good & service tax · pdf filegood & service tax salient features of gst presented by...

TRANSCRIPT

Good & Service TaxSalient Features of GST

Presented by

Goh Kin SiangDeputy Director of Customs rtd

ITS Management Sdn Bhd

Agenda:

• Why GST ?

• What is GST ?

• GST Models

• Basic Elements of GST

• Registration

Why introduce GST?

A better tax system as compared to the current indirect taxes such as:

• Sales tax since 29.2.1972

• Service tax since 1.3.1975

Current sales & service tax have some fundamental weaknesses:

a) Certain goods are subject to multiple taxes;

b) Problems of transfer pricing

c) Price cascading

d) Complicated exemption procedures such as CJ5, CJ5A, CJ5B; Credit system; Vendor system; drawback 29/99,etc;

e) Various & varied sales turnover/threshold for licensing purposes.

Sales Tax =RM100,000/- per year;

Service tax =RM150,000/- or RM300,000/- or RM3 million or zero threshold.

f) Different rates of tax.

Sales tax = 5%,10% or 20%; specific ( petroleum products)

Service tax = 6% or RM 50/- per credit card

• To ensure tax compliance & minimise tax evasion & tax avoidance;

• Decline in import duty collection as Malaysia started fullimplementation of AFTA on 1.1.2010

.

GST is a more effective taxation system

simply because:

• It discourages tax avoidance and tax evasion

• Better tax revenue collection for the stake-holder

• Self policing ( to claim input tax paid!)

Service tax and its cascading effect on services acquired by an engineer and subsequent sale :

Architectural

Service:

RM1,000

Service tax

6%=RM60.00

Surveyor fee:

RM500

Service tax 6%

=RM30.00

Engineer fee

RM 40,000

Service tax 6%

=RM2,400.00

Customer pays:

RM42,490.00 & includes

Service tax pays:

• RM60.00

• RM30.00

• RM2400.00

Total: RM2490.00

What happened if you are under the GST tax regime?

• GST is only paid once that is at the customer’s level.

• GST paid by the engineer to the architect and

surveyor can be claimed back as his input tax on

condition he is a registered person

GST on services acquired by an engineer and subsequent sale :

