government securities management - djppr · government securities management and ... 2004 2005 2006...

TRANSCRIPT

Directorate of Government Debt Securities Directorate General of Debt Management Ministry of Finance of The Republic of Indonesia

Government Securities Management February 16th, 2015

OUTLINE

1. Government Securities Management and Financing

Strategy

2. Government Securities Performance

3. Crisis Management Protocol & Bond Stabilization

Framework

4. Debt Outstanding & Risk Profile

2

Government Securities

Management and Financing Strategy

Key Initiatives to Develop Domestic Gov. Securities

Market

Facilitating the development of derivative instrument and Government securities repo:

• Develop a deep and liquid repo market, coordinate with FSA

• Facilitating the development of Government Bond Futures

Focused on a few benchmark series with large outstanding

Introduction of an electronic trading platform (ETP)

Strengthening Investor Relations (IR)

Launch a new primary dealer system

Increase domestic participation from key investors

Continuously improving bond stabilization framework

4

Financing Trend, 2004 – 2015

(trillion IDR)

Notes: * Preliminary 2014 ** Revised Budget 2015

5

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014* 2015**

Govt Securities - net 6.9 22.6 36.0 57.2 85.9 99.5 91.1 119.9 159.7 224.7 265.0 297.7

Domestic Loan - - - - - 0.4 0.6 0.8 0.4 0.5 1.7

External Loan - net (28.1) (10.3) (26.6) (26.6) (18.4) (12.4) (4.6) (17.8) (23.5) (5.8) (15.4) (20.0)

Others/Non-Debt - net 42.0 (1.2) 20.0 9.1 16.6 25.5 4.6 28.3 38.1 18.1 (12.2) (65.5)

Budget Defisit, % to GDP 1.1 0.5 0.9 1.3 0.1 1.6 0.7 1.1 1.9 2.3 2.2 1.9

1.1

0.5

0.9

1.3

0.1

1.6

0.7

1.1

1.9

2.3 2.2

1.9

(0.5)

-

0.5

1.0

1.5

2.0

2.5

-100

-50

0

50

100

150

200

250

300

Securities Financing Realization 2015

*Adjusted by changes in Cash Management & Debt Switch

6

*(Million IDR)

Budget 2015*Revised Budget

2015*

Realization

(ao Feb 13, 2015)*

% Realization to

Revised Budget

2015

Government Securities Net 277,049,800 297,698,382 92,443,113 31.05%

Government Securities Maturing in 2015 153,612,324 154,112,324 17,608,887 11.43%

-Buyback 3,000,000 3,000,000 - 0.00%

Issuance Need 2015* 430,662,124 451,810,706 110,052,000 24.36%

Government Debt Securities (GDS) 98,672,000

Domestic GDS 48,300,000

-Coupon GDS 34,300,000

-Conventional T-Bills 11,000,000

-Private Placement 3,000,000

-Retail Bonds -

International Bonds 50,372,000

-USD GMTN 50,372,000

-Euro GMTN -

-Samurai Bonds -

Government Islamic Debt Securities 11,380,000

Domestic Government Islamic Debt Securities 11,380,000

- IFR/PBS/T-Bills Sukuk (Islamic Fixed Rated

Bond/Project Based Sukuk) 11,380,000

- Retail Sukuk -

Global Sukuk -

General Strategy for Debt Financing 2015

1. Optimizes Governments securities (SBN) issuance from domestic sources to fulfill Budget need and uses

foreign debts as complimentary;

2. Determines debt instrument by taken into account of market need in regard to market development and

portfolio management;

3. Issues Retail Bond for instrument diversification and financial inclusion;

4. Optimizes foreign and domestic loan instrument to fulfill Budget need on capital expenditure;

5. Conducts active portfolio management of Government securities through, among others, debt buyback

and debt switch, in order to promote market liquidity and stability;

6. Strengthens the function of Investor Relations Unit, among others, through the proactive dissemination of

information, rapid and effective responses, and effective communication with investors and other stakeholders.

