group benefits administrative updategroupbenefits.manulife.com/canada/gb_v2.nsf/lookup... · plan...

TRANSCRIPT

Group Benefits AdministraImportant information for Plan A

First Quarter 2003

Important information for Nova

Province becomes second pafamilies with private dental i

Inside this issue

Manulife Financial’s first quarter 2003 Administr

�� The Nova Scotia Children’s Oral Health�� Drug Stop Loss �� Online Claim Statements

This Administrative Update and previous editionswww.manulife.ca/groupbenefits. Click on “New

Administrative Update is provided to share inforintended as advice. Although we strive for accurhighlights to your attention. Please refer to yourIf there is a discrepancy between our communicPolicy will apply.

Families with private dental plans nservices covered under the Nova ScThe COHP will pay for the portion oinsurance plans. The Children’s Orpreventative, and restorative servicetenth birthday. As part of its 2002-03 budget, the NMay 1, 2002 the COHP would no lofamilies with private dental plans. T2002, ensures families with private ithan families without private insuran

The Manufacturers Li

tive Update dministrators

ative Update contains information about:

Program � Saskatchewan Pharmacare � Verifying Enrolment � Coordination of Benefits

are available on our web site at: sletters.”

mation with Plan Administrators. It is not acy, we are only bringing summaries and Group Policy for complete terms and condiations and the Group Policy, the terms of the

tions.

Scotia plan members . . .

yor for Nova Scotia nsurance

URGENT!

ACTION REQUIRED BY APRIL 15, 2003.

o longer have to cover co-payment costs for otia Children’s Oral Health Program (COHP). f eligible dental fees not reimbursed by private

al Health Program covers the cost of diagnostic, s for children up to the end of the month of their

ova Scotia government announced effective nger provide dental coverage for children of he amended regulation, effective October 7, nsurance are no longer required to pay more ce.

Continued on next page fe Insurance Company

Province becomes second payor . . . continued April 15, 2003 – Deadline for reimbursement submissions The government will reimburse plan members for the portion of eligible dental claims not covered under private plans, retroactive to May 1, 2002. A claim statement showing the plan member’s out-of-pocket expenses must be submitted with each claim. These claims must be submitted by April 15, 2003. Plan members should submit claims for costs incurred between May 1, 2002 and October 7, 2002 to Quickcard Solutions, - the 3rd party administrator of the COHP. If you or your plan members have questions about the amended regulation, please call Quickcard Solutions toll free at 1-888-846-9199.

Introducing . . .

Drug Stop Loss Pooling – Effective February 1, 2003 Drug Stop Loss pooling is a new pooling arrangement designed to protect plan sponsors from the impact of catastrophic drug claims on drug rates. Drug Stop Loss pooling applies to the following non-refund accounted, non-ASO groups in all provinces except Quebec: �� New Signature groups quoted on or after February 1, 2003. �� Existing Signature groups with renewal dates May 1, 2003 or later. �� Corporate Accounts will be integrated into Drug Stop Loss pooling in the

second quarter of 2003. All of these groups will be required to participate in the Drug Stop Loss pool. How Drug Stop Loss pooling works At renewal, a pooling charge will be applied to all eligible groups. However, at the same time, individual drug claim amounts over $10,000 will be excluded from a group’s drug rate calculations.

2

Drug Stop Loss Pooling . . . continued Addressing a need New drug therapies are driving increases in the cost of health care. Canadians with an increasing range of medical conditions may require expensive prescription drugs that are not eligible for government sponsored coverage. Plan sponsors concerned about meeting members’ needs may find costs prohibitive. Although costs for expensive “blockbuster” drugs and out-of-hospital treatments will likely continue to escalate for private group benefit plans, this new pooling arrangement can help plan sponsors better manage plan expenses. . For more information about Drug Stop Loss pooling, please contact your Manulife account executive.

Introducing . . .

Bundling claim statements conserves paper and time With the introduction of Group Benefits’ new member claim statements, Manulife can offer plan members an additional benefit: health and dental statements will now be mailed together in a single envelope when claims for members and any of their eligible dependants are processed on the same day. Only those claim statements having the identical member name and mailing address will be mailed together. For plan members, bundling ensures statements produced and mailed the same day arrive at the same time. The new process also saves paper — fulfilling a request made by many members. The service is provided automatically and free-of-charge whether claim submissions are electronic or made using paper claims forms. If a member’s claim statement requires an attachment, such as a receipt that must be returned, the statement and attachment may be mailed separately from other statements. Please note: The bundling and direct mailing of health and dental claim statements to plan members is not available for plan sponsors who currently receive plan member claim statements via bulk mail.

3

Introducing . . .

Online claim statements are here!

Your plan members can now get their health and dental claim statements online when they sign up to have their claims payments deposited directly to their bank accounts. Plan members can access their online statements on the Plan Member Secure Internet Site. No trips to the mailbox; no trips to the bank. Direct deposit and online claim statements are especially useful for plan members who are traveling or temporarily located away from home. The fastest, easiest way to get a claim statement When plan members register for direct deposit*, their online statement will be available on the date their claim is processed. Members will receive an e-mail alerting them when their claim statement is available online. Members have the option of printing their statements from the Plan Member Secure Site. * Direct deposit may not be available to all groups. This option is dependant on your plan’s financial arrangements with Manulife Financial.

