goods and services tax - malaysia insurance online · the effective date of the implementation of...

TRANSCRIPT

Copyright Reserved @ 2014 PIAM P a g e 1

GOODS AND SERVICES TAX

GENERAL INSURANCE

HANDBOOK

DISCLAIMER:

This document is prepared as a reference guide for member companies of PIAM

and cannot be interpreted as GST law/regulations, which are governed by the

Goods and Services Tax Act 2014

Copyright Reserved @ 2014 PIAM P a g e 2

Table of Contents SECTION 1 GENERAL..................................................................................................... 6

A. Implementation Date ........................................................................................... 6

B. Registered Person ............................................................................................... 6

C. GST Guide on Tax Invoice and Record Keeping:.......................................................... 6

D. Time frame to make input tax claim: ....................................................................... 6

E. Multiple Policyholder Parties ................................................................................. 7

F. Unidentified credit balance in bank accounts ............................................................ 7

SECTION 2 UNDERWRITING ........................................................................................... 10

A. Determination of Applicability of GST .................................................................... 10

B. Time of Supply ................................................................................................. 11

C. Transitional Issues ............................................................................................ 12

D. Incorporate GST Notice into the product policy wordings ........................................... 14

SECTION 3 REINSURANCE/COINSURANCE BUSINESS ............................................................. 18

A. Definitions ...................................................................................................... 18

B. Self Billing for Reinsurance Contracts .................................................................... 21

C. Determination of Applicability of GST .................................................................... 22

D. Time of Supply for Reinsurance ............................................................................ 26

E. Co-Insurance Business ........................................................................................ 28

F. Facultative Business – Examples ........................................................................... 29

F.1) Facultative Business through CAB .................................................................... 29

F.2) Facultative Business – Proportional .................................................................. 30

F.3) Facultative Business - Non Proportional ............................................................. 31

F.4) Offshore Facultative Business ......................................................................... 32

F.5) Offshore Facultative Business with a local branch ................................................ 33

F.6) Facultative Transitional Issues ........................................................................ 34

G. Treaty Business Example .................................................................................... 36

G.1) Non-proportional Treaty Business .................................................................... 36

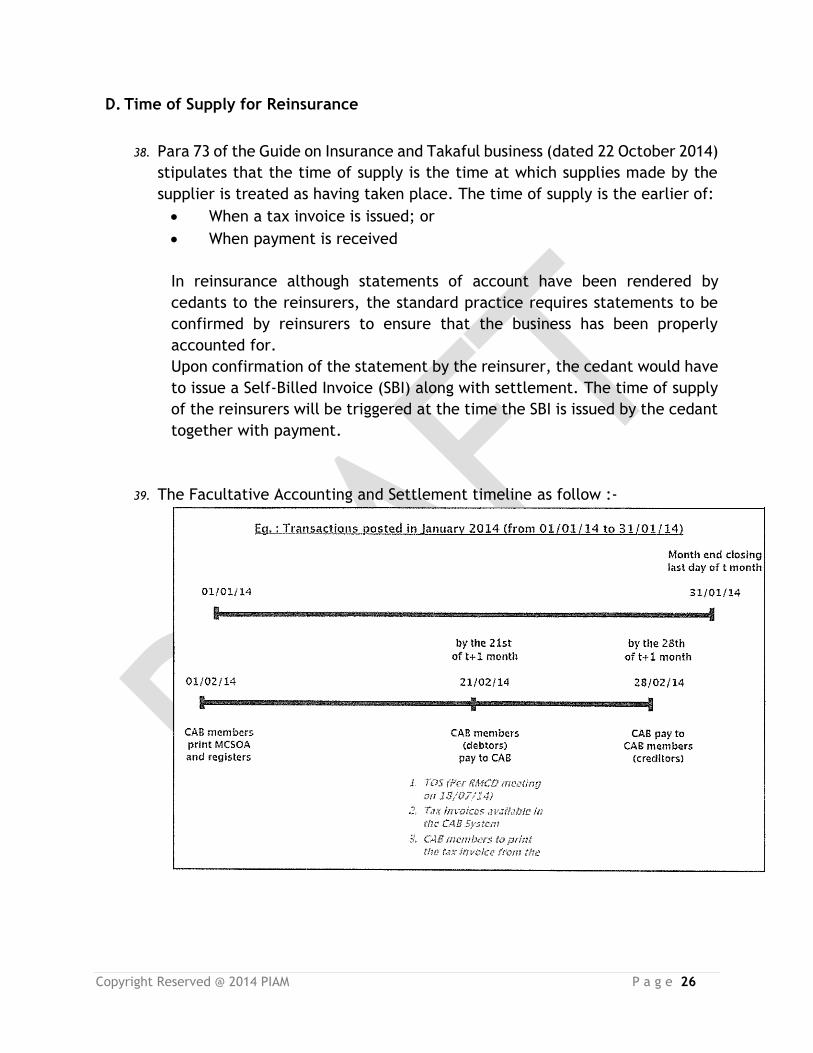

G.2) Non-proportional Treaty Business - Transitional Issues ........................................... 38

G.3) Proportional Treaty Business .......................................................................... 39

G.4) Proportional Treaty Business - Transitional Issues ................................................ 41

G.5) Claim Payments .......................................................................................... 41

SECTION 4 CLAIMS SETTLEMENT .................................................................................... 43

A. GST implications on Claims Settlement .................................................................. 43

B. Computation of deemed input tax credit ................................................................ 46

C. Reverse Charging GST on foreign services engaged: .................................................. 47

Copyright Reserved @ 2014 PIAM P a g e 3

D. Reimbursement under KFK Agreement: ................................................................. 47

E. Disposal of vehicles : ......................................................................................... 48

E.1) Disposal of vehicles as wrecks: ........................................................................ 48

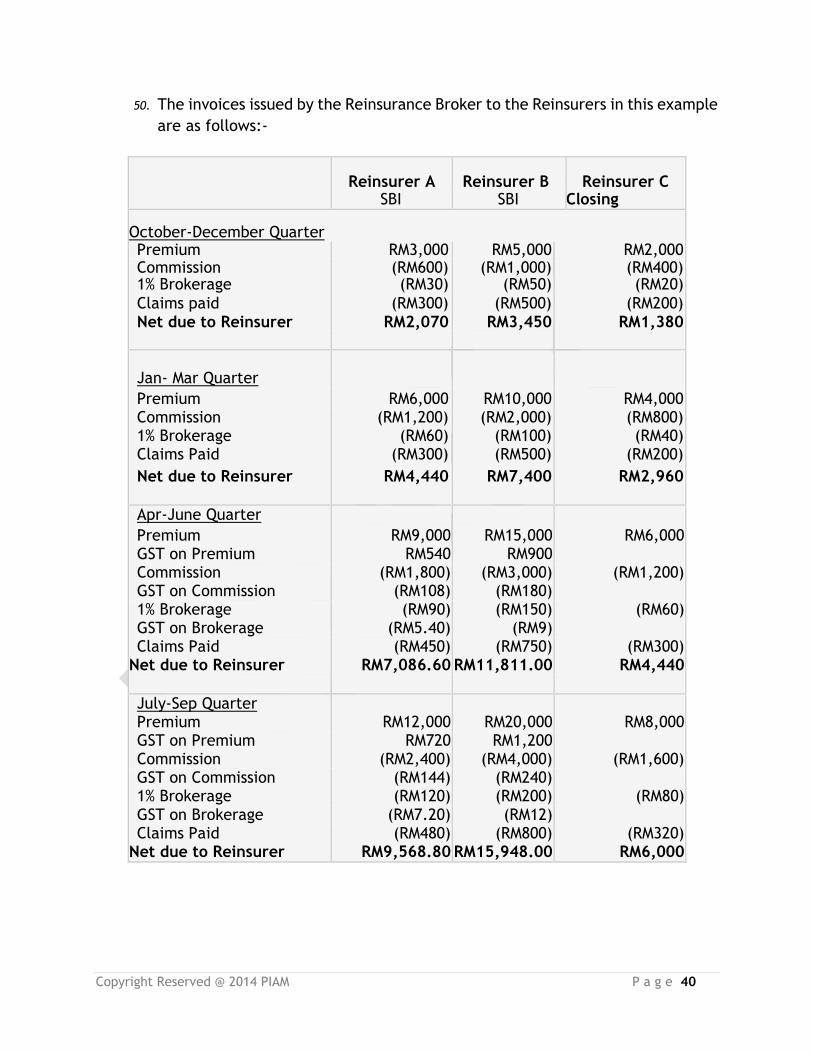

E.2) Disposal of vehicles as scraps : ........................................................................ 49

F. Cash Payment Involving Hire Purchase Agreement: ................................................... 49

G. Cash Payment .................................................................................................. 50

G.1) Cash Payment involving Ex Gratia settlement ...................................................... 50

G.2) Cash Payment involving Performance Bond ......................................................... 50

G.3) Cash Payments involving Hospital and Surgical (H & S) claims .................................. 50

H. Reimbursements: .............................................................................................. 51

I. Disbursements: ................................................................................................ 51

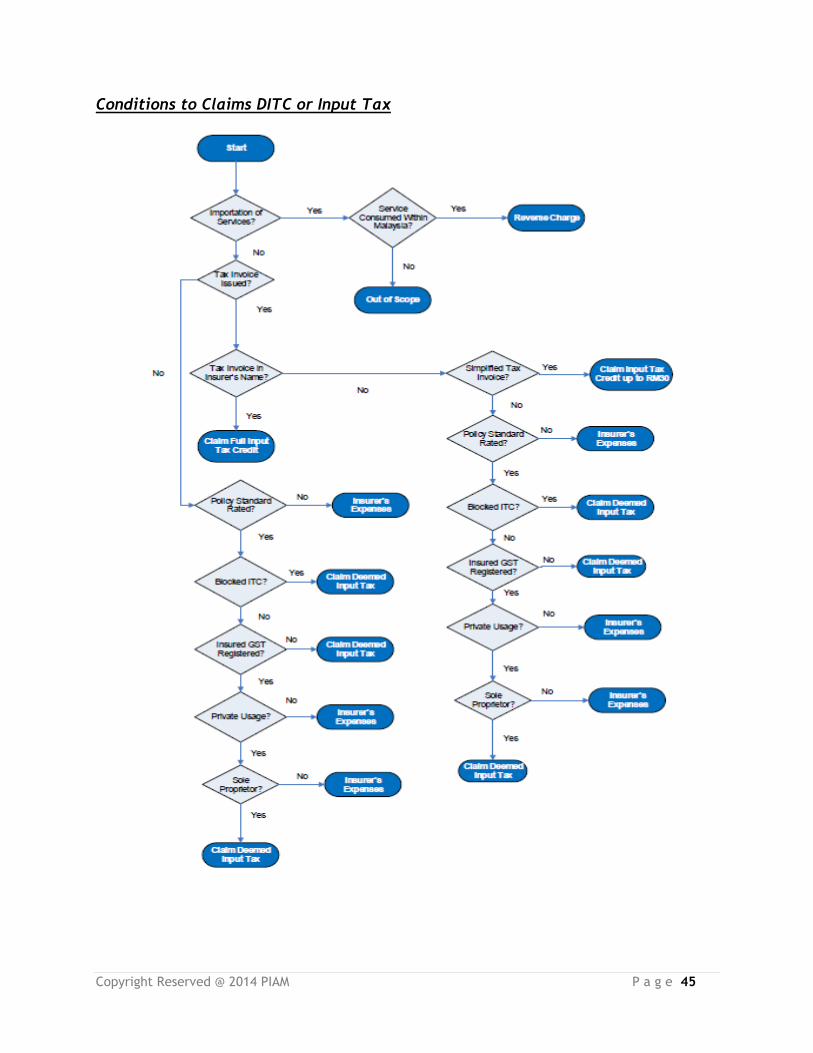

J. Recovery ........................................................................................................ 52

J.1) Excess ...................................................................................................... 52

J.2) Subrogation ............................................................................................... 52

J.3) Uncovered Charges ...................................................................................... 52

J.4) Reinsurance / Coinsurance Claims Recoveries ...................................................... 53

