goods and services tax (gst) july 1, 2017 rollout...

TRANSCRIPT

Goods and Services Tax (GST)

July 1, 2017 – Rollout target meeting reality

May 24, 2017

The conclusion of the fourteenth Goods and Services Tax (GST) Council meet paved the way for the

most awaited reform to get closer to reality with rates of most products being finalised. All products

and services will be taxed at either 5%, 12% 18% or 28%. Approximately 19% goods are being taxed

at 28%, 43% goods fall in the 18% slab, 17% will attract 12% rate while last 14% are in the 5% slab

and balance 7% are out of GST. All services will be taxed at 18% vs. the current rate of 15% while

about 40% of the CPI basket is exempt from GST. The decision on GST rates depicts the government’s

strong intention to roll out GST by July 1, 2017 as stated. We believe it will be a big boost for

corporates as it will bring a level playing field vis-à-vis the unorganised industry by reducing the

possibility of tax evasion. It should add significant revenues to the government’s kitty with an expected

widening of the tax base.

2

Impact on inflation, negated; anti–profiteering clause shines

Given that 81% of items are to be taxed below the 18% standard rate, we believe implementation of

GST is not expected to be inflationary in nature. Items whose rates have not been decided by the

council so far are gold, textile, agricultural implements, bidis, footwear and bio-diesel.

Impact on sectors

FMCG and consumer durables being the largest beneficiary, other key sectors to benefit include,

tourism, aviation, DTH cable, lubricants, laminates under building materials.

A negative impact is seen on sectors like luxury hotels, theme parks, luggage, breweries and

distilleries, upstream and downstream oil sector.

Majority of large sectors like auto, cement, banking, agri chemicals, power and pharma are expected to

witness a neutral impact.

3

Impact on inflation negated; anti–profiteering clause shines

•Input tax credit remains one of the major advantage under GST. However, practical implementation of

input tax credit refunds and its eligibility and dispute handling will be a big task. Anti-profiteering

clause warrants companies to pass on the tax cuts and gains from input tax credit to consumers in the

form of lower prices. Hence, if tax cuts are passed on along with success of input tax credit, various

goods may see lower prices and GST may also turn inflation friendly.

•The Union government has allowed multiple rates to enable the GST Council to juggle around items to

bring them under slabs that would help rein in inflation. Along with this, the provision on penal action

against businesses and traders indulging in profiteering, in the wake of the GST rollout, the Union

government’s primary focus has become clearer. The government wants to roll out a tax reform like

the GST but not at the cost of inflation.

•It has been observed that GST rates have been tweaked to encourage investments in the economy.

Items in the capital goods sector have been placed under the 18% duty slab, which essentially means

10% lower than the existing rate of~28%. This, along with the duty setoff that the manufacturers can

claim on taxes they pay on raw materials and components, would result in a substantial benefit.

•Goods and services like petrochemicals, healthcare, education and housing are either not included or

exist at 0% in GST with a possibility of being taxed in future. Alcohol is fully excluded under GST.

•We have sectorally analysed the impact. Certain stocks have already started reacting to the newsflow

however, the real impact can only be gauged post implementation as to how the mechanism works

and tax credits are received. Further pass on of lower tax will be key and has to be monitored. This will

entail use of huge work force by the government. Largely, corporates are positive on GST and are

ready for implementation. However, the IT infrastructure and other operational hurdles may marginally

impact the process.

4

Key benefits expected to pan out on GST implementation

•To provide enabling environment for businesses - “Make in India by making

one India”: Ease of doing Business

•Unorganised segment set to come under tax net

•Goods transportation set to become more efficient, cheaper

•To promote efficiency by providing buoyancy to tax base

•To enable improvement in India’s tax to GDP ratio

Sectoral Impact

Sector Segment/ Products Tax rate li

GST Rate View Positive/ Negative Stocks impactedearlier

FMCG

Toothpaste, Hair Oil Soaps 23 24% 18%

With the reduction in indirect tax incidence, the company is requiredto pass on the benefit due to the anti-profiteering clause. However, webelieve a price reduction is likely to result in an increase in consumerdemand, which, in turn, would result in a positive impact on volumegro th Positi e

Colagte, HUL, Dabur, Marico,ITC

Oil, Soaps 23-24% 18% growth Positive

Detergent 23-24% 28%

Indirect tax incidence has increased to 28% against the industryexpectation of 18%. Companies are required to increase prices to passon the increase in taxes Negative