7

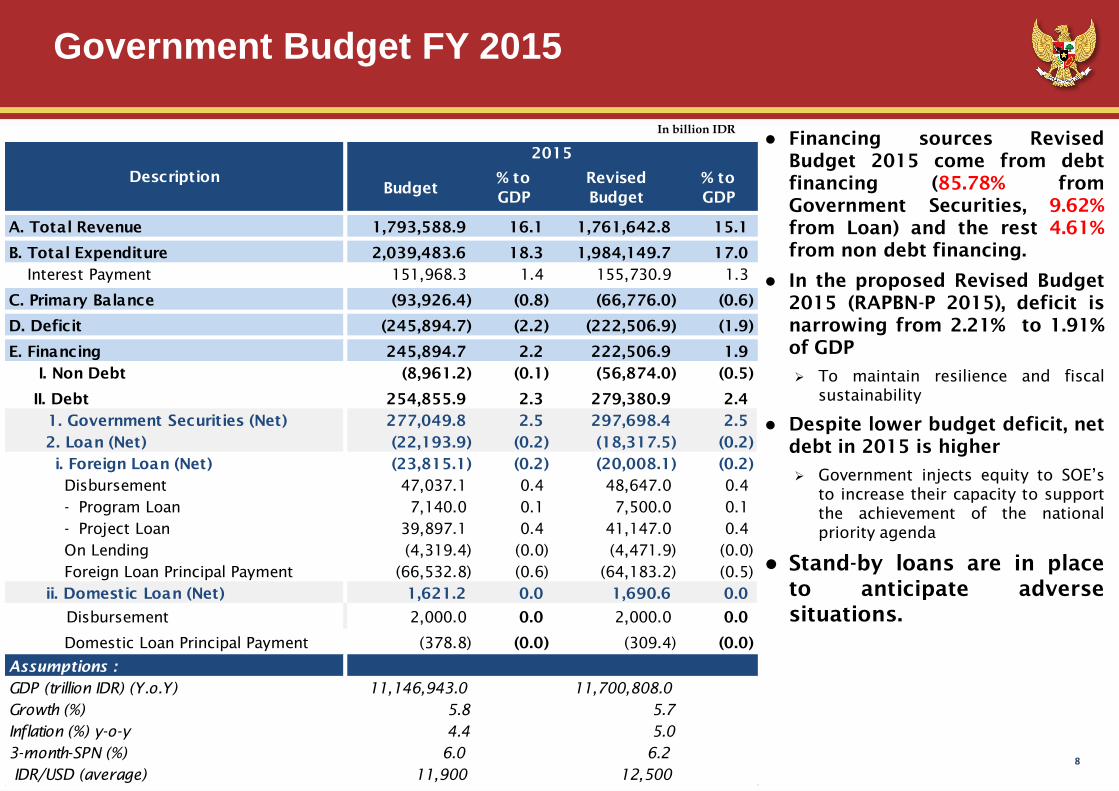

Government Budget FY 2015

8

In billion IDR Financing sources Revised

Budget 2015 come from debt

financing (85.78% from

Government Securities, 9.62%

from Loan) and the rest 4.61%

from non debt financing.

In the proposed Revised Budget

2015 (RAPBN-P 2015), deficit is

narrowing from 2.21% to 1.91%

of GDP

To maintain resilience and fiscal

sustainability

Despite lower budget deficit, net

debt in 2015 is higher

Government injects equity to SOE’s

to increase their capacity to support

the achievement of the national

priority agenda

Stand-by loans are in place

to anticipate adverse

situations.

A. Total Revenue 1,793,588.9 16.1 1,761,642.8 15.1

B. Total Expenditure 2,039,483.6 18.3 1,984,149.7 17.0

Interest Payment 151,968.3 1.4 155,730.9 1.3

C. Primary Balance (93,926.4) (0.8) (66,776.0) (0.6)

D. Deficit (245,894.7) (2.2) (222,506.9) (1.9)

E. Financing 245,894.7 2.2 222,506.9 1.9

I. Non Debt (8,961.2) (0.1) (56,874.0) (0.5)

II. Debt 254,855.9 2.3 279,380.9 2.4

1. Government Securities (Net) 277,049.8 2.5 297,698.4 2.5

2. Loan (Net) (22,193.9) (0.2) (18,317.5) (0.2)

i. Foreign Loan (Net) (23,815.1) (0.2) (20,008.1) (0.2)

Disbursement 47,037.1 0.4 48,647.0 0.4

- Program Loan 7,140.0 0.1 7,500.0 0.1

- Project Loan 39,897.1 0.4 41,147.0 0.4

On Lending (4,319.4) (0.0) (4,471.9) (0.0)

Foreign Loan Principal Payment (66,532.8) (0.6) (64,183.2) (0.5)

ii. Domestic Loan (Net) 1,621.2 0.0 1,690.6 0.0

Disbursement 2,000.0 0.0 2,000.0 0.0

Domestic Loan Principal Payment (378.8) (0.0) (309.4) (0.0)

Assumptions :

GDP (trillion IDR) (Y.o.Y) 11,146,943.0 11,700,808.0

Growth (%) 5.8 5.7

Inflation (%) y-o-y 4.4 5.0

3-month-SPN (%) 6.0 6.2

IDR/USD (average) 11,900 12,500

Budget% to

GDP

Revised

Budget

% to

GDP

2015

Description

Government Securities Financing (Gross) 2015

9

Domestic:

Auction:

conventional securities: 23 x

Islamic securities: 22 x

Non-Auction:

retail bonds: ORI + Sukuk

Retail.

International Bonds:

Issuance of International

Bonds as complement to

avoid crowding out in

domestic market and provide

benchmark for corporate

issuance, consist of USD,

YEN or EURO global bonds

Maximum issuance

international bond 22.6% from

target gross

Issuance targets for

GDS, Sukuk and ATM

target: – GDS (SUN): 79.9%

– Sukuk: 20.1%

– ATM for auctions: 8.2

year

Front Loading strategy:

• in the first semester is

targeted at 63%.

• for domestic issuance is

also targeted at first

semester at 59%

FR 69 – 5 Y

FR 70 – 10 Y

FR 71 – 15 Y

FR 68 – 20 Y

Benchmark Series for 2014 & 2015

(in trillion Rp)

Instruments Budget

Revised

Budget

Govt Securities (net) 277.0 297.7

Redemption 135.6 136.1

Cash Management 15.0 15.0

Buyback 3.0 3.0

Govt Securities (gross) 430.7 451.8

Domestic 80.0% 77.4%

Retail 9.3% 8.9%

Auctions 70.7% 68.5%

International Bond 20.0% 22.6%

Indicative Target

Government Securities Performance

0%

10%

20%

30%

40%

50%

60%

-

20,000

40,000

60,000

80,000

100,000

120,000

Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sept-14 Oct-14 Nov-14 Jan-15 16-Feb-15

Incoming Bids Awarded Bids Foreign Incoming Bids Foreign Awarded Bids % Foreign Incoming Bids (RHS)

11 11

• Average Foreign incoming bids 2015 is Rp11,95T, compare to period in 2014, which reached 7,85T • Average incoming bids 2015 = Rp38,49T, increased from average incoming bids 2014 = Rp23,37T

• Average awarded bid 2015 = 14,33 while average awarded bid 2014 = Rp11,29 T.