SECTION 5 INTERMEDIARIES .......................................................................................... 56

A. Determination of Applicability of GST .................................................................... 56

B. Time of supply:- ............................................................................................... 57

C. Transitional rules:- ............................................................................................ 58

D. Other benefits received by intermediaries ............................................................. 58

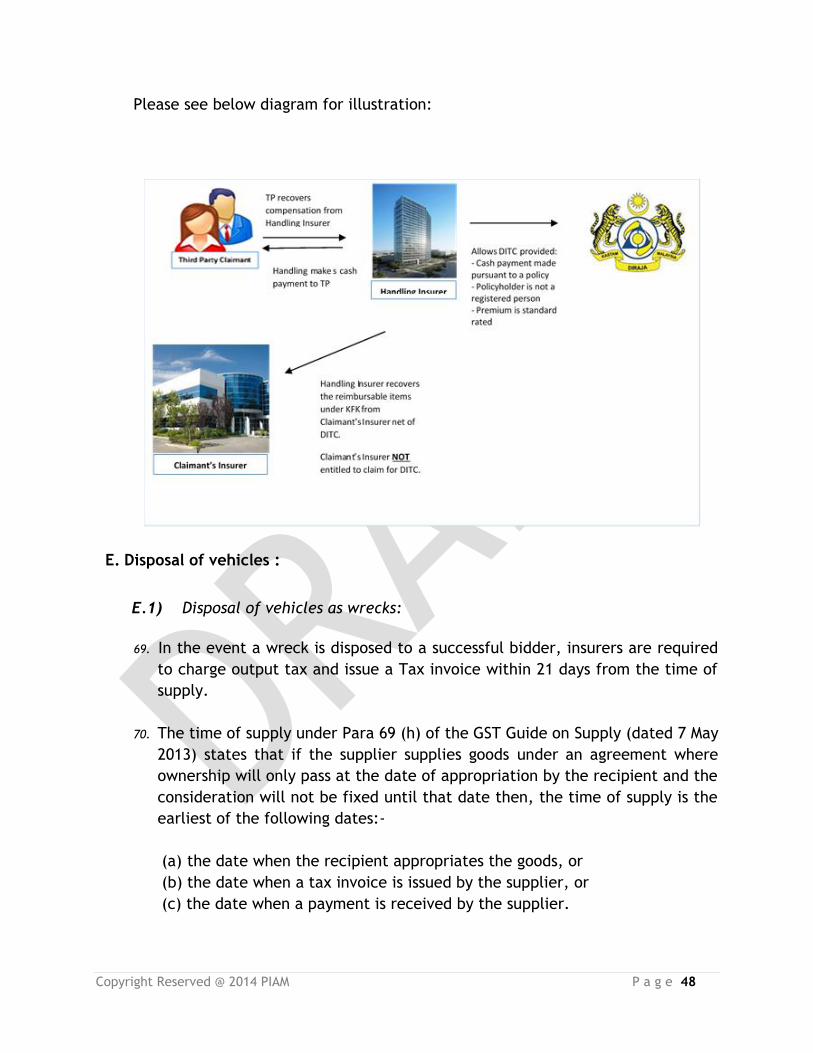

E. Self Billing for Intermediaries ............................................................................. 59

Copyright Reserved @ 2014 PIAM P a g e 4

Revision History

Version Date Author Changes Section

1.0 30/10/2014 PIAM Created Document

Document Approval

Reviewed By Role Signature Date

GST working Group

Approved By Role/Department Signature Date

Copyright Reserved @ 2014 PIAM P a g e 5

SECTION 1

GENERAL

Copyright Reserved @ 2014 PIAM P a g e 6

SECTION 1 GENERAL

A. Implementation Date

1. The effective date of the implementation of Goods and Services Tax (GST) is

on 1st April 2015.

B. Registered Person

2. A person who is registered under the GST Act 2014 is known as a “registered

person”. A registered person is required to charge output tax on his taxable

supply of goods and services made to his customers. He is allowed to claim

input tax credit on any GST incurred on his purchases which are inputs to his

business.

3. The threshold limit for a person to be a “registered person” is based on his

turnover of taxable supplies that exceeds or are expected to exceed RM500,000

over 12 months. Voluntary registration is allowed for those with turnover below

RM500,000.

4. The information of all registered persons will be made available by the Royal

Malaysian Customs Department (RMCD) and will be kept for more than 6 years.

This will take care of the time bar limit of 6 years.

5. Licensing fees for insurers, brokers and adjusters regulated by the Financial

Services Act 2013 are not subject to GST.

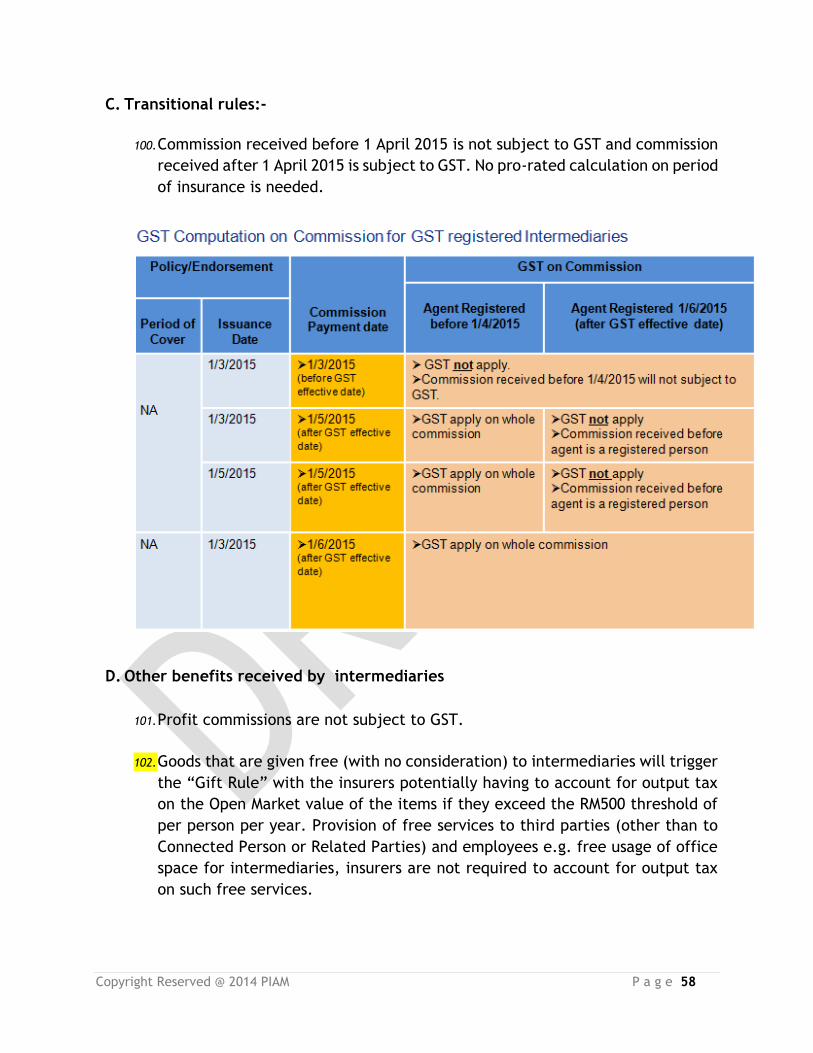

C. GST Guide on Tax Invoice and Record Keeping:

6. The specific GST Guide on Tax Invoice and Record Keeping requires us to keep

every reasonable accounting documents and records related to the tax credit

of all business supplies and acquisitions to enable GST auditors to establish the

nature, time and value of all taxable supplies and importation of goods and

services, including information which assists in reconciling accounting records

with the GST returns submitted. Electronic records are acceptable.

D. Time frame to make input tax claim:

7. If input tax is not claimed in the taxable period in which the tax invoice is

received, then such input tax can be claimed within six years from the date of

Copyright Reserved @ 2014 PIAM P a g e 7

the invoice. It should also be noted that an insurer is not required to make

payment before claiming input tax credit. Possessing a valid tax invoice is

sufficient evidence for making an ITC claim. However, it is important to take

note that if after 6 months of the invoice being issued, the insurer has still not

made payment to its service provider, the said insurer is required to repay any

input tax credit it has claimed with respect to this invoice. Upon settling the

invoice, the insurer may then reclaim the ITC.

E. Multiple Policyholder Parties

8. Some insurance contracts name multiple insured parties as the policyholder

and some may be based both in and outside Malaysia. The GST treatment in

this respect would be that the supply of insurance is treated as being received

in Malaysia irrespective of who is the party who stands to be the main

beneficiary and/or where the party belongs that has been most directly

involved in entering into the contract.

9. In other scenarios where a master policy is issued to Joint Management Body

and the respective unit owners are stated as joint policyholders and a claim is

filed by an individual unit owner, the DITC entitlement will be dependent upon

whether the individual claimant is a registered person or not.

F. Unidentified credit balance in bank accounts

10. The premium payment is treated as received by the insurers when the payment

is credited into the bank accounts of the insurers. However, it is not uncommon

that insurers are unable to identify the payees of the payment and match the

payment against the policies. This imposes challenges in complying to Time of

Supply rule particularly when payment is received but policy and tax invoice

has not been issued. To ensure compliance to the Time of Supply rule, the

unidentified premium received will be deemed inclusive of GST and insurers

will account the output tax by applying 6/106 on the unidentified payments in

the month when the amount is credited into the bank statements. When the

Comment:

To seek confirmation from EY and RMCD. The Task Force has received differing views

from different consultants on this matter. One consultant said that unit owner issued

with a Certificate of Insurance is regarded as a policyholder and thus if he/she makes a

claim, his status will be considered for DITC purpose. ) Confirmed by RMCD, Certificate

of insurance is regarded as policy holders.

Copyright Reserved @ 2014 PIAM P a g e 8

unidentified credits are subsequently identified and matched against the

policies, adjustment will be made to recover the “estimated” output tax which

has been paid. Similarly, when the insurer pay the unidentified credits to the

Registrar of Unclaimed Monies, adjustment will be made to recover the

estimated output tax.

Copyright Reserved @ 2014 PIAM P a g e 9

SECTION 2

UNDERWRITING

Copyright Reserved @ 2014 PIAM P a g e 10

SECTION 2 UNDERWRITING

A. Determination of Applicability of GST

11. Generally, all general insurance products are considered as taxable supplies.

Premiums charged to customers for the risks within Malaysia are subject to GST

at a standard rate.

12. All policies issued by locally domiciled insurers for a risk located overseas or

outside Malaysia will be a zero-rated supply.

13. Policies issued to non-profit organizations or charitable organizations are

subject to GST at a standard rate.

14. Personal Accident and Medical Insurance

i) Personal Accident and Medical Insurance products sold on a standalone basis

will be subject to GST. Similar covers sold as riders with a life policy will

also be subject to GST although a life policy is exempted from GST.

ii) Personal Accident policies purchased by an educational institution from

overseas, from a local general insurer for their scholars studying in Malaysia

will be subject to GST at a standard rate due to risks allocated in Malaysia

15. Marine and Hull Insurance

i) Hull Insurance on Vessel plying outside Malaysian shores will be zero rated

subject to Shipowners providing the necessary registration documents as

proof of trading limit that the Vessel not entering/leaving any port in

Malaysia during the period of insurance, failing which it will be standard

rated.

ii) Cargo insurance on goods in transit (i) from Malaysia to Overseas and vice

versa and (ii) Overseas to Overseas will be zero rated subject to

Exporter/Importer providing the invoice and bill of lading or airway bill or

road consignment note, failing which it will be standard rated.

Copyright Reserved @ 2014 PIAM P a g e 11

16. Fire and Others Class

i) Policies issued for a property located in Malaysia but is owned by a foreigner

will be subject to GST at a standard rate

ii) For fire insurance policies issued to cover a block of condominium arranged

by a Joint Management Body (JMB), and if the tax invoice is issued to the

JMB, the JMB can issue tax invoice to the individual condominium owners if

the JMB is a GST registered body.

17. If insurers issue a policy to cover the risks within and outside Malaysia and are

unable to segregate them into respective categories, the whole policy will be

subject to GST at standard rate. If an insurer is able to segregate the risks into

risks within Malaysia and outside Malaysia, the risk outside Malaysia will be

zero rated. For easy claims assessment in respect of eligibility to deemed input

tax credit, insurers may issue separate policy for risks outside Malaysia.

18. For a policy covering a risk in designated areas (Langkawi, Labuan and Tioman),

and if the insurer is in the designated areas as well, the premium will not be

subject to GST. However, if the insurer is in Principal Customs Area, the

premium will subject to GST.

19. In the event of a cancellation of a policy which entails a refund of premium to

the policyholder, the insurer will have to raise a credit note when he refunds

the premium, subsequently adjust his accounts, and reduce his output tax in

the return for the taxable period in which the credit note was issued.

B. Time of Supply

20. Insurance service is considered a continuous supply. The time of supply of an

insurance policy shall be deemed as follows, whichever is the earlier:-

i) When a tax invoice is issued; or

ii) When payment is received (or the date the money is credited into the

account)

However, in any event where (i) or (ii) is not triggered, then the basic tax

point will be the expiry date of the policy i.e. the date when service is

performed. If tax invoice is issued within 21 days from the basic tax point,

the time of supply is the tax invoice issuance date. If tax invoice is not issued

Copyright Reserved @ 2014 PIAM P a g e 12

within 21 days from the basic tax point, the time of supply is the expiry date

of the policy.

C. Transitional Issues

21. In the event a policy spans the period before and after 1 April 2015 (and is

currently not subject to service tax), GST will be chargeable on the part of the

supply of services that is made on or after 1 April 2015. GST will be computed

on a pro-rated basis and remitted to the Customs.

22. Insurers are not allowed to charge GST before 1 April 2015. If insurers do not

state in the policy the applicability of GST on the portion of premium for

insurance period span 1 April 2015, the amount received by insurers is deemed

inclusive of GST. For insurers to reserve the right to collect GST on the portion

of premium for insurance period spans 1 April 2015, Insurers are required to

include a clause in their policy contract or notification to the customers.

23. A copy of the GST Important Notice to facilitate the collection of pro-rated

GST (which has been approved by BNM) is attached.

24. The RMCD has offered relief from GST for policies which span the pre and post

period of GST and are currently not subject to service tax (i.e. issued to

individuals or non-business organizations) as follows:-

i) Motor vehicle insurance supplied before 1 April 2015 and the services

spans 1 April 2015, the premium charged and paid in full or in part

before 1 April 2015 for that supply is not subject to GST.

ii) Fire insurance supplied before 1 April 2015 and the services spans 1

April 2015, the premium charged and paid in full or in part before 1

April 2015 for the supply is not subject to GST.

The above relief will not be applicable to reinsurance premiums for such

policies.