It’s simple to sign-up When plan members register for direct deposit they’ll receive their claim payments quickly - usually within 1 to 5 days of the claim process date depending on the member’s banking institution. Here’s how your plan members can sign-up for direct deposit on the Plan Member Secure Internet Site. 1. Go to www.manulife.ca/groupbenefits 2. Choose “Plan Member.” 3. If you have already registered for secure site access, click "Login."

�� Enter your group/plan #, plan member/certificate #, and password. �� Click on “Submit.” �� Choose "Direct Deposit for claims" listed on the navigation bar on the

left-hand side of the screen. �� Provide and verify your banking information as requested.

If you have never used the Plan Member Site, click "Register." �� To ensure your confidential information is kept secure, a personal activation

code will be sent to your home address after you register for site access. �� Once you receive your activation code, you will be able to log-in to the

secure site. Please note: Only plan members can register for access to the Plan Member Secure Site. Plan administrators and providers cannot register for the secure site on behalf of plan members.

4

Online claim statements . . . continued

Plan member information If you would like to promote the features of the Plan Member Secure Site, including online claim statements, you can order two small flyers (GC2099E and GC2089E) suitable for distribution with payroll or other communications. Electronic versions of both these flyers are available on the Plan Administrator Site. Go to www.manulife.ca/groupbenefits and click on “Plan Administrator” to log-in to the site. GC2089E explains the advantages

of the Plan Member Secure Site GC2099E explains the convenience of online claim statements

5

Legislative change . . . .

New process for Saskatchewan claims

Coverage details Saskatchewan provides prescription drug coverage to residents of the province through the Saskatchewan Pharmacare Special Support Program, its provincial drug plan. However, as a result of recent changes to Pharmacare legislation, Saskatchewan residents are no longer automatically covered under the province’s prescription drug plan.* Residents may apply for and receive assistance under the Pharmacare Special Support Program if their drug costs exceed 3.4% of their individual or family income each benefit year. Manulife Financial’s standard drug plans supplement government drug programs, and normally cover eligible drug expenses not reimbursed under a government drug plan. Saskatchewan residents can claim eligible expenses not covered by the Saskatchewan Pharmacare Special Support Program through their Manulife plans. The use, and resulting costs, of private drug plans in Saskatchewan may increase significantly because coverage under Pharamcare is not automatic and residents with private insurance coverage may not recognize the need to enrol in the provincial plan. To help control costs, Manulife will establish claim threshold levels to track plan members’ prescription drug expenses and ensure claims are reimbursed by Pharmacare when a member’s drug costs exceed 3.4% of their individual or family income each benefit year. *Please see “Legislative update” (page 8) in the first quarter 2003 edition of Employee Benefit News for more information about the Saskatchewan Pharmacare legislative changes effective July 1, 2002. Threshold levels ensure proper claims adjudication Effective July 1, 2003, Manulife will introduce claims threshold levels to ensure proper adjudication of claims payments with the Saskatchewan Pharmacare drug plan. Manulife has established threshold limits on the ManuScript pay-direct and reimbursement drug claims we pay until proof of enrolment in the provincial drug program is submitted. This will help ensure Saskatchewan residents apply to the Pharmacare Special Support Program when they might first become eligible for coverage under the provincial plan. The threshold limits ensure accurate claims adjudication between Manulife and the Saskatchewan Pharmacare drug plan. Manulife has set threshold limits based on 3.4% of the provincial average family income.

6

New process for Saskatchewan claims . . . continued Eligible drug claims submitted by Saskatchewan residents to Manulife are paid up to the established thresholds. When a member’s expenses reach the threshold, Manulife Group Benefits advises the member to apply for provincial Pharmacare coverage and to forward a copy of the Pharmacare application form to us. Once a copy of the member’s application form is received, Manulife will continue to cover eligible drug expenses not reimbursed by Pharmacare.

If the plan member living in Saskatchewan is …

and total accumulated drug expenses are …

then …

below $1200 Eligible drug claims submitted to Manulife will be paid.

Under 65 years of age

above $1200 Manulife will require a copy of the member’s Saskatchewan Pharmacare application for the current benefit year before further drug claims can be processed.

below $800 Eligible drug claims submitted to Manulife will be paid.

65 years of age or older

above $800 Manulife will require a copy of the member’s Saskatchewan Pharmacare application for the current benefit year before further drug claims can be processed.

Plan members must enrol every year The Saskatchewan Pharmacare Special Support Program benefit year runs from July 1st to June 30th. Enrolment is not mandatory. Provincial residents are able to register for coverage annually by completing application forms available at local pharmacies. 7

Important reminders . . .