HUL, Jyothy Lab

Edible Oil 3-9% 5%

Tax incidence on edible oil has remained neutral for companies.However, keeping coconut oil in the definition of edible oil has been arelief for Marico Positive

Marico

Edible Oil 3-9% 5% relief for Marico Positive

Consumer Discretionary

Paints 24%-27% 28%GST rate for paint/varnishes have been kept at 28%, which isapproximately similar to the previous tax slab Positive

Asian Paints, Kansai Nerolac

LED

-Lamps 15% 12%To promote the use of efficient lighting products, the GST rate on LEDhas been kept at 12% Positive

Havells India, BajajElectricalsLamps 15% 12% has been kept at 12% Positive Electricals

-Fixtures 22% 12%

Air cooler 26% 18%

The air cooler category has been kept under the 18% bracket, whichwill benefit organised players in terms of a shift in demand fromunorganised categories (still 75% unorganised) Positive

Symphony, Bajaj Electricals

Air conditioner 26% 28%As expected GST rate for Air conditioner have been subsumed in the28% (nearest slab) Neutral

Voltas, Havells( )

Wires & Cables/Switches 18% 28%

Higher tax slab for wire & cable and switches would see an increase in prices of products as companies are likely to pass on to endcustomers Neutral

V-Guard, Havells India

PVC

GST rates for PVC pipes and furniture categories have been subsumedin the nearest tax bracket of 18% and 28%, respectively. We believethis would lead to a shift in demand from unorganised players to the

Supreme Industries,Wimplast, Prima Plastic

5

Source: cbec.gov.in, ICICIdirect.com Research

pipes/Furniture 18%/28 18%/28% organised industry Positive

6

Source: cbec.gov.in, ICICIdirect.com Research

Sector Segment/ Products Tax rate

earlier

GST Rate View Positive/ Negative Stocks impacted

Financials

Banks

15% (including

Swachh

Bharat Cess) 18%

Fee based services will get expensive for customers to the extent of

variation in GST over current service tax rate. No material impact

seen on banks Neutral

Insurance

15% (including

Swachh

Bharat Cess) 18%

Premium will increase for insurance policies - both life and non-life.

Modalities in terms of taxation on life insurance policies needs to be

seen Neutral

Multiplex

Entertainment 27% on ATP 28% on ATP

On ticketing revenues, companies were expecting the tax rate to be in

the range of 18%. The current rate, though higher than expectations, is

neutral from the current scenario of 27%. On the F&B side, though

rates are higher than the F&B VAT rate of 12.5%, the company will be

able to avail input tax credit paid on the raw materials leading to

benefits to the tune of 100-150 bps (against initial expectation of 250-

300 bps expansion) Neutral

PVR, Inox Leisure

F&B 13% 18% Neutral

Pharma & Heathcare

API 18% 18%

The overall sectoral impact remains neutral. However, as per the

management commentary, in the short-term, a negative impact of 4-

5% would be visible on the domestic formulations front due to the

downsizing of inventory at the dealer/pharmacy level over concerns on

availing credit on their closing stock a day before implementation of

GST Neutral

NA

Formulation 10-11% 12% Neutral

Life saving drugs 0 5% Neutral

Healthcare

Service tax:

0%

VAT: 5-12% 0%

The overall sectoral impact remains neutral

Neutral

NA

Cement

26-27% 28%

The new GST tax rate is 1-2% higher than the current prevailing rate for

cement companies. However, considering improved demand outlook,

we believe cement companies will be able pass on the additional tax

levy by taking price hikes Neutral

Sectoral Impact

7

Source: cbec.gov.in, ICICIdirect.com Research

Sector Segment/ Products Tax rate

earlier

GST Rate View Positive/ Negative Stocks impacted

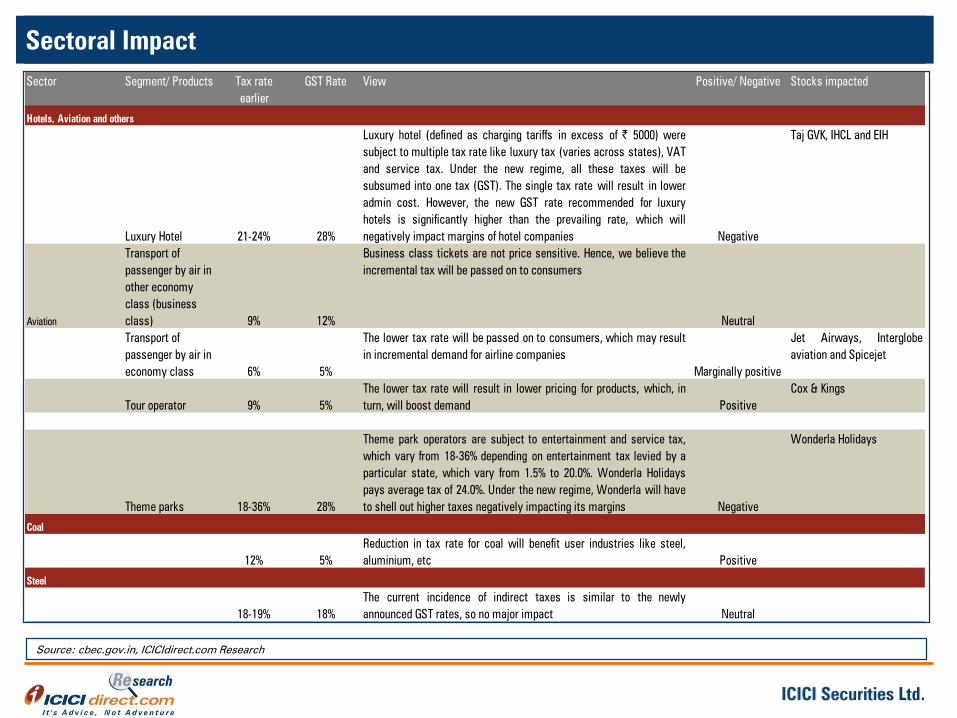

Luxury Hotel 21-24% 28%

Luxury hotel (defined as charging tariffs in excess of | 5000) were

subject to multiple tax rate like luxury tax (varies across states), VAT

and service tax. Under the new regime, all these taxes will be

subsumed into one tax (GST). The single tax rate will result in lower

admin cost. However, the new GST rate recommended for luxury

hotels is significantly higher than the prevailing rate, which will

negatively impact margins of hotel companies Negative

Taj GVK, IHCL and EIH

Aviation

Transport of

passenger by air in

other economy

class (business

class) 9% 12%

Business class tickets are not price sensitive. Hence, we believe the

incremental tax will be passed on to consumers

Neutral

Transport of

passenger by air in

economy class 6% 5%

The lower tax rate will be passed on to consumers, which may result

in incremental demand for airline companies

Marginally positive

Jet Airways, Interglobe

aviation and Spicejet

Tour operator 9% 5%

The lower tax rate will result in lower pricing for products, which, in

turn, will boost demand Positive

Cox & Kings

Theme parks 18-36% 28%

Theme park operators are subject to entertainment and service tax,

which vary from 18-36% depending on entertainment tax levied by a

particular state, which vary from 1.5% to 20.0%. Wonderla Holidays

pays average tax of 24.0%. Under the new regime, Wonderla will have

to shell out higher taxes negatively impacting its margins Negative

Wonderla Holidays

Coal

12% 5%

Reduction in tax rate for coal will benefit user industries like steel,

aluminium, etc Positive

Steel

18-19% 18%

The current incidence of indirect taxes is similar to the newly

announced GST rates, so no major impact Neutral

Hotels, Aviation and others

Sectoral Impact

8

Source: cbec.gov.in, ICICIdirect.com Research

Sector Segment/ Products Tax rate

earlier

GST Rate View Positive/ Negative Stocks impacted

Auto

2-W 24% 28%

The price of 2-Ws<350 cc will increase marginally by 0.5%. Given that

there is a cess of 3% on motorcycles>350cc, the price increase post

GST will by 2.6%. However, motorcycle above 350 cc contributes only

0.4% of the domestic 2-W sales Neutral

Bajaj Auto, Hero MotoCorp,

Eicher Motors

Small car/SUV

(Length<4 m;

engine size<1200

cc/1500 cc for

petrol/diesel

vehicles) 24% 29-31%

Although the gap between current tax incidence & GST appears

optically high, prices of these vehicles will increase in the range of ~1-

3% post GST implementation, because the base (ex-showroom price)

will also change with GST implementation. This potential price

increase will not have an impact on demand

Neutral

Maruti, Tata Motors

Sedan/SUV

(length> 4

m;engine size<

1500 cc) 32% 43%

Prices of these vehicles will increase ~6%. Prices of cars like Ciaz &

Ertiga fall in this segment, which form ~9% of Maruti's domestic sales

Negative

Maruti

Sedan/SUV

(length> 4 m with

engine size>1500

cc) 36% 43%

Prices of these vehicles will increase ~0.5%. There will not be an

negative impact on demand due to the potential price rise

Neutral

Tata Motors

CV 24% 28%

Prices of these vehicles will increase ~0.5%. Hence, the impact will

be neutral Neutral

Tata Motors, Ashok Leyland,

Eicher Motors

Tractors 12% 12% Prices of tractors will reduce ~1% Neutral

Real Estate 5-12% 12%

The impact of the new GST rate would vary for different micro markets

in which developers operate. The Bengaluru market would be least

impacted as the current incidence is also around ~11.5%.