*as of February 16,2015

Average incoming bids

2014 = Rp23,37T/auction

Average awarded bids

2014 = Rp11,29T/auction

Government Debt Securities Primary Market

Performance 2015

0%

10%

20%

30%

40%

50%

60%

-

20,000

40,000

60,000

80,000

100,000

120,000

Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Jan-15 16-Feb-15

Incoming Bids Awarded Bids Foreign Incoming Bids Foreign Awarded Bids % Foreign Incoming Bids (RHS)

12 12

• Average Foreign incoming bids 2015 is Rp9,16T vs Rp8,93T of average foreign incoming bids in 2014

• Average incoming bids 2015 = Rp28,35, increased from average incoming bids 2014 = Rp14,19T

• Average awarded bid 2015 = Rp9,81 T, while average awarded bid 2014 = Rp6,59T.

*as of February 16, 2015

Avr . Awarded bids

2014 = 6,59T Avr. Incoming Bid

2014: 14,19T

Avr. Foreign Incoming Bid 2014:

8,93T

Government Securities Primary Market Performance

2015

2468

10121416182022

Apr'0

8

Jul'0

8

Oct'0

8

Jan'0

9

Apr'0

9

Jul'0

9

Oct'0

9

Jan'1

0

Apr'1

0

Jul'1

0

Oct'1

0

Jan'1

1

Apr'1

1

Jul'1

1

Oct'1

1

Jan'1

2

Apr'1

2

Jul'1

2

Oct'1

2

Jan'1

3

Apr'1

3

Jul'1

3

Oct'1

3

Jan'1

4

Apr'1

4

Jul'1

4

Oct'1

4

Jan'1

5

5Y 10Y 15Y 20Y

7.08 (5Y), 7.34 (10Y), 7.53 (15Y), 7.73 (20Y)

(IDR Trilion)

Global Financial

Crisis

Eurozone sovereign debt crisis

[In Percentage]

As of Feb 13, 2015

Activities of the domestic bonds are growing Yields of Benchmark Series steadily decrease

Bid Ask Spread 10 Y Government Bond Turn Over 10 Y Government Bond

As of Feb 13, 2015

As of Feb 13, 2015

Secondary Market Performance

Spread 9.8 bps

(ask 7.347%%,

bid 7.445%)

13

5.12

7.04

5.15

14.12 12.88

10.75 10.53

-

3.00

6.00

9.00

12.00

15.00

2008 2009 2010 2011 2012 2013 2014

5.73 5.31 5.82 7.83

10.31

6.62 7.10 8.42 7.45 6.44

9.27 8.61 8.45 8.23 7.91

11.05 0.38 0.41 0.96

0.57

1.27

1.18 0.35

0.91 1.04

0.79

0.36 0.41 0.39 0.98 0.76

1.01

3.07 6.30

9.39 8.69

7.90

7.13 6.95

6.19 8.59 10.76

11.49

9.93 8.81

9.12 8.80

8.32

-

5.00

10.00

15.00

20.00

25.00

Trili

un

OUTRIGHT REPO BANK REPO BI

0

10

20

30

40

50

60

70

Jan

-09

Ma

y-09

Sep

-09

Jan

-10

Ma

y-10

Sep

-10

Jan

-11

Ma

y-11

Sep

-11

Jan

-12

Ma

y-12

Sep

-12

Jan

-13

Ma

y-13

Sep

-13

Jan

-14

Ma

y-14

Sep

-14

Jan

-15

LCY 10 Year

Government

Bonds

Latest Yield YTD Change (BP) MTD Change

(BP)

HK 1.417 -44.2 0.0

ID 7.495 -30.1 +32.7

JP 0.424 +9.5 +14.6

KR 2.397 -20.8 +15.7

MY 3.859 -28.8 +2.8

PH 3.418 -44.5 +25.5

SG 2.093 -18.7 +21.3

TH 2.761 +3.2 +14.5

US 2.050 -12.1 +41.0

VN 6.588 -64.2 -1.2

• Market Watch as of Feb 13, 2015

• Source: Asian Bonds Online

Yield GS on peer’s market (a.o. February 13, 2015)

14

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

22.0

1Y 2Y 3Y 4Y 5Y 6Y 7Y 8Y 9Y 10Y 15Y 20Y 30Y

13 Feb '15 6 Feb '15

13 Jan '15 9 Feb '12

23 Sep '11 27 Oct '08

13 Sep'05

[in percentage]

Tenor 13-Feb-15 6-Feb-15 13-Jan-15 9-Feb-12 23-Sep-11 27-Oct-08 13 Sep'05

1Y 5.66 5.69 6.19 3.30 5.29 19.37

2Y 6.47 6.30 6.99 4.21 6.01 17.35 14.59

3Y 6.88 6.57 7.28 4.33 6.13 19.93

4Y 7.11 6.74 7.40 4.39 6.54 17.17 14.14

5Y 7.11 6.84 7.39 4.44 6.69 17.46 14.96

6Y 7.25 6.89 7.54 4.79 6.81 17.05 15.24

7Y 7.27 6.91 7.56 4.88 7.08 17.06 16.17

10Y 7.40 7.01 7.67 5.02 7.43 20.91 15.75

15Y 7.53 7.09 7.98 5.47 7.83 16.65 14.12

20Y 7.74 7.30 8.10 5.96 8.20 20.27

30Y 7.90 7.66 8.43 6.17 8.29 20.37

Ownership of Tradable Domestic Government

Securities

In the end of January 2015, foreign investor ownership record the highest percentage of ownership,

showing their increasing appetite on the Indonesia’s government securities.

