green bonds markets trends and update thai bma

TRANSCRIPT

UNFCCC/IGES - Regional Collaboration Center, Bangkok

Green Bonds Markets Trends and Update

Thai BMA, Sustainability Finance Conference

October 2018, 16th, Bangkok

Discussion Overview

I. Sustainability Finance and Green Bond Market State

II. Types of Projects Financed by Green Bonds

III. Cost/Price Consideration of Green Bonds

IV. Incentive for Green Bonds in Global Markets

V. Current “Green Reaction”: Issuers / Investors Conclusion

I. SUSTAINABILITY FINANCEAND GREEN BOND MARKET STATE

The Global Landscape of Sustainable Finance

Sustainable investments required globally between now and 2030 -US$100tn or US$8tn annually (WEF)

Current global sustainable finance flows stand at US$741bn annually

US$7tn in DCM US$655bn equities, US$2tn business loans raised/provided annually

How can we channel these funds towards

green?

SustainableFinance GlobalLandscape

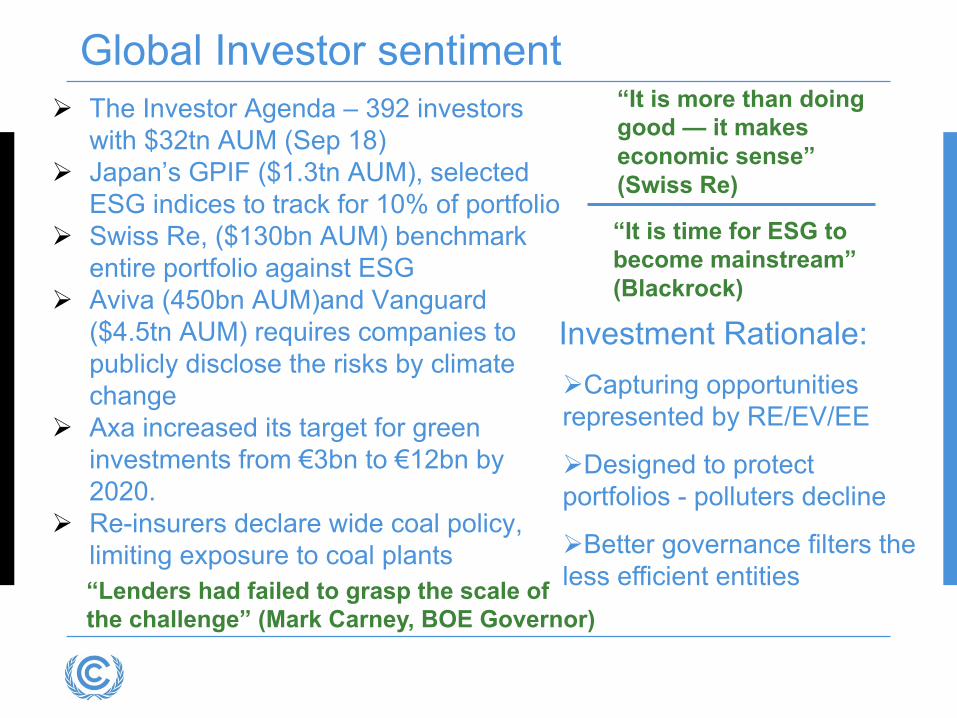

Global Investor sentiment

Global Investor sentiment Ø The Investor Agenda – 392 investors

with $32tn AUM (Sep 18)Ø Japan’s GPIF ($1.3tn AUM), selected

ESG indices to track for 10% of portfolioØ Swiss Re, ($130bn AUM) benchmark

entire portfolio against ESGØ Aviva (450bn AUM)and Vanguard

($4.5tn AUM) requires companies to publicly disclose the risks by climate change

Ø Axa increased its target for green investments from €3bn to €12bn by 2020.