Copyright Reserved @ 2014 PIAM P a g e 13

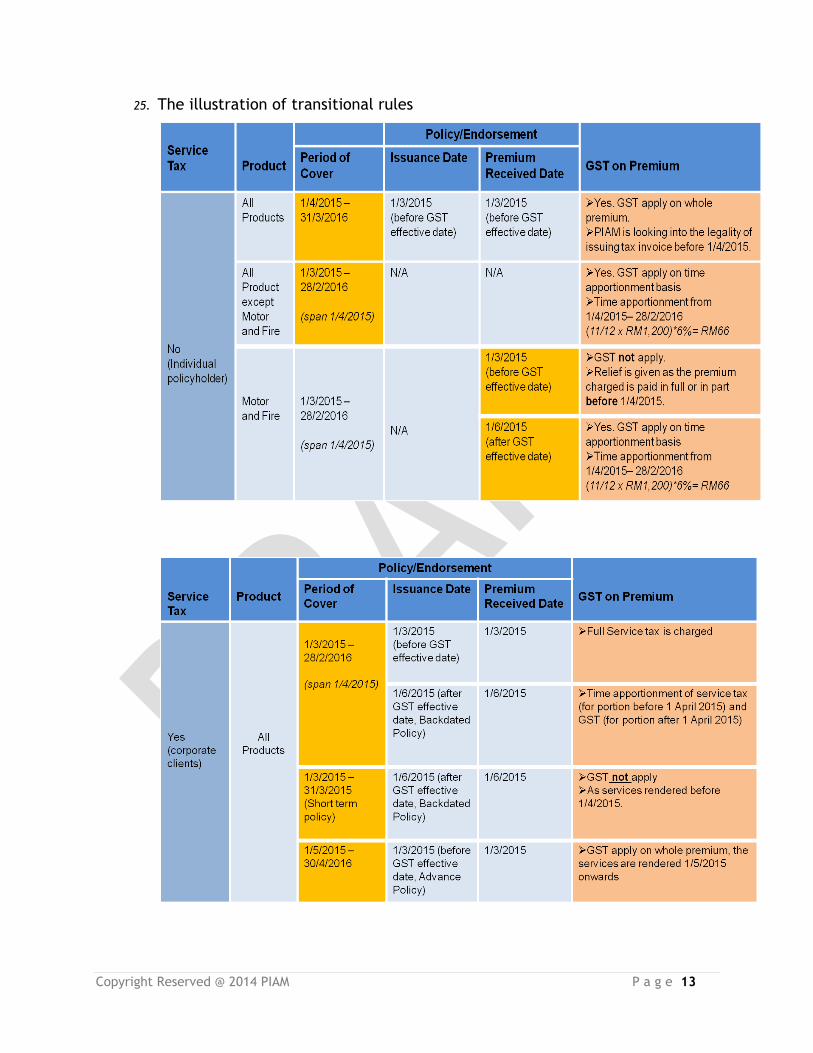

25. The illustration of transitional rules

Copyright Reserved @ 2014 PIAM P a g e 14

26. The transitional rules for policies subject to services tax :-

i) For policies spanning 1 April 2015, which are subject to service tax and

issued before 1 April 2015, insurers do not need to charge GST for the

portion after 1 April 2015 since service tax has been charged.

ii) For policies spanning 1 April 2015 but issued after 1 April 2015, service tax

and GST should be applied proportionally according to the period of

insurance.

iii) Even though the policy has been charged with service tax, any increasing

premium, e.g. increase in sum insured or extension after 1 April 2015, GST

will be applicable on the premium related to period after 1 April 2015.

iv) Any deduction of premium will be refunded to customers with service tax

or GST in accordance to the applicable taxes on the period of insurance

affected.

D. Incorporate GST Notice into the product policy wordings

27. Propose to incorporate GST Notice on Goods and Services Tax impact on Claims

Settlement into the product policy wordings as follow:-

a) (THIS WORDING IS FOR POLICY WITHOUT AVERAGE)

Claims settlement

We will pay your claim inclusive of the Goods and Services Tax on items which are taxable supplies, up to the limit of the Sum Insured. In the event that you are entitled to claim for the Input Tax Credit and if we make a payment under this policy as compensation to you, we will reduce the amount of the payment by deducting your Input Tax Credit entitlement irrespective of whether you have or have not claimed the Input Tax Credit, up to the limit of the Sum Insured.

b) (THIS WORDING IS FOR POLICY WITH AVERAGE CLAUSE)

Claims Settlement

We will pay your claim inclusive of the GST on items which are taxable

supplies, up to the limit of the Sum Insured.

Copyright Reserved @ 2014 PIAM P a g e 15

In the event that you are entitled to claim for the Input Tax Credit and if we

make a payment under this policy as compensation to you, we will reduce

the amount of the payment by deducting your Input Tax Credit entitlement

irrespective of whether you have or have not claimed the Input Tax Credit,

up to the limit of the Sum Insured.

Determining the adequacy of the Sum Insured

If the subject matter hereby insured (inclusive of the GST) shall, on the

happening of an insured peril, be collectively of greater value than the Sum

Insured thereon, then the Insured shall be considered as being his own insurer

for the difference, and shall bear a rateable proportion of the loss

accordingly. Every insured item, if more than one, of the policy shall be

separately subject to this condition.

In the event that you are entitled for the Input Tax Credit on each of the

insured item(s), the value as stated above will be reduced by deducting your

Input Tax Credit entitlement in determining the adequacy of the Sum Insured.

c) (THIS WORDING IS FOR LIABILITY POLICY)

Claims settlement

We will indemnify you on claims made by third party inclusive of the GST, up

to the limit of the Sum Insured.

In the event that you are entitled to claim for the Input Tax Credit and if we

make a payment under this policy as compensation to you, we will reduce

the amount of the payment by deducting your Input Tax Credit entitlement

irrespective of whether you have or have not claimed the Input Tax Credit,

up to the limit of the Sum Insured.

d) THIS WORDING IS FOR MOTOR POLICY (subject to the approval of authority)

(1) Claims Settlement

All claims settlement will be inclusive of GST on items which are taxable supplies. In the event that you are entitled to claim for the Input Tax Credit and if we make a payment under this policy as compensation to you, we will reduce

Copyright Reserved @ 2014 PIAM P a g e 16

the amount of payment by deducting your Input Tax Credit entitlement irrespective of whether you have or have not claimed the Input Tax Credit, up to the limit of the sum insured or the limits of liability.

(2) Sum Insured and the Limits of Liability

The maximum amount payable or Limits of Our Liability will be inclusive of

GST on items which are taxable supplies.

(3) Determining the adequacy of Sum Insured

The market value will be inclusive of GST on items which are taxable supplies. Should you be entitled for the Input Tax Credit on Your Vehicle, the market value as stated above will be reduced by deducting your Input Tax Credit entitlement in determining the adequacy of the Sum Insured.

Copyright Reserved @ 2014 PIAM P a g e 17

SECTION 3

REINSURANCE/

COINSURANCE

Copyright Reserved @ 2014 PIAM P a g e 18

SECTION 3 REINSURANCE/COINSURANCE BUSINESS

A. Definitions

28. The following terms have been defined for the purposes of these examples:

(a) Bordereaux:

A detailed list of premium or loss data and other agreed upon policy

information with respect to identified specific risks. It is furnished

periodically to the Reinsurer by the Insurer.

(b) Brokerage:

A payment by the Reinsurer for services rendered by the Reinsurance Broker,

including arranging the reinsurance and is usually based on a percentage of

premiums written.

(c ) Closing Slip/Closing:

An advice sent by the Insurer to the Reinsurer which specifies the actual

proportion of the risk allocated to the Reinsurer and the actual premium

receivable. The Insurer can authorize the Reinsurance Broker to prepare and

send this document to the Reinsurer.

(d) Commission:

A payment by the Reinsurer to the Insurer or Reinsurance Broker for the

handling of business placed with the Reinsurer (usually expressed as a

percentage of premiums written).

(e) Continuous Contract:

A reinsurance contract that remains in effect until both parties mutually

agree to terminate it or one of the parties sends the other a notice of

cancellation. A typical contract will either allow the parties to terminate at

any time or on any anniversary with three months' prior written notice.

(f) Facultative Reinsurance:

The reinsurance of an individual risk (a single primary/original policy) on

terms and conditions agreed with the Reinsurer specifically for that risk. The

Reinsurer may accept or decline the risk.

(g) Losses-Occurring Reinsurance:

Reinsurance cover provided on the basis that all losses occurring during the

Copyright Reserved @ 2014 PIAM P a g e 19

term of the reinsurance contract are covered, no matter when the loss is

notified.

(h) Loss Participation Clause:

An adjustment (negative) to the Commission paid and is out of scope.

(i) Non-Proportional Reinsurance:

A form of reinsurance where the Reinsurer makes loss payments to the

Insurer only when the Insurer's loss exceeds a pre-determined limit. It is

excess reinsurance.

(j) Premium:

A consideration for an insurance policy or treaty and it is earned over the

term of the policy or treaty.

(k) Profits Commission:

The share of treaty profits paid to the insurer and is out of scope.

(l) Proportional Reinsurance:

A reinsurance under which the insurer and the reinsurer share the risk in

agreed proportions which may be fixed or variable depending on the insurer's

retention and the sum insured. The reinsurer shares proportionally the

premiums earned and the claims incurred plus certain expenses incurred by

the insurer.

(m) Risk Attaching Policies:

This type of reinsurance covers the risk attaching to the primary or original

policies written during the period of the risk attaching policy. This means

that the cover will continue until the expiry of the original risks.

(n) Treaty Reinsurance:

A standing agreement between Insurers and Reinsurers for the cession or

assumption of certain risks as defined in the contract. Treaty reinsurance

may be divided into two broad classifications:-

(i) The participating type which provides for sharing of risks between the

Insurer and the Reinsurer. (Proportional Reinsurance)

(ii) The excess of loss type which provides for indemnity by the Reinsurer

only for loss, or losses, which exceed some specified predetermined

Copyright Reserved @ 2014 PIAM P a g e 20

amount. (Non-Proportional Reinsurance).

(o) Reinstatement Premium:

Additional premium paid in non-proportional treaties to reinstate the treaty

cover to original when liability is exhausted by a loss payment.

(p) Minimum Deposit Premium (MDP):

Premiums paid in advance in a non-proportional treaty either, annually, half

yearly or quarterly.

(q) Adjustment Premium:

Additional premiums paid in a non-proportional treaty calculated at the end

of the treaty period usually by applying a flat rate on actual gross premiums

received by the cedant.

(r ) Endorsement Premium:

Changes to original premiums charged due to amendments to the original

policy.

(s) Premium Portfolio Assumption:

Represents unearned premiums on original policies still in force credited at

the start of the treaty period to the incoming panel of reinsurers.

(t) Premium Portfolio Withdrawal:

Represents unearned premiums on original policies still in force debited at

the end of the treaty period to the outgoing panel of reinsurers.

(u) On Net Rate (ONR):

Reinsurance premiums reflected in the accounts are net of cedant’s original

acquisition costs.

Copyright Reserved @ 2014 PIAM P a g e 21

B. Self Billing for Reinsurance Contracts

29. It is assumed for the purposes of these examples that the relevant parties have

agreed that the premium is a GST exclusive amount and that GST is calculated

separately and added on top of the premium.

30. It is assumed for the purposes of these examples that the relevant parties have

a Self-Billed Invoice agreement (SBIA) and that the entity issuing the Self-

Billed Invoice (SBI) is a cedant registered for GST.

31. Para 70 of the Guide on Insurance and Takaful business (dated 22 October 2014)

stipulates that where self-billing is allowed, adjustments to originally

accounted amounts cannot be self–billed. It is the ordinary business that

cedants issue adjustments or endorsements to the originally accounted

amounts due to changes in the original policy premiums or cumulative claims

experience in non-proportional treaties. In addition, in treaty accounting it is

not possible to separate original premiums from endorsements or changes. Due

to the nature of insurance/reinsurance transactions, the self-billed invoice

issued by cedants will inevitably include all reinsurance premium,

endorsements, adjustment premiums and reinstatement premiums.

32. The cedant may choose to consolidate all the confirmed transactions in a

month and issue a monthly SBI reflecting the individual policy/treaty details

and respective GST where settlements are on a monthly basis. A single

consolidated SBI may also be issued for each settlement between cedant and

reinsurer where settlements are based on confirmed balances.

Please see Appendix 1, 2 and 3 for samples of an SBI agreement, SBI and

consolidated SBI.

Copyright Reserved @ 2014 PIAM P a g e 22

C. Determination of Applicability of GST

33. The reinsurance contract is treated as a contract separate from the underlying

insurance contracts that are protected. Hence, determination of the

treatment of GST on reinsurance premium is not based on the underlying

policies. Determination of the treatment of GST is determined based on the

domicile of the contracting parties.

34. For treaties which are accounted for on an ONR basis, GST will be calculated

on the premiums net of original acquisition costs.

35. The reverse charge mechanism is used when the supplier of services i.e. the

reinsurer is a non-resident. The recipient of the supply who is GST registered

person is required to account the GST on the reinsurance premium as output

tax and is entitled to claim the GST incurred as input tax (as the imported

services is used for making taxable supply of general insurance )at the same

time in the GST Return for the taxable period where the payment is made to

the non-resident reinsurer.

