group : ntu rangga aditya nandi wp danang widhi witoko kresna nandhityo frederika

TRANSCRIPT

Group : NTU RanggaAditya Nandi WP

Danang Widhi WitokoKresna Nandhityo

Frederika

AGENDA

GLOBAL INDUSTRY AUTOMOTIVE

55 million vehicles ware sold worldwide 32 million were passenger cars90 % demand from the “triad”, USA (26%), Europe (40%), and Asia (24%)

After crisis 1997 - 1999, Asia had largely growth 5,1 % , follow by South American market

In term of market share, General Motor and ford accounted 15 %, follow with Toyota 10 % and Renault Nissan 9 %

The US market stagnant and tend to decrease 5 %, this scenario could be aggravated by rising oil prices and interest rate ( most American use credit to buy cars )

Europe, where the effected of cycles are usually less strong

While Other market is tend to stagnant

Established in 1926

Originated merger between Kwaishinsha ( founded in 1911 ) and

Jitsuyo Jidosha ( founded in 1919 )

Was a pioneer in the manufacturing automobiles Product : Automobile, Trucks and Forklift Main Market : Japan, United States and Europe Revenue : 80, 92 billion USD Profit : 460 million USD ( 2009 )

INTRODUCTION TO NISSAN

Established in 1898 by Louis Renault Is a French Automaker

Product : Automobile and Commercial Vehicles

Main Market : Europe, Turkey, Argentina, North Africa and Brazil ad Rusia

Revenue : 38,97 billion USD Profit : 3.420 million USD ( 2009 )

INTRODUCTION TO RENAULT

MAIN ISSUE

Renault – Nissan Alliance merger ( 1999 ) between French auto manufacturer and Japanese auto manufacturer.

NISSAN( Declining Company )

1.Failed to materialize to compete Toyota2.54 % capacity utilized3.Overall economic stagnation4.Poor internal communication5.A lack of urgency & strategic future6.Lack of cost control

NISSAN( Declining Company )

1.Failed to materialize to compete Toyota2.54 % capacity utilized3.Overall economic stagnation4.Poor internal communication5.A lack of urgency & strategic future6.Lack of cost control

RENAULT( Expanding Company )

1.Full capacity2.High concentrate in western Europe3.High profile4.Intend to be global

RENAULT( Expanding Company )

1.Full capacity2.High concentrate in western Europe3.High profile4.Intend to be global

STRATEGIC ALLIANCE

DefinitionAgreement for cooperation among two or more independent firms to work

together towards common objective.Companies in a strategic alliance do not form a new identity to reach their aims

but cooperate while remaining apart and distinct

Advantages1. Economies of scale and scope2. Increasing international competition3. Penetration into new markets4. Access to new design, tech and processes5. Supporting a declining company

Disadvantages1. Culture clash between company2. Leadership disputes3. Layoff from either company

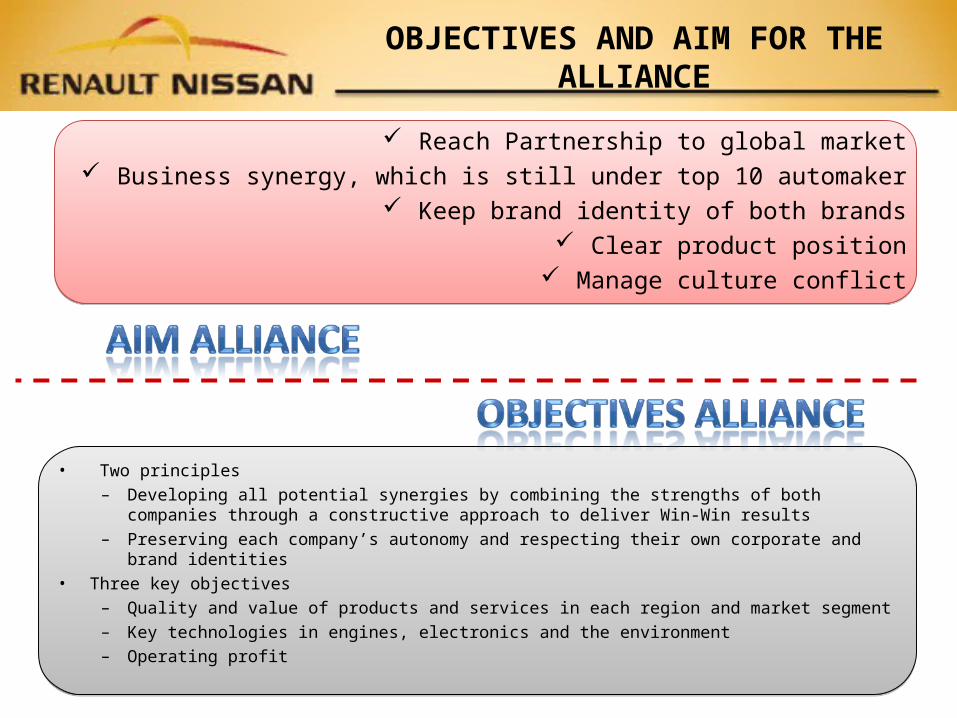

OBJECTIVES AND AIM FOR THE ALLIANCE

• Two principles– Developing all potential synergies by combining the strengths of both companies through a

constructive approach to deliver Win-Win results– Preserving each company’s autonomy and respecting their own corporate and brand identities

• Three key objectives– Quality and value of products and services in each region and market segment – Key technologies in engines, electronics and the environment– Operating profit

