growth and pattern of expenditure of the central...

TRANSCRIPT

85

CHAPTER 4

Growth and Pattern of Expenditure of the Central Government

Public expenditure is an important instrument of the

fiscal system of a federal nation. The size and pattern of the

public spending has great relevance in the growth process

and in the reduction of economic disparities.

The study of public expenditure was neglected till

1920s because of the belief that all public expenditure was

waste. Infact, this belief was strengthened by the writings of

the classical economists and especially that of Adam Smith

(1776) who advocated that the government should restrict

its activities to “justice, police and arms” (Zahir, 1972).

To J. B. Say, public spending was usually for useless

gratification of the wasteful whims of rulers; also it usually

interfered with the process of the private capital formation

necessary to the development of trade and industry by

draining of funds that otherwise might have been

accumulated by thrifty savers (Newman, 1968). Ricardo, too,

viewed public spending as wasteful because of its possible

effects on private capital formation. On the question of

government’s role, Malthus was also of the view that

public expenditure could be excessive, leading to

“injudicious taxation” or too large a national debt (Newman,

1968).

86

Less extreme but having much in common with

classical views is the position of John Stuart Mill who was

in favour of laissez-faire held that “the business of life is

better performed when those who have an immediate

interest in it are left to take their own course, uncontrolled

either by the mandate of law or the meddling of any public

functioning” (Groves, 1964). Contrary to it, in 1936, Lutz

favoured public expenditure as it directly adds to the

community wealth. He said, “Well run government

commercial enterprises, reforestation and reclamation

projects, and other forms of state business are the most

obvious illustrations. Even the expenditure on ordinary

services may result in the accumulation of certain assets,

such as public buildings, which are a useful addition to the

aggregate of community wealth”.

Keynes, a revolutionary economist, regarded public

expenditure as an exogenous factor which can be utilized as

a policy instrument to stimulate economic growth. Taylor

(1953) favoured public expenditure by saying, “Government

funds may not only help to fill in the troughs of deficiencies

in national income, but under proper circumstances may

generate increase in private spending which constitute

recovery and prosperity” (Taylor, 1953).

R. A. Musgrave, a twentieth century economist,

advocated public expenditure since a government is forced

to do many activities such as: (i) redistributive activities; (ii)

activities to secure a re- allocation of resources; (iii)

87

commercial activities, and stabilizing activities (Chand,

2008).

Governments today incur expenditure in order to fulfill

the following roles in the economy: (a) to correct distortions

of market failures; (b) regulate private activity that might

harm society; (c) provide public goods and services (i.e.,

economic and social infrastructure) and (d) often engage in

production activity (Sattar, 2006). The increased

participation of the government in economic activities has

brought public spending to the forefront among the fiscal

instruments.

Through public expenditure, the government

influences directly or indirectly production, consumption

and distribution of the nation. It thus helps towards the

economic and social development of the society. “It can be

used for stabilization, business cycle inversion, and growth

purposes. It gives rise to positive externalities to economy

and society, the more so through its capital component”

(Piana, 2001).

It is worth noting here that public expenditure has

played significant role in developed as well as

underdeveloped countries. “In the developed economies, the

role of public expenditure consists in preventing cyclical

fluctuations, counteracting a secular tendency towards

stagnation and improving income distribution. Public

expenditure can also be used as a lever to raise the level of

income and employment. However, public expenditure has

88

played threefold role in an underdeveloped economy in: (a)

promoting economic development; (b) redistribution of

income; and (c) balanced regional development” (Zahir,

1972). Public expenditure is also playing an important role

in the development of Indian economy.

Classification of Public Expenditure in India

Classification of Public Expenditure in India is

important because different categories of expenditure (a)

explain the interrelationship between the government sector

and the rest of the economy and (b) reveal the relative size of

different governmental activities in the economy. However,

the Constitution requires revenue and capital expenditures

to be shown separately in the budget. Article 112(2) states:

“The estimates of expenditure embodied in the annual

financial statement shall show separately – (a) the sums

required to meet expenditure charged upon the

Consolidated Fund of India; and (b) the sums required to

meet other expenditure proposed to be made from the

Consolidated Fund of India, and shall distinguish

expenditure on revenue account from other expenditure”.

The same provision is repeated under Article 202

under the State Section. The distinction between revenue

and capital expenditures not only is a constitutional

requirement but also an essential ingredient for policy

formulation and efficient resource allocation (Economic

Survey, 2006-07). Thus it is useful to analyse the various

89

components of public expenditure of central government of

India

Total expenditure of the central government comprises

of revenue and capital expenditure. Revenue expenditure is

expenditure incurred for purposes other than creation of

assets of the central government. In many countries, it is

known as current expenditure (Economic Survey, 2006-07).

On the other hand, those expenditures of the Government

which lead to the reduction in recurring financial liabilities

fall under the category of capital expenditure. Such

expenditures pertain to payments on acquisition of assets

and loans and advances given.

Trends of total expenditure, revenue expenditure and

capital expenditure have been calculated by using semi-

logarithmic trend (Y=abx). Total expenditure of the central

government since 1975-76 has been continuously growing

and revenue expenditure has grown at higher rate as

compared to capital expenditure (as shown in Graph 4.1).

