gramin bank of bangla desh : microfinan

TRANSCRIPT

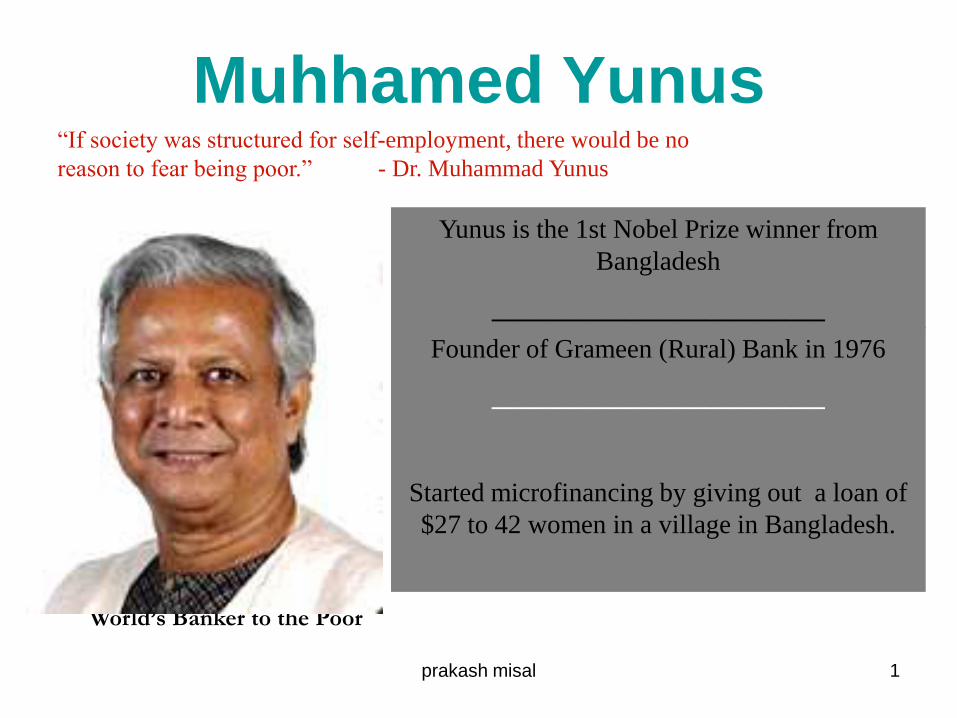

Muhhamed Yunus

Yunus is the 1st Nobel Prize winner from

Bangladesh

_________________________

Founder of Grameen (Rural) Bank in 1976

_________________________

Started microfinancing by giving out a loan of

$27 to 42 women in a village in Bangladesh.

World’s Banker to the Poor

“If society was structured for self-employment, there would be no

reason to fear being poor.” - Dr. Muhammad Yunus

1prakash misal

Microfinancing

• Supply of capital loans, consumer credit, savings,

insurance & other basic financial services to low income

households.

• People need to run their businesses, build assets, stabilize

consumption & shield themselves against risks.

•It’s a service in which the poor people desire & are willing

to pay for.

•Loans are typically less than $125 made to the rural poor

who normally do not qualify for traditionally banking

credit.

“say NO to poverty”

2prakash misal

• Microfinancing is very beneficial; it is a combination of

financial and non-financial education.

• Microfinancing used to be unknown, but it is now

worldwide.

• World Bank estimates that there are 7,000 microfinance institutions worldwide.

Microfinancing (continued)

3prakash misal

Micro-Credits & Micro-Banks

CREDITS

• The Grameen transactions take place at the village level, usually in a local hall or

temple.

• The borrowers will use a loan to buy tools and equipment to set up on their own.

BANKS

• Banks lend money to individual entrepreneurs in groups of five, each member

being responsible for their own loans before any one individual can re-apply for the

next level of funding.

• they use each other as collateral for their loans.

• This proven method has boasted over a 95% success rate in repayment and

flourishing businesses.

