grant allowability rules and ccageshanges … 1 grants...grant allowability rules and ccageshanges...

TRANSCRIPT

Grant Allowability Rules and Changes Under the OMB Uniform C a ges U de t e O U o

Grants Guidance

TIFFANY R. WINTERS, ESQ.BRUSTEIN & MANASEVITBRUSTEIN & MANASEVITWWW.BRUMAN.COMNOVEMBER 2014

1

WHY ARE THESE RULES IMPORTANT?

MARYLAND’S ARRA AUDIT REPORT

SEA Fiscal monitoring of LEAs inadequate Single audits did not uncover internal control and fiscal issues in LEAs

SEA did not require supporting expenditure documentation with the reimbursement requests (even on a sample or random basis).

SEA instrument included a step to review personnel expenditures, but no SEA instrument included a step to review personnel expenditures, but no findings

3

MARYLAND AUDIT (CONT)

LEA improper use of funds and inadequate documentationp p q

Nonpersonnel Expenditures- Unallowable $108,882 – unapproved travel (Title I)

$13,785 – obligation incurred before period of availability (SFSF)

$8,736 – gifts provided to staff (Title I)

$2,256 – overcharge for professional services (Title I)

$1,083 – advance payment to Turnaround Director for a rental car he did not usehe did not use

4

MARYLAND AUDIT (CONT.)

LEA improper use of funds and inadequate documentation Nonpersonnel Expenditures- Unallowable

$212 for a min-refrigerator and $199 for a microwave from Staples for personal use (SIG)

$4,352 – dinner cruises of Baltimore’s Inner Harbor (Title I)

5

MARYLAND AUDIT (CONT.)

LEA improper use of funds and inadequate documentation Nonpersonnel Expenditures- Inadequately supported

$22 741 d i did i l d h bill d i i $22,741 – documentation did not include hours billed on invoice

$1,425 – food (documentation did not show what the activity was or the number of people the food was ordered for)

$95,615 – utility costs charged to SFSF with no supporting documentation

6

MARYLAND AUDIT (CONT.)

LEA improper use of funds and inadequate LEA improper use of funds and inadequate documentation Personnel Expenditures- Baltimorep Time and effort certifications or PARs were not provided for

employees that were partially funded by grants

Extra-curricular activities / Professional Development

7

MARYLAND AUDIT (CONT.)

Technology At Risk of Being Used for Unauthorized Purposes Technology At Risk of Being Used for Unauthorized Purposes

Tablets purchased for all students and staff at Title I middle schoolsschools Teachers and staff allowed to take tablet home and use for personal

use

Policy against internet games not strictly enforced

13 of 37 tablets had apps for personal use – social networking sites, internet games, sporting sites, entertainment, music and religiong p g g

8

AGENDA

Background on Uniform Grants Guidance

Allowability Basic Cost Principles

Specific Items of Cost (Including Time and Effort Documentation)

G M S Grants Management Systems Financial Management, Procurement, Inventory

9

THE UNIFORM GRANTS GUIDANCE: WHAT IS COVERED?

A 21 C t R l R l IHE A-21 – Cost Rules – Rules – IHEs

A-87 – Cost Rules – State / Local Gov’t

A 122 C R l N f A-122 – Cost Rules – Nonprofit

A-102 – Administrative Rules State / Local Gov’t

A-110 – Administrative Rules IHEs

A-133 – Audit Rules

10

THE UNIFORM GRANTS GUIDANCE: THE UNIFORM GRANTS GUIDANCE: REASONS FOR THE CHANGE?

Si li i1. Simplicity

2. Consistency

3. Obama Executive Order on Regulatory Review

Increase Efficiency

Strengthen Oversight

11

KEY DATES:Key Dates

Feb 1 2013 Notice of Proposed RulemakingFeb 1, 2013 Notice of Proposed Rulemaking

Dec 26, 2013 Grants Guidance Published Federal Registerhttp://www.gpo.gov/fdsys/pkg/FR-2013-12-26/pdf/2013-p gp g y p g p30465.pdf

June 26 2014 Draft Regulations Due to OMBJune 26, 2014 Draft Regulations Due to OMB

August 29, 2014 COFAR Releases FAQs

Dec 26, 2014 Final Regulations Published

12

DATE OF APPLICABILITY OF REVISED RULES

COFAR FAQs: New awards and incremental Qfunding after 12/26/14 Applications for awards made after 12/26/14 should be developed in

accordance with Omni Circularaccordance with Omni Circular

Indirect cost rates will be developed in accordance with Omni Circular when due to be re-negotiated

One year grace period for procurementOne year grace period for procurement

Federal agencies may apply Omni Circular to unobligated funds as of the Federal award date of the first incremental funding received after 12/26/14

13

WHO IS COVERED?

All “nonfederal entities” expending federal All nonfederal entities expending federal awards

N F d l E tit 200 69 Non-Federal Entity 200.69

14

MOST SIGNIFICANT GENERAL CHANGES

Shift f f C pli t f Shift from focus on Compliance to focus on PERFORMANCE!!!

A dit (A 133 + F d l OIG) d M it (F d l Auditors (A-133 + Federal OIG) and Monitors (Federal and State Pass Through) must look more to “outcomes” than to “process”

The Omni Circular adds significant flexibility to way grantees / subgrantees can adopt their own processes

15

MOST SIGNIFICANT GENERAL CHANGES (CONT.)

The Omni Circular has a MAJOR emphasis on “strengthening accountability” by improving policies that g g y y p g pprotect against waste, fraud and abuse

16

NEW: REQUIRED CERTIFICATIONS 200.415

NEW: Official authorized to legally bind the non-federal entity must certify on annual and final fiscal reports or must certify on annual and final fiscal reports or vouchers requesting payment:

“By signing this report, I certify to the best of my knowledge and belief that the report is true, complete and accurate and the expenditures, disbursements and cash receipts are for the purposes and objectives set forth in the terms and conditions of the federal jaward. I am aware that any false, fictitious, or fraudulent information or the omission of any material fact, may subject me to criminal civil or administrative penalties for fraud, false statements, false claims, or

17

p , , ,otherwise.”

THE MORE ATTENTION PAID TO FINANCIAL MANAGEMENT CONTROLS, FEWER HEADACHES DOWN

THE ROAD!!!THE ROAD!!!