Table 4.1 presents the amount of revenue expenditure,

capital expenditure and total expenditure and the share of

revenue expenditure and capital expenditure in total

expenditure of the central government. Since mid-1970’s,

the main objective of the central government was to give a

concrete shape to the new design of development by

revamping public expenditure policy in the direction of more

employment programmes, rural development and also to

maintain price stability. To achieve this objective, the

90

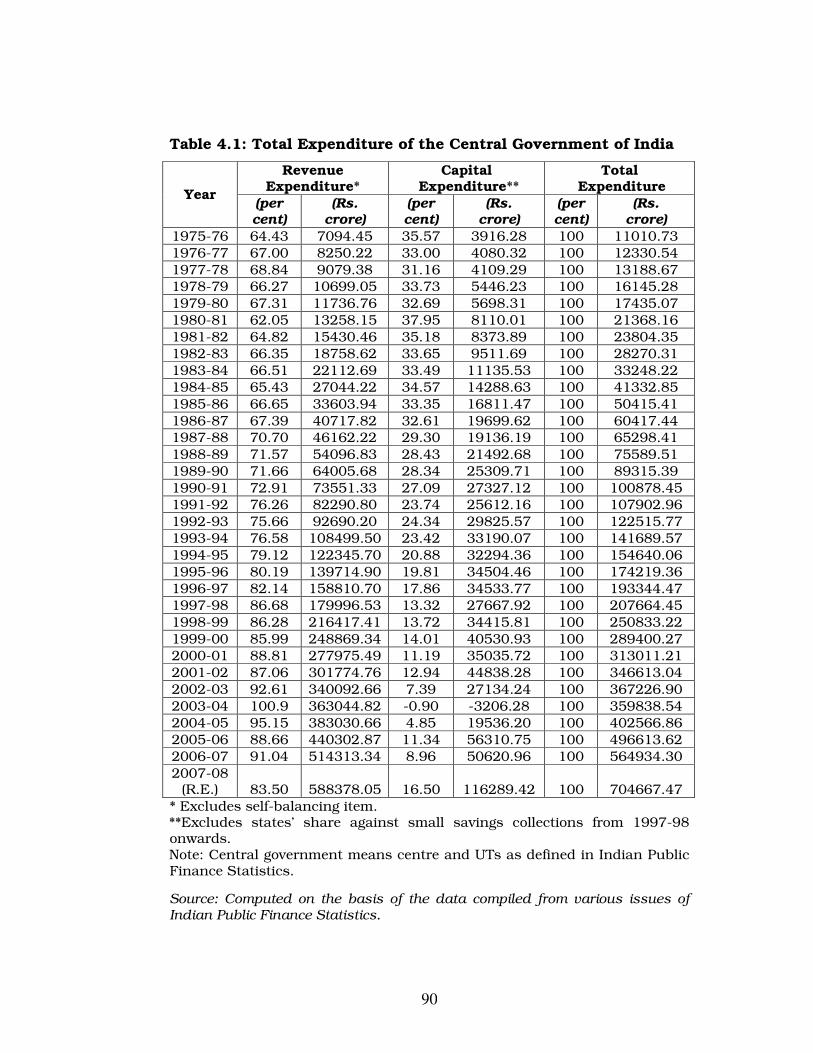

Table 4.1: Total Expenditure of the Central Government of India

Revenue Expenditure*

Capital Expenditure**

Total Expenditure

Year (per cent)

(Rs. crore)

(per cent)

(Rs. crore)

(per cent)

(Rs. crore)

1975-76 64.43 7094.45 35.57 3916.28 100 11010.73 1976-77 67.00 8250.22 33.00 4080.32 100 12330.54 1977-78 68.84 9079.38 31.16 4109.29 100 13188.67 1978-79 66.27 10699.05 33.73 5446.23 100 16145.28 1979-80 67.31 11736.76 32.69 5698.31 100 17435.07 1980-81 62.05 13258.15 37.95 8110.01 100 21368.16 1981-82 64.82 15430.46 35.18 8373.89 100 23804.35 1982-83 66.35 18758.62 33.65 9511.69 100 28270.31 1983-84 66.51 22112.69 33.49 11135.53 100 33248.22 1984-85 65.43 27044.22 34.57 14288.63 100 41332.85 1985-86 66.65 33603.94 33.35 16811.47 100 50415.41 1986-87 67.39 40717.82 32.61 19699.62 100 60417.44 1987-88 70.70 46162.22 29.30 19136.19 100 65298.41 1988-89 71.57 54096.83 28.43 21492.68 100 75589.51 1989-90 71.66 64005.68 28.34 25309.71 100 89315.39 1990-91 72.91 73551.33 27.09 27327.12 100 100878.45 1991-92 76.26 82290.80 23.74 25612.16 100 107902.96 1992-93 75.66 92690.20 24.34 29825.57 100 122515.77 1993-94 76.58 108499.50 23.42 33190.07 100 141689.57 1994-95 79.12 122345.70 20.88 32294.36 100 154640.06 1995-96 80.19 139714.90 19.81 34504.46 100 174219.36 1996-97 82.14 158810.70 17.86 34533.77 100 193344.47 1997-98 86.68 179996.53 13.32 27667.92 100 207664.45 1998-99 86.28 216417.41 13.72 34415.81 100 250833.22 1999-00 85.99 248869.34 14.01 40530.93 100 289400.27 2000-01 88.81 277975.49 11.19 35035.72 100 313011.21 2001-02 87.06 301774.76 12.94 44838.28 100 346613.04 2002-03 92.61 340092.66 7.39 27134.24 100 367226.90 2003-04 100.9 363044.82 -0.90 -3206.28 100 359838.54 2004-05 95.15 383030.66 4.85 19536.20 100 402566.86 2005-06 88.66 440302.87 11.34 56310.75 100 496613.62 2006-07 91.04 514313.34 8.96 50620.96 100 564934.30 2007-08

(R.E.) 83.50 588378.05 16.50 116289.42 100 704667.47 * Excludes self-balancing item. **Excludes states’ share against small savings collections from 1997-98 onwards. Note: Central government means centre and UTs as defined in Indian Public Finance Statistics.

Source: Computed on the basis of the data compiled from various issues of Indian Public Finance Statistics.

91

central government’s total expenditure stepped up to Rs.

50415.41 crore in 1985-86. This sharp increase in the total

expenditure is mainly because of continuous increase of

revenue expenditure which created serious imbalances in

the fiscal sector of the economy. The government undertook

number of measures to strengthen the control over

expenditure such as a large number of anti-poverty

programmes, employment creating activities and

implementation of a system of zero-base budgeting

(Economic Survey, 1986-87). Though top priority was given

by the government to reduce the expenditure but it did not

yield any fruitful results and the expenditure reached to the

level of Rs. 89315.39 crore in 1989-90, out of which 71.66

per cent (or Rs. 64005.68 crore) was revenue expenditure.

The main aspect for sharp increase in revenue expenditure

of the central government from 1975-76 to 1979-80 was the

rapid increase in subsidies. Thereafter, the substantial

increase was due to hike of expenditure on items like

defense , interest payments and grants and loans to States,

UTs on account of relief against drought and other natural

calamities (Economic Survey, 1982-83).

A tremendous increase in the share of expenditure on

revenue account of the central government was accounted

for by the decline in the share of capital expenditure in the

pre-reform period. Capital expenditure moved up from Rs.

3916.28 crore in 1975-76 to Rs. 25309.71 crore in 1989-90

– recorded the growth of 16 per cent per annum in the pre-

92

reform period of fifteen years (Table 4.2). It constituted

Graph 4.1: Trends in Revenue, Capital and Total Expenditure of the

Central Government of India

0

100000

200000

300000

400000

500000

600000

700000

800000

1975-7

6

1977-7

8

1979-8

0

1981-8

2

1983-8

4

1985-8

6

1987-8

8

1989-9

0

1991-9

2

1993-9

4

1995-9

6

1997-9

8

1999-0

0

2001-0

2

2003-0

4

2005-0

6

2007-0

8

Pre-reform period Post-reform period

Rs. cro

re

Revenue Expenditure Capital Expenditure Total Expenditure

Source: Computed on the basis of data compiled from the various issues of Indian Public Finance Statistics. 35.57 per cent of the total expenditure of the central

government in the year 1975-76. This percentage decreased

to 34.57 per cent in 1984-85 and further declined to 28.34

per cent in 1989-90. The share of capital account

expenditure in total expenditure declined by 7 percentage

points in the pre-reform period.

