grow deposits with fis digital account creationempower.fisglobal.com/rs/134-vdf-014/images/1106-grow...

TRANSCRIPT

Grow Deposits with FIS Digital Account Creation

April 11, 2017Lynn Jordan

Institutions are challenged with:

• Protecting customers from the

emerging threat landscape

• Providing tailored, personalized experiences

• Delivering on expectations for real-time

• Creating data-driven connections and

value across converged channels

• Driving new revenue streams

• Increasing engagement and loyalty

Expectations are rising

The Competitive

Landscape Is Changing

2

Drive Innovation and Expand Digital Capabilities

Grow Sales and Increase Engagement

Enhance Security and Reduce Fraud

Expand Real-time Offerings

Enable Data-driven Marketing and Analytics

Create Operational Efficiencies

Our VisionProvide industry-leading digital solutions that keep our clients

competitive and relevant with the top financial institutions

3

FIS Digital Drives Growth

102%CARDLESS CASH

136%PEOPLE PAY (P2P)

28%CHECK DEPOSIT

80M+DIGITAL USERS *

Annual Growth

*Includes Mobile, Online and ePayments Clients (Q3 2016)

4

• Account Creation: a deposit acquisition platform for

the digital channels

• FIS client perspective: client panelists

– Vilmarie Gaud, Vice President, Product Development Director

Popular Community Bank, Popular Direct

– Curt Trizzino, Retail Product Management

The Private Bank

• Discussion

Grow Deposits with Digital Account Creation

5

Over 50% of Consumers Use Digital Channels to Open Deposit Accounts

Consumers who shop in digital channels, expect financial institutions to provide all the information they need to choose products and apply for new accounts in digital channels.

6

Digital Account Creation

7

• Allows customers to easily apply, open and fund new deposit accounts through your public website

• Supports checking, CDs, savings, money markets and health savings accounts

• Applicant information is screened and verified for CIP information.

• Applicant can be screened through debit bureau and credit bureau based on your requirements.

• Customers can fund the new account through card transactions, electronic ACH transfer, check or direct deposit.

• Includes a “Fast Path” for your current customers

• Significant level of integration with the FIS core IBS

• New responsive design user interface expands your reach into all digital channels

Full-featured solution for deposit acquisition in self-service channels

Success in Digital Account Acquisition Includes Sales and Marketing Strategies

8

Account creation is the third step in the process.

• Your deposit acquisition strategy needs to include a digital marketing strategy.

• We recommend visiting a variety of FI websites to see how others are presenting their product offers.

• Prospects should be directed to your website from a digital search. Google “checking account” for a state in your footprint to see your competition.

• If you are expanding into Digital Account Opening with Responsive Design, your sales pages on your public website will need to be in Responsive Design for those shoppers that come in on their phones.

Digital Marketing Is a Critical Stage of the ProcessSuccessful FIs are investing more every year