18

FINANCIAL MANAGEMENT CONTROLSCONTROLS

THE KEY COMPONENT TO FEDERAL GRANTS

CROSSWORK BETWEEN CURRENT RULE AND OMNI CIRCULAR 200.302(B)

34 CFR 80.20(b) 2 CFR 200.302 (b)1 Identification of Awards (NEW)

1. Financial Reporting

2. Accounting Records

3 Internal Control

1. Identification of Awards (NEW)

2. Financial Reporting

3. Accounting Records (Source Docs)3. Internal Control

4. Budget Control

5. Allowable Cost

4. Internal Control

5. Budget Control

W C h M P d 6. Source Documentation

7. Cash Management

6. Written Cash Management Procedures (NEW)

7. Written Allowability Procedures (NEW)

20

1) IDENTIFICATION OF AWARDS (NEW)

All federal “awards” received and expended

The name of the federal “program”

Identification # of award

CFDA Title and Number CFDA Title and Number

Federal Award I.D. #

Fiscal Year of Award

Federal Agency

Pass-Through (If S/A)

21

2) FINANCIAL REPORTING

New shift to OMB approved approved performance metricsmetrics

22

2) FINANCIAL REPORTING 2) FINANCIAL REPORTING (CONT.)

Generally requires accurate, current, complete disclosure of financial results of each award

NEW: 200.327 – Federal awarding agency can only collect OMB approved data g g y y ppelements, no less than annually, no more than quarterly

NEW: 200.328 – Non federal entity must submit performance reports at intervals required by federal agency or pass through. intervals required by federal agency or pass through.

Annual performance reports due 90 days after reporting period; Quarterly performance reports due 30 days after reporting period

23

2) FINANCIAL REPORTING (CONT.)

NEW Performance Metrics:1. Compare actual accomplishments to objectives. (quantify to

extent possible)

2 Reasons goals were not met if appropriate2. Reasons goals were not met if appropriate

4. Additional pertinent information (e.g. analysis and explanation of cost overruns, high unit costs) Significant developments

a. Problems, delays. Adverse conditions that would impair ability to meet objective of the award

b Favorable developments Finishing sooner or at less costb. Favorable developments. Finishing sooner or at less cost24

3) ACCOUNTING RECORDS (SOURCE DOCUMENTATION)

Combines current requirements 80.20(b)(2) and 80.20(b)(6):

Source Documentation Must Be Kept On: Source Documentation Must Be Kept On:

1. Federal Awards

2. Authorizations

3. Obligations

4. Unobligated balances

5 A t5. Assets

6. Expenditures

7. Income

8. Interest (New) (Eliminated liabilities) 25

CASH MANAGEMENT

Payment Process

O Obligation

Liquidation

D d Drawdown

Payment

Obligation = Transaction that requires payment

26

WHEN ITEMS OBLIGATE

Type of Obligation When Obligation Occurs

Acquisition of Property Date of binding written commitment

Personal Servicesby Employee

When services are performed

Personal Services by Contractor

Date of binding written commitment

Travel When travel is taken 27

OBLIGATIONS (CONT.)

Grantees and subgrantees may begin to obligate funds when: Awarding agency approves application; orAwarding agency approves application; or

Awarding agency determines application is “substantially approvable”

Reimbursement subject to final Reimbursement subject to final approval

28

OBLIGATIONS (CONT.)

Tydings Amendment

Allows extra year to obligate funds

Does not apply to all grants

Under Tydings funds are available for 24 27 months: Under Tydings, funds are available for 24-27 months:

12-15 months under the grant award

(July 1, 2013 – September 30, 2014)(J y , p , )

Plus 12 months (carryover period)

(October 1, 2014 – September 30, 2015)

29

OBLIGATIONS (CONT.)

Under Tydings, unobligated funds can usually be “carried over” from first year

Generally, no limit on “carryover” unless stated

Title I Part A = 15% SEA may waive every 3 years (additional waiver b/c of Title I, Part A = 15%, SEA may waive every 3 years (additional waiver b/c of ARRA)

IDEA = no limit

Perkins = No carryover

30

30

4) INTERNAL CONTROLS

Essentially same as current requirements under 80.20(b)(3):

Effective control over and accountability for:

1. All funds

2. Property

3. Other assets

M t d t l f d ll t Must adequately safeguard all assets

Use assets solely for authorized purpose

31

4) INTERNAL CONTROL 200.303

New: Internal controls “should” be in compliance with: The U.S. Comptroller General’s Standard for Internal Control p

Integrated Framework; and

Internal Control Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission Sponsoring Organizations of the Treadway Commission

32

4) INTERNAL CONTROL 200.303 (CONT.)

Internal Controls must ensure compliance with federal pstatutes, regs, terms of the award.

Entities must: Evaluate and monitor compliance

Take prompt action when instances of noncompliance are identified; and and

Safeguard protected personally identifiable information (PII)

33

COMPONENTS OF INTERNAL COMPONENTS OF INTERNAL CONTROLS

ControlEnvironment

ControlActivities

Information and

Communications

RiskAssessment Monitoring

3434

CONTROL ENVIRONMENT

Allows management and employees to maintain a positive and supporting attitude toward compliancesupporting attitude toward compliance

Maintaining a level of competence that allows personnel to accomplish their assigned duties

Clearly defined organizational structure

Proper amounts of supervision

Maintaining a good relationship with oversight agencies (like ED and OIG for example!)

3535

CONTROL ENVIRONMENT (CONT.)

Examples:Examples:

Well-written policies and procedures manuals

Addressing employee responsibilities, limits to authority, g p y p yperformance standards, control procedures, conflict of interests and reporting relationships.

Organizational chartOrganizational chart

Clear job descriptions

Adequate training programs and performance evaluations.

36

RISK ASSESSMENT

You are all at risk for noncompliance You are all at risk for noncompliance

(and probably already are noncompliant!)

Determine internal and external risks to obtaining agency objectives: What could go wrong (or has gone wrong)?

What assets do we need to protect?

How could someone steal or disrupt operations?

What information do we rely on?What information do we rely on?37

RISK ASSESSMENT (CONT.)

Risks are not stagnate; they increase and change as laws and operational environments change and operational environments change.

Examples: New personnel

More Examples: Change in Laws and Regulations

Experienced personnel Lack of personnel Reorganizations C R d i S i

New Technology New Grants Competition R id h Cost Reduction Strategies Rapid growth

38

RISK ASSESSMENT (CONT.)