(In IDR Trillion)

15

`

Banks 299.66 36.73% 335.43 33.70% 359.99 33.56% 355.58 31.42% 420.50 35.06% 407.58 33.38% 375.55 31.04% 372.66 29.95% 369.16 29.45%

Govt Institutions (Bank Indonesia*) 3.07 0.37% 44.44 4.47% 30.44 2.84% 51.19 4.52% 0.00 0.00% 0.38 0.03% 41.63 3.44% 38.37 3.08% 53.17 4.24%

Non-Banks 517.53 63.09% 615.38 61.83% 682.31 63.60% 724.86 64.05% 778.90 64.94% 812.93 66.58% 792.78 65.52% 833.42 66.97% 831.21 66.31%

Mutual Funds 43.19 5.27% 42.50 4.27% 44.15 4.12% 45.80 4.05% 46.11 3.84% 45.46 3.72% 45.79 3.78% 47.16 3.79% 47.59 3.80%

Insurance Company 83.42 10.17% 129.55 13.02% 141.28 13.17% 151.36 13.38% 154.09 12.85% 150.78 12.35% 150.60 12.45% 149.95 12.05% 149.86 11.96%

Foreign Holders 270.52 32.98% 323.83 32.54% 360.91 33.64% 403.59 35.66% 447.37 37.30% 481.20 39.41% 461.35 38.13% 500.83 40.25% 497.80 39.71%

Foreign Govt's&Central Banks** 50.06 6.10% 78.39 7.88% 86.09 8.03% 93.59 8.27% 100.57 8.38% 102.61 8.40% 103.42 8.55% 104.66 8.41% 104.32 8.32%

Pension Fund 56.46 6.88% 39.47 3.97% 39.66 3.70% 38.95 3.44% 42.63 3.55% 42.48 3.48% 43.30 3.58% 43.00 3.46% 43.60 3.48%

Securities Company 0.30 0.04% 0.88 0.09% 0.83 0.08% 0.96 0.08% 0.99 0.08% 0.89 0.07% 0.81 0.07% 0.65 0.05% 0.71 0.06%

Individual 32.48 3.26% 45.75 4.27% 31.42 2.78% 28.88 2.41% 31.91 2.61% 30.41 2.51% 28.35 2.28% 27.31 2.18%

Others 63.64 7.76% 46.68 4.69% 49.72 4.64% 52.78 4.66% 58.83 4.90% 60.21 4.93% 60.51 5.00% 63.49 5.10% 64.33 5.13%

Total 820.27 100% 995.25 100% 1,072.74 100% 1,131.63 100% 1,199.39 100% 1,220.90 100% 1,209.96 100% 1,244.45 100% 1,253.54 100%

1) Including ownership of SBSN (government sukuk).

2) Foreign are consisted of Private Banking, Fund/Asset Management, Securities, Insurance, Pension Fund.

3) Others are consisted of Corporation, Individual, Foundation.

*) Since February 8th, 2008, repo transaction of Government Securities to Bank Indonesia was included.

**) Since November 21, 2014, foreign government(s) was included to the same category as foreign central bank(s).

13-Feb-15Sep-14Dec-13Dec-12 Mar-14 Jun-14 Jan-15Dec-14Nov-14

Domestic Institutional Investors

Pension Fund Insurance Company

Mutual Fund

Rp241.67

Rp326.23Rp356.45 Rp361.37

Rp497.03 Rp497.99

Rp545.54Rp567.13

27.09%

24.01%

21.77%

24.11%

19.74%21.02%

12.95%13.98%

0.00%

10.00%

20.00%

30.00%

0

100

200

300

400

500

600

2008 2009 2010 2011 2012 2013 Mar-14 Jun-14

Govt. Securities (GS) Bond

Deposit Stock

Mutual Funds Others

Rp90.11

Rp108.39

Rp141.51 Rp136.53

Rp156.45

Rp169.53 Rp164.15 Rp167.23

27.91% 27.43%

21.90%22.64%

19.68%18.36%

19.46%18.33%

0.00%

10.00%

20.00%

30.00%

0

30

60

90

120

150

180

2008 2009 2010 2011 2012 2013 Mar-14 Jun-14

Govt. Securities (GS) BondDeposit StockMutual Funds Others

45%

37%

33%

28%25%

20%

0%

10%

20%

30%

40%

50%

60%

0

30

60

90

120

150

180

210

240

270

Government Securities (GS) Deposit Bond Stock Others % SBN (RHS)