Copyright Reserved @ 2014 PIAM P a g e 23

36. The table below illustrates the various scenarios and the GST treatment

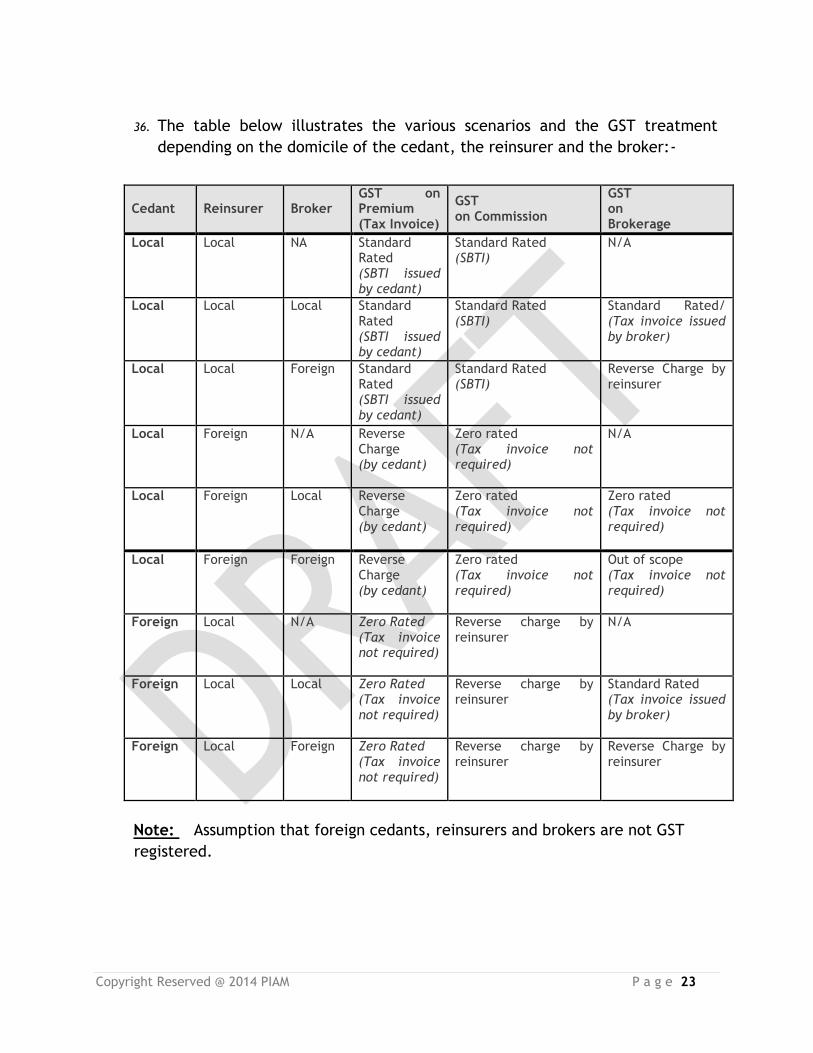

depending on the domicile of the cedant, the reinsurer and the broker:-

Note: Assumption that foreign cedants, reinsurers and brokers are not GST

registered.

Cedant Reinsurer Broker GST on Premium (Tax Invoice)

GST on Commission

GST on Brokerage

Local Local NA Standard Rated (SBTI issued by cedant)

Standard Rated (SBTI)

N/A

Local Local Local Standard Rated (SBTI issued by cedant)

Standard Rated (SBTI)

Standard Rated/ (Tax invoice issued by broker)

Local Local Foreign Standard Rated (SBTI issued by cedant)

Standard Rated (SBTI)

Reverse Charge by reinsurer

Local Foreign N/A Reverse Charge (by cedant)

Zero rated (Tax invoice not required)

N/A

Local Foreign Local Reverse Charge (by cedant)

Zero rated (Tax invoice not required)

Zero rated (Tax invoice not required)

Local Foreign Foreign Reverse Charge (by cedant)

Zero rated (Tax invoice not required)

Out of scope (Tax invoice not required)

Foreign Local N/A Zero Rated (Tax invoice not required)

Reverse charge by reinsurer

N/A

Foreign Local Local Zero Rated (Tax invoice not required)

Reverse charge by reinsurer

Standard Rated (Tax invoice issued by broker)

Foreign Local Foreign Zero Rated (Tax invoice not required)

Reverse charge by reinsurer

Reverse Charge by reinsurer

Copyright Reserved @ 2014 PIAM P a g e 24

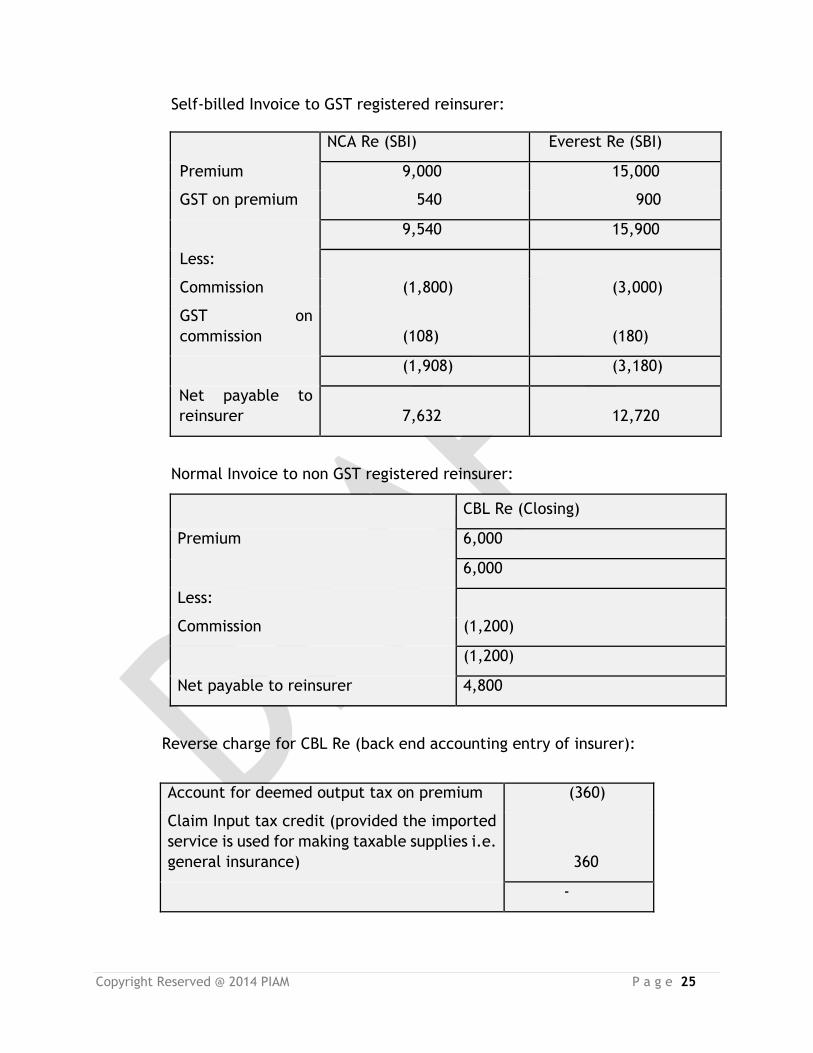

37. Example:

It is assumed for the purposes of this example that the relevant parties have

agreed that the premium is a GST exclusive amount and that GST is

calculated separately and added on top of the premium and that the

relevant parties have a Self-Billed Invoice (SBI) agreement and meets

the requirements. The parties are Reinsurers NCA Re, Everest Re and CBL

Re and insurer is Tamla Insurance.

Tamla, NCA Re and Everest Re register for GST. CBL Re is a non-resident and

is not registered nor required to be registered for GST.

Tamla underwrites a property insurance cover (general insurance services)

for an international industrial company with a premium of RM60,000 which

runs for one year commencing 1 October 2016.

On 1 October 2016, Tamla decided to proportionally reinsure this policy

as follows:

Reinsurers GST Status Share

NCA Re GST Registrant 15%

Everest Re GST Registrant 25%

CBL Re Non-Resident 10%

Tamla receives 20% commission for placing this policy.

Tamla issues a SBTI to both NCA Re and Everest Re. CBL Re is a non-resident

and is not a GST registered person nor required to be registered for GST in

Malaysia , its supply of reinsurance is not a taxable supply and Tamla need

only issue the usual commercial documentation, if requested. However,

Tamla has to account for GST under the reverse charge mechanism for the

supply of reinsurances services by CBL Re.

The SBI issued by Tamla is for a supply received by Tamla. In this

case, Tamla will issue a tax invoice detailing the supply of reinsurance.

The invoice issued by the Insurer to the Reinsurers in this example are as

follows: -

Copyright Reserved @ 2014 PIAM P a g e 25

Self-billed Invoice to GST registered reinsurer:

Normal Invoice to non GST registered reinsurer:

CBL Re (Closing)

Premium 6,000

6,000

Less:

Commission (1,200)

(1,200)

Net payable to reinsurer 4,800

Reverse charge for CBL Re (back end accounting entry of insurer):

NCA Re (SBI) Everest Re (SBI)

Premium 9,000 15,000

GST on premium 540 900

9,540 15,900

Less:

Commission (1,800) (3,000)

GST on

commission (108) (180)

(1,908) (3,180)

Net payable to

reinsurer 7,632 12,720

Account for deemed output tax on premium (360)

Claim Input tax credit (provided the imported

service is used for making taxable supplies i.e.

general insurance) 360

-

Copyright Reserved @ 2014 PIAM P a g e 26

D. Time of Supply for Reinsurance

38. Para 73 of the Guide on Insurance and Takaful business (dated 22 October 2014)

stipulates that the time of supply is the time at which supplies made by the

supplier is treated as having taken place. The time of supply is the earlier of:

When a tax invoice is issued; or

When payment is received

In reinsurance although statements of account have been rendered by

cedants to the reinsurers, the standard practice requires statements to be

confirmed by reinsurers to ensure that the business has been properly

accounted for.

Upon confirmation of the statement by the reinsurer, the cedant would have

to issue a Self-Billed Invoice (SBI) along with settlement. The time of supply

of the reinsurers will be triggered at the time the SBI is issued by the cedant

together with payment.

39. The Facultative Accounting and Settlement timeline as follow :-

Copyright Reserved @ 2014 PIAM P a g e 27

40. Below illustrates the Treaty Accounting and Settlement timeline

Copyright Reserved @ 2014 PIAM P a g e 28

E. Co-Insurance Business

41. If a co-leader issues the 100% tax invoice to the customer, co-leader will collect

100% GST and remit to the Customs. Co-followers will then issue their tax

invoice on their respective shares to charge the GST to the Co-leader. As the

principle of co-insurance is sharing the same risk, if the tax invoice issued by

co-leader is zero rated, the premium charged by co-followers will also zero

rated.

42. GST treatment for coinsurance transactions is based on underlying policy as

below:- (To confirm)

43.

44. If however co-followers issue their respective tax invoices to customers for

their own share, they will collect their respective share of the GST and remit

to the Customs

45. The recovery of direct commissions and co-insurance fees charged by the co-

leader to the co-followers is subject to GST.

Coinsurance Inward

GST Treatment on Underlying

Policy

GST On Premium

(Output Tax)

GST on Commission (Input Tax)

Local Co-insurer Standard Rated Standard Rated Input Tax Credit

Local Co-insurer Zero Rated Zero Rated Input Tax Credit

Foreign Co-insurer Standard Rated Standard Rated

Reverse Charge

Foreign Co-insurer Zero Rated Zero rated

Reverse Charge

Local Co-insurer Standard Rated Input Tax Credit

Standard Rated

Local Co-insurer Zero Rated No input tax - Zero rated

supply

Standard Rated

Foreign Co-insurer Standard Rated Reverse Charge Zero Rated

Foreign Co-insurer Zero Rated Reverse Charge Zero rated

Copyright Reserved @ 2014 PIAM P a g e 29

46. Co-leader and Co-followers are advised to enter into a self-billing arrangement

for co-leaders to issue self-billed invoices on behalf of co-followers

47. During the transition period, co-leaders should issue self-billed invoices and

pay the GST on premium to co-followers in respect of policies issued before

and with insurance periods span 1 April 2015 and claim back as input tax. Co-

followers to account it as output tax. The practice is same as reinsurance

(Refer to Section 3, sub section B).

F. Facultative Business – Examples

F.1) Facultative Business through CAB

o Cedant places policy closings in CABFAC System. The month is

identified as t month.

o Reinsurers can accept the closings or CABFAC System may auto-accept

the transactions. Acceptance is still within t month, at times

acceptance may flow to t+1 month.

o Cedant and reinsurer generate the monthly consolidated statement of

accounts (MCSOA) and registers. These MCSOA is a summary of the

transactions for t month. Details of the transactions are, however,

shown in the ceded policy premium/endorsement premium/claim

register and accepted policy premium/endorsement premium/claim

register. The documents are generated on t+1 month. These

documents will show the GST amount.

o On 21st of t+1 month all debtors need to settle the amount owing to

others. This includes everyone with ceded policy premium register,

ceded endorsement premium register and ceded claim paid register. At

this point the time of supply is triggered.

o CAB members generate self-billed invoice (SBI) on 21st of t+1 month.

The SBTI cannot be generated earlier than 21st of t+1 month in view of

Sec 33(7) GST Act 2014. Settlement to all creditors takes place on 28th

of t+1 month and the reinsurer will account payment to Royal Malaysian

Customs Department (RMCD) by the last day of t+2 month.

Copyright Reserved @ 2014 PIAM P a g e 30

o Example:

Transactions posted in April 2014, CAB members will print the

documents on 01/05/14. For amount due to CAB, the payment will be

made from debtors on 21/05/14 and the TOS is triggered. For amount

due from CAB, the payment will be made to creditors on 28/05/14.

Please refer to para 39 on the Facultative Accounting and Settlement

timeline.

F.2) Facultative Business – Proportional

o The Insurer, Reinsurer A and Reinsurer B are registered for GST.

Reinsurer C is not a resident of Malaysia and is not registered or required

to be registered for GST.

o The Insurer underwrites a property insurance cover for a global

industrial company with a premium of RM20,000 which runs for one year

commencing 1 July 2015.

o On 1 July 2015 the Insurer decided to proportionally reinsure this policy

as follows:

Reinsurer A - 15%

Reinsurer B - 25%

Reinsurer C - 10%

o The Insurer will receive 20% commission for placing this policy.