9

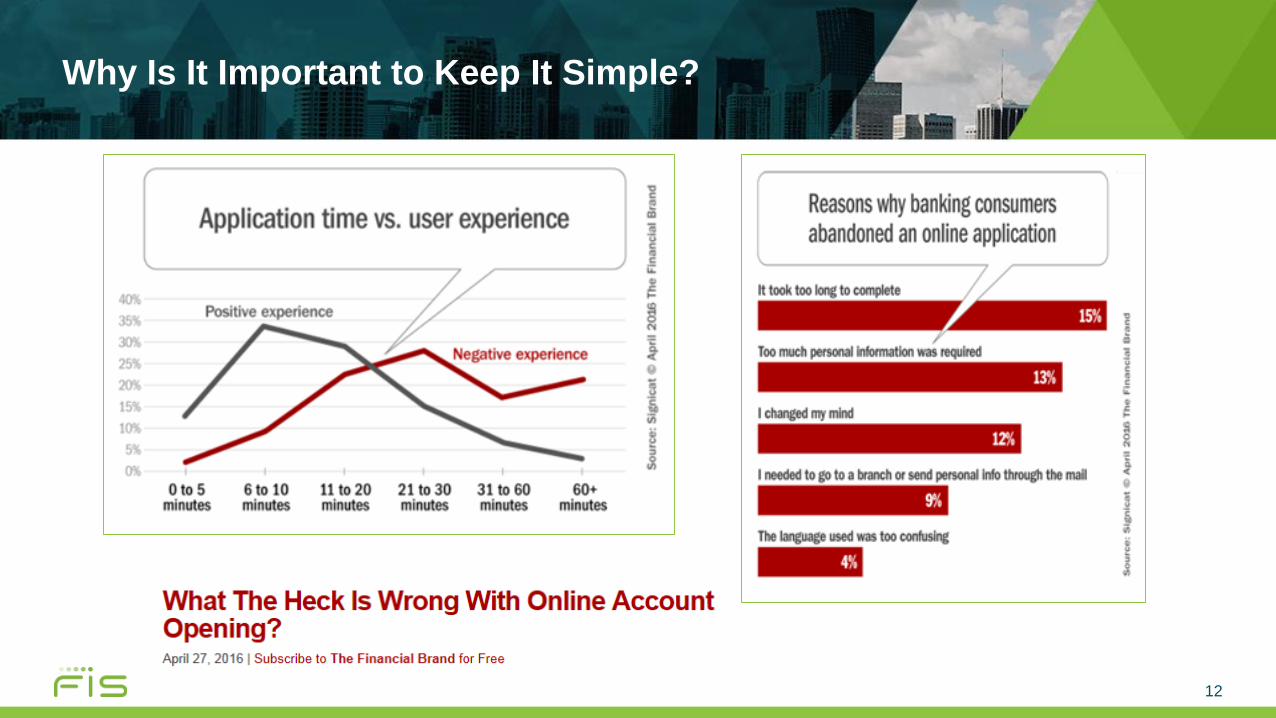

• The process needs to be different from branch account opening. Why?

– The customer’s attention is easily lost.

– Using a laptop, or a tablet or a phone is different than sitting in a branch bank.

Your prospective customer can easily slip away if:

The process is too long or hard to navigate

Questions seem intrusive or irrelevant

The product offer seems overly complex

They feel uncomfortable or confused by the process

• Regulations allow for a “paperless” process.

– Non-documentary verification of CIP information

– eSign acceptance of disclosures

– Signature cards not required when other processes are in place

• The most successful clients do not confine themselves to traditional

assumptions and processes but focus on building the best possible user

experience.

The Digital Account Opening ProcessUser experience is different from the branch account opening process

10

FIS Can Help You Design an Experience that Will Meet the Expectations of Your Prospects

• When you are implementing your Digital Account Creation experience, it is important to make branding and configuration choices that will provide a streamlined customer experience.

• Your public web site is critical to the sales process. You may need to refresh your public website to move the customer easily into the digital account opening experience.

Forrester recommends, when designing the account opening process “Reframe the discussion around the customer

rather than internal operations. Use Journey maps help employees adopt an outside-in perspective and understand how

their individual actions can collectively result in poor customer experiences”

11

12

Why Is It Important to Keep It Simple?

Starts after the customer has selected a product

The Account Creation Process

• Applicant enters information for application phase.

• Selects product options – ATM cards, checks, overdraft protection, etc.

• Reviews and accepts disclosures electronically

• Immediate identity verification (IDV) with OFAC screening

• Out-of-wallet questions (IDA)

• QualiFile screening

• ACH funding with immediate account validation or test transaction validation

• Check funding

• Card funding – credit and debit cards

• Customer record is created and account is opened in deposits.

• New account information is given to the customer.

Information

Gathering

Applicant

Screening

Funding the

Account

Account

Opening

13

14

Be Prepared for Some Customers to Switch Channels

New account opened and

delivered online. Activation

of online and mobile

servicing

Complete application

and accept

disclosures

Full evaluation of the

applicant from identity

verification to product

qualification

Funding the account -

multiple options and

safeguards

Account Creation Admin Tool with Login from Insight

Integration to IBS Deposit Origination

Digital User Interface

Banker can pick up failed applications, override

the failure, and return them to Digital Channels

to complete

UX

Banker

Action

Options

Deposit Origination Work Queue

Abandoned Failed Pushed

* All OAC data is sent into the BIC OAC Universe each night

15

The new Responsive Design User Experience expands your market reach to tablet and phone users.

Digital Account CreationIt’s here!

User experience options to support your sales strategies

Deposit Account Opening on Account Creation Platform

16

SINGLE ACCOUNT CREATION ADMIN TOOL FOR ANY UX

INTEGRATION TO Your FIS Core Deposit System FOR ONGOING SUPPORT

Digital Account

Creation

All Device Sizes

Browser

Mobile

Account

Opening

Phone App

Pilot 2017

AND

New account opened

and delivered online.