Ø Re-insurers declare wide coal policy, limiting exposure to coal plants

“It is time for ESG to become mainstream” (Blackrock)

“It is more than doing good — it makes economic sense” (Swiss Re)

Investment Rationale: ØCapturing opportunities represented by RE/EV/EE

ØDesigned to protect portfolios - polluters decline

ØBetter governance filters the less efficient entities“Lenders had failed to grasp the scale of

the challenge” (Mark Carney, BOE Governor)

Global Investors Sentiment

Mounting evidence in emerging markets in particular that equity funds which observe ESG standards outperform those that don’t by a significant margin

Green Banking (including project finance, corporate

lending)

Bonds (green bonds, corporate, thematic bonds)

Private Equity / Venture Capital

Stocks

Priv

ate

Sect

or F

inan

ce

Cap

ital M

arke

ts

DEBT

EQUITY

Mezzanine

Private Sector Financing Instruments

Green Bond Markets Focus

>90000

674

221

895

2007 December 31, bond market status (billion USD)

Global bond market Climate aligned bonds

Labeled green bond market

Ø Bond markets have the depth required for financing long term climate projects

Ø Green bond market accounts for about 2 per cent of global fixed income issuance

Ø $6tn of estimated investment will be needed annually over a 15-year period to meet the UN’s sustainable development goals

1H 2018, Green Bond issuance increased YOY, but below expectations

Source: Moody’s investors service

Ø The demand for Green bond investment in ASEAN until the year 2030 stands at approximately $2-3tn (DBS, UNEP):

Ø $1.2tn to $1.8tn are expected to come from private-sector and especially green bonds

Ø Green Bonds should provides with funds to build and upgrade infrastructure, accelerate a transition to renewable energy and energy efficiency, develop sustainable agriculture

Ø Market Standardization is Key - The ASEAN Capital Markets Forum (ACMF), released the ASEAN Green Bond Standards in November, 2017

Ø The anticipation is for a stream of green investment projects taking place within the region that adopt the ASEAN GBS

Ø Sovereigns, FI’s and Corporate issuers all have a major role to play

Green Bond in ASEAN – Demand

Ø City Developments Limited, issued the first green bond in SGX (April 2017). Followed by DBS, issuing a US$500m green bond (July 2017) - institutional demand Singapore was proven.

Further SGX issuance:Ø Indian Renewable Energy Development Agency issued an

INR 19.5bn green masala bond (Oct 2017). Ø Manulife Financial Corp issued a S$500m green bond (Nov

2017).Ø Star Energy Geothermal issued and listed a US$580m

amortizing green project bond (Apr 2018); (first Indonesian corporate green bond issuance) A 2 billion ringgit ($507m) securities issue by Permodalan Nasional, Malaysian government asset manager, marked the first use of ASEAN Green Bond Standards. (Nov 2017)

Ø Indonesia raised a $1.25bln green bond - first for ASEAN Sovereign – Cicero provided rating.

Green Bond in ASEAN - Milestones

Green Bonds – Public Sector Support Role

Southeast Asian governments have an important role to play:

Ø Governments can take the lead and issue sovereign green bonds Ø Credit insurance and guarantees from government or sub-

sovereign agencies allow for mainstream institutional investors participation.

Ø Governments to set investment guidelines for public Asset Owners including pension funds and other state funds, development banks

Ø Regulatory bodies can provide input over reporting requirements, third-party review procedures in line with ASEAN Standards

Ø Incentives are usually required to start off a market: tax breaks vs. incremental green cost debate.

Local Capital Markets Issuance

Key elements required for institutional investors participation in Asia and the Pacific Climate Finance

Ø Functional corporate bond markets Ø Investment grade rating, BBB- (S&P)Ø Currency stability

Climate finance could in-turn be a catalyst for development of a healthier local financial markets by:

Ø Setting the benchmark for other issuance Ø Diversify the investor base by introducing international investorsØ Development of risk mitigating tools: Guarantees, Currency

hedging, blended financeØ Increased investment governance, reporting and transparency