4prakash misal

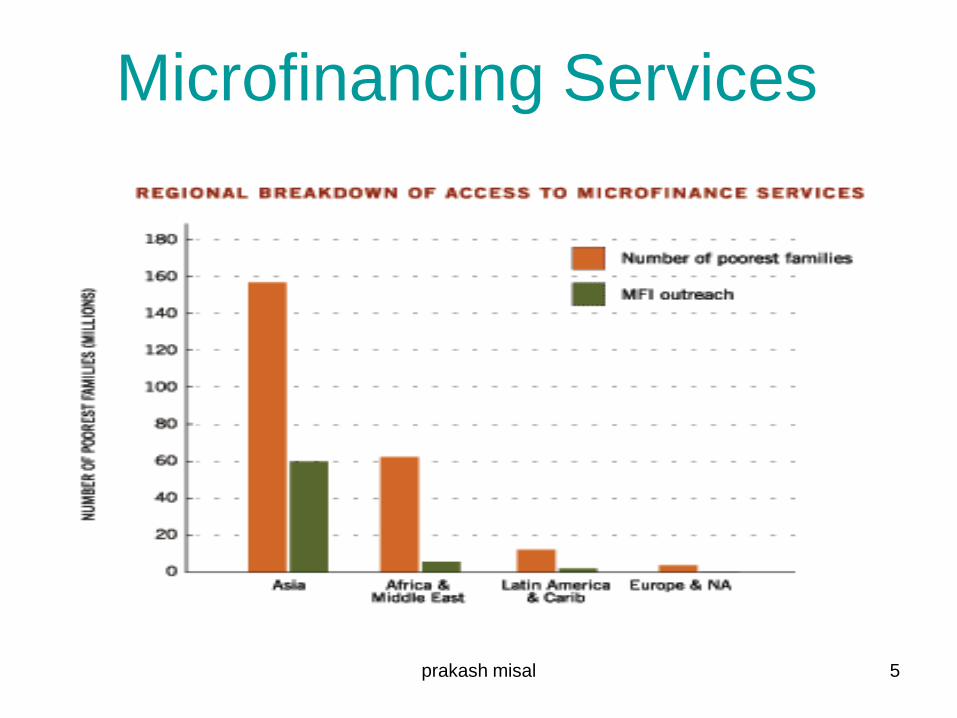

Microfinancing Services

5prakash misal

_______________________________________________________________________

Why Targeting Women?

“One billion people in the world are illiterate and two thirds of those

people are women.”

- Muhammed Yunus

“One billion people in the world are illiterate and

two thirds of those people are women.”

-

Muhammed Yunus

6prakash misal

General Information

Micro-entrepreneurs:

• Don’t need collateral

• Small and shorter loans

• Group borrowing

– Reputation and Peer pressure• Some criticism

Microfinance Institution: • Higher operating expenses

– Rural costs are higher than urban costs

• High transaction costs

– Because of the size of the loans

• Higher interest rates

Overall:

• Improves employment

7prakash misal

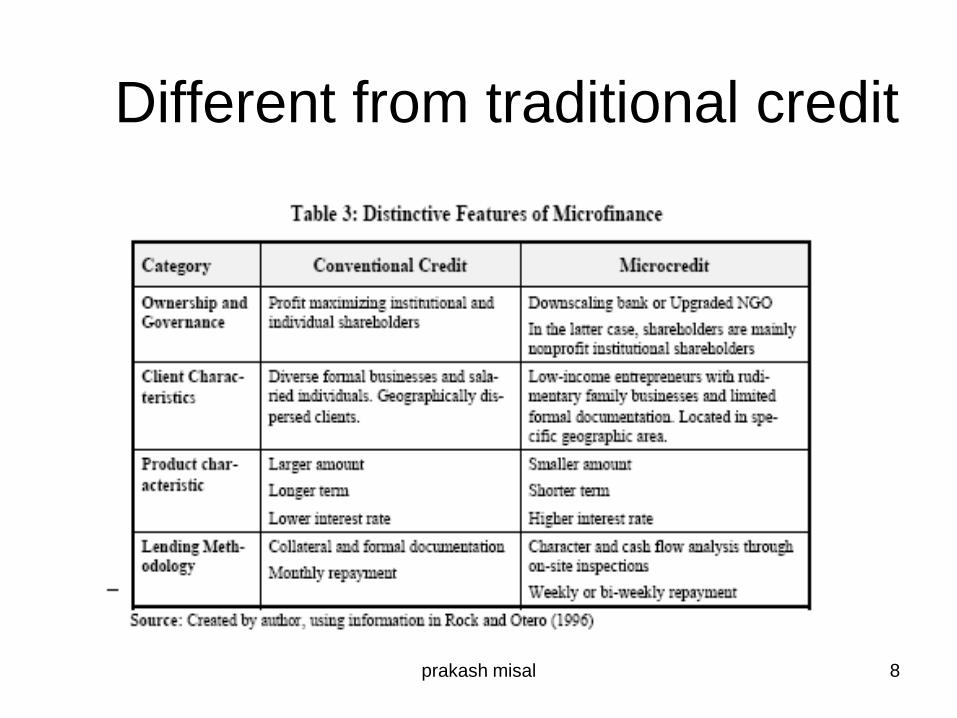

Different from traditional credit

8prakash misal

Broad Objectives

• To provide equity finance to the entrepreneurs without capacity to mobilize capital and/or collateral trying to setup innovative projects which holds promise for future growth and have direct or indirect impact on poverty alleviation, with preference to businesses concentrating in information and communication technologies and bio-engineering;