71.48

110.13

180.28

159

142.97

244.32

Source: Financial Service Authority (OJK), data

processsed

16

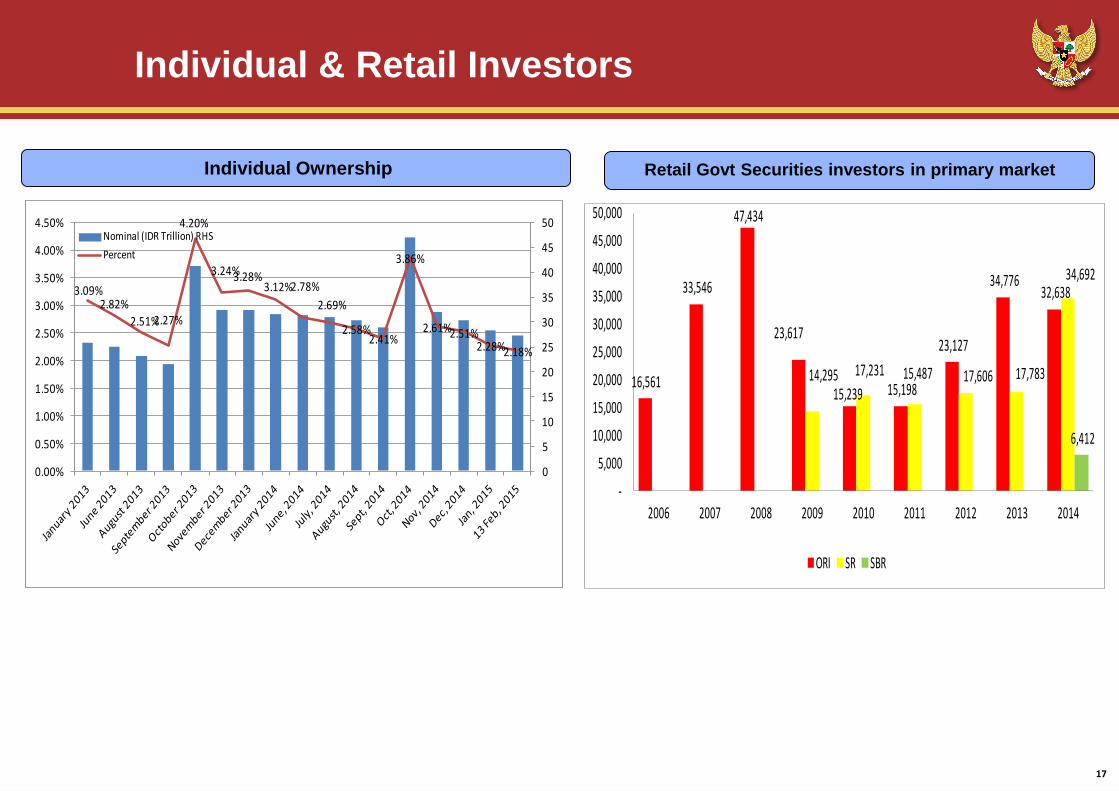

Individual & Retail Investors

Retail Govt Securities investors in primary market Individual Ownership

17

16,561

33,546

47,434

23,617

15,239 15,198

23,127

34,776 32,638

14,295 17,231 15,487 17,606 17,783

34,692

6,412

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

2006 2007 2008 2009 2010 2011 2012 2013 2014

ORI SR SBR

3.09%2.82%

2.51%2.27%

4.20%

3.24%3.28%3.12%2.78%

2.69%

2.58%2.41%

3.86%

2.61%2.51%2.28%2.18%

0

5

10

15

20

25

30

35

40

45

50

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%Nominal (IDR Trillion) RHS

Percent

Foreign Investor Activity 2014

Net Buyer (Seller) - Non Resident Foreign Ownership - Proportion by Tenor

[In IDR Trillion]

Foreign investors mostly dominated by high quality long term investors

18

10% 12% 8% 5% 6% 7% 7% 7% 6% 6% 5% 5% 5% 5% 5% 4%

5%8%

3% 5% 5% 4% 5% 3% 3% 3% 4% 4% 4% 4% 4% 3%

18%17%

16% 13% 11% 15% 15% 15% 16% 15% 15% 15% 16% 15% 14% 14%

21%

25%

28% 32% 38% 34% 33% 33% 33% 34% 34% 34% 33% 34% 34% 34%

46% 38% 45% 44% 41% 40% 41% 41% 42% 43% 42% 43% 42%43%

43% 43%

30.53%30.80%32.98% 32.54%

33.64%34.59% 35.72%35.66% 36.33%36.81%37.30% 37.80% 39.41% 38.13%40.25% 39.71%

-15.00%

5.00%

25.00%

45.00%

0%

20%

40%

60%

80%

100%

Dec-10 Dec-11 Dec-12 Dec-13 Mar-14 Apr-14 May-14 June 14 July 14 Aug 14 Sep-14 Oct-14 Nov-14 Dec-14 Jan-15 13-Feb-15

>10 >5-10 >2-5 >1-2 0-1 % Foreign Ownership to Total (RHS)

(1.49)

(29.29)

1.69

(4.99)

8.06

13.11

(8.99)

(2.27)

4.15

(4.37)

(0.08)

10.13

(1.41)

7.83 9.35

19.52

0.68 2.68

8.44

(0.88)

17.97

4.22

(19.98)

2.81

(1.76)

10.13

23.98

6.08

(0.37)

4.82

16.49

15.77 16.10

20.15

6.43

14.67

15.95

13.17 12.49

21.34

(19.84)

39.48

(3.03)

(0.15)

(0.10)

(0.05)

0.00

0.05

0.10

(40.00)

(30.00)

(20.00)

(10.00)