Increased threshold levels for Manitoba Pharmacare Coverage details Manitoba provides prescription drug coverage to residents of the province through the Manitoba Pharmacare program, its provincial drug plan. Pharmacare pays 100 percent of eligible drug expenses for each resident after he or she reaches a variable deductible each benefit year. Manitoba residents can claim eligible expenses they use to satisfy their Pharmacare deductibles through their Manulife plans. What’s changed? Manulife has established threshold limits on the ManuScript and reimbursement claims paid. Claims exceeding the established thresholds will not be paid until proof of enrolment in the provincial drug plan has been submitted. These thresholds ensure accurate claims adjudication between Manulife and Manitoba Pharmacare. Threshold limits are based on the average family deductible amount. On January 1, 2003 Manulife increased the claim threshold levels to reflect a more accurate deductible level with the Manitoba Pharmacare drug plan. Manulife now covers an increased level of expenses but continues to request confirmation of Pharmacare enrolment to ensure proper claims adjudication. If a plan member is under age 65 with total accumulated drug expenses below $1200, eligible drug claims submitted to Manulife will be paid. If total accumulated drug expenses are above $1200, Manulife will require a copy of their Manitoba Pharmacare application for the current benefit year before further drug claims can be processed. If a plan member is 65 year of age or older with total accumulated drug expenses below $800, eligible drug claims submitted to Manulife will be paid. If total accumulated drug expenses are above $800, Manulife will require a copy of their Manitoba Pharmacare application for the current benefit year before further drug claims can be processed. Need more information? If you have any questions about Manulife’s claims threshold levels relating to Manitoba Pharmacare, please call the Customer Service Centre at 1-800-268-6195, or contact your local Manulife Financial representative.

8

Important reminders . . .

Accurate enrolment and eligibility information key to proper coverage

Plan administrators must confirm the accuracy of plan member and dependant enrolment information to ensure accurate premium calculations and proper claims adjudication. Benefit coverage, and claims paid, may be based on member information provided at enrolment and during subsequent updates. If this information is not accurate, benefits payable to the member may differ from the amount the member expects, and may be entitled to. If inaccurate member information is provided, Manulife will not be held responsible for the difference between benefits paid and benefits a plan member may be entitled to. Where inaccurate member information results in a claim payment which a member is not entitled to, Manulife may hold the plan sponsor responsible for any payment made in error. Plan administrators are responsible for verifying and validating enrolment information provided by members. To help with this validation, a list of criteria has been included with this edition of Administration Update. (See page 10.) Reporting changes Maintaining current member information is essential. It is important that information provided at enrolment is kept up-to-date to ensure claims can continue to be assessed quickly and accurately. Dependant status, salary updates, occupation changes, and terminations should be kept current throughout the year and verified annually. For your convenience, changes to plan member information can be submitted electronically using the “Record Employment and/or Salary Changes” feature, the “Enrolment and Re-enrolment Application”, and the “Application for Change” form on the Plan Administrator Secure Site. Updates submitted electronically can be processed more quickly and accurately than paper forms. With electronic submissions, the “Member Coverage Summary” feature available on the secure site enables plan administrators to verify updates to member coverage information within two business days. Questions? If you have questions about reporting changes to plan member information, please call the Customer Service Centre at 1-800-268-6195. You may also use the Send a note feature on the Plan Administrator Secure Site contact the Customer Service Centre by e-mail.