• To provide loans, equity or both to risky ventures using untested technology and/or producing untested products, either to new companies or existing companies for balancing, modernization or expansion;

9prakash misal

•

• To assist in management buy-ins or buy-outs of existing companies needing finance and management support, provided that activities/products of such companies are socially desirable and bring benefits to the poor; and

•

• To promote or develop enterprises having prospects for export or import substitution that will use indigenous raw materials, provide extensive employment to the rural poor and/or help upgrade the skills of the rural or urban poor

10prakash misal

Objectives of Grameen Bank

• Extend banking facilities to poor men and women;

• Eliminate the exploitation of the poor by money lenders;

• Create opportunities for self-employment for the vast multitude of unemployed people in rural Bangladesh;

• Bring the disadvantaged, mostly the women from the poorest households, within the fold of an organizational format which they can understand and manage by themselves; and

• Reverse the age-old vicious circle of "low income, low saving & low investment", into virtuous circle of "low income, injection of credit, investment, more income, more savings, more investment, more income".

11prakash misal

Mission

• Grameen Fund is dedicated to promoting, managing and financing various enterprises, which aim to create wealth for poverty alleviation in the country.

• Grameen Fund's main strategy lies in venture capital finance, especially in technology based ventures. It equally lays stress on providing collateral free fixed capital and working capital loans to the micro-enterprises run by those who are newly emerging out of poverty.

12prakash misal

Successes and Failures

• Floods in 1998 had worst effect :

• A huge rehabilitation program by issuing fresh

loans for restarting income-generating activities

and to repair or rebuild their houses. Soon

borrowers started to feel the burden of

accumulated loans. They found the new

installment sizes exceeded their capacity to

repay. They gradually started to stay away from

weekly centre meetings. Grameen Bank

repayment started to show quick decline.

13prakash misal

Difficulties faced

• They tried to improve the situation, but it did not produce desired result. Impact of the post-flood repayment crisis was compounded by its overlap with a recovery problem from an earlier crisis. In 1995, a large number of our borrowers stayed away from centre meetings and stopped paying loan installments. Husbands of the borrowers, inspired and supported by local politicians, organised this, demanding a change in Grameen Bank rules to allow withdrawal of "group tax" component of "group fund" at the time of leaving the bank. It continued for months. At the end we resolved the problem by creating some opening in our rules, but Grameen's repayment rate had gone down in the mean time. Many borrowers continued to abstain from repaying their loans even after the matter was resolved.

14prakash misal

Weaknesses in the System

• These external factors reinforced the internal weaknesses in the system. The system consisted of a set of well-defined standardised rules. No departure from these rules was allowed. Once a borrower fell off the track, she found it very difficult to move back on, since the rules which allowed her to return, were not easy for her to fulfill. More and more borrowers fell off the track. Then there was the multiplier effect. If one borrower stopped payments, it encouraged others to follow.

15prakash misal

Improvements in the System

• Pilot-tested the system quietly in a few

branches to fine-tune the design; tried

again in larger number of branches;

reworked it; and in the end, came up with

the architecture of a new system that all

liked

16prakash misal

Staff Participation

• All the 12,000 staff participated very actively in designing the product at all the stages .

• Some were critical in the beginning, but by the time it was ready, everybody loved it.

• The response from the borrowers was so positive. Borrowers who did not show up at their centre meetings for years, started showing up to talk about the new system. Soon they were signing up to start all over again and repay the old loans with the accumulated interest. No reduction in the debt was offered. Still they opted to return.

17prakash misal

• Introduction of the New System became

effective

• Transition took place in more than 41000

villages

• Reluctance was replaced with enthusiasm

• Emergence of Grameen Bank II

• Change over from Grameen Classic

system to Grameen Generalised System

18prakash misal

Change

• The general loans, seasonal loans, family loans, and more than a dozen other types of loans were done away with; gone is the group fund; gone is the branch-wise, zone-wise loan ceiling; gone is the fixed size weekly installment; gone is the rule to borrow every time for one whole year,

• Even when the borrower needed the loan only for three months; gone is the high-level tension among the staff and the borrowers trying to steer away from a dreadful event of a borrower turning into a "defaulter", even when she is still repaying; and gone are many other familiar features of Grameen Classic System.