The central government has also taken number of

steps since 1990s to curtail built-in-growth in expenditure

and to bring about structural changes in the composition of

expenditure which include reduction of posts at various

levels, introduction of Expenditure Reforms Commission,

subjecting all existing schemes to zero-base budgeting and

review of all subsidies. Despite these numerous measures

93

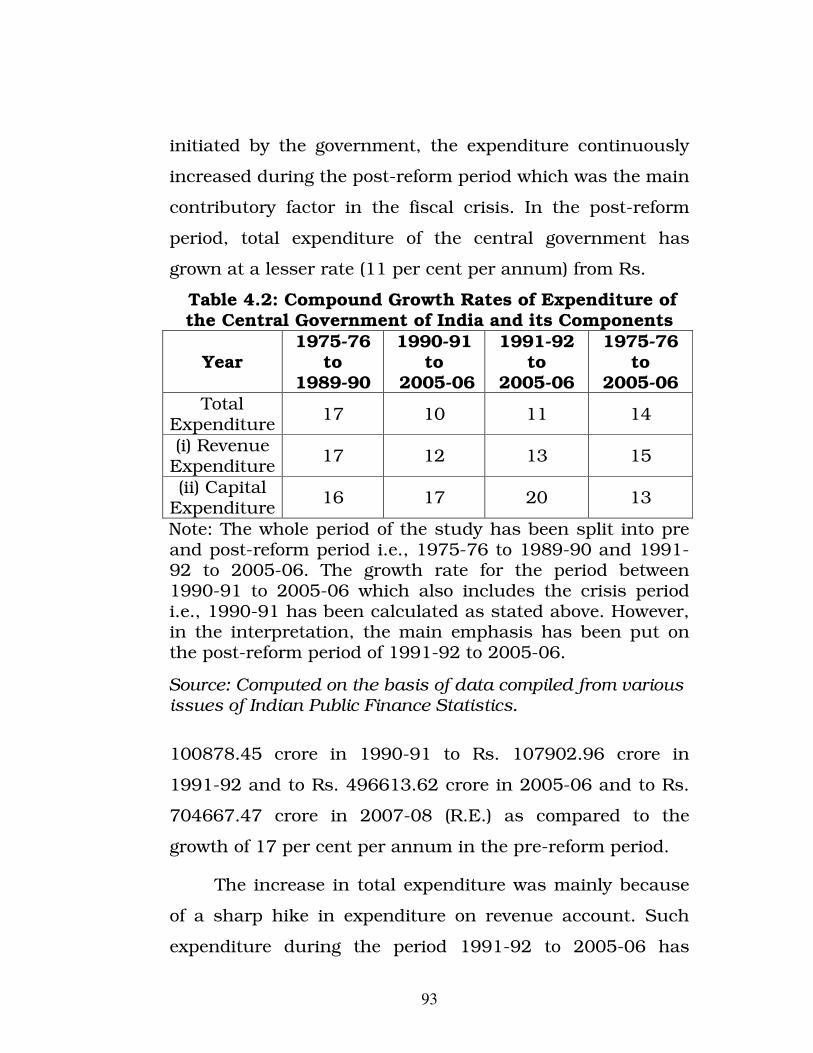

initiated by the government, the expenditure continuously

increased during the post-reform period which was the main

contributory factor in the fiscal crisis. In the post-reform

period, total expenditure of the central government has

grown at a lesser rate (11 per cent per annum) from Rs.

Table 4.2: Compound Growth Rates of Expenditure of the Central Government of India and its Components

Year 1975-76

to 1989-90

1990-91 to

2005-06

1991-92 to

2005-06

1975-76 to

2005-06 Total

Expenditure 17 10 11 14

(i) Revenue Expenditure

17 12 13 15

(ii) Capital Expenditure

16 17 20 13

Note: The whole period of the study has been split into pre and post-reform period i.e., 1975-76 to 1989-90 and 1991-92 to 2005-06. The growth rate for the period between 1990-91 to 2005-06 which also includes the crisis period i.e., 1990-91 has been calculated as stated above. However, in the interpretation, the main emphasis has been put on the post-reform period of 1991-92 to 2005-06.

Source: Computed on the basis of data compiled from various issues of Indian Public Finance Statistics.

100878.45 crore in 1990-91 to Rs. 107902.96 crore in

1991-92 and to Rs. 496613.62 crore in 2005-06 and to Rs.

704667.47 crore in 2007-08 (R.E.) as compared to the

growth of 17 per cent per annum in the pre-reform period.

The increase in total expenditure was mainly because

of a sharp hike in expenditure on revenue account. Such

expenditure during the period 1991-92 to 2005-06 has

94

registered the growth of 13 per cent per annum (from Rs.

82290.8 crore to Rs. 440302.87 crore). It constituted 76.26

per cent in 1991-92 and was as much as 88.81 per cent and

reached to the level of 91.04 per cent of total expenditure in

2000-01 and 2006-07, respectively. This increasing trend

was because of the rise in interest payments and the sharp

escalation in its salary bill (pay and allowances) and pension

payments. Another reason behind this growing share of

public expenditure on revenue account was the measures

designed by the government for the welfare of poor,

especially for those in rural areas. To benefit agricultural

64.43

35.57

68.84

31.16

67.31

32.69

64.82

35.18

66.51

33.49

66.65

33.35

70.70

29.30

71.66

28.34

76.26

23.74

76.58

23.42

80.19

19.81

86.68

13.32

85.99

14.01

87.06

12.94

100.90

-0.90

88.66

11.34

83.50

16.50

-20

0

20

40

60

80

100

120

As p

er cent of Tota

l

19

75-

76

19

77-

78

19

79-

80

19

81-

82

19

83-

84

19

85-

86

19

87-

88

19

89-

90

19

91-

92

19

93-

94

19

95-

96

19

97-

98

19

99-

00

20

01-

02

20

03-

04

20

05-

06

20

07-

08

Pre-reform period Post-reform period

Graph 4.2: Share of Revenue and Capital Expenditure in Total Capital

Expenditure of the Central Government of India

Revenue Expenditure Capital Expenditure

Source: Computed on the basis of data compiled from various issues of Indian Public Finance Statistics. sector like debt relief for agricultural loans up to Rs. 10,000,

introduction of an employment guarantee scheme in

drought prone areas with acute problems of rural

95

unemployment were the measures especially designed by

the government.

It is clearly observed from the Graph 4.2 that revenue

expenditure not only constitutes a significant share of total

expenditure of the central government, but has also

observed an increasing trend. As a result, there is a secular

fall in the share of capital expenditure, which is mirrored in

the rise in the share of revenue expenditure in the post-

reform period too. Capital expenditure of the central

government went up from Rs. 25612.16 crore in 1991-92 to

Rs. 56310.75 crore in 2005-06 - recorded the growth of 20

per cent per annum during the post-reform period. It rose to

Rs. 116289.42 crore in 2007-08 (R.E.). Looking at capital

expenditure as a proportion of total expenditure of the

central government, the share of capital expenditure has

been on the decline in the post-reform period and reached

to 8.96 per cent in 2006-07. This was due to the fact that

expenditure compression was brought about mainly

through cut in capital expenditure. During post-reform

period, the share stepped down by 11 percentage points.

This happened partly because of the cessation of loans from

the central government to states, which were classified as

capital expenditures (Reserve Bank of India Bulletin,

December 2008). So, in spite of all these reforms, the

decline in the share of capital account expenditure is

greater than the decline in this share in pre-reform period.

96

Thus it is clear from the table that the share of revenue

expenditure as compared to the capital expenditure of the

central government remained significantly higher during

1975-76 to 2005-06 and a little improvement as a result of

reform measures has been observed as revenue expenditure

has grown at a lower rate in the post-reform period (13 per

cent per annum) as compared to the pre-reform period (17

per cent per annum). On the other hand, capital

expenditure has recorded a higher growth in the post-reform

period (20 per cent per annum) than the pre-reform period

(16 per cent per annum).