0.00

10.00

20.00

30.00

40.00

50.00

Au

g-1

1Se

p-1

1O

ct-

11

No

v-1

1D

ec-1

1Ja

n-1

2Fe

b-1

2M

ar-

12

Ap

r-1

2M

ay-1

2Ju

n-1

2Ju

l-1

2A

ug

-12

Se

p-1

2O

ct-

12

No

v-1

2D

ec-1

2Ja

n-1

3Fe

b-1

3M

ar-

13

Ap

r-1

3M

ay-1

3Ju

n-1

3Ju

l-1

3A

ug

-13

Se

p-1

3O

ct-

13

No

v-1

3D

ec-1

3Ja

n-1

4Fe

b-1

4M

ar-

14

Ap

r-1

4M

ay-1

4Ju

n-1

4Ju

l-1

4A

ug

-14

Se

p-1

4O

ct-

14

No

v-1

4D

ec-1

4Ja

n-1

5Fe

b-1

5

Capital Inflows Capital inflows over total foreign holders

Crisis Management Protocol &

Bond Stabilization Framework

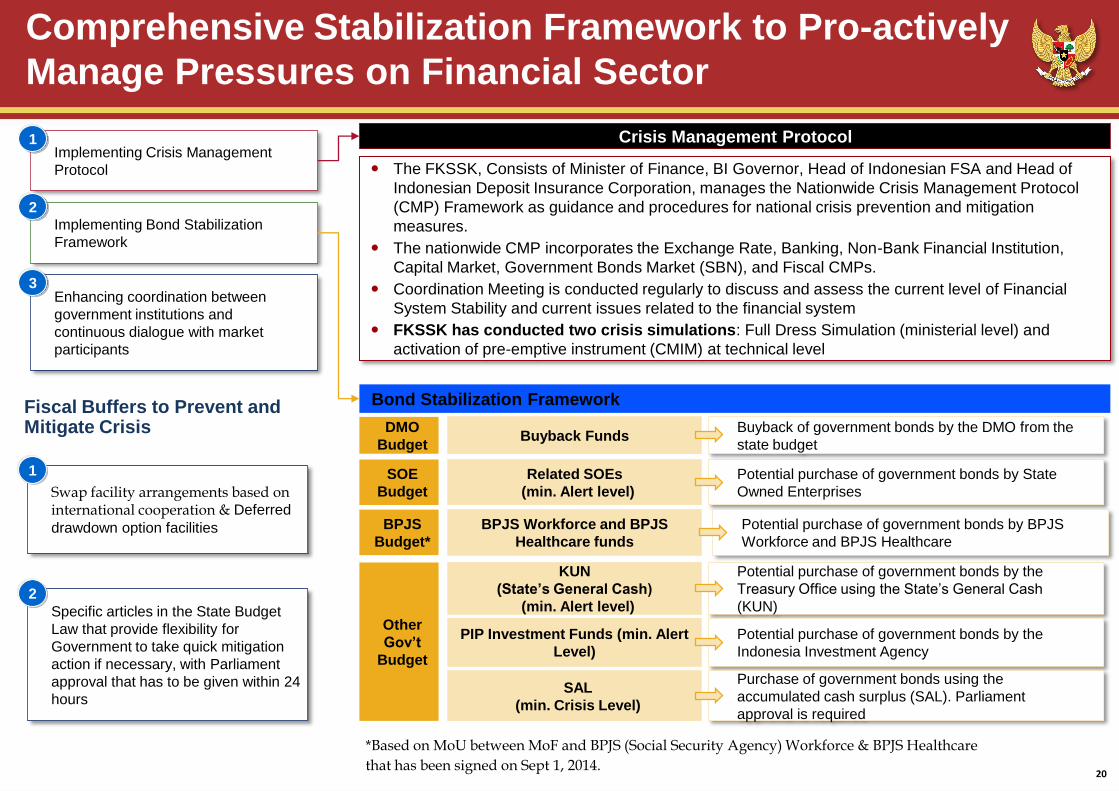

Comprehensive Stabilization Framework to Pro-actively

Manage Pressures on Financial Sector

Swap facility arrangements based on international cooperation & Deferred

drawdown option facilities

Implementing Crisis Management

Protocol

Implementing Bond Stabilization

Framework

Enhancing coordination between

government institutions and

continuous dialogue with market

participants

Specific articles in the State Budget

Law that provide flexibility for

Government to take quick mitigation

action if necessary, with Parliament

approval that has to be given within 24

hours

Fiscal Buffers to Prevent and Mitigate Crisis

The FKSSK, Consists of Minister of Finance, BI Governor, Head of Indonesian FSA and Head of

Indonesian Deposit Insurance Corporation, manages the Nationwide Crisis Management Protocol

(CMP) Framework as guidance and procedures for national crisis prevention and mitigation

measures.

The nationwide CMP incorporates the Exchange Rate, Banking, Non-Bank Financial Institution,

Capital Market, Government Bonds Market (SBN), and Fiscal CMPs.

Coordination Meeting is conducted regularly to discuss and assess the current level of Financial

System Stability and current issues related to the financial system

FKSSK has conducted two crisis simulations: Full Dress Simulation (ministerial level) and

activation of pre-emptive instrument (CMIM) at technical level

Crisis Management Protocol

Potential purchase of government bonds by State

Owned Enterprises

Buyback Funds DMO

Budget

SOE

Budget

Other

Gov’t

Budget

Buyback of government bonds by the DMO from the

state budget

Related SOEs

(min. Alert level)

KUN

(State’s General Cash)

(min. Alert level)

Potential purchase of government bonds by the

Treasury Office using the State’s General Cash

(KUN)

Potential purchase of government bonds by the

Indonesia Investment Agency

PIP Investment Funds (min. Alert

Level)

SAL

(min. Crisis Level)

Purchase of government bonds using the

accumulated cash surplus (SAL). Parliament

approval is required

Bond Stabilization Framework

Potential purchase of government bonds by BPJS

Workforce and BPJS Healthcare

BPJS

Budget*

BPJS Workforce and BPJS

Healthcare funds

*Based on MoU between MoF and BPJS (Social Security Agency) Workforce & BPJS Healthcare

that has been signed on Sept 1, 2014.