19prakash misal

Poor Always Pay Back

• Central assumption that the poor people always pay back their loans.

• On some occasions they may take longer time to pay back than it was originally stipulated, but repay they will.. Many things can go wrong for a poor person during the loan period. After all, the circumstances are beyond the control of the poor people.

• It is always advocated that micro credit programs should not fall into the logical trap of the conventional banking and start looking at their borrowers as some kind of "time-bombs" who are ticking away and waiting to create big trouble on pre-fixed dates.

• One can benefit enormously by having trust in them, admiring their struggle for and commitment to have decent lives for themselves.

20prakash misal

Loan Products

• Basic Loan : Easy Loan : To meet all

credit needs without any difficulty

• Alternate to this is Flexible Loan with a

fresh repayment schedule . It is

upgradation of Loan

• Housing Loan

• Educational Loan

21prakash misal

22prakash misal

“Sustainable development continuum for organic

microfarming”

23prakash misal

Job Creation

MFI’s do increase jobs in agriculture and transportation,

however they decrease construction and manufacturing24prakash misal

Some negative results…

• Depend on microcrediting for subsistence

• Engage in "copycat" behavior– Thus leads to more sellers saturating

the market as more microcredit is made available.

– low "barriers to entry."

• Largely, subsistence activities with no prospect of comparative advantage.

• Child Labor– Child labor increases current income

but reduces future income

25prakash misal

Four Principles

26prakash misal

Prosperity to Family

27prakash misal

Repair or Construct New Houses

28prakash misal

Grow Vegetables – Surplus sell

29prakash misal

Plantation Season: Plant many

Seedlings

30prakash misal

Small Families , Minimize

Expenditure and Good Health

31prakash misal

Educate Children and Pay for the

same

32prakash misal

Keep environment Clean

33prakash misal

Build and Use laterines

34prakash misal

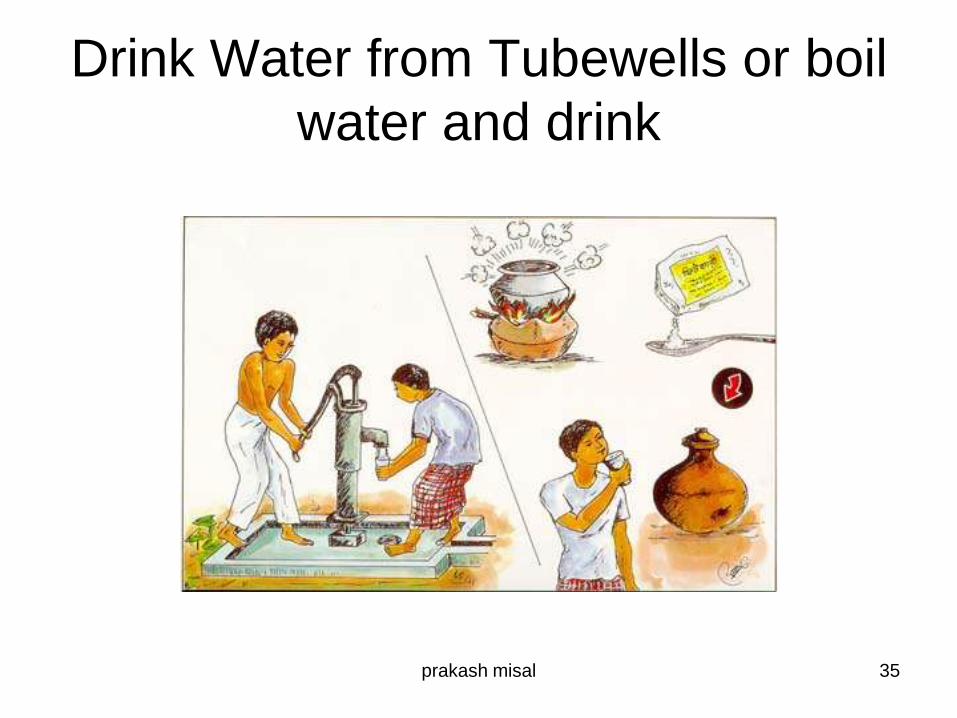

Drink Water from Tubewells or boil

water and drink

35prakash misal

No Dowry /No Child Marriages

36prakash misal

No Injustice tolrated

37prakash misal

Bigger Investments for higher

Income

38prakash misal

Ready to Help

39prakash misal

Restore Discipline

40prakash misal

• MFI’s are successful

• Increase profits and social prosperity

• Decrease risks, thereby increase loans

and the number of investors

• Number of lenders growing at 25% per

year

Is the future bright?