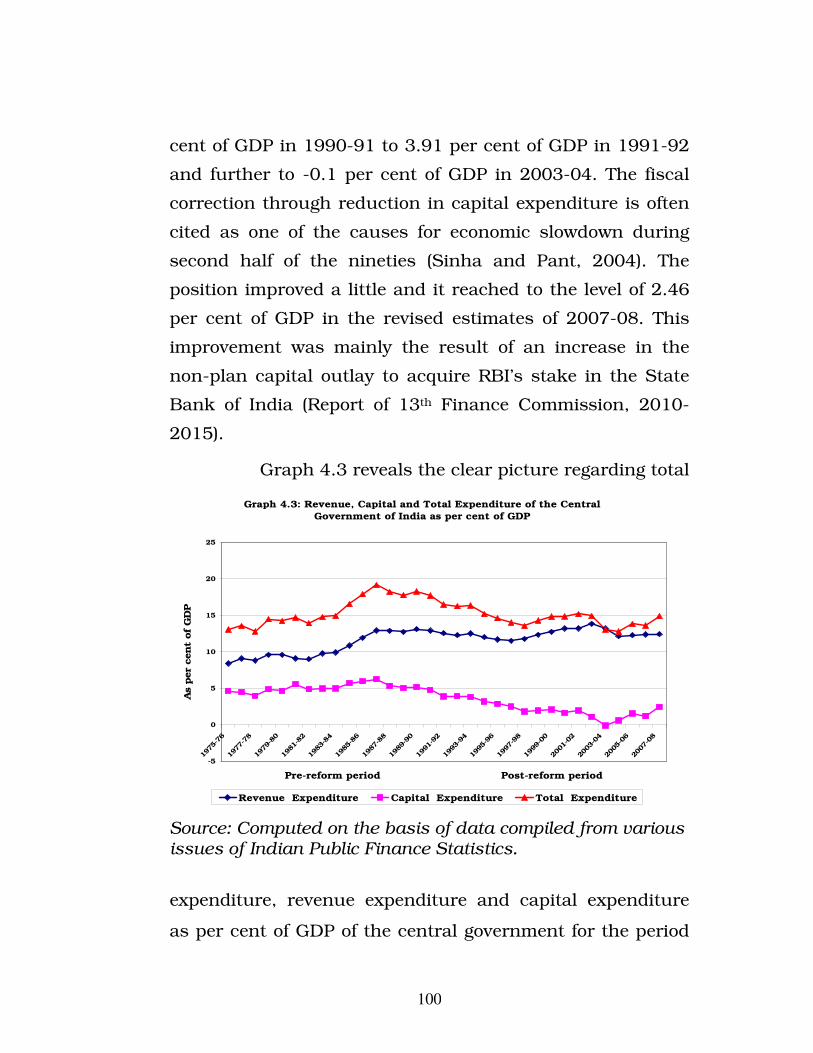

Total expenditure, revenue and capital expenditure of

the central government as per cent of GDP reveal the true

picture of the importance and quality of the expenditure of

this layer of government in Indian federal set-up. Table 4.3

shows that total expenditure of the central government as a

proportion of GDP had risen from 13.07 per cent in 1975-76

to around 20 per cent in the latter half of the 1980s due to

large number of anti-poverty programmes and employment-

creating activities. Besides it, a large part of total

expenditure (over 70 per cent) was accounted for by three

items namely interest payments, defense and subsidies

which had placed a difficult burden on budgetary balances.

This expenditure witnessed some fall relative to GDP in the

first half of the 1990s which was on account of steps taken

by the government in 1994-95. These include reduction of

97

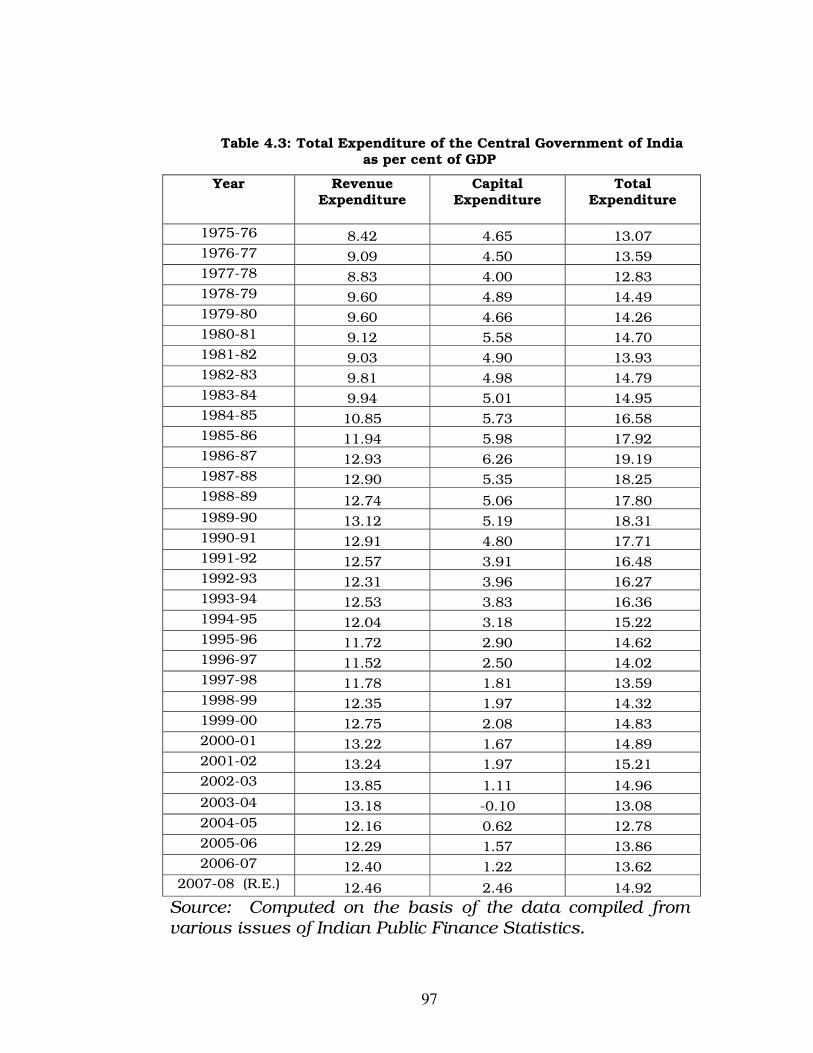

Table 4.3: Total Expenditure of the Central Government of India as per cent of GDP

Year Revenue Expenditure

Capital Expenditure

Total Expenditure

1975-76 8.42 4.65 13.07 1976-77 9.09 4.50 13.59 1977-78 8.83 4.00 12.83 1978-79 9.60 4.89 14.49 1979-80 9.60 4.66 14.26 1980-81 9.12 5.58 14.70 1981-82 9.03 4.90 13.93 1982-83 9.81 4.98 14.79 1983-84 9.94 5.01 14.95 1984-85 10.85 5.73 16.58 1985-86 11.94 5.98 17.92 1986-87 12.93 6.26 19.19 1987-88 12.90 5.35 18.25 1988-89 12.74 5.06 17.80 1989-90 13.12 5.19 18.31 1990-91 12.91 4.80 17.71 1991-92 12.57 3.91 16.48 1992-93 12.31 3.96 16.27 1993-94 12.53 3.83 16.36 1994-95 12.04 3.18 15.22 1995-96 11.72 2.90 14.62 1996-97 11.52 2.50 14.02 1997-98 11.78 1.81 13.59 1998-99 12.35 1.97 14.32 1999-00 12.75 2.08 14.83 2000-01 13.22 1.67 14.89 2001-02 13.24 1.97 15.21 2002-03 13.85 1.11 14.96 2003-04 13.18 -0.10 13.08 2004-05 12.16 0.62 12.78 2005-06 12.29 1.57 13.86 2006-07 12.40 1.22 13.62

2007-08 (R.E.) 12.46 2.46 14.92

Source: Computed on the basis of the data compiled from various issues of Indian Public Finance Statistics.

