growth of forex market in india from 1991

TRANSCRIPT

INTRODUCTION

Introduction

• Simultaneous purchase and sale of the currency or the exchange

of one country's currency for the one of another country

• Market in India is traced in the year 1978

• Exchange rate of the rupee is officially determined by RBI

• In 1994, unification of the exchange rate of rupee taken place

based on demand and supply of foreign exchange

• Average daily turnover in global foreign exchange markets is

estimated at $3.98 trillion

Purpose of Foreign Exchange Market

To convert the money of one country into the money of

another country

• To provide the security of the risk against the foreign

exchange

• Banks trade on the foreign exchange market to make

profits,

• The depreciation of a country's currency refers to a decrease in the value of that country's currency.

• The appreciation of a country's currency refers to an increase in the value of that country's currency

PARTICIPANTS AND DERIVATIVES

Participants in Forex market in India

Extent of RBI Intervention in Foreign exchange Market

2.9

3.8

1.5

0.4 0.40.7 0.7

0

0.5

1

1.5

2

2.5

3

3.5

4

2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09P

Foreign Exchange Derivative Instruments in India

Foreign Currency Rupee Swap

Foreign Exchange Forwards

Foreign Currency Rupee Options

Cross-Currency Options

Cross-Currency Swaps

EARLY STAGES

Early Stages

• Par Value System (1947-1971)Bretton Woods System

• Basket Peg (1971-1991)

Foreign Exchange Regulations Act• Enacted -1947 • Placed on permanent basis – 1957

• Reserve Bank

POST LIBERALISATION

Post-Reform period - 1991 onwards

• New economic policy of 1991

• Two-step devaluation of exchange rate by 9% and 11% in 1991 by RBI

• Closing of Pegged-exchange rate

• Rangarajan committee report & Market determined exchange rate

• LERMS and dual-exchange rate system (‘92)

• Convergence of dual rates in ‘93

• Current account convertibility in ‘94

• Sodhani Committee report ’95

• Tarapore committee report ‘97

• Internal Technical group on Forex Markets by RBI 2005

Measures initiated to develop Forex markets in India

• Institutionl framework –

FERA (1973) was replaced by the more market friendly FEMA (1999)

More power to Ads

Setting up of CCIL in 2001 recommended by Sodhani Committee

Increase in instruments in Forex market –

•More rupee-foreign currency swaps

•Additional hedging instruments such asforeign currency-rupee options, cross currency options, interest rate swaps, currency swaps, forward rate agreements (FRAs)

•Liberalization measures –ADs were allowed to trade in overseas markets

•Banks were allowed to:Fix net overnight position limits and gap limits, determine interest rates and maturity period of FCNR(B), use derivative products for asset-liability management