High

Once risks are identified, conduct risk analysis:

Assess the likelihood (or

Risk J d tAssess the likelihood (or

frequency) of risk occurring

Estimate the potential impact if the risk were to

kL

JudgmentRequired

poccur

Determine how the risk should be managed

Low

Low HighImpactg

39

CONTROL ACTIVITY EXAMPLES

S K R b l Segregating Key Responsibilities

Restricting Access to Systems and Records (Authorizations / Passwords)

Implementing Clear Written Policies in Key Areas Implementing Clear Written Policies in Key Areas

Maintaining Physical Control Over Valuable Assets (Security)

Maintaining Appropriate Documentation (Approvals, Record Retention)g pp p ( pp , )

Accurate and Timely Recording of Information

Check for accounting of transactions in numerical sequence

40

INFORMATION AND COMMUNICATIONS

Goal: Ensure personnel receive relevant, reliable and timely p , yinformation that enables them to carry out their responsibilities.

Develop procedures for identifying pertinent information and distributing it in a form and timeframe that permits people to distributing it in a form and timeframe that permits people to perform their duties efficiently.

All personnel must receive a clear message from top down that control responsibilities must be taken seriously control responsibilities must be taken seriously.

Personnel must understand how they relate to one another in the system.

41

MONITORING

Goal: Assess the quality of internal controls over time and f d l l densure any findings are promptly resolved.

Ongoing program and fiscal monitoring Regular oversight by supervisors Record reconciliation Formal program reviews/audits OMB Circular A-133 audits

Include policies and procedures for correcting any findings in a timely mannerg y

42

5) BUDGET CONTROL

Same as current rule 80.20(b)(4)

Comparison of expenditures with budget amounts for each award

43

6) WRITTEN CASH MANAGEMENT PROCEDURES (NEW)

Written Procedures to implement the Written Procedures to implement the requirements of 200.305

44

6) WRITTEN CASH MANAGEMENT PROCEDURES

For states, payments are governed by Treasury –State CMIA agreements 31 CFR Part 205State CMIA agreements 31 CFR Part 205

No Change

For all other non federal entities, payments must i i i i l i b d f G 5 d minimize time elapsing between draw from G-5 and

disbursement (not obligation)

45

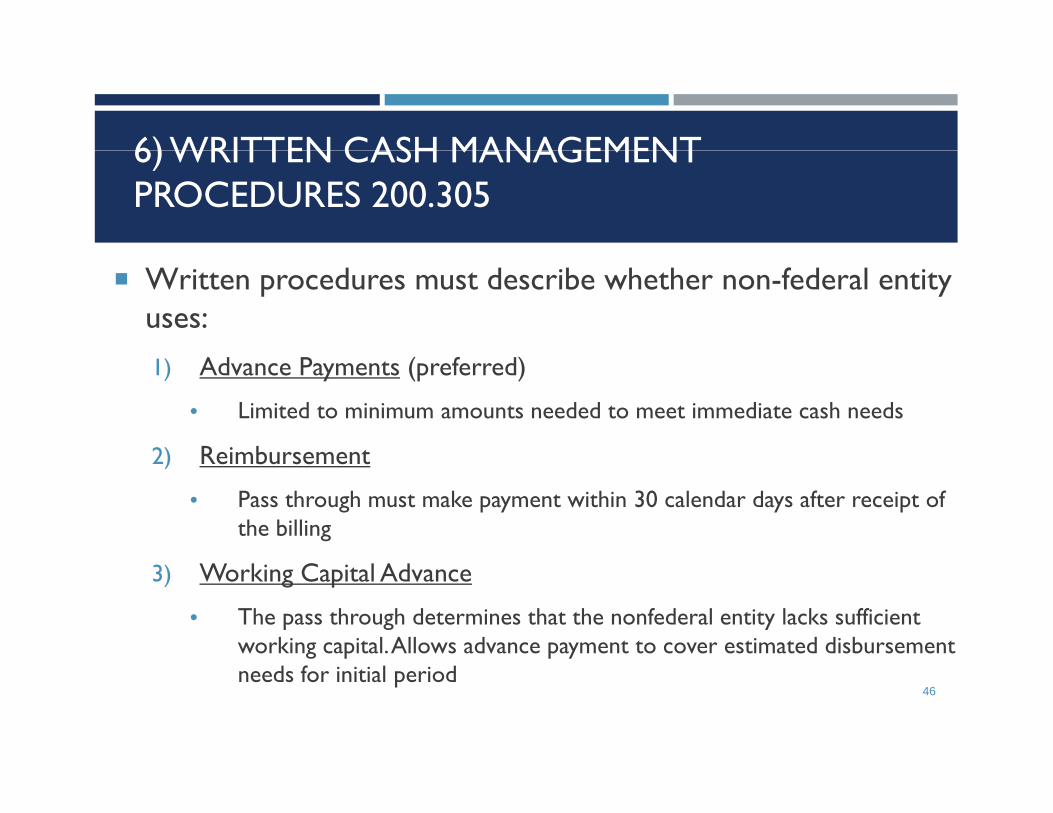

6) WRITTEN CASH MANAGEMENT 6) WRITTEN CASH MANAGEMENT PROCEDURES 200.305

Written procedures must describe whether non-federal entity uses:1) Advance Payments (preferred)

• Limited to minimum amounts needed to meet immediate cash needs

2) Reimbursement2) Reimbursement

• Pass through must make payment within 30 calendar days after receipt of the billing

3) Working Capital Advance

• The pass through determines that the nonfederal entity lacks sufficient working capital. Allows advance payment to cover estimated disbursement needs for initial period

46

6) WRITTEN CASH MANAGEMENT 6) WRITTEN CASH MANAGEMENT PROCEDURES 200.305 (CONT.)

NEW:Advances must be maintained in insured accounts

NEW: Pass through cannot require separate depository accounts

NEW: Accounts must be interest bearing unless:A f d l d d $120 0001. Aggregate federal awards under $120,000

2. Account not expected to earn in excess of $500 per year

3. Bank require minimum balance so high, that such account not feasibleq g ,47

6) WRITTEN CASH MANAGEMENT 6) WRITTEN CASH MANAGEMENT PROCEDURES 200.305 (CONT.)

NEW: Interest amounts up to $500 may be retained by non federal entity for administrative purposes Currently $100 for State and local Gov’ts

Currently $250 for IHEs and Non-profits.

Interest earned must be remitted annually to /DOLED/HHS, etc.