1

2

3

1

2

20

Debt Outstanding & Risk Profile

Maturity Profile Central Government Debt as of End of Jan 2015

Maturity Profile of Central Debt Government by Currency (in trillion Rp)

Maturity Profile of Central Government Debt by Instruments (in trillion Rp)

22

130111 108 102

144

95 99120

100

179

69

2248 53

7429 31 47 53

82

26 1042 48

8 12

178

6163 58 58

57

53 4741

36

31

27

23

20 1614

13 1313 12

8

53

21

11

5

020406080

100120140160180200220240

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

2041

-206

0

Gov't Sec Loan

118 100 8966

9663 53

76 69

135

4322

48 5374

29 31 47 5382

6 10 23 23 8 12

80

7374 77

93

104

84 9285

68

75

52

2320 16

14

13 1313 12

8

25 321

27

11

103

020406080

100120140160180200220240

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

2041

-206

0

Foreign Domestic

44.1%

55.9%

Foreign

Domestic

25.2%

74.8%

Loan

Gov't Sec

Outstanding Central Government Debt by Instrument

23

Nominal %

a. Foreign Loan (in billion USD) 68.6 68.4 63.6 58.4 53.9 53.7 25.1%

Bilateral 42.3 42.1 37.2 31.2 26.7 26.8 12.5%

Multilateral 23.2 23.5 23.8 23.6 23.5 23.3 10.9%

Commercial 3.0 2.8 2.5 3.2 3.7 3.6 1.7%

Suppliers 0.1 0.1 0.0 0.0 0.0 0.0 0.0%

b Domestic Loan (in billion USD) 0.0 0.1 0.19 0.2 0.2 0.3 0.1%

c. Government Securities (in billion USD) 118.4 131.0 140.8 136.3 155.2 160.1 74.8%

Foreign Currency Denominated 18.0 21.6 27.4 32.8 36.7 40.6 19.0%

Rupiah Denominated 100.4 109.4 113.4 103.5 118.5 119.4 55.8%

Total Central Government Debt

(in billion USD)187.0 199.5 194.9 209.4 214.0

Total Central Government Debt

(in trilion IDR)1,681.7 1,808.9 2,375.5 2,604.9 2,702.3

Exchange Rate Assumption (IDR/USD1) 8,991.0 9,068.0 12,189.0 12,440.0 12,625.0

GDP (in trillion IDR) 6,422.9 7,427.1 9,084.0 10,542.7

Debt to GDP Ratio 26.2% 24.4% 24.0% 26.2% 24.7%

Jan'15

20142013

8,241.9

9,670.0

2010

1,977.7

2011 2012

204.5

Description

Outstanding Central Government Debt by Currency

24

2010 2011

Original Currency

IDR (in trillion) 902.6 993.0 1,098.0 1,263.9 1,477.5 1,511.3

Gov't Securities 902.4 992.0 1,096.2 1,261.7 1,474.6 1,508.0

Loan 0.2 1.0 1.8 2.2 2.9 3.3

USD (in billion) 39.6 43.9 49.8 56.8 61.0 64.9

Gov't Securities 16.9 20.4 25.6 31.3 34.2 38.2

Loan 22.8 23.5 24.2 25.4 26.8 26.7

JPY (in billion) 2,689.8 2,589.8 2,498.8 2,395.3 2,204.0 2,204.0

Gov't Securities 95.0 95.0 155.0 155.0 155.0 155.0

Loan 2,594.8 2,494.8 2,343.8 2,228.8 2,049.0 2,059.4

EUR (in billion) 5.4 5.0 4.5 4.2 5.1 5.1

Gov't Securities - - - - 1.0 1.0

Loan 5.4 5.0 4.5 4.2 4.1 4.1

Other currencies

Equivalent in Billion USD

IDR 100.4 109.5 113.5 103.7 118.8 121.5 55.9%

USD 39.8 43.9 49.8 56.8 61.0 65.9 30.3%

JPY 33.1 33.4 29.1 22.8 18.5 19.0 8.8%

EUR 7.2 6.4 6.0 5.8 6.2 5.9 2.7%

Other currencies 6.5 6.3 6.1 5.8 5.0 4.9 2.3%

Total Eq. in Billion USD 187.0 199.5 204.5 194.9 209.4 217.2

Equivalent in Trillion IDR

IDR 902.8 993.0 1,098.0 1,263.9 1,477.5 1,511.3

USD 357.6 397.9 481.9 692.0 758.3 819.5

JPY 297.6 302.5 281.2 278.3 229.8 236.9

EUR 65.0 58.5 57.5 71.1 76.9 73.1

Other currencies 58.6 57.1 59.1 70.2 62.4 61.6

Total Eq. in Trillion IDR 1,681.7 1,808.9 1,977.7 2,375.5 2,604.9 2,702.3

Foreign Currency Portion 46.3% 45.1% 44.5% 46.8% 43.3%

Exchange Rate Assumption USD/IDR 8,991 9,068 9,670 12,189.0 12,440.0 12,625.0

2012

- - - - - - - - - - - - - - - - Multiple Currencies - - - - - - - - - - - - - - - - - - - - - - -