9

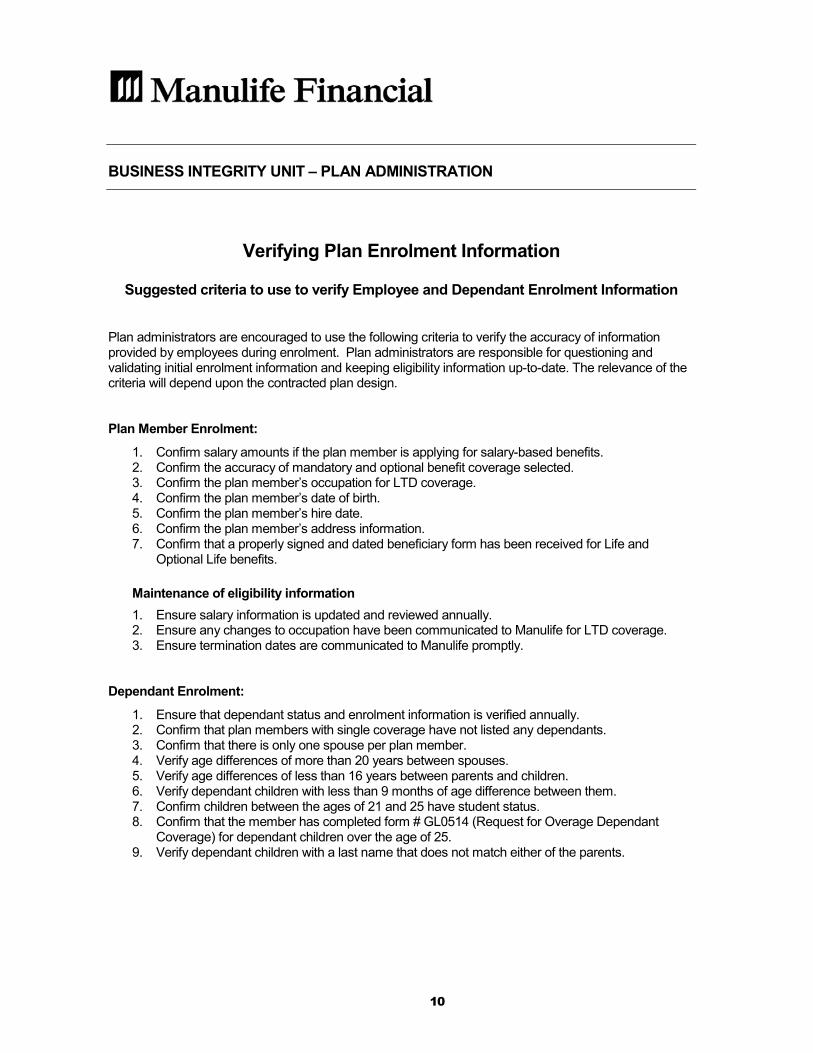

BUSINESS INTEGRITY UNIT – PLAN ADMINISTRATION

Verifying Plan Enrolment Information

Suggested criteria to use to verify Employee and Dependant Enrolment Information

Plan administrators are encouraged to use the following criteria to verify the accuracy of information provided by employees during enrolment. Plan administrators are responsible for questioning and validating initial enrolment information and keeping eligibility information up-to-date. The relevance of the criteria will depend upon the contracted plan design.

Plan Member Enrolment: 1. Confirm salary amounts if the plan member is applying for salary-based benefits. 2. Confirm the accuracy of mandatory and optional benefit coverage selected. 3. Confirm the plan member’s occupation for LTD coverage. 4. Confirm the plan member’s date of birth. 5. Confirm the plan member’s hire date. 6. Confirm the plan member’s address information. 7. Confirm that a properly signed and dated beneficiary form has been received for Life and

Optional Life benefits.

Maintenance of eligibility information

1. Ensure salary information is updated and reviewed annually. 2. Ensure any changes to occupation have been communicated to Manulife for LTD coverage. 3. Ensure termination dates are communicated to Manulife promptly.

Dependant Enrolment: 1. Ensure that dependant status and enrolment information is verified annually. 2. Confirm that plan members with single coverage have not listed any dependants. 3. Confirm that there is only one spouse per plan member. 4. Verify age differences of more than 20 years between spouses. 5. Verify age differences of less than 16 years between parents and children. 6. Verify dependant children with less than 9 months of age difference between them. 7. Confirm children between the ages of 21 and 25 have student status. 8. Confirm that the member has completed form # GL0514 (Request for Overage Dependant

Coverage) for dependant children over the age of 25. 9. Verify dependant children with a last name that does not match either of the parents.

10

Important reminder . . .

ManuScript – understanding program benefits The electronic claims submission feature of the ManuScript drug benefit program offers many advantages for plan sponsors, including the ability to control plan expenses related to costly paper claim submissions. Manulife Financial recently completed a survey to determine why some plan members with the ManuScript drug benefit program included in their group benefits plan, submit paper claim forms instead of using electronic claims submission. Survey results indicated that plan members are not opposed to using their ManuScript card, rather there are impediments to its use and the advantages are not always clear. Education is key to card use The survey suggested some plan members might not realize the conveniences and services offered by ManuScript. Educating members about ManuScript and encouraging the use of the pay-direct drug card is key to card use. A brochure entitled “A prescription for your health” provides important information about ManuScript and the convenient services available to members when they use their drug card. If your group plan includes ManuScript, please order form number GL3430E for distribution to plan members. An electronic version of this brochure is available on the Plan Administrator Site. Go to www.manulife.ca/groupbenefits and click on “Plan Administrator” to login to the site. Choose “Forms and Brochures” on the left navigation bar. Choose “ManuScript” from the Brochures drop-down box. Pharmacy support Some members have reported problems when using their card at the pharmacy. If the pharmacy has problems submitting claims electronically, plan members can ask their pharmacist to call ESI Canada, Manulife’s Pharmacy Benefit Manager, toll-free seven days a week. The ESI Pharmacy Help Desk can usually resolve problems on the spot, while the plan member is still at the pharmacy. Need additional cards? One in five members surveyed said they do not have a sufficient number of cards for all insured family members. Plan administrators and plan members can order additional cards, or request replacement ManuScript cards, by calling the Customer Service Centre at 1-800-268-6195. Or use the “Send a note” feature on the secure sites to send an e-mail to Customer Service. Manulife will automatically generate ManuScript cards for added plan members or family changes (including an added spouse or over-age dependant) – there is no need to order additional cards in these instances.

11

Did you know?

Understanding Coordination of Benefits Rising costs associated with health and dental benefits concern everyone. But a simple process — Coordination of Benefits (COB) — can help your members recoup up to100% of their eligible expenses while saving your plan money. A member with coverage under your plan may be a covered dependant with a spouse’s plan. If your member is not aware of COB, he might just submit claims to the 'better' of the two plans hoping to have more of his expenses reimbursed.

In all cases where benefits are being coordinated, plans will apply any deductibles, maximums or coverage limitations in accordance with the policy before any payments are issued for claims.