Furthermore, for markets like Maharashtra, the current incidence is

around 5.5%. Though developers would be receiving input credit on raw

materials and labour, the new rate would be slightly negative for them

Marginally negative

Oberoi Realty

Tiles 26.5-29% 28%

The current incidence of indirect taxes is similar to the newly

announced GST rates, so no major impact Neutral

Kajaria Ceramics, Somany

Ceramics

Plywood 27-29% 28%

The current incidence of indirect taxes is similar to the newly

announced GST rates, so no major impact Neutral

Century Plyboard, Greenply

Laminates 27-29% 18%

The newly announced GST rates for decorative laminates is much

lower than the current incidence, which is positive for laminate

players Positive

Century Plyboard

Real Estate & Building material

Sectoral Impact

9

Source: cbec.gov.in, ICICIdirect.com Research

Sector Segment/ Products Tax rate

earlier

GST Rate View Positive/ Negative Stocks impacted

18%-19% 28%

Since the proposed GST rate is higher than the existing tax rate (18-

19%), we believe it may dent the profitability of players in the short-

term. However, over the longer term, organised players may take a

gradual price hike to partially negate the impact on margins Negative

VIP Industries, Safari

Industries

Logistics

Road transport 4.5-6% 5%

Freight rates across modes of transport are expected to remain at

earlier levels. However, input tax credit for road is not allowed to

promote movement of goods from rail and coastal. Still, we continue

to believe that road transport would continue to play a pivotal role to

execute last mile delivery. In addition to the same, introduction of e-

way bill would enable seamless movement of goods resulting in cost

savings, improving vehicle efficiency Positive

TCI

Rail & Coastal

shipping 4.5-6% 5%

Rates maintained at earlier levels. However, input tax credit,

excluding capex, is allowed. This would bring in effective tax rate

lower or close to existing rates Positive

GPPL

Container Rail 6% 12%

Higher taxes coupled with elevated haulage charges would impact the

competitive positioning of rail vis-à-vis road. Any input credit allowed

in the sector would provide a breather. The market leader would be

able to pass on the hike in rates thereby maintaining the realisations

Neutral

Container corporation

Express,

Warehousing &

other value added

services 15% 18%

Given the recent hike in service tax rates to 14%, the industry was

prepared for 18% service tax in FY18. However, the shift to organised

would trigger volume growth, which would benefit players having a