41prakash misal

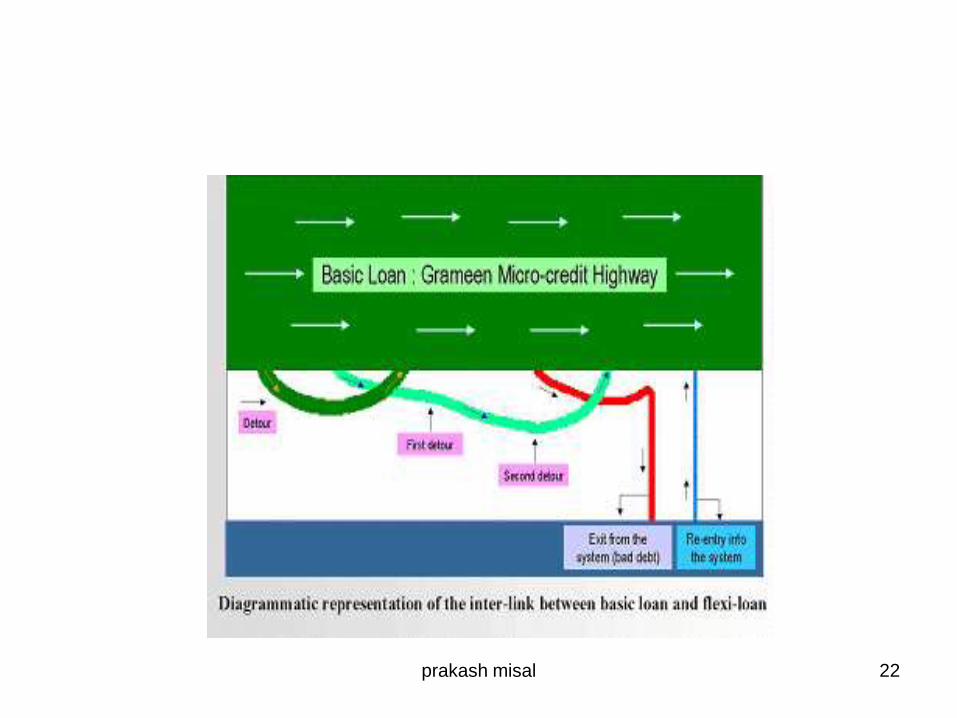

Flexible Loan

• Flexible loan is simply a rescheduled basic loan, with its own set of separate rules. As long as the borrower keeps her schedule, she moves forward uninterrupted with ease and comfort on the micro-credit highway. She can pick up speed according to the rules of the highway. If she drives well she can shift to higher and higher gear. In other words, on the Grameen highway, a borrower can routinely upgrade her loan size at each cycle of loan. This is done on the basis of

• Predetermined rules. She knows ahead of time how much enhancement in loan size is coming, and can plan her activities accordingly. But if a borrower faces engine trouble (business slow-down or failure, sickness, family problems, accidents, thefts, natural disaster, etc.) and cannot keep up with the highway speed, she has to quit the highway and take an exit on to a detour called a "flexible loan" or "flexi-loan". This detour will allow her a slower speed consistent with her situation. Now she can reduce the installment size that she can afford to pay, by extending the loan period. Taking a detour, however, does not in any way imply that she has changed the objective of her journey. She still proceeds with the same objective, but only through a winding narrow road for a while. Her immediate goal is to overcome her problems

42prakash misal

• Under GGS loans are written off as a part of financial prudence, but the amount is neither forgotten nor forgiven. GGS treats all written-off loans as recoverable loans. Under GGS, nearly 90 per cent of written-off loans and interest will ultimately be recovered, because the borrowers will pay them back, in their own interest, as and when opportunity arises.

• Poor people always need money. Their interest is to keep the door to money open. If this door shuts down for any reason, they'll do their best to reopen it - if that option is available. GGS provides this option.

43prakash misal

• There are many exciting features in GGS, but I

think removing tension from micro-credit and

permanently establishing full dignity to the poor

borrowers, are the two most important features

of them all. Tension-free micro credit is a great

gift of GGS. Now both sides in the micro-credit

system, the lender and the borrowers, can enjoy

micro-credit, rather than having occasional

nightmares created by one for the other.

44prakash misal