Activation of online and

mobile servicing

Funding the account:

multiple options and

safeguards

Full evaluation of the

applicant from identity

verification to product

qualification

Complete application

and accept disclosures

Online Account

Creation

PCs and Tablet

Browser

Phase 1 (early 2017)

• Leverage mobile responsive UI from OAC

platform, integrated to mobile banking app

Phase 2 (proposed TBD)

• SSO for existing customers to fast path OAC

user experience

Phase 3 (2018 target)

• Add functionality that allows for data capture

from a photo of the ID

Mobile App Account Opening Roadmap: Mobile integration options (pilot 2017 Q2)

17

FAQ: How Many New Accounts Can We Get?

From Javelin Research

– A large regional bank reports “tremendous year-over-year growth

in online account opening” for checking after upgrading its digital account

opening capabilities, but “we’re not quite at the one-third mark.”

– An FI’s size is a “horrible predictor” of digital account opening success.

The most successful FIs are the ones that emphasize digital account opening.

– Banks that succeed in online opening are the people who put a focus on it;

one FI might be successful, while others struggle because marketing support

is weak. “You still have to drive awareness and interest before you get clicks.”

FIS observations

– Success in account acquisition in the digital channels is driven by the FIs ability to

bring qualified, motivated people to the start of the process.

– The most successful clients are those that work at it all the time, adjusting

the process to maximize their results.

– Success metrics will be driven by the strategy and don’t look the same

for every FI.

18

Our Client Panel

Popular DirectSavings Made Simple.

Vilmarie GaudProduct Development DirectorPopular Community Bank

20

About Popular Direct

Popular Direct is the direct online channel of Banco Popular North America (Popular). Processing services for all Popular Direct deposit products are provided by Popular.

Banco Popular North America is the U.S. banking subsidiary of Popular, Inc. [NASDAQ:BPOP], a publicly traded, full-service financial services provider in the United States, Puerto Rico, and the Caribbean. Founded in 1893, Popular, Inc. is the leading banking institution by both assets and deposits in Puerto Rico and ranks among the top 50 U.S. banks by assets.

− Website designed based on User Needs and Personas assessments

− Marketing efforts Advertising campaign at launch SEM Bankrate

PO

PU

LAR

DIR

ECT

21

Popular Direct BackgroundSavings Made Simple.

Popular Direct Launch

− Launched in July 2016− Nationwide High Yield Savings and CDs− No access to Popular branches− New IBS instance− OAC, CeB, Mobile Banking− FIS VRU− FIS Call Center and Virtual Back Office− Mix of processes managed by FIS and Popular

Marketing

Application Volume

− Since launch we’ve received over 10,000 applications− Over 4,700 accounts have been opened − 281% of goal− 47% were completed, 35% of account opening applications were abandoned, and 15% failed.

PO

PU

LAR

DIR

ECT

22

Goals vs. ResultsSavings Made Simple.

Other Trends

− 17% of accounts from CA− 12% of accounts from NY− 10% of accounts from FL− CD products preferred by older customers− High yield savings products preferred by

younger customers

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Qtr3 Qtr4 Qtr1

2016 2017

PRODUCT DISTRIBUTION

C

S

0

1,000

2,000

3,000

4,000

5,000

6,000

Qtr3 Qtr4 Qtr1

2016 2017

APPLICATION VOLUME

Ineligible

In progress

Failed

Complete

Abandoned

1037840

471108

240128135

347575

103198

308107

138

Other States

FL

IL

MD

NY

PA

VA

0 200 400 600 800 1000 1200

ACCOUNTS BY STATE

Next StepsSavings Made Simple.

Customer Centered + Business Viable + Operationally Feasible

− Direct bank ecosystem is crowded and highly competitive

− Do not underestimate the effort of launching and maintaining a new bank

− Relentless focus on customer centered processes

− Continue using a funding lever− Continuous process optimization− Pricing discipline− Testing playground

Lessons Learned Next Steps

PO

PU

LAR

DIR

ECT

23

RETAIL PRODUCT MANAGER

CURT TRIZZINO

Who is The PrivateBank?

Middle Market Commercial Bank headquartered in Chicago, IL

• 36 Offices Concentrated in the Midwest

• 24 Retail Branches• 20 Billion in Assets• 1300 Employees

26

How We Use OAC

Initially Launched in 07’ – Palladian PrivateBank• Fund Commercial Loan Growth

Launched 2nd Instance of OAC in Q3 16’ – myPrivateBank & Advantage Banking• Cater to employees of new and existing businesses• Build on strong existing partnerships

How did we manage two different OAC platforms?