2014 Jan-152013

Central Government Debt Ratios

Debt to GDP Ratio Interest Payment to Revenue and

Expenditure Ratio

Debt Service to GDP Ratio Interest Payment to Tax Revenue &

Central Government Expenditure Ratio

25 Notes: • * Preliminary Figures

26.2% 24.4% 24.0%

26.2% 24.7%

0%

5%

10%

15%

20%

25%

30%

2010 2011 2012 2013 2014*

8.9

%

7.7

%

7.5

%

7.9

%

8.7

%

8.5

%

7.2

%

6.7

%

6.8

%

7.6

%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

2010 2011 2012 2013 2014*

Interest to Revenue Interest to Expenditure

3.4%

3.1%

3.3%

3.0%

3.4%

3%

3%

3%

3%

3%

3%

3%

4%

2010 2011 2012 2013 2014*

12

.2%

10

.7%

10

.8%

10

.5%

11

.7%

12

.7%

10

.6%

9.9

%

9.9

%

11

.2%

0%

2%

4%

6%

8%

10%

12%

14%

2010 2011 2012 2013 2014*

to Tax Revenue to Central Gov't Expenditure

Risk Indicators

26 Risk indicators are improving amidst pressure from rupiah depreciation Risk indicators show improvements in interest rate risk and stability in exchange and refinancing risks

Interest Rate Risk Exchange Rate Risk

Debt Maturing in 1,3, and 5 years Average Time To Maturity (ATM) - Years

22.0 20.3

18.8 16.2 16.0 14.8

28.2 26.1 25.9

22.5 23.2 21.0

2009 2010 2011 2012 2013 2014*

Variable rate ratio [%] Refixing rate [%]

9.7

9.5

9.3

9.7

9.6

9.8

2009 2010 2011 2012 2013 2014*

Average Time to Maturity (in percentage)

7.6 7.1 8.2 7.2 8.6 7.7

20.3 20.8 22.7 21.5 21.8 20.2

33.2 34.2 34.6 32.4 33.4 33.9

2009 2010 2011 2012 2013 2014*

Maturity debt portion < 1 year (%) Maturity debt portion < 3 year (%)

Maturity debt portion < 5 year (%)

*Preliminary Figures

13.4 12.1 11.0 10.6 12.2 10.7

47.4 46.2 45.1 44.4 46.7

43.3

2009 2010 2011 2012 2013 2014*

FX Debt to GDP ratio (%) FX Debt to total debt ratio (%)

Primary Market Performance 2015: Global Bonds (USD)

27

RI0125 RI0145

Summary Terms of Offering

Issuer

Issuer Ratings

Issue Ratings

Issue

Size USD2 billion USD2 billion

Pricing / Settlement Date 8 January / 15 January 2015 8 January / 15 January 2015

Maturity 10 years due 15 January 2025 30 years due 15 January 2045

Coupon 4.125% payable semi annually 5.125% payable semi annually

Reoffer Yield / Price 4.200% / 99.393% 5.200% / 98.867%

Format Rule 144A / Reg S Rule 144A / Reg S

Listing SGX-ST SGX-ST

Total Book Order USD10.05 billion USD9.23 billion

Republic of Indonesia

Baa3 Stable (Moody’s), BB+ Stable (S&P), BBB- Stable (Fitch)

Baa3 (Moody’s), BB+ (S&P), BBB- (Fitch)

USD fixed rate

Allocation by Geography

Allocation by Investor Type

Indonesia13%

Asia15%

Europe24%

USA48%

RI0125

Indonesia4%

Asia20%

Europe23%

USA53%

RI0145RI0125

RI0125

RI0145

RI0145

Fund / Asset Managers

73%

Banks14%

Insurance / Pension Funds

9%

Private Banks2%

SWF2%

Fund / Asset Managers

75%

Banks8%

Insurance / Pension Funds

13%

Private Banks2%

SWF2%

END OF PRESENTATION Directorate General of Debt Management Ministry of Finance of Republic of Indonesia Directorate of Government Debt Securities Frans Seda building, 4th floor, Jl. Wahidin Raya No. 1, Jakarta Pusat – Postal Code: 10710 Phone: +6221 3810175 Fax. : +6221 3846516 Site: www.djpu.kemenkeu.go.id

Securities Financing Realization 2014

*Adjusted by changes in Cash Management & Debt Switch

29

*(Million IDR)

Revised Budget

2014*

Realization

(ao Dec 31, 2014)*

% Realization to

Revised Budget

2014

Remaining target*

Government Securities Net 264,983,700 264,978,114 100.00% -

Government Securities Maturing in 2014 163,151,013 163,151,013 100.00% -

-Buyback 1,350,968 1,350,968 100.00% -

Issuance Need 2014* 428,134,713 428,129,127 100.00% 5,586

Government Debt Securities (GDS) 352,588,379

Domestic GDS 284,376,795

-Coupon GDS (Auction, Private Placement) 199,870,000

-Conventional T-Bills (Auction, Private Placement) 48,500,000

-SPNNT 20140303 12,400,000

-Retail Bonds 23,606,795

International Bonds 68,211,584

-USD Global Bonds 48,466,366

-USD Domestic Bonds 3,985,450

-Euro Denominated Bonds 15,759,767

-Samurai Bonds -

Government Islamic Debt Securities 75,540,748

Domestic Government Islamic Debt Securities 57,794,345

- IFR/PBS/T-Bills Sukuk (Islamic Fixed Rated Bond/Project Based Sukuk) 38,471,000

- Retail Sukuk 19,323,345

Global Sukuk 17,746,403