ArchitecturalService: RM1,000GST@6%=RM60.00

Surveyor fee:RM500GST@ 6%=RM30.00

Engineer fee=RM39910.00 i.e. RM 40,000-90.00GST@6%=RM2394.60

Customer pays:RM42,304.60 & includesGST pays:RM2394.60Saving: RM185.40

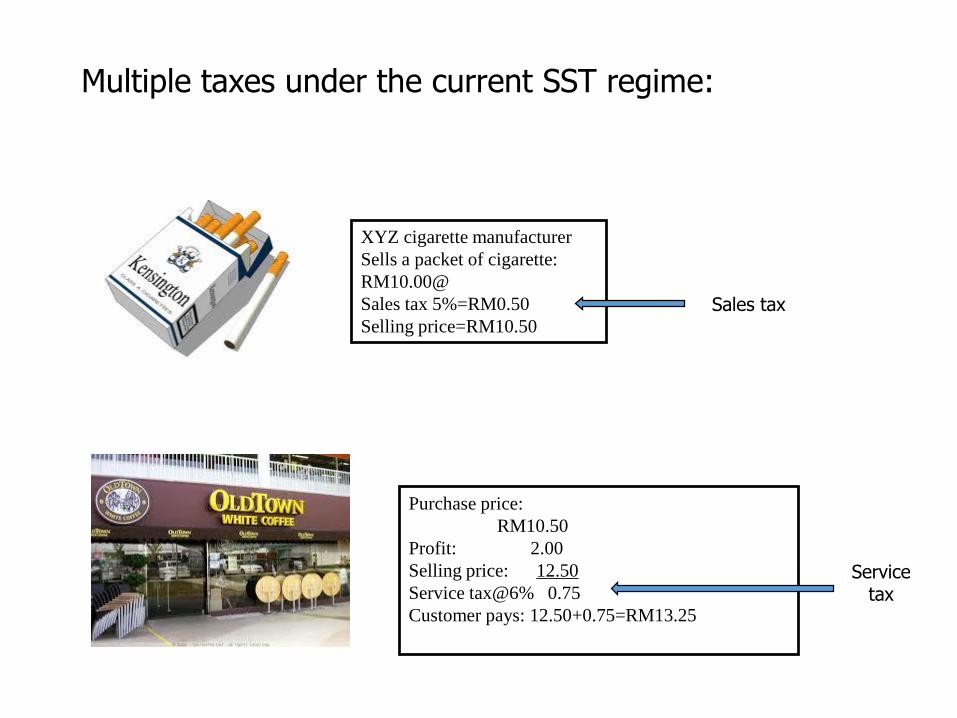

Multiple taxes under the current SST regime:

XYZ cigarette manufacturer

Sells a packet of cigarette:

RM10.00@

Sales tax 5%=RM0.50

Selling price=RM10.50

Purchase price:

RM10.50

Profit: 2.00

Selling price: 12.50

Service tax@6% 0.75

Customer pays: 12.50+0.75=RM13.25

Sales tax

Service tax

GST tax regime:

XYZ cigarette manufacturer

Sells a packet of cigarette:

RM10.00@

GST 6%=RM0.60

Selling price=RM10.60

Purchase price: RM10.00

Profit: 2.00Selling price: 12.00GST@6% 0.72Customer pays: 12.00+0.72=RM12.72Saving:(13.25-12.72)=RM0.53

GST paid is

not embedded

and can claim

back by Old

Town

Transfer of price

Package offer:

RM120.00 (service tax inclusive) includes:

Chalet and boat ride

Chalet : RM20.00Boat ride 100.00Total 120.00Service tax@6%=20X 6 =RM1.13

106Chalet operator transfers the actual chalet charge to boat ride (non-service tax activity)Its called tax avoidance.But government loses in revenuecollection

What is GST ?

GST stands for goods & service tax. In some countries its called value-

added tax (VAT). It is :

a) A consumption tax i.e tax on expenditure. It is imposed on all sectors of the

economy with the exception of medical care, financial (selective) & education;

b) Multi-stage based on net value at each stage of business transaction up to the

retail (consumer) level.

c) Its levied on the supply of goods & services made in Malaysia by a taxable person

in the course or furtherance of any business carried on by him; and

d) The importation of goods & services into Malaysia

Currently there are more than 160 countries in the worldimplementing GST/VAT tax structure in one form or another. InAsia, only Brunei, Hong Kong, Myanmar & Malaysia do not havea similar tax structure enforced.

Example:

• Singapore has a GST of 7%;

• Australia its 10%;

• United Kingdom is 5% & 20%

• New Zealand is 15%

GST Models

Business entity Selling price

(RM)

Tax on output

(RM)

Tax on Input

(RM)

Net Tax paid

(RM)

Log supplier 100.00 6.00 0.00 6.00

Sawn timber

supplier

500.00 30.00 6.00 24.00

Manufacturer of

Furniture

700.00 42.00 30.00 12.00

Retailer 900.00 54.00 42.00 12.00

Customer pays GST collected by the Customs:

54.00

1.GST rate: 6%

2.GST paid at each level is deductible ;3. The final customer pays GST RM54.00

Computation of standard-rated GST of 6%

Taxable supply is subject to 6% GST

The supplier needs to charge GST on his output & claim input tax (ITC) at each level of purchase

Log supplier supplies log to sawn timber miller:RM100@6%=RM6/-

Sawn timberSupplies sawn timber to furniture manufacturer:RM500@6%=RM30-He claims back RM6/-

Furniture maker sells furniture to retailer:RM700@6%=RM42/-He claims back RM30/-

Retailer sellsFurniture to buyer:RM900/-@6%=RM54/-He claims back RM42/-Buyer pays GSTRM54 +RM900=RM954/-

1

2

3

4

Computation of zero-rated GSTZero-rated GST means GST is 0%

The supplier of zero-rated supply does not collect any tax on output but is allowed to claim back GST paid on input