Partner BanksHigh Level of Customization

• Marketing Pages• OAC Platform• Products

27

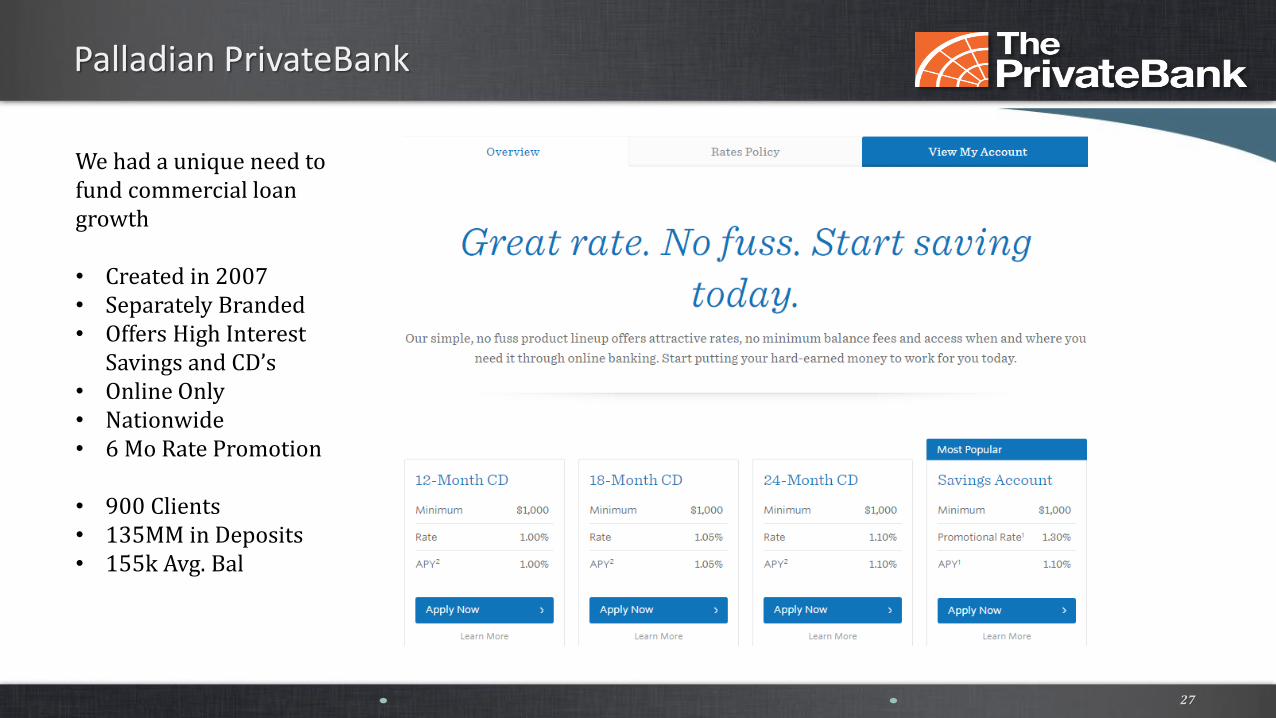

Palladian PrivateBank

We had a unique need to fund commercial loan growth

• Created in 2007• Separately Branded • Offers High Interest

Savings and CD’s• Online Only• Nationwide• 6 Mo Rate Promotion

• 900 Clients• 135MM in Deposits• 155k Avg. Bal

28

myPrivateBank

A vision to provide retail banking services to employees of new and existing businesses

• Rolled out in Q4 16’• Pilot Program• Onsite Concierge• Invitation Only• iPad Account Opening

• 60 Clients• 100k Bal

29

Advantage Banking

A vision to expand in our retail markets to employees of new and existing businesses

• Revamped in Q3 16’• Onsite Assistance• Invitation Only• Open Online or In Branch

• 150 Clients• 550k Bal

30

Lessons Learned

Customer Service

Rate Wins

Automation

High Touch

Follow Up

Dedicated Team

Reporting

Differentiation

31

Transformation

PalladianAnalytical MarketingNew Exciting OffersFull Service Digital Bank

myPrivateBankTech FirstCustomized OffersRelationship Based

General Account Opening

www.PalladianPrivateBank.com

Discussion

What’s Next

Join us at the following session

Session 1103 || Wednesday || 10:30 AM

Digital Transformation:

Strategies & Solutions for a New Banking Paradigm

Speakers: Susan Hawkins and Doug Peacock

Visit us in the Solutions Expo

Digital Account Creation kiosk

33