China

II. TYPES OF PROJECTSFINANCED BY GREEN BONDS

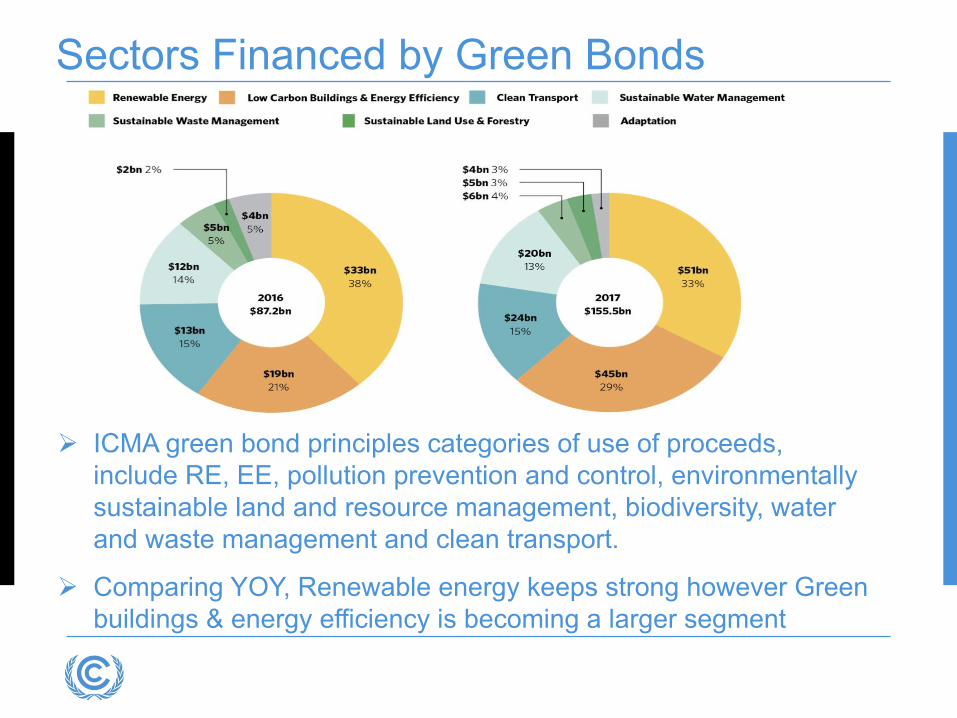

Sectors Financed by Green Bonds

Ø ICMA green bond principles categories of use of proceeds, include RE, EE, pollution prevention and control, environmentally sustainable land and resource management, biodiversity, water and waste management and clean transport.

Ø Comparing YOY, Renewable energy keeps strong however Green buildings & energy efficiency is becoming a larger segment

Ø Clean energy accounts for the largest allocation of green bond proceeds standing at USD6.8bn (30%) with wind and solar the dominant themes

Ø Low carbon transport is the second largest theme, accounting for 22% of proceeds raised