98

posts at various levels, overall cut on consumption of

petrol/diesel, reduction in expenditure on telephone and

restrictions on purchases of additional vehicles (Economic

Survey, 1994-95). Total expenditure-GDP ratio declined

from 17.71 per cent in 1990-91 to 16.48 per cent in 1991-

92 and further to 13.59 per cent in 1997-98. Consequently,

there was decline in the central government fiscal deficit.

The situation changed with growth in total expenditure

picking up from 1998-99. The compression in total

expenditure witnessed in the first half of the 1990s was

mainly on account of the fall in the capital expenditure-GDP

ratio. In 2001-02, total expenditure was 15.21 per cent of

GDP (13.24 per cent of GDP of revenue expenditure and

1.97 per cent of GDP of capital expenditure) which was

marginally higher than the level in the previous year. While

the level of expenditure is not very high by international

comparison, the main problem in public expenditure

management has been the poor quality outcomes of such

expenditure (Economic Survey, 2004-05). In 2004-05, the

government tried to “check the deterioration in the

composition of expenditure” and also “carried the process of

improving revenue expenditure and increasing capital

expenditure” (Singh, 2008). At the same time, the

compression entirely on non-plan account of revenue

expenditure became the target (Economic Survey, 2004-05).

As such, an important reform undertaken was the

enactment of the FRBM Act in 2003 which became effective

from July 5, 2004. It provides an institutional framework

and binds the government to prudent fiscal policies which

99

facilitated the process of fiscal consolidation. As a result,

the total expenditure fell to 12.78 per cent in 2004-05. But

it began to rise thereafter and reached to 14.92 per cent of

GDP in 2007-08 (R.E.).

Looking at revenue expenditure as per cent of GDP, a

secular rise was noticed. Revenue expenditure rose from

8.42 per cent of GDP in 1975-76 to 13.12 per cent of GDP in

1989-90. Due to continuous attempts since 1991-92,

revenue expenditure-GDP ratio of the central government

could be brought down from 12.57 per cent in 1991-92 to

only by 1.39 per cent points and reached to 11.52 per cent

in 1996-97. This was despite the fact that interest payments

continue to increase (Economic Survey, 1995-96).

Thereafter, fiscal discipline became loose on the expenditure

side of the central government. Revenue expenditure-GDP

ratio increased to 13.85 per cent in 2002-03. Due to the

enactment of the FRBMA in 2003, revenue expenditure of

the central government fell to 12.16 per cent of GDP in

2004-05 from 13.18 per cent of GDP in 2003-04. It again

increased to the level of 12.46 per cent of GDP in 2007-08

(R.E.). It has serious implications for economic growth as

well as for fiscal discipline.

Capital expenditure, on the other hand, hovered

around 4 to 6 per cent of GDP during pre-reform period.

However, the fiscal crisis of 1990-91 had its impact on the

total expenditure of the central government in the 1990s.

Infact, the expenditure cut of the nineties could be affected

at the cost of capital expenditure. It declined from 4.8 per

100

cent of GDP in 1990-91 to 3.91 per cent of GDP in 1991-92

and further to -0.1 per cent of GDP in 2003-04. The fiscal

correction through reduction in capital expenditure is often

cited as one of the causes for economic slowdown during

second half of the nineties (Sinha and Pant, 2004). The

position improved a little and it reached to the level of 2.46

per cent of GDP in the revised estimates of 2007-08. This

improvement was mainly the result of an increase in the

non-plan capital outlay to acquire RBI’s stake in the State

Bank of India (Report of 13th Finance Commission, 2010-

2015).

Graph 4.3 reveals the clear picture regarding total

Graph 4.3: Revenue, Capital and Total Expenditure of the Central

Government of India as per cent of GDP

-5

0

5

10

15

20

25

1975

-76

1977

-78

1979

-80

1981

-82

1983

-84

1985

-86

1987

-88

1989

-90

1991

-92

1993

-94

1995

-96

1997

-98

1999

-00

2001

-02

2003

-04

2005

-06

2007

-08

Pre-reform period Post-reform period

As p

er

cent

of G

DP

Revenue Expenditure Capital Expenditure Total Expenditure

Source: Computed on the basis of data compiled from various issues of Indian Public Finance Statistics.

expenditure, revenue expenditure and capital expenditure

as per cent of GDP of the central government for the period

101

1975-76 to 2007-08. Revenue expenditure as per cent of

GDP was not only high and continuously growing in the pre-

reform period but the gap between revenue expenditure and

capital expenditure started widening in the mid-eighties.

During the post-reform period, no doubt, it has followed a

stable path but has not only much higher than capital

expenditure and the gap between these two widened

extremely up to mid-2000s.

Composition of Revenue Expenditure

Revenue expenditure is classified into non-

developmental expenditure, developmental expenditure and

statutory grants to states. Non-developmental expenditure

consists of expenditure on administration and defense and

also payment of interests. Developmental expenditure

consists of expenditure on social and community services

such as education and health and on economic services

such as agriculture, industry, power, transportation and

communication.