•Forex market participants and FIIs were allowed to transact without any limits

•Foreign exchange earners were permitted to maintain foreign currency accounts

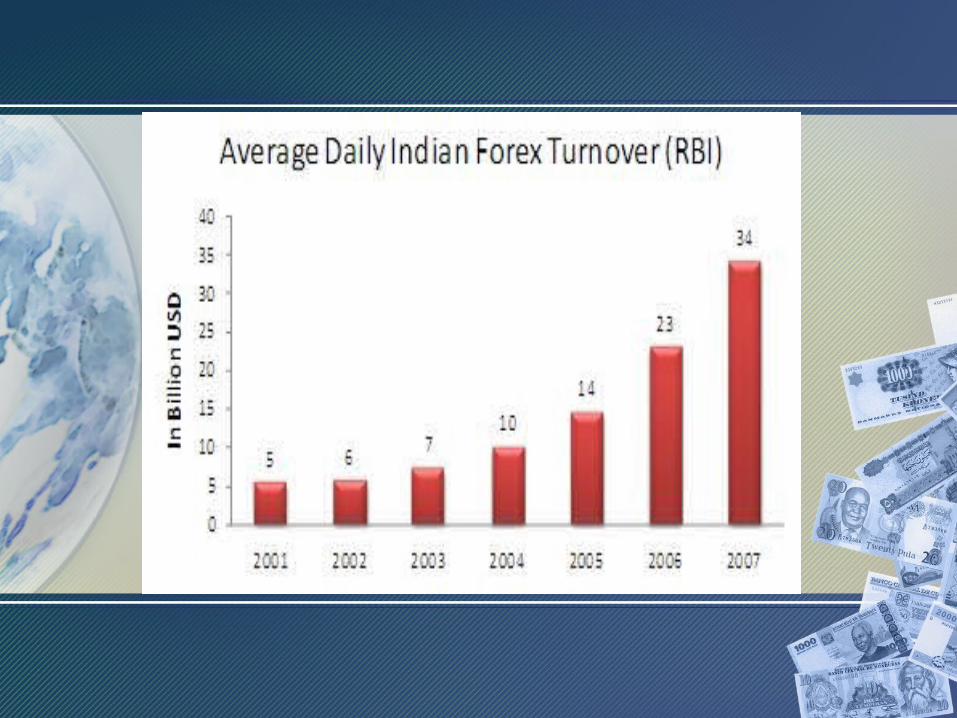

Global forex market turnover

Indian forex market growthItem 1997-98 (bn

USD)2005-06 (bn USD)

2006-07 (bn USD)

Total Annual Turnover

1306 4413 5734

Average Daily Turnover

5 18 23

Average Daily Merchant Turnover

1 5 7

Average Daily inter-bank Turnover

4 13 18

PHASES OF FOREIGN EXCHANGE MARKET POST-

LIBERALIZATION

First Phase of Stability• March 1993 to June 1995

• Stable at 1 USD = Rs. 31.37

• Policy aimed at: boosting exports

building up reserves

• Large FDI inflows & portfolio investments

• RBI purchased major chunk

First Phase of Volatility• August 1995 to March 1996

• Decrease in inflows and strengthening of USD

• Bid-Offer spread widened to 20 paise, 85 paise on some

days

• Two approaches by RBI: Sell in large lots

Continuous sale of small amounts

• Result: Stability at 1 USD = Rs. 34 to 35

Second Phase of Stability• April 1996 to Mid-August 1997

• Rate stable at 1 USD = Rs. 35.50 to 36

• Capital inflows increased again

• Forex reserve losses were recovered soon

Second Phase of Volatility• 2 Significant periods:

Mid-August 1997 to January 1998

May 1998 to August 1998

• South East Asian Crisis; depreciation of rupee by 9%

• Reversible Policy measures undertaken by the Reserve

Bank

Reversible Measures from Nov 1997 to Jan 1998

• CRR : Up from 9.5% to 10% to 10.5%

• Reverse Repo Rate : 4.5% to 6.5% to 7% to 9%

• Interest on Export Credit: Raised from 13% to 15% to

20%

Second Phase of Volatility

• Exchange rate back to 1 USD = Rs. 39.50

• Normalcy returned, policies rolled back

• 2nd Period: May 1998 to August 1998

• Appreciation of USD; Reduction in FIIs and downgrading of India’s

investment outlook

• Rupee falls to 42.50 = 1 USD by June 1998

• Indirect intervention by RBI

• RIBs get $4.2 billion

• Result: Volatility controlled and forex reserve increased

Phase of Relative Stability• September 1998 to March 2003

• Slight pressure during June to October 1999 due to Kargil War

• RBI loosens its kitty for oil imports and government service debts

• IMDs raise Forex reserve to USD 5.5 billion by November 2000

Phase of Surge in Capital Flows

• From 2003 to 2008

• 1 USD = Rs. 38.48 in October 2007

• Large purchasing by RBI to absorb excess supply

• Market Stabilization Scheme (MSS)

• Forex reserves of USD 203.1 billion (April 2007)

• Forex reserves of USD 294.82 billion (March 2012)

CHALLENGES AND CURRENT TRENDS

Challenges• Improvement in Market Infrastructure

• Accounting Standards

• Relaxation of the criteria of underlying for transactions

• Interest Rate Parity

• Reserve Management

• Implications of Global Imbalances

• Managing Exchange Rate Volatility

• Customer Service

• Greater Inter-linkages of Foreign Exchange Market

• with other Segments

Current trend• One of the emerging economies of the world

• Global forex market is presently estimated at USD 3 trillion

• Indian forest market is 16th forex market in the world in terms of daily turnover as the bureau of Indian standards

• 34 billion in 2007

• Reserve Bank of India, officially determined the exchange rate of rupee according to the weighed basket of currencies with the significant business partners of India.

• Open market policy in the year 1991 and implementation of the new economic policy by the Govt. of India

• Introduced LERMS

• Articles of Agreement with the International Monetary Fund

• Introduction of future derivative segment in Forex trading

• The trade of derivative contract at the leading stock exchanges NSE and MCX for three new currency pairs