The Insurer will issue a Self-Billed Invoice (SBI) to both Reinsurer A and

Reinsurer B. As Reinsurer C is not registered or required to be registered

for GST the supply of the reinsurance is not a taxable supply and the

Insurer will only need to issue the usual commercial documentation

(i.e. either closing or bordereau) if requested.

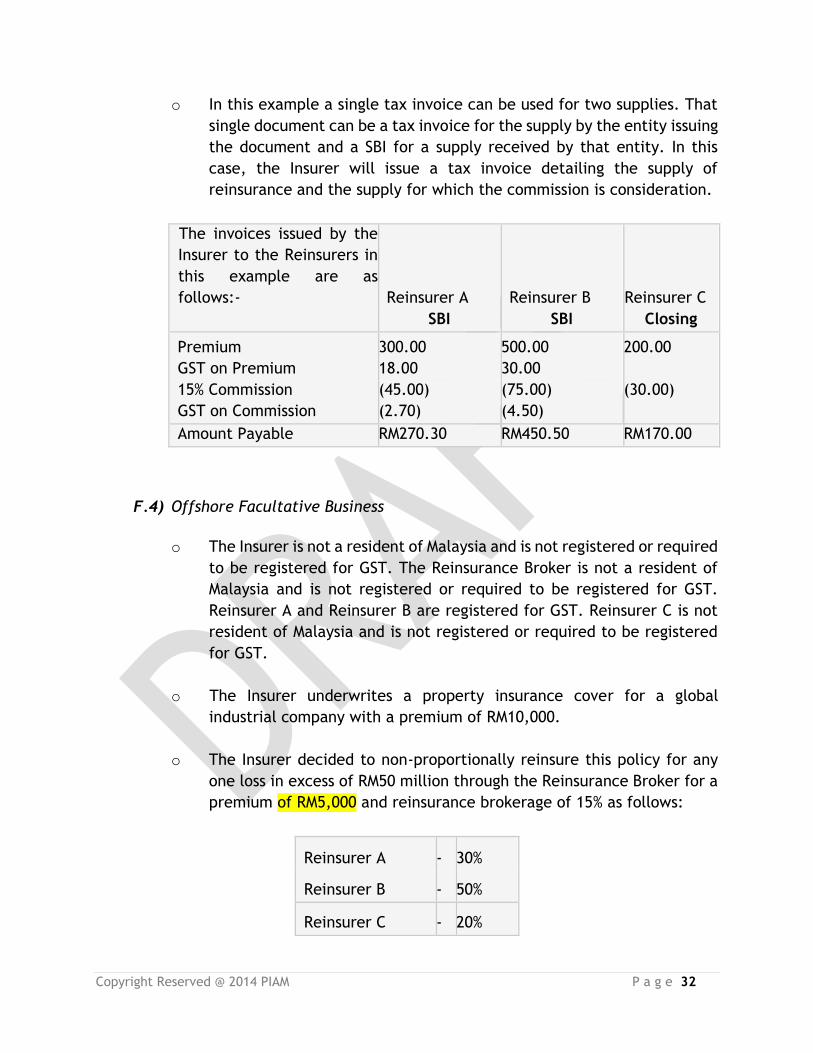

o In this example a single tax invoice can be used for two supplies. That

single document can be a tax invoice for the supply by the entity issuing

the document and a SBI for a supply received by that entity. In this

case, the Insurer will issue a tax invoice detailing the supply of

reinsurance and the supply for which the commission is consideration.

The invoices issued by the Insurer to the Reinsurers in this example are

Copyright Reserved @ 2014 PIAM P a g e 31

as follows:-

Reinsurer A Reinsurer B Reinsurer C

SBI SBI Closing

Premium 3,000.00 5,000.00 2,000.00

GST on Premium 180.00 300.00

20% Commission (600.00) (1,000.00) (400.00)

GST on Commission (36.00) (60.00)

Amount Payable RM2,544.00 RM4,240.00 RM1,600.00

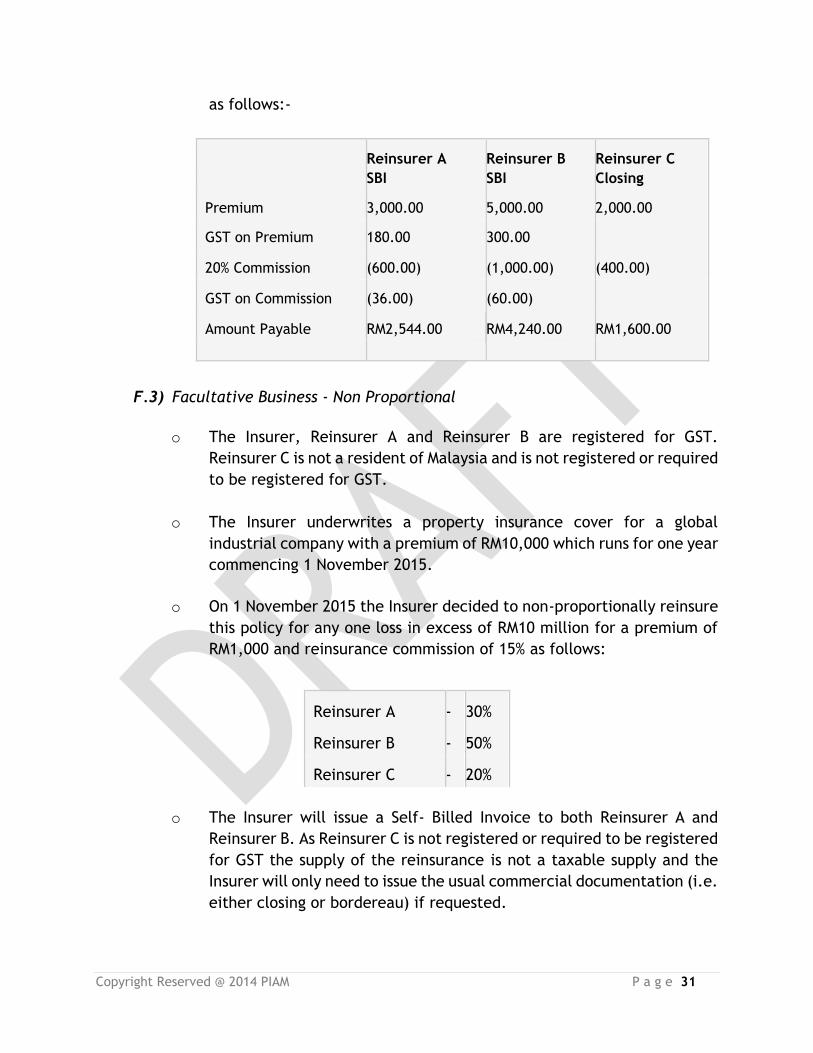

F.3) Facultative Business - Non Proportional

o The Insurer, Reinsurer A and Reinsurer B are registered for GST.

Reinsurer C is not a resident of Malaysia and is not registered or required

to be registered for GST.

o The Insurer underwrites a property insurance cover for a global

industrial company with a premium of RM10,000 which runs for one year

commencing 1 November 2015.

o On 1 November 2015 the Insurer decided to non-proportionally reinsure

this policy for any one loss in excess of RM10 million for a premium of

RM1,000 and reinsurance commission of 15% as follows:

Reinsurer A - 30%

Reinsurer B - 50%

Reinsurer C - 20%

o The Insurer will issue a Self- Billed Invoice to both Reinsurer A and

Reinsurer B. As Reinsurer C is not registered or required to be registered

for GST the supply of the reinsurance is not a taxable supply and the

Insurer will only need to issue the usual commercial documentation (i.e.

either closing or bordereau) if requested.

Copyright Reserved @ 2014 PIAM P a g e 32

o In this example a single tax invoice can be used for two supplies. That

single document can be a tax invoice for the supply by the entity issuing

the document and a SBI for a supply received by that entity. In this

case, the Insurer will issue a tax invoice detailing the supply of

reinsurance and the supply for which the commission is consideration.

The invoices issued by the

Insurer to the Reinsurers in

this example are as

follows:- Reinsurer A Reinsurer B Reinsurer C

SBI SBI Closing

Premium 300.00 500.00 200.00

GST on Premium 18.00 30.00

15% Commission (45.00) (75.00) (30.00)

GST on Commission (2.70) (4.50)

Amount Payable RM270.30 RM450.50 RM170.00

F.4) Offshore Facultative Business

o The Insurer is not a resident of Malaysia and is not registered or required

to be registered for GST. The Reinsurance Broker is not a resident of

Malaysia and is not registered or required to be registered for GST.

Reinsurer A and Reinsurer B are registered for GST. Reinsurer C is not

resident of Malaysia and is not registered or required to be registered

for GST.

o The Insurer underwrites a property insurance cover for a global

industrial company with a premium of RM10,000.

o The Insurer decided to non-proportionally reinsure this policy for any

one loss in excess of RM50 million through the Reinsurance Broker for a

premium of RM5,000 and reinsurance brokerage of 15% as follows:

Reinsurer A - 30%

Reinsurer B - 50%

Reinsurer C - 20%

Copyright Reserved @ 2014 PIAM P a g e 33

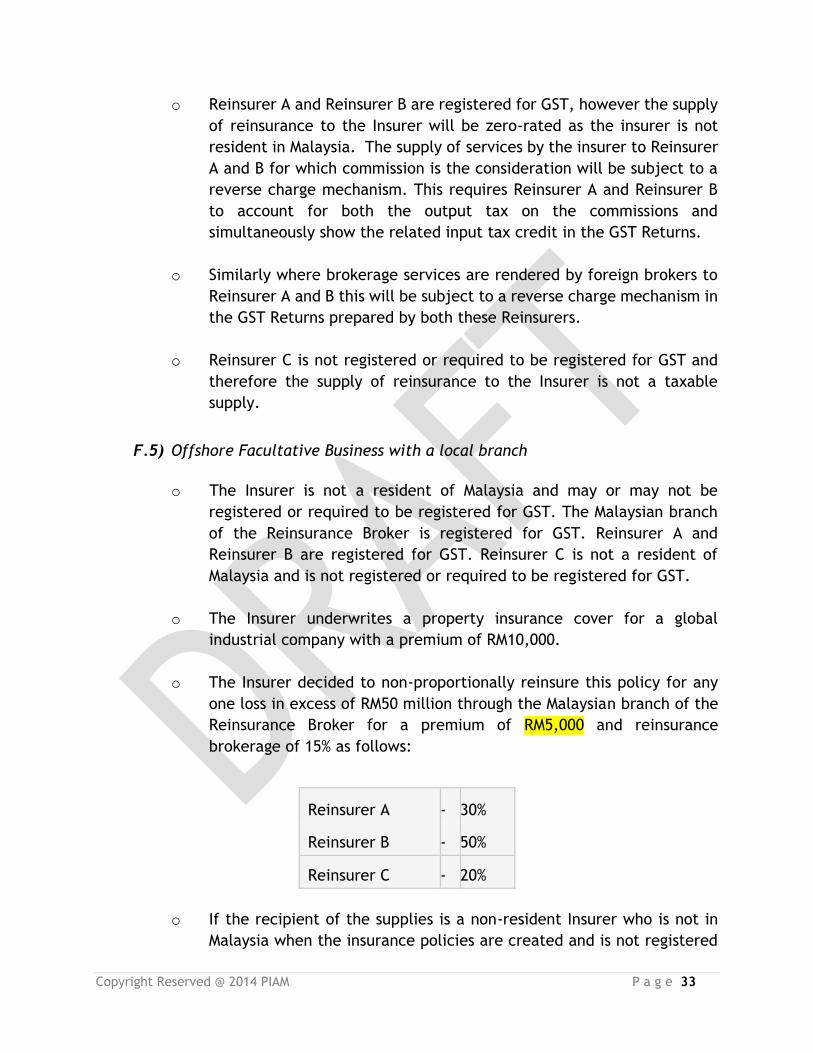

o Reinsurer A and Reinsurer B are registered for GST, however the supply

of reinsurance to the Insurer will be zero-rated as the insurer is not

resident in Malaysia. The supply of services by the insurer to Reinsurer

A and B for which commission is the consideration will be subject to a

reverse charge mechanism. This requires Reinsurer A and Reinsurer B

to account for both the output tax on the commissions and

simultaneously show the related input tax credit in the GST Returns.

o Similarly where brokerage services are rendered by foreign brokers to

Reinsurer A and B this will be subject to a reverse charge mechanism in

the GST Returns prepared by both these Reinsurers.

o Reinsurer C is not registered or required to be registered for GST and

therefore the supply of reinsurance to the Insurer is not a taxable

supply.