48

7) WRITTEN ALLOWABILITY PROCEDURES

NEW: Written procedures for determining allowability of costs in accordance with Subpart E –Cost Principles

49

7) WRITTEN ALLOWABILITY PROCEDURES 7) WRITTEN ALLOWABILITY PROCEDURES (CONT.)

Procedures can not simply restate the Uniform Guidance Subpart E

Should explain the process used throughout the grant development and budget process

Training tool and guide for employees Training tool and guide for employees

50

SUBPART E SUBPART E –COST PRINCIPLES

51

COST PRINCIPLES: “FACTORS AFFECTING ALLOWABILITY OF COSTS” 200.403

All Costs Must Be:1. Necessary, Reasonable and Allocable

2. Conform with federal law & grant terms

3 C i t t ith t t d l l li i 3. Consistent with state and local policies

4. Consistently treated

5. In accordance with GAAP

6. Not included as match

7. Net of applicable credits (moved to 200.406)

528. Adequately documented

NECESSARY & REASONABLE 200.404

Necessary and Reasonabley Must be necessary for the performance or administration of the grant

Must follow sound business practices:

A l h b i i (hi ) Arms length bargaining (hint: procurement processes)

Follow federal, state and local laws

Follow terms of the grant award

Fair market prices

Act with prudence under the circumstances

No significant deviation from established prices No significant deviation from established prices53

NECESSARY & REASONABLE (CONT.)

Practical aspects of “necessary”p y Do I really need this?

Is the expense targeted to valid programmatic/administrative need?

Is this the minimum amount I need to spend to meet my need?

Do I have the capacity to use what I am purchasing?

Practical aspects of “reasonable” Did I pay a fair rate? Can I prove it?

f f f ? If I were asked to defend this purchase, would I be comfortable?54

ALLOCABLE 200.405

Allocable: can only charge in proportion to the value received by the program

0% Example: Agency purchases a computer to use 50% on the grant program and 50% on a state program – can only charge half the cost to the grant

55

BASIC GUIDELINES

Be consistent with policies and procedures that apply uniformly to both federally- financed and other activities of the non-Federal entity.

Conform with federal law & grant terms

Example: Match RequirementsExample: Match Requirements

56

BASIC GUIDELINES (CONT.)

Consistently treated Cannot assign cost as direct cost if its

already allocated as an indirect costalready allocated as an indirect cost

In Accordance with GAAP

Not Included as Match Not Included as Match see also 200.306

57

BASIC GUIDELINES (CONT.)

Adequately documented

Amount of funds under grant

How the funds are used

Total cost of the project

Share of costs provided by th other sources

Records that show compliance

Records that show performance

Other records to facilitate an effective audit

Electronic copies ok Electronic copies ok See new Omni Rules 58

APPLICABLE CREDITS 200.406

Those receipts or reduction-of-expenditure type transaction that offset or reduce expense items – must be credited to the Federal award as either cost reduction or cash refund, as ,appropriate. Examples: purchase discounts, rebates or allowances, recoveries or

i d iti l i f d b t dj t t f indemnities on losses, insurance refunds or rebates, adjustments of overpayments

59

PRIOR WRITTEN APPROVAL 200.407

NEW: In order to avoid subsequent disallowance:

Non-Federal entity may seek prior written approval of cognizant agency (for indirect cost rate) or Federal awarding agency in advance of the incurrence of special or unusual costs

60

PROGRAM INCOME 200.307

Non-Federal entities are encouraged to earn income to defray program costs where appropriate where appropriate.

Costs of generating program income may only be deducted if:

Authorized by federal regulations or the Federal award;

Costs are incidental and not charged to the Federal award.

Property from the sale of real property or equipment is not program income – apply post award property rules.

Program Income Must Be Deducted from Total Allowable Costs (except for IHEsand Research Non-profits)

With prior approval may add to Federal award 61

With prior approval may add to Federal award.

DIRECT V. INDIRECT COSTS 200.413

NEW: Salaries of administrative and clerical staff should be treated as “indirect” unless all of following are met:

S h l h 1. Such services are integral to the activity

2. Individuals can be specifically identified with the activity

3. Such costs are explicitly included in the budget

4. Costs not also recovered as indirect

62

CONTRACT VS. GRANT 200.330

No change from the current requirement.

Entities must clearly determine what is a subgrant and what is a contract. Note the difference!!

63

SELECTED ITEMS OF SELECTED ITEMS OF COST

THE “OMNI” NOW HAS 55 SPECIFIC ITEMS OF COST!

200.420

SELECTED ITEMS OF COST EXAMPLES

Advertising/PR 200.421 (Clarified) ◦ Allowable for programmatic purposes including:◦ Recruitment◦ Procurement of goods

Di l f t i l◦ Disposal of materials◦ Program outreach◦ Public relations (in limited circumstances)

Alcohol 200.423◦ Not allowable

65

SELECTED ITEMS OF COST (CONT)

Conferences 200.432 (Changed) Prior Rule: Generally allowable Prior Rule: Generally allowable

Includes Meals / Conferences / Travel and Family Friendly Policies

Allowable conference costs include rental of facilities, costs of meals and ,refreshments, transportation, unless restricted by the federal award

New: Costs related to identifying, but not providing, locally available dependent-care resources dependent-care resources

New: But 200.474 “travel” allows costs for “above and beyond regular dependent care”

66 Conference hosts must exercise discretion in ensuring costs are appropriate,

necessary and managed in manner than minimizes costs to federal award

SELECTED ITEMS OF COST (CONT)

NEW: Collections of Improper Payments The costs incurred by the non-Federal entity to recover improper

payments are allowable as either direct or indirect costs, as appropriate.

67

SELECTED ITEMS OF COST (CONT)

Entertainment Costs 200.438 (Clarified)( ) Cost of entertainment are unallowable

Amusement, Diversion, Social Activities

Except where costs might otherwise be considered programmatic and are Except where costs might otherwise be considered programmatic and are authorized or have prior written approval of the Federal awarding agency.

Fines, Penalties, Damages and other Settlements 200.441 If l d i l i ll d i l i f il l i h F d l If related to violation, alleged violation or failure to comply with Federal, state,

tribal, local or foreign law and regulations then unallowable.

Except with prior written approval of Federal awarding agency.

68

SELECTED ITEMS OF COST (CONT.)