Business entity Selling price

(RM)

Tax on output

(RM)

Tax on

Input

(RM)

Net tax paid

(RM)

Log supplier 100.00 6.00 0.00 6.00

Sawn Timber

supplier

500.00 0.00 6.00 -6.00 (refund)

Manufacturer

Of furniture

700.00 0.00 0.00 0.00

Retailer 900.00 0.00 0.00 0.00

Customer pays Customs refund RM6.00 to sawn timber miller

1. Assuming log subject to GST 6%2. Sawn timber miller claims back GST 6%3. Assuming sawn timber and furniture are zero-rated

Log supplier supplies log to sawn timber miller:RM100@6%=RM6/-

Sawn timberSupplies sawn timber to furniture manufacturer:RM500. As sawn timber not subject to GST.He claims back RM6/-

Furniture maker sells furniture to retailer:RM700 & no GSTas furniture not subject to GST

Retailer sellsFurniture to buyer:RM900/- & no GSTas furniture not subject to GSTBuyer pays RM900

Example of GST on zero-rated goods

1

2

3

4

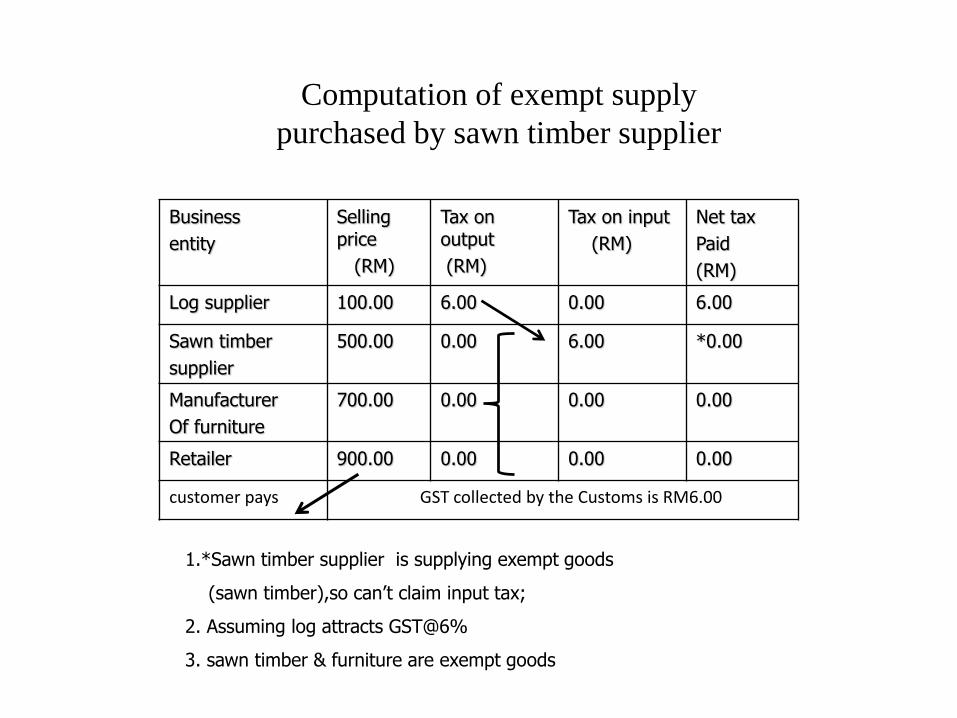

Computation of exempt supply

purchased by sawn timber supplier

Business

entity

Selling price

(RM)

Tax on output

(RM)

Tax on input

(RM)

Net tax

Paid

(RM)

Log supplier 100.00 6.00 0.00 6.00

Sawn timber

supplier

500.00 0.00 6.00 *0.00

Manufacturer

Of furniture

700.00 0.00 0.00 0.00

Retailer 900.00 0.00 0.00 0.00

customer pays GST collected by the Customs is RM6.00

1.*Sawn timber supplier is supplying exempt goods

(sawn timber),so can’t claim input tax;

