses, patents and trademarks. Other intangible assets are included in other assets.

Measurement at Recognition[IAS 16.15 – .28]

PP&E is initially recognized at cost. Cost is the cash price equivalent or fair value of other consideration given at the recognition date. If payment is deferred beyond normal credit terms, the difference between the cash price equivalent and the total payment is recognized as interest over the period of credit unless such interest is capitalized in accordance with IAS 23. Cost includes all expendi-tures directly attributed to bringing the asset to the location and condition nec-essary for it to be capable of operating in the manner intended by management.

IAS 16 provides guidance on the elements of the cost of an item of PP&E. The following illustration summarizes some elements of the cost of PP&E and some costs that are excluded. Note that this is not meant to be a comprehensive list.

illUSTraTiOn 1 — inClUded and exClUded COSTS OF pp&e

included costs excluded costs

• purchase price, including import duties and non-refundable purchase taxes, after deducting trade discounts and rebates

• costs of site preparation (e.g., surveying, clearing, leveling, grading, and other civil engineering tasks involved in preparing the site for construction)

• initial delivery and handling costs• installation and assembly costs• costs of testing whether the asset is func-

tioning properly, after deducting the net proceeds from selling any items produced while bringing the asset to that location and condition (such as samples produced when testing equipment)

• costs of employee benefits (including share-based payments) arising directly from the acquisition or construction of the PP&E

• professional fees (e.g., legal, architectural, engineering)

• initial estimate of the costs of dismantling and removing the item and restoring the site where it is located to its original con-dition when an obligation to do so exists

• costs of opening a new facility• costs of introducing a new product or

service (including costs of advertising and promotional activities)

• costs of conducting business in a new location or with a new class of customer, including costs of staff training

• administrative and general overhead costs• training costs, including those incurred for

employees who must learn how to oper-ate a new piece of equipment

• costs incurred while an item capable of operating in the manner intended by management has yet to be brought into use or is operated at less than full capacity

• initial operating losses, such as those incurred while demand for the item’s output builds up

• costs of relocating or reorganizing part or all of an entity’s operations

18 Guide to International Financial Reporting in Canada

The following insight looks at costs of testing whether an asset is functioning properly and the treatment of any proceeds before the asset is ready for com-mercial production.

appliCaTiOn inSighTS

Costs of testing

Source niFriC

Meeting date July 2011

Insight

The following insights were obtained from “IFRIC — items not taken onto the agenda” report.

issuereason for not adding to the iFriC agenda

The Interpretations Committee received a request to clarify the accounting for sales proceeds from testing an asset before it is ready for commercial production. The submitted fact pattern is that of an industrial group with several autonomous plants being available for use at different times. This group is subject to regulation that requires it to identify a ‘commercial produc-tion date’ for the whole industrial complex. The question asked of the Committee is whether the proceeds from those plants already in opera-tion can be offset against the costs of testing those plants that are not yet available for use.

The Committee noted that para-graph 17(e) of IAS 16 applies sepa-rately to each item of property, plant and equipment. It also observed that the ‘commercial production date’ referred to in the submission for the whole complex was a different concept from the ‘available for use’ assessment in paragraph 16(b) of IAS 16. The Committee thinks that the guidance in IAS 16 is sufficient to identify the date at which an item of property, plant and equipment is ‘available for use’ and, therefore, is sufficient to distinguish proceeds that reduce costs of testing an asset from revenue from commercial production.

As a result, the Committee does not expect diversity to arise in practice and therefore decided not to add this issue to its agenda.

Details of the issues that have been considered by the IFRIC but not added to its agenda are available online at www.ifrs.org/.

Costs of a Self-Constructed Asset[IAS 16.22]

The costs of a self-constructed asset are determined using the same principles as for an acquired asset. They normally include the direct costs of construct-ing the asset (e.g., the purchase price of raw materials including transportation, handling and other direct costs, and direct labour costs).

19IAS 16 Property, Plant and Equipment

June 2013

If an entity makes similar assets for sale in the normal course of business, the costs of the asset are usually the same as the costs of constructing an asset for sale. Therefore, any internal profits are excluded.