Travel Costs 200.474 (Changed)

P i l ll bl i h i i iPrior rule: allowable with certain restrictions

Travel costs may be charged on actual, per diem, or mileage basis

Travel charges must be consistent with entity’s written travel Travel charges must be consistent with entity s written travel reimbursement policies

Grantee must retain documentation that participation of i di id l i f i f h jindividual in conference is necessary for the project

Travel costs must be reasonable and consistent with written travel policy / or follow GSA 48 CFR 31.205-46(a)

69

TIME AND EFFORT DOCUMENTATION

70

TIME AND EFFORT (CURRENT A-87 RULE)

Semi-Annual Certifications

If an employee works on a single

Personnel Activity Report (PAR)

If an employee works on multiple If an employee works on a single cost objective: After the fact

If an employee works on multiple cost objectives: After the fact

Account for the total activity Signed by employee or

supervisor

Account for total activity Signed by employee Prepared at least monthly and p

Every six months (at least twice a year)

Prepared at least monthly and coincide with one or more pay periods

71

TIME DISTRIBUTION RECORDS

Must be maintained for all employees whose salaries are: Paid in whole or in part with federal funds

Used to meet a match/cost share requirement

72

REQUIRED TIME DISTRIBUTION REQUIRED TIME DISTRIBUTION DOCUMENTATION

Type of documentation depends on how many “cost objectives” the employee worked onobjectives the employee worked on

These cost objectives must be connected to the employee’s salary source

What is a cost objective?◦ A specific grant award or other category of costs that ◦ A specific grant award, or other category of costs, that

requires the grantee to track specific cost information

73

MULTIPLE ACTIVITIES OR COST MULTIPLE ACTIVITIES OR COST OBJECTIVES

More than one Federal award.Ti l I i Ti l I i bl i◦ Title I program services v. Title I equitable services

◦ 21st CCLC program services v. adminisitration

A Minimum Set-Aside or Maximum Cap:◦ Title I- LEA Parent Involvement minimum (at least 1%);

Titl III C d i i t ti ( th 2%)◦ Title III – Cap on administration (no more than 2%)

A Federal award and a non-Federal award.

OCFO CLARIFICATIONS RE “SINGLE OCFO CLARIFICATIONS RE: “SINGLE COST OBJECTIVE”

OCFO: “The criteria for whether an employee may document time and effort using a may document time and effort using a

semiannual certification or must fill out a monthly PAR can be confusing.monthly PAR can be confusing.

OCFO GUIDANCE

It is possible for multiple programs to have the same cost objective, which creates confusion over whether the presence of a single cost objective or being funded by multiple programs should determine what time-and-effort documentation and employee must complete.p y p

OCFO GUIDANCE (CONT.)

It is possible to work on a single cost objective even if an employee works on more than one Federal award or on a p yFederal award and a non-Federal award.

The key to determining whether it is a single cost objective is whether the employee’s salary and wages

b pp t d i f ll f h f th F d l d can be supported in full from each of the Federal awards on which the employee is working or from the Federal award alone if the employee’s salary is also paid with non-Federal funds.

A 87 SINGLE COST OBJECTIVES A-87 SINGLE COST OBJECTIVES –SEMI-ANNUAL CERTIFICATION

If an employee works on a single cost objective:◦ Semi-Annual Certification◦ Signed by employee or supervisor ◦ Every six months (at least twice a year)◦ After the FactAfter the Fact◦ Account for 100% of the activity

Example: “I, Tiffany Winters, hereby certify that for the period January 1, 2012 through June 30, 2012 one-hundred percent (100%) of my time and effort was spent on percent (100%) of my time and effort was spent on 21stCCLC Administration.” 78

A 87 MULTIPLE COST OBJECTIVES A-87 MULTIPLE COST OBJECTIVES –PERSONNEL ACTIVITY REPORT (PAR)

If an employee works on multiple cost objectives:

Personnel Activity Report (PAR) or equivalent documentation

After the fact

Account for total activity Account for total activity

Signed by employee

Prepared at least monthly and coincide with one or more pay p y p yperiods

79

OCFO GUIDANCE EXAMPLES OF SINGLE OCFO GUIDANCE EXAMPLES OF SINGLE COST OBJECTIVES:

Title I, Part A funds and State compensatory education funds

An LEA supports a supplemental math teacher to serve low-achieving students with 50 percent Title I, Part A funds and 50 percent State compensatory education funds50 percent State compensatory education funds.

OCFO GUIDANCE EXAMPLES OF SINGLE OCFO GUIDANCE EXAMPLES OF SINGLE COST OBJECTIVES:

Title I, Part A funds and local funds

A teacher in a Title I schoolwide school is paid with local funds to teach first grade in the morning to decrease class size for reading and is paid with Title I Part A funds to teach size for reading and is paid with Title I, Part A funds to teach a supplemental reading recovery class in the afternoon. (The school has a sufficient number of first-grade teachers

h i f ESEA i 1114( )(2)(B) )to meet the requirements of ESEA section 1114(a)(2)(B).)

OCFO GUIDANCE EXAMPLES OF SINGLE COST OCFO GUIDANCE EXAMPLES OF SINGLE COST OBJECTIVES:

Title I, Part A funds and local funds (cont.)

Because the part-time first-grade teacher is not needed in order t id th b i d ti i th h l id to provide the basic education program in the schoolwide program school, her salary could be supported with Title I, Part A funds, even though it is not.

Similarly, her salary for providing reading recovery could be supported with Title I, Part A funds.

Both her functions, therefore, are fully supportable with Title I, , , y pp ,Part A funds, and the schoolwide program constitutes a single cost objective.

OCFO GUIDANCE EXAMPLES OF SINGLE OCFO GUIDANCE EXAMPLES OF SINGLE COST OBJECTIVES:

Funds under Sections 611 and 619 of the Individuals with Disabilities Education Act (IDEA)

A preschool special education teacher is funded with 50 percent IDEA section 611 funds and 50 percent with IDEA section 619 fundssection 619 funds.

Teaching preschool special education is an allowable activity under both IDEA sections 611 and 619.

OCFO GUIDANCE EXAMPLES OF SINGLE OCFO GUIDANCE EXAMPLES OF SINGLE COST OBJECTIVES:

Title I, Part A funds and CEIS (comprehensive early intervening services) funds under IDEA

A teacher works with low-achieving students and is supported with 60 percent Title I, Part A funds and 40

t CEIS f dpercent CEIS funds.