2. Assuming log attracts GST@6%

3. sawn timber & furniture are exempt goods

Log supplier supplies log to sawn timber miller:RM100@6%=RM6/-

Sawn timberSupplies sawn timber to furniture manufacturer:RM500. No GST as sawn timber is exempt goodsHe can’t claim GST RM6/-.Its a cost to him

Furniture maker sells furniture to retailer:RM700. No GSTas furniture is exempt goods

Retailer sellsFurniture to buyer:RM900/-No GSTas furniture is exempt goodsBuyer pays RM900

Example of GST on exempt goods

2

1 3

4

GST Elements:

• Taxable person (Registrant)

a) any person who is required under the GST Act, to register

b) it includes an individual, company, sole proprietor-ship,partnership, trust, estate, society, union, club, association,organization with an annual sale turnover exceeding thethreshold

c) he charges & collects GST on his taxable supplies

• Taxable period ( Sec.40(1) GST Act 20xx)

a) Category A: one month ending on the last day of any month;

b) Category B: three month ending on the last day of any month;

c) Category C: other month as approved by the DG

Category A:

for business with annual sales turnover exceeding RM5 million;

Category B:

for business with annual sales turnover not exceeding 5 million;

Category C:

special case as approved by the DG

• Supply

• Supply includes all form of supply done for a consideration

• A supply includes sales of goods & provision of services

• A supply can be :

i. Standard-rated

ii. Zero-rated

iii. Exempt

iv. Out-of-scope

• Standard-rated supply

A standard-rated supply is a supply of goods & services made in Malaysia/imported into Malaysia. GST is chargeable at the rate of 6% (proposed) on the value of supply.

Is manufactured goods standard-rated?

• Zero-rated supply

A zero-rated supply is a zero GST rate chargeable on export ofgoods & services. GST chargeable is 0%.Examples of zero-ratedgoods & services are:

• A event management company charges a fee for organizing aconcert in Singapore

• A training company conducts a course in China

• An accountant provided accounting service for a company inAustralia

• An architect who designs a house in Singapore,even though thedesign is done in Malaysia

• A factory exports its manufactured goods

• A merchant exports his goods to oversea market

Zero-rated supply would also includes the following

( Budget 2014)(lampiran A1 dated 25.10.2013)

Foodstuff such as rice,sugar,flour,cooking oil,salt,live animals,meat &

offal,fish & fillets,international transportation services such as

transportation of passengers by sea or air, supply of treated water,

excluding distilled water,de-ionised water,oxygen water & mineral

water; supply of electricity for the 1st 200KWH,etc.

Is industrial manufactured goods zero-rated?

• Exempt Supply

An exempt supply is a supply of any goods or services which shall not be subject to the imposition of tax.

The Minister will from time to time announce in the government gazette what are the exempt supplies

Budget 2014, Lampiran A2 dated 25.10.2013

Examples of exempt supplies:

Domestic transportaton of passengers for mass public transport by rail, ships, boat, ferries, express bus, stage bus, workers’ bus, school bus, feeder bus & taxi.

Highway toll;

Residential property;

Land for agricultural purposes;

Land for general use e.g.government building & burial ground;

Private health;

Education;

Financial services;

Life insurance;

Is industrial manufactured goods considered exempt goods?