IAS 16 specifically excludes the cost of abnormal amounts of wasted material, labour or other resources incurred in self-constructing an asset.

exTraCT 6 — exCerpT FrOM rOgerS COMMUniCaTiOnS inC. 2012 FinanCial

STaTeMenTS

NOTE 2 — SIGNIFICANT ACCOUNTING POLICIES

(r) Property, plant and equipment: (in part)

(i) Recognition and measurement: (in part)

NO

TE

S T

O C

ON

SO

LIDA

TE

D FIN

AN

CIA

L ST

AT

EM

EN

TS

obligation. Actuarial gains and losses are determined at the endof the year in connection with the valuation of the plans and arerecognized in OCI and retained earnings.

The Company uses the following methods and assumptions forpension accounting associated with its defined benefit plans:

(a) the cost of pensions is actuarially determined and takesinto account the expected rates of salary increases, for instance, as the basis for future benefit increases;

(b) for the purpose of calculating the expected return onplan assets, those assets are valued at fair value; and

(c) past service costs from plan amendments are expensedimmediately in the consolidated statements of income to the extent that they are already vested. Unvested past service costs are deferred and amortized on a straight-line basis over the average remaining vesting period. Contributions to defined contribution plans are recognized as an employee benefit expense in the statement of income in the periods during which related services are rendered by employees.

Contributions to defined contribution plans are recognized as an employee benefit expense in the consolidated statements of income in the periods during which related services are rendered by employees.

(ii) Termination benefits:Termination benefits are recognized as an expense when theCompany is committed without realistic possibility ofwithdrawal, to a formal detailed plan to terminate employmentbefore the normal retirement date.

(r) Property, plant and equipment:(i) Recognition and measurement:Items of PP&E are measured at cost less accumulated depreciation and accumulated impairment losses.

Cost includes expenditures that are directly attributable to theacquisition of the asset. The cost of self-constructed assetsincludes the cost of materials and direct labour, any other costsdirectly attributable to bringing the assets to a workingcondition for their intended use, the costs of dismantling andremoving the items and restoring the site on which they arelocated, and borrowing costs on qualifying assets. Thedetermination of directly attributable costs involves significantmanagement estimates. These estimates include certain directlabour and direct costs associated with the acquisition,construction, development or betterment of the Company’snetwork are capitalized to PP&E, and interest costs which arecapitalized during construction and development of certainPP&E.

The cost of new cable subscriber installation costs are capitalized to cable and wireless network and is depreciated over the useful lives of the related assets. Costs of other cable connections and disconnections are expensed, except for direct incremental installation costs related to reconnect Cable customers, which are deferred to the extent of reconnect installation revenues.

Gains and losses on disposal of an item of PP&E are determinedby comparing the proceeds from disposal with the carryingamount of PP&E, and are recognized within other income in theconsolidated statements of income.

(ii) Depreciation:Depreciation is charged to the consolidated statements of income over the estimated useful lives of the PP&E as follows:Asset Basis Estimated useful life

Buildings Diminishing balance 5 to 25 yearsCable and wireless network Straight-line 3 to 30 yearsComputer equipment and software Straight-line 4 to 10 yearsCustomer premise equipment Straight-line 3 to 5 yearsLeasehold improvements Straight-line Over shorter of estimated

useful life and lease termEquipment and vehicles Diminishing balance 3 to 20 years

Components of an item of PP&E may have different useful lives.The selection of depreciation methods, rates, and useful livesrequires significant estimates that take into account industrytrends and company-specific factors. Depreciation methods, ratesand residual values are reviewed at least annually or when thereare changes in circumstances, and revised if the current method,estimated useful life or residual value is different from thatestimated previously. The effect of such changes is recognized inthe consolidated statements of income prospectively.

Development expenditures are capitalized if they meet thecriteria for recognition as an asset. The assets are amortized overtheir expected useful lives once they are available for use.Research expenditures, as well as maintenance and trainingcosts, are expensed as incurred.