F.5) Offshore Facultative Business with a local branch

o The Insurer is not a resident of Malaysia and may or may not be

registered or required to be registered for GST. The Malaysian branch

of the Reinsurance Broker is registered for GST. Reinsurer A and

Reinsurer B are registered for GST. Reinsurer C is not a resident of

Malaysia and is not registered or required to be registered for GST.

o The Insurer underwrites a property insurance cover for a global

industrial company with a premium of RM10,000.

o The Insurer decided to non-proportionally reinsure this policy for any

one loss in excess of RM50 million through the Malaysian branch of the

Reinsurance Broker for a premium of RM5,000 and reinsurance

brokerage of 15% as follows:

Reinsurer A - 30%

Reinsurer B - 50%

Reinsurer C - 20%

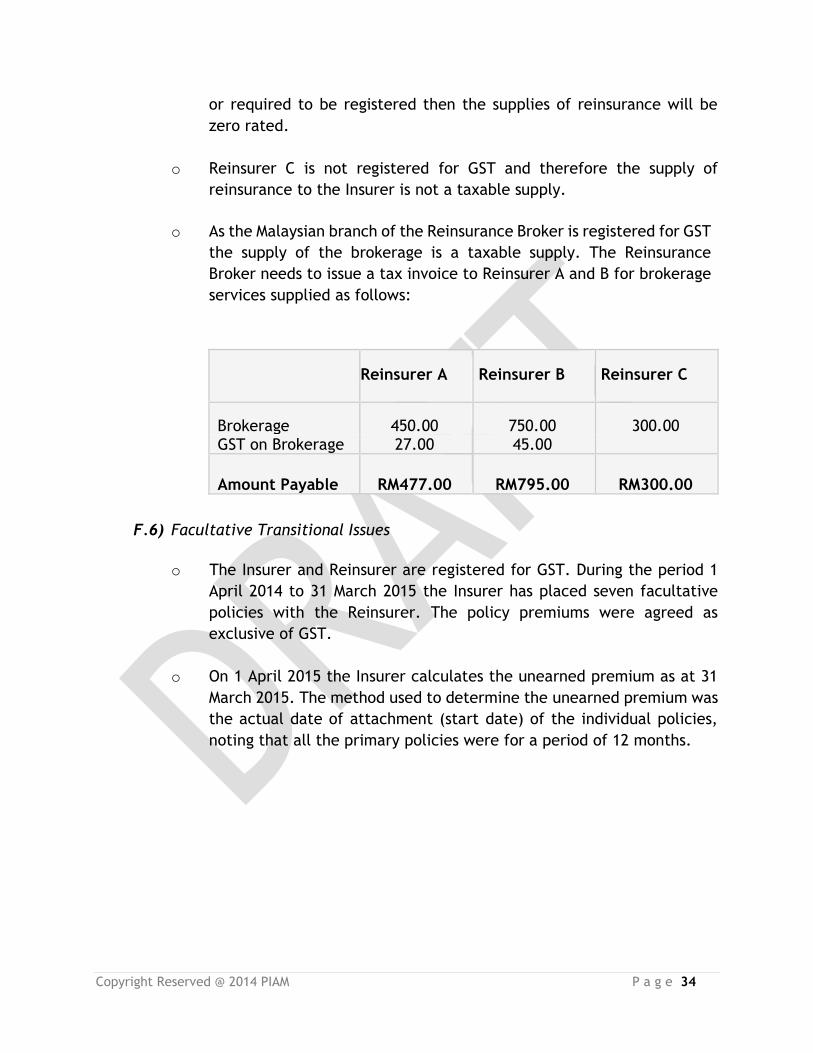

o If the recipient of the supplies is a non-resident Insurer who is not in

Malaysia when the insurance policies are created and is not registered

Copyright Reserved @ 2014 PIAM P a g e 34

or required to be registered then the supplies of reinsurance will be

zero rated.

o Reinsurer C is not registered for GST and therefore the supply of

reinsurance to the Insurer is not a taxable supply.

o As the Malaysian branch of the Reinsurance Broker is registered for GST

the supply of the brokerage is a taxable supply. The Reinsurance

Broker needs to issue a tax invoice to Reinsurer A and B for brokerage

services supplied as follows:

Reinsurer A Reinsurer B Reinsurer C

Brokerage 450.00 750.00 300.00 GST on Brokerage 27.00 45.00

Amount Payable RM477.00 RM795.00 RM300.00

F.6) Facultative Transitional Issues

o The Insurer and Reinsurer are registered for GST. During the period 1

April 2014 to 31 March 2015 the Insurer has placed seven facultative

policies with the Reinsurer. The policy premiums were agreed as

exclusive of GST.

o On 1 April 2015 the Insurer calculates the unearned premium as at 31

March 2015. The method used to determine the unearned premium was

the actual date of attachment (start date) of the individual policies,

noting that all the primary policies were for a period of 12 months.

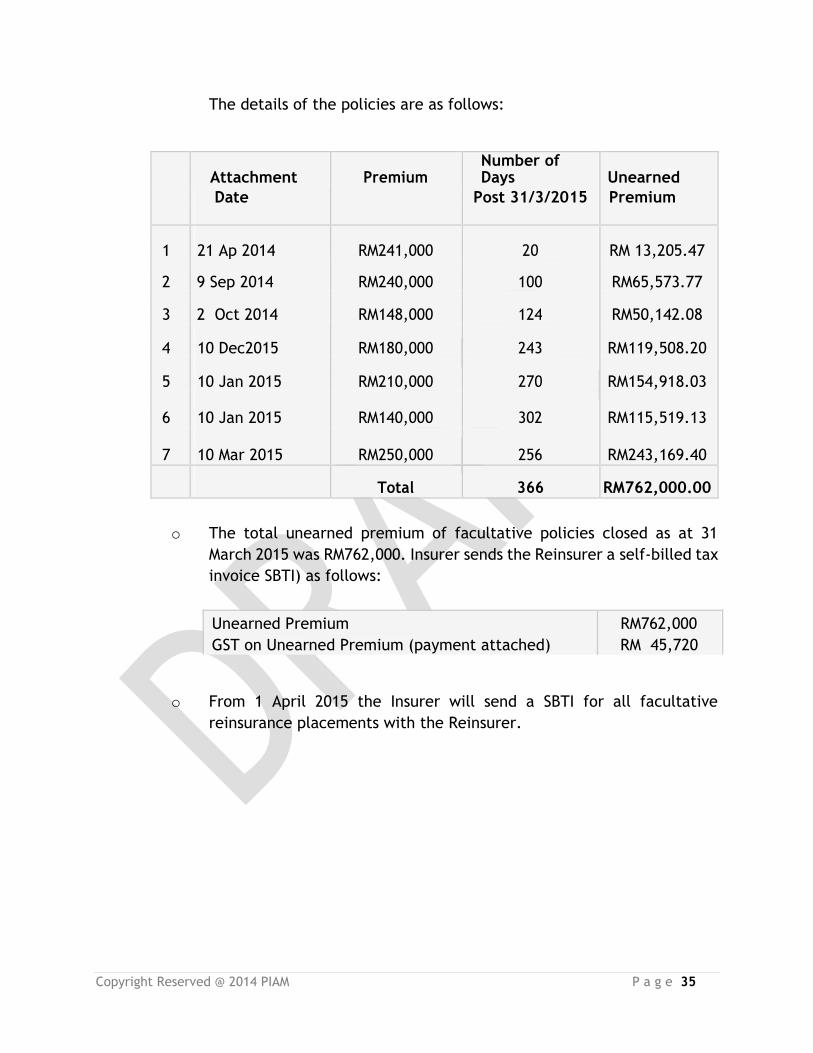

Copyright Reserved @ 2014 PIAM P a g e 35

The details of the policies are as follows:

Attachment Premium Number of Days Unearned

Date Post 31/3/2015 Premium

1 21 21 Ap 2014 RM241,000 20 RM 13,205.47

2 9 Sep 2014 RM240,000 100 RM65,573.77

3 2 Oct 2014 RM148,000 124 RM50,142.08

4 29 10 Dec2015 RM180,000 243 RM119,508.20

5 27 10 Jan 2015 RM210,000 270 RM154,918.03

6 28 10 Jan 2015 RM140,000 302 RM115,519.13

7 21 10 Mar 2015 RM250,000 256 RM243,169.40

Total 366 RM762,000.00

o The total unearned premium of facultative policies closed as at 31

March 2015 was RM762,000. Insurer sends the Reinsurer a self-billed tax

invoice SBTI) as follows:

Unearned Premium RM762,000

GST on Unearned Premium (payment attached) RM 45,720

o From 1 April 2015 the Insurer will send a SBTI for all facultative

reinsurance placements with the Reinsurer.

Copyright Reserved @ 2014 PIAM P a g e 36

G. Treaty Business Example

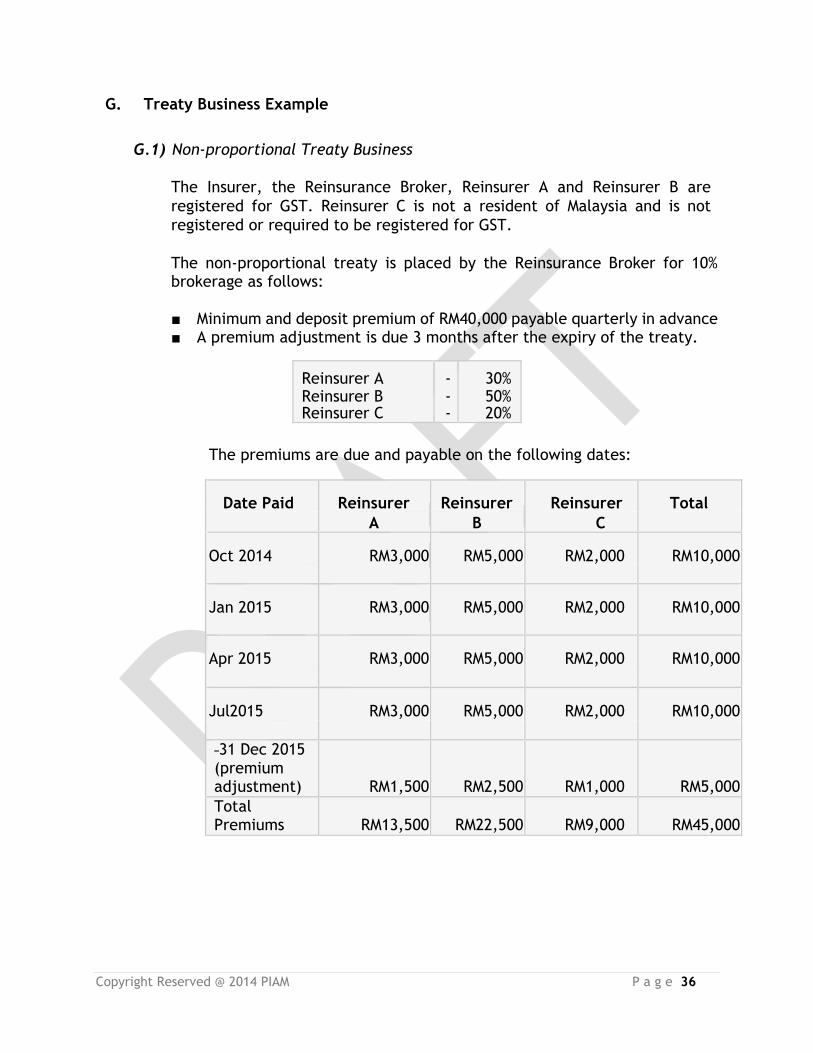

G.1) Non-proportional Treaty Business

The Insurer, the Reinsurance Broker, Reinsurer A and Reinsurer B are

registered for GST. Reinsurer C is not a resident of Malaysia and is not

registered or required to be registered for GST.

The non-proportional treaty is placed by the Reinsurance Broker for 10% brokerage as follows:

■ Minimum and deposit premium of RM40,000 payable quarterly in advance ■ A premium adjustment is due 3 months after the expiry of the treaty.

Reinsurer A - 30% Reinsurer B - 50% Reinsurer C - 20%

The premiums are due and payable on the following dates:

Date Paid Reinsurer Reinsurer Reinsurer Total

A B C

1 Oct 2014 RM3,000 RM5,000 RM2,000 RM10,000

1 Jan 2015 RM3,000 RM5,000 RM2,000 RM10,000

1 Apr 2015 RM3,000 RM5,000 RM2,000 RM10,000

1 Jul2015 RM3,000 RM5,000 RM2,000 RM10,000

31 Dec 2015 (premium adjustment) RM1,500 RM2,500 RM1,000 RM5,000

Total Premiums RM13,500 RM22,500 RM9,000 RM45,000

Copyright Reserved @ 2014 PIAM P a g e 37

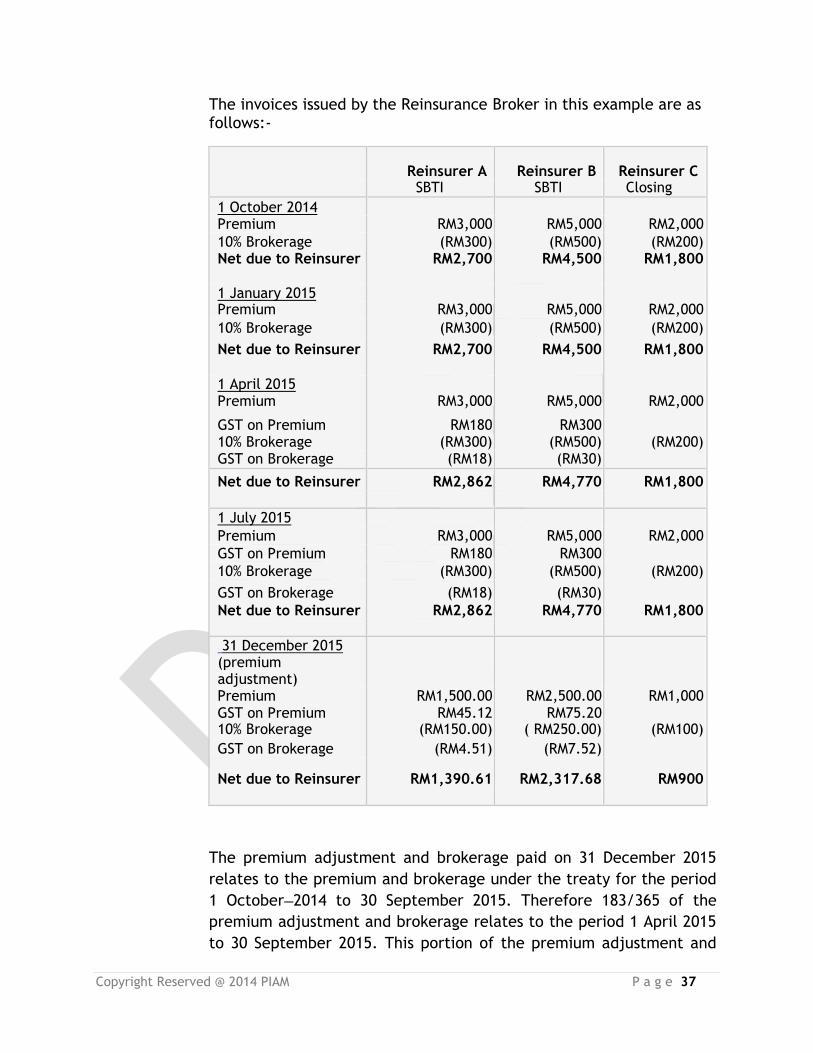

The invoices issued by the Reinsurance Broker in this example are as follows:-

Reinsurer A Reinsurer B Reinsurer C SBTI SBTI Closing

1 October 2014

Premium RM3,000 RM5,000 RM2,000

10% Brokerage (RM300) (RM500) (RM200) Net due to Reinsurer RM2,700 RM4,500 RM1,800