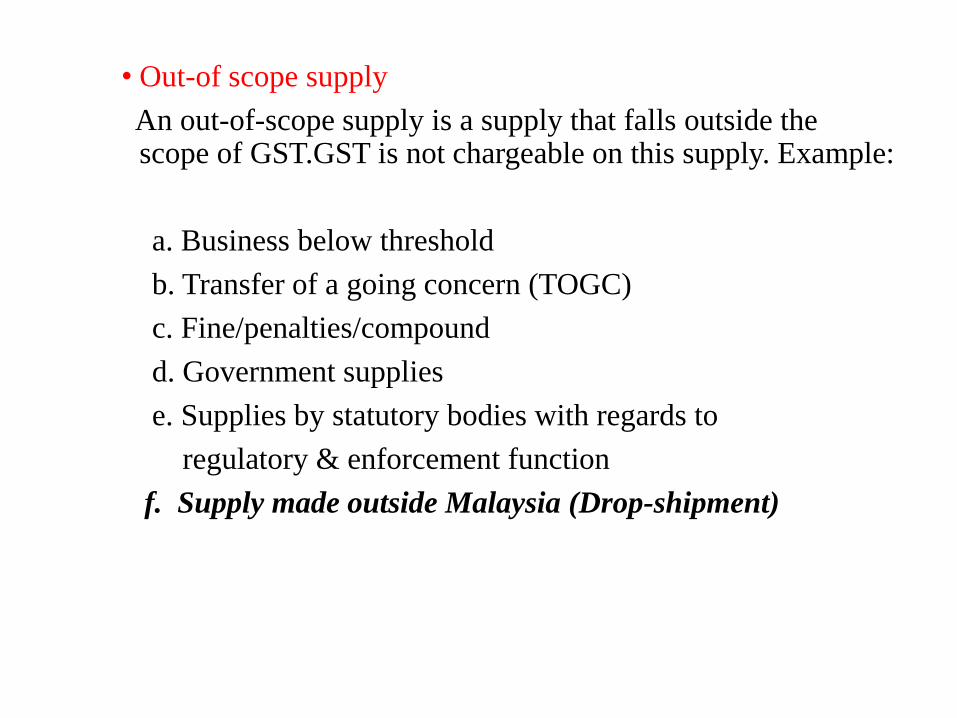

• Out-of scope supply

An out-of-scope supply is a supply that falls outside the scope of GST.GST is not chargeable on this supply. Example:

a. Business below threshold

b. Transfer of a going concern (TOGC)

c. Fine/penalties/compound

d. Government supplies

e. Supplies by statutory bodies with regards to

regulatory & enforcement function

f. Supply made outside Malaysia (Drop-shipment)

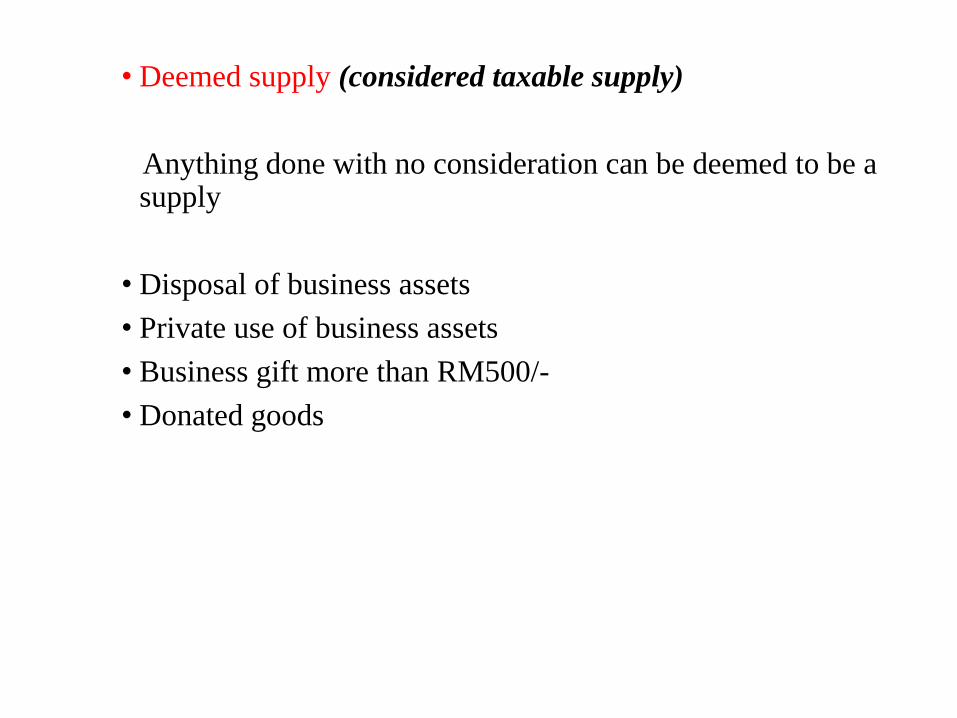

• Deemed supply (considered taxable supply)