A consistent handling process Industry-wide guidelines developed by the Canadian Life and Health Insurance Association (CLHIA) establish a consistent handling process for all insurance companies to follow when processing health and dental claims. Plan members need to understand these guidelines so they know how to submit personal and spousal claims to all carriers. The CLHIA guidelines outline which insurance company pays first when both parents have coverage for their eligible dependant children. The parent whose date of birth falls earlier in the calendar year submits claims to his or her insurance company first. If the claim is approved, payment will be issued from that parent’s plan. If the ‘birthday rule’ results in a stalemate, then an ‘alphabetical rule’ (the parent whose first name begins with a letter occurring earlier in the alphabet) is applied. If parents are divorced or legally separated, or if they have re-married or entered into new common-law relationships, there are additional CLHIA payment guidelines applied to dependant children’s claims related to custody arrangements. In most cases, payment is issued to the insured parent whose plan is considered first payer, regardless of which parent paid the service provider for the treatment. This can be an issue where parents are not on good terms. Plan members in this situation should contact the first carrier’s customer service center, before any claims are submitted, to request a special handling arrangement for claims payments. Plan member information Regardless of which method is used to share information, when members take advantage of COB, they are undertaking a cost savings strategy for your plan as well ensuring expenses are shared between all insurance companies involved. An information sheet detailing the different scenarios outlined in your policy document is available to help members understand Coordination of Benefits rules. A sample is attached to this edition of Administrative Update. To order a supply of these forms, please request form number GL3618E.

12

S

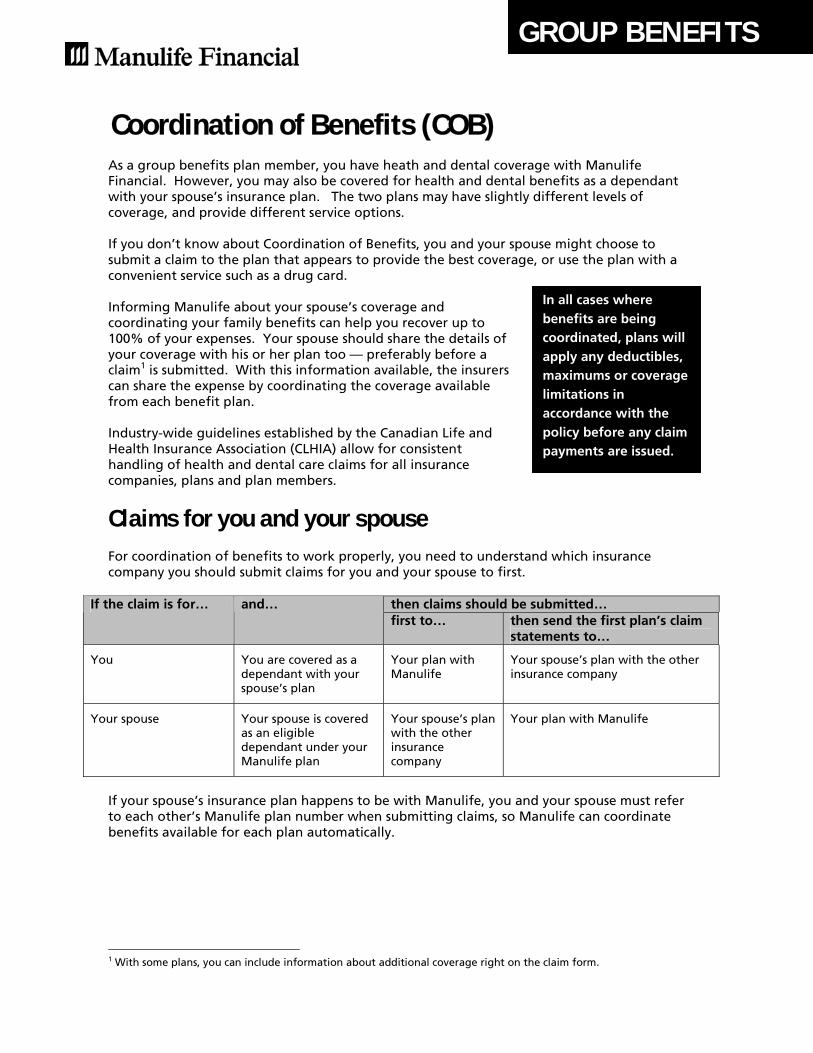

As a group benefits plan member, you have heath and dental covFinancial. However, you may also be covered for health and dentwith your spouse’s insurance plan. The two plans may have slighcoverage, and provide different service options. If you don’t know about Coordination of Benefits, you and your ssubmit a claim to the plan that appears to provide the best coverconvenient service such as a drug card. Informing Manulife about your spouse’s coverage and coordinating your family benefits can help you recover up to 100% of your expenses. Your spouse should share the details of your coverage with his or her plan too — preferably before a claim1 is submitted. With this information available, the insurers can share the expense by coordinating the coverage available from each benefit plan. Industry-wide guidelines established by the Canadian Life and Health Insurance Association (CLHIA) allow for consistent handling of health and dental care claims for all insurance companies, plans and plan members.

Claims for you and your spouse

For coordination of benefits to work properly, you need to undercompany you should submit claims for you and your spouse to fir

then claims should If the claim is for… and… first to…

You

You are covered as a dependant with your spouse’s plan

Your plan with Manulife

Your spouse

Your spouse is covered as an eligible dependant under your Manulife plan

Your spouse’s plan with the other insurance company

If your spouse’s insurance plan happens to be with Manulife, youto each other’s Manulife plan number when submitting claims, sobenefits available for each plan automatically.