When we categorize revenue expenditure into

developmental and non-developmental categories, it has

been observed that expenditure in both of these categories

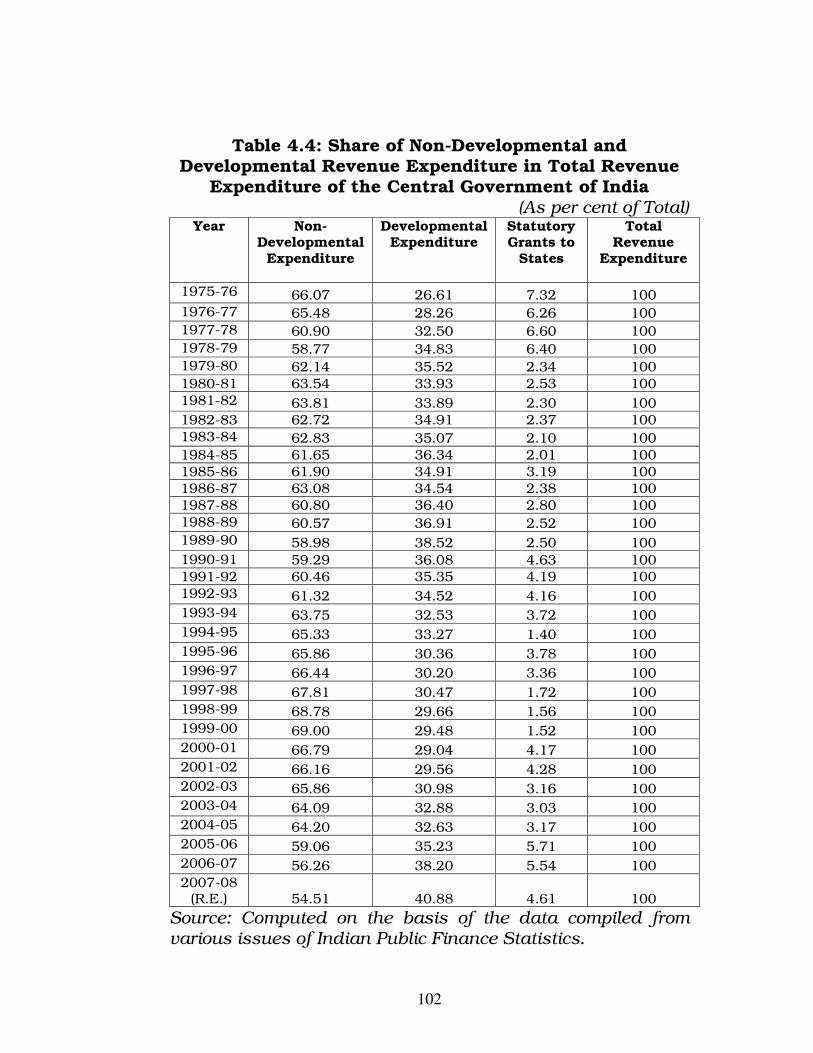

has increased during the period under study (Table 4.4).

From the share of non-developmental and developmental

revenue expenditure in total revenue expenditure of the

central government, it can be observed that non-

developmental revenue expenditure contributes a significant

102

Table 4.4: Share of Non-Developmental and Developmental Revenue Expenditure in Total Revenue

Expenditure of the Central Government of India (As per cent of Total)

Year Non-Developmental

Expenditure

Developmental Expenditure

Statutory Grants to

States

Total Revenue

Expenditure

1975-76 66.07 26.61 7.32 100 1976-77 65.48 28.26 6.26 100 1977-78 60.90 32.50 6.60 100 1978-79 58.77 34.83 6.40 100 1979-80 62.14 35.52 2.34 100 1980-81 63.54 33.93 2.53 100 1981-82 63.81 33.89 2.30 100 1982-83 62.72 34.91 2.37 100 1983-84 62.83 35.07 2.10 100 1984-85 61.65 36.34 2.01 100 1985-86 61.90 34.91 3.19 100 1986-87 63.08 34.54 2.38 100 1987-88 60.80 36.40 2.80 100 1988-89 60.57 36.91 2.52 100 1989-90 58.98 38.52 2.50 100 1990-91 59.29 36.08 4.63 100 1991-92 60.46 35.35 4.19 100 1992-93 61.32 34.52 4.16 100 1993-94 63.75 32.53 3.72 100 1994-95 65.33 33.27 1.40 100 1995-96 65.86 30.36 3.78 100 1996-97 66.44 30.20 3.36 100 1997-98 67.81 30.47 1.72 100 1998-99 68.78 29.66 1.56 100 1999-00 69.00 29.48 1.52 100 2000-01 66.79 29.04 4.17 100 2001-02 66.16 29.56 4.28 100 2002-03 65.86 30.98 3.16 100 2003-04 64.09 32.88 3.03 100 2004-05 64.20 32.63 3.17 100 2005-06 59.06 35.23 5.71 100 2006-07 56.26 38.20 5.54 100 2007-08

(R.E.) 54.51 40.88 4.61 100

Source: Computed on the basis of the data compiled from various issues of Indian Public Finance Statistics.

103

proportion of the total revenue expenditure of the central

government (as shown in Graph 4.4). Throughout the period

covered by the study, the share of non-developmental

revenue expenditure was more than developmental revenue

expenditure of the centre and has remained 60 to 70 per

cent. The share for most of the years of non-developmental

revenue expenditure of the central government fell down to

58.77 per cent in 1978-79 from 66.07 per cent in 1975-76.

The share of non-developmental revenue expenditure rose to

62.14 per cent in 1979-80. An important factor responsible

for this was the increasing interest burden on the budget

(Economic Survey, 1980-81). Thereafter, this expenditure

category indicates roughly a stable and a high share in the

pre-reform period. During post-reform period, non-

developmental revenue expenditure of the central

government raised from Rs. 43614.83 crore in 1990-91 to

Rs. 49754.40 crore in 1991-92 and further to Rs.

320739.25 crore in 2007-08 (R.E.). The share of non-

developmental revenue expenditure in total revenue

expenditure increased from 59.29 per cent in 1990-91 to

60.46 per cent in 1991-92 and to 69 per cent in 1999-00. It

was only in the twenty first century that the non-

developmental revenue expenditure’s share in total revenue

expenditure began to fall. In 2001-02, it fell to 66.16 per

cent of total revenue expenditure, to 64.2 per cent in 2004-

05 and 54.51 per cent in 2007-08 (R.E.). The reason behind

this fall was the significant measures introduced by the

104

government. One among them was regarding pension

reforms. A new pension programme based on defined

contributions was envisaged for those entering central

government services after October 1, 2001 (Economic

Survey, 2001-02).

Further, developmental revenue expenditure increased

from Rs. 1888.1 crore in 1975-76 (26.61 per cent) to Rs.

4168.96 crore in 1979-80 (35.52 per cent) and it was due to

66.07

26.61

7.32

60.90

32.50

6.60

62.14

35.52

2.34

63.81

33.89

2.30

62.83

35.07

2.10

61.90

34.91

3.19

60.80

36.40

2.80

58.98

38.52

2.50

60.46

35.35

4.19

63.75

32.53

3.72

65.86

30.36

3.78

67.81

30.47

1.72

69.00

29.48

1.52

66.16

29.56

4.28

64.09

32.88

3.03

59.06

35.23

5.71

54.51

40.88

4.61

0

10

20

30

40

50

60

70

80

90

100

As p

er

cen

t o

f T

ota

l

19

75-

76

19

77-

78

19

79-

80

19

81-

82

19

83-

84

19

85-

86

19

87-

88

19

89-

90

19

91-

92

19

93-

94

19

95-

96

19

97-

98

19

99-

00

20

01-

02

20

03-

04

20

05-

06

20

07-

08

Pre-reform period Post-reform period

Graph 4.4: Share of Non-developmental and Developmental Revenue

Expenditure in Total Revenue Expenditure of the Central Government

of India

Non-Developmental Revenue Expenditure Developmental Revenue Expenditure Statutory Grants to States

Source: Computed on the basis of data compiled from various issues of Indian Public Finance Statistics.

the sharp increase in subsidies. Thereafter, there was

reduction in the share of developmental revenue

105

expenditure in total revenue expenditure to 33.93 per cent

in 1980-81. This was achieved due to reduction in the

subsidies of fertilizers. Its share further rose to 38.52 per

cent in 1989-90. The major components which contributed

to this increase were defense and interest payments. On the

other hand, developmental revenue expenditure, as a

proportion of total revenue expenditure, has observed a

declining trend till 2000-01 but thereafter it has been

showing a positive trend around 34-35 per cent during post-

reform period.