Anything done with no consideration can be deemed to be a supply

• Disposal of business assets

• Private use of business assets

• Business gift more than RM500/-

• Donated goods

• Place of supply

A supply is only taxable if made in Malaysia. Generally

speaking, goods are considered as being supplied at a place

where they are removed from and services are treated as

being supplied at a place where services are rendered

• Time of supply

The time of supply refers to when a supply is made for GST purposes. This will decide when a taxable person should account for GST on the supply made.

See more illustration at slides below…

• Value of Supply

Value of supply = consideration – GST

GST is charged on the value of supply of goods & services when the time of supply takes place

Consideration= Includes any payment made, whether in money or other than money for the supply of goods or services

For standard and zero-rated registrant, GST paid is

not a cost to his purchase because he can treat

GST paid as his input tax claimable

Example:

A tax invoice issued by a supplier to RR is RM 106.00 (inclusive of

6% GST) and RR decides to mark up 20% on the cost of goods.

GST on purchase is RM106.00x6/106= RM6.00

Actual cost of purchase is RM106.00-6.00= RM100.00

He can only mark up 20% on RM100.00 and not 106.00

So RR selling price is RM100+20.00=RM120.00

GST is RM120.00x6%=RM7.20

( Charged to the customer and RR paid to the Customs department)

Consideration

Value

GST

• Input tax

A. GST that a taxable person pays on the goods & servicespurchased for the purpose of his business

B GST paid by a taxable person on any importation of

goods & services

• Output tax

GST that a taxable person charges on his taxable

supplies of goods & services

GST

Is charged on

Importation of

goods & services

into Malaysia

Charging and Collection of GST

GST is collected by the supplier

who is registered with the

Malaysian Customs

GST is collected by the

Malaysian Customs at

the point of importation

Supply of goods

& services in

Malaysia

• Input tax credit (ITC)

A taxable person claims as credit (ITC) any GST incurred by him in acquiring a taxable supplies for the purpose of his business

ITC is claimed through a GST return (GST No.3) for the taxable period based on tax invoice received

GST collected from customers

Less

GST paid on businesspurchases

Equal

Net GST

Payable toCustoms

Refundable byCustoms

If output taxInput tax

If output taxInput tax

Output tax

Input tax

Basis of GST process

Time of Supply

General Rules:

In most cases, the supply is treated as taking place at the earliest of the following events:

1. the goods are removed i.e.

a. the supplier sends the goods to the customers

or

b. the customer collects the goods from the supplier

Tax point

or 2. The time when the goods are made available.

Example:

the supplier assembles something on the

customer’s premises;

3. In the case of services:

the time when the services are performed

or 4. the supplier issued a tax invoice for that supply;

or 5. the supplier receives payment for that supply

Tax point

Tax point

Example:

1/1/2016 20.3.2016 23.4.2016 30.4.2016

Sign contract goods received/ tax invoice payment made

service rendered issued

When is the time of supply?

The time of supply is the earliest of the 3 events i.e 20.3.2016.Thus if

your accounting period covered in your GST return is 1.1.2016-31.3.2016

,you must account for the GST in this taxable period.