1 With some plans, you can include information about additional coverage right o

GROUP BENEFIT

Coordination of Benefits (COB)

erage with Manulife al benefits as a dependant tly different levels of

pouse might choose to age, or use the plan with a

In all cases where benefits are being coordinated, plans will apply any deductibles, maximums or coverage limitations in accordance with the policy before any claim payments are issued.

stand which insurance st.

be submitted… then send the first plan’s claim statements to…

Your spouse’s plan with the other insurance company

Your plan with Manulife

and your spouse must refer Manulife can coordinate

n the claim form.

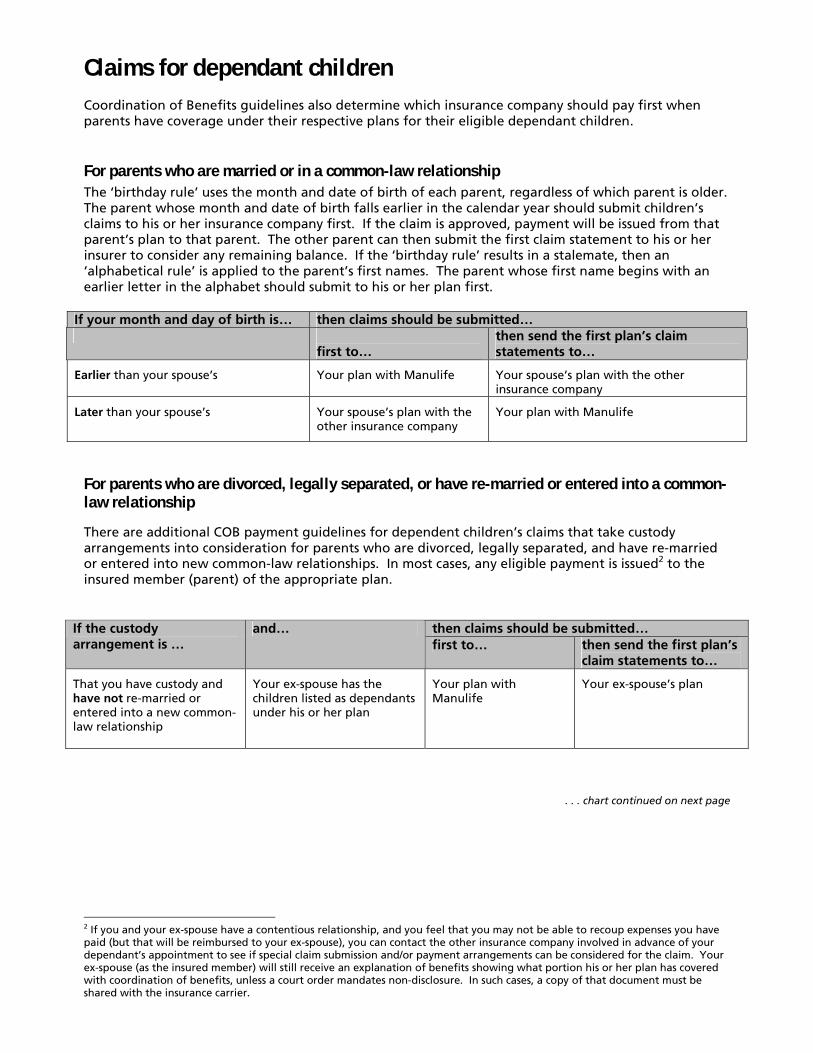

Claims for dependant children

Coordination of Benefits guidelines also determine which insurance company should pay first when parents have coverage under their respective plans for their eligible dependant children.

For parents who are married or in a common-law relationship

The ‘birthday rule’ uses the month and date of birth of each parent, regardless of which parent is older. The parent whose month and date of birth falls earlier in the calendar year should submit children’s claims to his or her insurance company first. If the claim is approved, payment will be issued from that parent’s plan to that parent. The other parent can then submit the first claim statement to his or her insurer to consider any remaining balance. If the ‘birthday rule’ results in a stalemate, then an ‘alphabetical rule’ is applied to the parent’s first names. The parent whose first name begins with an earlier letter in the alphabet should submit to his or her plan first.

If your month and day of birth is… then claims should be submitted…

first to… then send the first plan’s claim statements to…

Earlier than your spouse’s

Your plan with Manulife

Your spouse’s plan with the other insurance company

Later than your spouse’s

Your spouse’s plan with the other insurance company

Your plan with Manulife

For parents who are divorced, legally separated, or have re-married or entered into a common-law relationship

There are additional COB payment guidelines for dependent children’s claims that take custody arrangements into consideration for parents who are divorced, legally separated, and have re-married or entered into new common-law relationships. In most cases, any eligible payment is issued2 to the insured member (parent) of the appropriate plan.

then claims should be submitted… If the custody arrangement is …

and… first to… then send the first plan’s

claim statements to…

That you have custody and have not re-married or entered into a new common-law relationship

Your ex-spouse has the children listed as dependants under his or her plan

Your plan with Manulife

Your ex-spouse’s plan

. . . chart continued on next page

2 If you and your ex-spouse have a contentious relationship, and you feel that you may not be able to recoup expenses you have paid (but that will be reimbursed to your ex-spouse), you can contact the other insurance company involved in advance of your dependant’s appointment to see if special claim submission and/or payment arrangements can be considered for the claim. Your ex-spouse (as the insured member) will still receive an explanation of benefits showing what portion his or her plan has covered with coordination of benefits, unless a court order mandates non-disclosure. In such cases, a copy of that document must be shared with the insurance carrier.