Teaching low-achieving students is a single cost objective because it can be fully supported under both Title I Part A because it can be fully supported under both Title I, Part A and CEIS.

OCFO GUIDANCE EXAMPLES OF SINGLE OCFO GUIDANCE EXAMPLES OF SINGLE COST OBJECTIVES:

Title I, Part A funds and local funds

An LEA s rts an elementar sch l teacher ith l cal f nds An LEA supports an elementary school teacher with local funds but pays her with Title I, Part A funds to provide after-school tutoring for low-achieving students.

Although the teacher could not be paid with Title I, Part A funds to provide elementary education, the portion of her time spent on after-school tutoring is easily separated from her teaching g y p gposition by her schedule.

BRUMAN GAME:WHY ARE THESE EXAMPLES

WRONG?

SEMI-ANNUAL CERTIFICATION EXAMPLES

I, Justin Beiber, certify that I worked solely on the Federal I, Justin Beiber, certify that I worked solely on the Federal Grant program from January 1, 2014 to June 30, 2014.

Signature of Employee

____/s/__________________ ______________

Date: September 1, 2014

SEMI-ANNUAL CERTIFICATION EXAMPLES

I, Taylor Swift, certify that I worked 100% of my time on Title I, Taylor Swift, certify that I worked 100% of my time on Title I,A Administration from January 1, 2014 to June 30, 2014.

Signature of Employee

____/s/__________________ ______________

Date: June 20, 2014

SEMI-ANNUAL CERTIFICATION EXAMPLES

I, Julia Roberts, certify that I worked 100% of my time on Title I A hi l f J 1 2014 J 30 I,A program teaching class from January 1, 2014 to June 30, 2014.

Signature of District Superintendent

/s/____/s/______________

Date: July 2, 2014

SEMI-ANNUAL CERTIFICATION EXAMPLES

January 1 through June 30, 2014

I, Barack Obama, certify that I worked solely on project, initiatives, and issues which have implications and consequences based and/or related to Federal programs and policies. p g p

Signature of Employee Signature of Supervisor

____/s/______________ ____/s/_______________

Date: June 30, 2014 Date: August 2, 2014

PAR EXAMPLES

I certify that for the month of December 2013 I, Lady Gaga, spent my time working on the following programs:y g g p g

Title I, Admin 100%

State programs 100%____

Total 200%

Signed: ___/s/____

January 5, 2014

PAR EXAMPLES

I certify that for the month of August 2014 I, Michelle Obama, spent my time working on the following programs:

Title I, Admin 20%

State programs 30%____

Total 50%

Signed: ___/s/____

September 10, 2014

PAR EXAMPLES

Dear Employee:

Please sign the pre-populated form if accurate.

I certify that for the month of July 2014, Ashton Kutcher, spent my time working on the following programs:

Title I, Admin 75%

State programs 25%State programs 25%____

Total 100%

Signed: /s/Signed: ___/s/_______

August 5, 2014

SUBSTITUTE SYSTEMS GENERALLY

OMB Circular A-87 authorizes the use of substitute systems for allocating salaries and wages.

ED must approve SEA’s system. Can include:

Random moment sampling

Case counts

Other quantifiable measures of employee effort

SUBSTITUTE SYSTEM CHANGES

An SEA would be permitted to allow an LEA to use alternative documentation through approved substitute system documentation through approved substitute system.

For example, could use a teacher's course schedule (instead of PARs) for an individual who works on multiple activities or cost objectives

but

does so on a predetermined schedule.

An individual documenting time and effort under the substitute system would be permitted to certify time and effort on a system would be permitted to certify time and effort on a semiannual basis, provided certain requirements are met.

THE UNIFORM GRANTS GUIDANCE THE UNIFORM GRANTS GUIDANCE: TIME AND EFFORT RULE

New Name: Time Distribution Records “Standards for Documentation of Personnel Expenses” If federal funds are used for salaries, then time

di t ib ti d i ddistribution records are required.

How staff demonstrate allocability Paid in whole or in part with federal funds 200 430 (i)(1) Paid in whole or in part with federal funds 200.430 (i)(1) Used to meet a match/cost share requirement 200.430(i)(4)

96

COST OBJECTIVES 200.28

What is a cost objective? (slightly changed)• Program, function, activity, award, organizational subdivision,

c ntract r rk nit f r hich c st data are desired and contract, or work unit for which cost data are desired and for which provision is made to accumulate and measure the cost of processes, products, jobs, capital projects, etc.

97

“STANDARDS FOR DOCUMENTATION OF PERSONNEL EXPENSES” 200.430

NEW: Charges for salaries must be based on records that accurately reflect the work performed

1. Must be supported by a system of internal controls which provides reasonable assurance charges are accurate, allowable

d l ll dand properly allocated

2. Be incorporated into official records

3. Reasonably reflect total activity for which employee is compensated

N t t d 100% Not to exceed 100%98

“STANDARDS FOR DOCUMENTATION OF PERSONNEL EXPENSES” 200.430 (CONT)

4. Encompass all activities (federal and non-federal)

5. Comply with established accounting polices and practices

6. Support distribution among specific activities or cost objectivesobjectives

99

“STANDARDS FOR DOCUMENTATION OF PERSONNEL EXPENSES” 200.430 (CONT)

Budget estimates alone do not qualify as support for g q y ppcharges to Federal awards 200.430(i)(1)(viii)

NEW: Percentages may be used for distribution of NEW: Percentages may be used for distribution of total activities 200.430(i)(1)(ix)

100

“STANDARDS FOR DOCUMENTATION OF PERSONNEL EXPENSES” 200.430 (CONT)

Grantees encouraged to adopt “substitute systems” if approved by cognizant agency for indirect cost 200.430(i)(5)

Acceptable to allocate sampled employees’ supervisors, clerical and support staffs, based on

lt f l d lresults of sampled employees

101

“STANDARDS FOR DOCUMENTATION OF PERSONNEL EXPENSES” 200.430 (CONT)

NEW: If records meet the standards: the non-federal entity will NOT be required to provide additional support or documentation for the work performed (200.430(i)(2))f p f ( ( )( ))

BUT, if “records” of grantee do not meet new standards, ED may require PARs (200.430(i)(8)) PARs are not defined!!

102

Procurement

BRUSTEIN & MANASEVIT, PLLC 103

PROCUREMENT STANDARDS

State, Local and Tribal Governments:

States may use their own procurement policies and procedures to y p p pprocure equipment.