Exception: If the supplier issues a tax invoice within

21 days after the events in (1) or (2) or

(3),then the time of supply is the date of

the tax invoice.This is known as the 21

days rule

This rule will not apply if event in (5) takes place the

earliest. If payment is received before the events

in (1) or (2) or (3) or (4),the time of supply is the

date when payment receives

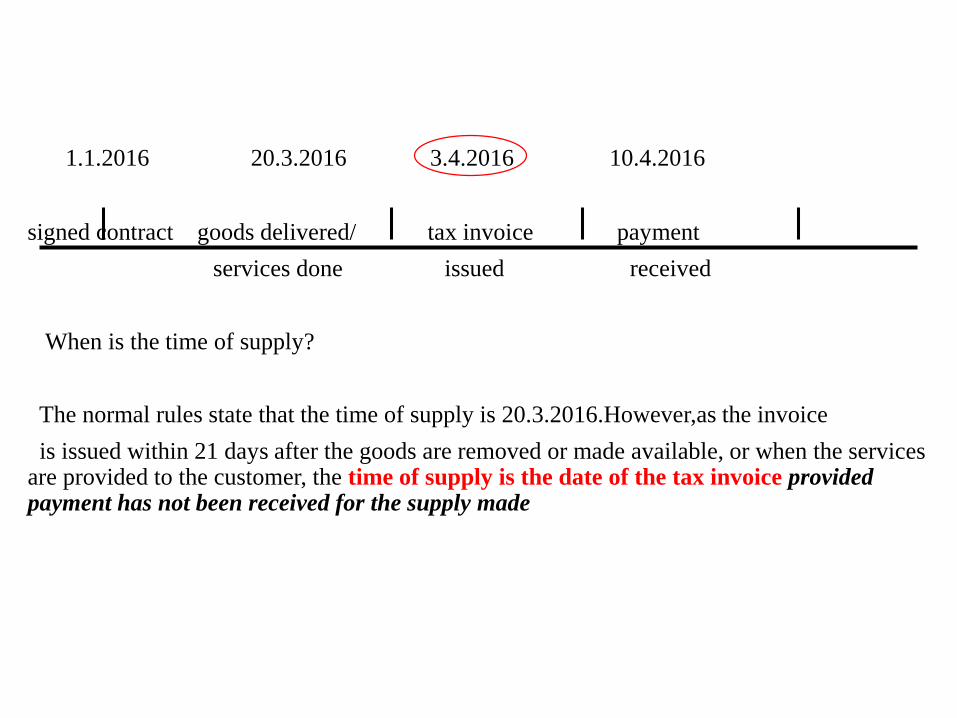

21 day rule: It is an exception to the general rule of supply as shown above.

If the supplier issued a tax invoice within 21 days after the goods are removed or made available,or when the services are provided to the customer, the time of supply is the date of invoice provided payment has not been received for the supply made

1.1.2016 20.3.2016 3.4.2016 10.4.2016

signed contract goods delivered/ tax invoice payment

services done issued received

When is the time of supply?

The normal rules state that the time of supply is 20.3.2016.However,as the invoice

is issued within 21 days after the goods are removed or made available, or when the services are provided to the customer, the time of supply is the date of the tax invoice provided payment has not been received for the supply made

Why TIME OF SUPPLY is important?

Because it determines when a taxable person should charge GST and account for GST in his return

Registration

Any person is liable to register when his taxable goods & services per year exceeds the threshold (RM500,000/ per annum-proposed)

If you are not a registrant, you cannot charge GST and at the same time your cannot claim input tax credit for all your purchases in making a taxable supply

Types of Registration

• Mandatory

• Voluntary

• Group

• Branch/divisional

• Partnership

• Mandatory registration

A person will be liable for registration

when his taxable supplies exceed the

threshold.

Its an offence if you carry on business

without GST registration

• Voluntary registration

A person can apply for voluntary registration if his annual taxable supplies is below the RM500,000.00 threshold.Once he has been registered for GST,he must remain registered for a minimum of 2 years

Benefits :

Is allowed to claim Input tax credit (ITC);

e-Registration

(on line registration vie GST Portal)

Website: gst.customs.gov.my

Late registration

Person who is late in registering his business

will be subject to a registration penalty from the date he should be registered to the date immediately before the date he is so registered, and this period is referred to as the late registration period

Deregistration ( Sec.25.1 GST Act 20xx)

1. He ceases business;

2. Taxable turnover falls below the threshold

3. Ceases making taxable supplies

4. Mandatory deregistration

5. To notify ( Form: GST Adm 4) the Customs department within 30 days after cessation of taxable business

6. Pay GST on assets & stock on hand