1 January 2015 Premium RM3,000 RM5,000 RM2,000

10% Brokerage (RM300) (RM500) (RM200)

Net due to Reinsurer RM2,700 RM4,500 RM1,800

1 April 2015 Premium RM3,000 RM5,000 RM2,000

GST on Premium RM180 RM300 10% Brokerage (RM300) (RM500) (RM200) GST on Brokerage (RM18) (RM30)

Net due to Reinsurer RM2,862 RM4,770 RM1,800

1 July 2015

Premium RM3,000 RM5,000 RM2,000

GST on Premium RM180 RM300

10% Brokerage (RM300) (RM500) (RM200)

GST on Brokerage (RM18) (RM30)

Net due to Reinsurer RM2,862 RM4,770 RM1,800

31 December 2015 (premium adjustment)

Premium RM1,500.00 RM2,500.00 RM1,000 GST on Premium RM45.12 RM75.20 10% Brokerage (RM150.00) ( RM250.00) (RM100)

GST on Brokerage (RM4.51) (RM7.52)

Net due to Reinsurer RM1,390.61 RM2,317.68 RM900

The premium adjustment and brokerage paid on 31 December 2015

relates to the premium and brokerage under the treaty for the period

1 October 2014 to 30 September 2015. Therefore 183/365 of the

premium adjustment and brokerage relates to the period 1 April 2015

to 30 September 2015. This portion of the premium adjustment and

Copyright Reserved @ 2014 PIAM P a g e 38

brokerage is subject to GST as it relates to the supply of reinsurance

made after 31 March 2015.

Note that in this example it is assumed that the brokerage, is

consideration for a supply for a period.

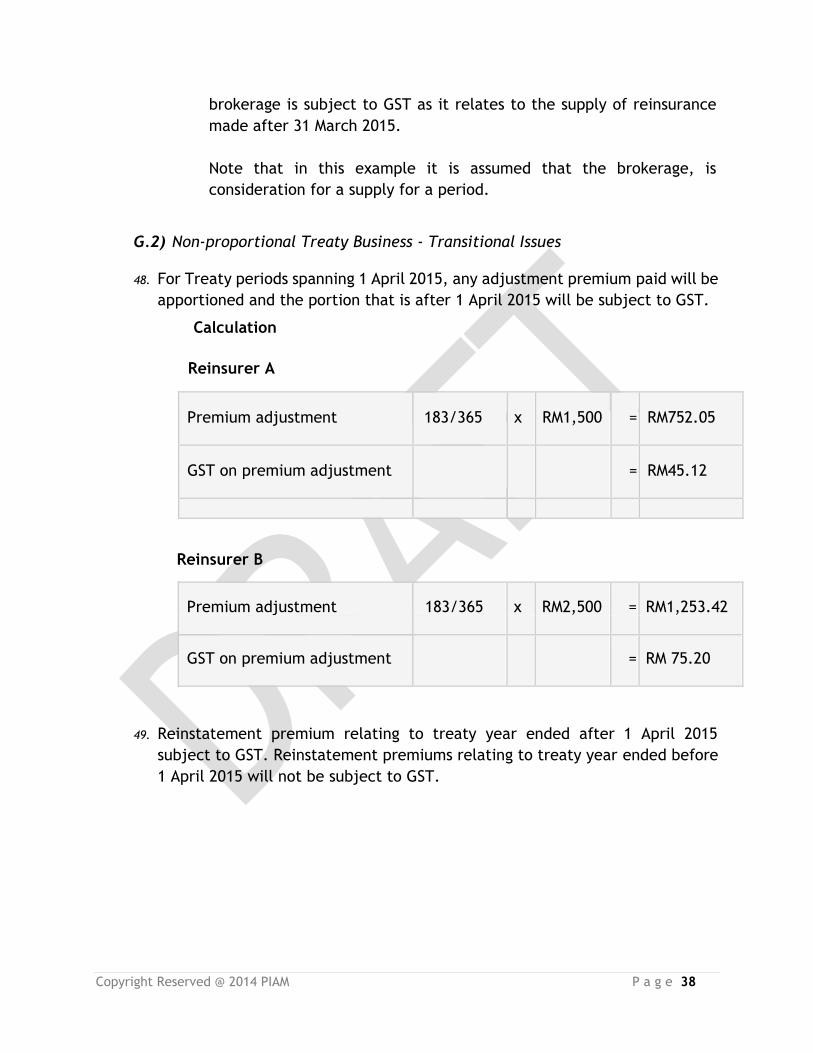

G.2) Non-proportional Treaty Business - Transitional Issues 48. For Treaty periods spanning 1 April 2015, any adjustment premium paid will be

apportioned and the portion that is after 1 April 2015 will be subject to GST.

Calculation

Reinsurer A

Premium adjustment 183/365 x RM1,500 = RM752.05

GST on premium adjustment = RM45.12

Reinsurer B

49. Reinstatement premium relating to treaty year ended after 1 April 2015

subject to GST. Reinstatement premiums relating to treaty year ended before

1 April 2015 will not be subject to GST.

Premium adjustment 183/365 x RM2,500 = RM1,253.42

GST on premium adjustment = RM 75.20

Copyright Reserved @ 2014 PIAM P a g e 39

G.3) Proportional Treaty Business

(i) The Insurer and Reinsurer A and Reinsurer B are registered for GST.

Reinsurer C is not a resident of Malaysia and is not registered or required

to be registered for GST. The Reinsurance Broker is registered for GST.

(ii) The Insurer places a continuous property proportional reinsurance cover

commencing 1 October 2014 through the Reinsurance Broker as follows:

Reinsurer A - 30%

Reinsurer B - 50%

Reinsurer C - 20%

(iii) The Reinsurance Broker receives 1% brokerage from the Reinsurers deducted quarterly from the premium due to the Reinsurers. The Insurer receives a 20% commission from the Reinsurers paid quarterly by the Reinsurer. The Reinsurance Broker has prepared the quarterly accounts on behalf

of the Insurer and will forward these accounts to the Reinsurer.

In this example the details of the Reinsurance Broker's accounts are:

Oct - Dec Jan -Mar Apr - June July - Sep

Qtr Qtr Qtr Qtr

Reinsurance RM10,000 RM20,000 RM30,000 RM40,000

Premiums

written

Commission (RM2,000) (RM4,000) (RM6,000) (RM8,000)

Brokerage (RM100) (RM200) (RM300) (RM400)

Claims Paid (RM1,000) (RM1,000) (RM1,500) (RM1,600)

Net Cash Paid RM6,900 RM14,800 RM22,200 RM30,000

Copyright Reserved @ 2014 PIAM P a g e 40

50. The invoices issued by the Reinsurance Broker to the Reinsurers in this example

are as follows:-

Reinsurer A Reinsurer B Reinsurer C SBI SBI Closing

October-December Quarter Premium RM3,000 RM5,000 RM2,000 Commission (RM600) (RM1,000) (RM400) 1% Brokerage (RM30) (RM50) (RM20)

Claims paid (RM300) (RM500) (RM200) Net due to Reinsurer RM2,070 RM3,450 RM1,380

Jan- Mar Quarter

Premium RM6,000 RM10,000 RM4,000 Commission (RM1,200) (RM2,000) (RM800) 1% Brokerage (RM60) (RM100) (RM40) Claims Paid (RM300) (RM500) (RM200)

Net due to Reinsurer RM4,440 RM7,400 RM2,960

Apr-June Quarter

Premium RM9,000 RM15,000 RM6,000 GST on Premium RM540 RM900 Commission (RM1,800) (RM3,000) (RM1,200) GST on Commission (RM108) (RM180) 1% Brokerage (RM90) (RM150) (RM60) GST on Brokerage (RM5.40) (RM9) Claims Paid (RM450) (RM750) (RM300)

Net due to Reinsurer RM7,086.60 RM11,811.00 RM4,440

July-Sep Quarter Premium RM12,000 RM20,000 RM8,000 GST on Premium RM720 RM1,200 Commission (RM2,400) (RM4,000) (RM1,600) GST on Commission (RM144) (RM240) 1% Brokerage (RM120) (RM200) (RM80) GST on Brokerage (RM7.20) (RM12) Claims Paid (RM480) (RM800) (RM320)

Net due to Reinsurer RM9,568.80 RM15,948.00 RM6,000

Copyright Reserved @ 2014 PIAM P a g e 41

G.4) Proportional Treaty Business - Transitional Issues 51. The Reinsurance policy is treated as a separate supply from the underlying

contracts. The time of supply for the proportional treaty will be based on

settlement date of the treaty technical statement. Hence any technical

statement rendered prior to 1 April 2014 will not have GST. Any technical

statement rendered after 1 April 2014 will include GST on the premium and

commission regardless of when the contracts incepted would be subject to GST.

G.5) Claim Payments

52. It is common for insurers and takaful operators to purchase reinsurance or

retakaful contracts. If a claim is made against the insurer or takaful operator,

he will recover his losses by making a claim against the reinsurer or

retakaful operator under the reinsurance or retakaful contract. As such

claims are made under a separate contract of reinsurance or retakaful for

which the insurer or takaful operator is now an policyholder or participant,

it will not be treated as a recovery of cash payment. Therefore, the

insurer or takaful operator need not reduce its input tax claims if he receives

any cash payment under a separate reinsurance or retakaful contract.

53. Hence claim settlements by reinsurers will be considered out of scope. Any

GST incurred by the cedants when settling claims that can be claimed as input

tax will be recovered by the cedant and no GST will be passed to reinsurer.

54. Any deemed input taxes received by the cedant for cash payments that were

recovered from reinsurers should be shared proportionately as a claim recovery

with the reinsurer.

55. Input tax on GST incurred on adjuster fees, lawyer fees etc. paid directly by

the reinsurer will be recovered by the reinsurer. If the reinsurer had incurred

the fees on behalf of a panel of fellow reinsurers, then the fees should be

recovered as reimbursement from the remaining reinsurers. The

reimbursement will attract an output tax. The remaining panel will then claim

the input tax on their respective reimbursement.

Copyright Reserved @ 2014 PIAM P a g e 42

SECTION 4

CLAIMS SETTLEMENT

Copyright Reserved @ 2014 PIAM P a g e 43

SECTION 4 CLAIMS SETTLEMENT

A. GST implications on Claims Settlement

56. Generally, where an insurer acquires the goods or services directly from the

supplier/contractor/repairer for the supply of the goods/services to the

policyholder or third party as an insurance settlement pursuant to its obligation

under the insurance policy, the said insurer would be entitled to claim the GST

as Input Tax Credit (ITC), provided that a valid GST tax invoice is issued to the

said insurer by the supplier/contractor/repairer. An example would be a

direct billing in respect of an Own Damage claim by an authorized repairer.

57. Where the contract is with a service provider to provide services for example

surveyors, adjustors, lawyers, investigators and other experts in the course of

processing an insurance claim, any GST incurred by the insurer would be

entitled to input tax credit.

58. The cash payment by the insurers in respect of an insurance settlement claim

does not represent a supply by the insurer nor does it represent consideration

for a supply made by the policyholder. Hence, indemnity payments or

settlements are not subject to GST. However, the insurer is entitled to a credit

of input tax deemed incurred known as “deemed input tax credit” (DITC).

59. An insurer will be entitled to claim Deemed input tax credit if ALL of the

following conditions are met:-

Conditions for DITC

(a) the payment is made pursuant to a standard rated insurance policy (i.e. 6%

GST is charged on the premium for the policy):-

The cash payment must be made pursuant to an insurance policy upon

the occurrence of an insured event

Cash payment made pursuant to zero rated policies (for an example;

international travel insurance, outbound marine, aviation, hull &

cargo) would not be entitled to DITC

Copyright Reserved @ 2014 PIAM P a g e 44

Cash payment made pursuant to policy issued pre-GST period of which

no GST is chargeable would not be entitled to DITC (although the

insured event occurred post GST period)

The payment can be made to any person including the policyholder,

third party, claimant, or beneficiary.

(b) The Cash Payment is made pursuant to an insurance policy issued to a

(i) Not GST registered

Condition (b) is satisfied if the policyholder is not GST registered at the

effective date of the insurance policy. This effective date is the

inception date of the insurance policy. For renewal cases, it refers to

the inception date of the renewal policy.

The registration status of the policyholder may be obtained at the GST

Portal maintained by the Royal Malaysian Customs.

(ii) GST Registered

GST registered but the claim of input tax on the insurance premium is

disallowed (i.e. blocked input tax credit such as Medical and Personal

Accident insurance)

(c) GST-registered sole-proprietor who buys insurance policies in his own

capacity, there is a need to ascertain that the insurance policy is for a GST-

registered policyholder’s personal use and is not related to any business

carried on by him.

(d) Where the insurance coverage begins on or after 1 April 2015. Hence, the

commencement date of the insurance cover or insurance policy has to be on

or after 1 April 2015.