Other grantees and subgrantees must follow policies and procedures that meet the standards set out in EDGAR 80.36.that meet the standards set out in EDGAR 80.36.

Omni Circular - 200.317 Still provides flexibility for States; all other nonfederal entities follow

policies and procedures under Section 200.318-200.326.

BRUSTEIN & MANASEVIT, PLLC 104

PROCUREMENT STANDARDS 200.308

NEW: Omni Circular : All nonfederal entities must have documented procurement procedures which reflect applicable Federal, State, and local laws and regulations.

BRUSTEIN & MANASEVIT, PLLC 105

OPEN COMPETITION

All procurement transactions must be conducted with full and open competition.p p Must have protest procedures to handle disputes

To eliminate unfair advantage, contractors that develop or draft specifications, requirements, statement of work, and invitations for bids or RFPs must be excluded from competing for such for bids or RFPs must be excluded from competing for such procurements. Now applicable to all nonfederal entities (200.319(a))

BRUSTEIN & MANASEVIT, PLLC 106

OPEN COMPETITION

Situations that restrict competition: Unreasonable requirements on vendors to qualify to do businessq q y

Pre-qualified lists should not limit competition

Requiring unnecessary experience or excessive bonding

Noncompetitive pricing practices Noncompetitive pricing practices

Noncompetitive awards to consultants on retainer

Organizational conflicts of interest

Specifying a brand name

Any arbitrary action in the procurement process

In-state or local preferences

BRUSTEIN & MANASEVIT, PLLC 107

CONFLICT OF INTEREST

Must maintain written standard of conduct, including conflict of interest policyinterest policy.

A conflict of interest arises when any of the following has a financial or other interest in the firm selected for award: Employee, officer or agent

Any member of that person’s immediate family

That person’s partner

An organization which employs, or is about to employ, any of the above or has a financial interest in the firm selected for award

BRUSTEIN & MANASEVIT, PLLC 108

CONFLICT OF INTEREST

If the non-federal entity has a parent, affiliate, or subsidiary organization that is not a state or local government the entity organization that is not a state or local government the entity must also maintain written standards of conduct covering organization conflicts of interest! 200.318(b)(2)

NEW: All non federal entities must establish conflict of interest policies and disclose in writing any potential conflict to policies, and disclose in writing any potential conflict to federal awarding agency in accordance with applicable Federal awarding agency policy. 200.112

BRUSTEIN & MANASEVIT, PLLC 109

COST/PRICE ANALYSIS

Must perform a cost or price analysis in connection with every procurement action, including contract modifications

NEW (200.323): Only required for costs in excess of the simplified acquisition threshold ($150,000)

Cost analysis generally means evaluating the separate cost elements that make up the total price (including profit)

P i l i ll l i h l i Price analysis generally means evaluating the total price

BRUSTEIN & MANASEVIT, PLLC 110

VENDOR SELECTION PROCESS 200.320

Method of procurement:p NEW: Micro-purchase

Small purchase procedures

Competitive sealed bids

Competitive proposals

Noncompetitive proposals

BRUSTEIN & MANASEVIT, PLLC 111

VENDOR SELECTION PROCESS: MICRO-PURCHASE 300.320(a)

NEW: Acquisition of supplies and services under $3,000 or less.

May be awarded without soliciting competitive quotations if nonfederal entity considers the cost reasonable considers the cost reasonable.

To the extent practicable must distribute micro-purchases equitably among qualified suppliers.

BRUSTEIN & MANASEVIT, PLLC 112

VENDOR SELECTION PROCESS SMALL PURCHASE VENDOR SELECTION PROCESS: SMALL PURCHASE PROCEDURES

Good or service that costs $100,000 or less (NEW: $150,000 (under 200.88) Organization may set lower threshold

Must obtain price or rate quotes from an adequate number of qualified sources

“R l l l d f l” “Relatively simply and informal”

BRUSTEIN & MANASEVIT, PLLC 113

VENDOR SELECTION PROCESS

Can only contract with responsible contractors possessing the ability to f f llperform successfully:

Contractor integrity

Compliance with public policyp p p y

Record of past performance

Financial and technical resources

200.318(h)

BRUSTEIN & MANASEVIT, PLLC 114

VENDOR SELECTION PROCESS: NONCOMPETITIVE PROPOSALS

Appropriate only when: The good or services is available only from a single source (sole source)

There is a public emergency

The awarding agency authorizes

NEW: awarding agency or pass-through must expressly authorize noncompetitive proposals in response to written requires from nonfederal entity - 200.320(f)(3)

After soliciting a number of sources, competition is deemed inadequate

BRUSTEIN & MANASEVIT, PLLC 115

VENDOR SELECTION PROCESS: NONCOMPETITIVE VENDOR SELECTION PROCESS: NONCOMPETITIVE PROPOSAL

As a practical matter, noncompetitive contract raises “red flags”g Ensure persuasive and adequate documentation to

facilitate audit

BRUSTEIN & MANASEVIT, PLLC 116

VENDOR SELECTION PROCESS

Cannot contract with vendor who has been suspended or debarred

http://www.sam.govp g

Appendix II(I) Appendix II(I)

BRUSTEIN & MANASEVIT, PLLC 117

CONTRACT ADMINISTRATION 200.318

(Ch d) N f d l i i i i i h (Changed) Nonfederal entities must maintain oversight to ensure that contractors perform in accordance with the terms, conditions, and specifications of the contract

BRUSTEIN & MANASEVIT, PLLC 118

Property Management

BRUSTEIN & MANASEVIT, PLLC 119

INVENTORY MANAGEMENT

M t h d t t l Must have adequate controls in place to account for: Location of equipmentq p

Custody of equipment

Security of equipment

BRUSTEIN & MANASEVIT, PLLC 120

WHAT IS EQUIPMENT? 200.33

Equipment: tangible, nonexpendible, personal property having a useful life of more than one year and an acquisition cost of $5,000 or more per

iunit.

Grantee may also use its own definition of equipment as long as the definition would at least include all equipment defined above.