pan-India presence Positive

Gati and Bluedart

Breweries & Distilleries

Malt 22-24% 28%

Malt remains a key raw material for preparing beer. The increase in

RM material prices would impact the margins of the business Negative

United Breweries & United

Spirits

Glass 5-6% 12-18%

Bottling and other packaging expenses form ~25% of overall

revenues, which would further increase on the back of higher taxes Negative

United Breweries & United

Spirits

Bags & Luggage

Sectoral Impact

10

Source: cbec.gov.in, ICICIdirect.com Research

Sectoral Impact

Sector Segment/ Products Tax rate

earlier

GST Rate View Positive/ Negative Stocks impacted

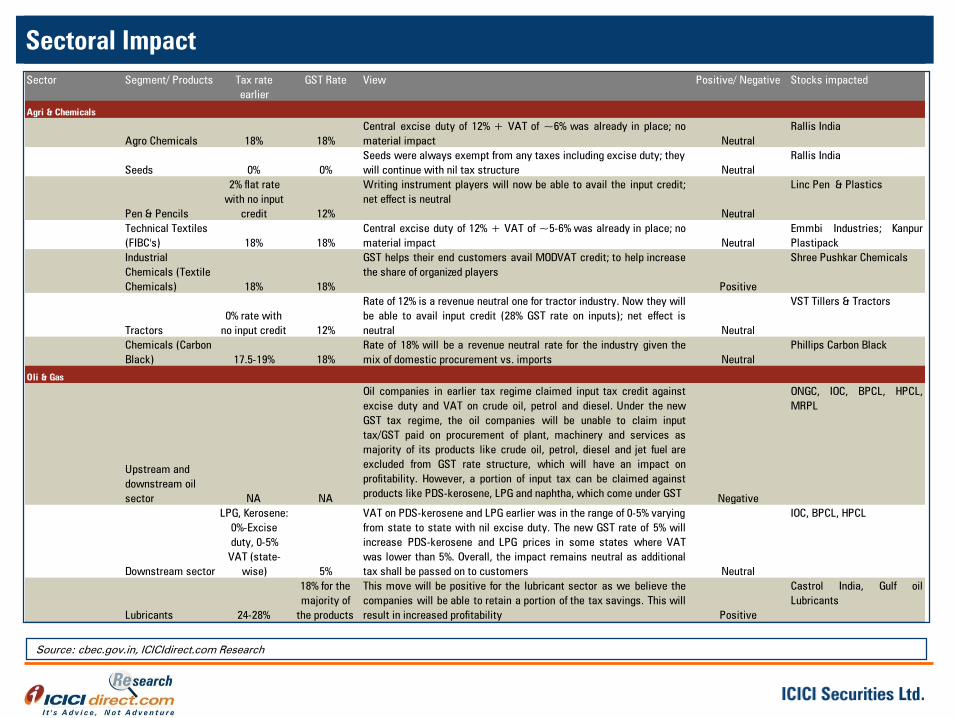

Agri & Chemicals

Agro Chemicals 18% 18%

Central excise duty of 12% + VAT of ~6% was already in place; no

material impact Neutral

Rallis India

Seeds 0% 0%

Seeds were always exempt from any taxes including excise duty; they

will continue with nil tax structure Neutral

Rallis India

Pen & Pencils

2% flat rate

with no input

credit 12%

Writing instrument players will now be able to avail the input credit;

net effect is neutral

Neutral

Linc Pen & Plastics

Technical Textiles

(FIBC's) 18% 18%

Central excise duty of 12% + VAT of ~5-6% was already in place; no

material impact Neutral

Emmbi Industries; Kanpur

Plastipack

Industrial

Chemicals (Textile

Chemicals) 18% 18%

GST helps their end customers avail MODVAT credit; to help increase

the share of organized players

Positive

Shree Pushkar Chemicals

Tractors

0% rate with

no input credit 12%

Rate of 12% is a revenue neutral one for tractor industry. Now they will

be able to avail input credit (28% GST rate on inputs); net effect is

neutral Neutral

VST Tillers & Tractors

Chemicals (Carbon

Black) 17.5-19% 18%

Rate of 18% will be a revenue neutral rate for the industry given the

mix of domestic procurement vs. imports Neutral

Phillips Carbon Black

Oli & Gas

Upstream and

downstream oil

sector NA NA

Oil companies in earlier tax regime claimed input tax credit against

excise duty and VAT on crude oil, petrol and diesel. Under the new

GST tax regime, the oil companies will be unable to claim input

tax/GST paid on procurement of plant, machinery and services as

majority of its products like crude oil, petrol, diesel and jet fuel are

excluded from GST rate structure, which will have an impact on

profitability. However, a portion of input tax can be claimed against

products like PDS-kerosene, LPG and naphtha, which come under GSTNegative

ONGC, IOC, BPCL, HPCL,

MRPL

Downstream sector

LPG, Kerosene:

0%-Excise

duty, 0-5%

VAT (state-

wise) 5%

VAT on PDS-kerosene and LPG earlier was in the range of 0-5% varying

from state to state with nil excise duty. The new GST rate of 5% will

increase PDS-kerosene and LPG prices in some states where VAT

was lower than 5%. Overall, the impact remains neutral as additional

tax shall be passed on to customers Neutral

IOC, BPCL, HPCL

Lubricants 24-28%

18% for the

majority of

the products

This move will be positive for the lubricant sector as we believe the

companies will be able to retain a portion of the tax savings. This will

result in increased profitability Positive

Castrol India, Gulf oil

Lubricants

11

Source: cbec.gov.in, ICICIdirect.com Research

Sectoral Impact

Sector Segment/ Products Tax rate

earlier

GST Rate View Positive/ Negative Stocks impacted

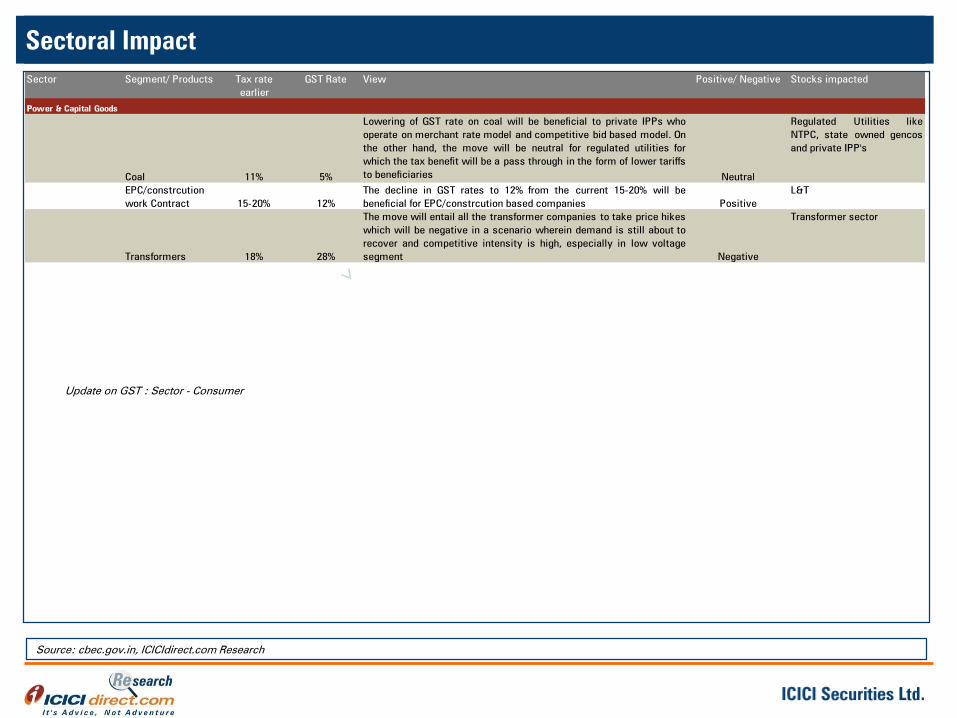

Power & Capital Goods

Coal 11% 5%

Lowering of GST rate on coal will be beneficial to private IPPs who

operate on merchant rate model and competitive bid based model. On

the other hand, the move will be neutral for regulated utilities for

which the tax benefit will be a pass through in the form of lower tariffs

to beneficiaries Neutral

Regulated Utilities like

NTPC, state owned gencos

and private IPP's

EPC/constrcution

work Contract 15-20% 12%

The decline in GST rates to 12% from the current 15-20% will be

beneficial for EPC/constrcution based companies Positive

L&T

Transformers 18% 28%

The move will entail all the transformer companies to take price hikes

which will be negative in a scenario wherein demand is still about to

recover and competitive intensity is high, especially in low voltage

segment Negative

Transformer sector

Update on GST : Sector - Consumer

12

Pankaj Pandey Head – Research [email protected]

ICICIdirect.com Research Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC

Andheri (East)

Mumbai – 400 093

ANALYST CERTIFICATION

We /I, Pankaj Pandey, Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views about the

subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report.

Terms & conditions and other disclosures:

ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI Securities

Limited is a Sebi registered Research Analyst with Sebi Registration Number – INH000000990. ICICI Securities is a wholly-owned subsidiary of ICICI Bank which is India’s largest private sector bank and

has its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture capital fund management, etc. (“associates”), the details in respect of

which are available on www.icicibank.com.

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking

and other business relationship with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to

analysts and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and

meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form,

without prior written consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the

information current. Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has

been suspended temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory

capacity to this company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed.

This report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other

financial instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by

virtue of their receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your

specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own

investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should

independently evaluate the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no

liabilities whatsoever for any loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk

Disclosure Document to understand the risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are

not predictions and may be subject to change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other

assignment in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services

in respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies

mentioned in the report in the past twelve months.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its analysts did not receive

any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research

Analysts and their relatives have any material conflict of interest at the time of publication of this report.

It is confirmed that Pankaj Pandey Research Analysts of this report have not received any compensation from the companies mentioned in the report in the preceding twelve months.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the

month preceding the publication of the research report.

Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject

company/companies mentioned in this report.

ICICI Securities has received an investment banking mandate from Government of India for disinvestment in ONGC. This report is prepared based on publicly available information

ICICI Securities has received an investment banking mandate from Government of India for disinvestment in Bharat Electronics. This report is prepared based on publicly available information.