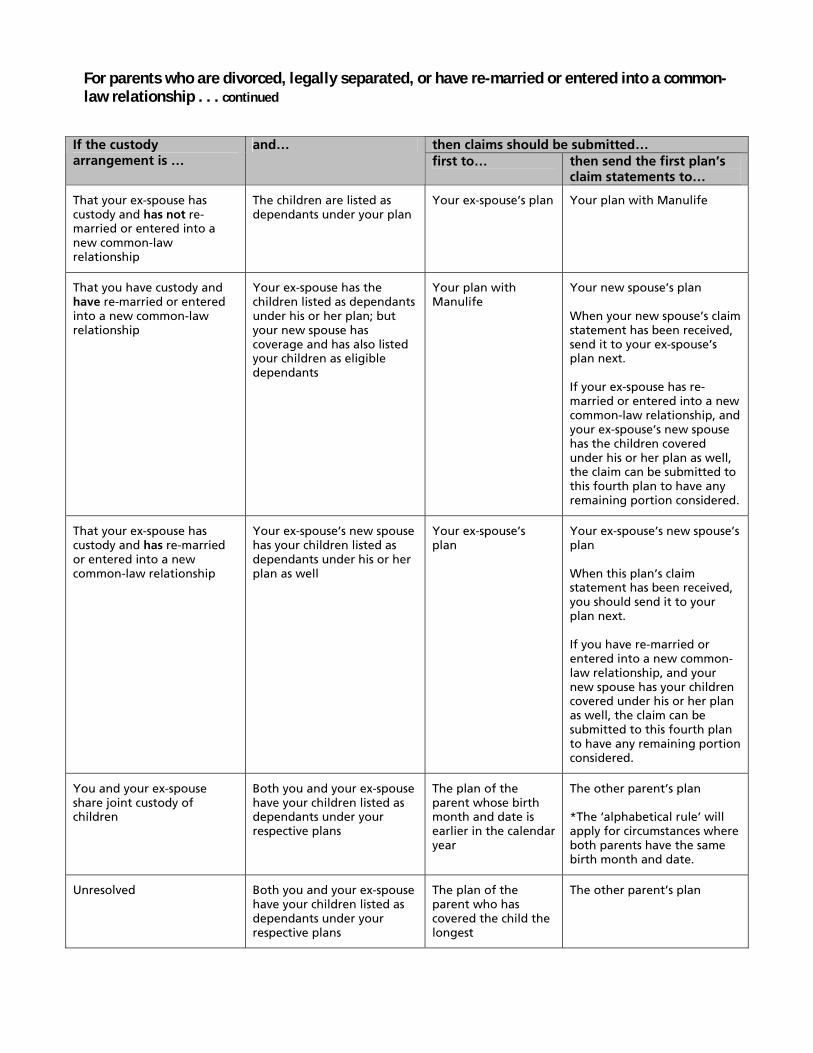

For parents who are divorced, legally separated, or have re-married or entered into a common-law relationship . . . continued

then claims should be submitted… If the custody arrangement is …

and… first to… then send the first plan’s

claim statements to…

That your ex-spouse has custody and has not re-married or entered into a new common-law relationship

The children are listed as dependants under your plan

Your ex-spouse’s plan

Your plan with Manulife

That you have custody and have re-married or entered into a new common-law relationship

Your ex-spouse has the children listed as dependants under his or her plan; but your new spouse has coverage and has also listed your children as eligible dependants

Your plan with Manulife

Your new spouse’s plan When your new spouse’s claim statement has been received, send it to your ex-spouse’s plan next. If your ex-spouse has re-married or entered into a new common-law relationship, and your ex-spouse’s new spouse has the children covered under his or her plan as well, the claim can be submitted to this fourth plan to have any remaining portion considered.

That your ex-spouse has custody and has re-married or entered into a new common-law relationship

Your ex-spouse’s new spouse has your children listed as dependants under his or her plan as well

Your ex-spouse’s plan

Your ex-spouse’s new spouse’s plan When this plan’s claim statement has been received, you should send it to your plan next. If you have re-married or entered into a new common-law relationship, and your new spouse has your children covered under his or her plan as well, the claim can be submitted to this fourth plan to have any remaining portion considered.

You and your ex-spouse share joint custody of children

Both you and your ex-spouse have your children listed as dependants under your respective plans

The plan of the parent whose birth month and date is earlier in the calendar year

The other parent’s plan *The ‘alphabetical rule’ will apply for circumstances where both parents have the same birth month and date.