BRUSTEIN & MANASEVIT, PLLC 121

SUPPLIES 200.94

Anything that is not equipment is considered supplies. “Significant Technological Devices” Significant Technological Devices

NEW: Computing devices Machines used to acquire, store, analyze, process, public data and ac es use to acqu e, sto e, a a y e, p ocess, pub c ata a

other information electronically

Includes accessories for printing, transmitting and receiving or storing electronic informationelectronic information

Computing devices are supplies is less than $5,000

BRUSTEIN & MANASEVIT, PLLC 122

INTERNAL CONTROLS 200.302(b)(4)

Regardless of cost, grantee must maintain effective control and “safeguard all assets and assure that they are used solely for authorized purposes.”

BRUSTEIN & MANASEVIT, PLLC 123

INVENTORY MANAGEMENT

Must have inventory management system Property recordsProperty records

Description, serial number or other ID, title info, acquisition date, cost, percent of federal participation, location, use and condition, and ultimate disposition

Physical inventory Physical inventory

At least every two years

Control system to prevent loss, damage, theft

All incident must be investigated

BRUSTEIN & MANASEVIT, PLLC 124

USE OF GRANT-ACQUIRED EQUIPMENT 200.313

Clarified: shared use is allowed if such use will not “interfere”: 1st preference – projects supported by federal awarding agency

2nd preference – project funded by other federal agencies

3 d f f f d ll f d d 3rd preference – use for non federally funded programs

NEW: Cannot “encumber” the property without approval of Federal agency or Pass-through agencyFederal agency or Pass through agency

BRUSTEIN & MANASEVIT, PLLC 125

INVENTORY MANAGEMENT 200.313

NEW: When grantee acquiring replacement equipment, the equipment to be replaced may be used as a “trade in” without equipment to be replaced may be used as a trade-in without recourse to federal agency

BRUSTEIN & MANASEVIT, PLLC 126

DISPOSITION-EQUIPMENT 200.313

When property no longer needed, must follow disposition rules:When property no longer needed, must follow disposition rules:

Transfer to another federal program

Over $5,000 – pay federal share

Institutions of Higher Education, Hospitals and Other Nonprofits must request disposition instructions from the Secretary of the before disposal of equipment.

Under $5,000 – no accountability

NEW: Nonfederal entity must request disposition instructions from the federal awarding agency if required by the terms of the grant.

BRUSTEIN & MANASEVIT, PLLC 127

DISPOSITION – SUPPLIES 200.314

If there is a residual inventory of unused supplies exceeding $5,000 in total aggregate value upon termination or completion of the project or program gg g p p p j p gand the supplies are not needed for any other federal award, must compensate the federal government for its share.

BRUSTEIN & MANASEVIT, PLLC 128

Records and Reviews

BRUSTEIN & MANASEVIT, PLLC 129

METHODS FOR COLLECTION TRANSMISSION AND METHODS FOR COLLECTION, TRANSMISSION AND STORAGE OF INFORMATION 200.335

NEW Wh i i l d l t i d t b lt d th i o NEW: When original records are electronic and cannot be altered, there is no need to create and retain paper copies.

o When original records are paper, electronic versions may be substituted thr h the se f d licati n r ther f rms f electr nic media r ided through the use of duplication or other forms of electronic media provided they:

o Are subject to periodic quality control reviews,

o Provide reasonable safeguards against alteration; and

o Remain readable.

BRUSTEIN & MANASEVIT, PLLC 130

131

REQUIREMENTS OF PASS-OF PASS-

THROUGH ENTITIESENTITIES

131

FEDERAL AWARDING AGENCY REVIEW OF 132

FEDERAL AWARDING AGENCY REVIEW OF RISK POSED BY APPLICANTS 200.205

NEW: ED and “Pass-Through” must have in place a framework for evaluating risks before applicant receives funding

1 Financial Stability1. Financial Stability

2. Quality of Management System

3. History of Performance3. History of Performance

4. Audit Reports

5. Applicant’s Ability to Effectively Implement Program

133

SPECIFIC CONDITIONS 200.207

ED or “Pass Through” May Impose “additional Federal award g y pconditions”: Require reimbursement;

Withhold funds until evidence of acceptable performance;

More detailed reporting

Addi i l i i Additional monitoring;

Require grantee to obtain technical or management assistance; or

Establish additional prior approvals Establish additional prior approvals.

MONITORING AND REPORTING PROGRAM 134

MONITORING AND REPORTING PROGRAM PERFORMANCE 200.328

NEW: Monitoring by the “Pass Through”

Monitor to assure compliance with applicable federal p pprequirements and performance expectations are achieved

Must cover each program, function or activity(see also 200.331)

Must submit “performance reports” at least annually

REQUIREMENTS FOR PASS THROUGH ENTITIES 135

REQUIREMENTS FOR PASS-THROUGH ENTITIES 200.331

NEW: Depending on assessment of risk, the following monitoring tools may be useful for the pass through entity monitoring tools may be useful for the pass-through entity to ensure proper accountability and compliance with program requirements and achievement of performance p g q pgoals: 1. Training + technical assistance on program-related matters

2. On-site reviews

3. Arranging for “agreed-upon-procedures” engagements (d ib d i 200 425)(described in 200.425)

136

AUDIT REQUIREMENTS

136

137

AUDIT REQUIREMENTS

C h h ld $500 000 Current threshold $500,000.

NEW: Threshold increased to $750,000

The federal agency, OIG, or GAO may arrange for The federal agency, OIG, or GAO may arrange for audits in addition to single audit

138

FEDERAL AGENCY RESPONSIBILITIES 200.513

NEW: The federal awarding agency must use cooperative audit resolution to improve federal p pprogram outcomes Cooperative Audit Resolution: means the use of audit follow-up techniques

which promote prompt corrective action by improving communication, fostering collaboration, promoting trust and developing an understanding between the Federal agency and non-Federal entity 200.25.

139

AUDIT FINDINGS 200.516

The auditor must report (for major programs):p ( j p g )

Significant deficiencies and material weaknesses in internal controls

Significant instances of abuse

Material noncompliance

Known questioned costs > $25,000

Auditor will not normally find questioned costs for a program that is not audited as a “major program”

NEW: But if auditor becomes aware of questioned costs NEW: But if auditor becomes aware of questioned costs > $25,000 for non-major program, must report

QUESTIONS?QUESTIONS?

140

~ LEGAL DISCLAIMER ~

This presentation is intended solely to provide general information and does not constitute legal advice. Attendance at the presentation or later review of these printed materials does not create an attorney-client relationship with

B i & M i Y h ld k i b d Brustein & Manasevit. You should not take any action based upon any information in this presentation without first consulting legal counsel familiar

with your particular circumstances.

141