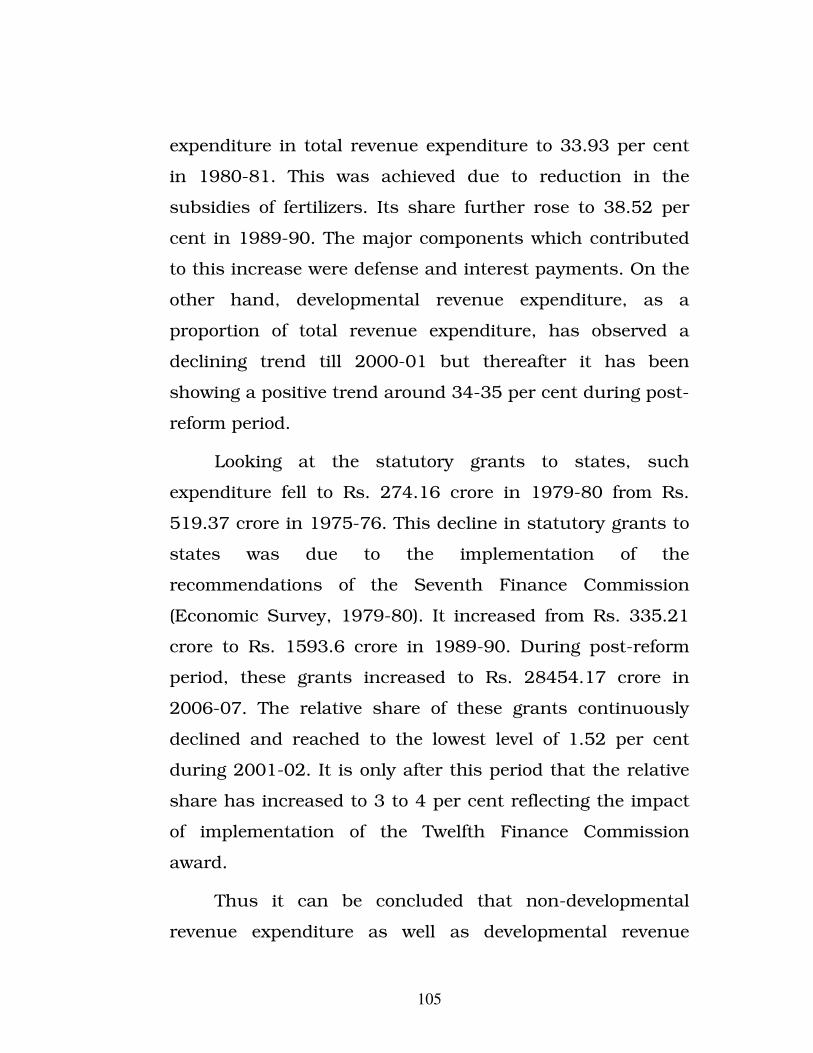

Looking at the statutory grants to states, such

expenditure fell to Rs. 274.16 crore in 1979-80 from Rs.

519.37 crore in 1975-76. This decline in statutory grants to

states was due to the implementation of the

recommendations of the Seventh Finance Commission

(Economic Survey, 1979-80). It increased from Rs. 335.21

crore to Rs. 1593.6 crore in 1989-90. During post-reform

period, these grants increased to Rs. 28454.17 crore in

2006-07. The relative share of these grants continuously

declined and reached to the lowest level of 1.52 per cent

during 2001-02. It is only after this period that the relative

share has increased to 3 to 4 per cent reflecting the impact

of implementation of the Twelfth Finance Commission

award.

Thus it can be concluded that non-developmental

revenue expenditure as well as developmental revenue

106

expenditure of the central government has been growing.

But the share of non-developmental revenue expenditure

has remained greater than developmental revenue

expenditure. Even during the post-reform period, the share

of developmental revenue expenditure declined till 2000-01.

It is only recently that no doubt the share of non-

developmental revenue expenditure is greater but is

declining and the share of developmental expenditure is

increasing.

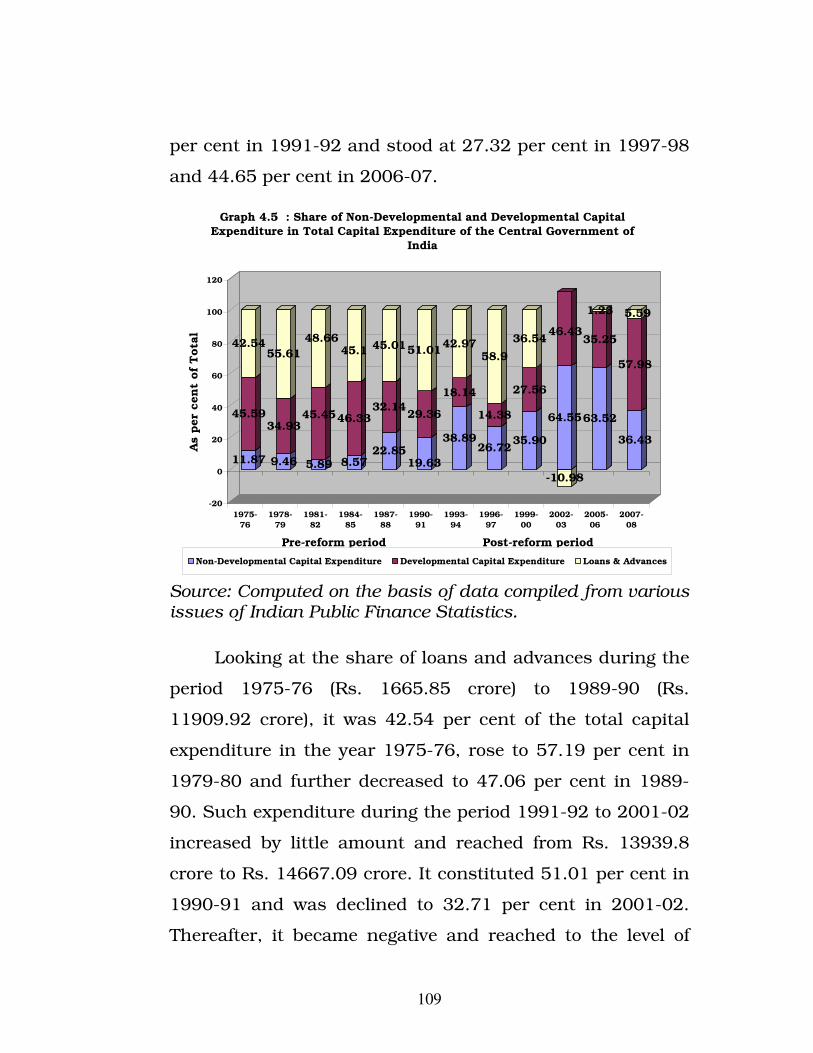

Composition of Capital Expenditure

Capital expenditure is incurred on capital projects

both of a non-development and development nature. It also

includes loans and advances to states and other bodies.