(s) Acquired program rights:Program rights represent contractual rights acquired from thirdparties to broadcast television programs and are carried at cost lessaccumulated amortization. Program rights and the related liabilities

are recorded on the consolidated statements of financial positionwhen the licence period begins and the program is available for useand is amortized to other external purchases in the consolidatedstatements of income over the expected exhibition period, whichranges from one to five years. If programs are not scheduled, therelated program rights are considered impaired and written off.Otherwise, they are subject to non-financial asset impairment testingas intangible assets with finite useful lives. Program rights for multi-year sports programming arrangements are expensed as incurred,when the games are aired.

(t) Goodwill and intangible assets:(i) Goodwill:Goodwill is measured if the fair value of considerationtransferred, including the recognized amount of any non-controlling interest of the acquiree, is greater than the fair valueof the identifiable net assets acquired. If the excess is negative,the difference is recognized immediately in the consolidatedstatements of income.

2012 ANNUAL REPORT ROGERS COMMUNICATIONS INC. 91

Borrowing Costs[IAS 23.1 and .5]

IAS 23 establishes criteria for the recognition of borrowing costs as an element of the carrying amount of a qualifying asset. A qualifying asset is defined in IAS 23 as “an asset that necessarily takes a substantial period of time to get ready for its intended use or sale”. IAS 23 does not provide guidance on what constitutes a substantial period of time. This is a matter of judgment.

An entity must capitalize borrowing costs for qualifying assets that are directly attributable to the acquisition, construction or production of the qualifying asset.

20 Guide to International Financial Reporting in Canada

exTraCT 7 — exCerpT FrOM pOTaSh COrpOraTiOn OF SaSKaTChewan inC.

2012 FinanCial STaTeMenTS

NOTE 5 — PROPERTy, PLANT AND EqUIPMENT

Accounting Policies (in part)

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS In millions of US dollars except as otherwise noted

Note 4 Inventories continued

SUPPORTING INFORMATION

Inventories at December 31 were comprised of:

2012 2011

Finished products $ 417 $ 395Intermediate products 82 98Raw materials 91 91Materials and supplies 172 147

$ 762 $ 731

The following items affected cost of goods sold during the year:

2012 2011 2010

Expensed inventories $ 3,659 $ 3,653 $ 3,087Reserves, reversals and writedowns of inventories 8 8 5

$ 3,667 $ 3,661 $ 3,092

The carrying amount of inventory recorded at net realizable value was $23 at December 31, 2012 (2011 – $7), with the remaining inventory recorded at cost.

NOTE 5 PROPERTY, PLANT AND EQUIPMENT

ACCOUNTING POLICIESProperty, plant and equipment (which include certain mine development costs, pre-stripping costs and assets under construction) are carried at cost (which includes all expenditures directly attributable to bringing the asset to the location and installing it in working condition for its intended use) less accumulated depreciation and any recognized impairment loss. Income or expenses derived from the necessity to bring an asset under construction to the location and condition necessary to be capable of operating in the manner intended is recognized as part of the cost of the asset. The cost of property, plant and equipment is reduced by the amount of related investment tax credits to which the company is entitled. Costs of additions, betterments, renewals and borrowings during construction are capitalized. Borrowing costs directly attributable to the acquisition, construction or production of assets that necessarily take a substantial period of time to ready for their intended use are added to the cost of those assets, until such time as the assets are substantially ready for their intended use. The capitalization rate is based on the weighted average interest rate on all of the company’s outstanding third-party debt. All other borrowing costs are charged through finance costs in theperiod in which they are incurred. Each component of an item of property, plant and equipment with a cost that is significant in relation to the item’s total cost is depreciated separately. When the cost of replacing part of an item of property, plant and equipment is capitalized, the carrying amount of thereplaced part is derecognized. The cost of major inspections and overhauls is

capitalized and depreciated over the period until the next major inspection or

overhaul. Maintenance and repair expenditures that do not improve or extend

productive life are expensed in the period incurred.

Any gain or loss arising on the disposal or retirement of an item of property,

plant and equipment is determined as the difference between the sale

proceeds and the carrying amount of the asset, and is recognized in

operating income.