Sectors Financed by Green Bonds - China

CBI Principles Categories Use of Proceeds

III. COST & PRICE CONSIDERATIONS OFGREEN BONDS

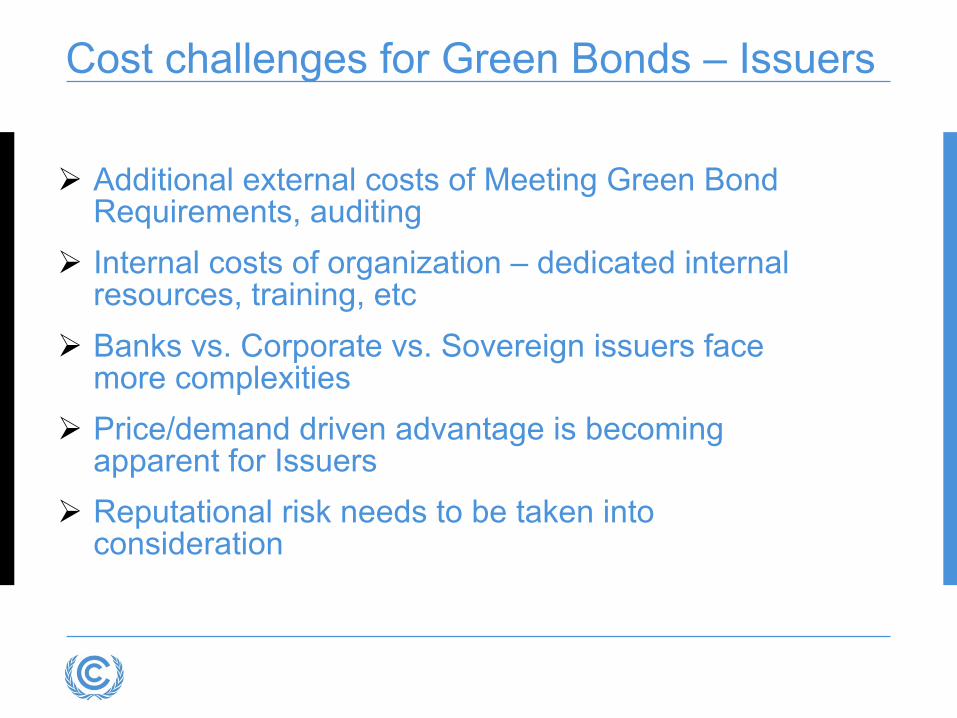

Ø Additional external costs of Meeting Green Bond Requirements, auditing

Ø Internal costs of organization – dedicated internal resources, training, etc

Ø Banks vs. Corporate vs. Sovereign issuers face more complexities

Ø Price/demand driven advantage is becoming apparent for Issuers

Ø Reputational risk needs to be taken into consideration

Cost challenges for Green Bonds – Issuers

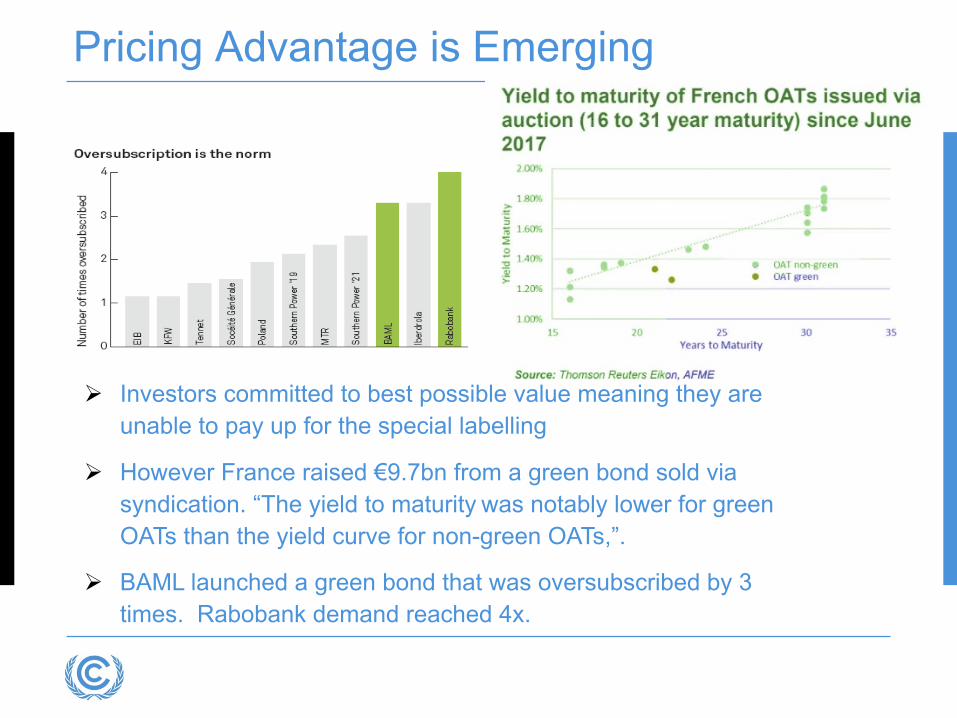

Pricing Advantage is Emerging

Ø Investors committed to best possible value meaning they are unable to pay up for the special labelling

Ø However France raised €9.7bn from a green bond sold via syndication. “The yield to maturity was notably lower for green OATs than the yield curve for non-green OATs,”.

Ø BAML launched a green bond that was oversubscribed by 3 times. Rabobank demand reached 4x.