Table 4.5 displays the components of capital

expenditure of the central government. Except the year

2003-04, there has been significant rise in the total capital

expenditure during the study period. The share of

developmental capital expenditure has remained more than

non-developmental capital expenditure out of total capital

expenditure of the central government in the pre-reform

period, but the situation reversed in the post-reform period

(as shown in Graph 4.5). Non-developmental capital

expenditure of the centre increased from Rs. 464.95 crore in

1975-76 to Rs. 5241.38 crore in 1989-90. Its share

as a proportion of total capital expenditure has shown a

107

Table 4.5: Share of Non-Developmental and Developmental Capital Expenditure in Total Capital Expenditure of the Central

Government of India (As per cent of Total)

Year

Non-Developmental

Expenditure

Developmental Expenditure

Loans and Advances

Total Capital

Expenditure

1975-76 11.87 45.59 42.54 100 1976-77 7.43 37.91 54.66 100 1977-78 6.37 48.20 45.43 100 1978-79 9.46 34.93 55.61 100 1979-80 5.08 37.73 57.19 100 1980-81 11.38 37.73 50.89 100 1981-82 5.89 45.45 48.66 100 1982-83 7.62 43.46 48.92 100 1983-84 12.31 44.05 43.64 100 1984-85 8.57 46.33 45.10 100 1985-86 9.64 40.90 49.46 100 1986-87 13.07 39.70 47.23 100 1987-88 22.85 32.14 45.01 100 1988-89 22.30 30.46 47.24 100 1989-90 20.71 32.23 47.06 100 1990-91 19.63 29.36 51.01 100 1991-92 27.15 27.17 45.68 100 1992-93 42.61 24.06 33.33 100 1993-94 38.89 18.14 42.97 100 1994-95 21.87 24.28 53.85 100 1995-96 32.88 15.51 51.61 100 1996-97 26.72 14.38 58.90 100 1997-98 36.02 27.32 36.66 100 1998-99 48.92 23.14 27.94 100 1999-00 35.90 27.56 36.54 100 2000-01 40.58 31.84 27.58 100 2001-02 39.82 27.47 32.71 100 2002-03 64.55 46.43 -10.98 100 2003-04 -629.00 -472.00 1201.00 100 2004-05 179.20 92.21 -171.41 100 2005-06 63.52 35.25 1.23 100 2006-07 72.48 44.65 -17.13 100 2007-08

(R.E.) 36.43 57.98 5.59 100

Source: Computed on the basis of the data compiled from various issues of Indian Public Finance Statistics.

108

fluctuating trend. It was 11.87 per cent in 1975-76 and

reached to 8.57 per cent in 1984-85 and climbed to 20.71

per cent in 1989-90. During the post-reform period, it rose

from Rs. 5364.08 crore in 1991-92 to Rs. 42370.83 crore in

2007-08 (R.E.). To curtail this high growth rate of non-

developmental capital expenditure, the government

undertook various reforms on this front very late with the

beginning of the process of downsizing government. These

included abolishing of four-secretary level posts in April 1,

1999, introduction of Expenditure Reforms Commission in

February 29, 2000 and ban on creation of new posts for one

year in 2000-01 but even then the share of non-

developmental expenditure remained very high. As a

proportion of total capital expenditure, the share of non-

developmental capital expenditure went up to 72.48 per

cent in 2006-07.

Further, developmental capital expenditure increased

from Rs. 1785.48 crore in 1975-76 to Rs. 8158.41 crore in

1989-90. The share of developmental capital expenditure in

total capital expenditure increased continuously till 1984-85

which was 46.33 per cent. Thereafter, the share of

developmental capital expenditure decreased to 30.46 per

cent in 1988-89. During post-reform period, developmental

capital expenditure which stood at Rs. 6958.08 crore in

1991-92 galloped to Rs. 22602.49 crore in 2006-07. As a

proportion of total capital expenditure, its share was 27.17

109

per cent in 1991-92 and stood at 27.32 per cent in 1997-98

and 44.65 per cent in 2006-07.

11.87

45.59

42.54

9.46

34.93

55.61

5.89

45.45

48.66

8.57

46.33

45.1

22.85

32.14

45.01

19.63

29.36

51.01

38.89

18.14

42.97

26.72

14.38

58.9

35.90

27.56

36.54

64.55

46.43

-10.98

63.52

35.25

1.23

36.43

57.98

5.59

-20

0

20

40

60

80

100

120

As p

er

cen

t of

Tota

l

1975-

76

1978-

79

1981-

82

1984-

85

1987-

88

1990-

91

1993-

94

1996-

97

1999-

00

2002-

03

2005-

06

2007-

08

Pre-reform period Post-reform period

Graph 4.5 : Share of Non-Developmental and Developmental Capital Expenditure in Total Capital Expenditure of the Central Government of

India

Non-Developmental Capital Expenditure Developmental Capital Expenditure Loans & Advances

Source: Computed on the basis of data compiled from various issues of Indian Public Finance Statistics.

Looking at the share of loans and advances during the

period 1975-76 (Rs. 1665.85 crore) to 1989-90 (Rs.

11909.92 crore), it was 42.54 per cent of the total capital

expenditure in the year 1975-76, rose to 57.19 per cent in

1979-80 and further decreased to 47.06 per cent in 1989-

90. Such expenditure during the period 1991-92 to 2001-02

increased by little amount and reached from Rs. 13939.8

crore to Rs. 14667.09 crore. It constituted 51.01 per cent in

1990-91 and was declined to 32.71 per cent in 2001-02.

Thereafter, it became negative and reached to the level of

110

17.13 per cent in 2006-07 because of Debt Consolidation

and Debt Waiver Schemes for the state governments started

by the central government.

After a look at the trends in expenditure at the central

level in the end, it is concluded that total expenditure of the

central government has been rapidly growing and it

increased at the rate of 14 per cent per annum throughout

the study period. This sharp increase has been mainly on

account of continuous increase in the share of revenue

expenditure which created serious fiscal imbalance in the

fiscal sector of the economy. What is more disturbing is that

revenue expenditure shot up at the cost of capital

expenditure. Besides it, as a result of reform measures,

revenue expenditure has grown at a lower rate in the post-

reform period than the pre-reform period. On the other

hand, capital expenditure has recorded a higher growth in

the post-reform period than the pre-reform period. As a

proportion of GDP, total expenditure of the central

government increased from 12 to 18 per cent in the pre-

reform period but again declined to 12 per cent by mid-2000

in the post-reform period. Revenue expenditure as per cent

of GDP was not only high and continuously growing in the

pre-reform period but the gap between revenue expenditure

and capital expenditure started widening in the mid-

eighties. During the post-reform period, no doubt, it has

followed a stable path but has not only much higher than

111

capital expenditure and the gap between these two widened

extremely up to mid-2000s.

While analyzing the components of revenue

expenditure, it can be observed that non-developmental

revenue expenditure contributes a significant proportion

(more than 60 per cent) of total revenue expenditure of the

central government. With the significant measures

introduced by the government, only during 2000s, the share

of growth of non-developmental revenue expenditure has

started declining in the post-reform. Looking at the share of

non-developmental and developmental capital expenditure

in total capital expenditure of the central government, it is

observed that the share of developmental capital

expenditure has remained more than non-developmental

capital expenditure in the pre-reform period, but this

situation has been reversed in the post-reform period. It

may thus be concluded that there is a need to give more

emphasis in the reform process on improvement in the

composition of revenue expenditure as well as of capital

expenditure.