Reach Partnership to global market Business synergy, which is still under top 10 automaker

Keep brand identity of both brands Clear product position

Manage culture conflict

RENAULT AND NISSAN ALLIANCE

FIVE FORCES ANALYSIS

Domestic rivalries

High, many automaker in Japan and Franch

Threats from the new entrants

Low, due to high cost production and innovation

Subtitution Threats

Medium, consider with price of vehicle market has an alternative such as motorcycle or public transportationBuyer’s Purchasing Power

High, Buyer can switch the supplier for getting the competitive rate

Supplier’s Power

Medium, depend with commodity and loyalty between supplier and buyer

Competitiveness in an Industry – Automotive Vehicles

Competitiveness in an Industry – Automotive Vehicles

SWOT ANALYSIS

CORPORATE STUCTURE OF THE ALLIANCE

CARLOS GHOSN CONTRIBUTION

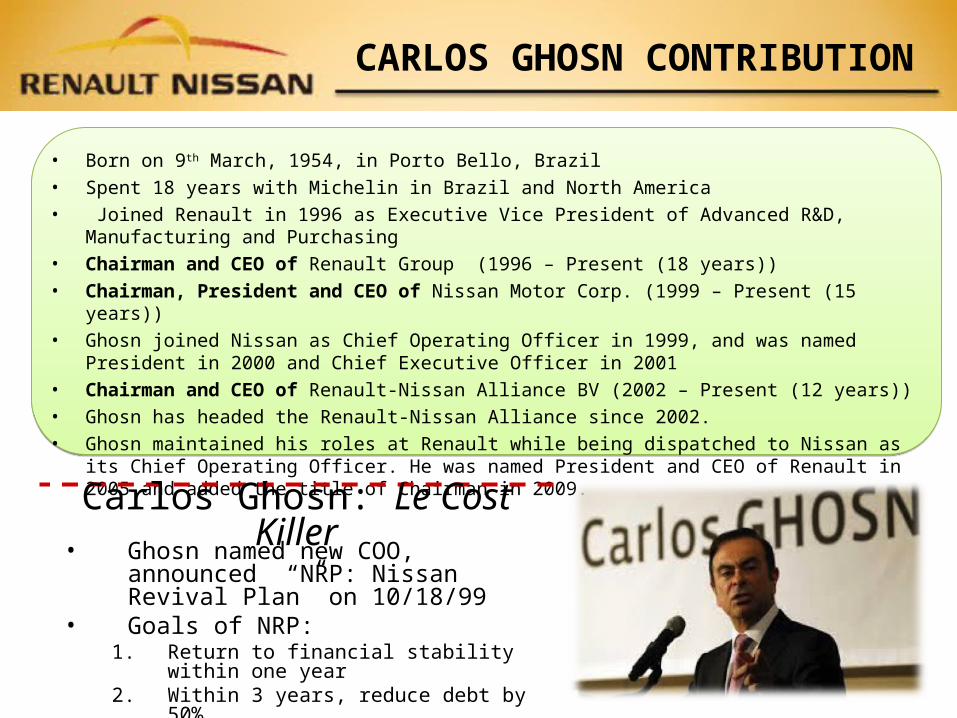

• Born on 9th March, 1954, in Porto Bello, Brazil • Spent 18 years with Michelin in Brazil and North America• Joined Renault in 1996 as Executive Vice President of Advanced R&D, Manufacturing and Purchasing• Chairman and CEO of Renault Group (1996 – Present (18 years))• Chairman, President and CEO of Nissan Motor Corp. (1999 – Present (15 years))• Ghosn joined Nissan as Chief Operating Officer in 1999, and was named President in 2000 and Chief Executive

Officer in 2001• Chairman and CEO of Renault-Nissan Alliance BV (2002 – Present (12 years))• Ghosn has headed the Renault-Nissan Alliance since 2002. • Ghosn maintained his roles at Renault while being dispatched to Nissan as its Chief Operating Officer. He was

named President and CEO of Renault in 2005 and added the title of Chairman in 2009.

Carlos Ghosn: Le Cost Killer• Ghosn named new COO, announced

“NRP: Nissan Revival Plan” on 10/18/99• Goals of NRP:

1. Return to financial stability within one year2. Within 3 years, reduce debt by 50%3. Within 3 years, operating margin rise to 4.5%

of sales

MANAGEMENT STUCTURE OF THE ALLIANCE

VALUE CHAIN RENAULT - NISSAN

PROCURMENT : Coordinated procurement and improvement in NiSSAN supply chain

PROCURMENT : Coordinated procurement and improvement in NiSSAN supply chain

TECNOLOGY : Faster production development, joint product development & economies of scale

TECNOLOGY : Faster production development, joint product development & economies of scale

HRM : Mainly Nissan executive exchange across the board HRM : Mainly Nissan executive exchange across the board

INFRASTUCTURE : Main head office back up & administration office internationally

INFRASTUCTURE : Main head office back up & administration office internationally

ALLIANCES KEY SUCCESS FACTOR

RESULTS OF THE ALLIENCE

RESULTS OF THE ALLIENCE

• The Alliance is also the only carmaker to offer a large range of all-electric vehicles. In 2013, global sales of Alliance vehicles producing zero emissions in use jumped to 66,809 units, up 52% on 2012. The Alliance’s share of the zero-emission vehicle market reached 63%

• Third largest global automaker (based on sales for the year 2008)• Global market share of 9% (by volume) • Significant presence in major world markets (United States, Europe,

Japan, China, India, Russia)