Unresolved

Both you and your ex-spouse have your children listed as dependants under your respective plans

The plan of the parent who has covered the child the longest

The other parent’s plan

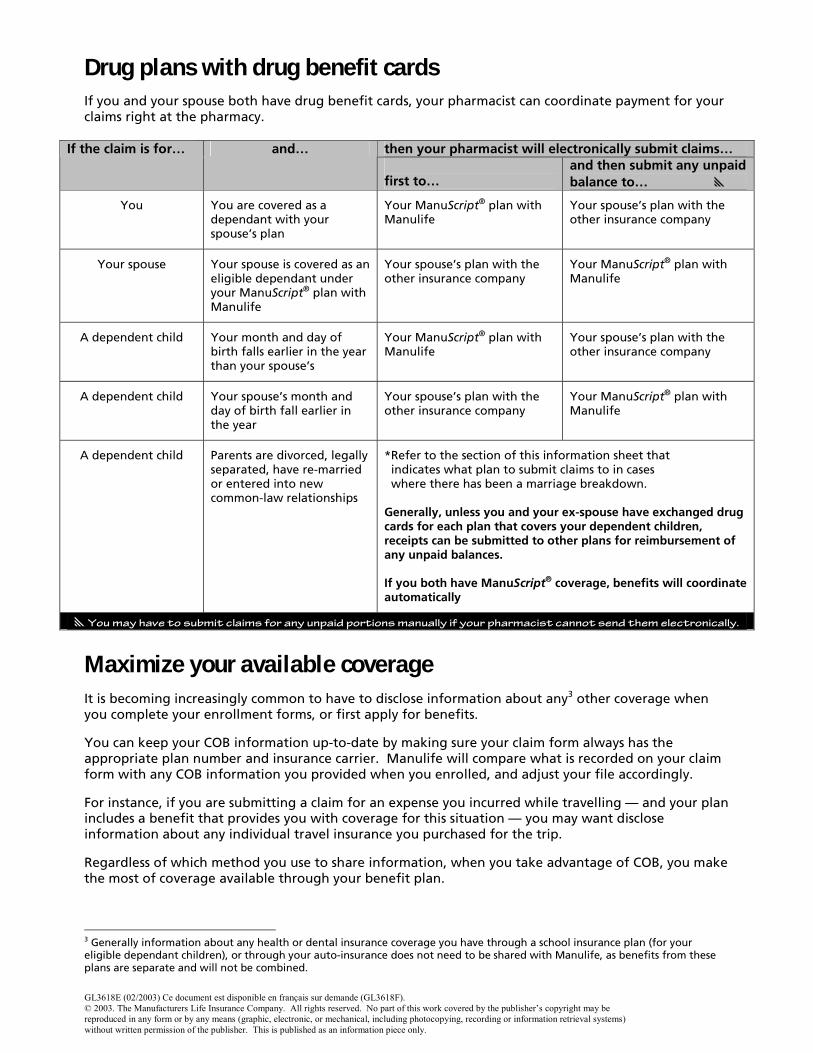

Drug plans with drug benefit cards If you and your spouse both have drug benefit cards, your pharmacist can coordinate payment for your claims right at the pharmacy.

then your pharmacist will electronically submit claims… If the claim is for… and… first to…

and then submit any unpaid balance to… �

You

You are covered as a dependant with your spouse’s plan

Your ManuScript® plan with Manulife

Your spouse’s plan with the other insurance company

Your spouse

Your spouse is covered as an eligible dependant under your ManuScript® plan with Manulife

Your spouse’s plan with the other insurance company

Your ManuScript® plan with Manulife

A dependent child

Your month and day of birth falls earlier in the year than your spouse’s

Your ManuScript® plan with Manulife

Your spouse’s plan with the other insurance company

A dependent child

Your spouse’s month and day of birth fall earlier in the year

Your spouse’s plan with the other insurance company

Your ManuScript® plan with Manulife

A dependent child

Parents are divorced, legally separated, have re-married or entered into new common-law relationships

*Refer to the section of this information sheet that indicates what plan to submit claims to in cases where there has been a marriage breakdown. Generally, unless you and your ex-spouse have exchanged drug cards for each plan that covers your dependent children, receipts can be submitted to other plans for reimbursement of any unpaid balances. If you both have ManuScript® coverage, benefits will coordinate automatically

�You may have to submit claims for any unpaid portions manually if your pharmacist cannot send them electronically.

Maximize your available coverage

It is becoming increasingly common to have to disclose information about any3 other coverage when you complete your enrollment forms, or first apply for benefits. You can keep your COB information up-to-date by making sure your claim form always has the appropriate plan number and insurance carrier. Manulife will compare what is recorded on your claim form with any COB information you provided when you enrolled, and adjust your file accordingly. For instance, if you are submitting a claim for an expense you incurred while travelling — and your plan includes a benefit that provides you with coverage for this situation — you may want disclose information about any individual travel insurance you purchased for the trip. Regardless of which method you use to share information, when you take advantage of COB, you make the most of coverage available through your benefit plan.

3 Generally information about any health or dental insurance coverage you have through a school insurance plan (for your eligible dependant children), or through your auto-insurance does not need to be shared with Manulife, as benefits from these plans are separate and will not be combined.

GL3618E (02/2003) Ce document est disponible en français sur demande (GL3618F). © 2003. The Manufacturers Life Insurance Company. All rights reserved. No part of this work covered by the publisher’s copyright may be reproduced in any form or by any means (graphic, electronic, or mechanical, including photocopying, recording or information retrieval systems) without written permission of the publisher. This is published as an information piece only.