It is also important to note that ZERO Rated Policies do not qualify for

deemed input tax credit claim.

Copyright Reserved @ 2014 PIAM P a g e 45

Conditions to Claims DITC or Input Tax

Copyright Reserved @ 2014 PIAM P a g e 46

B. Computation of deemed input tax credit

60. To determine the amount of deemed input tax credit, the insurer must apply

the tax fraction to the amount of cash payment made by the insurer in

accordance to the formula given below.

Deemed input tax credit = GST rate X cash payment

100% + GST rate

61. In the case where the policyholder takes up a motor third party cover, where

the insurer makes a cash payment in settlement of a claim by the third party,

the insurer’s entitlement to DITC would still depend on the GST registration

status of the policyholder and not the recipient (third party) of the cash

payment.

62. All insurers are allowed to claim for deemed input tax credit (DITC) if there is

a court order for insurers to pay a claim to a TP directly or into the account of

the TP’s lawyer. If the settlement with the TP is not registered in the court,

but through a Discharge Voucher or a Settlement letter, insurers are similarly

entitled to claim for the DITC. Insurers are also entitled to claim for the DITC

for the party to party costs payable to the TP’s lawyer

63. Insurers are also entitled to claim for the DITC if the settlement involved a

foreign claimant following an accident in the foreign country, e.g. Singapore

or Brunei. Subject always to all the basic conditions of the DITC being met,

namely the policyholder is not a registered person on the policy’s effective

date, the policy is standard rated and the supporting documents are

maintained.

64. For settlement of claims where the repairer bills the insured and cash payment

is made by the insured to the repairer, who will then submit the bill for

reimbursement from the insurer, in this instance the insurer is not allowed to

claim input tax on the amount of repairs reimbursed to the claimant (but

allowed to claim Deemed Input Tax Credit (DITC) provided all the DITC

conditions are met.) However, if the repairer bills the insurer directly for the

repairs, the insurer should then claim input tax credit (ITC) instead.

65. Insurer is advised to check on the latest GST registration status of the Insured

in every claim - in the event of an insured not being a registered person at the

effective date of the policy but subsequently registered before the loss date

Copyright Reserved @ 2014 PIAM P a g e 47

(which is after 1/4/2015) – they will be entitled to claim ITC (if satisfied all

conditions of ITC) on bills issued to them by repairer after 1/4/2015. When

this happens, insurer may exclude GST element charged to the insured by his

repairer (and insurer subsequently file DITC on amount net of GST)

C. Reverse Charging GST on foreign services engaged:

66. Where the service provider is based outside Malaysia, the expense will be

subject to "imported services" rule. Imported services is defined as any

services provided by a foreign service provider and which is consumed in

Malaysia. "Consumed in Malaysia" is determined by the place where the supply

of services are provided. In situations where payment relates to services

consumed outside Malaysia, imported services rule would not apply. Examples

of no reverse-charging of GST on foreign services engaged are when insurers

engaged a Singapore based adjuster to assess the repairs cost to a collision-

damage vehicle in Singapore, approved repair of a vehicle in Singapore, or

engage a Singapore based lawyer to defend a liability claim in a Singapore

court.

67. An insurer is required to self-account for output tax of 6% on the value of an

invoice issued by the foreign service provider. This is referred to as the "reverse

charge mechanism". Please take note that the reverse charge mechanism

would only be applicable if the services would have been subject to GST if

supplied by a Malaysian service provider.

D. Reimbursement under KFK Agreement:

68. In the settlement of a TP’s claim where the KFK Agreement is applicable, the

Handling insurer will claim for the DITC (subject to all the DITC conditions

being met) and recover the reimbursable items net of DITC from the Claimant’s

insurer. Claimant’s insurer is NOT allowed to claim for DITC for the payment

made.

Copyright Reserved @ 2014 PIAM P a g e 48

Please see below diagram for illustration:

E. Disposal of vehicles :

E.1) Disposal of vehicles as wrecks:

69. In the event a wreck is disposed to a successful bidder, insurers are required

to charge output tax and issue a Tax invoice within 21 days from the time of

supply.

70. The time of supply under Para 69 (h) of the GST Guide on Supply (dated 7 May

2013) states that if the supplier supplies goods under an agreement where

ownership will only pass at the date of appropriation by the recipient and the

consideration will not be fixed until that date then, the time of supply is the

earliest of the following dates:-

(a) the date when the recipient appropriates the goods, or

(b) the date when a tax invoice is issued by the supplier, or

(c) the date when a payment is received by the supplier.

Copyright Reserved @ 2014 PIAM P a g e 49

In the case of the sale of a vehicle as a wreck, the time of supply will be on

the earliest of the following dates:

(a) the date insurers pass the Ownership transfer documents to the bidder, or

(b)the date when insurers issue the Tax invoice, or

(c) the date when the bidder pays the insurers for the wreck.

E.2) Disposal of vehicles as scraps:

71. Disposal of vehicles as scraps where no Ownership transfer documents will be

passed on to the bidder. Insurers would have to issue a Tax invoice within

21days from the sale.

72. Input tax credit is claimable for any expenses incurred (e.g. storage charges

etc.) in relation to disposal of the damaged property provided there is a tax

invoice issued to support the claim.

73. There will also be rare situations where the sales of wreck/recovered property

occurs outside Malaysia due to the occurrence of the loss/accident which is

outside Malaysia and the recovery is made outside Malaysia, in such situations

it would not be economical to bring the recovered item back to Malaysia for

disposal. As the supply is made outside Malaysia, it will be considered as Out

of Scope and no GST will be chargeable. In this instance, no tax invoices are

required.

74. In the case where an insurer settles a loss by repairing or replacing the property,

the insurer will pay GST only if the repair services or replacement of property

is subject to GST. In this instance, the insurer is allowed to claim the input

tax incurred.

F. Cash Payment Involving Hire Purchase Agreement:

75. In the event of a theft of a vehicle, the insurer will pay the sum insured or the

market value of the vehicle at the time of loss excluding the excess clause.

76. However, in the event that the property/vehicle insured is still under a hire

purchase agreement, the insurer may decide to settle the outstanding loan

with the financier and make a cash payment of the balance amount to the

policyholder or the property/vehicle owner insured under the policy. The

Copyright Reserved @ 2014 PIAM P a g e 50

insurer is allowed to claim deemed input tax credit on the total payout to the

financier and the policyholder. Deemed input tax credit is allowed only on the

actual amount of cash payment made by the insurer.

G. Cash Payment

G.1) Cash Payment involving Ex Gratia settlement

77. An ex gratia payment is made where a claim does not meet the terms and

conditions of the insurance contract but the insurer chooses to make a

voluntary payment out of goodwill, kindness or compassion, without

recognizing any obligation to make such a payment. In view of this being a non-

obligatory settlement, insurer will not be entitled to DITC claim.

G.2) Cash Payment involving Performance Bond

78. Insurers normally require contractors to provide "cash collateral" to guarantee

the performance of their contractual obligations under the contract with the

principal. In the event of default by the contractor, the principal is entitled

to call upon the amount of collateral (bond) from the said insurer and, the

insurer is obliged to pay the amount under the Bond agreement. Unlike an

insurance settlement, there is no Deemed Input Tax credit available when

insurer make a cash payment on a Performance Bond as this is not a contract

of insurance.

79. Where the contractor has performed and completed their obligation

accordingly, the cash collateral will be refunded by the insurer to the

contractors, together with a certain proportion of the interest earned. The

cash collateral collected from contractors serves as a security deposit and is

not considered received for any supply made by the insurer as such will not be

subject to GST. The deposit of the cash collateral in financial institutions of

which the insurer earns interest, is a supply of financial services which is

exempt supply. The payment of interest by the insurer to the contractors

reflects a financial supply made by the contractor to the insurer and is an

exempt supply in the account of the contractors.

G.3) Cash Payments involving Hospital and Surgical (H & S) claims

80. H & S policies can be arranged either on Reimbursement basis (customers pay

and file claim later) or Cashless. In the case of Cashless Plans, an insurer

Copyright Reserved @ 2014 PIAM P a g e 51

usually appoints a Third Party Administrator (TPA) to administer the hospital

admissions, follow up and billings.

H. Reimbursements:

81. These are recoveries of hospital charges and expenses incurred by the TPA in

the course of providing their services to an insurer. GST should be charged on

those charges and expenses upon invoicing the insurer.

82. The GST incurred by the insurer is claimable as input tax credit.

I. Disbursements:

83. These are costs and expenses paid by the TPA on behalf of insurers. These

charges and expenses are the liability of the insurer and relate to a supply by

the hospital to the insurer (and not to the TPA). For disbursement

arrangements, any GST charged by the hospitals (only if there is on exceptional

items) cannot be claimed by the TPA as input tax credit. This is because the

services are supplied by the hospital to the insurer (and not to the TPA).

84. When an invoice is issued by the TPA to the insurer, it should separately

identify which expenses are "reimbursement" and which are "disbursement" and

correctly identify the GST treatment on the invoice.

The contractual terms between the hospital, the TPA and the insurer will show

whether the related charges/recovery of expenses are categorized as

"reimbursement" or "disbursement" accordingly. Establishing the position as

the "principal" or "agent" is important.

85. When the TPA is merely acting as the ‘payment agent’, the recovery of the

expenses is termed a ‘Disbursement’. The recovery of expenses does not

constitute a supply made by the ‘agent’ and hence will not be subject to GST.

This treatment applies where the ‘agent’:-

(a) has helped arrange for the supply of services and paid the hospital charges

on behalf of the insurer and is not a party to the contract between the

hospital and the insurer; and

(b) subsequently passes on the related costs to the insurer without a mark-up

where the cost qualify as strict pass-through cost.

Copyright Reserved @ 2014 PIAM P a g e 52

The ‘agent’ (in this case the TPA) may issue their invoice to the insurer to

recover the hospital charges and it is not subject to GST. The insurer may

claim input tax credit for the supply of TPA services based on the arrangements

between them and the TPA. The TPA, on the other hand is not entitled to any

input tax claim since the services are not supplied by the agent but by the

hospitals.

J. Recovery

J.1) Excess

86. All claims payment made to the policyholder, repairer or third party claimant

is net of the excess amount as stipulated in the Excess Clause. The excess

amount is exclusive of GST. In this respect, the policyholder will settle the

claim amount not covered by the insurer with the repairer or the third party

claimant. Hence, the insurer is making cash payment indemnifying the

policyholder according to the insurance contract. Deemed input tax credit is

allowed only on the actual amount of cash payment made by the insurer.

87. For various scenarios involving GST application on Excess, kindly refer to the

Guide on Insurance and Takaful business (dated 22 Oct 2014) under the heading

of Cash Payment Involving Excess Clause.

J.2) Subrogation

88. Upon receipt of subrogation recovery and if the insurer has claimed deemed

input tax, the insurer should reduce their deemed input tax claims since they

did not bear part or whole of the cash claim payment. The adjustment should

be made in the period in which the recovery was received and the value to

adjust is the relevant tax fraction of that amount of recovery received. The

time of the adjustment must be the tax period in which the recovery was

received by the insurer. The value of the adjustment is the proportion of

recovery received (deemed input tax recovered).

J.3) Uncovered Charges

89. Uncovered charges involving Cashless Hospital and Surgical claims (where

insurer fronts on full guarantee and seeks recovery thereafter). Upon settling

the full charges to the hospital or third party administrator, the insurer will

Copyright Reserved @ 2014 PIAM P a g e 53

proceed to seek recovery from the policyholder/insured person. As this does

not involve supply of goods or services, an insurer is not required to charge

Output Tax hence Tax Invoice is not required.

Collection can be done via Debit Note?

90. In ALL of the above recoveries, the insurer should reduce their Deemed Input

Tax Credit claims accordingly. The adjustment should be made in the period

in which the recovery was received and the value to adjust is the relevant tax

fraction of that amount of recovery received.

J.4) Reinsurance / Coinsurance Claims Recoveries

91. If a claim is made against an insurer, the cedant/co-leader will recover its

losses from the panel reinsurers/co-followers (or both) for their share of the

loss. It is deemed that such claims are made under a separate contract of

reinsurance which the insurer is now a policyholder. Should the following co-

follower decides to settle their share of the loss directly to the Insured and the

service provider, their position on ITC and DITC will be similar to that of the

lead insurer for the amount they settle.

92. Reinsurers/co-followers are not entitled to Deemed Input Tax Credit if they

pay the claims to the cedant/co-leader. In the event a reinsurer decides to pay

its portion of a claim directly to the claimant, the reinsurer will also not be

entitled to Deemed Input Tax claim.

93. The various scenarios are presented below for a better understanding of the

members

(i) Personal Accident claim involving unregistered insured person:-

o Death benefit settlement for RM100,000 payout

o Cedant claims DITC for RM5660 (6/106 X RM100,000)

o Hence recovery from Reinsurer A with 20% share will be 20% of

RM100,000 Less RM5,660 = RM18,868 (instead of RM20,000)

Comment:-

Claims Task force seeks confirmation from PIAM WG and PIAM GST consultant to

verify the above and examples below i.e. if they are correct-

Copyright Reserved @ 2014 PIAM P a g e 54

(ii) Cash settlement to insured

o Example repair cost is RM100,000 + GST 6% = RM106,000

o Assuming insurer effects settlement to Insured for RM106,000

and claims DITC of RM6000 (6/106 X RM106,000)

o Recovery from Reinsurer A will be 20% of RM106,000 Less DITC

RM6,000) = RM20,000 instead of RM21,200

(iii) Settlement to repairer (registered person)

o Example repair cost is RM100,000 + GST 6% = RM106,000

o Repairer issues tax invoice to insurer and upon collecting the