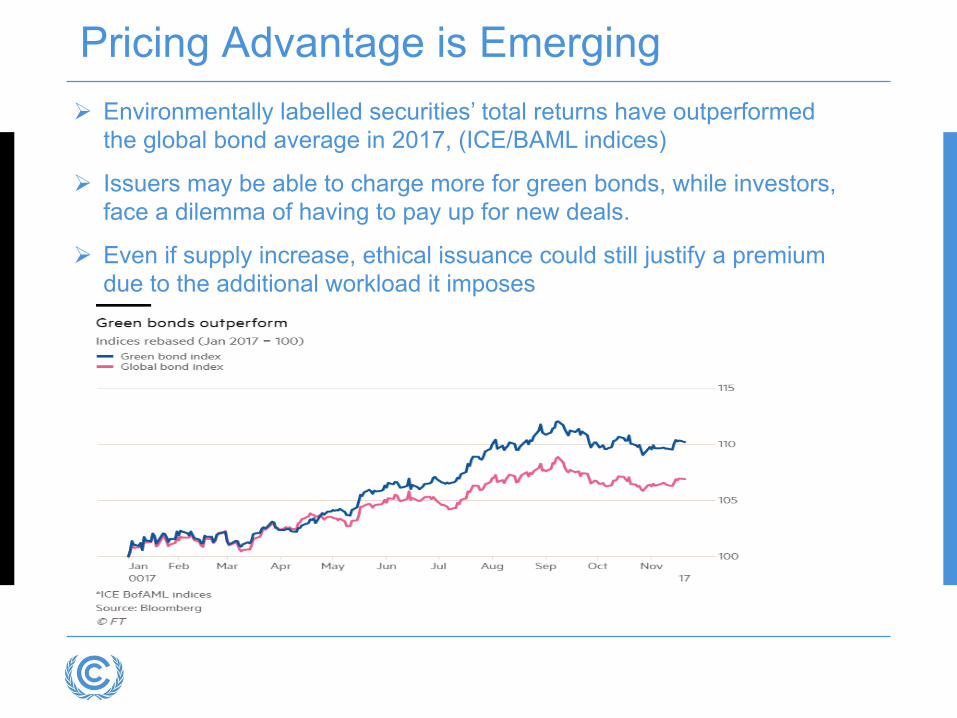

Ø Environmentally labelled securities’ total returns have outperformed the global bond average in 2017, (ICE/BAML indices)

Ø Issuers may be able to charge more for green bonds, while investors, face a dilemma of having to pay up for new deals.

Ø Even if supply increase, ethical issuance could still justify a premium due to the additional workload it imposes

Pricing Advantage is Emerging

Cost challenges for Green Bonds –investors perspective

Ø Lack of liquidity in the secondary market

Ø Lack of clear definition for Green Bonds

Ø Cost of due diligence/risk evaluation to verify that the proceeds of the bond/loan issue comply with a low-carbon, climate-resilient framework. Not relying solely on second party reviewers

Ø Overpaying for Green Labeled products while Facing more pressure and will to a portfolio transition

Ø Reputational risk

IV. INCENTIVES FOR GREENBONDS IN GLOBALMARKETS

Incentives for Green Bonds in the global market

Ø In 2017, Singapore Monetary Authority, the country’s central bank, announced their green bond grant scheme that will absorb the full cost of an external green bond review.

Ø This year, we have seen the launch of a three-year “Green Bond Grant Scheme” from Hong Kong, which will provide up to HKD800,000 (USD102,000) in subsidies for issuers.

Ø Malaysia: In 2017, the Securities Commission of Malaysia announced a tax incentive scheme for socially responsible (SRI) sukuk, including green sukuk, until 2020. The scheme encourages independent review of the green credentials of the sukuk.

Ø China: An additional type of government support seen in 2017 is China’s fast-tracking of green bond issuance approval.

Incentives for Green Bonds in the global market

Ø Tax credit bonds: bond investors receive tax credits instead of interest payments, so issuers do not have to pay interest on their green bond issuances

Ø Direct subsidy bonds: bond issuers receive cash rebates from the government to subsidize their net interest payments.

Ø Tax-exempt bonds: bond investors do not have to pay income tax (withholding) on interest from the green bonds they hold

“Calls to rewrite the mandate of the Monetary Policy Committee to include green objectives explicitly and called on the Bank of England to look at ways to build climate-related risks into its macroeconomic models” “central banks should do more to ensure

the availability of green finance and divest from fossil fuel companies that showed no inclination to change their business”

Incentives for Green Bonds in Global MarketØ Even if reaching $1trillion in next few years, the Green Bond

market is still very small

Ø Greater standardization of performance measurement could fuel growth. Consensus on what is green is key

Ø Meeting such standards imposes costs on issuers (especially the very important small issuers) and investors are not willing to pay for it

Ø Clear frameworks and guidance on labelling and impact, should though make it easier and cheaper for issuers to come to market

Ø Green Bonds Increased corporate disclosure and investor dialog with issuers may affect mainstream capital markets and ESG disclosure

V. CURRENT “GREENREACTION” ISSUERS / INVESTORSCONCLUSION

ISSUERS

INVESTORS

The growth momentum of Green Bonds action is strong. Here are some of the drivers of this process:

Investors are increasingly attracted by green bonds

• Meeting growing demand by consumers

• Balancing portfolio and risk mitigation

• Regulatory requirements

• Straightforward way to boost green credentials

Drivers for issuance

• Favorable government policies

• Diversification of investor base

• Brand enhancement

• Long Term Financing

• Growing investor demand for green

Current Green Reaction

UNFCCC/IGES - Regional Collaboration Center, Bangkok

Thank you! Yossef Zahar

Senior Climate Finance Advisor

+66 (0) 96-894-4918